In case you’ve not heard, Amazon Prime Big Deals Day is almost with us. It extends over two days, Tuesday 8th and Wednesday 9th October 2024.

This is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products from leading brands including Philips, Logitech, Oral-B, Braun, Tefal, Ghd, Swarovski, Bosch, Shark, and so on.

Some of the best deals will be reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts of up to 60% will be on offer for these products. If you’re thinking of buying any of them, Amazon Prime Big Deals Day is definitely the day – or two days – to do it.

There are also some great ‘early deals’ available now. For example, at the time of writing you can buy an Amazon eero mesh Wi-Fi Router 5 system (2 pack), offering up to 280 square metres coverage, for just £54.99. That’s a 57% discount on the normal £129.99 asking price (offer closes 10th October).

I have been a member of Amazon Prime for almost ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a host of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next few days, so you can benefit from the Prime Big Deals Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Big Deals Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Big Deals Day offers by clicking here.

As always, if you have any comments or questions about Amazon Prime or Prime Big Deals Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m featuring a way you can get a free share worth up to £100 by signing up with an online share trading platform called Trading 212.

Trading 212 is unusual in that it offers commission-free and fee-free share trading. As a special offer, until Wednesday 6th November 2024 they are offering people new to the platform a free share just for signing up via a referral link (such as the links in this post). The share you will get is chosen at random, but could be worth up to £100. You can either keep this share or sell it.

How to Sign Up

Signing up with Trading 212 is pretty straightforward. Just visit the Trading 212 website via any of the (referral) links in this post and follow the on-screen instructions to register. Note that you will be required to provide various items of information, including your date of birth, National Insurance number, annual income, employment status, and contact details. I understand that this is to meet their legal ‘Know Your Customer’ duty.

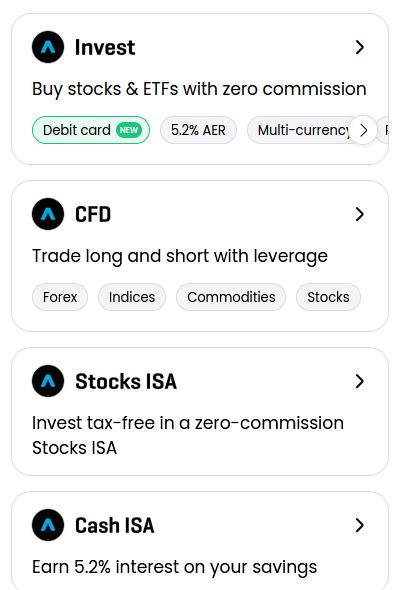

You will also need to indicate the type of account you want from the options available (see screen capture below).

As you will see, the four account types on Trading 212 are Invest, CFD, Stocks ISA and Cash ISA. You can apply for any or all of these if you like.

CFD stands for Contract for Difference. CFDs are quite complex financial instruments, and unless you know what you’re doing I recommend giving them a miss.

If you just want the free share my suggestion would be to tick the Stocks ISA box. An ISA is, of course, a tax-exempt Individual Savings Account. As from April 2024 you can open any number of ISA accounts in a year as long as you don’t exceed your annual £20,000 allowance.

If you have already used up your entire £20,000 this year, you should choose Invest instead to open a general investment account without any tax benefits. Obviously if you don’t want a Stocks ISA with Trading 212 for any reason, you can choose this option as well.

For more information about the new Trading 212 Cash ISA, see my review here. Be aware that you must open either an Invest account or a Stocks ISA account to qualify for a free share. Of course, there is nothing to stop you opening a Cash ISA account as well, but my recommendation would be to open an Invest or Stocks ISA account first.

Getting Your Free Share

There is one more step you will need to take in order to get your free share. You will need to deposit a minimum of £1 into your account. There are various ways you can do this, but i just used my debit card. There is no obligation to invest the £1 (or whatever you choose to deposit) and if you wish you can withdraw it once your free share has been credited.

The next business day you should receive an email confirming that a free share has been added to your account. As mentioned above, this is allotted at random. If you’re lucky you might get one worth up to £100. Even if you get a less valuable one, though, it’s still a share for free. If you choose to keep it, it may rise in value. There may also be dividends payable in future (and credited to your account).

Already have a Trading 212 account? You can also get a free ETF share worth up to £200 (and now guaranteed to be worth at least £10) with new DIY wealth-building app Wealthyhood. A minimum investment of £50 is required to get the free share (although if you’re not bothered about this you can start investing on the platform with as little as £20). Click through here for more info.

Selling Your Share

You can’t sell your share immediately. You have to wait three business days before doing so, but it is then just a matter of clicking the Sell button on your member’s dashboard.

The money will be credited to your Trading 212 account but you will have to wait 30 days before withdrawing it. So there may be a case for waiting to see if your share’s value goes up in that time. Of course, it could also go down!

In my case, I received a free share in the Ford Motor Company worth just under £8 at the time. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort 😀

How Safe Is Trading 212?

Trading 212 is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £85,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks and shares, which can go down as well as up. All investments carry a risk of loss, although in the case of your free share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Trading 212 member can also refer new members. In this case, both you and the person concerned will receive one free share worth up to £100. Obviously, the links in this blog post include my referral code – so if you register and get a free share, I will receive one also. Under the terms of the current offer you can get up to five free shares in this way. Five is the limit per person. Although you can still refer new members who will get a free share after this, as a referrer you won’t receive one as well.

Final Thoughts

I first heard about Trading 212 a while ago, but wasn’t initially sure whether it was legit and here for the long term. And I thought the free share offer was, frankly, too good to be true. However, my own experiences have been entirely positive. My original free share in the Ford Motor Company was credited the next business day as promised and I received an email notifying me about it.

I can log in to my Trading 212 account any time to see how my Ford share is doing. I have also collected a few other shares from referrals as well. These include a share in AMD (the semiconductor company), which is currently worth £117.92, and one in Nike, which is worth £105.83. I still have my original Ford Motor Company share and it has risen in value to £8.16. I also received an annual dividend payment from them a while ago. I haven’t sold any of my free shares yet but could of course do so any time I choose. I am not in any rush, as Trading 212 do not impose any platform or inactivity fees.

Although in this post I have focused on the free share offer, Trading 212 is worth considering as a share-dealing platform too. In particular, the fact that it’s fee-free and commission-free means it is well suited for people who are dipping a toe in stocks and shares investment for the first time. By contrast, the dealing fees and commissions charged by some other share-trading platforms can make small share purchases prohibitively expensive. This review by Money Savvy Daddy looks at the pros and cons of Trading 212 as a share-dealing platform in a bit more detail.

It’s also worth bearing in mind that Trading 212 pays interest on any uninvested funds in your ISA or Invest account, currently at a rate of 5.1% AER. You can also make money allowing your shares to be lent out. Rates on offer for this vary according to investor demand, with the process handled automatically by Trading 212 once authorized. You can read more about share lending on Trading 212, including the risks and safeguards provided, here.

In conclusion, I hope this post has inspired you to consider registering with Trading 212 to claim your free share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And, as always, any other comments or questions are very welcome too.

Don’t forget, the current free share offer ends on Wednesday 6 November 2024.

Disclosure: The links in this post include my referral code. If you click through and register as described above, I will receive a free share (as will you). Please note also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss (although not in the case of free shares, obviously).

This is an update of my original post about this special offer.

If you enjoyed this post, please link to it on your own blog or social media:

For older people in particular, heating bills can be among their biggest expenses. And it’s especially important for older people to keep warm, as getting chilled can lower your body’s resistance to infection and – in the worst cases – lead to hypothermia.

In addition, as you doubtless know, gas and electricity bills have gone up considerably in the last year or two. And many older people will no longer get Winter Fuel Payments, as the new government have opted to restrict this to just the very poorest pensioners (those in receipt of Pension Credit).

So today I thought I’d set out some ways you may be able to save money on your heating and energy bills. Following these tips could save you hundreds of pounds in the months and years ahead.

Switch Energy Supplier

It’s important to check regularly whether you could save money by switching to a different supplier and/or tariff. The quick and easy way of doing this is via a price comparison website. There are a number of these available, including GoCompare and USwitch.

Just visit the comparison site and enter a few details, including your current supplier and tariff and how much you spend on gas and electricity in the course of a year (it doesn’t have to be exact). The site will then display the best deals currently open to you and how much you might be able to save by switching to them. In most cases you can also start the switching process by clicking on the relevant link. Before you do, though, it’s worth checking on cashback sites like Quidco and Top Cashback, as some energy companies pay cashback via these sites to people switching their supply to them.

If you are one of the 1.1 million households who use oil for heating, you can save money by shopping around for suppliers too. Check out the oil price comparison service BoilerJuice. Type in your postcode and how many litres of heating oil you’re looking to buy, and BoilerJuice will show you quotes from suppliers covering your area.

Switching energy suppliers is generally quick and easy, and can save you hundreds of pounds a year at a stroke. In these challenging times, it should be high on your list of potential money-saving strategies this winter.

Special Offer! If you switch to EDF Energy via my link, you can get a FREE £50 credited to your energy account. Terms and conditions apply. For more info, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 [referral link].

Get Financial Help

If you’re in certain priority groups, you may be able to get cash payments to help offset your energy bills.

Winter Fuel Payment is a one-off annual payment of £200 to £300 which was previously made to everyone over state pension age. Unfortunately, as mentioned above, the new government have decided to limit this benefit to the very poorest pensioners who are in receipt of pension credit (or certain other welfare benefits). To qualify this winter, you must have been born on or before 23 September 1958 and been in receipt of a qualifying benefit for at least one day during the week of 16 to 22 September 2024 (the ‘qualifying week’). If that applies to you, this money should be paid automatically, but you can phone the Winter Fuel Payment Centre on 0800 731 0160 if you haven’t received the payment before and need to claim.

If you think you might be eligible for Pension Credit but are not currently receiving it, it’s now more important than ever to apply. Not only will it qualify you to receive Winter Fuel Payments, it can act as a gateway to a range of other discounts and benefits as well. See my blog post about applying for Pension Credit for more information.

In addition, those on certain welfare benefits (including Pension Credit, Income Support and Universal Credit) may be eligible for Cold Weather Payments. This is £25 for any period of seven consecutive days when temperatures fall below zero. More information can be found on this page of the government website.

You may also be eligible for £150 off your energy bill under the Warm Home Discount Scheme. This is run by some (not all) of the energy companies. If you get the Guaranteed Credit element of Pension Credit you will qualify automatically. But if you’re on a low income and meet the energy supplier’s other criteria, you may also qualify. Contact your supplier directly for more information. The large energy companies such as EDF and British Gas all operate this scheme, but some of the smaller ones don’t. The Warm Home DIscount scheme for 2024/25 opens in October 2024. More information can be found on the official website.

Finally, if you’re on a very low income, you may qualify for help from the Household Support Fund: This is money provided to councils by the government to assist pensioners and others on very low incomes. You will need to contact your local council to find out if you’re eligible.

More Top Tips

Here are some more ways you may be able to save money on your heating and energy bills.

Have your boiler serviced regularly, to ensure it is operating at peak efficiency.

If you have an old boiler that keeps breaking down, the time may have come to replace it. The Energy Saving Trust say that you could save up to up to 40 percent on your gas bill by installing a new ‘A’ rated condensing boiler with a programmer, room thermostat and thermostatic radiator controls.

Upgrading your insulation can also cut bills by reducing the amount of heat going to waste. Depending on your circumstances, you may be able to get a free boiler and/or insulation under the government’s Energy Company Obligation (ECO) scheme. You can apply for this via your energy company. Even if you’re not on a low income, you may be able to get a discount on home insulation, so it’s worth checking to see what’s available.

If your radiators aren’t heating up properly at the top, you may need to bleed them to release air in the pipes. Depending on the radiator, you may need a special key to do this or a flat-bladed screwdriver.

Turn down your thermostat by one degree - this can reduce your heating bill by up to 10%.

Ensure you don’t put furniture right in front of radiators, as this can block heat from entering the room.

Replace old light-bulbs with new energy-saving bulbs. The latest LED bulbs are just as bright as old incandescent bulbs and use a tenth of the energy. They last longer too.

Exclude draughts with heavy curtains and draught excluders by doors.

Turn off heaters in rooms you aren’t using and close the doors to keep heat in.

Place reflective foil behind radiators on exterior walls to bounce heat back into the room.

Don’t leave electrical appliances on standby.

Wash clothes at 30 degrees and try to avoid using tumble driers. Hang washing outside whenever possible or place it over an airer.

Consider investing in a smart thermostat system such as Nest or Hive. This will give you precise, automated control over your heating system, allowing you to use just as much energy as you need and no more. See this Money Supermarket article for more information.

If your funds are limited and you have or develop a disability you may be able to get a Disabled Facilities Grant (DFG) from your local authority to pay for adaptations such as stairlifts.

By taking these steps you should be able to cut your heating and energy bills significantly this winter.

If you have any comments or questions about this post, as always, please do leave them below.

This is a fully updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, Age UK, The Stroke Association, PDSA, and many others. Free Wills Month happens twice a year, in March and October.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I have talked about the importance of creating a will and why you should get it done by a properly qualified solicitor previously on PAS. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website during October and fill in your details. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s best to apply as soon as possible to avoid disappointment.

Free Wills Month October 2024 starts officially on Tuesday 1st October 2024 but you can sign up on the FWM website to be notified when when the campaign starts in your area.

If you have any comments or questions about this subject, as ever, please do post them below.

Note: This is a revised and updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the price of stamps is rising again on Monday 7 October 2024. That is the second price rise this year, after they also went up in April.

On this occasion a standard first class stamp is going up from £1.35 to £1.65, an inflation-busting 22%. The price of sending a large letter is going up even more, from £2.10 to £2.60. That’s an increase of 50p or 24%.

One bit of good news is that the price of sending a standard or large letter by second class post is not increasing this time. That remains at 85p and £1.55 respectively.

Standard letters can weigh up to 100g and measure a maximum of 24cm x 16.5cm x 5mm. Large letters can measure 35.3cm x 25cm x 2.5cm but still have to weigh under 100g. If they weight over 100g, higher rates apply, and if they weigh over 750g they have to go at parcel rates.

The cost of many of Royal Mail’s ‘Signed For’, ‘Special Delivery Guaranteed’ and ‘Tracked’ services will also rise from 7 October, as will the price of sending parcels first and second class. You can see a full list of prices by clicking here (PDF).

Saving Money on Stamps

So is there anything you can do to mitigate the impact of the latest price rises?

Well, my number one recommendation is to stock up now while stamps are still at the old price. Standard and large-letter stamps don’t have values printed on them and will still be valid after the October price rise comes in. If you can afford to buy (say) 100 standard first-class stamps and 100 large letter first class stamps, that will save you an impressive £80 in total.

The best bet for buying stamps is – of course – your local post office. If you don’t have one near at hand, however, you can also buy in bulk from The Royal Mail Shop (minimum order £50 for free delivery)..

Amazon also sell postage stamps, though costs vary and when I checked some prices were significantly higher than at post offices. But they may be worth a look, especially if you are an Amazon Prime member.

