With the current cost-of-living crisis, we all need to save money any way we can. So today I’m looking at some ways you may be able to reduce your water bills.

It should be said that water pricing varies across the UK. In England and Wales, unless you have a water meter, the price you pay will depend on the rateable value of your home. In Scotland – again unless you have a meter – you will pay a standard water charge with your council tax. Domestic customers in Northern Ireland are fortunate in that they are not generally required to pay a water bill at all.

Should You Get a Water Meter?

The average water bill for unmetered customers is currently around £400 a year.

If you’re on a low income, that can represent a significant portion of your money. And unlike gas and electricity, you can’t just shop around for a better deal with a different supplier. You may, though, be able to make substantial savings by having a water meter installed.

With a meter, you are of course charged according to the amount of water you use. A rule of thumb here is that if your home has more bedrooms than occupants or the same number, it is worth looking into getting a meter installed.

Of course, people vary considerably in how much water they require. So you can use this free calculator from the Consumer Council for Water to check whether you are likely to save money with a meter. It asks a series of questions about your home and your water usage and shows the estimated cost if you had a meter. You can then compare this with what you ‘re paying currently.

The good news is that in England and Wales (though not Scotland) water companies will normally install a water meter free of charge if requested. Even better, they will usually let you switch back to unmetered within 12 or even 24 months if you find you are paying more than you were before. You should check with your water company to find out their policy about this.

If your water company can’t fit a meter for some reason, you can ask for an ‘assessed charge bill’. This is calculated according to the size of your home and how many people live there. If it comes to more than you’re currently paying you can stick with your present billing method, so there is nothing to lose by asking for this.

Ways to Save Money With A Water Meter

Once you have a meter installed, there are many ways you can reduce your water usage and save yourself money (and benefit the environment too). Here are just a few…

Only ever use the washing machine with a full load.

Have showers rather than baths and keep them short.

Fit a water-efficient ‘low-flow’ showerhead.

Do all the washing-up in one go.

Use a dishwasher, or at least a washing-up bowl.

Turn off the tap while brushing your teeth.

Don’t use the toilet as a waste bin for paper tissues, etc.

Fix dripping taps and other leaks as soon as possible.

Go easy on watering the garden. If possible, collect rain in a water butt and use this.

Finally, most water companies offer gadgets to save water, which they will send you for free. Phone them or check on their website to find out what’s available.

Other Ways to Reduce Your Water Bills

If you’re on a low income, all the water companies have schemes designed to help you. These vary a lot and you will need to check with the company supplying you to find out what they offer.

Severn Trent, for example, has what it calls The Big Difference Scheme. If your household income is below £16,480, you could get up to 90 percent off your bills. You can read more about this here.

I hope this advice will help you reduce your water bills. If you have any additional suggestions – or other comments or questions about this post – please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at Bestinvest, an investment platform I have used myself for many years. My SIPP (Self Invested Personal Pension) is held with them.

Bestinvest was founded in 1986, so it is one of the UK’s longest established platforms. In 2014 they merged with Tilney, and the company rebranded as Tilney Group in 2017.

Bestinvest has around £2.7 billion in assets under management (AUM). This puts it in the mid-size category, some way behind the UK’s three biggest investment platforms, Hargreaves Lansdown, AJ Bell YouInvest and Interactive Investor.

Of course, size isn’t everything. As a well-established platform with competitive fees and a reputation for high-quality customer service, Bestinvest has plenty to offer discerning investors.

What Does Bestinvest Offer?

Bestinvest offers four main types of account. These are:

General Investment Accounts can be used for investments outside your tax-free allowance (e.g. the £20,000 annual ISA allowance). You can also use this account for day-to-day share trading. But be aware that any income or capital gains generated within this account (above your personal allowance) may be liable for income tax, dividend tax and/or capital gains tax.

Within their accounts, investors can select from a wide range of funds and individual company shares. You can choose from over 2,500 funds, UK shares, ETFs, and investment trusts. There is no access to US shares, though. So if that is something you might require, another platform such as Hargreaves Lansdown or eToro might be a better choice for you.

As someone asked me this, I should maybe clarify that while you can’t buy US shares directly on Bestinvest, you can of course buy funds investing in the US market if you wish. Personally I have some of my SIPP money invested in the HSBC American Index C fund.

What Are The Charges?

Bestinvest recently revamped and in many cases reduced their charges. They are now highly competitive in many areas.

For most accounts there is a tiered platform fee. This begins at 0.4% for the first £250,000, 0.2% for the next £250,000, 0.1% for £500,000 to £1,000,000, and zero over that.

Bestinvest do, however, offer a range of ready-made portfolios, where the fee for the first £250,000 is just 0.2%. This is half the standard rate (and makes them extremely competitive with other platforms). For more information about fees and charges, see the Bestinvest website.

Buying and selling funds on Bestinvest is free (though you will of course still have to pay fund charges). Bestinvest recently slashed their share dealing charge to £4.95 per deal.

Information and Advice

Bestinvest is aimed at people who are comfortable choosing their own investments. They do, though, offer plenty of information and advice for investors, much of it for free.

As mentioned above, they have a range of ready-made portfolios you can choose from. Bestinvest charge half their normal fee for these (0.2% rather than 0.4% for the first £250,000). They comprise a carefully selected collection of investments, so you don’t have to spend time choosing yourself. They have two fund ranges, Expert and Smart. Each has different investment portfolios, from defensive to maximum growth and everything in between. If your focus is sustainability or income, they have funds for those as well.

But if you prefer to choose your own investments, Bestinvest have tools and articles to assist with this too. Their investment search tool lets you search according to a wide range of criteria. You can then access in-depth information on any potential investments that look appealing.

Advice from registered financial advisers is also available via the Bestinvest platform. If you plan to invest over £20,000 in ready-made portfolios, personalized advice about choosing the best option/s for you is available for free. You can also get free ‘coaching’ calls, and more in-depth personal financial advice, for which there is a charge. Again, see the Bestinvest website for more information.

What Are the Pros and Cons of Bestinvest?

PROS

Well-established platform with a large client base

Range of accounts to meet most needs

Well-designed, user-friendly website

No dealing fees when buying or selling funds

Reasonable fees (£4.95) when buying shares

Low minimum investment (just £50 in most cases)

Highly rated UK-based customer service

Information, advice and ready-made portfolios available

Ready-made portfolios are exceptionally good value

User-friendly investment research tools

Bestinvest pay up to £500 towards any exit fees your current providers charge when you transfer your investments to them

CONS

No access to US shares

No mobile app currently

Some users have had issues with the website (though see below)

What Do Users Think?

On the independent TrustPilot website, Bestinvest has an average rating of 3.8 (‘Great’) at the time of writing, with 38% of users awarding them a maximum five stars rating. That is roughly on a par with other leading UK investment platforms.

Positive comments typically emphasize the high-quality customer service and range of advice and information available. Some of the negative comments concern issues with the website, though it is worth noting that this has just been revamped.

Bestinvest has also received various industry awards, including Best Customer Service at the 2021 Shares Awards run by Shares Magazine, and Best ISA Provider in the 2020 COLWMA Awards. You can see a full list of their recent industry awards here.

Closing Thoughts

If you are planning to start investing (or switch from your current platform) Bestinvest is certainly worthy of your consideration. It is a popular, well-established platform with a good range of accounts and services. Their charges are competitive, and (as I can testify from my many years as a client) their UK-based customer service is first rate.

The Bestinvest SIPP is widely considered their flagship product, and as I have one of these myself (now in drawdown) I wouldn’t argue with that. There are no set-up fees, no fund-dealing charges and they pay up to £500 towards your exit fees if transferring from another provider. The Bestinvest SIPP has recently become even more competitive with the scrapping of the £100 (plus VAT) administration fee and certain other charges. Note that there is still a minimum charge of £120 per annum, though.

Bestinvest’s ready-made portfolios are an attractive (and great value) option for novice investors and those who don’t have time to research all their investments themselves. But equally, if you are happy to pick your own funds and shares, Bestinvest has all the information and tools you will need.

While Bestinvest’s share-trading fees are relatively low, if you’re planning to buy and sell individual shares regularly, a low-cost dealing service such as eToro might be better for you. They offer commission-free trading on shares and charge no monthly account fee. That makes them ideal for short-term traders and investors looking to build a portfolio of shares cheaply. Of course, this is a riskier approach to investing, and not recommended for those new to the field.

As ever, if you have any comments or questions about this blog post or Bestinvest in particular, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

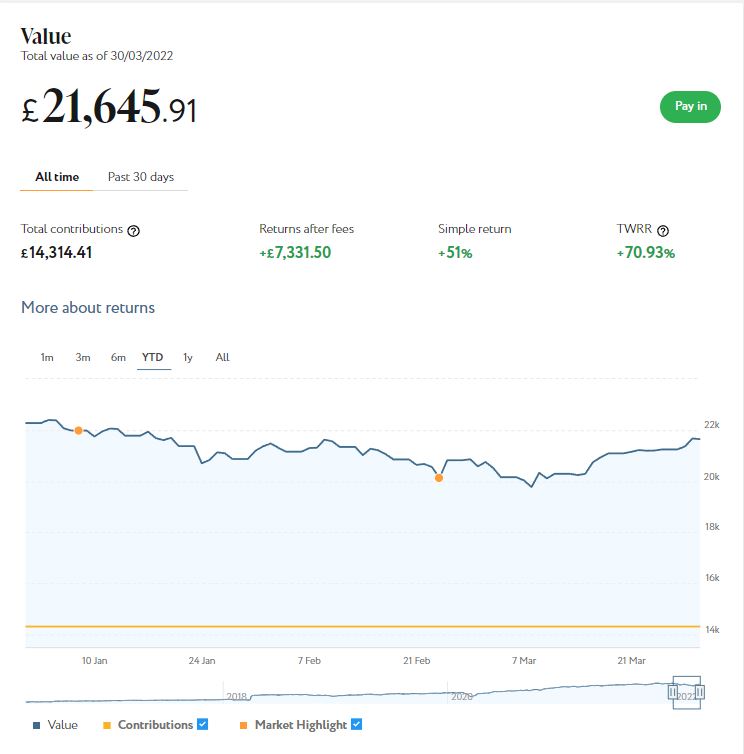

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio is currently valued at £21,646. Last month it stood at £20,859, so that is a rise of £787.

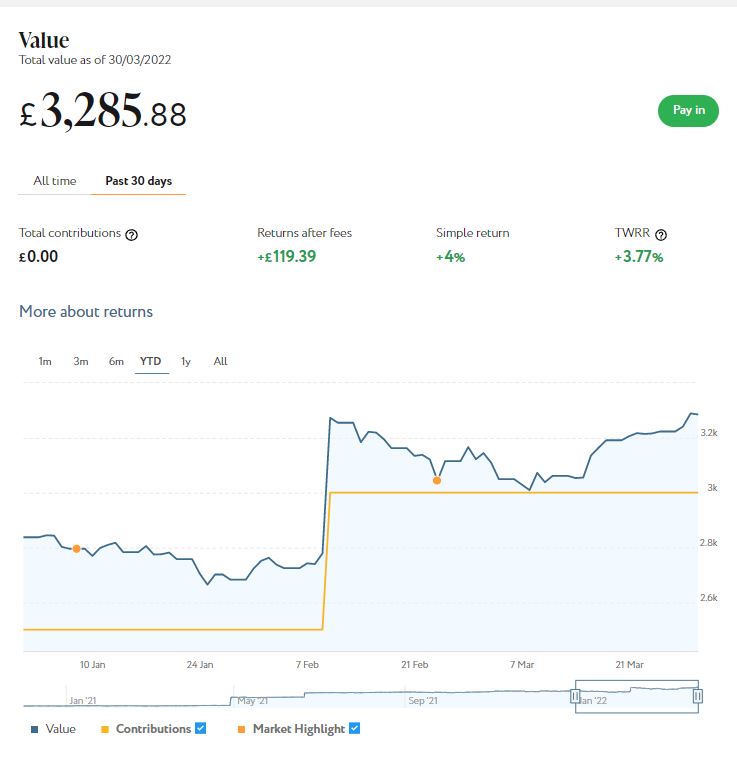

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,286 compared with £3,166 last month, a rise of £120

Here is a screen capture showing performance over the last month.

Obviously these rises are good news, and cancel out a good part of the falls since January this year. I hope this trend will continue in the coming months! I don’t know the exact reasons for the recovery in share prices, but I guess some of it may be down to the likelihood of nuclear Armageddon in Ukraine receding a bit. In any event, it does demonstrate the importance to investors of holding your nerve when prices fall and not bailing out at the first sign of trouble. As I often say on Pounds and Sense, investing should always be regarded as a medium- to long-term venture.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put an initial £100 into this in mid-February 2021 and another £400 in April. Everything went well, so in June 2021 I added another £500, bringing my total investment on the platform up to £1,000.

Since I opened my account, my Assetz Exchange portfolio has generated £47.60 in revenue from rental and £73.85 in capital growth, a total of £121.45. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

At one time Assetz Exchange had a problem with demand from investors outstripping supply, but in recent months an influx of new projects has helped alleviate that. AE also has a sensible policy of limiting the amount any one person can invest in a project for the first few weeks (typically £2,000 to £3,000 maximum), to ensure everyone has a fair chance to participate.

I recently invested some of the rental income I’ve received in another project on AE, a housing association property for people with learning difficulties in Doncaster. I now have investments in 22 different projects and all are performing as expected, generating rental income and – in every case but one – showing a profit on capital. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

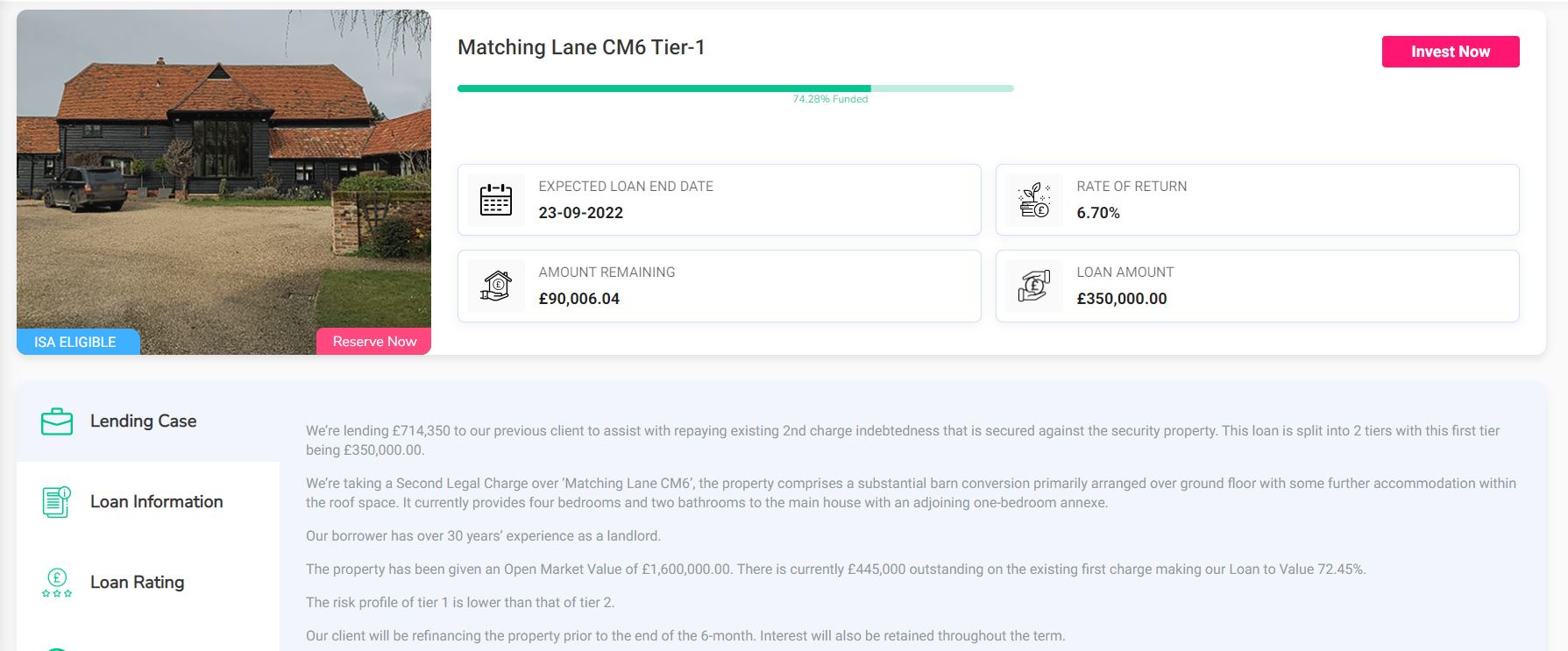

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have over £2,150 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present all my Kuflink loans are performing to schedule, with several due to mature in the next three months. So I will be planning to reinvest with Kuflink as this happens, in projects such as the one below.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £150 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

I’d also draw your attention to Kuflink’s revised and more generous cashback offer for new investors [affiliate link]. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

I also recently published a blog post about another P2P property investment platform called BLEND. Like Kuflink, they offer the opportunity to invest in secured loans to experienced property developers. They offer (on average) somewhat higher rates of return than Kuflink, though arguably with a little more risk. As well as my blog post about BLEND, you can also check out what they have to offer on their website [affiliate link].

Moving on, I have two more articles on the always-excellent Mouthy Money website. The first contains my best tips and advice about cruise holidays. As I say in the article, the cruise industry was hit hard by the pandemic, but it is up and running again now and desperate to lure holidaymakers back. So there are some great deals to be had at the moment!

My other Mouthy Money article is about two state benefits that many older people who would be eligible are currently missing out on. You can read this article here.

That’s plenty for now, so I’ll sign off till next time. I hope you are keeping safe and well, and making the most of the better weather and more relaxed Covid restrictions that now apply (apart from in Scotland). I am looking forward to visiting Llandudno in a few weeks time (and duly grateful the Welsh government has recently eased restrictions there). I also have breaks in Criccieth and Lavenham booked for later in the summer, with more to come. If you’re planning any UK holidays, don’t forget I have a list of places I have visited and recommend here 🙂

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links (disclosed). If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media: