In this recent blog post I discussed how over-75s may be able to avoid losing their free TV licence by claiming pension credit.

As I said then, I have recently done this myself on behalf of an elderly couple who are friends of mine. As promised, today I’ll be sharing my experience of the telephone application process. I hope anyone thinking of doing this themselves or on behalf of elderly friends or relatives may find this helpful.

But first, let’s recap on what pension credit is…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions (DWP), around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4%). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify.

While for most people pension credit won’t be a huge amount, it has the big advantage that it acts as a gateway to a range of other discounts and benefits. The free TV licence for over-75s is just one of them. Pension credit recipients may also get reduced council tax (or free if awarded guarantee credit), free NHS dental treatment, help towards the cost of glasses, help with the cost of travel to hospital, cold weather payments, automatic entitlement to the Warm Home Discount, help with rent, free home insulation and boiler grants, and more. All of this means it is well worth applying for, even if you’re not certain whether you qualify.

Checking Your Entitlement

The government is keen that anyone eligible for pension credit should claim it. To that end they recently launched a free online calculator you can use to work out whether you qualify and how much you might get.

You can use the calculator anonymously to check your entitlement (or someone else’s), either as an individual or a couple. You can’t actually apply via the calculator, though. It is just for guidance, to help you decide whether it’s worth putting in a claim.

The calculator asks a variety of questions about your circumstances and current income, including any pensions or other benefits you may receive. The latter may actually improve your chances of getting pension credit. For example, if you receive attendance allowance and/or carer’s credit (as my friends do) this can improve your chances of qualifying. When I did this on behalf of my friends, the calculator showed that they should be eligible for a payment of just over £10 a week.

As mentioned above, the results on the calculator are for guidance only, and there is no guarantee that you will receive the amount shown. However, in my friends’ case it definitely confirmed that applying would be worth doing.

Applying for Pension Credit

By far the easiest way to apply for pension credit is to phone the DWP’s Pension Credit Helpline on 0800 991234. You will need to have your National Insurance number, information about your income, savings and investments and your bank account details to hand.

If you’re applying on someone else’s behalf, the DWP like you to have the person concerned with you at the time. The call handler spoke briefly to my friend to confirm her personal details and that she was happy for me to take over the application process.

It turned out to be a two-stage procedure. Initially I spoke to a male call handler who asked a list of questions about my friends’ circumstances and their finances. This was basically the same set of questions I had answered on the online calculator. It was reasonably straightforward, and at the end he informed me that my friends did indeed appear to have a valid claim, so he was going to put me through to his colleague who would take me through the actual application.

This meant that I had to answer the same set of questions again from another DWP employee – a woman this time, as it happens. This did strike me and my friend as rather a waste of everyone’s time. We wondered why the answers I had given initially couldn’t just be passed on to the second person, but I suppose the DWP must have their reasons.

Anyway, we duly went through all the questions (and a few more) again. I would, incidentally, comment that the young woman I spoke to – who told me her name was Jenny – was extremely pleasant and helpful. At one point we went off at a tangent and started talking about our favourite cakes (well, it was tea-time by then). I felt she went out of her way to help us, and she certainly made the whole application process a lot less stressful.

After going through all the questions, Jenny said she would need information about how much exactly was in my friends’ bank accounts and when their (small) private pensions were paid in. This could have been problematic, as it involved logging in to my friends’ online bank accounts and finding this information there. But Jenny was patient and flexible about this, and in the end we found all the information she needed.

The whole process took a little over an hour. if you have to break off half-way through that is possible and you can ask for a reference number so you can complete the application another time. But I really wanted to get the whole thing done and dusted in one call, and thankfully – with Jenny’s help – we achieved that.

The Outcome

After about six weeks my friends received a letter from DWP saying their application had been successful and they had been awarded pension credit.

The amount was the same as had been shown on the online calculator. It was about £10.50 a week, going up to almost £12 in April (I’m sorry I can’t remember the exact figures). This money was savings credit rather than guarantee credit, but that makes no difference as far as the free TV licence is concerned. If you are over 75 and qualify for either type of pension credit (or both) you are entitled to a free TV licence.

We then submitted the short application form to the TV licence people, with a copy of the first page of the DWP letter confirming the award of pension credit. We haven’t heard any more since, but presumably my friends will receive their free TV licence in the coming weeks.

So that was my experience of applying for pension credit on my friends’ behalf. I hope it has encouraged you to proceed with your own application if you are considering making one. If you get to speak to the lovely Jenny in Scotland, do pass on my regards to her!

And if you have any comments or questions about this post, of course, pleased free free to leave them below as usual.

This is a fully updated repost of my March 2020 article.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a method for making money online I have used for many years, including (of course) on this blog.

Affiliate marketing entails promoting other people’s products and getting a proportion of the sales generated as commission.

In a way affiliate marketers are like freelance salespeople, but rather than visiting potential buyers in person, they simply have to get them to click through to their merchant partners’ websites via their affiliate links.

Why Affiliate Marketing?

For home-based entrepreneurs, affiliate marketing offers a great opportunity to make money online with a minimum of hassle. One beauty of the method is that you don’t actually have to supply the product or service you are promoting. Once you have delivered your prospect to the merchant’s sales page, the rest is up to them. You can simply sit back and await your commission!

A further benefit is that when someone clicks on your affiliate link, in many cases a tracking cookie is applied to them. These vary in duration from 24 hours to six months or more. If the prospect returns to the merchant’s website at any time during this period, as the referring affiliate you will still be credited with any commission generated.

Affiliate marketing can be great for earning a sideline income, but if you’re prepared to put a bit more work in, the returns can be substantial. Some so-called ‘superaffiliates’ allegedly make six-figure incomes this way. Of course, when first starting out your earnings are likely to be more modest than that, but there is no reason why in time you could not emulate their success.

There are lots of ways you can apply the affiliate marketing method. They include blogging, email newsletters, social media, and more. In fact, if you have any sort of online presence, the chances are you could boost your income through affiliate marketing. In this article I will look at some of the most popular (and effective) approaches. But before we get to that, let’s look at how it works in a bit more detail…

Getting Started

To become an affiliate marketer you will first need to be an online publisher. If that sounds daunting, don’t worry. It could simply mean setting up a free blog using Blogger.com, which you can do in 10 minutes or less. Or you could use social media and/or build a mailing list (all discussed in more detail below)

You can then apply to become an affiliate with one or more merchants. Affiliates are supplied by the merchants with special links and other advertising tools, and can place them on their websites. No particular technical expertise is required, just the ability to copy and paste a bit of code.

If someone visits your site and follows your affiliate link to the merchant’s site and buys something there, you will get a proportion of the money they pay as commission. Special tracking systems are used so that merchants know where customers have been referred from and pay affiliates their due.

Commissions vary widely. The biggest are typically paid in respect of downloadable products, such as e-books and software. Commissions of 50% or more are routinely paid for such products. By contrast, with physical products, where the merchant’s profit margins are typically much lower, your commission may be just a few percent. Of course, with an expensive item, even a commission of a few percent can be a significant amount.

Large companies such as Amazon run their own affiliate programmes. Many smaller companies, however, use the services of affiliate marketing platforms to run affiliate operations on their behalf. Some well-known affiliate marketing platforms include ClickBank, Commission Junction and Awin. As a publisher you can apply to join any of these platforms and will then be able to promote any of the merchants listed on them (though sometimes the merchant will need to give their approval as well).

I will now look at the platforms mentioned in a little more detail…

Affiliate Marketing Platforms

Amazon

Amazon is of course the world’s favourite online store. They sell a huge range of products, from books to clothing, cameras to garden equipment, computers to groceries.

Their affiliate programme is called Amazon Associates and any online publisher can apply to join. As long as your site looks reputable and has some relevant content, you are likely to be accepted.

Amazon does not offer especially generous commission to affiliates, currently starting at around 1% and going as high as 12% in limited cases. There are various good reasons for choosing to promote them, though. As well as the huge range of products on offer, Amazon have an excellent reputation for value and customer service. If you can get customers to the store, there is every chance they will buy something there.

A further consideration is that if a customer makes other purchases at the same time, you will also receive commission for these. In the run-up to Christmas in particular, when people often make multiple purchases, this can give your affiliate income a real boost.

ClickBank

ClickBank is an affiliate marketing platform. They list downloadable manuals and software in a wide range of categories, with commission of up to 80 percent paid by vendors. If you sign up as an affiliate with them you can immediately start promoting any of the thousands of products in their marketplace.

My top tip for new ClickBank affiliates is to focus on products with a “gravity” between 20 and 100. Gravity is a score given by ClickBank that shows how many affiliates have earned a commission by promoting that product during the last three months. Lower than 20, and it’s probably not selling very well. Over 100, and the competition from other affiliates will be intense.

Commission Junction

While ClickBank focuses solely on downloadable products, Commission Junction is an affiliate marketing platform covering a huge range of products and services. They list thousands of merchants, in categories from travel to legal services, beauty to sports and fitness.

As a publisher you start by applying to join Commission Junction. Once you have been accepted, you can then browse the merchant offers and apply to promote any that catch your eye. Some merchants automatically accept all applications, but others like to approve affiliates themselves. This normally only takes a day or two.

Commission rates on CJ vary considerably, but they are clearly set out on the site. Once you have been approved, you will be able to download affiliate links and advertising banners for the merchant in question. You will be able to monitor sales by logging in to your CJ account. Payments are then made monthly by direct transfer to your bank account.

Awin

Awin has lots of well-known consumer brands on board, and is a very popular platform among UK bloggers. It operates in a similar way to Commission Junction (see above). You have to pay a small fee (£5) to register as an affiliate with them, but this is refunded once you have earned enough commission to qualify for your first payout.

Blogging

In my view one of the best ways to make money from affiliate marketing is through blogging. If you don’t have a blog already, you can easily set one up at Blogger.com, the free blogging platform run by Google. Ideally, though, I recommend setting up your blog using a self-hosted WordPress platform (like Pounds and Sense). There is more of a learning curve with WordPress, but you have the freedom to configure your blog exactly as you want it.

The best type of blog for this purpose is a niche blog – that is to say, a blog devoted to a particular interest or activity. That could be anything from gardening to fishing, photography to computers. You can then write about this subject on your blog and include affiliate links to relevant products and services.

One of the best ways of doing this is by publishing reviews, with affiliate links to the product (or service) concerned. If a reader is inspired to buy after reading your blog review, as long as he/she visits the merchant’s site via your link, you will receive a commission.

Of course, if you’re going to do this, you will need to give a balanced review of whatever you are promoting. Emphasize its good qualities, certainly, but don’t be afraid to mention any shortcomings as well. Readers will be more inclined to believe you – and trust you in future – than if you simply hype any product you are selling to the skies.

Another tactic that can work well is to offer a free, downloadable bonus to anyone buying via your link. This can be especially effective with business opportunities and software products. You could offer a complementary product such as a user guide or case study. Ask people to email you a copy of their receipt and send them your bonus in the same way.

Naturally, for this type of marketing to work, you will need to attract a steady stream of interested visitors to your blog. A full discussion of how to do this is outside the scope of this post, but there is of course plenty of free information on this subject online (see also Taking It Further, below).

List Marketing

Affiliate marketing also works extremely well in conjunction with running a mailing list or online newsletter. If you have a list of people interested in a specific topic, you can email them with a series of affiliate offers relevant to their interest, and potentially make multiple sales to the same buyers.

Running a niche blog, as mentioned above, gives you a great opportunity to start building a list. All you need do is add a sign-up box on the front of your blog.

One thing I strongly recommend, though, is opening an account with a mailing list management service such as GetResponse or Aweber. These services handle subscribe and unsubscribe requests automatically, together with changes of email address. They also ensure that any would-be subscriber must click on a link in a confirmation email before being added. This ‘double opt-in’ method ensures you have proof they did actually subscribe to your list if any accusations to the contrary are made later.

There are many other benefits to using a mailing list service. For example, most such services will monitor how many people are opening your messages, and even let you selectively remail those who didn’t read them first time round.

As with affiliate reviews, another good tactic is to offer potential subscribers a ‘bribe’ for signing up. A short report or e-book could be a suitable choice. Choose a downloadable bonus if at all possible, as the process of getting it to your subscriber can then be automated.

Social Media

You can also promote affiliate offers through social media such as Facebook, Twitter and Instagram.

A word of warning is in order, however. The social media platforms all have their own rules about affiliate marketing and what they will and won’t allow. That means affiliate links may be frowned upon and in some cases banned. There are ways around this, e.g. you can convert your affiliate link using a link-shortening service such as the free tinyurl.com. This may work, but it’s not guaranteed! There are also rules to follow about disclosing promotional posts and/or affiliate links (see below).

A better method, in my opinion, is to use social media to help drive traffic to your blog posts, where your money-making affiliate links are located. Another option is to create a dedicated landing page which is designed to get visitors to click on your link (you could also use your landing page to sign people up for your newsletter). You will need your own blog or website to host a landing page, but you can also get basic landing pages for free if you join an autoresponder service such as Aweber.

Once you have a landing page, you can link to it from Facebook or other social media with no fear of being blocked or banned.

Affiliate Disclosure

In the UK (and most other countries) there is a legal requirement to make clear that you are using affiliate links for marketing purposes. This is to avoid consumers being misled.

In the UK this area is overseen by the Advertising Standards Authority (ASA). They publish guidelines which do not in themselves have the force of law but are based on the relevant laws.The guidelines are not always as clear or specific as one might like, but a guidance document relating to ‘influencers’ (which includes bloggers and social media personalities) can be downloaded here.

The main point made in the ASA guidelines is that it should always be clear to a visitor to your website (or whatever) when they are reading an advertisement or clicking on an affiliate link. There are no hard and fast rules about how exactly this must be done, so different people take different views. Personally with Pounds and Sense I have a general Affiliate Disclosure page, and also include a separate disclosure paragraph in any post with affiliate links or other commercial associations. At the start of each post it will also say if it is (for example) a sponsored post. I have never encountered any problems using this approach, but obviously it is something everyone needs to decide for themselves based on the guidelines.

If you also use email marketing, you can (and almost certainly should) include a note near the end of every email such as, ‘The sender of this email has an affiliate relationship with the authors of the products mentioned and may receive compensation from them in the event of a purchase.’

More Top Tips

Here are a few more tips for maximizing your income from affiliate marketing…

Promote products you can genuinely recommend, preferably because you’ve used them yourself, or at least based on solid evidence.

Talk about what you like and don’t like. Be honest with your readers and build trust. People are far more likely to buy things you recommend if they have learned to trust you in the past.

Take any opportunity to promote products in passing, as well as in dedicated posts. For example, in a gardening blog, if you’re talking about a particular plant species, you might mention in passing a supplier from whom you have received good specimens in the past. Low-key recommendations such as this can be surprisingly effective for generating sales.

Don’t put all your eggs in one basket. Promote multiple affiliate products. Better yet, diversify across all income streams. In other words, use affiliate marketing, but also use other forms of income generation such as selling your own product, offering a service, or selling advertising space on your blog.

Although most affiliate offers involve a payment per sale, in some cases merchants will pay for other outcomes, e.g. a quotation request (for insurance perhaps). As you gain experience it is worth looking out for such offers to promote, as they can be very lucrative. The same goes for recurring subscriptions.

Create a ‘Tools I Use’ or ‘Things I Love’ page on your blog. Many readers will enjoy seeing a handy list of your favourites, plus it’s an easy way to promote some affiliate links.

Taking It Further

Once you have made your first few commissions from affiliate marketing, the chances are you will want to take it further to increase your earnings from it.

Key to this is driving more potential buyers to your website. I have provided some tips above, but if you want to boost your income to the next level, you might want to consider engaging an SEO (search engine optimization) company – like my friends at the UK-based Lojix, perhaps.

Lojix are a digital marketing agency offering affordable SEO, pay-per-click advertising management, PR, marketing and website design services. They say they will work with you to increase the number of leads that you get from your website, whether that is an increase in orders from an e-commerce site or an increase in sales leads for businesses that are service providers. They say they work with businesses that require just a local presence right up to companies that trade all over the world. I asked my colleagues at Lojix what were their top tips for boosting your income from affiliate marketing, and they came up with the following:

1. Don’t be lazy by copying and pasting descriptions of products you want to promote. If your marketing strategy involves getting organic visits – which should be top of your list – Google is likely to ignore your content if you do this and won’t rank your site high in their search results at all.

2. If you are just starting out with your site or blog you should probably go down the niche route, as trying to get organic visits from Google for popular products will be difficult.

I definitely agree with both these points. There is much to be said for researching search terms and targeting those that have reasonable traffic but not so much competition that it’s hard (or impossible) to compete. A reputable, professional SEO agency such as Lojix can assist with this. If you think they might be able to help you – without any obligation – please do drop them a line.

Closing Thoughts

Affiliate marketing is a great way to make money online, with a minimum of hassle and expense. It is therefore ideally suited to home-based entrepreneurs. The method can be applied in many different ways, though blogging and email marketing are especially effective.

It has a further advantage in that once you have published, say, a product review on your blog, it will remain there indefinitely, potentially generating further affiliate fees for you over a long period. One review I wrote some years ago on my former freelance writing blog (for a self-development product) made me well over £3,000 in total.

Obviously, not all of your affiliate promotions are likely to prove as profitable as this, but the beauty of affiliate marketing is that you can promote almost anything you like. If one offer doesn’t perform as well as you hoped, there is always something else you can try.

Good luck, and I hope you make lots of money from affiliate marketing!

As always, if you have any comments or questions about this article, please do post them below.

Disclosure: This is a sponsored post on behalf of Lojix.

If you enjoyed this post, please link to it on your own blog or social media:

One thing the virus pandemic has brought home is how ill-prepared many of us are for sudden emergencies that impact on our finances.

In a short space of time many people have been thrown out of work and/or seen their income plummet, due in part to the virus but also to the measures taken to control it.

Obviously in future there will be enquiries to determine what things government did well and what they did badly, and what lessons need to be learned. But for all of us it has been a wake-up call on how quickly things can change, and the importance of being prepared for a sudden, unexpected hit on your finances.

Of course, that need not mean another pandemic. It could just as well be an accident or illness, losing your job, or a sudden change in your domestic circumstances.

In general financial experts say you should aim to have at least three months’ worth of income in an easily accessible form to cover sudden emergencies. This will give you breathing space to respond and (hopefully) get your finances back on an even keel. The reality is, however, that many of us are not fortunate (or prudent) enough to be in this position.

A survey of 2,000 UK adults by OnePoll commissioned by online banking website Raisin produced some eye-opening results…

Survey Findings

The key findings of the Raisin survey are summarized below:

The average savings amount of a person in the UK is £9,633.30.

Men have almost double (£13,140.61) the average savings of women (£6,869.84).

The lowest average savings in the UK are found in the East Midlands (£6,438.48) followed closely by Northern Ireland (£6,710.00).

Londoners have by far the highest average savings with £28,978.40. This is more than double the second-placed West Midlands (£13,318.35).

Almost 1 in 5 of those aged 55 or over (approaching or at retirement age) has just £1000 or less in savings.

When asked ‘How much, to the nearest pound, do you have in your savings account(s) today?’ 848 of the 2,000 respondents declined to answer the question. Of the 1,152 people who did, replies were as follows:

6.5% said they have no savings whatsoever.

26% said they had less than £1,000 saved.

Using the Trimmean mean, taking the middle 66% of responses to give a realistic figure excluding outliers, the average savings of a person in the UK is £9,633.30.

Regional Variations

Those living in London have more than four times the savings of those living in the East Midlands.

The lowest average savings in the UK are found in the East Midlands (£6,438.48) followed closely by Northern Ireland (£6,710.00)

London has the highest average savings by far with £28,978.40. This is more than double second placed West Midlands (£13,318.35)

Age Variations

The survey found that in general, as you might expect, those in older age groups tend to have more savings:

Average Savings

% With £0 in Savings

% With £100 or Less in Savings

% With £1000 or Less in Savings

18 to 24

£2,481.16

10.83%

27.50%

50.83%

25 to 34

£3,544.16

12.38%

21.78%

42.08%

35 to 44

£5,995.92

7.91%

12.99%

33.33%

45 – 54

£11,013.99

6.34%

11.22%

25.85%

55 and Over

£20,028.60

2.23%

7.59%

18.08%

It’s not all good news for older people, though. Almost 1 in 5 of people aged 55 or above in the survey had less than £1,000 of savings.

The average savings among over-50s are admittedly almost double those of the 45s to 54s (and more than double the national average). But £20,028.60 – the average savings of someone over 55 in the UK – is still less than the national average salary of a full-time employee (£28,677 according to the most recent Government data).

It’s important to note that these findings don’t take into account other assets (such as properties or businesses) people may own. They do, however, represent a large cohort of people who are approaching retirement age and don’t have any significant savings to cushion them from financial turbulence.

My Thoughts

Overall, the Raisin survey indicates that many of us are ill-prepared for any crisis that may affect our finances.

Older people in general are slightly better off, but there are still large numbers heading towards retirement with almost nothing in reserve. That is especially alarming for those who – for reasons such as ill-health or caring responsibilities – are unable to work and dependent on state benefits.

There are, of course, no easy answers. I do appreciate that many people have barely enough income to cover their day-to-day spending. And the appeal of putting money into a savings account has undoubtedly reduced in recent years due to the ultra-low interest rates on offer.

Nonetheless, I do still think it’s essential for everyone to have some accessible savings for emergencies. And the earlier you start saving – even if it’s only small amounts – the more time your money has to grow.

Personally I am currently keeping most of my ’emergency savings’ in a Santander 123 Lite account (as discussed in this recent blog post). This doesn’t pay interest, but you do get cashback on a range of household bills. Even with their £1 a month fee, I am earning around £50 a year tax-free (cashback minus fees) from this account, which in this low-interest-rate environment is at least something. Santander is protected by the Financial Services Compensation Scheme (FSCS) which protects savers with UK banks against losses of up to £85,000 if the bank fails. I am therefore confident that my cash will always be available quickly if I need it.

Another savings option that might suit some people is Raisin (who sponsored the survey mentioned above). They say their ‘free one-stop online savings solution has been designed to help you earn more money from your savings. With a range of partner banks offering FSCS-protected savings accounts with competitive rates in one place, we take the hassle out of finding the right savings account for you.’ On their website Raisin also say they plan to launch an easy access savings account of their own soon.

I hope you enjoyed reading this post and found it informative. I’d love to hear what you do about emergency savings and where (if you have any) you keep them. As always, any comments or questions can be posted below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. You should always do your own ‘due diligence’ in financial matters, and seek advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

The infographic is based on a YouGov survey commissioned by Paymentshield as part of National Conversation Week, which this year runs from 11-18 May.

Among other things, the survey revealed that money is currently the third-biggest concern for the public, following fears for friends and family, and health worries. More than a third of respondents (39%) also reported a decline in their mental health since March 2020. Thirty-eight per cent of people said their financial worries had increased during the coronavirus outbreak.

About National Conversation Week

National Conversation Week aims to get people talking in a bid to improve the nation’s well-being, at a time when people are facing unprecedented challenges and are separated from each other. In particular, this year’s awareness week encourages conversations about money, to tackle increasing financial worries among consumers.

Financial organisation Paymentshield has teamed up with independent financial research company Defaqto and mental health charity Mind to emphasise the importance of financial conversations, and the close relationship between financial and mental well-being.

Financial worries have a huge impact on mental health, and talking to someone about the situation can be very helpful. However, the survey found that nearly a quarter of people (24%) are avoiding talking about finances with friends and family, for fear of burdening them or making them anxious.

As well as the effect on mental health, coronavirus is affecting consumer behaviour. Thirty-six per cent of people say that coronavirus has already had a negative impact on their personal finances, with 35% increasingly trying to cut costs during lockdown.

During periods of financial uncertainty, people tend to consider their outgoings and can be tempted to make risky financial decisions based purely on cost alone. Despite the increase in money worries and a drive to cut costs, 92% of people had not spoken to a professional financial adviser. Doing so could help alleviate concerns and provide greater understanding of each individual’s situation for peace of mind.

Jennifer Ripley, Head of Marketing at Paymentshield, said:

“The current situation has affected everyone in different ways. People are facing a variety of challenges, from health worries to loneliness, and concerns about loved ones on top of financial difficulty and uncertainty. National Conversation Week aims to encourage safe, socially-distant talking as a way of alleviating some of those worries. In particular, we want to raise awareness that a simple chat about money can help, especially when it comes to making risky financial decisions. This week, we urge everyone that is worried about finances to talk to a professional financial adviser.

“Our research found that 41% of people are actually talking to friends and family more during the lockdown, through messages, video calls, and phone calls. We’re calling on the nation to keep the conversations going, so people can help to cheer each other up and take care of each other during these tough times.”

The annual awareness week, founded by Paymentshield, is now in its fourth year. For more information, resources and advice, or ways to get involved, visit: http://www.nationalconversationweek.co.uk

My Thoughts

Thank you to my friends at National Conversation Week for the information above and the infographic. There are some pretty shocking stats in this, including the fact that nearly 40% of people admit to their mental health declining since the start of the pandemic.

So it really is essential to reach out for support if you need it right now, whether for financial, mental health or other reasons. Speak to friends and family members, and to financial experts if appropriate (here’s a link to my blog post about why I have a personal financial adviser). There is also some great advice about looking after your mental health during the pandemic at www.mind.org.uk/coronavirus.

Above all, though, be kind to yourself, and don’t suffer in silence. And equally, if you know someone who may be struggling – or you just haven’t seen or heard from them for a while – reach out by phone or at least message them to check they are okay. It may be a bit of a cliche, but we really are all in this together. And pretty much everyone is struggling in their own way.

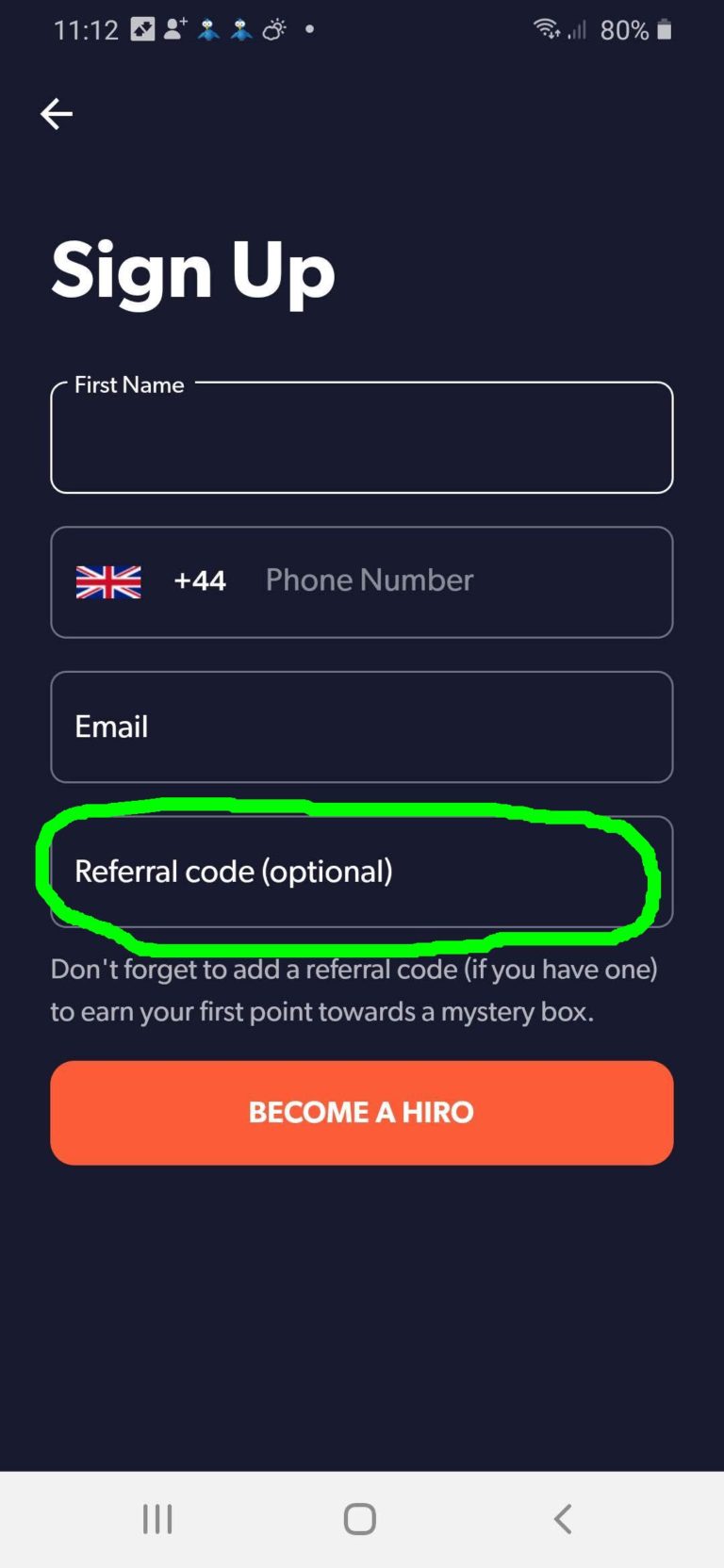

Hiro is a brand new new mobile phone app currently offering a range of incentives just for downloading it and answering a few quick questions about the smart tech you have in your home.

Hiro say that in future they plan to offer members personalized discounts on home insurance and similar products based on their home technology – from Amazon Alexa devices to smart thermostats, doorbell cameras to smart locks.

Right now, though, there is nothing to buy. They are simply looking to build a community of people who may be interested in saving money on insurance in future. And to do this they are offering gifts for downloading the app and signing up. These range from £5 Amazon gift vouchers to £5/£10 Hiro credits, and lots of other weird and wonderful things as well. Here’s how it works…

Grab Your Free Prize

Start by downloading the Hiro app from Google Play or the Apple Store. Open the app and here is what you should see…

Enter your first name, (mobile) phone number and email address in the appropriate boxes. Where it says ‘Referral code’ (highlighted above) please enter nic637, then tap on ‘Become a Hiro’.

You will then be presented with a short questionnaire about your use of smart tech in the home. When I did this, the app told me that with my modest complement I would be eligible for a 17% discount on my home insurance. That’s nice to know, though of course it won’t mean much until Hiro start selling actual insurance.

They say as well that even if you don’t currently have any smart technology, they will be making recommendations and special offers, and explaining the extra discounts the tech in question can bring you.

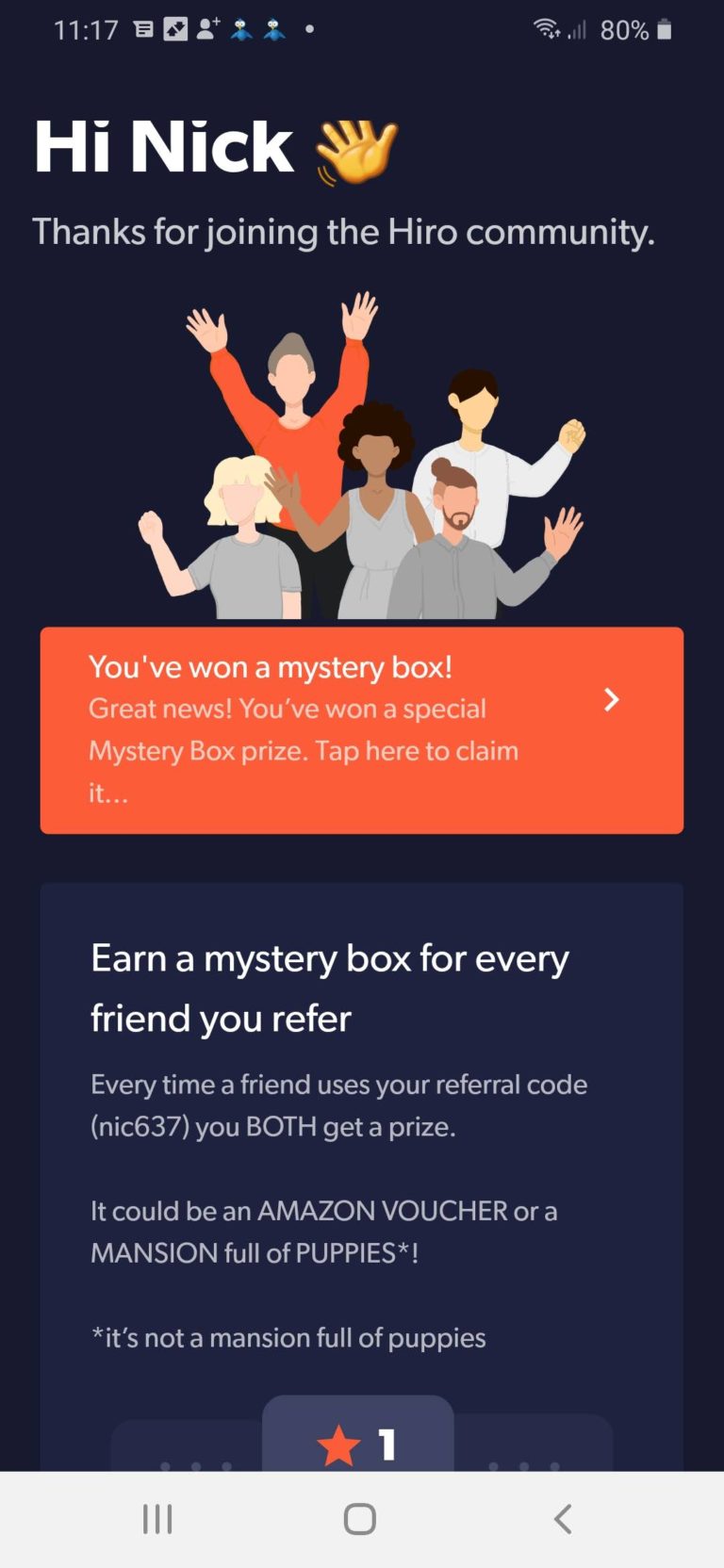

In addition, once you’ve answered the questions, we will BOTH be eligible for a prize (or mystery box, as they call it). Here’s the screen you should see…

Just tap on the the orange box (see screen capture above) to see what you have won.

Of course, once you have signed up you will get a personalized link as well and be able to share this with friends and family. Any time someone signs up using your link, both of you will win a prize. As I said above, there is nothing to buy now and no obligation in future.

Good luck, and I hope you win something almost as exciting as a mansion full of puppies 🤣🤣🤣

As always, if you have any comments or questions about this post, please do leave them below..

Update 19th May 2020 – I have just heard that Hiro aren’t offering Amazon vouchers as prizes at the moment. Other prizes such as Hiro credits are still on offer.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing some information about National Conversation Week, a collaborative initiative between financial organizations Paymentshield and Defaqto, together with mental health charity Mind.

What is National Conversation Week?

National Conversation Week – which this year runs from 11 to 18 May – aims to get people talking in a bid to improve the nation’s well-being, at a time when we are all facing unprecedented challenges and are separated from one another. This annual awareness week, founded by Paymentshield, is now in its fourth year.

Through safe conversations via phone, video calls, or any other socially-distanced method, people can bring comfort and care to one another during the current crisis. National Conversation Week reminds people to get in touch, and encourages creative ways of connecting with friends, family, neighbours, acquaintances, online communities and professionals, to give and receive much-needed support.

In particular, National Conversation Week hopes to encourage conversations about money, to tackle financial worries. A recent YouGov study of over 1000 GB adults, commissioned by Paymentshield, revealed that finances were the single biggest concern when asked to select from a list of 7, with 32% of respondents admitting that money is the thing that worries them the most – ranking higher than work, family, friends, fitness, housework, and hobbies. This is likely to have increased following the outbreak of coronavirus, with many people facing additional financial difficulty and uncertainty.

Financial Worries and Mental Health

Financial worries have a huge impact on mental health, and talking to someone about the situation can be very helpful. Shockingly, Paymentshield’s research discovered that 41% of people rarely ask for financial advice when they need it.

According to financial experts at Paymentshield, during periods of financial uncertainty, people tend to consider their outgoings and can be tempted to make risky financial decisions based purely on cost. Seeking the help of professionals is especially recommended during these periods, to avoid being left vulnerable if, for example, you cancel an insurance policy and are no longer protected, or swap to a cheaper policy without understanding how to avoid higher compulsory excess fees. National Conversation Week raises awareness of the benefits of talking to financial advisers, so that people can have a better understanding of what they can do if their circumstances have changed.

As part of the awareness week, a variety of free resources and information have been released. This includes mental health information from Mind, which is National Conversation Week’s charity partner for the second year in a row.

Stephen Buckley, Head of Information at Mind, says:

“The coronavirus outbreak will have a long-term impact on our economy – we’re likely to see another recession as the nation attempts to get back on its feet. We know there is a strong link between issues like debt, unemployment, poor housing and poor mental health.

“So, it stands to reason that factors like job insecurity, unemployment, low paid work and redundancy could have a knock-on impact on mental health. Unfortunately, we know these kinds of factors disproportionately affect people who have existing mental health problems. That’s why it’s important that financial support and support with wider social issues are there for people when they need it.

“Speaking about these issues and asking for help may seem daunting but sharing your worries can be a real relief and is often the first step in getting the help you need. We’re supporting National Conversation Week in the hope that it will encourage people to speak to a friend, family member, or another trusted individual about how you’re feeling.”

Jennifer Ripley, Head of Marketing at Paymentshield, says:

“We might not be able to see each other face-to-face, but that doesn’t mean that conversations have to stop. We know that right now is a particularly worrying and challenging time, especially with so much uncertainty, and whilst people are cut off from their usual support networks. It’s more important than ever before that we stay in touch, especially when it comes to financial conversations. Money is one of the biggest contributors to poor mental health. We’re calling on the nation to keep the conversation going – from video calls with a financial expert, to a chat with grandparents – and support each other.”

Independent financial research company Defaqto is also supporting this year’s National Conversation Week. Its independent comparison tools can be used alongside conversation on many websites (such as this one) to gain a better understanding of the overall value and quality of a financial product.

To mark the start of the week, Paymentshield has also launched an online quiz to help people find out more about their financial personality, and how conversation could benefit them. Why not try it out now to see what sort of financial personality you have? I am ‘Budget Bobby’, apparently!

Thank you to my friends at National Conversation Week for sharing the information above and, in particular, raising the very important issue of mental health and financial awareness at this challenging time. I strongly recommend checking out the website resources mentioned. And I’d like to endorse the advice that if you have money worries, don’t bury your head in the sand. Speak to friends and family members, and to a financial expert if appropriate (here’s a link to my blog post about why I have a personal financial adviser).

As so many of us are struggling financially right now, I’ve teamed up with some fellow UK bloggers for a great giveaway. We have over £100 worth of supermarket vouchers to help two lucky winners with their grocery shopping 🙂

The first prize is a whopping £75 voucher. The runner-up will receive a £30 voucher. Both vouchers will be for supermarkets of the winners’ choice. The prizes will be e-vouchers for supermarkets that offer home delivery, including Tesco, Asda, Sainsbury’s, Waitrose and Iceland (subject to availability).

This giveaway has been organised by my fellow blogger Kellie Steed at the comping website Prize Warriors. Do check out her excellent site if you are interested in winning more cash and prizes from consumer competitions!

To enter the Bloggers Together Giveaway, all you have to do is work down (or up) the Rafflecopter widget below. As you will see, for each action you take (e.g. following a blogger on Twitter or visiting their Facebook page) you will receive one entry. The winners will be drawn at random, so the more times you enter, the better your chances of success.

The closing date is 31st May 2020, so get clicking now!

All of the bloggers listed below have contributed towards this giveaway prize. Please check out their blogs via the links below. They are all well worth reading, and many run giveaways of their own too.

I do hope you enjoy taking part in this giveaway, and even if you don’t win a prize you discover some wonderful bloggers to follow in future.

One small point is that if a winning entry comes from following someone on social media, Kellie will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow (or claim to be following when you’re not), as your entry won’t then count.

Good luck if you enter the Bloggers Together Giveaway – it would be great if a Pounds and Sense reader won one (or both) of the prizes!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m focusing on a money-making opportunity that is literally open to anyone. It involves advertising your services on a website called Fiverr.

What is Fiverr?

Fiverr is a US-based site that lets anyone advertise ‘gigs’ (tasks) they are willing to perform for five dollars – hence the name, of course. You are also allowed to charge more than $5 as you gain positive feedback and experience.

Gigs range from the serious (e.g. write a press release) to the creative (e.g. design a tee-shirt – see cover image) to the downright quirky (e.g. write your message, name or URL in chocolate). Most gigs are services that are delivered electronically, though there is nothing to stop you selling physical products if you wish (you can charge extra for postage).

Fiverr was launched in 2009, and they recently revealed that freelance earnings via the site now exceed a billion dollars. Whatever your skills or interests, there is bound to be a service people will pay you to provide there.

Of course, you may already have noticed one potential drawback. Five dollars is only around £4.03 at current exchange rates. And in fact it’s worse than that, because Fiverr’s fees and charges have to be deducted, meaning that you will only receive about $4, or £3.22, for each $5 gig you complete.

Read on, though, because there are techniques you can use to boost your Fiverr income to something far more substantial. But first, you will need an account…

Getting Started on Fiverr

Joining Fiverr is straightforward (and free).

Navigate to the Fiverr homepage and at the top, click on ‘Join’. A sign-up box will then be displayed.

Fill in the fields for your email address, username, and password (your choice). Read and accept the terms of service, and complete the inevitable captcha form. Then click the Join button. You will see a page displayed with a message that says ‘Activation link was emailed to you’.

Check your email for a message from Fiverr with the subject line ‘Fiverr: Registration Confirmation’ and click the link inside the email message. You should then be taken to a page on Fiverr that says, ‘Account successfully activated. Hey, this is a great time to edit your Profile.’

Congratulations! You’ve completed the registration and sign-up process for Fiverr. Make a note of your user name, password, and the email address you used to sign up so that you can log in again in future.

One other thing you should do as soon as possible is to fill in all the fields in your profile, including a picture of yourself. It’s important to have a completed profile, so that potential clients can see the person they will be dealing with. In addition, your gigs will only be eligible for extra (free) promotion on Fiverr when your profile has all the blanks filled in.

Finally, you will need a Paypal account to receive your fees. If you don’t have one already, you can sign up here. As you will be running a business, you should get a business account rather than a personal one. Note that Fiverr operates primarily in US dollars, but with PayPal it’s very easy to change one currency in your account to another.

Listing Your First Gig

Once you’ve decided what service you are going to offer – spend some time browsing Fiverr for ideas if you’re not sure – you’ll want to list your first gig. Here are six tips for getting off to the best possible start…

Very important – create a high-quality digital image that’s relevant to the gig you’re selling. This will be different from your profile photo. Make the image colourful, vivid, and expressive. It should stand out and draw a potential customer’s eye.

Add keywords to the listing for your ad. This is important, too, as it increases the number of views your gigs will receive. The more views you receive, in general, the more sales you are likely to make.

Write a thorough, easy-to-understand description of your gig. If you’re unsure how to do this, search for other gigs that are generating a lot of ‘stars’ and positive comments.

State a realistic length of time it will take you to deliver the product. Get this wrong, and the negative comments will affect your ability to sell that gig in the future.

Provide clear instructions to the buyer. This will save you hours of answering unnecessary emails from customers. Tell them exactly what they must do, how they should do it, and what they can expect. If you still receive the same questions repeatedly, add another sentence or two to your instructions.

Consider creating a video to introduce your gigs.

The latter is becoming more and more common on Fiverr. For some types of gig nowadays, having a ‘gig video’ is virtually obligatory. In your video you can talk about (and preferably demonstrate) the service you are offering.

As well as adding interest to your listing, using a video will increase the exposure to your gig, not only on Fiverr, but in the search engines as well.

You can also use YouTube to promote your Fiverr videos. As Google owns YouTube, there’s a good chance your Fiverr video will be shown high in Google’s search results for your selected keyword/s.

If you don’t have a dedicated video camera, you can, of course, make perfectly serviceable videos nowadays using a mobile phone, smartphone, or even a webcam.

Another option is to use screencasting software, such as the free web-based Screenr. This will allow you to record a video up to five minutes long showing whatever is on your computer screen with your spoken commentary over it.

And, of course, there is no shortage of people on Fiverr offering to create a gig video for you!

Promoting Your Gig

Fiverr is one of the top 200 sites on the internet and attracts huge amount of traffic – so the very fact of listing your gig there will ensure plenty of people see it.

You should, however, make an effort to promote it yourself as well, especially when you’re just starting out and don’t have much of a track record.

Every Fiverr gig has its own unique web page URL, and you should share this as widely as possible. Put it in your email signature, and post it on Facebook, Twitter and any other social networks you belong to. If you use online forums, include the link in your signature text (most forums will permit this). If you’re a blogger, blog about it too.

As mentioned, it can also be a good idea to create a gig video and post it on YouTube. This is another site that generates huge amounts of traffic, and can provide another route for potential buyers (and search engines) to find you.

Techniques for Boosting Your Income

At first glance the earning potential of Fiverr looks limited. But with a little imagination, you can effectively boost your returns many times over. Here are three top techniques you can use…

Do the Work Once, Sell Multiple Times

This is a technique anyone can use, even if they are brand new to Fiverr. For example, you could write a short report or e-book and sell it through the site multiple times. This is slightly against the spirit of Fiverr, but I’ve seen plenty of people doing it. Here’s one current example…

‘I will list ten great under-appreciated horror movies by cult and old-school movie directors for you and write a brief synopsis for $5.’

I assume this individual has already written his report and simply sends it to anyone who pays the $5 for it.

One top tip here is to make it sound as if you are personalizing your offer for each recipient. As in the example above, refer to the reader as ‘you’ and explain exactly what you (and your report) are going to do for them. Essentially, by this method, you could sell the same report dozens of times, potentially making hundreds of pounds or more from a single short report.

Offer Multiples and Extras

This is really the key to making big money on Fiverr. ‘Multiples’ simply means that a client can buy the same gig from you multiple times (e.g. if you are offering logo design for $5, they could buy five different logo designs for $25).

Extras are additional features you offer on top of your basic gig. For example, someone offering to write a 250-word blog post for $5 might offer a 500 word article for $10, and so on.

As a newbie on the platform you will be quite limited in the multiples and extras you can offer. Currently you can offer just two gig extras ($5, $10 and $20) and five gig multiples

Once you have ten gigs on Fiverr completed with no complaints against you, you will be promoted to what the platform calls Level One. At this point you can add more multiples and extras to your gigs. The most you can charge for extras is $40 at Level One, and $50 at Level Two (for which you require 50 completed gigs).

You can read more about Levels on Fiverr, what is required to achieve them, and the benefits of reaching any particular level on this page of the Fiverr website.

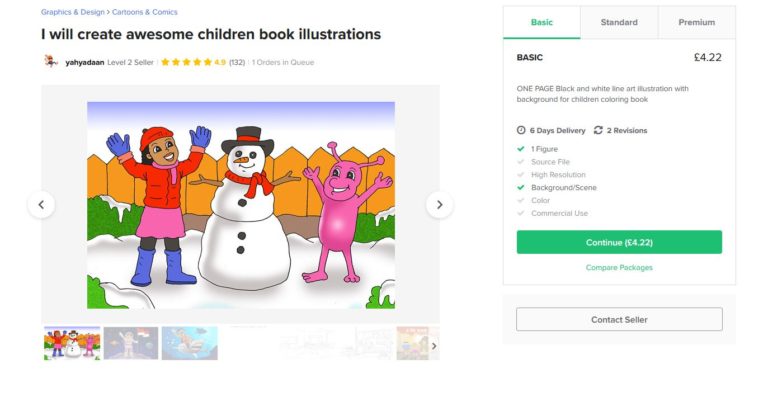

As an example, a Level Two children’s book illustrator by the name of Yahyadaan (see screen capture below) is currently offering to draw a picture in black and white for $5. Paying $15 gets you a colour illustration, and $30 gets you a full colour illustration with ‘high quality detail’ and commercial use allowed. You can also pay an extra $10 for rapid delivery (within a day). The latter is a very common extra, incidentally, and in effect triples your fee for a basic $5 job.

The ability to offer multiples and extras greatly boosts the money-making potential of Fiverr, so it’s well worth putting in a bit of extra effort with your first few gigs to ensure you get good feedback and are quickly promoted to the higher levels.

Ask for a Tip

Buyers on Fiverr generally realise they are getting a good-value service, and many are happy to pay a bit extra to recognize this. This applies especially with US clients, as tipping there is pretty much a way of life!

There is an etiquette to asking for a tip on Fiverr, and you shouldn’t just demand one. The preferred approach is to set up a separate ‘tip gig’. This is just like any other gig, except you don’t have to do anything in return.

Just include a link to your ‘tip gig’ when delivering your gigs and let clients decide whether to pay. If you have given good service, there is every chance they will. As an example, here is a link to a tip gig for a Fiverr member I worked with a few years ago, although I see that her account is on hold (maybe she has moved on to bigger and better things by now).

By using the techniques set out here, you should realistically be able to generate a substantial part-time or even full-time income on Fiverr, while doing something you enjoy from the comfort of home.

Although in this post I have focused on making money from Fiverr, of course it can also be a great way of getting assistance with a wide range of entrepreneurial and personal projects. I have hired other Fiverr members on various occasions for tasks ranging from designing a banner ad to removing malware from this blog after it was hacked. In general I have received excellent service for keen prices. And while on the subject, I highly recommend the WordPress specialist named Zerotech who came to my rescue in the aforementioned hacking attack and got my blog back to normal within 48 hours 🙂

Good luck, and if you have any comments or questions, as always, please do post therm below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting another survey site that offers the opportunity to generate a sideline income.

You may well have heard of YouGov already, as they often run opinion polls on political preferences and other current issues.

YouGov are always on the lookout for new people to join their panel and complete surveys via their website. Naturally, they provide financial incentives for doing this.

How Does It Work?

For each survey you complete on YouGov, you are allotted points. For a typical survey taking 10 to 15 minutes you will get 50 points. Of course, the longer the survey, the more points you will receive.

You can complete surveys on a computer, smartphone or tablet. You will be notified by email of new surveys you are eligible for, though it’s also worth logging on regularly to see the full range of surveys currently available.

Once you have accumulated 5000 points you can redeem them for a £50 fee. YouGov refer to this as a ‘cheque’, but the money is actually paid direct to your bank account.

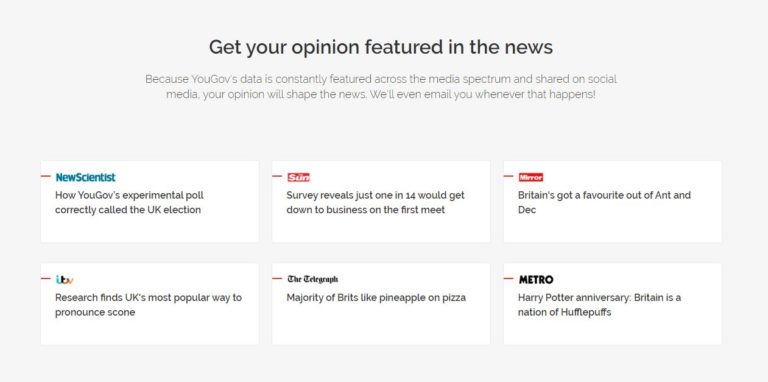

To get 5000 points you would need to complete 100 fifty-point surveys, so this is clearly not a get-rich-quick opportunity. Nonetheless, the surveys are generally interesting and not too demanding to complete. And you will also have the satisfaction of knowing that your responses will ultimately influence decision-makers in government and the private sector. You can see some example media coverage of YouGov surveys in the screen capture from the website below.

How Do You Join?

Joining the YouGov panel is very simple. Just click on this referral link (see below) and complete the short online application form. Acceptance is normally automatic, and you can start earning points immediately.

Disclosure: if you join YouGov via my link I will get 200 points credited to my account (worth £2). If you join YouGov you can also refer other people and earn extra points as well. It all helps get you closer to that next £50 payment!

As always, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

The ability to offer multiples and extras greatly boosts the money-making potential of Fiverr, so it’s well worth putting in a bit of extra effort with your first few gigs to ensure you get good feedback and are quickly promoted to the higher levels.

The ability to offer multiples and extras greatly boosts the money-making potential of Fiverr, so it’s well worth putting in a bit of extra effort with your first few gigs to ensure you get good feedback and are quickly promoted to the higher levels.