Another option you could consider is the online auction site eBay (search for “new UK stamps”). There can be good savings to be made here, but check reviews and ratings carefully and be wary of offers that are clearly too good to be true.

For the sake of completeness, though, I thought I should publish (or more accurately republish) a post about matched betting. This is something I did for several years and earned about £3,000 (tax-free!) from. I am not doing it as much these days, for reasons I’ll explain below. But if you’ve never done it before, I do still recommend matched betting as a way of making some quick tax-free cash.

So Why Am I Doing Less?

There are two main reasons. The first is that since I started matched betting around six years ago I have had my account restricted (or gubbed, as we say in the business) by many online bookmakers. That obviously makes it harder to take advantage of the offers matched bettors need in order to generate their guaranteed profits.

My second reason is that during the pandemic, with many sporting events cancelled, there were far fewer matched betting opportunities. Thankfully that is behind us now and normal life (more or less) has resumed. Even so, the bookies are more cautious than they once were, and offers are somewhat thinner on the ground.

I still do a small amount of matched betting but keep it very low-key. There are only a few good online bookmakers I can now use, and I’d like to go on flying under their radar for as long as possible before they ban me!

If you are new to matched betting – or have let it fall by the wayside – then as stated above I do still recommend it. But be aware that it may not be quite as profitable as it was pre-Covid.

But let’s start with a recap of the basics…

What is Matched Betting?

Matched betting is a method for making risk-free profits by taking advantage of offers made by online bookmakers.

The best offers are those made to attract new clients. Here’s an example. The bookmakers Sky Bet offer £30 in free bets (3 x £10) for new online customers. To get this, you have to open an account with them and deposit a minimum of £5. You then have to place a minimum 5p bet at odds of evens (2.0) or better. Once you have done this, Sky Bet will immediately credit you with £30 worth of free bets.

So how do you turn this into a guaranteed profit? Well, that’s the clever bit. You make use of a website called an exchange (Smarkets and Betfair are two of the better known). These sites allow anyone to lay a bet (i.e. bet that the outcome in question won’t happen). By backing with a bookmaker and laying the same bet at an exchange you can ensure that however the event pans out, you will only make a small loss or occasionally a tiny profit (depending on the odds available).

With a normal bet this is obviously of limited value, as the two bets more or less cancel each other out. But when your first bet qualifies you for a second (and in Sky Bet’s case much larger) free bet, it suddenly becomes a lot more interesting. Here’s an example…

Let’s say Wolverhampton Wanderers are about to play Spurs in the Premier League. You can back Wolves to win with Sky Bet at 4.75 (15/4 in the more traditional but less useful fractional style) and lay them with Smarkets at 4.80. If you put £5 on Wolves with Sky Bet and at the same time lay Wolves to the appropriate stakes (something I’ll come to shortly) you can ensure that whether they do or don’t win, your net loss will be just 13p (allowing for Smarkets’ standard 2% commission charge). The lay bet covers you for the draw as well, as in effect you are betting that Wolves won’t win – so if Spurs win or the match ends in a draw, the lay bet will pay out.

But now, because you are a new member, Sky Bet will give you £30 worth of free bets. You can back and lay these again to generate a guaranteed profit. For the sake of simplicity let’s say you use the same market, Wolves v. Spurs, although you certainly don’t have to. At the odds mentioned, and backing to the correct stakes, if you use all three £10 free bets you can guarantee yourself a net profit of £23.05 however the match pans out. Subtract the 13p loss from your qualifying bet, and once the dust has settled you will have made a risk-free (and tax-free) £22.92. If your bet loses with the bookie, your profit will be in the exchange (remember, this is a free bet so it hasn’t cost you anything). If the bet wins at the bookie, you will lose money at the exchange, but your winnings with the bookie will exceed this, giving you the same net profit either way.

Those are the bare bones of matched betting. Of course, there’s more to it than that, but most matched betting opportunities boil down to this. You place an initial qualifying bet and lay it to ensure (at worst) a small net loss, and then back and lay the free bet you receive to make yourself a guaranteed profit.

One or two people have asked me whether matched betting is legal. The answer is a clear yes. It’s fair to say the bookies don’t like it, though. And if they suspect you are doing it, they may close or limit your account. As mentioned above, this is called ‘gubbing’ and it is an occupational hazard for matched bettors. As a matter of interest, I had to change the example used at the start of an earlier version of this blog post after being threatened with legal action by the bookmaker in question.

How Do You Get Started?

You can, of course, do all this yourself, researching opportunities and comparing odds to find the most profitable matched betting opportunities. When you are starting out, though – and especially if you are new to online betting – it obviously helps a lot to get some instruction and guidance.

Fortunately there are some excellent online services that will do all this for you and provide step-by-step instructions. You can apply these even if you have never placed a bet in your life before. Here’s the service I recommend for beginners to matched betting…

Outplayed

Outplayed (formerly Profit Accumulator) is a dedicated matched betting website. You can get a 7-day free trial which gives you access to over 60 welcome offers of the type mentioned above. If you wish to continue, you can then pay a fee (currently £39.95 a month) to become a ‘Platinum’ member and get access to Outplayed’s full range of betting offers and services.

As well as detailed instructions on offers, Outplayed also provide various online tools you can use. Their oddsmatcher, for example, helps you find markets where the back and lay odds are as close as possible, so you can minimize your losses on qualifying bets and maximize the value of your free bets. They also have calculators where you enter the back and lay odds and how much you want to bet at the bookmaker. The calculator then reveals how much you need to lay at the exchange to guarantee a set profit (or qualifying loss) with either outcome.

A further advantage of joining Outplayed is that you get access to the members-only community forum, where you can get any questions you may have answered by more experienced members and/or the Outplayed team.

For more information about Outplayed and its different membership levels, just click through this link [affiliate].

If you are at all sceptical about the Outplayed service, you might like to check out the reviews on the independent Trust Pilot website. They currently average 4.7 out of 5 stars, with 89% of respondents awarding them a five star (‘Excellent’) rating. That is among the highest average ratings I can recall seeing on Trust Pilot.

What Happens When You’ve Exhausted the Welcome Offers?

This was something I wondered about before I started, and I know other people do as well.

First of all, it will take you quite a long time to work through all the offers on the Outplayed website. Not all are as simple and straightforward as the Sky Bet offer mentioned above, but nonetheless if you follow the step-by-step instructions they can all generate a healthy profit for you.

After that, you can move on to ‘reload’ offers. These are offers made by bookmakers for existing members to encourage them to keep coming back and using their service. Reload offers work in a wide range of ways. Some provide a guaranteed profit if you apply them correctly, while others may sometimes make a small qualifying loss but other times produce a much larger profit, generating a good net profit overall. Reload offers are also listed on the Outplayed website and updated every day.

Is Matched Betting for Everyone?

In principle anyone can do matched betting, but it is probably more suitable for some people than others. In particular, it will help if you have a small amount of capital to get started – at least £50, preferably £100 or more.

If you have less you can still do it, but it will take longer to build up your earnings. Remember that you will need money to fund your qualifying bets at the bookmaker sites and also your exchange account. You don’t lose this money – it simply moves between bookie and exchange according to how events pan out – and you can always withdraw it if required. But to operate as a matched bettor you do need to have some ‘working capital’.

Another requirement to make a success of matched betting is that you need to be organized and methodical. Matched betting is not difficult once you grasp the basic concept, but if you make a mistake it is possible to lose money doing it. Initially at least it’s important to take it slowly and steadily and follow the instructions on Outplayed (if you have signed up with them) to the letter. It helps to be reasonably numerate as well, although the actual calculations are done for you by the oddsmatching tool and calculators.

And finally, if you think you might get drawn in to gambling through matched betting, you may be better giving it a miss. This applies especially if you have ever had a gambling problem in the past. To emphasize again, matched betting is NOT gambling if you do it properly and follow the correct procedures. But if you are tempted to go off-piste and start placing random bets, the likelihood is that you WILL lose money overall.

Final Thoughts

If you are looking for a tax-free sideline earning opportunity, matched betting can certainly fit the bill. Done properly it is risk free, and (as mentioned earlier) I have made around £3,000 from it myself.

For reasons discussed in this blog post I don’t recommend matched betting as a substitute for a full-time job. In these challenging times, however, if you need another tax-free string to your money-making bow, it can certainly perform that role. But be aware that the first few months are likely to be the most profitable. After that, as you run out of welcome offers (and are perhaps ‘gubbed’ by some bookies) it will get harder.

As always, if you have any comments or questions about this post or matched betting more generally, please do leave them below.

This is a fully updated version of an earlier post.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

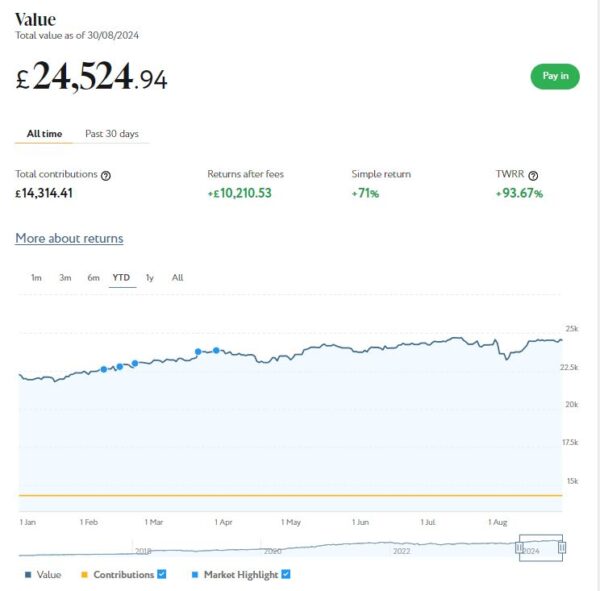

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,525 (rounded up). Last month it stood at £24,237, so that is an increase of £288.

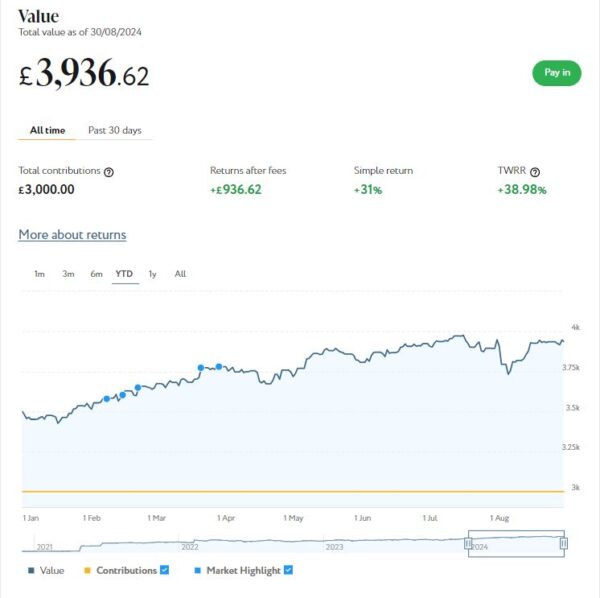

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,937 compared with £3,895 a month ago, a rise of £42. Here is a screen capture showing performance over the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £772 compared with £769 last month, a small rise of £3.

As you can see from the charts, August was generally a decent month for my Nutmeg investments, despite a hiccup early in the month. Their overall value has risen by £333 or 1.16% since the start of August. They are also up by £2,919 or 11.08% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024 and you have a full £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £200.41 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 6 are breaking even, and the remaining 17 are showing losses. My portfolio of 33 properties is currently showing a net decrease in value of £43.69, meaning that overall (rental income minus capital value decrease) I am up by £156.72. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

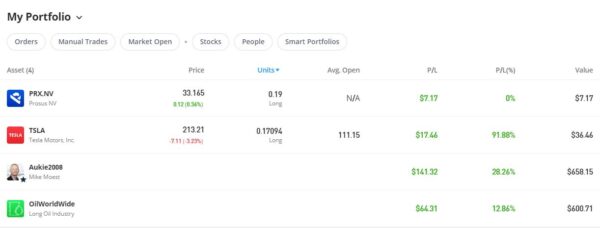

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.27 an overall increase of $281.01 or 27.51%.

As you can see, my Oil WorldWide investment is showing 12.85% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

You might also notice that I have a small holding in Prosus NV, a Dutch internet group. To be honest I don’t understand how I acquired this, but it may be connected to my copy trading investment with MIke Moest (who is Dutch). In any event, I am happy to have it in my portfolio as well!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in August on the excellent Mouthy Money website. The first is Win Fame and (Maybe) Fortune as a TV Quiz Show Contestant. This can be an exciting and occasionally lucrative pastime. I revealed how to find opportunities and apply for them. I also explained how the auditioning process works, and offered some tips on how to boost your chances of success.

Also in August I revealed my Ten Top Tips for Working From Home. This is something I’ve done for over 30 years now, so in this article I set out my top ten tips based on my experience. If you have recently started working from home, or expect to do so in future, you may find this article helpful.

Finally, I wrote an article titled How Understanding Cognitive Dissonance Theory Can Help Us Manage Our Finances Better. This article drew on my experiences of studying psychology back in the 1970s. Developed by psychologist Leon Festinger in 1957, cognitive dissonance theory explores the discomfort we experience when we simultaneously hold conflicting beliefs or attitudes. By understanding this, we can gain insights into our financial behaviour, helping us make more informed decisions and achieve better financial results.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in August, I particularly enjoyed How to Save Money on Your Home Removal by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in August. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In these challenging times, we all need to ensure our savings stretch as far as possible. So in How to Maximize Your Savings Interest l set out a range of tax-free allowances you can use to help do this. They include the Personal Savings Allowance (PSA), Starting Rate for Savings, Individual Savings Accounts (ISAs), and various others.

I also published How to Win Cash and Prizes in Online Competitions. This can be another tax-free way to boost your finances! In this post I revealed how to find online competitions to enter, why you should set up dedicated ‘comping’ accounts, how to identify potential scams, and more. Good luck if you decide to try this 🤞

As we all know Labour achieved a landslide victory in the general election, and it appears that austerity measures are on the way now. So in How to Reduce the Impact of Tax Rises in Rachel Reeves’ First Budget, I set out some recommended steps to try to protect your finances in the months (and years) ahead. The Chancellor’s first budget is scheduled for 30th October 2024, with tax rises and cuts to public services widely anticipated.

Finally, in August I published What Alternatives Are There to Heat Pumps? The government are currently pushing heat pumps hard in their frantic quest to achieve Net Zero. For a range of reasons, however, they are not suitable for every property. And even if your home might theoretically be suitable, there are good reasons you might not want one (discussed a while ago in this Mouthy Money article). So in this post I set out some possible alternatives you might like to consider instead.

Next, a few odds and ends. I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you decide to invest, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Speaking of energy, a quick reminder that if you switch to EDF via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight the decision by the new Labour government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you have any source of income apart from the state pension, even a tiny one, the chances are you won’t be eligible. I do therefore recommend writing to your MP and asking for this Draconian decision to be reversed. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK. The latter is up to almost half a million signatures now.

That’s all for now. If you have any comments or queries about this update, as ever, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: