PLEASE NOTE: This welcome offer has now changed. Details of the new ‘Invest £1,000, Get £100’ free welcome offer can be found in my fully updated RateSetter review.

As I said then, RateSetter is one of my favorite lower-risk P2P lending sites. It lets you save via a tax-efficient IFISA and/or an ordinary (taxable) Everyday account. Although their rates aren’t the highest (currently 3% to 4%) I like the fact that risk is spread across all loans on the platform, with a provision fund to cover any defaults.

In my previous articles I mentioned their welcome offer of a £100 bonus for anyone investing £1000 for a year or longer. This offer is now closed, though if you took advantage and are waiting for the £100 bonus to be credited twelve months on, that will (of course) still be honoured.

What RateSetter do have now is an enticing (and much lower cost) Invest £10, Get an Extra £20 offer.

New Welcome Offer

Currently if you are new to RateSetter you can get £20 added to your account for free just by signing up and depositing £10. Full terms of the offer are reproduced below, and you can also find them on the RateSetter website.

You can take advantage of this offer so long as you

have not previously registered with RateSetter;

register after 23rd January 2020; and

deposit a minimum of £10 through the RateSetter ISA or Everyday account within 56 calendar days of registering.

Your bonus will be credited to your Everyday Account and invested in RateSetter’s Access (instant access) product at the going rate (currently 3%) within 30 working days of qualifying. From here you can transfer it to your ISA account if you like or simply withdraw it.

My Thoughts

This is a great offer from RateSetter if you are wary about P2P investing and want to dip a toe without risking any significant money. It is also good if you only have very small amounts available to invest, or you just like the idea of getting your hands on a free twenty pounds! It will also give you a chance to see how the RateSetter P2P platform works for yourself.

Although the bonus is ‘only’ £20 as opposed to the £100 on offer before, you only have to invest £10 to get it rather than £1,000. In addition, your bonus will be credited within 30 working days of qualifying for it, rather than having to wait a full year as before.

Clearly, this is a generous promotional offer by RateSetter and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

As always, if you have any questions or comments about this post, please do leave them below.

Disclosure: This post includes my referral link. If you click through and make an investment for this offer, I will receive a bonus for introducing you. This has no effect on the terms or benefits you will receive. Please be aware also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. You should do your own ‘due diligence’ before making any investment, and take professional advice if at all unsure how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Over the last few weeks I’ve received several queries about 20 COGS. I’ve also seen people asking about it on Facebook. Some of my fellow UK money bloggers have been promoting it as well.

I did try 20 COGS myself about 18 months ago. I didn’t like it and have therefore never written about it or promoted it (and I’m not now, so there are no affiliate links in this post). As it still seems to be generating a lot of interest, however, I thought I’d share my experiences (and opinions) about it here.

I guess I’d better start with a word of explanation, though…

What is 20 COGS?

For those who don’t know, 20 COGS is a home money-making opportunity. The way it works is that you undertake a set of twenty online tasks. Once you have completed all twenty as specified – and not before – you receive a cash reward. This is generally between £150 and £200, but you are likely to incur some costs in completing the tasks (e.g. paying for trial subscriptions) and these will need to be deducted from your reward to calculate your net profit.

The tasks are, of course, the twenty COGS in the name. COGS stands for Competitions, Offers, Gaming, Surveys. A typical task might involve signing up with an advertiser for a free or low-cost trial subscription (which you have to remember to cancel before they start charging the full monthly amount). Or it might involve signing up to an online casino site and wagering a set amount of money on their slot machines. It might also just involve filling in a (long) survey, but quite a few tasks do involve some financial outlay (with the risk of more if you don’t cancel in time).

My Experience

I saw 20 COGS recommended by a few bloggers I generally trust, so decided to give it a go. Unfortunately I didn’t prepare as well as I could have done, which was my first big mistake. In particular, I made the rookie error of giving out my own email address and mobile phone number.

I soon discovered that this was a serious mistake, as after the first few tasks I began getting spammed mercilessly. The spam emails weren’t so bad, as they were generally filtered out by my email program. However, my mobile phone became unusable due to the torrent of marketing calls and text messages I received. In the end I had no alternative but to bite the bullet, cancel my mobile number and get a new one. In my defence, I naively assumed that this wouldn’t happen due to GDPR and data protection rules – but when you sign up with 20 COGS these appear to go out the window.

I also had problems with some of the tasks. To start with, I couldn’t do quite a few of the gaming ones due to previously being a matched bettor. This meant I had already signed up with many of the websites concerned so I wasn’t eligible for the tasks in question. In those circumstances you can ask for a substitute task but this all takes time and in my case there weren’t enough replacement tasks available (although over time new ones do of course get added). As I mentioned earlier. this was about 18 months ago, so it’s possible there are more alternative choices available now.

I also had major reservations about the amount of personal information some of the survey-related tasks asked for – from holiday plans to dates of renewal for home and car insurance. Pretty obviously, this information was likely to be used for (unwanted and intrusive) marketing purposes.

Eventually, after completing about half a dozen cogs, I decided enough was enough and closed my account. That didn’t stop the spam, but at least I could breathe a sigh of relief that I didn’t have to do any more tasks. Of course, I got no money for the ones I had done, which I assume is one major way 20 COGS make their profits.

My Recommendations

As I said at the start, based on my experiences I don’t recommend signing up with 20 COGS at all.

It is an awful lot of hassle to go through for a probable net profit of £100 or so after costs are deducted. And you can easily end up with less than this if you forget to cancel a subscription (which is very easy to do).

If, despite all this, you are still tempted to give it a try, here are my recommendations…

1. Sign up via the link on Top Cashback. This will earn you an extra £1.20 cashback (at the time of writing).

2. Before starting, create a disposable email address and use this for all tasks. You could set up a new email address on Gmail or use a free disposable email service like ThrowAwayMail.

3. In addition, don’t use your real mobile number. You could use a pay-as-you-go SIM, or pick a number from https://fakenumber.org/united-kingdom. They have a list of UK mobile numbers that are not in use currently.

4. Keep detailed records of everything you do and when you do it. To avoid unwanted charges, it is clearly essential to cancel subscriptions before you have to pay the full amount (but after the qualifying period required by the advertiser). You might also want to set up automated reminders on your phone or computer to do this.

5. Read and follow all instructions carefully. Every advertiser on 20 COGS has its own specific requirements and you need to follow these carefully or you may not be credited for the task in question.

6. Take screenshots as you complete your tasks. If an advertiser disputes whether you completed a task correctly, you will then have visual proof that you did.

Finally, bear in mind that 20 COGS is a once-only scheme. After you have completed it, you won’t be able to do it again. It is not an ongoing money-making opportunity like matched betting or Prolific Academic, to take two random examples from the many I have covered on Pounds and Sense.

In Conclusion

As I said above, based on my experiences with 20 COGS I am not a fan and don’t recommend it.

It’s an awful lot of hassle to go through in order to earn £100 or so. And there is a very real risk of earning less than this if you make a mistake such as forgetting to cancel a subscription. There are also privacy issues, and you are potentially opening the door to a torrent of spam emails, texts, phone calls and more (though using fake/disposable mobile numbers and email addresses as recommended can reduce this).

Of course, this is just my opinion. I do know of people who have completed 20 COGS and (eventually) received a payout. If you are still on the fence about it, I recommend reading this comprehensive 20 COGS review by my colleague Adam who blogs at Money Savvy Daddy. Adam did actually complete 20 COGS and says he made about £100 from it. He is honest in his review about the time it took and the obstacles he faced along the way, however.

As always, if you have any comments about this post – or 20 COGS more generally – please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As you may have heard by now, the Spanish-owned bank Santander recently announced that they are cutting the interest paid on their popular 123 current account by a third.

From 5th May 2020 they are paying just 1% a year interest up to £20,000. That’s a big drop from the maximum 3% on offer when the account was launched (to great fanfare) in 2012. At that time the account topped the best-buy tables and many thousands of people (including me) switched to it as a result. As well as offering market-leading interest rates, they also paid cashback of up to 3% on a range of household bills if paid by direct debit from the account.

Since the heady days of 2012, though, Santander have steadily watered down the benefits of this account. They introduced a monthly fee that was originally £2 and then went up to £5. They also cut the interest rate in 2016 to 1.5%, and now – as mentioned above – to 1%. They are still charging £5 a month, though, which means you need to have an average balance of £6,000 in your account just to cover the fee (which works out as £60 a year).

Cashback is still on offer, but from being unlimited it has now been capped at £15 a month maximum. The 123 account currently pays 1% cashback on water bills, council tax and Santander mortgage payments, 2% on gas and electricity and Santander home insurance, and 3% on phone, broadband, mobile and TV packages. From 5th May onwards each of these three tiers will be capped at £5.

All this means that if you are one of the millions of customers who still have a Santander 123 account, you need to look carefully at whether it is still the best option for you.

Crunching the Numbers

Although Santander is no longer the clear market leader among current accounts, it may still be a good (and possibly the best) choice for some people. But you do need to look carefully at how you use the account and what alternatives are on offer. That’s what I did, and in the end I stayed with Santander, but switched my account to 123 Lite.

Here how I worked this out…

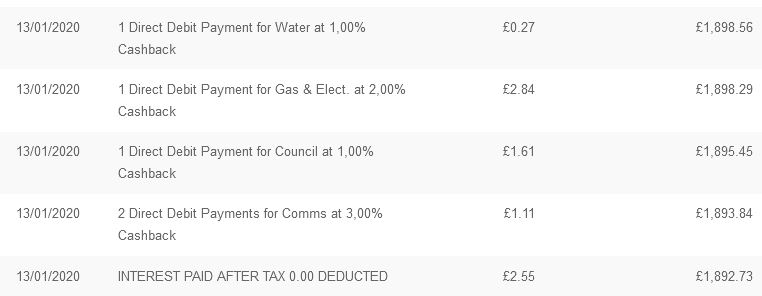

I started by looking at what I currently get from my Santander 123 account in terms of cashback and interest and setting this against the monthly charge. I have already cut down the amount of money I keep in my account due to the falling interest rates, so I now hold an average balance of around £1,800 in it. Here is a screengrab of the relevant section of my latest bank statement.

Adding this up, you can see that in January 2020 I received a total of £5.83 in cashback and £2.55 in interest. That’s a total of £8.38. Subtract the £5 monthly fee from this, and my net returns from the account are £3.38 a month or about £40 a year. On an average balance of £1,800, that works out as a return of about 2.25% – not great, but still better than most bank accounts currently (I am obviously counting cashback and interest together in this calculation – it’s all money, after all).

With the reduction in interest rates from 1.5 to 1%, though, that would have cut my monthly interest by a third to around £1.70. This would reduce my monthly ‘profit’ to £2.53, or about £30 a year. That works out as a rate of return on an average balance of £1,800 of about 1.7%. That’s obviously significantly worse than the previous 2.25%. Although again – taking into account the cashback as well as the interest – it still beats most ordinary current accounts.

The 123 Lite Alternative

With the potential rate of return on my 123 account falling to around 1.7%, I wanted to see if there were any better alternatives for me. Other things being equal, though, I didn’t want the hassle of switching to a different bank if the returns weren’t going be appreciably better for me.

So I looked into what alternative accounts Santander offer and learned about the Santander 123 Lite account. This doesn’t pay interest at all, but it offers the same cashback as a standard 123 account. And, very importantly, the monthly charge is only £1 instead of £5.

Looking at my potential returns with this account, I came up with the following: total cashback £5.83 minus £1.00 monthly charge = £4.83 a month net profit. Multiplying that by 12 gives a total annual return of £57.96. On an average £1,800 balance that works out as a notional interest rate of 3.22%, which was obviously a lot better than staying with a standard 123 account. So I decided to do that. Even at the current 1.5% interest rate which applies till 5th May 2020, I realized I would still be better off switching to 123 Lite, so there was no reason to delay.

As a matter of interest, if I reduce the average balance in my Santander account to £900 while still earning the same cashback, that will effectively double the rate of return I receive. Perversely, with the Santander Lite account, the lower the balance you can keep in it while still servicing your direct debits, the better the percentage return on your capital you will get 🙂

The other advantage of switching to a Santander 123 Lite account is that, as I discovered, it is a very simple process. I logged in to my account and selected the option to ‘upgrade’ my account. I had to answer a few simple questions and click to confirm my application. The next day I received an email confirming that I was now the proud owner of a Santander 123 Lite account. The account still has the same sort code and account number, the same PIN card number, and I can log in in exactly the same way. But at a stroke I have effectively doubled the returns I will be making from my account!

Other Alternatives

I strongly recommend that anyone with a Santander 123 account performs a similar calculation to the one I described above (bearing in mind there is now a cap of £5 a month on cashback in each of the three tiers). This will reveal if you would be better off switching to a 123 Lite account (and by how much per year). If you choose this option, switching is – I promise – a quick and painless process.

There are, of course, other alternatives, though. For example, HSBC have just introduced (or actually reintroduced) a one-off £175 bonus for anyone switching to their Advance current account. Note that to qualify for this you have to pay at least £1,750 into the account each month (or £10,500 every six months) and set up at least two direct debits or standing orders. More information about this can be found in this article from Which?

There are also still a few other current accounts that pay interest. An example is Nationwide’s FlexDirect account, which pays 5% interest on balances of £2,500 a year for the first 12 months (reducing to 1% a year after that). You have to pay in a minimum of £1,000 a month to qualify for this. Neither HSBC nor Nationwide offers cashback as well, so it is important to take that into account when deciding whether switching to them will be worth your while.

I hope you found this post of value if you have a Santander 123 account. I wish you every success in deciding how best to proceed. As ever, if you have any comments or questions, please do post them below..

UPDATE 5th MAY 2020 – I have just heard that Santander are cutting the interest rate on their 123 account AGAIN to 0.6% in August 2020. That makes the case for changing to a 123 Lite account – or switching away from Santander entirely – even more compelling.

If you enjoyed this post, please link to it on your own blog or social media:

Many of us have old gadgets that we no longer use and are just gathering dust. These include mobile phones, tablets, laptops, cameras, games consoles, and even desktop computers. They may still work, but we have replaced them with new and (hopefully) better products.

There is a natural tendency to hang on to the old products for a while, just in case we need a backup if our shiny new replacements fail. Modern brands are generally very reliable, however. And once you have established that a new product isn’t faulty, there isn’t really much reason to hang on to the old one – certainly not for months or years on end.

You might think the only thing to do with an old gadget is take it to the tip – sorry, household recycling centre. Before doing that, though, it’s worth noting that there are various ways you can make money from your old tech, even if (in some cases) it’s no longer working.

The High Street

There are various shops that will pay for old technology of all kinds. For example, CeX (who also have a website) will pay for smartphones, satnavs, cameras, speakers, headphones, laptops, games consoles, and even TVs in some cases. The device needs to be working but doesn’t have to be in its original packaging. Buy-and-sell stores like Cash Converter and Cash Generator will buy your old tech too.

eBay

Whatever the product you want to sell, the online auction house eBay is worth considering. It has a huge audience, and there will always be potential buyers looking for any item you want to dispose of.

Of course, you will have to spend a little time preparing your auction listing, taking photos, writing a description, and so on. However, eBay make this as easy as possible for sellers by showing you similar items that have sold on the site recently. This will help you prepare your own listing and assess the likely amount you may be able to get. Bear in mind that eBay does impose charges for sellers, which will reduce the amount you receive.

Facebook and Other Community Sites

Facebook local pages can be a great way of selling larger items in particular that may not be easy to post. You will need to include a photo and write a description stating the price you want. With a bit of luck someone living nearby will want the item and collect it from you for the price asked.

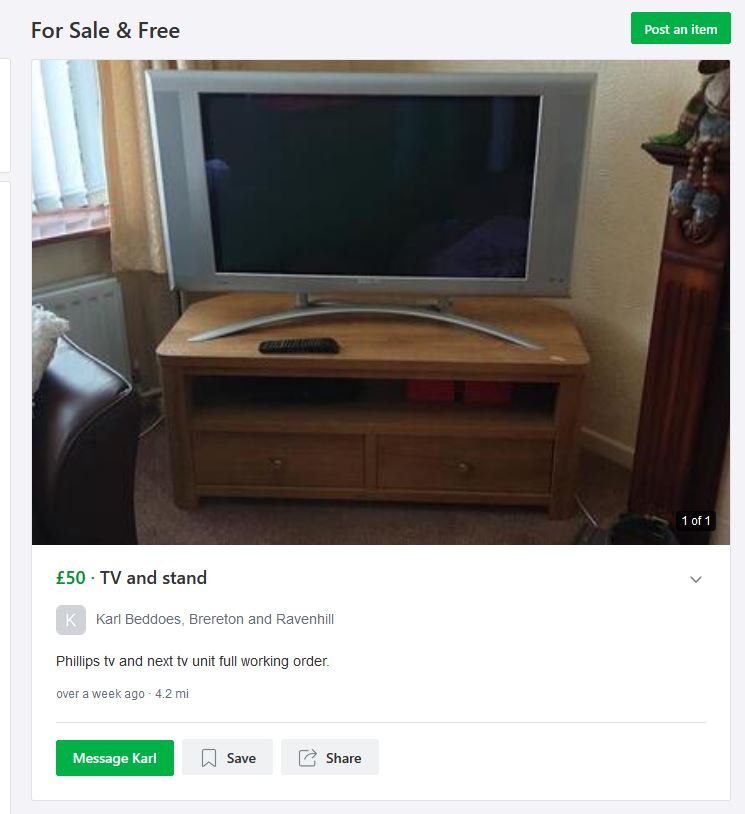

There are also other local community websites that may be worth trying. One I belong to myself is NextDoor. This is primarily a forum for the discussion of local news, seeking/sharing recommendations, publicizing local events, and so on. However, you can also advertise items for sale on the site. Here’s a typical example…

Specialist Sites

There are also specialist websites that want your old tech and will pay you for it. This can be a quick and hassle-free solution, with the advantage that you know exactly what price you will be getting (the sites quote a price online and it is up to you whether or not to accept this). Most will also accept products that are no longer working, though of course they will pay a lower price for them.

One such site I used recently and recommend is Cash in Your Gadgets. I sold them my seven-year-old Samsung Chromebook. The item in question was still working but by modern standards it was slow and the display wasn’t great. I went to the Cash in Your Gadgets website and spent a minute or so entering some details. I received an instant offer of £18 for the Chromebook, which I accepted.

Okay, I know £18 isn’t a fortune, but I was pleased to have the money and get the device off my hands. Cash in Your Gadgets arranged collection by courier, who arrived the next day, put the item in a box, sealed it, and gave me a receipt. A few days later I got the promised £18 in my bank account.

Cash in Your Gadgets pay for laptops, Chromebooks, Macbooks, iMacs and desktop PCs, though not smartphones or tablets. If you have one of those to dispose of, there are various other options.

One well-known site that buys phones and tablets is MusicMagpie. They also buy consoles, tablets, smartwatches, Kindle e-book readers, and more. If you use my referral link you can get an extra £5 when you sell your first product to them (and so will I) 🙂

Other options include Mazuma and Sell My Mobile. My best advice is to try these and similar sites and see who offers the best price. When I wanted to dispose of my old Samsung J5 (2016) smartphone, I was surprised by how much the offers I received varied. I was offered between £25 and £40, and naturally opted for the £40 (which happened to come from MusicMagpie).

.When using these services you will need to send the item to them in a padded envelope or a box. You will have to provide this yourself, but the postage is normally free.

Data Security

Before disposing of any item that may contain sensitive information it’s important to erase any personal data, ideally by performing a factory reset. All the specialist companies perform a data wipe on receipt anyway, but it’s clearly advisable to do this yourself as well. If you are selling privately – perhaps via eBay or Facebook – it is essential to ensure that any personal data on the device is permanently erased and can’t be restored.

I hope this article has inspired you to gather together any old tech you no longer need and turn it into useful cash. As always, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post from my colleague Will Pointing from GreatDealsMadeEasy.com.

In his article below, Will sets out his top tips for saving money on many of your home utilities.

Over to Will then…

Many people stay with their utility providers for years and years without changing, on the principle that ‘loyalty pays’.

Sadly, this only really applies with lifelong friends and the Cafe Nero loyalty app (where you get a free coffee after buying eight!). With yearly price rises on most home utilities, it’s a good idea to review them annually (at least) and save yourself £100s in the process.

As a general rule, new customers get the best deals. Below are some tips on how to uncover the golden deals that are right for you…

Broadband – prices increase to £152/year when you remain with them

A survey by Which? magazine found that 71% of respondents stayed with their ISP (Internet Service Provider) for over three years. Most providers offer the best deals on broadband for 12-18-month contracts, meaning after that period prices shoot up significantly.

Tips: Look for what is included in your deal and whether you really need it. Do you need all those TV channels when you have Netflix? Do you need calls included when you have a mobile phone?

Mobile phone – prices increases to £264/year when you stay with them

It so easy to forget when you have paid off your mobile handset (the companies rarely remind you if you have) and then stay on an inflated monthly rate for years. Phone companies create these fashionable adverts to try and convince you to get the latest phone, when actually buying a SIM-only deal until you really need a handset upgrade is the cheapest way. If you want a new SIM-only deal or a new handset, check out comparison sites like my one here.

Tips: Out of contract? Switch to a SIM-only deal. If not, ensure you are on the right tariff for you and you are not paying for unnecessary data (use free wifi when you can to save on using your data).

Water – average bill is £415 a year

Water UK estimate that the average water and sewerage bill is £415 a year or £34.58 a month. It is recommended to get a water meter installed, so the cost is as accurate as possible.

Tips: Water saving tips include having a shower not a bath, washing up manually, and putting a full load of clothes into the washing machine. Many modern machines also have an ‘Eco’ mode, which uses less water and electricity.

Heating and power – cost around £1,254 a year

Using comparison sites to evaluate different energy suppliers and tariffs is perhaps the simplest, most valuable money-saving action you can take. You can often save hundreds of pounds a year by doing this, especially if you haven’t switched for a while (or ever). Again, many customers continue on a high rate for years without asking the question, ‘Is this the best deal for me?’ I suggest using websites like Compare The Market, Money Saving Expert and Go Compare.

Tips: After getting the best possible deal, I recommend submitting regular meter readings to your supplier, so you are not overpaying. And turn off your lights as much as possible!

GreatDealsMadeEasy.com is the website to help you save money online the easy way. Whether you’re looking to cut back on your broadband bill, save on a holiday abroad or come up with a side hustle, Great Deals Made Easy will help you find useful tips and top deals. Expect great articles, interviews, reviews and advice. It’s written by digital marketing expert Will Pointing. Expect to find out how you can save money every month, the easy way!

Many thanks to Will for some great money-saving tips. Do check out his website at GreatDealsMadeEasy.com as well.

My own top tip would be to check out deals from cashback websites when changing utility suppliers. Sites such as Quidco and Top Cashback are especially worth a look when swapping energy companies. I talked about this recently in my blog post about How to Save Money with Cashback Sites.

On various occasions I have pocketed £70 or more in cashback when switching my gas and electricity providers. You can do this directly by signing up with an energy company via the cashback site (check first on a price comparison site that they are offering a competitive deal, obviously). Alternatively, many comparison services are also listed on cashback sites – so by clicking through to the comparison site and then switching via them, you can get cashback – and a good deal – this way.

And speaking of energy suppliers, you can also save money by getting a smart meter installed. These are currently being fitted free of charge by the energy companies. They help you monitor your energy usage and discover ways you can save money. In addition, a growing number of energy suppliers now reserve their best tariffs for people with smart meters. Check out my blog post Should You Get a Smart Meter Installed?

As always, if you have any comments or questions about this article, for me or for Will, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Cashback sites give you money back when you shop with a wide range of online retailers. In the UK the two best known are Quidco and Top Cashback, but there are others as well.

All cashback sites offer different deals which change frequently, so it can be hard to assess which has the best offer at any time. However, a new comparison website called CashbackAngel promises to make this task much easier.

CashbackAngel

CashbackAngel allows you to quickly check and compare deals on offer from cashback sites for any online retailer you may be planning to purchase from. It is therefore much more than just a website that lists and compares cashback sites.

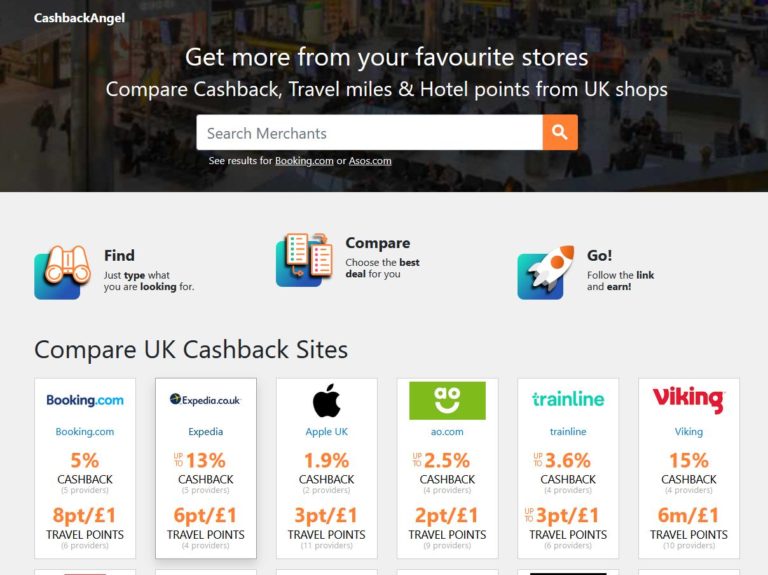

I have posted a screen capture of the CashbackAngel front page below.

The main search box is at the top of the screen and lets you search for any merchant. Below this are example merchants showing the best deal currently available for each one, both in terms of percentage cashback and travel points (should this interest you).

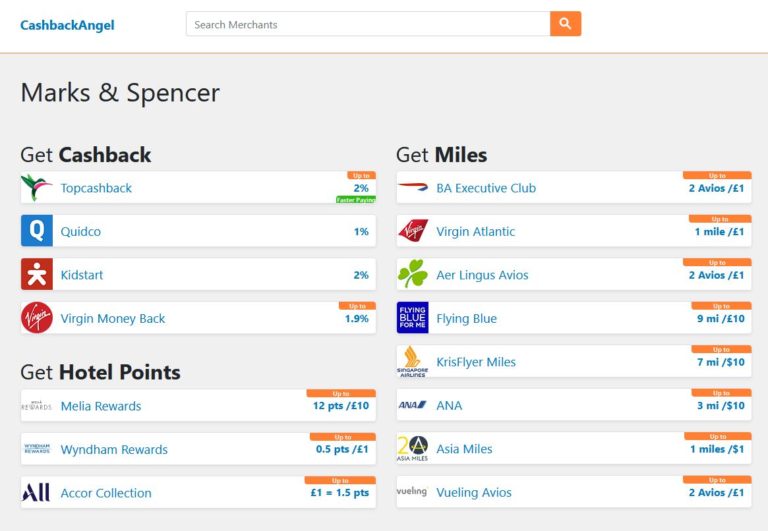

Let’s say you want to find which cashback site offers the best deal for purchasing from Marks & Spencer. Enter the retailer’s name in the search box and click on the search icon. When I did this, the results below were displayed.

As you will see, in this instance CashbackAngel displays results from four different cashback websites: Top Cashback, Quidco, Kidstart and Virgin Money Back (If you’re not familiar with Kidstart – I wasn’t – it’s a site that pays cashback into a dedicated children’s savings account).

In this example, Top Cashback (along with Kidstart) looks as though it might offer the best deal, with cashback of up to 2%. Obviously you would need to check on the Top Cashback site to find out their exact terms. You can do this by clicking through the link on the CashbackAngel results page (shown above). When I did this myself, I found that new M&S customers arriving via Top Cashback get 2%, returning customers 1%.

As you can also see from the screenshot above, cashback is by no means the end of it. If you are collecting Air Miles, CashbackAngel lists a number of providers who are offering these in exchange for shopping with the retailer in question. And you can also earn Hotel Points for various hotel chains if that is your preference.

My Verdict

Overall, I was impressed with CashbackAngel. In particular, I like the way it compares offers in real time, so you can always see which cashback site has the best deal at the time of asking.

It is also good to see a wide range of cashback and rewards sites included – though slightly disappointing that the new My Money Pocket website (which I reviewed here) doesn’t appear to be included currently. Hopefully this will be added soon. [UPDATE: I just heard from CashbackAngel that they intend to add My Money Pocket by the end of January 2020.]

If you use cashback sites – and in my view everyone should! – CashbackAngel is well worth checking out and adding to your online bookmarks.

As ever, if you have any comments or queries about this post, please do leave them below.

Disclosure: Some links in this article include my affiliate code. If you click through and make a transaction, I may receive a commission for introducing you. This will not affect any rewards you receive or terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

I’m starting 2020 by highlighting a banking app called Chip. This is designed to help you put money aside painlessly for any purpose – from holidays to major purchases, or just for a ‘rainy day’ fund.

Chip is one of a growing range of apps that make use of so-called Open Banking. This allows third-party apps to access your bank details – so long as you provide the necessary authorization, of course – and perform certain transactions on your behalf.

Open banking is now becoming well established in the UK, and safeguards are in place to ensure that your security isn’t compromised. Even so, this is something you need to be aware of – and comfortable with – before signing up with Chip or similar apps.

How It Works

Chip is an iOS and Android app that moves money for you in an intelligent way.

Every few days, Chip’s algorithm calculates what you can afford to stash away based on your spending habits. It then transfers that money automatically from your current account to your Chip account. In this way you put money aside regularly while barely being aware of it – so it builds up, and in due course you can spend it on things that really matter to you.

You can change the amounts the app takes at any time, and also pause the service if you wish. This means you don’t have to worry about Chip pushing you into the red (although you do have the option to let it do this if you wish). You always stay in control and are guided by the Chip ‘chatbot’ (see below) through every step.

Chip currently fully connects with Halifax, Lloyds, Nationwide, Barclays, First Direct, Santander, TSB, Metro Bank and Co-operative Bank. If you bank with Monzo, Starling, Revolut, NatWest, HSBC, RBS and N26 (and soon any bank in the UK), you can connect using just your bank card.

How to Get Started

Start by clicking through to my dedicated sign-up page and click on the Download Chip Today button, then follow the on-screen instructions. This page includes my unique referral code which is POUNDS10, so please don’t alter this or you won’t be eligible for the £10 bonus offer (see below).

Once you’ve downloaded the app to your mobile and signed up, you will begin a dialogue with the Chip chatbot to help you set up your account. This includes plenty of cheery repartee, stickers and emoticons. The app is obviously aimed especially at younger adults – who I guess like this sort of thing – but there is no reason older people can’t use it as well.

In any event, it’s relatively straightforward to connect the app to your bank (you will of course need to have your bank account details to hand). Once it’s set up, turn notifications on. This will allow the app to alert you when it wants to start saving for you.

There is an option to speak to a real person if you need to. You can also increase or decrease the level of saving, set savings goals, and even pause saving for up to 90 days.

Do You Get Interest?

The answer to this question – at present anyway – is no. The app is free and helps you set money aside painlessly, but Chip don’t pay interest on this. It is therefore sensible to withdraw money at intervals as it builds up and place it in an interest-paying savings account (assuming you don’t have any immediate requirement for it).

You can withdraw money from your Chip account any time without charge. Tap the ‘withdraw’ button on the app before 5pm on a working day and the money will be back in your current account the same day. If you ask to withdraw your money over the weekend, or after 5pm, it’ll be with you the next working day.

Note though that if you’ve just moved money into your Chip account (either manually or with an auto-save), it may take up to 48 hours for this money to be cleared for withdrawal.

Where Do Chip Keep Your Money?

The app puts money away in your Chip account, which is a new account you open when you sign up. You can access the money in this account at any time but it’s important to note that it is not a savings account and doesn’t have FSCS protection. Rather, your cash is stored as e-money.

Chip work in partnership with electronic-money specialists PFS (Prepaid Financial Services) to store your cash. PFS store the money with a major retail bank (currently Barclays) in a ring-fenced account, which means it’s never used for any trading activities. Chip also boasts 128-bit encryption to ensure your data is safe.

Welcome Bonus

Currently I am able to offer Pounds and Sense readers a special offer for trying Chip out. If you sign up now using my unique referral code of POUNDS10, you can get a £10 bonus credited to your account.

After just two auto-saves using the app, you will be eligible for the £10 bonus. This will usually happen within two weeks. The bonus will then be credited to your Chip account within 30 days.

The £10 Welcome Bonus is available from today (1st January 2020). I am not sure how long this offer will remain open, however. So if you don’t want to miss out, I highly recommend that you sign up as soon as possible.

Final Thoughts

If your new year’s resolution is to put a bit more aside – or you just need a little help and encouragement doing so – Chip is well worth a look.

I like the way it stashes money away automatically, so in all probability you won’t even notice it. You can set it to take as much or as little as you like, and you can also make one-off additional payments if you are feeling particularly flush. You can also withdraw some or all of your money back to your bank account at any time.

Admittedly Chip doesn’t (currently) pay interest, but it doesn’t impose any charges either. Even so, it is obviously sensible to move money from your Chip account to a savings account at intervals rather than letting it build up too much.

In my view Chip is likely to work best for people with a regular monthly (or weekly) income. If you receive income more irregularly – e.g. you’re self-employed – it might not work quite as well. Even so, Chip say that their algorithm can detect patterns in your income and expenditure and adjust your transfers accordingly.

In any event, there’s no reason not to try Chip yourself to see if it can help you put aside more and take advantage of the current £10 welcome bonus. Just click through this link for more information and to sign up.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I am an affiliate for Chip so if you click through any link in this article and sign up using my referral code, I will receive a modest commission. This will not affect the service or benefits you receive. Indeed, clicking through a referral link such as mine is the only way you can get your hands on the £10 Welcome Bonus!

If you enjoyed this post, please link to it on your own blog or social media: