Today I have a sponsored guest post for you on behalf of Fife Autocentre. The post sets out four advantages to using a mobile tyre-fitting service for tyre replacements and repairs.

Taking good care of your tyres is crucial to maintaining your car’s longevity and performance while keeping you safe. The best way to do this is to engage mobile tyre-fitters to get your tyres repaired, fixed or fitted.

Cost-effective

Why waste time and money trying to get to a garage for tyre replacements and repairs? Mobile tyre-fitting provides an ideal, cost-effective solution. An expert fitter will attend at your preferred location and provide a professional service when conducting repairs and replacements. You will therefore avoid the expense (and risk) involved if you do the job incorrectly yourself. For mobile tyre-fitting, check with the experts at Fife Autocentre.

Increased safety

Why risk damaging your tyres even more when you can be served by a mobile tyre-fitting service at your home or workplace? Attempting to take your car to a garage on damaged tyres is extremely dangerous, as you may end up broken down in the middle of nowhere or even having an accident. A mobile tyre fitting service will immediately respond and act accordingly.

Supremely convenient

Why stress to get tyre problems fixed if you can be reached and attended to at your convenience? Mobile tyre fitters will serve you without disrupting your day’s activities. Just call for help, then carry on with your day as normal.

Instant emergency service

Getting stranded due to tyre problems is a driver’s worst nightmare. So reaching out to a mobile tyre-fitting service is the best solution. Simply contact them and they’ll send someone directly to your location to offer the most effective solution wherever you may be. By this means you can avoid unnecessary delays and be back on the road again in the least time possible.

Final Thoughts

Mobile tyre fitting is the modern way to approach your tyre problems as it is affordable, swift and effective.

I’d just like to add my own endorsement to the advice above. Early on in the first lockdown my car had a puncture and I made the mistake of driving to a tyre and exhaust fitting centre to have it repaired.

Even though I reinflated the tyre before departing, it quickly went flat again. By the time I got to the centre the tyre was flat as a pancake and the wheel had gone out of shape as a result. Instead of paying a small fee for a puncture repair, I therefore had to shell out for a new tyre. So I am very much on board with the advice to use a mobile tyre-fitting service in this situation!

As always, if you have any comments and/or questions about this post, please do leave them below.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

Nobody would pretend life insurance is an exciting subject, but in these uncertain times it’s something we all need to think about at least. So in this post I thought I’d set out the basics regarding life insurance and why you might need it.

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life insurance policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

Over 50s Life Insurance

This type of whole-of-life insurance may be of particular interest to Pounds and Sense readers (PAS is particularly targeted at over 50s).

It allows you to leave a guaranteed fixed lump sum to your loved ones when you’re no longer around. To apply, you need to be aged 50 to 80 (85 in some cases) and a UK resident. No medical is normally required, and your monthly premium (which can be as low as £7) won’t change for as long as you live. In most cases cover for accidental death applies immediately, but for death from other causes there may be a waiting period (typically a year). This type of insurance is not normally index-linked, so over time the value of the lump sum payable may be eroded by inflation.

Who Needs Life Insurance?

Life insurance is intended to protect your dependants from getting into financial difficulties if you die. So if you’re single with no dependants and/or on a very low income, it may not be necessary or appropriate for you.

But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death. Many people take out life insurance when they get married or start a family, or when taking on a major financial commitment such as a mortgage.

Most financial experts recommend you take out life insurance before you reach 35, as the sooner you get cover, the cheaper your premium.

What Doesn’t Life Insurance Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

As mentioned above – and other things being equal – the younger you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Get Life Cover Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It’s therefore important to establish what is the most appropriate choice for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Get Life Cover. They will put you in touch with an independent financial adviser in your local area, not some anonymous call centre. The adviser will take the time to establish your exact requirements and recommend a bespoke policy tailored to your (and your family’s) needs. They will be able to arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on. Being independent they will also be able to select from the whole of the market. They are not tied to one insurance company, ensuring you get the best possible value for money.

If you wish, Get Life Cover’s independent advisers can also assist you with other financial matters, including investments, pensions, mortgages, tax, and so on.

To get an initial personalized quote, click through to the Get Life Cover website and provide a few basic details to get a quick quote in 30 seconds, without obligation. You can then discuss this with a local adviser to ensure you get exactly the right type and level of cover for your needs.

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Get Life Cover. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

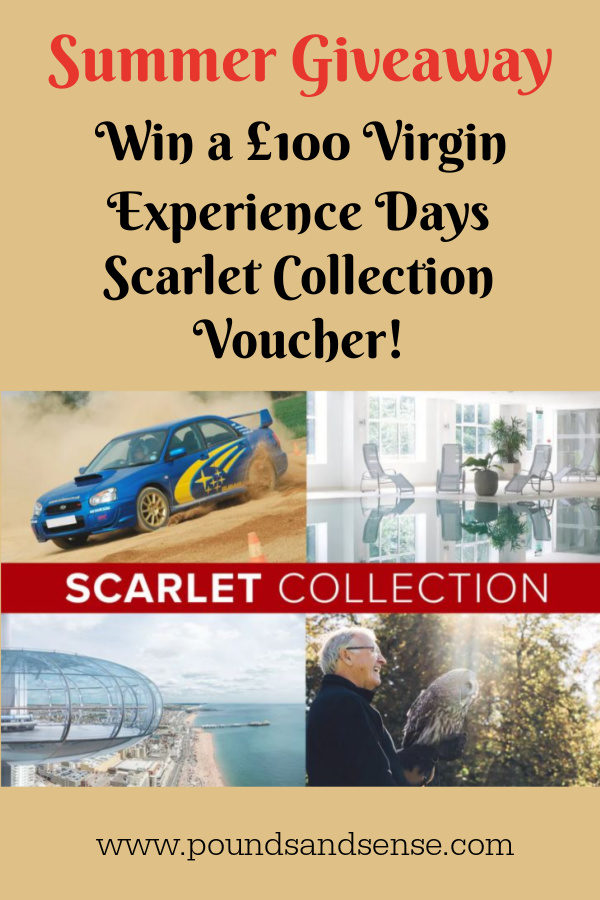

Summer is here, so it’s high time for another exciting giveaway on Pounds and Sense 🙂

I have joined forces with some of my fellow UK money bloggers to bring you the chance of winning a fantastic Virgin Experience Days Scarlet Collection voucher, worth £100. You can use this voucher on any of a huge range of experiences: from an introductory microlight flight to dinner for two at Coombe Abbey; a pamper day with cream tea for two at a Hallmark Hotel to a three-hour oriental cookery class at School of Wok.

After the last eighteen months we all need and deserve a treat, so here’s your chance to grab one for free!

This giveaway has been organized by my colleague Dan from The Financial Wilderness blog, so I should like to thank him very much for this. More details provided by Dan himself, along with instructions on how to enter, can be found below…

The Prize

The wonderful prize on offer today is a voucher allowing a choice of experience from the Virgin Experience Days Scarlet Collection.

This voucher worth £100 gives you the opportunity to choose a variety of exciting experiences, with something for just about everyone. To give you a flavour of the options on offer in the Scarlet Collection:

For the adventurous – A rally or Porsche driving thrill experience

For the foodies – A range of afternoon teas and dinner options

For the sporty – Have a round of golf at some great courses or learn archery

For the relaxed – A collection of overnight breaks around the country

You can view details of all the available experiences with the Virgin Scarlet Collection on the Virgin Experience Days website here.

The Bloggers Taking Part

This giveaway in run in conjunction with some of my fellow UK Money Bloggers – we run these events to help each other out, so please do visit at least some of the excellent blogs concerned 🙂

Enter to Win a Virgin Experience Days Scarlet Collection Voucher!

Use the Rafflecopter Widget below to make your entry. You’ll need to fill out your basic details and click ‘claim 1 entry’ to be in for the competition.

You also have the opportunity to claim bonus entries by performing an action relevant to the above websites, such as following an account on Twitter or visiting an article. You can do as many or as few of these as you like.

1. There is one top prize of a voucher for Virgin Experience Days “The Scarlet Collection.”

2. There are no runner up prizes

3. Open to UK residents aged 18 and over, excluding all bloggers involved with running the giveaway

4. Closing date for entries is midnight on 18.09.21

5. The same Rafflecopter widget appears on all the blogs involved, but you only need to enter on one blog

6. Entrants must log in to the Rafflecopter widget, and complete one or more of the tasks – each completed task earns one entry in the prize draw

7. Tweeting about the giveaway via the Rafflecopter widget will earn five bonus entries into the prize draw.

8. 1 winner will be chosen at random.

9. The winner will be informed by email within 7 days of the closing date and will need to respond within 28 days with their delivery address, or a replacement winner will be chosen.

10. The winners’ names will be published in the Rafflecopter widget (unless the winner objects to this).

11. The prizes will be dispatched within 14 days of the winner confirming their address.

Due to the pandemic many people are now working from home some or all of the time. And many others, who may have lost their jobs due to the crisis, are now running home-based businesses or considering setting one up.

I have been working from home for over 30 years now, so in this post I thought I’d set out the main pros and cons as I see them. I hope if you have recently started working from home, or expect to in future, you might find this helpful.

I’ll start with some of the advantages…

The Pros

Save money – If you work from home you will avoid having to pay travel costs and potentially other work-related expenses like takeaway coffees and meals.

Be safer – Working from home means there is less chance of catching (or passing on) Covid-19 or other infections. You also avoid having to venture out during the winter months on dangerous wet or icy roads and pavements.

Save time – You will also avoid wasting many potentially productive hours in your car or on public transport. Many people (e.g. with jobs in London and other major cities) spend two or more hours a day just commuting; added up over a year, the total amount of time ‘lost’ in this way can be quite staggering.

Feel more comfortable – In general you can wear whatever you like. You don’t even have to dress or shave if you don’t wish (though you will, of course, need to make an effort with your appearance when meeting other people in real life or on online platforms like Zoom). You can take tea, coffee and meal breaks as you like, whenever it happens to suit you. You can arrange your office furniture, lighting, temperature and so on exactly as you prefer. And unlike many offices and other workplaces at the moment, you won’t have to wear a mask all day!

Benefit from flexibility – Many aspects of family life can be easier to arrange if you work from home. For example, if you want to pop out at 3.30 to collect your youngest child from school, this should be a lot more feasible. To a degree you will be able to choose your own hours, working early in the morning or late at night if these options suit you best. You can be around in the day when the plumber or meter reader calls; you can put out the washing and bring it back in if it starts to rain; and you will not miss important deliveries because you are toiling away at a separate workplace.

Enjoy tax advantages – If you run a home-based business you may be able to claim a proportion of your household expenses (heating, lighting, mortgage/rent, etc.) against tax. Even if you are working for an employer, you may be able to claim working from home tax relief.

Improve home security – The fact that you are around in the day can help deter burglars (most burglaries in residential areas take place during the daytime). You will also be on the premises – and therefore able to take prompt action – in the event of fires, burst pipes and other such emergencies. Some insurance companies are starting to recognise this fact and offer lower premiums for homeworkers – though this must be set against the fact that work-related computers and other equipment may have to be insured separately for an additional premium.

If you run your own home business there are various additional advantages.

You will no longer have to endure the horrors of office politics or attend long, dull, pointless meetings (been there, got the tee-shirt). With your own business you can work as many or as few hours as you wish. If you want to work a fifteen-hour day, you can (though hopefully not every day!). Equally, however, you can work part-time if you prefer, perhaps to fit in with family responsibilities. You can also set your own pace, with no-one standing over you telling you to work harder or faster. For older people, or those with disabilities that slow them down, this can be a particular attraction.

As long as your business is bringing in enough money to meet your needs and those of your dependants, you can work as hard or as easily as you wish – you have complete control over your ‘terms and conditions’. But, of course, while you won’t have a boss looking over your shoulder, you will still have clients/customers who will expect a good quality product or service from you within a certain deadline.

The Cons

Although working from home has many attractions, it does possess a few potential drawbacks as well. Some of the main points to consider are set out below.

May disrupt family life – Working from home means you and your family’s domestic lives will inevitably be affected. Obviously you will need a space in the house to work that might otherwise be used by other family members. If running a business you may have to work during the evenings, public holidays and weekends, when most ‘normal’ people are at leisure. Clients may contact you by phone at any time, even outside normal working hours, so family members will need to become accustomed to receiving calls and be briefed on how to handle them. If you have other heavy phone users in the house you may need to get a separate line for business calls.

May be distractions – Friends and relatives who would never dream of interrupting you at a ‘proper’ job may think nothing of phoning up or arriving unannounced, not realising (or perhaps caring) that you are at work. Regular interruptions of this nature can seriously reduce your productivity. Even if you avoid this problem, working from home offers a huge range of potential distractions, from pets and family matters, through shopping and household chores, to gardening and watching television. You will need to be self-disciplined, or you can fritter away many working hours on non-productive (in business terms anyway) activities such as these.

May be lonely – Working from home can be lonely at times. This applies especially if you live on your own, when you may not speak to another person face-to-face (apart from perhaps the post office clerk) for days on end. Even if you do have a family – or at least a spouse/partner – you may find the isolation during the day difficult to bear. This applies especially if you have previously worked in a busy office or factory, or you have a naturally sociable temperament.

Can be hard to get away from work – If you work from home, you may find that work and domestic life become indivisible and it is very hard to ‘switch off’ and relax when the day’s work is done. People who have previously worked in a separate establishment often find the journey between home and workplace provides a valuable psychological dividing line. When your home is also your workplace this line is gone, and the distinction between work and leisure can therefore become blurred.

May need better security – As mentioned previously, in some ways working from home is helpful for home security. But if you have high-value, easily portable equipment such as computers, cameras, tools, and so on, this may make your home a more attractive target for burglars. You may therefore need to increase your security, perhaps fitting a burglar alarm, security lighting/cameras, window locks, and so on.

Finally, if you are setting up a home-based business, planning restrictions may apply. This is most likely to be a problem if your business is likely to cause noise or other irritation to your neighbours. If you live in rented accommodation, the landlord may object to your running a business from his property; and if you are buying your house with the aid of a loan or mortgage, the lenders may be unhappy. There may also be terms in the lease or deeds of your property prohibiting its use for business purposes. And there is a possibility that running a business from home may mean that you become liable for business rates as well as your normal council tax.

The best types of business for running from home are those that are small and office-based – or based predominantly on clients’ premises – rather than those requiring workshops and machinery or selling directly to the public. A wide range of home-based franchise opportunities are also available.

In Conclusion

As I said at the start, I have worked from home for over thirty years now, initially as a freelance writer and editor, more recently as a blogger.

I enjoy working from home and in general do recommend it. I do just think that there are two key secrets to doing it successfully in the long term.

First, you should have a part of your home as your designated workspace. Ideally this could be a separate study or office, but at least a quiet corner where you can set up your equipment and files and not have to pack everything away at the end of the day. Growing numbers of people are now using garden sheds or extensions for home working, and this can also be a good solution. But if that’s not an option, work pods can provide a space-saving refuge in which you can avoid noise and other distractions and focus on getting your work done.

I also think that if you’re working from home, it’s vital not to let yourself become isolated. I know that has been easier said than done during the pandemic, but it’s very important to keep up connections with friends, family and colleagues. Home working can be especially challenging if you like and are accustomed to having colleagues to talk to. You really do need to build some social interactions into every day if possible – ideally face to face, but at least via the phone and/or social media. Your mental health may depend on it!

If you have any other comments or questions, as always, please do post them below.

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

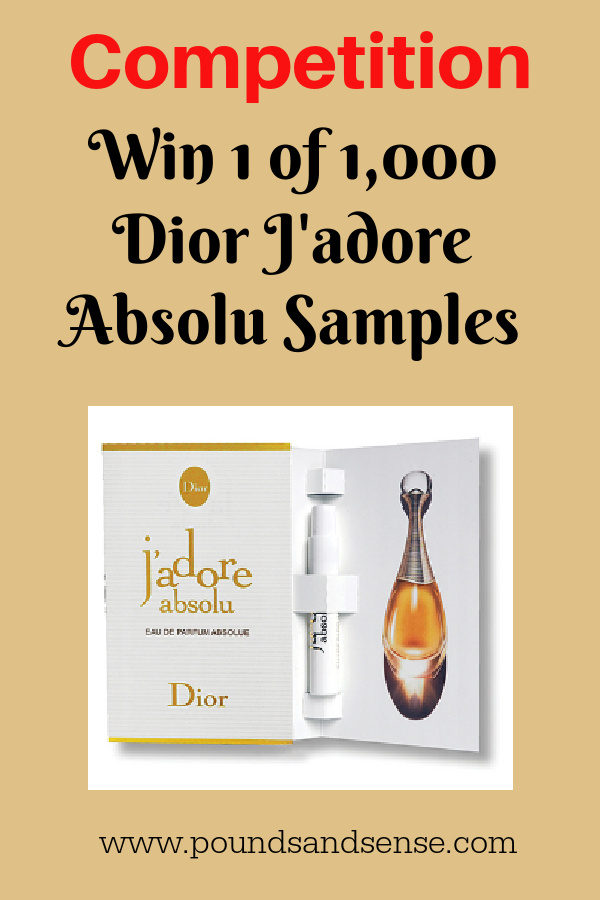

Just a quickie today to share details of a free-to-enter competition from my friends at All Free Stuff. You can win 1 of 1000 Dior J’adore Absolu samples (see cover image). This is a great women’s floral fragrance by Dior.

To enter, all you have to do is sign up to the Free Stuff email newsletter. This daily email contains all the latest freebies, free samples, competitions, and more (of course, you can unsubscribe any time). Entrants must be over 18 and live in the UK. For the full rules and to enter the competition, please click here.

Good luck, and I hope you win one of the 1000 prizes!

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another Coronavirus Crisis Update. Regular readers will know I’ve been posting these since the first lockdown started in March 2020 (you can read my July 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

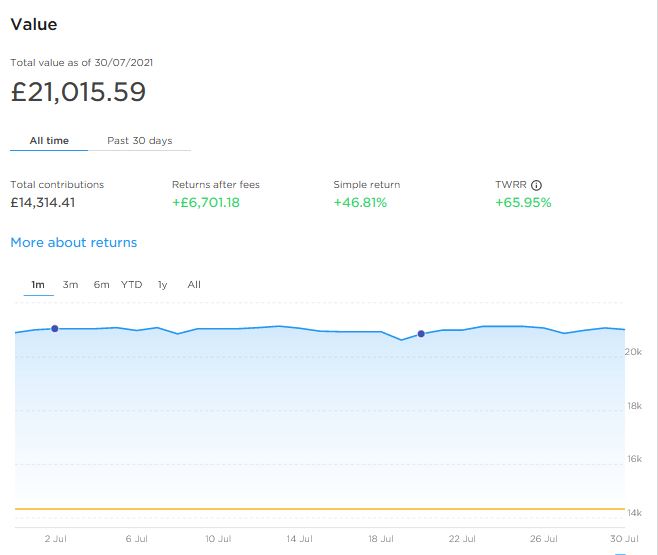

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, the value of my main portfolio remained pretty steady in July. It is currently valued at £21,015. Last month it stood at £21,045, so that is a slight drop of £30.

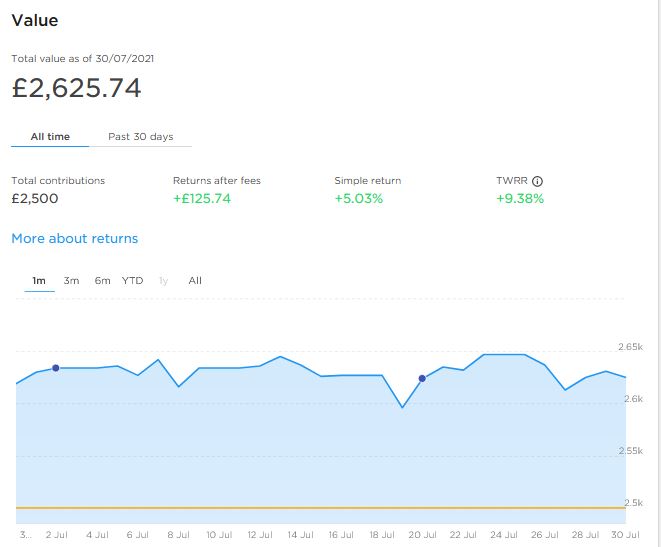

Apart from my main portfolio, I also have a second pot using Nutmeg’s new Smart Alpha option. This pot is now worth £2,625, compared with £2,635 last month, so a small decrease again. Here is a screen capture showing performance in July 2021.

Although it’s a little disappointing both portfolios are down slightly, over the last six months (and longer) both are still well up overall, so I’m certainly not going to lose any sleep over this. This is a long-term investment and some ups and downs are to be expected. In 2021 the overall trend has been mainly upwards, so I hope and expect this to be resumed soon.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering.

If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually amazed by the difference the risk level you choose makes.

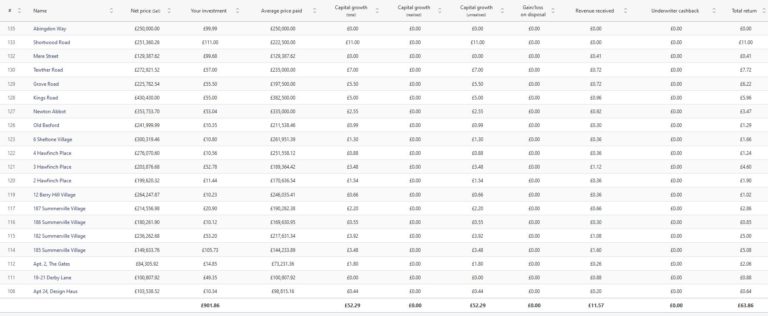

.As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Touch wood, everything has been going well, so in June I added another £500, bringing my total investment on the platform up to £1,000.

Since I opened my account, my portfolio has generated £11.57 in revenue from rental and £52.29 in capital growth, for a total return of £63.86. Here is my current statement:

As I said last time, to a degree Assetz Exchange has been a victim of its own success. They have had a big influx of new members, meaning all available investments were quickly snapped up. At the same time, some of the new projects that were due to launch were delayed. As a result I still haven’t invested all the money in my holding account. One new project did come on stream last week, so I put £100 into that.

My colleagues at Assetz Exchange assure me that more new projects are coming very soon. They are also limiting how much members can invest in the first few weeks of any new launch, so that everyone has a fair chance to purchase shares. And as time goes on more members may opt to offer their shares for sale on the exchange, opening up additional buying opportunities.

I am investing relatively modest amounts in new projects as they come onto the platform, so I don’t therefore put more than around £100 into any one project. As you can see, I already have a well-diversified portfolio comprising 20 different projects. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

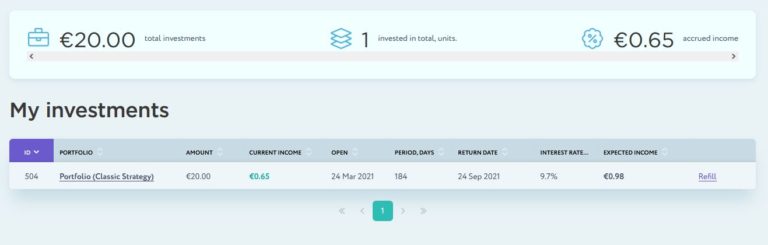

I haven’t mentioned my trial investment on European loan crowdfunding platform Nibble for a while, so thought I should remedy that this month. This has been proceeding without any issues and my initial test investment of 20 euros has accrued income of 0.65 euros, corresponding to an annual interest rate of 9.7 percent (see screen capture below).

I get weekly updates from Nibble confirming how much interest has been added to my portfolio. Based on my experiences to date I am considering investing a more substantial sum with them soon. My full review of Nibble can be found here.

Finally, in July 2021 two more PAS readers signed up with the low-key sideline-earning opportunity mentioned in previous updates. They will have received their initial £100 reward payments about now. I still have a few more invitations available if anyone else would like to take advantage.

This opportunity is based on matched betting, a sideline I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). It doesn’t require any financial outlay and is risk-free and entirely hands-off (once you have set up your account). No knowledge of betting is required and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company.

The company has changed its terms somewhat for new members. You now get a larger £!00 initial reward payment once your account is up and running, and then £25 every month you remain a member. I think this is a good move personally, as setting up the account does involve a little work on your part (though it’s certainly not rocket science). So the £100 in effect compensates you for your time, and once it’s done you continue to get £25 a month for no effort at all. The company is constantly developing its offering, partly in response to feedback from PAS readers. They recently launched a new mobile-friendly website to make it even easier for new members to sign up (once you’re up and running you shouldn’t need to use the website at all). They also recently incorporated an Open Banking app so that members don’t have to provide their online banking info to the company, as some people were concerned about this.

Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more information (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page. And yes, I will receive a reward for introducing you, but this will not affect the service or the rewards you receive.

Finally, in the interests of full transparency, I should say that if you do matched betting yourself, you may be able to make more money than what is being offered by the company. However, you will have to research the techniques in detail, place all bets yourself, and probably subscribe to a matched betting advisory service such as Profit Accumulator [affiliate link]. This opportunity is really for those who want an easy way to make some extra money without the hassle (or expense) of learning/applying matched-betting methods themselves.

Personal

The big news in July – in England at any rate – was that so-called Freedom Day took place as promised on 19th July 2021. Most of the legal restrictions on our lives, including mandatory masks and social distancing, were lifted from that date.

Since then – to the surprise of many experts and pundits (though not me) – new case numbers have been falling steadily week on week. Hospitalizations and deaths were slower to fall, but are now starting to follow the same path.

It is of course far too soon to say that the pandemic is over – and Covid is, in any event, likely to remain with us in some form for the foreseeable future. But it is all very encouraging, especially in the face of predictions from doom-mongers such as Professor Neil Ferguson that daily case numbers could reach 100,000 or even 200,000 as a result of restrictions easing.

In my view it is now high time we got back to something close to normal life and learned to live with the virus. But while out and about I notice that people generally are still being ultra-cautious. That is particularly the case in shops and supermarkets, where I should say that four out of five people are still wearing masks (though the numbers without are slowly increasing). On trains I would say it is about two in three, though on a couple of occasions when I travelled in the evening recently (after 7 pm) mask-wearers were in a minority.

I don’t use buses so can’t comment about them. At my local gym and swimming pool, however, almost nobody is wearing a mask now. Assuming that the numbers keep going in the right direction, I hope that more people will find the confidence to ditch the masks. It is wonderful to be able to see smiles and happy faces again after all this time!

In July I took a rail trip to Swindon to visit my old friend Jeff, who at the start of this year moved to Wiltshire. Unfortunately we chose what was probably the hottest day of the year. The whole round trip involved seven trains from three different train companies. So I can report that by far the best company for aircon, wifi, drinks/snacks service, and general all-round comfort, was Great Western Trains. Second were Cross Country, and last were West Midlands Railway. I travelled on three WMR trains in total and I don’t believe any of them had working aircon (one seemed to have the heating turned on despite the fact that the temperature outside was over 30). WMR had also by far the worst wifi, something I’ve experienced on many occasions before. I think West Midlands Mayor Andy Street should be turning his attention to improving this service rather than indulging in virtue-signalling gestures like offering passengers free masks. That aside, I did of course enjoy seeing Jeff again and also visiting Swindon for the first time. I would happily go back there, but hopefully on a cooler day!

As I said last time, I recently subscribed to Britbox and have been making good use of this. I really enjoyed watching all three series of the original House of Cards trilogy featuring Ian Richardson. I remembered the original series the best, but thought the second series (To Play the King) was equally good. I didn’t like the last series (The Final Cut) quite as much. It was never going to be quite the same without Michael Kitchen or Colin Jeavons, and I thought the ending was a bit of a let-down. But if you haven’t seen them before, I highly recommend watching all three.

Last week Britbox added Dennis Potter’s Lipstick on Your Collar (see image below) to their platform. I am very much enjoying watching this again almost 30 years since it first aired. I am a huge fan of Dennis Potter’s work and think he is probably our greatest-ever TV writer. His masterpiece was undoubtedly The Singing Detective, but Lipstick on Your Collar runs it pretty close. As with The Singing Detective, the series intersperses the action with lip-synched musical numbers, in this case classic 1950s rock ‘n’ roll. It has drama, comedy, great characters and some amazing music. What more could you possibly want?!

As I mentioned last time, now that Freedom Day has happened, this will be my last Coronavirus Crisis Update. I plan to continue with my monthly investment updates, and will also do more personal/general ones as and when the occasion arises.

I do hope you have enjoyed these monthly updates and found them of value. I have enjoyed writing them, and find it interesting looking back over them now as a sort of diary of the pandemic. I have listed them all below for convenience.