Today I have a collaborative post with my friends at HSBC Life for you. It’s about home insurance and how well people really understand it.

Let’s start with the most basic question, though…

What Is Home Insurance?

Home insurance provides financial protection in the event of something happening to your property (i.e. home) or your possessions. There are two main types of home insurance, contents and buildings.

Contents insurance covers your belongings for loss or damage caused by fire, theft, flood and other disasters. Buildings insurance covers the structure of the building itself, including the walls, floors, ceilings, roof, etc.

While contents insurance is generally optional (though highly recommended), buildings insurance is likely to be compulsory if buying your home with a mortgage. People who are renting will not normally require buildings insurance as this is the landlord’s responsibility, but they may still wish to take out contents insurance.

You can have separate buildings and contents insurance, but if you need both it will usually work out cheaper to get a combined policy. This may also make life simpler when the time comes to make a claim.

Home insurance clearly isn’t the most exciting of subjects, with most people regarding it as a necessary evil. But of course, if the worst happens, having the appropriate insurance cover may stop a misfortune turning into a catastrophe.

HSBC recently commissioned a study from market research company YouGov about people’s attitudes to home insurance. They polled 2,000 people in the survey, the fieldwork for which took place in May 2022.

Survey Results

The main questions asked in the HSBC survey are set out below, along with the results.

What are the main reasons people do or don’t have home insurance?

30% say it is expensive

18% say it is comforting

41% say it gives them peace of mind

49% say it is necessary

31% say it is reassuring

How much time does the average person spends researching their home insurance?

47% up to 1 hour

17% 1-2 hours

7% 1 day to 1 week

Where they do their research, if at all?

60% use price comparison websites

16% recommendations

12% customer reviews

What consideration is most important to them if they do select an insurer?

69% say price

71% say quality of cover

38% say reputation

Even for those who have purchased, do they understand what they’re buying?

72% say they understand what they have purchased

10% say they do not understand

Finally, what proportion have made a claim on their home insurance before?

39% of respondents have made a claim before

61% of respondents have not made a claim before

My Thoughts

One thing the HSBC survey results suggest is that many people don’t fully understand home insurance or give it the careful consideration it merits. In these times of rapidly rising living costs, that could be a serious mistake.

I would offer two main pieces of advice. First, think carefully about what home insurance you require. Do you need both buildings and contents insurance, or just one or the other? Think also how much cover you need, based on the value of your belongings (for contents insurance) and of your property (for buildings insurance). In the latter case, you should insure for total rebuilding costs rather than just market value, as this is what you would have to pay if your house was destroyed by fire, flood or some other disaster.

And second, shop around for your home insurance, as prices vary widely. Using a price comparison service such as GoCompare can be a smart strategy, though bear in mind that not all insurers appear on these platforms (Aviva, Zurich and Direct Line are three that don’t).

I also recommend using cashback sites like Top Cashback, as these frequently offer cashback to people taking out home insurance from companies listed with them. They may also offer cashback to anyone purchasing via a price comparison service listed on the cashback site, giving you the best of both worlds.

I’d also highly recommend reading my blog post How I Saved £511.08 on my Annual Home Insurance. And yes, I really did save that much. Though as you’ll see I had clearly been paying over the odds for my home insurance for some time. I had separate buildings and contents insurance which, as mentioned above, typically works out more expensive. What’s more, I had lazily allowed both policies to keep rolling over year after year without checking whether better deals were available. Don’t make the same mistakes I did!

Many thanks again to my friends at HSBC Life for sharing their survey results with me and allowing me to reproduce them.

As always, if you have any comments or questions about this post, please do leave them below.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Sadly scams of all kinds are on the rise at the moment, with older people especially vulnerable to them. Read on for some top tips on how to spot attempted scams and keep your money safe.

Scams are a growing problem in the UK, with millions of people being taken advantage of each year.

From fake investment schemes to phishing e-mails, scammers are constantly finding new ways to trick unsuspecting individuals into giving away their money or personal information. The financial impact of scams can be devastating, leaving victims with empty bank accounts and a damaged credit rating.

Over 12% of UK consumers have fallen victim to payment fraud over the past four years, with an estimated £1.2 billion lost to scams in 2021 alone. With so many people having their savings impacted by fraud, it’s crucial to know how to protect yourself.

This article will set out four practical ways to prevent scams from reducing your savings.

Table of Contents

Be cautious of unsolicited phone calls, e-mails and text messages

Scammers often use the promise of quick and easy money to lure people into their schemes. They do this through unsolicited phone calls, e-mails and text messages. Elderly people are particularly vulnerable to these monetary scams as they may not have the same level of technological literacy to spot one. However, anyone can easily fall into this trap as scamming methods grow increasingly sophisticated.

To protect your savings, you must not disclose your personal or financial information if you receive suspicious communication. You can also report dubious messages to the Information Commissioner’s Office, which has the power to take enforcement action against those involved in the scam.

Use strong passwords and security features

The government’s Cyber Aware campaign was launched in 2021 in response to growing scam and cybercrime incidents in the UK. One central piece of advice from the campaign is to use strong passwords and security features to prevent scammers from gaining access to your bank accounts.

For example, you can use a combination of letters, numbers and symbols on passwords to make them difficult to crack. Two-factor authentication provides another layer of protection by requiring a second form of verification in addition to your password. These two measures can significantly reduce your risk of falling victim to a scam that can empty your savings accounts.

Familiarise yourself with the technology used by merchants

As technology continues to evolve in the UK, so do the methods scammers use to steal your hard-earned savings. One way to protect yourself is to understand the methods used by merchants for their transactions.

Case in point, mobile card machines are commonly used by restaurants, cafés and pubs to process payments on the go. These devices are held to compliance standards like the Payment Card Industry Data Security Standard or PCI-DSS, which ensures that the machine follows protocols to protect cardholder data. Similarly, online merchants use virtual payment terminals to process payments online. Because shopping fraud schemes are on the rise in the UK, familiarising yourself with the technology merchants use can ensure you only interact with trusted businesses to keep your savings safe.

Choose banks with comprehensive fraud protection

In the UK, many banks offer fraud protection services as a standard feature. However, it’s still important to do your research and check that the bank holding your savings has the necessary fraud protection measures.

The Financial Ombudsman Service website offers resources regarding local banks’ anti-fraud policies. Additionally, you can check for your bank’s participation in the ‘Confirmation of Payee’ scheme. This initiative aims to protect customers from Authorised Push Payment scams, a type of fraud that tricks consumers into making a payment to a scammer. Banks participating in this scheme can check the recipient’s name against the account details provided by the customer and ensure the money is being sent to the correct person.

Scams can have a devastating impact on your savings—the fruit of your hard work. By taking the preventative measures outlined in this article, you can be vigilant and reduce your risk of being conned by one.

As always, if you have any comments or questions about this article, please do leave them below.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I joined the online trading and investment platform eToro earlier this year and have become a fan of it.

You can purchase a wide range of investment products on eToro, including individual company shares, ETFs, commodities, cryptocurrencies, thematic portfolios, and so on. You can also avail yourself of their popular copy trading facility, where you sign up to automatically copy the trades of an experienced (and hopefully successful!) eToro investor.

My own investments on eToro now comprise a thematic portfolio, a copy-trading portfolio, and a few shares in Tesla (basically because I had a spare $20 burning a hole in my account!). I will write more about thematic portfolios in a future post. Today, though, I want to talk about eToro Money.

Table of Contents

What is eToro Money?

eToro Money is a recently-launched e-money account for eToro investors. It can be managed via a mobile phone app. It is free to set up and there are no ongoing charges.

The key attraction of eToro Money is that it allows you to deposit to your eToro investment account without paying the usual currency conversion fee. This can save you up to £5 per £1,000 compared with depositing directly to eToro using a bank debit card.

Essentially what happens is that you deposit to your eToro Money account with your bank debit card using the account details provided. This money then appears instantly in your eToro Money account and you can use it to invest on anything on eToro when you are ready.

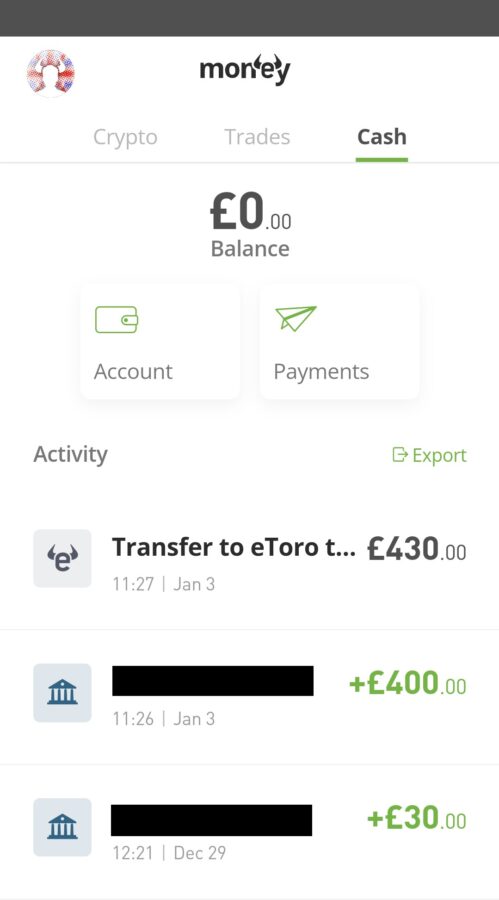

When I tried this myself, I was impressed by how straightforward the process was, and in particular the speed with which the money showed up in my account (it really did seem to appear instantly). Using it to invest on the eToro platform was then straightforward. Of course, eToro operates in US Dollars, so I worked out in advance roughly how much I would need to deposit in GB pounds to get the $500 I was aiming to invest (I transferred £430 in total to be on the safe side). The money was then converted at a fair rate with no fees or charges. You can see these transactions listed in the screen capture of the app on my phone below. I have redacted my account name for security reasons.

You can also use eToro Money to withdraw funds from your eToro account. I haven’t tried this yet, but again eToro promise that the process is instant and I have no reason to doubt that. There are modest fees for withdrawing from eToro and you will still have to pay them, but having an eToro Money account keeps costs as low as possible. As I noted in my original review, eToro’s fees are very reasonable and they don’t generally impose any transaction charges.

Other Features

As well as managing your main (‘fiat’) currency in eToro Money, you can also securely store, send and receive most popular cryptocurrencies. eToro Money incorporates the functionality of the previous eToro Wallet app for cryptocurrencies, while offering additional features as well.

You can also use your eToro Money account to send money to and receive money from friends and family, set up direct debits, manage your household expenses, and so forth.

The eToro Money Debit Card

This is a further benefit of eToro Money some may wish to take advantage of. It is a debit card linked to your eToro Money account which you can use in the same way as a bank debit card to fund purchases, exchange currencies, and so on. They claim to offer market leading exchange rates across the globe.

To qualify for an eToro Money debit card, you must be a member of the eToro Club. Anyone with over $5,000 in realised equity on eToro is eligible for this. Realised equity in this context means the combined value of the available funds in your eToro account plus the original amount invested in all your holdings. So if you have $1,000 in cash in your account and have invested $4,000 in shares and other investments on the platform, you will have $5,000 in realised equity and qualify for a free eToro Money debit card if you want one.

Closing Thoughts

For most users the primary benefit of an eToro Money account will be to eliminate the currency conversion fee when depositing on eToro. It also speeds up the process of depositing to the platform and withdrawing from it.

While eToro Money is not a fully-fledged online banking service, you can also use it to send payments and/or set up direct debits. In that respect, it is a bit like PayPal. Though you will need to know the sort code and account number of the person or business you want to pay. An email address alone (as with PayPal) won’t cut it!

As mentioned above, if you have $5,000 or more in realised equity on eToro you are also entitled to an Etoro Money debit card if you wish. You can read more about this on the eToro Money website.

Overall, I think anyone who plans to invest via eToro should seriously consider opening an eToro Money account to reduce costs and speed up depositing and withdrawing. They will obviously then have the opportunity to take advantage of the other benefits too.

To set up an eToro Money account, the best option is to download the eToro Money app from Google Play (Android) or the App Store (Apple) and follow the instructions in the app. Obviously you should have an account on eToro already in order to use eToro Money.

If you have any questions or comments about this post, as always, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on Pounds and Sense may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension), from which I recently started withdrawing again.

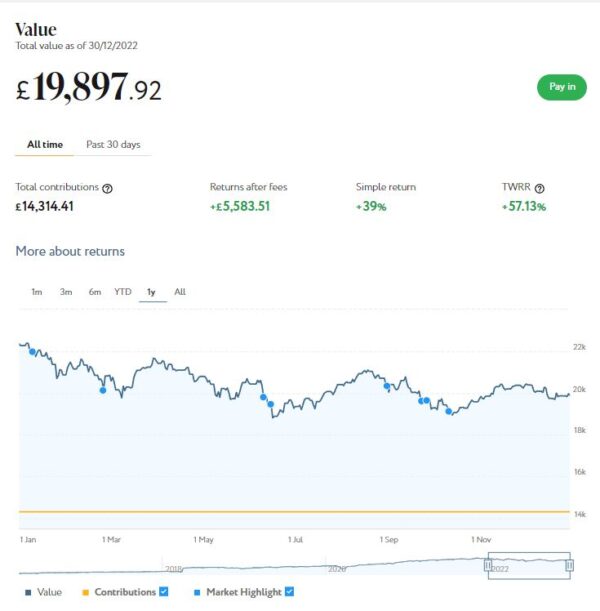

As the screenshot below of performance over the last year shows, my main Nutmeg portfolio is currently valued at £19,898. Last month it stood at £20,391 so that is a fall of £493.

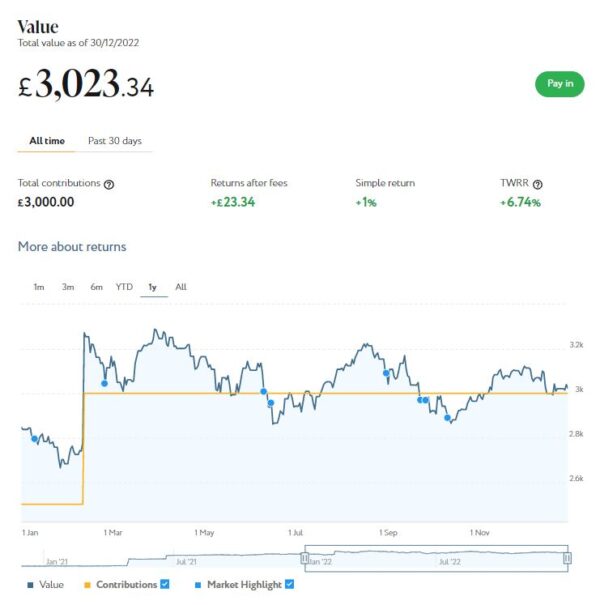

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,023 compared with £3,114 a month ago, a decrease of £91.

Here is a screen capture showing performance over the last year. As you can see from the ochre line, I topped up this account in February 2022.

That is a net month-on-month decrease of £584. That is obviously disappointing, but needs to be set against an increase of £785 the month before.

As the charts above clearly illustrate, 2022 was a volatile year for stock market investments generally. The outlook is still uncertain, but according to this article in the Financial Times the majority view is that stock markets overall will remain flat or see a very modest recovery in 2023. But obviously a lot depends on world events. If the war in Ukraine ends and/or China makes a reasonably smooth recovery from the pandemic, things could improve faster. Probably the best strategy, as this article from Forbes puts it, is to hope for the best but be prepared for the worst!

Overall, my Nutmeg investments are down £2,191 or about 8.7% since the start of 2022. To put this in context, though, in 2021 they rose in value by £3,552. And I am still more than £5,600 ahead since I started investing with Nutmeg in 2016. For my main portfolio that represents a return on capital of 39.01% or 57.13% time-weighted. My Smart Alpha portfolio hasn’t been going as long, but it is at least showing a small profit on the total I have put into it 🙂

Of course, the main lesson from all this is that investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to generate good returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a very respectable £91.61 in revenue from rental income. Capital growth has stalled, though, in line with what is happening in housing markets more generally. While some of ‘my’ properties are still showing gains, others are showing losses on capital. Overall my portfolio is currently showing a small net decrease in value of £7.88.

The latter is obviously a little disappointing, although of course capital values are largely academic unless and until you want to sell. The rental income is still coming in steadily without any issues or dramas. As I’ve said before, £91.61 is a decent rate of return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio when equity markets are volatile. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,400 invested with them in 18 different projects (I withdrew £200 in December to help pay for Christmas). To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest). My investment has been up and down in the last few months, but it is currently $33 (about £27) in profit. In these turbulent times I am quite happy with that.

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, probably in one of their themed portfolios. You can read my full review of eToro here. You may also like to check out my recent more in-depth look at eToro copy trading.

You might also like to know that eToro recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my more in-depth article about eToro Money here.

I had two more articles published in December on the always-excellent Mouthy Money website. One addressed the question of whether you can Save Money by Cancelling Your TV Licence. I looked at what this entails and what TV you are still permitted to watch without a licence. I also set out some ways you may be able to save money on your TV licence if cancelling altogether is a bridge too far for you.

My other piece was Why We All Need to Be a Bit More Branson! The title is obviously tongue-in-cheek. But the article sets out my strongly held view that – in these challenging times especially – we can all benefit from being a bit more entrepreneurial. I really enjoyed writing this one, I must admit!

Last month I updated my post about the Warm Home Discount, which this year is being increased from £140 to £150. The eligibility rules are changing somewhat, and I shall probably be one of the people who misses out, which is clearly disappointing. But on the plus side, most people won’t now have to apply for this benefit – if you are eligible, the grant should be applied automatically to your bill by your energy company.

The government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

That’s all for today. I hope you and your family are coping in these undoubtedly challenging times, and wish you a happy, healthy and prosperous 2023.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2022, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a Very Merry Christmas (strikes and cost-of-living crisis permitting) and for all of us a much better new year 🍾

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you about something many of us in icebox Britain would no doubt love to do at the moment.

Buying a Spanish holiday home, both for your own enjoyment and as a potential investment, has many attractions. But there are various important matters to consider before signing on that dotted line.

Learn more below 🏖

If you and your partner have spent many happy years holidaying in Spain, perhaps you’d like to consider investing in a Spanish holiday home?

Not only would a stunning sun-kissed property provide a wonderful place to enjoy your retirement years, but you could also let it out while you are not there and make some additional income. After all, Spain is a highly popular vacation spot with much to recommend it, so you would certainly never be short of guests.

Whatever you would like to use your Spanish holiday property for, there are a few important things you need to be aware of before you start house-hunting on the Costa Blanca…

Table of Contents

Many Stunning Locations To Choose From

As you surely already know if you relish a vacation in Spain, the country has a plethora of gorgeous locations to choose from. While on the one hand this is clearly a good thing, on the other, it could make deciding on a particular location rather tricky.

If you’re struggling to settle on one spot, take some time to think about your requirements for the property. For example, if you’re planning to purchase a home solely for your own use, it makes sense to choose a property in a location you particularly love. Alternatively, if you’re buying a home as an investment, you may prefer to think about the locale that draws the biggest number of visitors and has the highest rental prices.

Insurance Is Important

Insuring your Spanish holiday home is of the utmost importance, even if you won’t initially be spending a great deal of time there. After all, you never know what might go wrong – from fire and theft to flood damage or structural damage caused by extreme weather. If you don’t have cover then you could be liable for some truly hefty repair bills.

Fortunately, finding the right holiday home insurance for Spain should be a breeze, thanks to Quotezone.co.uk’s helpful comparison service. You can compare and contrast quotes from a range of UK providers and potentially save yourself a lot of time and money along the way.

You Will Need An NIE

When you buy a property in Spain as a foreigner, you will be required by law to have an NIE number. The authorities will be able to use this number to work out how much tax (if any) you owe each year.

Your NIE number can be applied for at the Spanish Consulate in your country of residence or in Spain itself. You will need to fill out forms and provide various supporting documents. The process can take anywhere between two weeks and two months.

Factor In All The Costs

Before you take the plunge and commit to buying your Spanish holiday home, it’s a good idea to dedicate some time to running through all the potential costs you are likely to incur.

After all, you won’t just be paying the asking price of the home itself. You will also have to pay various associated fees, not to mention mortgage payments, lawyers’ fees and surveyor charges.

There will also be additional annual costs, as you will have to keep the property maintained to a good standard, particularly if you’re letting it out.

To ensure a Spanish holiday home is the right choice for you and won’t prove to be too big a drain on your retirement savings, take some time to pause and reflect on the various costs involved. This will help ensure you choose the option that works best for you.

Thank you to my friends at Quotezone.co.uk for an informative article. If you have ever dreamed of owning a holiday property in Spain, I hope it will give you food for thought.

As always, please feel free to leave any comments or questions below as usual. I would be particularly interested to hear from any readers who have gone ahead and bought a property in Spain or are actively considering it.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post on a subject I freely admit I didn’t previously know much about.

Of course I was aware of Capital Gains Tax and the annual tax-free allowance. However, it transpires there is much more to know about CGT, especially surrounding the disposal of physical assets known in law as ‘chattels’. But I’ll let my guest Lilly Whale, an expert on this subject, explain in detail…

As well as freezing several tax thresholds, the Chancellor’s Autumn Statement also reduced the annual exemption amount for capital gains tax (CGT) from £12,300 this current tax year to £6,000 in 2023/2024 and to just £3,000 in 2024/2025. Any assets sold above the available threshold may be subject to CGT on the increase in the asset’s value between acquisition and disposal (disposal here means selling and gifting – of particular relevance for parents and grandparents who may wish to make gifts of long-held assets). Typically such assets could include second homes, buy-to-let properties, shares, business assets and valuable personal items such as jewellery and art.

During times of economic uncertainty, people with assets, such as a retirees, may be tempted to invest in alternative assets such as fine wine, art, classic cars and even luxury handbags – after all, the value of the much coveted Hermes Birkin bag has increased annually by approximately 14% over the last 35 years, easily outstripping returns on more traditional assets such as stocks and shares, property and even gold. As well as providing the lucky owners with considerable pleasure, these types of assets (or ‘chattels’) may have tax advantages over traditionally favoured assets, such as stocks and shares. This article focuses on the potential CGT triggers on a chattel’s sale and the potential advantages of investing in an asset of this kind.

Table of Contents

What is a chattel?

A chattel is a legal term used to describe an asset which you can both touch and move. Many personal items are categorised as chattels, including books, fine wine, antiques, clothes, shoes, handbags, silverware, records, jewellery, art and cars. The definition also encompasses items of plant and machinery not permanently fixed to a building.

Chattels: exempt from CGT?

Disposals of chattels for £6,000 or less are exempt from CGT. Say, for instance, that you buy a piece of fine art from a little-known artist for £250. Over the next few years, that artist becomes exceptionally popular and you eventually sell the artwork for £5,000 – a realised gain of £4,750. Since the sale proceeds are less than £6,000, the chattels exemption is applicable and no CGT is due.

Sets of items

Care must be taken when a chattel forms part of a set: if the individual parts were owned at the same time and are sold either to the same person, a number of people acting together, or a number of people who are connected (e.g. family members), then the £6,000 limit will apply to the set collectively and not to the individual member of the set.

For example, many years ago you purchased four first-edition books by the same author on the same topic for £5,000 (£1,250 each). Today, the books altogether are worth £20,000 and you sell them all to a book collector.

If the limit was applied to each book’s sale price then all four disposals would be exempt from CGT because individually they are, at £5,000 apiece, under £6,000. However, in HMRC’s eyes the books would be a set and the £6,000 limit cannot apply. There would consequently be a maximum chargeable gain of £15,000 for CGT purposes.

Note that any costs relating to the sale can be deducted from this, and the annual exemption of – at least during the 2022/2023 tax year – up to £12,300, provided it has not been used against other asset sales in the same tax year. Accordingly CGT would be levied on £2,700 at either 18% or 28%.

Other exemptions

Some types of chattels qualify for CGT exemption no matter how large the sale proceeds or gain.

For instance, a private car can be sold for any price without attracting a charge to CGT – including vintage and classic cars. Further specific assets which attract no CGT on disposal are medals or decorations which, HMRC notes, were ‘awarded for valour or gallant conduct’; the seller, however, cannot have ‘acquire[d] it for money or money’s worth’. In practice this means that the seller benefits from this exemption if they were the person who was originally awarded the medal/decoration, or if they are the person to whom the medal/decoration was gifted or left as an inheritance by the individual so-awarded.

Wasting assets

Other chattels which qualify by right for CGT relief are ‘wasting assets’, i.e. assets with a predictable life of 50 years or less. Specific assets within this class range greatly and certain chattels, such as plant or machinery, will always be treated as wasting assets. Highlighted below are a few examples.

While the purchase of fine wine may provide long-term capital growth, whether it is classed as a wasting asset (and the consequent CGT ramifications) is a grey area. An everyday bottle bought from a supermarket (or as HMRC put it, ‘cheap table wine which may turn to vinegar’) would fall squarely within the wasting asset bracket, meaning that CGT on sale is not a consideration; not so, however, for port and other fortified wines with a storage life far beyond 50 years, which would not be considered a wasting asset and CGT on sale may well be relevant. But what about wines which are between these two extremities?

In short, there are several key factors which HMRC would consider when deciding if fine wine is a wasting asset or not and therefore subject to CGT on disposal. It should be noted that the 50-year time limit runs from the wine’s acquisition, not when it was first bottled: thus the drinkability in 50 years’ time of a recently purchased yet very old vintage compared with a relatively young vintage could be starkly different – one may have turned to vinegar; the other simply matured. Investors in this sphere are well-advised to keep detailed records pertaining to the wine’s condition, vintage, provenance, and so on.

Where wine is not considered a wasting asset, the seller can benefit from the £6,000 CGT exemption and therefore disposals of less than this are free from CGT. (Care should be taken if multiple wine bottles are sold at once as the above ‘set’ rules may be triggered.)

Other types of wasting assets include racehorses, shotguns, and clocks and watches (even very expensive ones, as their mechanics are deemed to have a predictable lifespan of not more than 50 years). However, this list is by no means exhaustive and a professional advisor can help to ascertain whether an investment would be considered a wasting asset or not.

There was no indication in the Autumn statement that the various chattels exemptions would be removed; yet clearly CGT thresholds and dispensations are of demonstrable importance to the Government. Now, therefore, seems an opportune moment for individuals to consider what allowances and reliefs – both for CGT and other tax purposes – may be useful and viable, and whether they can realise assets free of tax.

Lilly Whale is an associate in the private client team at RWK Goodman, the law firm.

Many thanks to Lilly Whale (pictured, right) for an informative and eye-opening article. Please do check out her company website (linked above).

As the article indicates, the special tax status of chattels can make them an attractive option for investors, especially if they have maxed out their other tax-free allowances. Passion investments, from rare books to classic cars, antique jewellery to fine art, typically fall into this category.

It is, however, essential to be aware of the rules that apply regarding CGT when the time comes to dispose of the assets in question. The same applies if you currently possess valuable assets you are planning to sell to raise funds (or indeed to give away). In either case, to minimize your tax liability and avoid any potential disputes with HMRC, it may well be advisable to speak to an experienced professional in this field.

As always, if you have any comments or questions about this article, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). I will discuss the latter a bit further down.

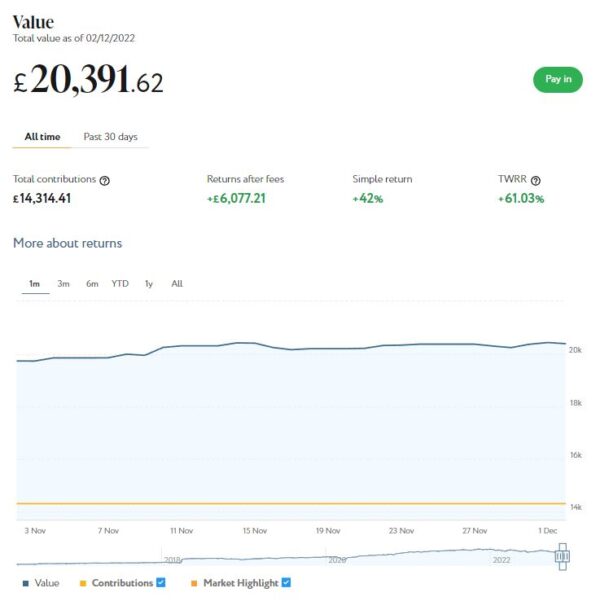

As the screenshot below of performance last month shows, my main Nutmeg portfolio is currently valued at £20,391. Last month it stood at £19,733 so that is a rise of £658.

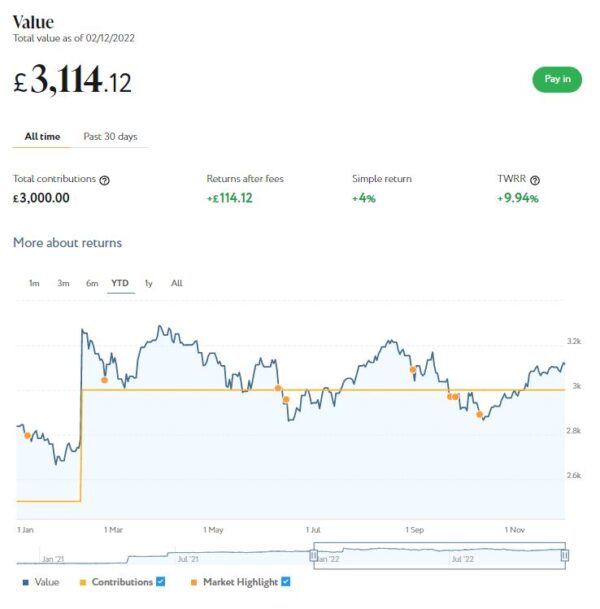

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,114 compared with £2,987 a month ago, an increase of £127.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

That is an overall month-on-month increase of £785. Furthermore since mid-October the total value of my Nutmeg investments has risen by £2,007 or around 8%. Anyone who was brave enough to invest in Nutmeg around the middle of October will therefore be looking at a substantial profit now. Of course, it’s always easy to spot an investment opportunity with 20/20 hindsight!

In my case, while the recent rises are very welcome, my Nutmeg investments are still down £1,607 or about 6.5% since the start of the year. To put this in context, though, in 2021 they rose by £3,552 (over 21%). And overall, I am still over £6,000 ahead since I started investing with Nutmeg in 2016. For my main portfolio that represents a return on capital of 42% or 51.03% time-weighted.

Of course, the real point of this is that investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £88.30 in revenue from rental and £17.59 in capital growth, a total of £105.89. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest). My investment has been up and down in the last few months, but it is currently $38 (about £31) in profit. In these turbulent times I am quite happy with that.

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full review of eToro here. You may also like to check out my recent more in-depth look at eToro copy trading.

Moving on, earlier I mentioned my Bestinvest SIPP (personal pension). This is now in drawdown, but regular readers will know that I suspended withdrawals from it in May this year to reduce the risk of pound-cost ravaging. I was able to do this because since December 2021 I have been receiving the state pension. And in association with my other income streams this has given me enough to live on (though by no means in luxury).

Anyway, with the cost of living crisis starting to bite, and energy bills shooting up at an alarming rate, I decided the time had come to resume taking payments from my SIPP. Plus, with the markets seemingly on an upward trajectory, the risk of pound-cost ravaging appeared to have receded.

I therefore asked Bestinvest to reinstate my payments from this month, though at a lower rate of £100 a month. One of the attractions of flexible drawdown pensions such as those from Bestinvest is that you can increase or decrease withdrawals at any time or even (as I did) suspend them completely. Obviously if you draw an excessive amount there is a risk of depleting your fund too quickly, so it runs out before you do. But Bestinvest sent me some reassuring projections that in any feasible scenario this was unlikely to happen in my case even if I live to the age of 99 (as I fully intend to 😀 ).

One other consideration I had with my SIPP is that withdrawals from it are taxable, whereas withdrawals from some of my other investments (e.g. Nutmeg ISA) are not. With the state pension also being taxable, this means withdrawing larger amounts from my SIPP would result in a portion of the money being grabbed by the taxman, which seems a waste. While I do of course accept that taxes have to be paid, I prefer to minimize my liability as much as possible (which we are all perfectly entitled to do).

I had two more articles published in November on the always-excellent Mouthy Money website. One of them was Win Fame and (Maybe) Fortune as a Quiz Show Contestant. This is something I have done myself in the past and enjoyed writing about again for MM. It can be a lot of fun, and any prizes you win are tax-free under UK law.

My other article was How to Cash in on Your Old Tech. Most of us have old technology we no longer use gathering dust in cupboards and drawers. This articles sets out ways you can make some much-needed cash out of this.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. Everyone should be receiving a monthly rebate of £66 on their energy bill (going up to £67 in the new year). If you’re not, chase it up with your energy supplier.

I also recently updated my post about the Warm Home Discount, which this year is being increased from £140 to £150. The eligibility rules are changing somewhat, and I shall probably be one of the people who misses out, which is clearly disappointing. But on the plus side, most people won’t now have to apply for this benefit – if you are eligible, it should be applied automatically to your bill by your energy company.

The government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The current Trading 212 offer closes on 29 December 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course

That’s all for today. I hope you and your family are coping in these challenging times and wish you the happiest Christmas possible. I shall of course continue to update this blog over the coming weeks, and will return with a further update about my investments at the start of January.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Christmas is coming, so here’s a chance to make it extra special for one lucky winner!

I’ve joined forces with some of my fellow UK bloggers in this festive giveaway with prizes valued at over£800 in total. You can read about all the amazing prizes below and see photos as well!

Entering the giveaway is free of charge and full instructions can be found below the list of prizes. There are multiple ways to enter, and the more you do, the better will be your chances of winning. But note that where an entry requires following a social media account, you will need to continue following this account until the winner has been drawn on 20 December 2022 (or as soon after that as practicable). Before the winner is announced the organiser will check that they are still following the account in question. If not, they will be disqualified and another winner drawn.

2022 has undoubtedly been another challenging year. Although we are (touch wood) emerging from the pandemic now, the cost of living crisis is hitting many families hard. Whether you win this giveaway or not, I wish you and yours a very happy and peaceful Christmas 2022. Here’s hoping that 2023 is a brighter and more prosperous year for all of us 🙂

This giveaway has been organised by my fellow blogger Rowena Becker, who blogs at My Balancing Act. Please check out her blog and those of the other talented UK bloggers taking part (listed further down the page). And read on for full details from Rowena of all the prizes on offer and how you could win this mammoth bundle!

Table of Contents

The Great Festive Gift Guide Giveaway 2022

We are back for another Festive Giveaway! Some of the UK’s top bloggers have united to bring you the most amazing holiday bundle of prizes. Last year’s giveaway proved to be very popular and this year’s is just as exciting, with so many prizes for one lucky winner to make their family Christmas dreams come true. In fact, we have over £800 worth of festive goodies and gifts!

KEEP SCROLLING DOWN TO ENTER AND FOR THE FULL LIST OF AMAZING PRIZES – We’ve saved some of the best till last! This is not only a giveaway but also a great holiday gift guide with ideas for the whole family this festive season.

The Prizes

PAJ GPS ALLROUND Finder 4G, a GPS Tracker for vehicles, cars, people and objects

The PAJ GPS ALLROUND Finder 4G will help our lucky winner protect what they love! The small and handy device has an SOS emergency button and alarm. Splashproof, it offers flexible use with a battery that lasts about 20 days with an active tracking time of approximately 1h/day and up to 40 days in standby mode!

The Online Tracking Advantages include:

Real-time location and live tracking. Its location will be updated every 30 seconds (even sooner if the tracker is changing direction)

365 days’ route information

SIM card will always search for the best available network

Tracking in over 100 countries

Built-in vibration sensor. As soon as the tracker is moved, an alarm will be sent via email or as push notifications via the app

We have a PAJ GPS ALLROUND Finder 4G as part of our prize bundle.

Jurassic World REAL FX Baby Blue Dinosaur Toy

This is the must have Christmas Toy this year for any dinosaur fans and we have one Jurassic World REAL FX Baby Blue Dinosaur Toy from WOW! STUFF for our lucky winner! The hyper-realistic Real FX Baby Blue makes genuine Velociraptor life-like roars, chatters, snarls and purrs, just like in the Jurassic World Dominion movie. She also replicates the actual size from the Jurassic World movies. You can hold and control Baby Blue and activate protect, lunge, battle and bite actions. Simple to operate Real FX Baby Blue makes an incredible gift for Jurassic World fans of all ages, from kids to adults!

Merlin Theme Parks Anytime Choice Voucher from Red Letter Days

Get set for an exhilarating day to remember! Our winner can spend a fun-filled day out for two people with anytime entry to a Merlin theme park with a Merlin Theme Parks Anytime Choice Voucher from Red Letter Days. The prize includes entry to either: Alton Towers Resort, Chessington World of Adventures Resort, LEGOLAND® Windsor Resort or THORPE PARK Resort.

Snuggle Slipper: Navy blue suede NSPCC rainbow slip-on slippers from Start-Rite

To mark Start-Rite’s 230th birthday, they’ve partnered with the UK’s leading children’s charity, the NSPCC to create an exclusive Snuggle slipper with a joyful rainbow design. The traditional moccasin style slipper, Snuggle, can now help to support thousands of children across the country and for every pair of Rainbow slippers sold, Start-Rite will make a donation to the NSPCC.

Crafted from a navy blue suede upper, with a bright rainbow motif and lined with snuggly faux fur, these slip-ons are sure to keep your little ones’ feet comfy and warm around the house. Our lucky winner can choose a Snuggle Slipper in the available size of their choice and you can check out the full range of slippers here.

A Swimsuit and Goggles from Halocline

You’re going to love the new styles from Halocline Swimwear! You can get your New Year off to a fresh start by winning a swimsuit and goggles of your choice. Pick your favourite design from their new range of ladies’ swimsuits at Halocline and team with a pair of goggles.

Many styles in Halocline’s collection are made from Econyl® recycled nylon yarn, which is created using waste plastics that would have otherwise ended up in the ocean.

You’ll love the fit of a Halocline swimsuit – there are styles for all shapes and sizes. There are longer length styles for the taller swimmer, swimwear with bust support, plus size swimwear and, for those looking for a bit more coverage, they even have legsuit and kneesuit swimsuits.

Not only that but the lovely people at Snow Windows are also giving our lucky winner their new One Snowy Night Scented Candle. The candle has a delightful scent of myrrh and tonka bean. Tom at Snow Windows designed the beautiful imagery . And there’s even a QR code in the candle box so you can see a video of him hand spraying the design in snow spray! Keri at Snow Windows worked with the fabulous team at Molecule to create the fragrances to stimulate your senses, create a festive mood and provoke festive memories for years to come.

Individually hand poured with love and care in a farmhouse workshop using a blend of coconut and rapeseed wax, essential oils and botanical perfume oils. They contain absolutely NO nasty phthalates, paraffin, palm , beeswax or artificial additives. The slowly burning candle features a crackling wood wick.

Milk and White Chocolate Christmas Jumpers from choconchoc

The clever folk at choconchoc have managed to combine two of our favourite Christmas traditions – the Christmas jumper and chocolate! The artisan chocolatiers have combined the two to bring you their festive Chocolate Christmas Jumpers Gift Box. These festive treats are made from a blend of the finest dark, milk and white Belgian chocolate. Each box contains four chocolate jumpers featuring Christmas reindeer and penguins and we have one box for our winner to enjoy.

Personalised Fleece Blanket from VistaPrint

Our lucky winner has the chance to get cosy with their own unique personalised fleece blanket, worth £45.00. Whether you’re looking for a fun yet practical gift or just want to add something new to your home design, personalised fleece blankets are a memorable keepsake and VistaPrint has a wonderful selection to choose from, all of which can be easily customised with your own personal messages and photos of your friends, family or even your pets!

NEW LIFE PRO Frying Pan 20cm

This is the perfect gift for any kitchen lover. It will also help you make the Christmas dinner in style! The NEW LIFE PRO frying pan is more environmentally friendly than most frying pans. It’s made of high quality 100% recycled aluminium from Europe and is produced with up to 95% less energy than conventional aluminium pans.

Produced in Switzerland, the thick base stores and distributes heat perfectly. The durable 3-layer non-stick coating reinforced with ceramic particles, is ideal for low-fat frying. It has an ergonomic stainless steel stay-cool handle and it is suitable for all hobs, including induction.

The easy cleaning saves time and water. The packaging is made of 100% recycled paper. NEW LIFE PRO from Kuhn Rikon is a range of pans produced with the aim of creating a greatly reduced impact on the environment.

Utensil Set from Mason Cash

Another wonderful gift for anyone who loves cooking, the gorgeous range of kitchen utensils from Mason Cash will put a smile on any home baker’s and cook’s face! The winner will receive the following from the set:

Innovative Kitchen Turner & Rack Grabber: Ideal for turning meat and vegetables in pans or oven trays, the slots allow liquid and oils to run free when stirring or lifting food. The handle is specially designed to pull out and push in oven racks when checking on bakes.

Innovative Kitchen Solid Spoon & Jar Scraper: The Baker’s Spoon with Jar Scraper is ideal for beating, stirring and blending. This 3-in-1 utensil features measurements for 1 tablespoon, 1 teaspoon and 1/2 teaspoon on the spoon head and a silicone jar scraper and spatula on the handle.

Innovative Kitchen Slotted Spoon: The Slotted Spoon with Egg Separator is a specially designed 2-in-1 utensil. The spoon is ideal for stirring and draining food in water, sauces or oils and the slots on the spoon head are designed to separate egg whites from yolks. The grooves on the back of the spoon handle allows the spoon to sit on a Mason Cash Mixing Bowl or Pudding Basin, making separating your eggs easy.

Innovative Kitchen Spatula: The Spatula is perfect for stirring mixes and scraping bowls and pans clean. The head can be removed and used as a bowl scraper and the small spatula is perfect for spreading frosting onto cakes and scraping the inside of jars.

Innovative Kitchen Whisk & Reamer: The Whisk and Reamer is a specially designed 2-in-1 Utensil. The stainless steel balloon whisk is perfect for whisking eggs, cream and cake mixtures and the reamer handle is perfect for juicing lemons and limes.

NORDIC WARE Cosy Village Pan

This lovely cast aluminium non stick cake tin features six unique cottages. The intricate cosy village cake pan detailing makes them fun and easy to decorate so your guests and family will love having their own mini cottage cake. The cast aluminium non stick cake tin is made to last so you can use time-after-time. The interior non-stick coating on the muffin moulds pan makes for easy release and quick clean up time after baking.

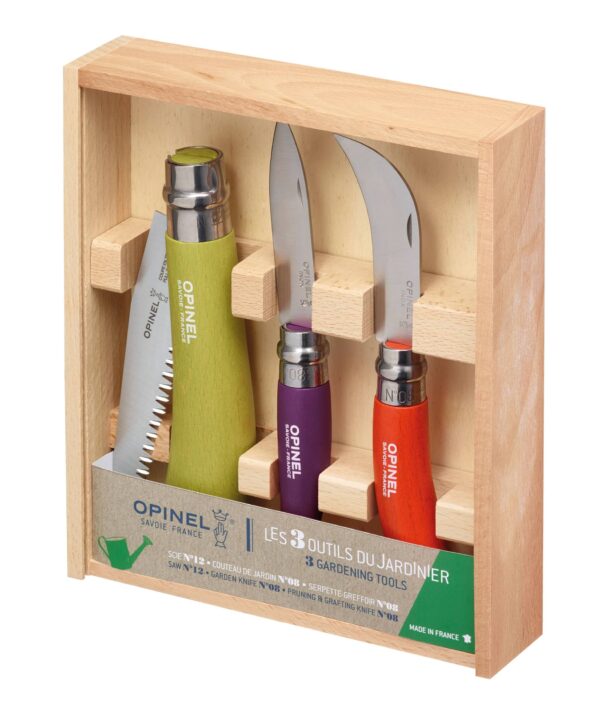

Opinel Gardeners Gift Set

This 3pc Opinel Gardening Set makes a beautiful Christmas gift for any garden lover. Presented in an attractive wooden display box, the set includes a folding saw, garden knife and pruning knife, all with beautiful beech handles and VIROBLOC safety locking ring.

Kids Against Maturity Card Game

Are you ready to laugh out loud with your kids this Christmas? Good, because this game will have the whole family in stitches! Kids Against Maturity is the perfect way to spend quality family time together. Made and played by parents, the game includes age-appropriate toilet humour and funny innuendos for the adults. It can be enjoyed by the whole family and is the ideal game to keep everyone entertained on Boxing Day!

The Fuzzies Game

The Fuzzies is the must have game this Christmas! Create gravity-defying towers out of the fuzzy little balls. The aim of the game is to not knock over the tower as you skilfully remove the colour of fuzzy that you’ve drawn from the cards using either tweezers or your fingers. Sounds simple right?! Wrong! The rules state you can not get out of your seat! Once you’ve removed your fuzzy you can stick it anywhere higher on the tower. The Fuzzies is so much fun for all ages.

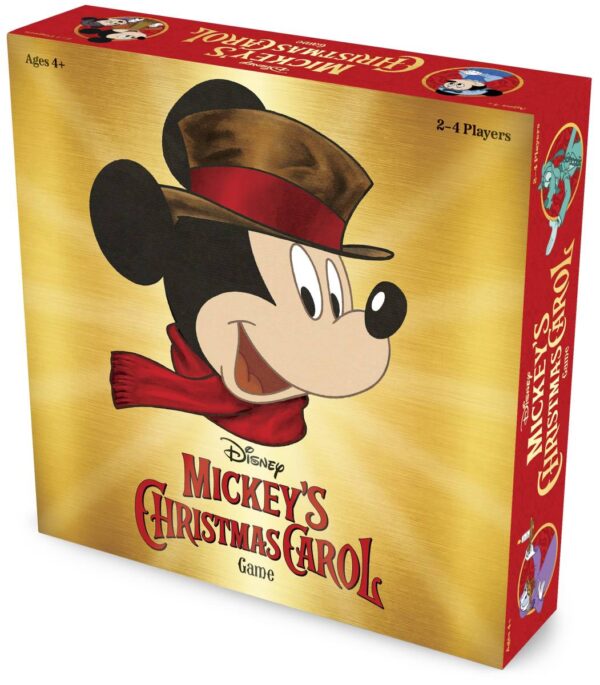

Mickey’s Christmas Carol

Another fantastic game for the whole family to enjoy, Mickey’s Christmas Carol is both festive and fun! Focusing on simple gameplay and collaboration, players work together to complete their story tableau – Christmas Past, Present and Future from this timeless classic. Puzzle tableaus depict iconic moments from the story, and players must complete them in order before Scrooge wakes on Christmas morning. The game includes a wooden Scrooge mover to track your progress and six beautifully illustrated scenes inspired by the Disney classic.

RAINBOW Notebook from Belly Button Designs

This lovely RAINBOW notebook is perfect for writing down all your dreams and ambitions for 2023. With a gorgeous rainbow on the front cover and the words Dream Big, it makes a lovely gift for Christmas.

Christmas Robins China Mug

This beautiful new bone china Robins Mug from Belly Button Designs is perfect for Christmas. The lovely robins will get you in the festive spirit. We have one gorgeous mug for our lucky winner as part of the prize bundle.

Magic and Cheer Luxury Scented Christmas Candle

You will be transported to a festive wonderland with this lovely citrus led scented Magic and Cheer Candle in a tin from The Copenhagen Company. The fragrance is entwined with a blend of delicious Christmas spices including cinnamon and cloves, sweetened with a touch of vanilla and held together with the warm and woody notes of sandalwood and cedar.

CARDOLOGY Peter Rabbit Christmas card

This lovely Peter Rabbit keepsake Christmas gift from the iconic Beatrix Potter stories will make Christmas extra special for your little ones. This officially licensed handmade 3D pop up Peter Rabbit Christmas Card brings to life, all of the characters, like Peter Rabbit, Flopsy, Mopsy, Cottontail, Jemima Puddleduck and Mrs Tiggywinkle as they decorate the Christmas tree.

This is a beautiful Christmas card that can be kept on display long after the event and can be brought out year after year as a Christmas decoration. A keepsake Christmas gift for the memory box, especially with the addition of a pull out notecard insert so your message won’t be on show when the card is displayed. The packaging cleverly reverses to become a beautifully designed gifting envelope, making it a lovely gift and card for a loved one.

This card is produced under licence from Penguin Ventures.

Forever Living – Smoothing Exfoliator

This smoothing exfoliator won the Woman & Home Beauty Award 2021 in the Best Exfoliator category. It is eco-friendly using natural jojoba and bamboo – no nasty plastic microbeads. It combines ingredients that gently reveal healthy, glowing skin. Round jojoba beads massage the skin and penetrate hard-to-reach places for ultimate cleansing while sustainably sourced granules of bamboo delicately remove dead skin cells.

Natural extracts including bromelain, papain and lemon essential oil help regenerate the skin. Bromelain, an enzyme obtained from pineapple, destroys keratin, a protein in dead skin cells. Papain from papaya is rich in vitamins A, C, E as well as pantothenic acid, better known as B5—a water-soluble vitamin crucial for healthy skin. Lemon essential oil then richly moisturises and hydrates the skin for a youthful glow.

Grape juice extract and other antioxidants ensure effective and gentle exfoliation to reveal glowing skin. Designed to be used 2-3 times a week, exfoliated skin feels silky and smooth and is primed for better absorption of subsequent skincare products.

This stylish pink handbag from Amazon Fashion makes a beautiful gift for someone this Christmas. Amazon Fashion have the perfect present, whatever your budget.

The Bloggers

In order to be able to bring you this incredible giveaway some of the UK’s top bloggers got together and contributed. A massive thank you to our bloggers for making someone’s Christmas extra special! The bloggers taking part are:

You can enter the Christmas Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collected and one winner will be randomly chosen. Good luck!

The giveaway will run from 11:59 am 3rd December 2022 to 11.59 pm 19th December 2022.

The winners will be notified by email from rowena@mybalancingact.co.uk

The winner will have 7 days to respond after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, Twitter, YouTube, BlogLovin or Pinterest.

Prize open to over-18s only. Age verification may be required to receive some prizes.

If any prizes are out of stock then we will do our best to find a suitable replacement, but cannot guarantee it. The prize for the Innovative Utensils only includes what is listed and not the full set in the picture.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage. Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace these.

In the unlikely event one of the companies withdraws a prize we cannot offer an alternative. The winner’s name will be stated on some or all of our blogger’s websites and announced on Twitter and other social media channels. It will also be displayed on the Rafflecopter Entry. By entering this prize draw you give your permission for this.

Please note the winner may have the same name as you so if you see your name displayed, be aware that you are not the winner unless you have been notified by us. We cannot guarantee the prizes will arrive in time for Christmas and there may be some delays in receiving prizes.

Good luck, and I hope that a Pounds and Sense reader wins this amazing giveaway!

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you on a subject I don’t generally cover on Pounds and Sense.

Cryptocurrency investing/trading is risky and I appreciate that it may not appeal to many readers of this blog. On the other hand, I can’t deny there is a lot of interest in crypto, from younger people in particular. So today I am publishing a guest post for anyone who might be interested in finding out a bit more…

While some people prefer to invest in crypto as a side hustle, others want to take it a step further and become a full-time home-based crypto investor.

Investing time and money into crypto can be risky, so it’s important that you know what you are doing and you pay attention to how the markets change. In this article we will go over a few tips and tricks to help you get started.

Table of Contents

Create a Working Space

One of the first things you will need to do is set up a working space for yourself. It is important that you have a designated area to work in, as this will help you stay concentrated and focused throughout the day. If you can, it would be a good idea to have your workspace away from anything else, as this will stop you from getting distracted. A spare room or even just a corner in one room of your house will work well.

Keep Updated with Crypto News

Keeping up to date with crypto news is a great way to start off as a crypto investor. The financial markets can be volatile, so you must stay current with all the latest changes so that you can make any necessary adjustments to your investments. There are plenty of ways to stay up to date, but it could be helpful to download a crypto app that will help you manage your investments and also learn about any changes to the market.

Research Ways to Earn Bitcoin

It would be beneficial for you as a home-based crypto investor to start researching ways that you can earn Bitcoin, one of the most popular types of cryptocurrency. Learning the different ways you can earn Bitcoin will help you become a successful investor. One way you can earn Bitcoin is by trading a gift card you don’t need for it. Paxful allows you to safely buy Bitcoin with a gift card, which makes earning Bitcoin super easy.

Join Crypto Communities

If you are new to the world of cryptocurrency, then a good way to get started is joining different crypto communities. There are plenty of discord servers or Reddit subs that are specifically for crypto investors, so these can be helpful to be a part of. Users share their different experiences with the crypto market and offer advice and suggestions about when and how you should invest. For someone starting out as a crypto investor this can be invaluable, as you will learn about crypto from people who have more knowledge and experience than you (though don’t take everything you read as gospel!). Having a supportive community behind you will allow you to learn and grow as a crypto investor.

Thank you to my friends at Paxful for an interesting article.

Just to emphasize what I said at the start, cryptocurrency trading is high risk and definitely not for everyone. Yes, you can make a lot of money, but you can also lose your shirt!

My personal advice if nonetheless you want to explore cryptocurrency trading/investment is to start small with money you can afford to lose in a worst-case scenario. I also like the idea mentioned in the article of earning cryptocurrency rather than buying it. Obviously if your crypto is something you have earned or otherwise acquired yourself (perhaps by exchanging a gift card), losing it isn’t likely to be as painful 😮

I would love to hear your reactions to this article, and whether you think I should cover cryptocurrency more often on Pounds and Sense. I’d also be interested to hear about your personal experiences with crypto (no spam, please). Please leave any comments or questions below as usual.

This is a collaborative post.

Disclaimer: Nothing in this article should be construed as personal financial advice. As stated in the article, cryptocurrency trading/investment can be very high risk and is not suitable for everyone. Proceed with care and take professional advice if in any doubt whether it is right for you. All investing carries a risk of loss and this is especially so with cryptocurrencies.

If you enjoyed this post, please link to it on your own blog or social media: