Today I’m reviewing an app called JamDoughnut which can help you save money on your shopping.

What is JamDoughnut?

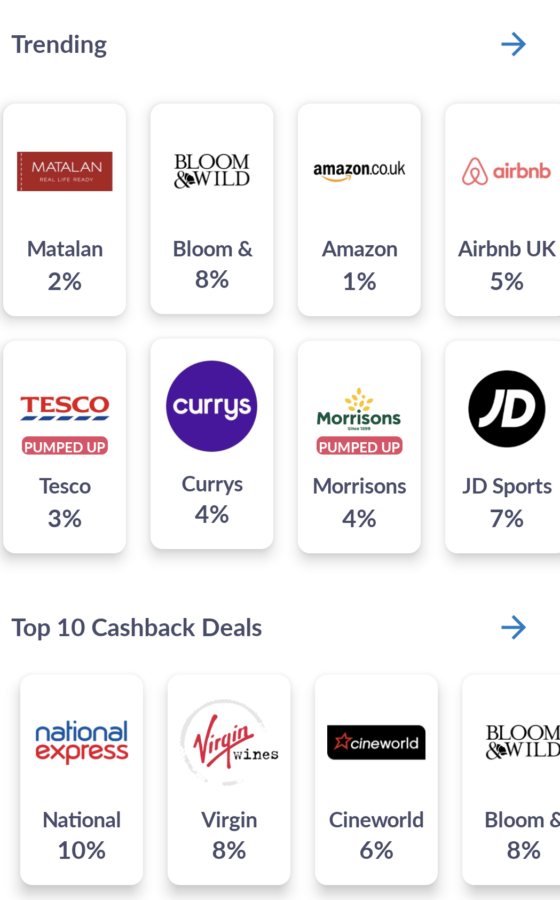

JamDoughnut is an instant cashback app that allows users to earn cashback when they spend money with over 150 leading supermarkets, restaurants and shops (see sample screenshot below).

Rather than cashback on specific purchases (as with sites like Quidco), you get cashback of up to 20% when you purchase gift cards from retailers on the app. These gift cards can then be used just like money, both online and in-store (in most cases).

How Does It Work?

The first step is to download the JamDoughnut app to your mobile phone from Google Play for Android or the Apple iStore. Open the app and follow the instructions to create an account (don’t forget to enter my referral code GBGN to get a 200 points [£2] bonus – see below). This should only take a couple of minutes.

Then check the list of retailers on the app and find one you shop with regularly. Most of the big supermarkets (with the exception of Waitrose) are included, for example.

You can even get cashback on Amazon gift cards, though admittedly only at a rate of 1% at the time of writing.

Once you have found a suitable retailer, buy a gift card for that retailer using the app. This is straightforward and you can get cards of up to £100 in value.

Once your gift card purchase has gone through, cashback will be credited to your account in the form of points (100 points = £1). In my experience this normally happens instantly. Once you have earned 1000 points, representing £10 cashback, you can withdraw the money to your bank account.

Note that there is a standard 30p transaction fee when making a withdrawal via bank transfer, and more than that if you use Apple Pay or Google Pay (so I don’t recommend doing that). So it may be best to let cashback build up a bit before withdrawing, to reduce the impact of the transaction fee. Alternatively you can withdraw in the form of a gift voucher (e.g. an Amazon voucher). In that case no charges are payable and you also get bonus points added to your account 🙂

In most cases, as mentioned, you can use gift cards either online or in-store. In the latter case, you can show/scan the code on your mobile phone at the checkout, or you can take a printed version with you and use that.

You can use gift cards for full or part payment. If you don’t use the whole amount on the gift card in one go, you can use what remains towards another purchase at a later date.

Other Benefits

Another attraction of JamDoughnut is that you can use the app in addition to your existing cards and loyalty programme points, allowing you to earn and/or save even more.

In addition, JamDoughnut offers a range of other benefits. These include a daily £100 (10 x £10) giveaway, free competitions, ‘Jammy Deals’, double discounts, and more. These are all listed on the ‘Daily Doughnut’ page of the app (see below).

Finally, if you’re so inclined, you can invite friends and relatives to join JamDoughnut using the ‘refer-a-friend’ scheme. If someone signs up using your referral code (see below), not only will they get an extra 200 points (worth £2) when they buy their first gift card, you will receive a bonus as well when they cash out for the first time (400 points, equivalent to £4).

Special Bonus Offer

Speaking of which, if you download the JamDoughnut app via this blog post and enter my referral code GBGN when requested, then (as mentioned above) you will get an extra 200 points (£2) when you use the app to buy a gift card for the first time – bringing.you that much closer to receiving your first £10+ cashback payment!

Closing Thoughts

In summary, I think JamDoughnut is a great little app and I have been pleased to add it to my armoury of money-saving tools and resources.

I do most of my grocery shopping at my local Morrisons, which is currently offering 4% cashback on JD gift card purchases – so in effect I am getting a 4% discount on all my shopping there.

And I am still getting all the benefits of my Morrisons Card too, including special discounts and regular £5 vouchers. In these challenging times, this really does help my money go a little bit further 🙂

As always, if you have any comments or questions about this JamDoughnut review, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Public speaking can be a good paying sideline for retired and semi-retired people. As well as the financial benefits, it can offer an enjoyable opportunity to talk about your hobbies and interests, or your current or former career. I’ve also known people who have done public speaking as a method of raising money for charities or other causes close to their heart. Although the pandemic and lockdowns temporarily put paid to most public speaking work, as life has returned to normal the opportunities are definitely out there again.

Over to Sally then…

Wouldn’t it be great to make extra money by following your passion? A hobby that pays makes ‘working’ a pleasure. Unfortunately, things like stamp-collecting, rambling and local history rarely turn a profit, but there is a way to make them pay: share your specialist knowledge with others.

Community organisations such as the WI, Probus and independent Leisure and Learning clubs struggle to find speakers for their meetings. I speak about novel-writing at many such groups and am always asked if I know of any other speakers open for bookings. These are paid gigs. How much you charge, how far you travel and what type of bookings you take are all up to you. Depending on the policy of the organisation, these events may also give you the opportunity to sell produce from your hobby. For example, I sell copies of my books, but a creator of conserves might sell jam and marmalade or an artist, his paintings.

Below are some tips for starting a speaking career:

Collate enough material for a 45-minute talk and sort it into a logical sequence. Include stories that will capture the listener rather than a lot of heavy facts.

Refine the material into minimal bullet-pointed notes. It’s important to talk freely around each bullet point rather than read from a manuscript. Reading makes eye contact with the audience difficult and hand gestures to illustrate your words are almost impossible.

Think about any visual aids; these add variety and colour to a talk. When I talk about thriller-writing I produce some ‘murder weapons’ – a rolling-pin, a (blunt) knife and a packet of tablets. The conserve creator might show her jam pan and specialist thermometer. The artist might have a range of brushes to discuss.

Practise! Producing a successful talk is like an iceberg. At least 90% of the work is in the preparation beforehand. However, once you’ve perfected your performance, you can give that same talk many times to different groups.

Don’t be surprised if you are handed a microphone to use. This often happens in large halls or where several audience members are hard of hearing. Hold it at a consistent distance from your mouth and don’t turn your face away from it. Practise at home by holding a wooden spoon – this will give you an idea of what it’s like to talk with only one free hand.

Enquire at your local church hall about community groups who meet there and use speakers.

Do a couple of small bookings for free and ask for feedback from the audience. Once you’re confident, don’t make a habit of speaking for free (unless it’s a charitable cause) because that makes it harder for other speakers to ask for a fee.

Receiving a cheque at the end of a talk is good but public speaking brings other benefits, such as the opportunity to meet new people and share your knowledge. It will improve your everyday confidence as well. When you can speak in front of an audience, complaining in a shop or restaurant is less daunting, putting your point of a view in a meeting is easier and making small talk with strangers at a party is no problem.

Many thanks to Sally Jenkins (pictured) for an interesting and inspiring article. Although as I said to her, I hope she never gets stopped by the police on the way to one of her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!

I have done a bit of speaking myself, both for work reasons (in the long-ago days when I had a proper job) and to talk about writing or blogging. I always get nervous beforehand, but once I start I normally enjoy it and get a buzz from doing it.

I would maybe add one more tip to Sally’s list and that is to compile a list of topics you can speak about (with appropriate visual aids, of course). You can then offer potential bookers a ‘menu’ they can choose from. This has the benefit that if they don’t like one idea, they may well go for another. It also means you can potentially get repeat bookings, maybe on a regular basis, speaking on a different subject each time. This certainly happens with some of the speakers who are booked by my local U3A.

As always, if you have any questions about this article, for Sally or for me, please do post them below.

This is a fully updated version of an original post from 2019.

If you enjoyed this post, please link to it on your own blog or social media:

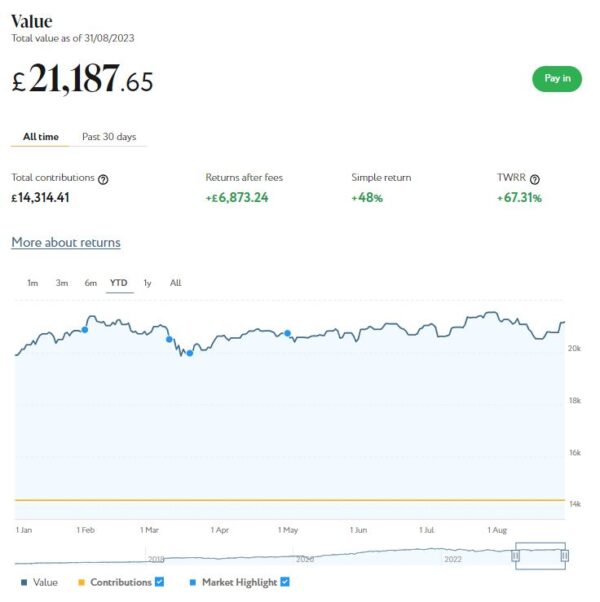

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,188. Last month it stood at £21,548 so that is a fall of £360.

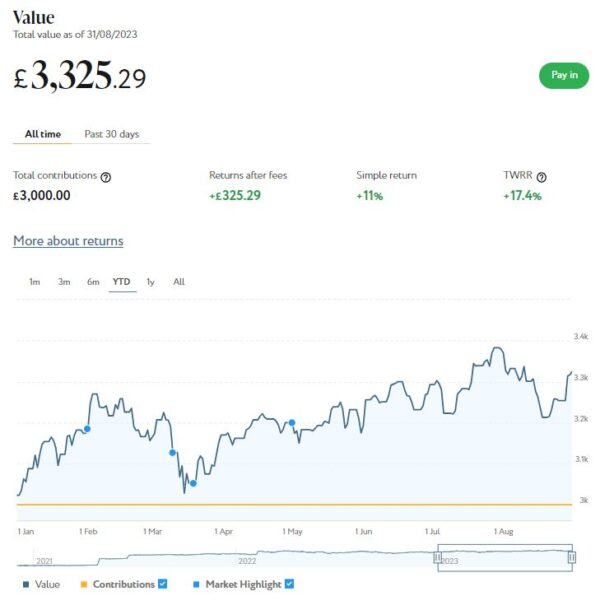

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,325 compared with £3,383 a month ago, a fall of £58. Here is a screen capture showing performance since the start of this year.

The net value of all my Nutmeg investments has fallen this month by £418 or 1.68% month on month. That’s obviously a bit disappointing, but both pots are still comfortably up on where they were at the start of the year. Their total value has risen by £1,592 (6.95%) since 1st January 2023.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have £2,145 invested with them in 17 different projects paying interest rates typically around 7%. I also have just over £100 in my cash account after another loan was repaid. I am currently considering whether to withdraw this money or (in due course) reinvest it.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

As mentioned last time, Kuflink recently changed their terms and conditions. As from Monday 21st August there is an initial minimum investment of £1,000 and a minimum investment per project of £500. I wondered if this would also apply to their secondary market and this does indeed seem to be the case. When I checked just now, there was only one loan on offer for under £500 (£413) and all the others were £500 or more.

Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean the option to ‘test the water’ with a small first investment has been removed. It will also make it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget. As mentioned, my current portfolio of £2,145 comprises 17 different investments ranging from £50 to £200. If I was starting out again now, that same amount of money would only stretch to four deals!

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. The rates on offer from August 1 2023 are shown in the graphic below.

As you may gather, you can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £134.95 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 9 of ‘my’ properties are showing gains, 1 is breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £28.83, meaning that overall (rental income minus capital value decrease) I am up by £106.12. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

Also, as I noted last time, the recent high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. Assetz Exchange recently published a blog post about this which is worth a read.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

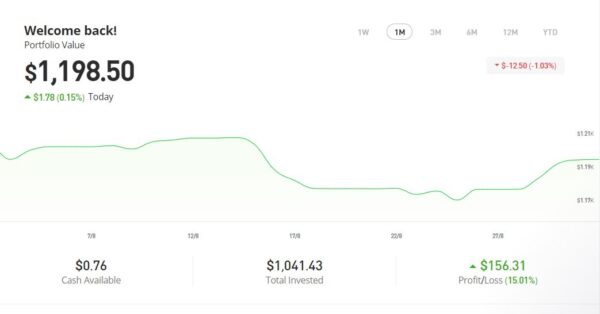

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen capture below, my original investment of $1,022.26 is today worth $1,198.50, an overall increase of $176.24 or 15.05%. in these turbulent times I am very happy with that.

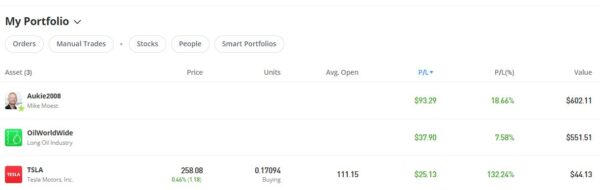

In the last month my copy trading portfolio with Aukie2008 has fallen in value, though I am not too concerned about this as the investment is still well up overall. My Tesla shares have again done well (thank you, Elon Musk). I am also pleased that Oil Worldwide continues to forge ahead since it was rebalanced in July by eToro. Looking at my eToro virtual portfolio, I can see that Oil Worldwide is still doing much better than the two renewables smart portfolios I hold, which are currently showing substantial (thankfully virtual) losses. Make of this what you will!

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had three more articles published in August on the excellent Mouthy Money website. The first was Can You Make Money From Holiday Lets? This is a dream for many people, and there is no doubt you can make a valuable extra income this way (not to mention the opportunity to enjoy cheap holidays at the property yourself!). In my article I set out some key things you need to be aware of.

I also wrote How to Become an Amazon Vine Reviewer. This is a subject close to my heart. I’ve been an Amazon Vine reviewer for over ten years and in some ways it’s been the most profitable sideline I’ve ever had. You don’t get paid for Amazon Vine reviews, but you do get to keep the items concerned (my most valuable so far being a £1200 gaming laptop). In my article I spill the beans on how the scheme works and suggest how you might get an invitation to become a ‘Vine Voice’ yourself.

My third article was Play Your Supermarket Loyalty Cards Right. In this article I explained why stores use loyalty cards and their pros and cons for customers. I also described the leading loyalty cards in the UK (including Tesco Clubcard, Nectar, Morrisons, Boots, and so on), covering how they work in practice and how to get the most from them.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here

I also published several new posts on Pounds and Sense in August. The deadlines on some of these have now passed, so I hope you took advantage at the time! You might, however, still want to check out What is U3A and Is It For You?

U3A stands for University of the Third Age. It is a non-profit organization offering a range of leisure activities for retired and semi-retired people. I recently joined my local U3A myself, and in this post set out my experiences and impressions, for the benefit of anyone else who might be interested in joining now or in future.

In other news, the Trading 212 free share offer is back. If you haven’t done this before, you can get a free share worth up to £100. You just have to sign up on the website and deposit a minimum of £1 into your account. This offer is running till 27 September 2023. See Get a Free Share Worth up to £100 with Trading 212 for more info.

The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is also still open. Wealthyhood is a DIY wealth-building app aimed especially at people new to stock market investing. As from June 2023 they changed their fee structure to make it (even) more attractive to small investors. They have increased the minimum investment to qualify for the free share offer from £20 to £50 – but on the plus side, they guarantee that your free ETF share will be worth at least £10.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to learn to call it now). Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

As a matter of interest, I recently paid £100 for Twitter/X premium membership. Although I do like the snazzy blue tick, my main reason was to get continued access to the scheduling tool Tweetdeck (now called X-pro) which became subscriber-only last month. I was accused the other day of ‘selling out’ to Elon Musk for doing this. But personally I don’t begrudge the money, as the extra tools and features make working with Twitter much easier and more enjoyable. And if my money helps keep the platform afloat, that’s an additional benefit in my book.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!

her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!