Today I’m pleased to bring you a guest post from my friend and near-neighbour Sally Jenkins, a successful published fiction and non-fiction author (check out her latest novel Out of Control – a later-life romance perfect for summer holiday reading!).

Many older people (in particular) harbour an ambition to write a book and make money from it. If that includes you, I hope you will find Sally’s article of interest. In it she sets out the main options for getting your book published, and shares some valuable resources she has found.

Over to Sally then…

Everyone has at least one book in them, or so the saying goes. It might be a thriller, a memoir, a collection of poems or short stories, a ‘how-to’ non-fiction manual or something completely different. Finishing that manuscript is a laudable achievement in itself but don’t stop there. It takes guts to send any literary work out into the public arena; however, doing so can lead to an additional passive income stream in the form of royalties that continue to hit your bank account long after you’ve finished writing.

There are three main routes to publication that you might like to consider:

Traditional Publishing

Traditional publishers come in all shapes and sizes, from the giants like Penguin and Hachette to far smaller, less well-known companies who publish in e-book format only.

Traditional publishers bear all the costs of publishing a book, meaning there is no financial risk for the author. These costs may include editing, proofreading, cover design, marketing and the printing of physical copies. The author contributes nothing to these costs and receives a small royalty for each copy of the book sold.

The competition to be signed by a traditional publisher is fierce and only a very small number of authors are taken on. The larger companies will only accept manuscript submissions via a literary agent but it is possible for authors to submit directly to many of the small publishing houses. There is nothing to lose by trying this traditional route but be prepared to develop a thick skin to deal with the probable rejections. A good place to start is an up-to-date copy of the Writers’ and Artists’ Yearbook, which contains a comprehensive list of publishers and literary agents.

Partnership Publishing

In the partnership publishing model, the publisher and the author share the financial risk of publishing the book. This means the author will be asked to make a financial contribution towards the publishing costs. What proportion and how much this means in monetary terms will vary from company to company, so it’s worth approaching more than one partnership publisher and requesting explicit information about their offering. In return for contributing to the publishing costs, the author can expect to receive a higher percentage of royalty payments than under the traditional model.

However, care is needed when choosing a partnership company to work with – there are many rogue or ‘vanity’ publishers out there who will publish anything and charge a lot of money for very little service. Ensure that the company you choose has a manuscript selection process – even if this means you might face rejection as in the traditional model. A true partnership publisher will only publish books that it thinks have merit and will sell. Even so, there is no guarantee that you will recoup all or any of your publishing costs via royalties. Do not spend more than you can afford to lose.

Authors who self-publish carry all the financial risk themselves but retain all the royalties (bar the amount taken by distribution platforms such as Amazon). It is possible to self-publish on Amazon at no cost or you might choose to spend hundreds of pounds depending on what services you buy in. The main services requiring financial outlay will be:

Cover Design – don’t attempt this yourself unless you are a graphic designer with a knowledge of the book covers currently selling in your genre. An amateur cover design will be obvious and off-putting to potential readers.

Editing – a novel (particularly a first novel) may benefit from a full structural edit. This will advise on plot, character development, pace etc. You might also want to consider a sentence level copyedit and/or proofread.

Formatting – some authors pay for this but, with a little patience, anyone who can use Microsoft Word can do this themselves.

Printing – there is no need to pay for a print run of books and hold them in stock.

Amazon (and other companies) use print-on-demand (POD) technology. This means that when someone orders a copy of your book it is printed individually and sent direct to the customer. Authors can also order copies at a reduced rate to sell direct to friends, family or the public at large.

The Alliance of Independent Authors has a directory of reputable editors, cover designers, proofreaders, etc. The directory also lists companies who can offer a complete self-publishing service for authors who don’t want to do any of the leg work – but this can be very expensive. As with partnership publishing, never spend more than you can afford to lose.

If you would like to know more about low-cost self-publishing via Amazon, the e-book Kindle Direct Publishing for Absolute Beginners (pictured, left) offers a good introduction. If you don’t currently read on Kindle, download the free Kindle app to your laptop, tablet or smartphone.

Whichever publishing route you choose, enjoy the journey and the royalties!

Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher Choc Lit (part of Joffe Books). She has also had a novel published in partnership with The Book Guild and has self-published several books via Amazon KDP. When not at the keyboard, she feeds her addiction to words by working part-time in her local library and running two reading groups. Sally can also be found walking, church-bell ringing and enjoying shavasana in her yoga class. Follow her writing blog at https://sally-jenkins.com/.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest monthly update about my investments (slightly earlier than usual due to other commitments). You can read my March 2025 Investments Update here if you like.

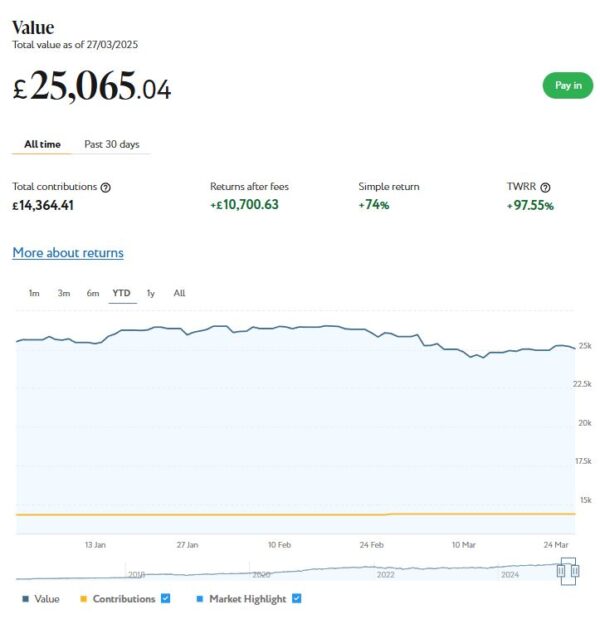

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,065. Last month it stood at £25,850, so that is a drop of £785.

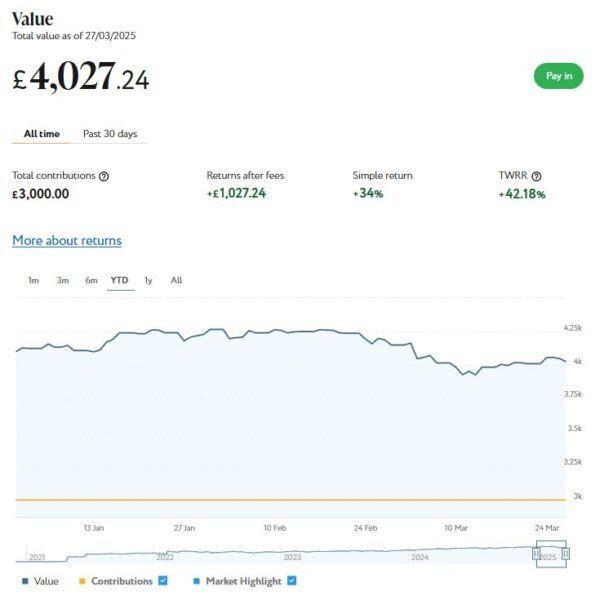

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,027 compared with £4,151 a month ago, a fall of £124. Here is a screen capture showing performance for the year to date.

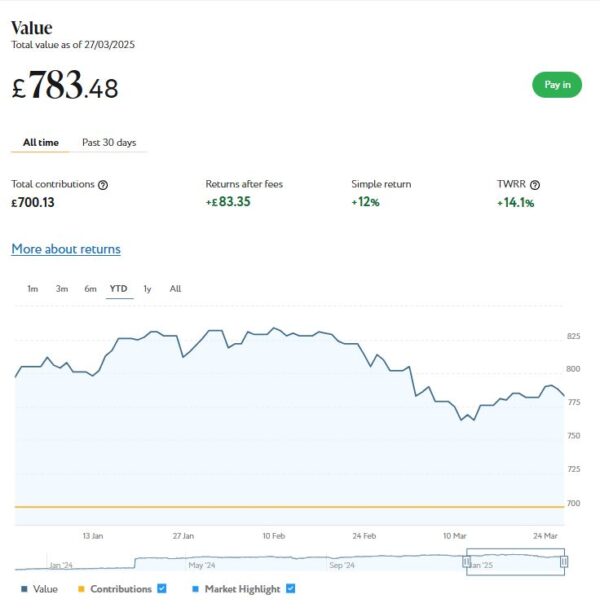

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £783 compared with £803 last month, a fall of £20.

As you can see, March has been another disappointing month for my Nutmeg investments. Overall I am down by £929. This is mostly due to the continuing instability in world markets, caused by the the trade tariffs imposed by US President Donald Trump and other economic and social factors.

Nonetheless, the value of my Nutmeg investments is still up £1,477 in the last twelve months. And their value has increased by £3,559 or 13.52% since the start of January 2024. So the recent falls do need to be taken in context. Ups and downs are always to be expected with stock market investments, and over time they tend to even themselves out. In general the worst thing you can do is panic and sell up when downturns occur, as you are then crystallizing your losses. Indeed, I am considering topping up some of my investments now while values are depressed. That’s just how I’m thinking, of course, and doesn’t constitute investment advice!

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £238.70 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 15 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 19 are showing losses. My portfolio of 36 properties is currently showing a net decrease in value of £52.78, meaning that overall (rental income minus capital value decrease) I am up by £185.92. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

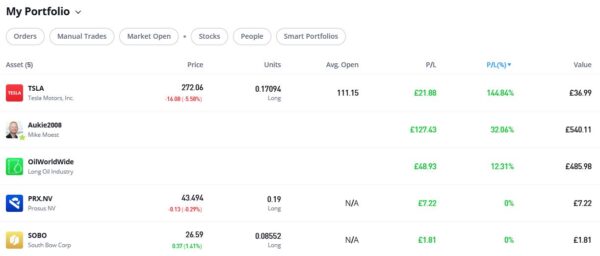

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,072.80, an overall increase of £184.44 or 20.76%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is currently showing a profit of 12.31%. That’s a welcome improvement since the portfolio was rebalanced by eToro. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 32.06% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 144.84%. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

Moving on, as I said last time, I am no longer writing for the Mouthy Money website, as they have decided to take their content creation in-house. From a personal perspective I am obviously disappointed about this, but I had a good run with them and wish them every success going forward. You can still read all the articles I contributed to Mouthy Money over the years by visiting my profile page on the website. How long they will keep this in place I really can’t say!

I also published several posts on Pounds and Sense in March. Some are no longer relevant, but I have listed the others below.

In Beat the Postage Stamp Price Rise!, I pointed out that stamp prices are rising again on 7th April 2025. This will actually be the the SIXTH rise in the price of first class stamps in just three years. See what prices are going up, along with my recommendations for mitigating the effects of the increases.

And in From Saving to Spending – The Retirement Mindset Shift I discussed a subject that has been on my mind recently as I enter my 70th year. This is how to negotiate the mindset shirt from saving to spending in retirement, and how (hopefully) to get the balance right.

The Pros and Cons of Investing for Dividends discusses a strategy that has been growing in popularity with older investors particularly. Dividend investing offers the potential for generating income combined with capital appreciation. In this post I examine the pros and cons of a dividend investing strategy and set out a few tips and guidelines for those new to this.

Finally, in Spotlight: The Mintos P2P European Investing Platform I take a closer look at Mintos, Europe’s largest P2P investment platform. As well as the ability to generate above-average returns by investing in loans to businesses world-wide, they have added new diversification options, including bonds, ETFs and real estate. And until the end of April they have a bonus offer for anyone investing €1,500 or above on the platform. In my blog post I look at the pros and cons of investing with Mintos and provide more details about their April bonus offer.

One other thing is that we’re currently just over a week away from the end of the 2024/25 financial year. If you still haven’t used all of your 2024/25 £20,000 tax-free ISA allowance, you have just a few days left before it’s gone. It is more important than ever to use all your tax-free allowances while you can, as the government looks set to reduce some of these allowances later in the year. See my recent blog post for more information.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. For the time being anyway, Twitter/X will remain my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at Mintos, a European P2P crowdlending platform based in Latvia but open to investors in the UK.

Since its launch in 2015 Mintos has grown to become Europe’s largest P2P investment platform, with over half a million registered users. They offer access to loans (and other investment types) from multiple countries, regions and sectors. While Mintos is not directly regulated in the UK, UK investors can still use Mintos to diversify their investment portfolios.

With Mintos, your money is invested in loans to businesses and private individuals arranged by Mintos’s partner lending companies around the world. Mintos act as intermediaries between lenders and borrowers. They aim to ensure that both groups act responsibly and loans are repaid in a timely way.

Currently Mintos offer the opportunity to invest commission-free in loans, bonds, ETFs and real estate (the latter offering the potential for both income and capital appreciation). Opening and operating an account is free of charge, with personal support available in ten languages.

You can begin investing with just €50 (around £42). Since 2015 investors with Mintos have earned an average 11.9% return per year. Of course, past performance is no guarantee of how any investment platform will do in future.

Mintos generally has good reviews on the popular Trust Pilot website, with an average score of 4.1 out of 5 (‘Great’) and 54% five-star ratings. It does also have a few one- and two-star reviews. These are for various things, including issues with the website and complaints about the KYC (‘Know Your Customer’) checks that Mintos is legally obliged to conduct. There are also a few complaints about people losing money on investments in Russia after sanctions were imposed. To be fair this is entirely outside Mintos’s control.

Mintos is licensed and supervised by Latvijas Banka, the central bank of Latvia, and a member of the Latvian national Investor Compensation Scheme. If Mintos fails to provide investment services, retail investors are entitled to compensation of 90% of the irrevocable loss resulting from the non-provision, up to a limit of €20,000. This does not, however, provide protection in the event of poor performance of the underlying loans or investor default.

In addition, as is generally the case with crowdlending/P2P platforms, your assets are held quite separately from Mintos’s assets.

Here are some pros and cons to investing with Mintos.

Pros of Investing with Mintos

Diversification Opportunities

Mintos offers a wide range of loan types, including personal loans, business loans, agricultural loans, and mortgages.

Investors can diversify across different countries and lending companies to spread risk.

Other types of investment including bonds, real estate and ETFs are available too.

Potentially High Returns

In recent years Mintos has offered average annual returns on loans of around 10-12%.

Some loans come with buy-back guarantees, providing additional security in case of borrower default.

User-Friendly Platform

The platform provides automated investing tools and diversification settings.

Detailed loan information and transparency on loan originators help investors make informed decisions.

Secondary Market

Investors can buy and sell loans on the Mintos secondary market, providing liquidity if they wish to exit before a loan matures.

Cons of Investing with Mintos

Currency Risk

Many loans are denominated in non-GBP currencies, exposing UK investors to currency exchange risks.

Platform and Regulatory Risk

Mintos is regulated under the EU’s financial laws but it is not directly regulated by the UK Financial Conduct Authority (FCA). This may limit investor protection.

Credit and Default Risk

Loans issued through Mintos are subject to borrower defaults. Although buy-back guarantees mitigate this risk, guarantees are only as reliable as the lending companies that provide them.

Tax Considerations

UK investors must declare any income from Mintos to HMRC on their self-assessment tax returns and pay tax on this if they have exhausted their personal tax-free allowance. There are no automatic tax-free wrappers like ISAs or SIPPs available for Mintos investments.

Top Tips for UK Investors

Start Small: Begin with a small investment to understand how the platform works.

Diversify Broadly: Spread your investments across multiple loan originators, regions and loan types.

And Broader Still: Don’t overlook either the diversification opportunities presented by bonds, ETFs and real estate.

Monitor Currency Exchange Rates: Consider the potential impact of currency fluctuations on your returns.

Evaluate Loan Originators: Research the financial health and reputation of lending companies offering loans via Mintos.

Consider Investing via the Mintos Core ETF: This provides instant global diversification aligned with your risk tolerance and investment time-frame.

Closing Thoughts

Mintos can be an attractive platform for investors seeking to diversify their portfolios and potentially achieve higher returns through P2P lending. It’s important, however, to understand the associated risks, particularly around currency exposure and regulatory protection. By conducting thorough research and managing risk through diversification, Mintos can be a useful addition to a well-balanced portfolio.

If you’re looking for a hands-on investment experience with the potential for higher returns, Mintos may be worth exploring. However, cautious investors may prefer more traditional options within regulated UK markets. The lack of availability of tax-efficient wrappers such as ISAs may also be a consideration. Always ensure that any investments align with your financial goals and risk tolerance.

Special Bonus for New Investors!

Until 30 April 2025, if you click through any link to Mintos in this article and invest €1,500 or more in loans, bonds, ETFs or real estate, you can get a bonus of up to €200 paid into your account. Note that you will need to enter the promo code DIVERSIFY to qualify for this.

If you invest €5000, for example, in addition to the returns advertised (currently averaging 11.9% for loans), you will also receive a €50 bonus. Effectively that’s an extra 1% bonus. Remember, this special offer closes on 30 April 2025. Note that to qualify for the bonus you must not withdraw funds from your Mintos account until 31.July 2025. The bonus will then be paid into your Mintos account on 10 August.2025. For full details of the bonus offer, please click through to the Mintos website.

If you have any comments or questions, as always, please do leave them below.

Disclosure: I am not a registered financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and if in any doubt seek advice from a registered financial adviser before proceeding. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make an investment (or perform some other designated action) I may receive a commission for introducing you. This will not affect the product or service you receive or any charges you may pay. Note also that the special bonus referred to in this article is only available if you click through one of my links. It will not apply if you go to the Mintos website directly.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at investing for dividends. This is an increasingly popular strategy among investors seeking to generate passive income while potentially also growing their capital.

Dividend stocks can provide a steady income stream, but they also come with risks and considerations. So I’ll begin by looking at the pros and cons of this approach. I will set out some hints and tips for anyone who may be interested in getting started at dividend investing. I will also mention some established UK companies that have a reputation for paying regular dividends, and some online share-dealing platforms that may be suitable for anyone applying this strategy.

Let’s begin with some of the attractions of dividend investing, though…

Pros

Table of Contents

Regular Income Stream

One of the biggest benefits of dividend investing is receiving regular cash payments, typically every quarter or six months, though occasionally monthly. This can be particularly appealing for retirees or anyone seeking passive income.

Potential for Long-Term Growth

Many well-established companies that pay dividends also experience share price growth. Reinvesting dividends through a dividend reinvestment plan (DRIP) can compound returns over time.

Stability in Market Downturns

Dividend-paying companies are often large, well-established firms that can weather economic downturns better than smaller, high-growth companies. Investors may find these stocks less volatile.

Tax Efficiency for UK Investors

UK investors benefit from the £500 dividend allowance (as of 2024/25) before dividend income is taxed. Additionally, holding dividend stocks in an ISA (Individual Savings Account) or SIPP (Self-Invested Personal Pension) shields the income from tax altogether.

Indication of a Strong Business

Companies that consistently pay and grow dividends often have strong financials, stable earnings, and a track record of profitability. This can be a sign of a well-managed company.

Cons

Slower Growth Compared to High-Growth Stocks

Dividend stocks are typically in mature industries, meaning they may not offer the rapid price appreciation seen in high-growth technology or small-cap stocks.

Dividends Are Not Guaranteed

A company can cut or suspend its dividend payments if it faces financial trouble, as seen during economic crises. This can lead to both income loss and share price declines.

Dividend Tax for Higher Earners

If your dividend income exceeds the £500 tax-free allowance, you will pay 8.75% tax (basic rate), 33.75% (higher rate), or 39.35% (additional rate) on the excess amount. This reduces overall returns compared to capital gains, which have different tax rates.

Sector Concentration Risk

Many high-dividend stocks are concentrated in certain industries, such as utilities, oil, and consumer goods. This can limit diversification and expose investors to sector-specific risks.

Tips for Beginners

If you’re new to dividend investing and want to try it, here are a few tips and guidelines to get you started…

Look for Dividend Growth, Not Just High Yields – A high yield can be a red flag if unsustainable. Instead, focus on companies with a history of gradually increasing dividends over time.

Diversify Your Portfolio – Don’t put all your money into one or two high-dividend stocks. Consider spreading investments across different sectors.

Check the Dividend Cover Ratio – This metric (earnings per share divided by dividends per share) shows whether a company can afford its dividend. A ratio above 1.5 is generally considered safe.

Use Dividend Reinvestment – Reinvesting dividends can significantly increase long-term returns through compounding. Many brokers and online share-dealing platforms offer automatic reinvestment options.

Consider Dividend-Focused Funds – If picking individual stocks feels overwhelming, dividend ETFs or investment trusts like City of London Investment Trust (CTY) and Murray Income Trust (MUT) provide diversification and professional management.

Examples of Strong Dividend-Paying UK Companies

Here are some UK companies known for consistent dividend payments in recent years.

Unilever (ULVR) – A consumer goods giant with a strong dividend history and steady growth.

Legal & General (LGEN) – A leading financial services company offering an attractive dividend yield.

National Grid (NG) – A stable utility company known for reliable dividend payouts.

BP (BP) – A major oil company that has historically paid strong dividends, though with some fluctuations.

Diageo (DGE) – A global leader in alcoholic beverages with a track record of dividend growth.

Online Share Dealing Platforms

Here are three UK share dealing platforms that are well-suited for dividend investors looking for relatively low costs.

Interactive Investor (ii)

Flat-fee pricing model, which can be cost-effective for those with larger portfolios.

Monthly plans start from £4.99, including a Stocks & Shares ISA.

Offers one free trade per month, with additional trades at £5.99.

Free regular investing option for cost-effective reinvestment of dividends.

Each of these platforms has strengths depending on your investing style. Trading 212 (a personal favourite of mine) is great for beginners and low-cost investors; Interactive Investor suits those with larger portfolios; and IWeb is a solid, no-frills option for long-term dividend investors.

Closing Thoughts

Dividend investing can be a great way to generate passive income, but it requires careful stock selection and risk management.

By focusing on financially strong companies with sustainable dividends and using tax-efficient accounts, investors can make the most of this strategy.

If you’re looking for a regular income from your investments combined with the potential for long-term growth, dividend investments have the potential to play a valuable role in your investing portfolio..

See also this guest post by my colleague Lewys Lew on his personal approach to dividend investing. Although it was published a while ago, there are still some useful tips to be gleaned from it.

PLEASE NOTE: I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a subject that may affect many readers of this blog who have recently (or not so recently) retired. It’s certainly a concern that I’ve faced myself (discussed later in the article).

For decades, many of us save diligently for retirement, carefully managing our finances to ensure what we hope will be a comfortable future. But once we finally reach retirement, a surprising challenge can emerge: shifting from a saving mentality to a spending one.

This transition can be difficult, even stressful, leading to problems such as excessive frugality, missed opportunities for enjoyment and unnecessary financial anxiety. Understanding why this happens – and how to navigate it – can help retirees make the most of their ‘golden years’.

Why Can it be Hard to Spend in Retirement?

For most of our working lives, we are conditioned to save for the future. The importance of building a pension pot, maximizing savings and preparing for the unexpected is constantly emphasized. Over time, this mindset becomes deeply ingrained, making it hard to reverse once retirement begins.

Here are some key reasons why many retirees struggle with spending…

Fear of Running Out of Money – With no regular salary coming in, retirees often worry that their savings won’t last. This fear can be worsened by rising living costs, potential healthcare expenses, and uncertainty about how long they will need their money to last.

A Lifetime Habit of Frugality – Many people have spent decades budgeting carefully, avoiding unnecessary expenses and prioritizing financial security. Suddenly being told it’s ‘okay’ to start spending feels unnatural, even reckless.

Uncertainty About the Future – Unlike a working salary, which can be replenished, a pension pot or savings account feels (and generally is) finite. Economic uncertainty, stock market fluctuations and potential care costs make it difficult for retirees to gauge how much they can safely spend.

The Problems of Excessive Frugality

While being cautious with money is clearly advisable, being overly frugal can unnecessarily reduce quality of life. Some retirees deny themselves experiences, comforts and even essentials because they feel they ‘shouldn’t’ spend. Here are some reasons why this can be problematic…

Missed Opportunities – Retirement is meant to be enjoyed, yet some people avoid holidays, hobbies or social outings because they fear dipping into their savings.

Health and Well-being Risks – Reluctance to spend on home improvements, heating or even nutritious food can have serious consequences for health and safety.

Unnecessary Financial Stress – Constantly worrying about money can take a toll on our mental well-being, even when there are sufficient funds available.

Regret Later in Life – Some realize too late that they were overly cautious and could have enjoyed their retirement more. By the time they feel comfortable spending, they may no longer be fit and healthy enough to do so.

How to Develop a Healthy Spending Mindset

Making the shift from saver to spender requires a conscious effort, but is possible with the right approach. Here are some suggested guidelines to embrace the opportunities presented by retirement whilst still maintaining financial security…

Create a Retirement Spending Plan

Just as saving required a strategy, so too does spending. Work out a realistic budget that includes essentials, discretionary spending and an emergency fund. This can provide reassurance that spending on enjoyment is both affordable and sustainable.

Think of Your Savings as a Paycheque

Rather than seeing savings as a lump sum to be preserved, treat it like an income stream. Regular withdrawals – whether from a pension or other savings – can make spending feel more structured and less daunting.

Prioritize Experiences

Research shows that spending money on experiences rather than possessions leads to greater happiness. Travel, hobbies and social activities can provide fulfilment while keeping finances under control.

Reframe Money as a Tool for Happiness

Rather than viewing savings as something to hoard, retirees can shift their perspective to see money as a resource for a fulfilling and comfortable life. This change in mindset can help ease spending anxieties.

Consider Gradual Adjustments

If spending feels uncomfortable, starting small can help. For example, try increasing your leisure budget gradually or treating yourself to one extra luxury per month. Over time, this can help you feel more at ease with enjoying your wealth.

Take Financial Advice

A professional financial adviser can help retirees feel confident about how much they can afford to spend while ensuring their money lasts. Regular reviews of pensions and investments can provide reassurance (see My Experience, below).

Give Yourself Permission to Enjoy the Rewards of Saving

Remember why you saved in the first place – to have security and enjoyment in later life. A balanced approach ensures financial stability while allowing for a fulfilling retirement.

My Experience

I have been officially retired for several years now. I still do a bit of freelance work (and run this blog) but my freelance income has tapered off. I am fortunate to have some savings and investments, the bulk of which I acquired through inheritances (though some from money I saved over the years).

As regular readers will know, although I’m a money blogger with a particular interest in such matters, I do have a personal financial adviser myself (I talked about this a while ago in this article). His name is Mike, and in my recent annual review he gently suggested that I could afford to withdraw a bit more from my investments. Essentially, he told me that I wasn’t getting any younger (I’m 70 this year) and there would be no benefit to dying with a lot of money left in my account. In some ways I found this advice encouraging, in others a bit depressing!

I do accept the gist of Mike’s advice, though. Even though I’m basically in good health, none of us knows what the future may hold. So I have promised Mike that I will think about what he has said and consider whether to draw more from my investments, while still leaving enough to cover my possible health and care needs in future. Of course, without a functioning crystal ball this isn’t an easy task, especially with the very high cost of care in the UK. But it’s important to take a balanced view and ensure you aren’t depriving yourself unnecessarily now whilst still retaining sufficient funds in case circumstances change in future.

Closing Thoughts

As I said at the start, the shift from saving to spending can be one of the biggest psychological adjustments in retirement.

Retirement is meant to be enjoyed, but many retirees find themselves trapped in a frugality mindset that stops them fully embracing the opportunities presented by this stage of life.

While financial prudence is important, excessive caution can lead to missed opportunities and unnecessary sacrifice. By shifting perspectives, planning carefully and embracing the idea that money is there to be used and enjoyed, retirees can – hopefully – strike a balance between financial security and enjoying their hard-earned wealth.

As ever, I’d love to hear any views (or tips) from readers about walking the tightrope between preserving your savings and making the most of life while you can.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the price of stamps is rising again on Monday 7 April 2025. That will be the SIXTH rise in the price of first class stamps in just three years.

On this occasion a standard first class stamp is going up from £1.65 to £1.70, a 3% increase. The price of sending a large letter first class is going up by substantially more, from £2.60 to £3.15. That’s an increase of 55p or an inflation-busting 21%.

The price of sending a standard letter by second class post is increasing from 85p to 87p (a 2% rise), One small bit of good news is that the cost of sending a large letter second class is not rising and remains at £1.55.

Standard letters can weigh up to 100g and measure a maximum of 24cm x 16.5cm x 5mm. Large letters can measure 35.3cm x 25cm x 2.5cm but still have to weigh under 100g. If they weight over 100g, higher rates apply, and if they weigh over 750g they have to go at parcel rates.

The cost of many of Royal Mail’s ‘Signed For’, ‘Special Delivery Guaranteed’ and ‘Tracked’ services will also rise from 7 April, as will the price of sending parcels first and second class. You can see a full list of prices by clicking here (PDF).

Saving Money on Stamps

So is there anything you can do to mitigate the impact of the latest price rises?

Well, my number one recommendation is to stock up now while stamps are still at the old price. Standard and large-letter stamps don’t have values printed on them and will still be valid after the April price rise comes in. If you can afford to buy (say) 100 standard first-class stamps and 100 large letter first class stamps, that will save you an impressive £60 in total.

The best bet for buying stamps is – of course – your local post office. If you don’t have one near at hand, however, you can also buy in bulk from The Royal Mail Shop (minimum order £50 for free delivery)..

Amazon also sell postage stamps, though costs vary and when I checked some prices were significantly higher than at post offices. But they may be worth a look, especially if you are an Amazon Prime member.

Another option you could consider is the online auction site eBay. There can be good savings to be made here, but check reviews and ratings carefully and be wary of offers that are clearly too good to be true.

Remember, also, that older UK stamps without barcodes are no longer valid.

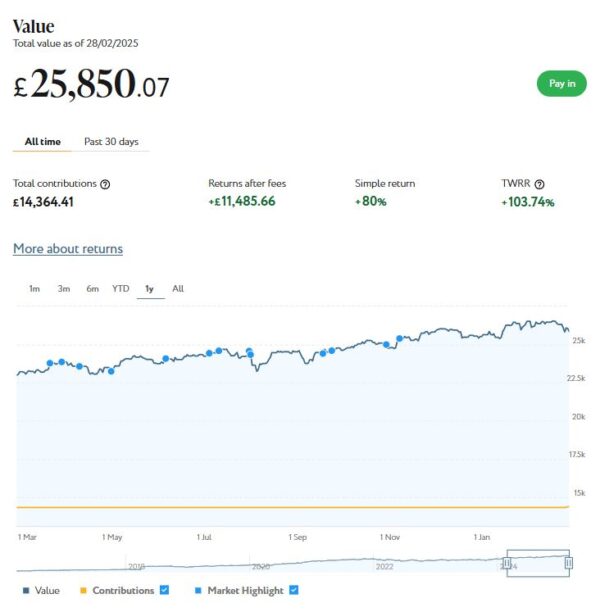

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last twelve months shows, my main Nutmeg portfolio is currently valued at £25,850. Last month it stood at £26,528, so that is a decrease of £678.

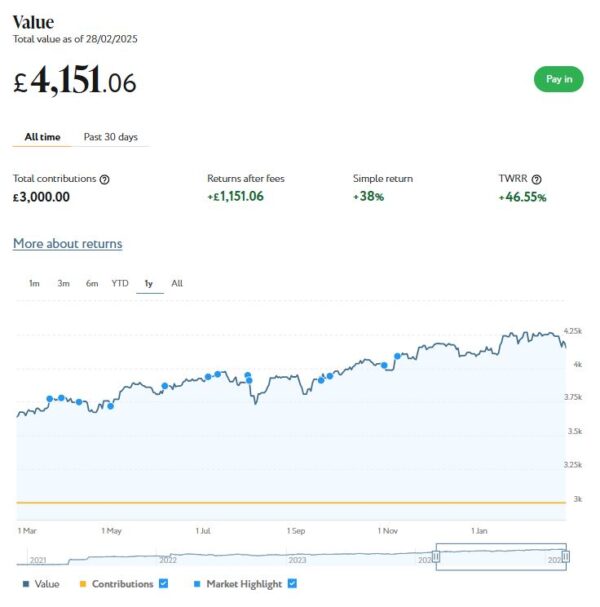

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,151 compared with £4,267 a month ago, a fall of £116. Here is a screen capture showing performance over the last twelve months.

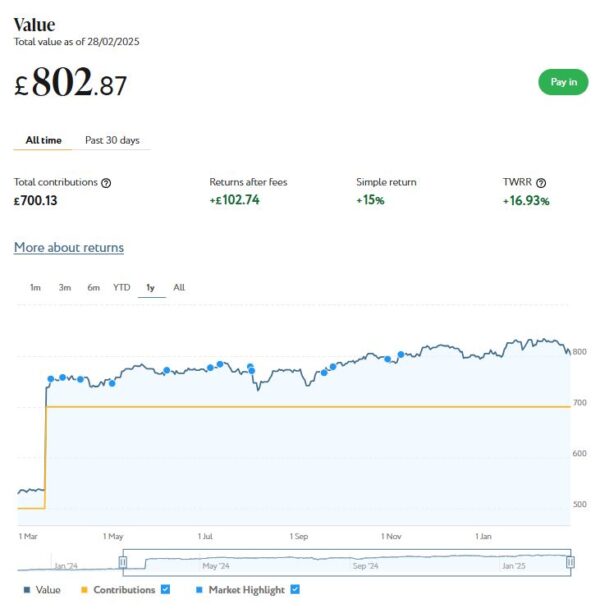

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the screen capture below, this portfolio is now worth £803 (rounded up) compared with £832 last month, a fall of £29.

As you can see, February has been a disappointing month for my Nutmeg investments. Overall I am down by £823. This is mostly due to a general decrease in share values in the second half of the month.

Nonetheless, the value of my Nutmeg investments is still up £390 since the start of the year. And their value has increased by £3,441 or 12.67% in the twelve months since the end of February 2024.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £235.31 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 17 of ‘my’ properties are showing gains, 1 is breaking even, and the remaining 19 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £50.24, meaning that overall (rental income minus capital value decrease) I am up by £185.07. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange/Housemartin here. You can also sign up for an account directly via this link [affiliate]. Bear in mind that, as from the current financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

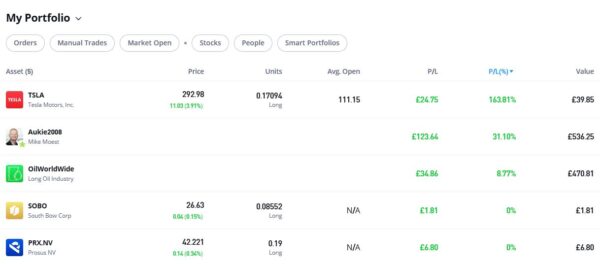

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,056.29, an overall increase of £167.93 or 18.90%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is showing a profit of 8.77%. That’s a small but nonetheless welcome improvement since the portfolio was rebalanced by eToro. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 31.18% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 163.81%. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

I had six more articles published in February on the excellent Mouthy Money website. The first is titled Travelling to Europe This Year? Here’s Why You Need a GHIC Card. If you’re unfamiliar with the GHIC or how it differs from the previous European Health Insurance Card (EHIC), this article reveals everything you need to know, from how to apply to why it’s so important for your travels.

Also in February Mouthy Money published How to Check Your Tax Code and Correct it if Necessary. Understanding your tax code and ensuring its accuracy can prevent you from overpaying (or underpaying) tax. In this article I explained everything you need in order to check and understand the code you have been allocated.

And in Make Extra Money Renting a Room I turned the spotlight on this traditional (but none the worse for that) method for making some extra money. If your circumstances allow it, letting a room in your home can be a great way of generating a sideline income. It will provide a regular, ongoing income stream, which could prove a lifeline in these financially challenging times. And you can choose between getting a full-time lodger or offering short-term lets. Better still, under the Rent a Room Scheme you can make up to £7,500 a year this way entirely tax free!

In What is the Trading Allowance and How Can You Profit From It? I discussed this valuable allowance for UK residents looking to earn extra income from trading or side hustles. Even if you have a full-time job already, under the Trading Allowance you can earn up to £1,000 a year without having to declare that income to the taxman or paying tax on it. Read my article for the full lowdown!

And in Could You Benefit From the Help to Save Scheme? I discussed this lesser-known government initiative which, if you’re eligible, can give your finances a valuable boost. The Help to Save scheme aims to help people on lower incomes build up their savings. Offering generous tax-free bonuses, Help to Save can provide significant benefits for qualifying individuals.

Finally, in Could a Smart Thermostat Save You Money?, I revealed how these clever devices can save you money on your energy bills. I recently had one fitted myself. In this article I reveal which I chose (and why) and share some tips based on my own experiences. My heating engineer Dave, who installed it for me, also gets an honourable mention!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the range of articles published in February, I particularly enjoyed Where to Find the Best Money-Saving Resources in 2025 by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

The not-so-good news about Mouthy Money is that due to a change in their business strategy they will no longer be commissioning external content writers such as me and Jane. From a personal perspective I am obviously disappointed about this, but I have had a good run with them and wish them every success going forward. I will continue to follow Mouthy Money with interest and recommend PAS readers do the same. I am also available for other writing work in the personal finance sphere if anyone else should need me!

I also published several posts on Pounds and Sense in February. Some are no longer relevant, but I have listed the others below.

Debunking Common Myths About Over-50 Life Insurance is a guest post on behalf of my friends at British Seniors Insurance Services. It sets out seven common myths about life insurance for over-50s, including ‘I’m too old to get life insurance’ and ‘Life insurance for over-50s is too expensive’, and explains why these commonly-held beliefs are incorrect.

Marriage in Later Life – A Guide to the Financial and Legal Implications is another guest post, this time by my colleagues at HCR Law. In this eye-opening article, their family law specialist, Victoria Fellows, sets out some important considerations to take into account if you are thinking of marrying (or remarrying) in later life.

In How to Make Money From Stoozing, I discuss this method of making extra income by taking advantage of interest-free offer periods on credit cards. If you are well organized you can make hundreds of pounds by doing this, but there are certain pitfalls to avoid. My article sets out everything you need to know and shares some useful resources.

Don’t Miss Out! Use Your £20,000 ISA Allowance Before It’s Too Late is a reminder that the current tax year ends on 5 April 2025 – and if you don’t use your 2024/25 tax-free ISA allowance before that date, it will be gone forever. In my article I explain the main types of ISA and reveal the ones I invest in myself. I also reveal why using your ISA allowance may be especially important in the current tax year if certain rumours are to be believed.

Finally, in Get Your Will Written Free of Charge in March, I discuss Free Wills Month, which actually starts today (3rd March 2025). This event brings together a group of well-respected charities to offer members of the public aged 55 and over the chance to have their wills written (or updated) free using participating solicitors across the UK. If you don’t currently have a will, this no-obligation opportunity is well worth checking out.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. For the time being anyway, Twitter/X will remain my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK. The next one begins on Monday 3rd March 2025.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, Stroke Association, PDSA, Royal British Legion, Alzheimers Research UK, Mencap, British Heart Foundation, Age UK, and many more.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I strongly believe in using a properly qualified solicitor to draw up your will. In the last few years there have been a couple of occasions when failing to do this has caused problems and delays for members of my family. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website on or after March 3rd 2025. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s important to call as soon as possible. Once all available appointments are taken, the campaign will close. This may happen before the end of March.

Until March 3rd you can enter brief details on the Free Wills Month website and will then receive an email reminder when the scheme opens.

If you have any comments or questions about this subject, as ever, please do post them below.

This is an annual update of this post.

If you enjoyed this post, please link to it on your own blog or social media:

As the end of the tax year on 5 April 2025 approaches, so too does the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance.

The clock is ticking, and unless you take action in the next few weeks, this opportunity to maximize your tax-free savings for the 2024/25 financial year will be gone.

ISAs are a popular choice for savers and investors alike, offering a tax-efficient way to grow your wealth. With a diverse range of options available, from cash ISAs to stocks and shares ISAs and innovative finance ISAs, individuals have the flexibility to tailor their savings strategy to suit their financial goals and risk appetite.

The current ISA allowance stands at £20,000, providing a significant opportunity to shield your savings and investments from tax. This allowance represents a generous sum that, if left unused, cannot be carried forward to future years. In essence, any portion of the £20,000 allowance that remains untapped by the upcoming deadline will be lost, representing a missed opportunity for tax-free growth.

For those who have yet to fully utilize their annual ISA allowance, now is the time to take action. Whether you’re looking to bolster your rainy-day fund with a cash ISA, seeking to invest in the stock market through a stocks and shares ISA, or diversify your investment portfolio with an IFISA, there’s no shortage of options available.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potentially higher returns by investing in a wide range of assets such as equities, bonds and funds, albeit with a higher level of risk. And an Innovative Finance ISA, or IFISA for short, allows you to invest via P2P/crowdfunding platforms, further diversifying your portfolio (though again with a higher level of risk).

With an ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me (almost 20% over the last year alone). You can read my in-depth review of Nutmeg here. I have also invested some money in a property IFISA from Housemartin (previously Assetz Exchange). You can see my latest post about Housemartin here. You can also check out my February 2025 Investments Update to see how my Nutmeg and Housemartin investments (and others) have been faring recently.

Finally, for shorter-term savings, I am currently using the Trading 212 Cash ISA. The interest rate paid by Trading 212 is reducing from the current 4.9% to 4.5% from the start of March, but it’s still competitive with other cash ISA providers and has fewer strings attached..

With just a few weeks left to take advantage of this valuable tax benefit, delaying now could prove costly. By acting swiftly you can ensure that your savings and investments are positioned to grow tax-free, setting yourself up for a better financial future.

This has become all the more important with reports (such as this one) suggesting Chancellor Rachel Reeves is considering changing the rules applying to ISAs, and in particular reducing the tax-free allowance for cash ISAs to as little as £4,000.

In summary, the £20,000 annual ISA allowance for the 2024/25 tax year presents a golden opportunity to maximize your tax-free savings and investments. Time is of the essence, though. Unless you act before the impending deadline on 5th April 2025, this valuable allowance will be lost forever. If you have the money available, therefore, seize the opportunity now to help secure your financial future.

As always, if you have any comments or questions about this article, please feel free to leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Having fallen out of favour for a while due to a lack of suitable opportunities, the sideline-earning system of stoozing is back in the spotlight again!

Stoozing is a financial strategy that allows individuals to profit by leveraging 0% interest credit card offers. By using the interest-free periods, you can earn interest on borrowed funds without incurring additional costs.

Here’s a guide to effectively implementing a stoozing strategy…

1. Understanding Stoozing

Stoozing involves borrowing money through a credit card offering a 0% interest period and depositing that money into a high-interest savings account. The goal is to earn interest on the borrowed funds and repay the credit card balance before the interest-free period ends. This method requires careful planning and discipline to ensure profitability.

2. Steps to Implement Stoozing

Table of Contents

Select a Suitable 0% Interest Credit Card

Begin by researching credit cards that offer a 0% interest period on purchases or balance transfers. Opt for cards with the longest interest-free durations to maximize potential gains. Ensure you understand any associated fees, such as balance transfer fees, which could impact your overall profit. A useful resource for tracking down cards with 0% interest-free offers can be found on the popular MoneySavingExpert website.

Use the Credit Card for Everyday Purchases

Instead of using your debit card or cash, utilize the 0% interest credit card for daily expenses. This approach allows your regular income to remain in your bank account. This money can then be transferred to a high-interest savings account. Note that you should never withdraw cash directly from your credit card as you will be charged interest on this and it may also adversely affect your credit score (see below).

Deposit Funds into a High-Interest Savings Account

Transfer the money that would have been used for purchases into a high-interest savings account. This strategy enables you to earn interest on funds that would otherwise have been spent. Regularly monitor interest rates using a platform such as MoneySuperMarket to ensure you’re getting the best possible return on your savings.

Make Minimum Monthly Payments

It’s essential to make at least the minimum monthly payments on your credit card to maintain the 0% interest offer. Setting up a direct debit can help prevent missed payments, which could result in losing the interest-free benefit.

Repay the Full Balance Before the 0% Period Ends

Before the end of the 0% interest period, ensure you repay the entire credit card balance using the funds in your savings account. The difference between the interest earned and any fees paid represents your profit.

3. Example of Potential Earnings

Let’s say you obtain a 0% interest credit card with a 24-month interest-free period and a credit limit of £5,000. You deposit the full £5,000 into a high-interest savings account offering an annual interest rate of 5%.

Year 1 Interest: £5,000 x 5% = £250

Year 2 Interest: £5,000 x 5% = £250

Total Interest Earned Over 2 Years: £500

Assuming there are no fees and you meet all minimum payments on time, your profit from stoozing would be £500, simply by leveraging the 0% interest period.

4. Calculating Potential Profits

To assess the potential gains from stoozing, you can use online calculators designed for this purpose. These allow you to enter details such as the balance to be transferred, the introductory period, balance transfer fees, and minimum monthly payments to estimate your profit. One such calculator is available at stoozing.com.

5. Risks and Considerations

While stoozing can be profitable, it’s important to be aware of potential risks:

Discipline Required: Failure to make minimum payments or repay the balance before the 0% period ends can lead to interest charges that outweigh your earnings.

Credit Score Impact: Applying for multiple credit cards can affect your credit score. It’s advisable to check your credit report before proceeding. And it may be best to avoid stoozing if you plan to apply for a mortgage or business loan in the near future.

Changing Interest Rates: Savings account interest rates can vary, potentially reducing your anticipated profits.

Fees: Be mindful of any fees associated with the credit card or savings account, as they can erode your gains.

6. Closing Thoughts

Stoozing offers a method to earn additional income by strategically using 0% interest credit card offers and high-interest savings accounts.

Success in stoozing hinges on careful planning, disciplined financial management, and a thorough understanding of the terms and conditions associated with the financial products involved. Always ensure that the interest earned exceeds any fees incurred to achieve a net profit.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

If you would like to know more about low-cost self-publishing via Amazon, the e-book Kindle Direct Publishing for Absolute Beginners (pictured, left) offers a good introduction. If you don’t currently read on Kindle, download the free Kindle app to your laptop, tablet or smartphone.

If you would like to know more about low-cost self-publishing via Amazon, the e-book Kindle Direct Publishing for Absolute Beginners (pictured, left) offers a good introduction. If you don’t currently read on Kindle, download the free Kindle app to your laptop, tablet or smartphone. Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher Choc Lit (part of Joffe Books). She has also had a novel published in partnership with The Book Guild and has self-published several books via Amazon KDP. When not at the keyboard, she feeds her addiction to words by working part-time in her local library and running two reading groups. Sally can also be found walking, church-bell ringing and enjoying shavasana in her yoga class. Follow her writing blog at https://sally-jenkins.com/.

Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher Choc Lit (part of Joffe Books). She has also had a novel published in partnership with The Book Guild and has self-published several books via Amazon KDP. When not at the keyboard, she feeds her addiction to words by working part-time in her local library and running two reading groups. Sally can also be found walking, church-bell ringing and enjoying shavasana in her yoga class. Follow her writing blog at https://sally-jenkins.com/.