As you will doubtless know, yesterday the Chancellor delivered his 2023 Autumn Statement. This included various economic measures, which you can read about on the Moneysaving Expert website (among other places).

I thought today I would highlight one particular change to the rules about tax-free ISAs (Individual Savings Accounts) which caught my eye. From April 2024, you will be allowed to open more than one of any particular type of ISA in a single tax year. This is a change I was particularly pleased to see, and have in fact been advocating on Pounds and Sense for some time.

As you may know, there are various types of ISA, including the stocks and shares ISA, cash ISA and IFISA. The latter stands for Innovative Finance ISA and allows people to save tax-free with peer-to-peer lending and similar platforms. Everyone has an annual tax-free ISA allowance, which currently stands at £20,000. Despite rumours to the contrary, this limit was not changed in the Autumn Statement.

So why do I think the change in the rules announced yesterday is so important? Well, for one thing, it brings about much greater flexibility in ISA transfers. Investors will now be able to transfer funds freely between different types of ISA without jeopardizing their tax-free status. They will also be able to transfer just part of a holding to a different provider, regardless of when they paid in the money.

This will empower investors to optimize their investment strategy by making it easy to move money between cash, stocks and shares, and Innovative Finance ISAs. This enhanced transfer flexibility should enable investors to adapt to changing market conditions, seize new opportunities, and align their portfolios with their evolving financial goals.

A further benefit of the rule change is that it will make it easier for investors to build a well-diversified portfolio. Rather than having to put all their money into just one stocks and shares ISA per year (for example) they can divide it among a range of providers. Regular readers will know that I am a big fan of diversifying your portfolio as much as possible to help manage risk, and this rule change certainly facilitates that.

The change will also make it easier for investors to try out new platforms with relatively small investments initially. Previously they may have been deterred from doing this by the realization that once they had committed to one particular provider, they would have to stick with that provider for the rest of the financial year. FOMO (fear of missing out) may even have inhibited some people from investing at all.

This is certainly something I’ve experienced myself. At the start of a new financial year, I was wary of investing in any type of ISA, because I knew that once I did so, I would then have to stick with that provider for that type of ISA for the rest of the financial year.

So those are just some reasons I particularly welcome this rule change. From a broader perspective, I think it will also encourage more people to start investing, which has to be good for UK PLC in general. Apart from a few admin costs, it seems to me this measure will cost the government nothing, while bringing major benefits to the economy and individual investors. Really, the only thing I don’t understand is why it wasn’t done sooner!

So those are my thoughts anyway. But what do you think? Will the new rule encourage you to make more use of ISAs in future? I’d be interested to hear any views.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing some interesting data from my friends at HSBC regarding how British people choose life insurance.

This information comes from an online survey of over 2,000 people in the UK conducted on behalf of HSBC Life Insurance. It provides some interesting insights into who is – and isn’t – getting life insurance, and their reasons for doing so.

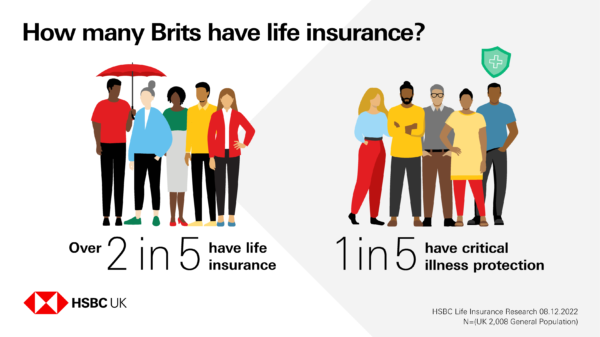

As you can see from the graphic below, the study revealed that more than two in five people in the UK have life insurance (43%), with another one in five (20%) saying they have critical illness protection. The latter provides protection (generally in the form of a one-off tax-free payment) if you become seriously ill or injured. It is typically purchased in addition to life insurance.

Financial worries are a key factor for those Brits who have researched their options but still decided against getting life insurance. One in two (50%) who’ve considered getting a policy but decided not to go ahead say that it’s because they’ve had to tighten their belts.

Reasons for Choosing a Policy and a Provider

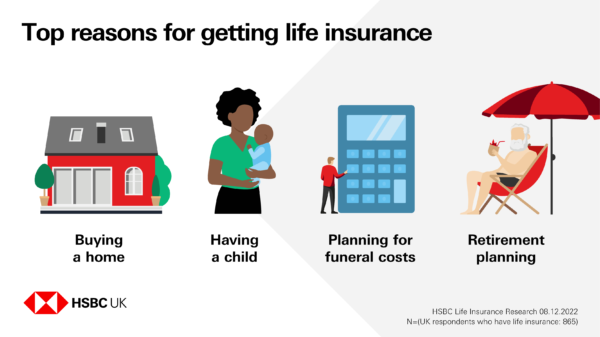

Brits with a policy said the primary reasons they got life insurance were: buying a home (19%), having a child (14%), planning for funeral costs (10%) and retirement planning (9%).

Perhaps surprisingly, people with long-term partners were more likely to say they had a single (54%) than a joint (42%) policy. Those couples who had a joint policy were most likely to say the main reason they chose it was simplicity (37%), followed by “level of cover” (30%) and budget (19%).

The biggest driver for those with life insurance or those who had considered purchasing it in the past two years was price (25%), closely followed by trust in their chosen provider (18%), and confidence that a claim would be paid (13%).

Understanding of Terms

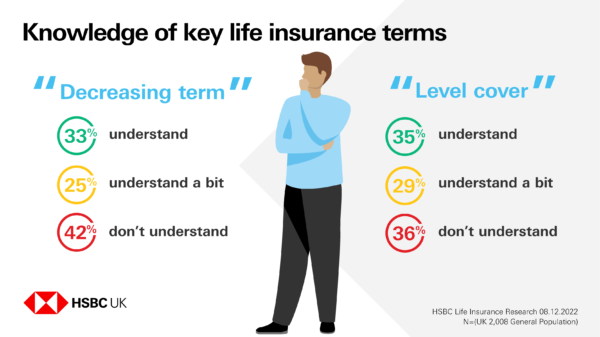

When it comes to key terms relating to life insurance, only around a third of people in the UK say they fully understand the phrases “level cover” and “decreasing term”.

More than two in five Brits (42%) say they don’t know what “decreasing term” means, and more than one in three (36%) don’t fully understand “level cover”.

Most people (53%) say they think “level cover” is the most important consideration when choosing which life insurance policy to purchase, after the terms were explained to them.

Purchase Preferences

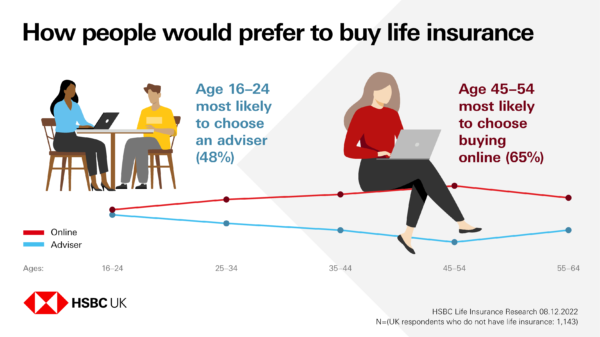

People in the UK who have life insurance are pretty evenly split when it comes to how they bought it, with 49% purchasing through an adviser and 47% completing their transaction online.

And overall, those without any cover are more likely to say they’d buy online if they did decide to purchase a policy (58%), compared with through an adviser (40%).

But there are some interesting differences in age – with nearly half (48%) of 16-24-year-olds without insurance saying they’d prefer to use an adviser, more than any other age group. Meanwhile the 45-54 age group were the most likely to say they’d go online (65%).

Closing Thoughts

Many thanks to my friends from HSBC for allowing me to share and discuss their data and graphics.

Nobody would pretend life insurance is an exciting subject, but in these uncertain times it’s something we all need to think about, cost-of-living crisis notwithstanding. Life insurance protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

I discussed this subject in more detail in my blog post Do You Need Life Insurance? (mentioned earlier) and I recommend checking this out if you haven’t already. You may also want to speak to a personal financial adviser to find out more about life insurance and what might be the best option for you.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

For the second winter in a row, some energy companies are offering incentives to customers to reduce their electricity use during periods of peak demand. Payments are made to those who succeed in doing this.

Most large energy companies – and some smaller ones – are running schemes, though some by invitation only. At the time of writing they include British Gas, EDF, Octopus Energy, E-on, OvoEnergy, Shell Energy, Scottish Power and Utilita. You can see a regularly updated list on this page of the Moneysavingexpert website.

If you aren’t with one of these companies, however, you may still be able to benefit by signing up with an app-based service such as Loop Energy or Power Rewards.

Don’t, though, be tempted to sign up for more than one scheme at a time. That is against National Grid’s rules and could see you being banned from receiving ANY payments.

This programme is part of a broader initiative from the National Grid Electricity System Operator (ESO), the organization responsible for transporting electricity around England, Scotland and Wales and keeping homes and businesses powered. The aim is to balance supply and demand, thus reducing the need to fire-up fossil-fuel plants and (in the worst case) avoiding power cuts.

During cost-cutting events, National Grid ESO pays participating suppliers a certain amount for each unit (kWh) of electricity saved by any of their users signed up to schemes. Suppliers then pass some or all of this payment on to customers.

One thing all schemes have in common is you must have a smart meter capable of sending half-hourly readings. Smart meters are of course somewhat controversial, and for various reasons not everybody wants one. If you wish to benefit from this particular opportunity, however, having a smart meter is essential. For the record I do have a smart meter and believe it has saved me money. But I do of course respect those who have differing views about this.

How It Works

To make money from these schemes you will be asked to reduce your electricity (not gas) consumption during certain periods. This is most commonly around the evening peak time of 4 pm to 7 pm, but exact times vary depending on the supplier concerned and the needs of National Grid.

The duration of events varies but in my experience is typically an hour or 90 minutes. But I understand they could be anywhere between 30 minutes and three hours.

You are unlikely to make a fortune from these schemes, but could earn up to £100 (or more) over the course of the winter. Payments vary from around £2.50 to £4.50 per unit (kWh) saved, the rate depending on what National Grid is paying. The actual rate you receive will also depend on how much of the payments from National Grid your supplier chooses to pass on.

One other important point is that you may be expected to reduce your usage by a certain minimum amount (e.g. 40%) from your average in order to receive a payment. If you cut your usage by less than this, unfortunately you may not qualify for any payment on that occasion.

You will be required to opt in to the scheme run by your energy supplier (or other provider). You will likely also have to opt in to specific energy-saving events, with advance notifications sent via email and mobile phones.

How to Maximize Your Returns

Here are a few tips and ideas for cutting your electricity use during power-saving events and maximizing the returns you receive…

Turn off as many lights as possible, including outside lights (easily forgotten).

Turn off all mains-powered computers, printers and other electronic devices (again, easily forgotten).

Avoid cooking with electricity during events.

Avoid using other high-energy-consumption devices such as dishwashers and washing machines.

Obviously, avoid using electric heating if possible. If there’s no alternative, heat up the room/s you will be in beforehand and close all doors, windows and curtains to keep the warmth in.

Avoid taking electric showers while events are in progress.

Be sure no electrical devices have been left on to charge.

Switch off the TV and watch instead on your laptop/tablet using its internal battery.

Avoid boiling the kettle as this uses a lot of electricity (albeit for a short period). Make a flask of coffee/tea beforehand and drink from that during the event.

Avoid opening fridge/freezer doors during events. But you can also switch off fridges and freezers entirely to save more. This should be perfectly safe for up to three hours.

If it’s feasible, arrange to go out during some or all of the power-saving event. This is the easiest way to save as much electricity as possible!

Create a checklist of things to do at each event to save power. You can also use this after the event to ensure you remember to turn things like fridges and freezers back on again.

One other slightly left-field idea is to use high-energy devices such as washing machines and electric cookers MORE during evening peak times when there isn’t a power-saving event happening. That will boost your average energy consumption at this time, giving you the opportunity to save more when a power-saving event comes along. Obviously you shouldn’t use high-energy devices more than you would overall. But if you can shift your usage to peak times when power-saving events are typically scheduled, this should help you save more when events occur.

I hope this post has given you some ideas for how to maximize your returns from these schemes. As always, if you have any comments or questions, please do leave them below. I’d also be very pleased to receive any other tips for making more money from power-saving events.

Don’t forget, you can also get a FREE £50 credited to your energy account when you switch to EDF Energy via my affiliate link. Terms and conditions apply.

This is a fully updated version of my original 2022 post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post on what can become a major issue for parents when making gifts or loans to their married children. Specifically it looks at what you can do to ensure that your wishes are respected should the worst happen and the marriage fails.

The article is by Joanna Toloczko, a partner, family law solicitor and mediator at UK law firm RWK Goodman.

Over to Joanna then…

According to the UK House Price Index in August 2023, the average house price in the UK was £291,000 and in London a whopping £536,000. To put this into context, the average house price back in January 2013 was £167,716, representing an increase of around 73%.

A bank or building society will normally require a minimum deposit of between 10% and 25% of the property value as a term of a mortgage offer, and the more you are able to put down as a deposit, the lower rate of interest you are able to secure. It is not surprising, then, that an increasing number of married couples rely on a contribution from one or both sets of parents for their deposit.

In my work as a family lawyer and mediator I often come across cases where a divorcing couple are at loggerheads about whether such a contribution was a loan or a gift. The party whose parents provided the funds will often argue that the funds were a loan which should be returned to their parents before the remaining funds are distributed between the husband and wife. The other party will usually argue that the funds were a gift and are available for distribution between the parties.

If the couple are not able to reach agreement and the case proceeds to court significant sums of money can be spent on arguing this point as a preliminary issue. Very often the parents will be drawn into the litigation.

Even if the Court accepts that the funds were a loan, it is possible that the Court will take the view that it was a “soft loan”, i.e. a loan where repayment is unlikely to be enforced. In these circumstances, the Court may choose to disregard the liability.

Usually, at the time the funds are made available to the couple no-one has formally addressed the issue of the nature of the advance. Everyone is excited about the new house purchase; no-one anticipates that the marriage may fail.

So, what can be done to ensure that gifts made to married children stay in the family of the parents making the gift, in the event of a divorce?

If the funds are being advanced to assist with the purchase of a property, a Declaration of Trust can be a useful tool. In this situation the married couple are the legal owners of the property and hold the property as “tenants in common”, which means that they have their own distinct share in the property. The Declaration of Trust can be used to set out the beneficial interests in the property, including the interests of third parties. For example, a Declaration of Trust could make it clear that as parents had contributed to the purchase price of the property, they are entitled to a specified share of the equity. Alternatively, the Declaration of Trust could set out that once the property is sold, the parents have to be reimbursed prior to the distribution of the remaining equity between the couple.

If parents are to receive a share of the equity, they need to be aware of a potential Capital Gains Tax liability, should their interest in the property increase in value.

Another alternative would be to use a formal loan agreement or for the parents to take a Legal Charge over the property. A Legal Charge works like a second mortgage. It is secured over the property and registered at the Land Registry. The Charge sets out details of the sum loaned to the couple, whether interest is payable and when/in what circumstances the parents are entitled to call for repayment of the loan.

Nuptial Agreements are also becoming more popular. These can be entered into either before the marriage (Prenuptial Agreement) or during the course of the marriage (Postnuptial Agreement).

These agreements make clear what is to happen to the couple’s assets in the event of divorce or separation.

If parents are gifting money, transferring properties, leaving an inheritance, providing an interest in a business, etc, and they wish to protect those assets in their child’s favour in the event of separation or divorce, a Pre- or Postnuptial agreement can be an extremely useful document.

Although Nuptial Agreements are not legally-binding and can be over-ruled by a judge in the divorce proceedings, if they are prepared in the correct manner, they have good prospects of being upheld or will certainly be heavily influential on the judge.

In summary, when advancing funds to a married child, always be clear about whether the funds are a gift or loan and seek legal advice about how best to ensure that the funds remain in the family in the event of a divorce. It is usually also a good idea to discuss any tax implications of your plans with an accountant or tax adviser.

Joanna Toloczko is a partner, family law solicitor and mediator at RWK Goodman and can be contacted on 07553 058485 or at Joanna.Toloczko@RWKGoodman.com.

Many thanks to Joanna Toloczko (pictured, below) for an informative and eye-opening article. Please do check out her company’s website (linked above).

While nobody likes to think about the marriage of their offspring failing, the reality is that an estimated 42% of marriages in the UK today will end in divorce. So it is vital to be realistic and ensure that, should the worst happen, any money you give or lend is returned or divided in accordance with your wishes.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

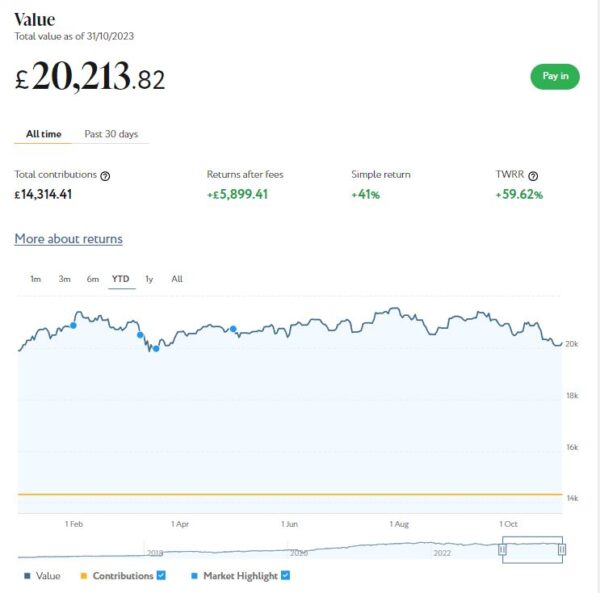

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £20,214. Last month it stood at £20,945 so that is a fall of £731.

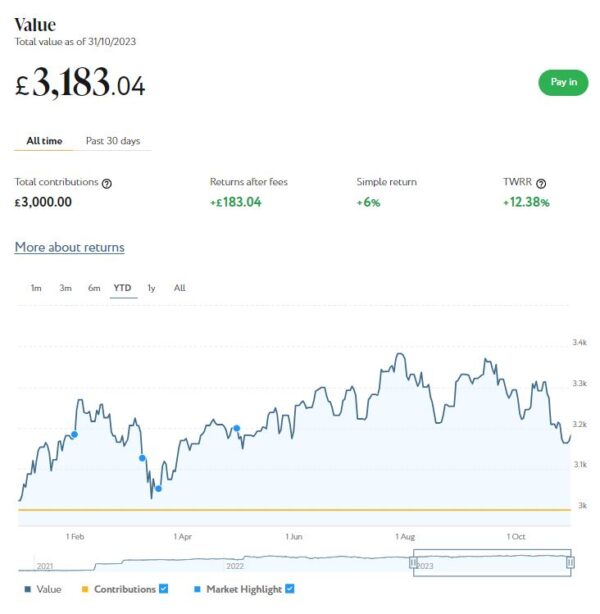

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,183 compared with £3,295 a month ago, a fall of £112. Here is a screen capture showing performance since the start of this year.

The net value of all my Nutmeg investments has fallen this month by £843 or 3.47% month on month. That’s obviously disappointing, but both pots are still up on where they were at the start of the year. Their total value has risen by £476 (2.08%) since 1st January 2023. I’m not saying that’s anything to cheer about, but due to world events nearly all stock market investments have taken a hit in the last few weeks, and Nutmeg is no exception.

As I always say, investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

As you may know, I recently revised and updated my full Nutmeg review. This was mainly to incorporate details of their new thematic investment option, but I took the opportunity to update some other information and performance stats as well.

As it says in the updated review, the new thematic style provides a globally diversified, risk adjusted portfolio with a tilt (up to 20% of equity exposure) towards your chosen theme. The majority of the portfolio will be actively managed by Nutmeg’s investment team, whilst the ’tilted’ part of the portfolio will be made up of ETFs that their investment team believes will deliver the best returns from the trend in question (to be reviewed annually).

Currently three themes are available, these being Technical Innovation, Resource Transformation and Evolving Consumer. For more details about what each of these comprises, check out the Nutmeg website.

Nutmeg thematic portfolios are only available on Risk Level 5 or above. There’s a minimum investment of £100 for Junior ISAs and Lifetime ISAs or £500 for stocks and shares ISAs and pensions. There is a 0.75% management fee.

I do quite like the new thematic styles on Nutmeg and may well be investing in one myself. They are similar in concept to the so-called smart portfolios on eToro, which I discussed in this recent blog post. Nutmeg’s thematic styles appear to be more broadly diversified, however, so may be a good choice for those who are new to thematic investing and want to dip a cautious toe in the water first.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,400 invested with them in 12 different projects paying interest rates typically around 7%. I also have just over £600 in my cash account after several loans were recently repaid.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

As mentioned last time, Kuflink recently changed their terms and conditions. There is now an initial minimum investment of £1,000 and a minimum investment per project of £500.

Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean the option to ‘test the water’ with a small first investment has been removed. It will also make it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. The rates currently on offer are shown in the graphic below.

As you may gather, you can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £145.22 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 6 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £37.80, meaning that overall (rental income minus capital value decrease) I am up by £107.42. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

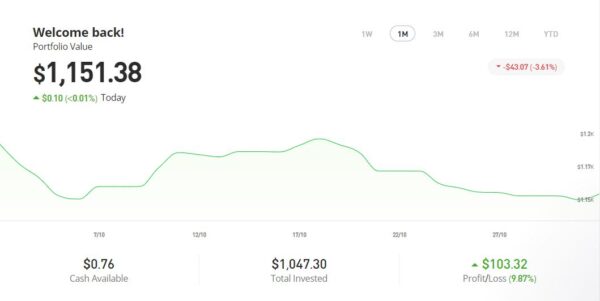

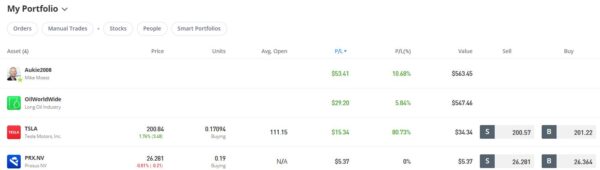

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,151.38, an overall increase of $129.12 or 12.63%. in these turbulent times I am happy enough with that.

Incidentally, if you’re wondering what the bottom item in the list is (PRX.NV), it’s a partial share in Dutch internet company Prosus NV. I don’t honestly know where this has come from – it’s not something I deliberately bought. I assume it may be some sort of bonus from eToro, or maybe it’s connected with my copy trading account with Dutch investor Mike Moest. But I’m happy to have it in my portfolio, obviously!

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in October on the excellent Mouthy Money website. The first was How to Make Money From Retail Deal Arbitrage. This is a relatively under-used approach to online auction trading (though you don’t necessarily have to use online auctions at all). It normally proceeds one item at a time, so you don’t need large amounts of space (or capital) for stock. You can ramp it up to multiple items later if you like, though.

I also wrote Could You Make Money as a Freelance Proofreader and Editor. This can be a great sideline, or even a full-time business, for anyone who enjoys working with words. No special tools or equipment are required, so it’s quick, cheap and easy to get started. It’s reasonably paid, and you can work from home at hours to suit yourself. It’s also suitable for older people and people with disabilities (with the one proviso that it becomes harder if – as in my own case – your eyesight isn’t as good as it once was).

I also updated my article published last month titled Will a Heat Pump Save You Money? This is obviously a hot topic and one where policy is constantly changing. I thought I should update it with the latest information about government bribes – sorry, incentives – to get one. Do take a look if you haven’t already!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here

I am also a fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her articles – such as this one on Frugal Swaps to Save You Money – are always worth a read. You can see all her articles for Mouthy Money via this web page.

I also published various posts on Pounds and Sense in October. I won’t bother to mention those that are out of date now, but the rest are listed below.

Exploring the Potential of Investing in Alternative Rental Properties was a guest post by my colleague Jackie Edwards. Jackie is a semi-retired property developer and restorer. In her article she presents the case for businesses and individuals to invest in rental properties for the growing over-50s market. At the end of the article I also suggest an alternative method for those whose pockets may not be as deep to invest in this field.

I also published Will You Get the Warm Home Discount? The 2023/24 WHD scheme opened in October. As last year, those eligible will receive a £150 discount off their energy bills. Most people no longer have to apply for WHD and should receive it automatically. Read the article to learn more, along with other support towards the cost of your energy bills that you may also qualify for.

Finally, I published a short post about Over 60s Discounts, a new website dedicated to helping older people save money. It’s free to sign up, and there are loads of savings, discounts and concessions on offer. Read my blog post for more info, and check out the website yourself!

On other matters, the opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is still open. This DIY wealth-building app is aimed especially at people new to stock market investing. The minimum investment to qualify for the free share offer was raised recently from £20 to £50 – but on the plus side, they now guarantee that your free ETF share will be worth at least £10. What’s more, for the next two months Wealthyhood say they will plant a tree for every new account opened, so what’s not to like 🙂 🏝

Another thing that happened in October is that I finally got some of my money back from the Bricklane property REIT. I invested several thousand pounds in this a few years ago. At first all went well, but then came the Grenfell Tower tragedy followed by the cladding scandal.

Bricklane (or more precisely investors such as me) owned a number of properties which required (expensive) remedial work. Bricklane didn’t go into liquidation, but they felt they had no option but to sell their entire property portfolio and distribute whatever funds were generated (after all costs had been covered) to investors.

Anyway, to cut a long story short, investors in the Bricklane London fund (including me) should all now have been repaid. I got about £880 of my £1,000 investment back, which I suppose isn’t too bad considering. The Bricklane Regional Capitals fund, in which I also invested, is taking a bit longer to wind up, and I am not expecting to see any return from this until some time next year.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to learn to call it now). Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: