How to Save Money by Saving Energy

As I’m sure you know, energy bills in the UK (and worldwide) are rising rapidly at the moment. Add this to tax hikes and surging inflation, and many of us will undoubtedly be feeling the pinch in the months (and years) ahead.

The government has announced various measures to try to mitigate the impact of energy price rises. These include £150 council tax rebates for those in Bands A to D and a (somewhat controversial) £200 rebate on energy bills, repayable at £40 a year over five years. These measures may help a bit, but they are unlikely to cover all the increased costs on their own.

So today I am looking at how you may be able to cut your bills by reducing the amount of gas and electricity you use. I am indebted to my friends at renewable energy specialists Ecoflow for their infographic (below) and research, which I shall be quoting from in this article.

Infographic

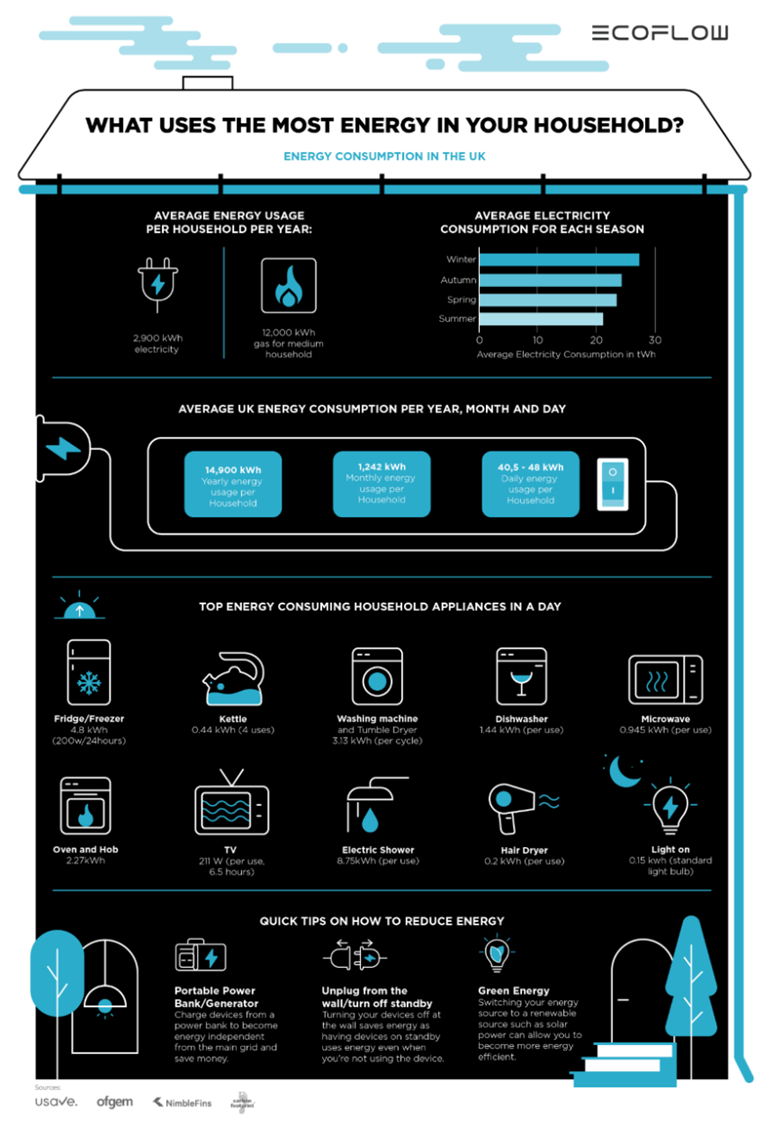

The Ecoflow infographic below shows a range of data about household energy consumption, including how much electricity we typically use in a year and which appliances use the most.

The graphic shows that an average UK household consumes 14,900 kWh of energy (gas and electricity) per year. That represents a daily energy consumption of 40.5 – 48 kWh per household.

The graphic also shows the amount of power used by different appliances in the home. Not surprisingly, the ones using most energy are cookers (19% of our total energy consumption) and so-called wet appliances (21%). Wet appliances include any that use water – washing machines, dishwashers, electric showers, and so on.

Covid has of course led to a huge increase in working from home – a trend which looks set to continue even as we move out of the pandemic. This has inevitably resulted in an increase in household energy consumption. Ecoflow say that the UK’s electricity consumption saw a 10% increase in 2021, reversing the trend in 2020 during which consumption fell by 14% year on year. The sharp increase in 2021 came largely from a return to relative normality following the restrictions and lockdowns of 2020.

When Is Most Energy Used?

EcoFlow have produced a breakdown of how our daily habits affect our energy consumption, which appliances are the most energy-hungry, and how we can change our habits to reduce our energy consumption. I have set out the main findings below, along with some ‘top tips’ for reducing energy consumption in the part of the day concerned.

Morning

A survey into Britain’s most popular breakfast choices found that 4/5 of Brits’ favourite breakfast foods are cooked. Despite changing lifestyles and eating habits, a cooked breakfast is clearly still a very popular choice. But how much electricity does it consume? Cooking appliances such as hobs (0.71 kWh per use), ovens (1.56 kWh per use) and microwaves (0.945 kWh per use) account for 19% of average electricity use.

Top Tip – As microwaves are more energy efficient than ovens, try batch cooking at the beginning of the week and reheating leftovers, rather than using the oven for every meal.

Afternoon

Working from home obviously increases electricity consumption, as devices such as laptops (0.4 kWh for 8-hour days), monitors and webcams become essential aspects of our home office. But WFH also allows us to carry out daily chores such as vacuuming and using the dishwasher (3.13 kWh per cycle) throughout the day. As mentioned above, wet appliances account for around 21% of our total electricity use.

Top Tip – Simple things to look out for to reduce electricity consumption include switching your washing machine to ‘eco’ mode and ensuring you only run it when it’s full. This will not only save energy, it will save water as well (and money if you are on a water meter).

Evening

Ecoflow’s research found that electricity consumption increased by 21% during the winter of 2020 compared to the summer. As the days become shorter during the winter months, our electricity consumption goes up and use of lighting increases significantly. Lighting accounts for 14% of the overall electricity usage in a home – per bulb this is 0.84 kWh.

Top Tip – Turning off lights and/or switching to energy-saving LED bulbs is an essential part of moving towards a more energy-efficient way of living.

More Tips for Saving Energy

Here are a few more tips for reducing your energy consumption and cutting bills, starting with one from the infographic.

- Unplug devices from the wall and turn off standby. Leaving devices such as TVs on standby uses extra electricity. Though only a relatively small amount, if devices are left on 24/7 the cost adds up.

- With rising energy prices, switching to renewables such as solar panels becomes ever more attractive. Although the government has reduced financial incentives such as feed-in tariffs, the savings alone from generating your own energy are increasingly compelling.

- Insulating your home to keep warmth in during the winter months can reduce your heating bills. Even simple, inexpensive things like putting draft-excluders at the bottom of doors can make a significant difference over the course of a year.

- If you have an old, inefficient gas boiler, consider replacing it with a more modern one. The Energy Saving Trust estimates that an average household could save £195 by switching from an old, G-rated boiler to a new, A-rated condensing boiler with a programmer, room thermostat and thermostatic radiator valves. If you live in a detached house, you could save up to £300 a year. Obviously installing a new boiler isn’t cheap, but if you can find the money it should be a very good investment.

- If you have an old, inefficient boiler and receive pension credit or tax credits, you may be eligible for a FREE boiler replacement under the government’s ECO scheme. For more information about this, check out the in-depth article above from my colleagues at Over 60s Discounts.

- Keep tumble dryer usage to a minimum as they use large amounts of electricity. According to the Energy Saving Trust, an average tumble dryer uses roughly 4.5 kWh of electricity per cycle. Dry clothes outside if possible or over an airer.

- Wash clothes at 30 degrees (or cooler) wherever possible. Modern washing machines will still do a good job at these lower temperatures, and again the energy savings add up.

Closing Thoughts

Obviously I hope rising energy costs will not cause you serious hardship. No-one should ever be forced to choose between ‘heating and eating’. But I hope the information and tips in this article will at least help you reduce your energy consumption in the months ahead and hence lower your bills.

Remember also that if you’re on a low income, there are government schemes such as the Warm Home Discount to help you.

In addition, you may be able to save money by switching energy supplier. Right now there aren’t many good deals around, but if you switch to EDF via my (affiliate) link you can get £50 credited towards your energy account, which should certainly help a little 🙂

Thank you again to my friends at Ecoflow for their infographic and research data. As their R&D Director, Thomas Chan, says: ‘We have to remain mindful of our energy usage and the direct effects it has on the environment and climate change. By becoming energy independent and using renewable sources of energy such as solar, people can avoid high electricity bills during the winter months.’

As always, if you have any comments or questions about this post, please do leave them below.