What Are the Benefits of Opening a Junior ISA for Your Child?

Updated 21 May 2024

Today I’m looking at a savings product that will be relevant mainly to the parents among you

A Junior ISA (sometimes abbreviated to JISA) is a savings product aimed at under-18s (and more specifically at their parents/guardians). These accounts allow money to be stashed away tax-free for a child until their 18th birthday. After this the money becomes the child’s to do with as they wish. The JISA account turns into an ordinary ISA at this time, thus retaining its tax-free status.

What Types of JISA are There?

There are two types of JISA: the Cash JISA and the Stocks and Shares JISA.

A Cash JISA is basically just a tax-free savings account. Interest is normally paid annually. According to the MoneySavingExpert website, the best-paying Cash JISA provider at the time of writing is Coventry Building Society, who are paying 4.95%. However, this is only available if you open an account in a branch or by post. If you want to open an account online, the best paying Cash JISA currently comes from Tesco Bank or NS&I, both paying 4%.

With a Stocks and Shares JISA, as the name indicates, the money is invested in the stock market. This offers the potential for greater returns, but with a higher degree of risk in the short term especially. I will say more about Stocks and Shares JISAs below.

As with adult ISAs, there is an annual limit to how much you can put into a Junior ISA. In the current (2024/25) tax year this is £9,000. You can put all of this into a Cash JISA or a Stocks and Shares JISA, or divide it between the two. You can switch providers as often as you like, but can only hold one of each type of JISA at any time.

Only a child’s parent or guardian can open a Junior ISA for them, but others including grandparents, friends, other relatives and the child him/herself can contribute. But it is important to be aware that (barring exceptional circumstances) all the money and interest in the account will be locked away until the child’s 18th birthday.

Which JISA is Best?

You won’t be surprised to hear that there is no simple answer to this.

If you want to avoid any risk of losing money, a Cash JISA is the way to go. Under the Financial Services Compensation Scheme (FSCS) the money will be completely safe so long as it’s invested with a UK-regulated provider and you have no more than £85,000 with that institution. Every year a known amount of interest will be added. The only risk you are taking is that the money won’t grow at the same rate as inflation.

On the other hand, if you are investing for at least a five-year period, there is certainly a case for putting at least some money into a Stocks and Shares JISA – and if it will be for ten years or more, the case becomes even more compelling. Over a five-year period stocks have outperformed cash in the great majority of such periods, and in almost all periods of ten years and over.

So if you are opening a JISA for a young child or infant, where the money may be invested for up to 18 years before it can be accessed, a Stocks and Shares ISA is very likely (though not guaranteed) to produce better returns than a Cash JISA. Of course, there is nothing to stop you hedging your bets and putting some money into one of each type.

What About Child Trust Funds?

Any child under the age of 18 born before January 2011 would have had a Child Trust Fund (CTF) opened for them by the government.

The government gave every child born between 1 September 2002 and 2 January 2011 a £250 voucher (£500 in the case of some low-income households). Parents could top up their child’s CTF themselves if they wished. The scheme ended in 2011 when CTFs were replaced by Junior ISAs. Unfortunately the government does not make a contribution towards these!

As with Junior ISAs, the money in a CTF could be placed in a Cash CTF or one where the money was invested in stocks and shares. Although new CTFs are no longer issued, there are many young people who still have one and will be able to access it on their 18th birthday. The first CTFs matured in September 2020, when the oldest account-holders turned 18. The last will mature in 2029. On maturity, a CTF can either be cashed in or transferred into an adult ISA.

Unfortunately the interest rates currently paid on Cash CTFs are generally very low indeed. So if your child has one, there may be a case for transferring it to a better-paying Junior ISA. Most JISA providers allow transfers from CTFs (or other JISAs), and it is certainly worth looking into this if your child has a low-interest-paying Cash CTF.

The Nutmeg Junior ISA

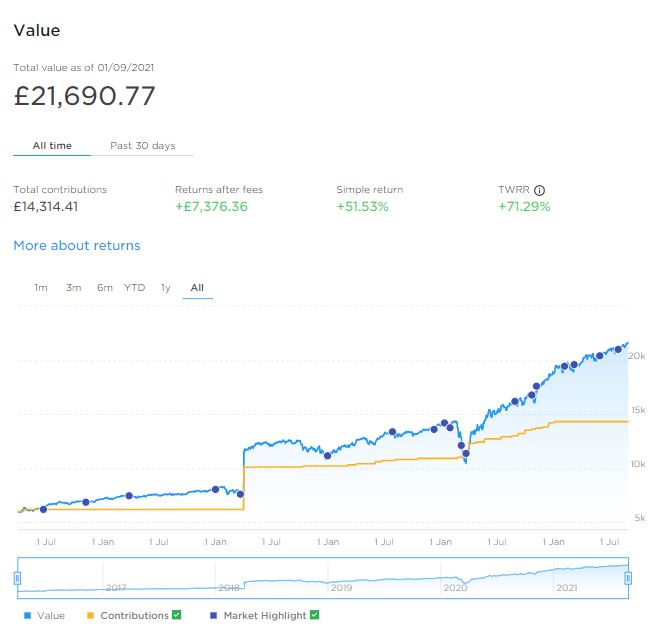

Regular readers of Pounds and Sense will know that I am a fan of of the Nutmeg investment platform and have a fairly large amount in an account with them. My money is invested in the form of a Stocks and Shares ISA. You can read more about this if you wish in my Nutmeg review or one of my regular investment updates such as this one.

Nutmeg do not offer a Cash JISA but they do offer a Stocks and Shares JISA. So if you are thinking of opening one of these for your child (maybe in addition to a Cash JISA) in my view they are well worth checking out.

With the Nutmeg Stocks and Shares JISA you have the same range of investment options as their adult ISA. These are discussed in detail in my Nutmeg review, but in brief they include Fully Managed, Smart Alpha, Socially Responsible and Fixed Allocation. My own investments are in the Fully Managed and Smart Alpha categories, and I am very happy with how both have been performing. But you should, of course, check the terms and conditions (and charges) carefully when deciding which is right for you.

Note that, unlike an adult ISA, in a Nutmeg JISA you cannot have different ‘pots’ within the same JISA wrapper. So you will need to pick your preferred option from one of the four mentioned, though you can change this any time later if you wish. You can also set a risk level between 1 and 10 and again you can change this at any time. You can read my recent blog post about Nutmeg risk levels here. My general advice, though, is that if you’re investing over a period of at least five years, it may pay not to be too cautious. In addition, if you choose to invest in a Nutmeg Junior ISA via my refer-a-friend link, you can get six months free of any charges.

- Of course, Nutmeg are not the only providers of Junior ISAs. Some other possible options include Hargreaves Lansdown and BestInvest.

Closing Thoughts

If you are a parent or guardian, opening a Junior ISA is one of the best gifts you can give your child (or children).

The money will grow tax-free and can’t be touched until they are 18, when they can withdraw it or keep it as an ISA. It may provide a much-needed lump sum at a time when they are setting out in the world and really appreciate a financial leg-up. A JISA will also give them an early introduction to saving and investing, and form a valuable part of their financial education.

The main selling point of JISAs is, of course, their tax-free status. Admittedly this is not as big a deal with Cash JISAs as it used to be, as nowadays almost everyone has a tax-free Personal Savings Allowance of up to £1,000 and other tax-free allowances as well. As a result, interest on savings is usually paid without any deductions. So there may be no immediate tax advantage to investing in a Cash JISA if a non-JISA savings account pays better interest.

In the case of a Stocks and Shares JISA the tax-free status may be more significant, as it also gives exemption from dividend tax and capital gains tax (CGT) both of which have had their tax-free allowances slashed by the government.

Either way, though, money saved in a JISA will carry on growing tax-free forever (until it’s withdrawn) – so even if there is no immediate tax advantage, there may well be in years to come. This applies to an even greater extent if the young person stays invested on reaching maturity rather than immediately withdrawing all their money.

According to the This is Money website more parents open Cash JISAs than Stocks and Shares JISAs. As a money blogger, however, I would definitely think about opening a Stocks and Shares ISA for at least part of your child’s JISA allowance. That applies especially if it is more than ten years till their 18th birthday. As mentioned above, over almost any given ten-year period, stocks and shares have outperformed cash. And the longer timescale allows the inevitable ups and downs in the stock markets to even out. If you put all the money into a Cash JISA, by contrast, it is quite likely that the value of your child’s account will not keep up with inflation.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Everyone’s circumstances are different and what is right for one person may not be appropriate for another. It is essential to do your own ‘due diligence’ before investing and seek help from a qualified financial services professional if in any doubt how best to proceed. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make a purchase (or perform some other defined action) I may receive a fee for introducing you. This will not affect in any way the product or service you receive.