Being a pet parent can be an enriching experience or an abject disaster, depending on how prepared you are. Whether you are looking to bring a fluffy, four-legged friend into your home or you’re looking for something more exotic, there are several things you should keep in mind when bringing any animal into your family.

Consider All the Costs Involved in Pet Keeping

When we consider adopting a pet, the cost may not be your first consideration, but it should be. Aside from the adoption fees and the cost to feed your new friend each month, there are several other costs you will need to consider when you’re budgeting for a new pet. According to some sources, the estimated cost to keep a pet dog in the UK is around 1,875 GBP a year, which excludes any adoption fees or travel costs associated with bringing your new companion home.

Unexpected veterinary bills can also involve hefty costs if you’re not prepared. To keep these unexpected costs to a minimum, consider taking out pet insurance from Petsure for your new family member.

Prepare for a Long-Term Companion

While our furry, scaly, or feathered companions may not have the same lifespan as us, with some exceptions, it is essential that you research how long your pet’s average lifespan is in captivity before you adopt. Many people don’t consider that some fish can reach the ripe old age of 15 years old or that some reptiles have been known to exceed the 60-year mark. This is a huge time commitment and not one that should be taken lightly.

Pet-Friendly Properties and Pet Proofing

Thanks to the popularity of pet ownership, with an average of 62% of UK households owning at least one pet, many residential properties allow pet ownership in some form. However, while the average landlord may not have an issue with a small dog or cat, you should always check to see if they have any restrictions before starting any adoption process. This is particularly important if you plan to adopt a large dog breed or an exotic pet like a lizard or snake.

Even smaller animals that require some outdoor exercise time, like rabbits and guinea pigs, may not be welcome in all complexes. Once you’ve checked that your pet is welcome, ensure that your property is ready for them too. If you live in an area with open gardens, you may need to make a plan to install a fence or barrier to keep your pet within your property.

Get Your Whole Household On Board

While you may be super excited to adopt a new family member, pets tend to take over households. Whether it’s a cute kitten looking to make mischief under the sofa or a ball python that enjoys the occasional frolic around the living room, animals should be allowed some freedom to play outside of your bedroom. So, make sure your whole household approves of the new addition before you bring them home. Also, keep in mind that you may need to rely on the people in your house to take care of your animal when you are away, so making sure they are comfortable with your critters should be a top consideration.

Whether you are looking to add a cute fluffy hamster or a large scaly tortoise to your family circle, doing your research is key to a long and happy future together. And remember to always keep the animal’s needs and care requirements in mind before making any adoption decisions.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

I’ve mentioned several times on PAS why I believe having an independent financial adviser makes sense, even if – like me – you consider yourself reasonably money-savvy.

So today I thought I would set out some reasons over-50s (in particular) may benefit from having an independent financial adviser (IFA) or at least speaking to one.

This post has been created in association with my colleagues at Unbiased.co.uk, a well-established financial services website that can put you in touch with suitable IFAs in your area.

Reasons for Having an IFA

1. Helping Your Children Through College or University

If you have children, you will naturally want to help them complete their education safely and with a reasonable degree of comfort. Sadly the days of student grants (which I was lucky enough to benefit from in the 1970s) are well behind us now. There are various options for helping finance your children’s college or university education and a financial adviser will be able to explore these with you. They will also explain the pros and cons of the student loans system.

2 – Pension Planning

If you are over 50 you will inevitably be thinking about pension options, including when you can retire and how much income you can expect. An IFA will go through your finances with you and look at ways you may be able to boost your pension pot. From 55 onwards you can normally start to draw your pension, but you shouldn’t do this unless a financial adviser has assured you it will last you through retirement.

3. Investing

Hopefully by your fifties you will be earning a decent salary and may also have paid off your mortgage. You may also receive an inheritance or other windfall. Either way, if you find yourself with some spare cash you will want to invest it to get the best possible returns from it. An IFA will have access to all the latest information about a vast range of investment opportunities. They will guide you towards investments that are suitable for you based on your financial goals, your investment timeframe and your appetite for risk.

4. Starting Your Own Business

Especially at this time of upheaval due to Covid, many people are looking to start their own businesses in mid-life. That may be in response to redundancy or unemployment, or simply in search of a better work/life balance. An IFA can help you with the financial aspects of doing this, including raising money for tools, premises, transport and so on, or perhaps buying a franchise.

5. Emigrating or Retiring Abroad

Another way to revitalize your life may be to start afresh somewhere else, with new challenges and opportunities (and perhaps a better climate as well!). Or you may be looking to move to a favourite vacation destination to enjoy your retirement. Either way, an IFA will be happy to discuss the pros and cons with you, point out all the things you will need to take into account, and assist you with the financial arrangements.

6. Divorce

Sadly middle age sees the largest number of divorces. Your first priority here will be appointing a good solicitor to act on your behalf and protect your interests. Beyond that, though, divorce can have major ramifications for your finances. An IFA can help you assess your situation objectively and plan for a financially secure and stable future.

7. Downsizing

As the children grow up and leave home you may want to move to a smaller property – to make life simpler, save time on housework and free up money for more exciting things. An IFA can help you explore the implications of doing this and make the necessary financial arrangements.

8. Equity Release

If you don’t want to move – and are over 55 – equity release is another option for releasing funds. In recent years it has grown a lot in popularity. There are various possibilities, including home reversion plans and flexible lifetime mortgages. Most now come with a no-negative-equity guarantee, ensuring you won’t end up passing on debts to your next of kin. An IFA can go over the options with you and point out the pros and cons before you contact any providers.

9. Estate Planning

This obviously includes writing your will, but depending on your circumstances it can cover a lot of other things as well. Nobody wants to see all their money and assets falling into the hands of the taxman rather than going to their nearest and dearest. Speaking to an IFA who specializes in estate planning can give peace of mind and ensure that your loved ones are well provided for when you are no longer here yourself.

10. Helping Elderly Relatives

If you have elderly parents (or other relatives) you may find they are increasingly reliant on you for help and support. It may be up to you to arrange care for them and/or set up power of attorney so you can manage their affairs if this becomes necessary. They may also need help with estate planning (see above). An IFA can assist with all these things as well.

Getting a Free Financial Check-Up

Independent financial advisers do of course charge for their services. They are by definition unaffiliated and do not receive commission, so any recommendations they make are based solely on their client’s best interests. As I have said before on PAS, I certainly don’t begrudge paying my own financial adviser, Mike, as he has undoubtedly saved (and made) me a lot more money than he has cost me over the years.

Nonetheless, most IFAs will be happy to see you for an initial financial healthcheck free of charge. This can focus on a particular area of concern, so you could request an investments review, a pension review or a mortgage review. Alternatively, if you’re not sure which aspect of your finances needs more attention – or indeed whether you need advice at all – you could simply request a broad financial healthcheck.

Here’s what. Adrian Kidd, a financial planner at Radcliffe & Newlands, says about his approach on the Unbiased website:

‘I’d generally offer one or possibly two free consultations, taking about an hour, and these can be as specific or as broad as required. When someone books a financial healthcheck with me, I ask them to bring along all their documents relating to their finances – savings, investments, mortgages, loans, insurance, pensions, the works – so I can build up a complete picture of their affairs. I then go through these in more detail after the consultation, and follow up with an email that gives a summary of their overall financial situation.’

In these free check-ups: advisers won’t generally talk to you about products at all. The process of choosing the right products comes later, after the adviser has built up an understanding of you as a person and your financial planning needs. Only then will they recommend products, if asked to do so.

If you follow my link to the Unbiased website, you can complete a short, step-by-step questionnaire designed to identify the best type of financial adviser for your needs. You will then be shown a selection of suitable advisers in your area with contact information. They will be happy to answer any queries you may have and arrange an initial meeting without obligation.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Unbiased.co.uk. If you click through my link and end up becoming a client of a financial adviser listed on the Unbiased site, I may receive a commission for introducing you. This will not affect the service you receive or any fees you are charged if you decide to proceed further.

This is a fully updated version of a post originally published in 2020.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m reviewing a new book called Extreme Frugality by my blogging colleague Jane Berry, also known as Shoestring Jane.

Jane runs a popular blog called Shoestring Cottage which follows her journey towards making a creative, happy and sustainable life on much less. She also runs a YouTube channel as Shoestring Jane, where she shares her thrifty life and money-saving ideas. And she is also a writer for the estimable Mouthy Money site, to which I am a regular contributor myself.

Extreme Frugality is divided into 13 main chapters, as follows:

Chapter 1: Frugal Foundations

Chapter 2: Stuff, Stuff and More Stuff

Chapter 3: Cooking and Eating Like Grandma

Chapter 4: Granny’s advice – ‘Make do & Mend’ and ‘Waste Not, Want Not’

Chapter 5: Buying Second-Hand and Getting Everything for Less

Chapter 6: Slashing Your Monthly Bills

Chapter 7: Making a Frugal Home

Chapter 8: The Frugal Cleaner

Chapter 9: The Frugal Garden

Chapter 10: Frugal Fashion: Dress for Less

Chapter 11: Frugal Fun and Travel

Chapter 12: A Frugal Christmas

Chapter 13: Health and Well-being on a Budget

There is also a section of references and resources at the end.

As you may gather, Extreme Frugality aims to show you how to develop thrifty habits (as our grandparents had to). The author says the purpose of doing this is to cushion you against hard times, be creative with what you have, buy just what you need, and eliminate waste from your home.

As a one-time professional writer and editor myself, I was impressed by the high standard to which Extreme Frugality has been produced. The style is clear and accessible, and the content neatly set out without any unnecessary typographical or design gimmicks.

Obviously in the current cost-of-living crisis we are all having to tighten our belts, so the advice in the book is very apposite at present. There are also plenty of suggestions for preventing waste, so the book should appeal to anyone concerned with their environmental impact as well.

It’s hard to pick out highlights as every chapter is packed with valuable tips and advice, but I especially enjoyed Chapter 6, which takes you through a wide range of methods for slashing monthly bills, including energy, water, Council Tax, broadband and so on. The advice in this chapter alone could easily save you thousands of pounds a year. But all the chapters contain useful advice, ideas and information. Even as a money blogger myself, I don’t mind admitting I learned a lot from it.

In summary, Extreme Frugality is a great guide for anyone looking to save money and reduce waste in these challenging times. It would also make an excellent gift for a friend or family member. I am happy to give it my highest recommendation.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I was sent a free copy of Extreme Frugality (in PDF form) to review. Please be aware also that this post (and others on PAS) includes affiliate links. If you click through one of these and make a purchase or perform some other defined action, I may receive a commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. As I only updated my full review of Nutmeg last week, however, I will keep it fairly brief today.

Nutmeg is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold to avert the risk of pound-cost ravaging.

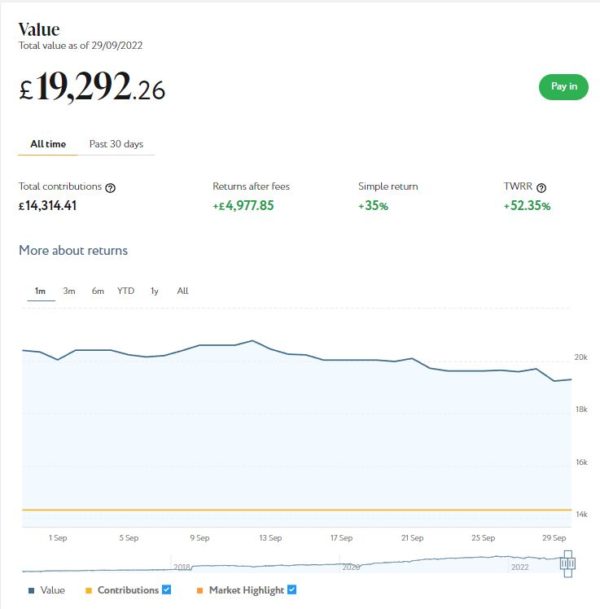

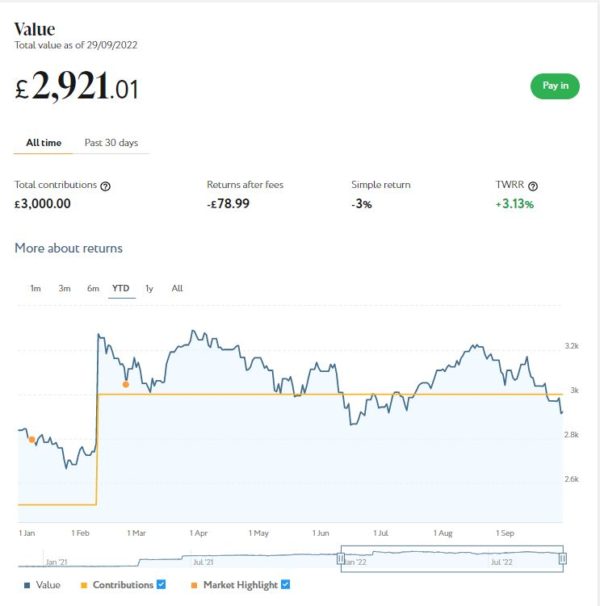

My main Nutmeg portfolio, which I opened back in 2016, is currently valued at £19,733. Last month it stood at £19,292 so that is a rise of £441. My smaller Smart Alpha investment (opened in 2020) is currently valued at £2,987. Last month it stood at £2,921, so that is a rise of £66. My total Nutmeg investments have therefore increased by £507 month on month.

While the rise in October is of course welcome, my Nutmeg investments are still down by about 11% in value since the start of the year. As I said in my recent Nutmeg review, that’s clearly disappointing, but it’s still a lot less than the amount by which they went up in 2021 alone. And I am still over £5,400 in profit overall. I am therefore philosophical about this, recognising that all investments have their ups and downs and Nutmeg is hardly alone in seeing a drop in values this year. But I do understand why people who started investing with them in the last twelve months or so may be feeling disappointed. You might like to read this recent article on the Nutmeg blog where they discuss the performance of Nutmeg portfolios in 2022 and examine the outlook going forward.

There is actually an argument that now may be a good opportunity to invest while asset values are depressed. At some point we will see a recovery and people who invest at the present time will be well placed to benefit from this. Of course, nobody knows for sure when the recovery will happen or how much further asset values might fall first. Nonetheless, I am certainly considering adding further to my Nutmeg investments in the coming months.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £81.40 in revenue from rental and £30.80 in capital growth, a total of £112.20. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though five have had their repayment dates put back.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie. Unsurprisingly my investment has been up and down in the last few months, but it is currently about $8 in profit. In these turbulent times I am quite happy with that.

In addition, since I started on eToro, the pound has weakened against the US dollar, so my investment has benefited from this. My $508 US is now worth around £440 in UK pounds, so I am effectively £28 up overall. I am not claiming this as a particular benefit of eToro, but it does demonstrate how exchange rate fluctuations can sometimes work in your favour!

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full in-depth review of eToro here. I am also planning to publish a more in-depth look at eToro copy trading on the blog soon.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled How to Save Money on Petrol. I was actually commissioned to write this when petrol prices were peaking. Since then they have fallen back somewhat, but with no end in sight to the war in Ukraine prices could easily shoot back up again. In the article I discuss my favourite website for monitoring petrol prices locally and also set out my top tips for cutting your petrol (or diesel) consumption.

As a matter of interest, Mouthy Money recently asked if I could increase the number of articles I write for them (so I guess I must be doing something right!). From November they will be publishing two articles a month from me. While they don’t pay me a fortune, the extra cash will undoubtedly help a lot in the cold winter months ahead.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. By now everyone should have received the first instalment (£66) of the £400 rebate all UK residents are due on their energy bills for the next six months. If not, chase it up with your energy supplier.

I am with EDF, and they are crediting the rebate payments to my bank account once my monthly direct debit has been taken. Other energy suppliers are doing it differently, e.g. deducting the rebate from monthly direct debits before they are taken. This article from the popular Moneysavingexpert website explains how different energy suppliers are applying the rebate.

I also received a letter last week confirming that, as I receive the state pension, I shall be getting an enhanced Winter Fuel Payment of £500 in November or December this year, which will be very welcome as well 🙏

In the last few years I also qualified for the Warm Home Discount, which this year is being increased from £140 to £150. The rules are changing, however, and I suspect I shall be one of the people who misses out. The full new rules still haven’t been announced, but I will update my blog post about WHD as soon as I know more.

As I’ve said previously, the government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The Trading 212 offer closes on 8 November 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course 🙂

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Investing can be confusing, and it’s easy to lose track of where your money is going. Thankfully, Microsoft Excel has many tools that can help you effortlessly track your investments.

Excel offers many ways for users to easily track their investments, such as by tracking the value of their portfolio over time, analyzing past performance, and comparing how different asset classes performed in similar market conditions.

Excel can also help investors stay on top of balances and transaction activity across multiple accounts. It allows them to visualize how these transactions affect their total wealth over time. This information can help investors decide when to invest more or pull out some cash for other uses.

Excel can be beneficial for investment tracking, especially if you’re saving for retirement and want to see how much progress you’ve made over time.

You can either enrol in Excel training to learn a few tips or tricks to analyze your investment data (which will serve you well for life), or you can follow the guide below for a quick solution.

Table of Contents

Create a Portfolio

A portfolio is a collection of individual investments held by an investor. A typical portfolio will include stocks, bonds, mutual funds, exchange-traded funds (ETFs), options, and other securities.

If you’re looking to create a portfolio in Excel, here’s how to do it:

1. Open up the spreadsheet application on your computer,

2. Click on ‘File’ and select ‘New’.

3. Select ‘Blank Workbook’ from the new screen’s drop-down menu. This will open up a new file for you to start creating your portfolio in Excel.

4. Type the heading ‘Accounts’ in one of the columns. The accounts should be listed from largest to smallest by value or assets under management (AUM). We recommend listing these accounts as rows instead of columns to make it easy to track.

5. Create columns for the type of investment you have in your portfolio against each account. These include cash accounts, bonds, fixed-income funds, stocks and equity funds, commodities, and other assets like real estate or intellectual property rights.

6. Now create another column with the heading ‘Shares/Investment’ and enter the data for each investment appropriately.

7. You can add columns related to Date, Security Name, Number of Shares or Units Owned, Purchase Price Per Share/Unit (or Cost Basis), and Current Market Value Per Share/Unit (or Current Value). In addition, add columns for Cost Basis (the original purchase price), Gain/Loss Per Unit, and Total Gain/Loss For All Units (for each security).

8. You may also want to include columns for Percent Gain/Loss.

9. Save the spreadsheet as an Excel file and then close it.

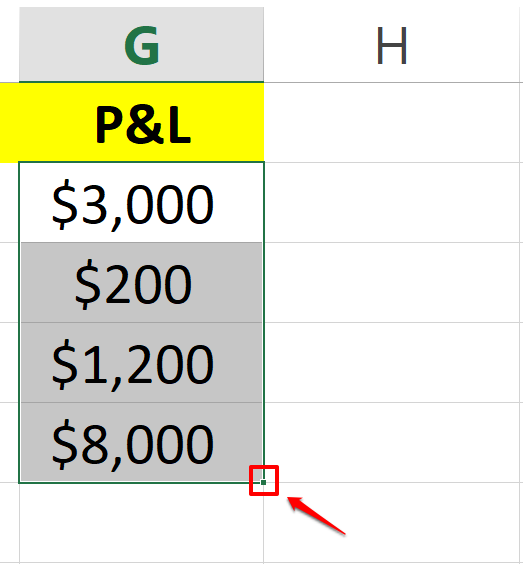

Use the ‘Difference Formulas’ in Excel

Excel’s most useful feature is its ability to calculate differences between two numbers. For example, if you have a list of investment values and you want to know how much money you have made since your purchase, you can try the following method:

1. Click the cell where you want to calculate the difference between your asset’s current price minus its original purchase value.

2. Type the equal sign ‘=’ and then select the cell containing the current value of your investment.

3. Type the minus sign ‘-‘ and then select the cell containing the original purchase price of the investment.

4. Press enter, and the difference will be calculated.

5. Now click and press the small square at the end of that cell (containing the difference), and drag it downwards to calculate the difference of each dataset automatically.

Use the ‘Percent Return Formulas’ in Excel

To track the return on investment over time, you can use Microsoft Excel’s percent return formulas. These formulas calculate the percentage increase or decrease in an investment’s value over time.

The formula for percent return is: (Current price – Purchase price) ÷ Purchase price

Here’s how you can apply the percent return formula in Excel:

1. Select the cell where you want the percent return formula to be calculated.

2. Type the equal sign ‘=’ and add an open parenthesis ‘(‘.

3. Select the cell containing the current value of your investment.

4. Type the minus sign ‘-‘ and select the cell containing the original purchase price of your investment and then close the parenthesis ‘)’.

5. Now, type the forward slash ‘/’ and select the cell containing the original purchase price.

6. Press enter, and the percent return will be calculated.

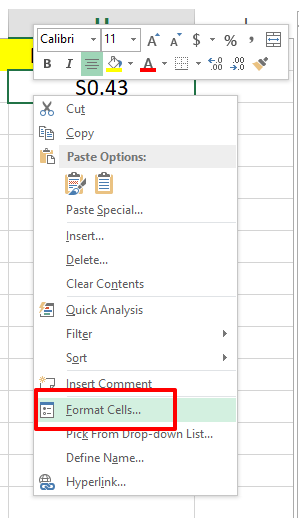

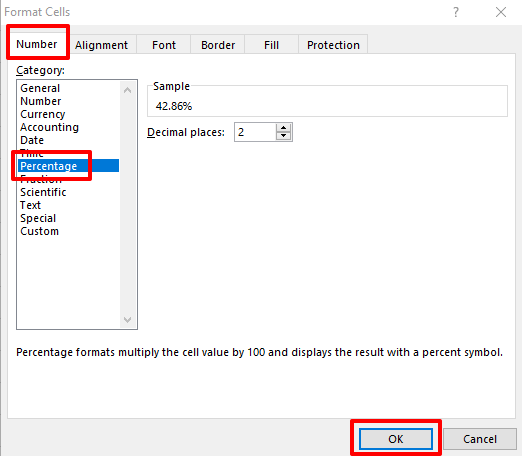

7. To make values appear as percentages, right-click on the cell, select the option of Format Cells, and select Percentage under the number tab.

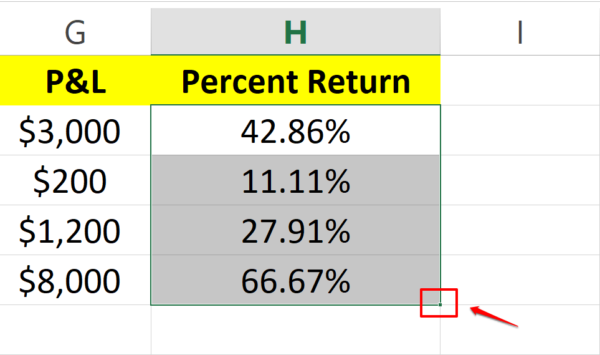

8. Once done, click and drag the small square at the bottom right corner of your percent return cell and copy the formula for the rest of the dataset.

Use Advanced Excel Features to Customize your Sheet

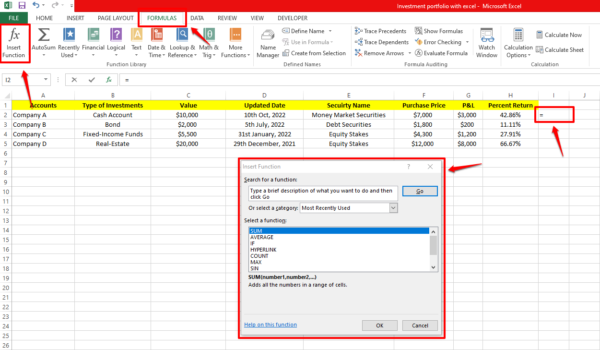

Functions in Excel are a way for you to manipulate data in Excel programmatically. They can be used to perform calculations, transform data, and create new values.

You can find a list of all built-in functions in the Formula tab menu in Excel. To access it, click on any cell, navigate to the Formula tab and choose the ‘Insert Function’ option. The Insert Function dialogue box will appear, from where you can choose the function you are looking for by going through the list.

Here are the 10 most popular functions in Excel:

SUM function

IF function

LOOKUP function

VLOOKUP function

MATCH function

CHOOSE function

DATE function

DAYS function

INDEX function

FIND, FINDB functions

The best way to learn about each function is by using it. Try out different arguments and see what happens.

To Conclude

Excel is an excellent way to track investments because it saves and calculates dependable data. Also, you can use the program to graph your data and see how they change over time.

Thank you to my friends at Acuity Training for an informative guest article.

I use Excel spreadsheets for keeping track of my self-employed earnings and send them to my accountant once a year so that he can produce my annual accounts from them.

I do also use Excel for keeping track of my investments, but only in a very basic way. This article has inspired me to be a bit more ambitious with Excel and use formulas to automatically calculate the total and percentage returns from my investments, and so forth.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have an infographic for you from my friends at ecommerce platform Quill. It sets out some of their top tips for working from home, and especially making the most of technoiogy.

While the purpose of technology is to make life easier, working from home comes with its own set of challenges. But with time – and by following some basic tips and guidelines – remote work can go from feeling like an uneasy compromise to becoming an accessible, convenient and comfortable way of working.

Whether you’re a technology guru or a novice, remote work shouldn’t feel like an obstacle course. Technical problems such as lagging wifi, for example, can be resolved by means of an upgraded modem or network extender. Other common consequences of working remotely, however – including loneliness and lack of motivation – are more difficult to tackle and can negatively affect efficiency and productivity.

Fortunately a few changes to your remote working approach can make a huge difference. From your choice of attire to the design of your workspace and how you communicate with colleagues, this graphic shares a few simple but effective hacks to help overcome remote-working challenges.

Many thanks again to Quill for their infographic and tips. I have been working from home for over 30 years myself now, so I do generally agree with all of the above. I have very occasionally been known to work in my pajamas but have to admit this is best avoided really!

I definitely agree it’s best to have part of your home as your designated workspace. Ideally this could be a separate study or office, but at least a quiet corner where you can set up your equipment and files and not have to pack everything away at the end of the day. Growing numbers of people are now using garden sheds or extensions for home working, and this can also be a good solution.

Garden office pods are another option that is growing in popularity. These can provide a space-saving refuge in which you can avoid noise and other distractions and focus on getting your work done.

I also think that if you’re working from home, it’s vital not to let yourself become isolated. It’s very important to keep up connections with colleagues, friends and family. Home working can be especially challenging if you like and are accustomed to having colleagues to talk to. You really do need to build some social interactions into every day if possible – ideally face to face, but at least via the phone and/or social media. Your mental health may depend on it 🙂

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: Posts on Pounds and Sense may include affiliate links. If you click on one of these and go on to make a purchase or perform some other defined action, I may receive a commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a three-night break in Barmouth in Wales. The town is also known by its Welsh name of Abermaw.

Barmouth is a traditional Welsh seaside resort. I’ve visited a few times over the last few years but haven’t actually stayed there for over 25. I thought it was high time I rectified that!

On this occasion I stayed at Tyr Graig Castle, a hotel I discovered online and booked via Booking.com. I’ll say more about the accommodation below.

Barmouth is about ten miles south of Harlech. The nearest large town is Aberystwyth. Here is a map of the area from Google Maps.

Table of Contents

Accommodation

As mentioned above, I stayed at a hotel called Tyr Graig Castle. Unfortunately I neglected to take any photos of the exterior, but you can see the view from my bedroom window in the cover image (including a length of parapet!). There are, of course, more photos on the hotel website.

Tyr Graig Castle is a characterful Victorian building, originally constructed in the late 1890s. it retains the style of the Victorian era, with stained glass windows, wood panelling and highly decorated floors and ceilings.

Tyr Graig is a traditional Welsh name and translates as ‘House on the Rock’. It stands about 200 feet above Barmouth, overlooking Cardigan Bay, across which can be seen the Llyn peninsula and Bardsey Island. The building was completed in 1892 as a family home for W.W. Greener, a famous Birmingham gunsmith. It was designed in the Gothic style that was popular at the time. Its unique shape was chosen by Mr Greener himself. It resembles both a medieval castle and an open double-barrelled shotgun when viewed from above.

I stayed in a first-floor turret room. This had round walls, and windows providing stunning views across the bay. There was a small bathroom with a shower rather than a bath. While generally I found the room perfectly comfortable, I did find the lighting rather dim. There was no ceiling light, just some uplighters on the walls and bedside lamps with low-powered energy-saving bulbs. My eyes are admittedly not the best these days, but I had to use the torch app on my phone in the evening to see well enough to read!

The breakfasts (and optional evening meals) at Tyr Graig Castle are served in the dining room and adjacent conservatory. The latter has wonderful views out to sea and there was a bit of a rush to get one of the four window tables (see photo below). Early risers had a definite advantage here! I was pleased to discover that they recently reinstated the breakfast buffet, where you can help yourself to cereal, fruit, yogurt and so forth. You could then order a cooked breakfast which was brought to your table. These were excellent and set me up for the day 🙂

You could also opt to eat in the restaurant in the evening. Like most guests (as far as I could judge) I chose to do this, as Tyr Graig Castle is a little way out of the town centre and other dining options in the area are limited unless you want to drive. The food was good and the portions were generous. My only slight criticism is that the menu was the same every night. There was a reasonable choice, but a bit more variety day to day (even if just a daily special) would have been appreciated.

The service from both the staff and the charming owners (Mike and Trudy) was uniformly excellent. The hotel had free wifi which worked perfectly during my stay (not always the case in my experience).

One other observation is that this is the first time I had stayed in a hotel – as opposed to self-catering – since the days of the pandemic. I was pleased to discover that by and large things are back to normal now. One small difference is that I was asked at check-in if I wanted my room serviced every day. It was the first time I can remember being asked this, as pre-Covid it would have been assumed. But I guess some people are still nervous about having someone else in their room even if they aren’t there at the time. So I do understand why the hotel ask this now.

Financials

As Pounds and Sense is primarily a money blog, I should say a word about this.

I paid £336 for my three-night stay at Tyr Graig Castle, which works out to £112 per night (including VAT). Considering that included a substantial breakfast as well, I thought the price was very reasonable.

The optional evening meals were, of course, extra. The prices were, I would say, good value as well. I paid around £25 a night for my evening meals, which included a main course and dessert (or cheese and biscuits) and coffee. I generally had a small bottle of sparkling water with the meal, but if I had gone for wine or beer, that would obviously have pushed the price up a bit.

Things to Do

I won’t give you a full account of everything I did while I was there, but here are a few highlights.

Harlech

Harlech is about 20 minutes’ drive north from Barmouth (or a short train journey on the scenic Cambrian line). I spent my first morning here.

Harlech has some charming shops and cafes, and a long, sandy beach. But it is probably best known for its stunning castle (see photo above).

Harlech Castle was built by Edward I during his invasion of Wales between 1282 and 1289. Since then it has had a long and interesting history, including serving as the home and military HQ of Owen Glendower, the Welsh prince who led a long-running war of independence with England during the late Middle Ages. UNESCO considers Harlech Castle, with three others at Beaumaris, Conwy and Caernarfon, to be one of “the finest examples of late 13th century and early 14th century military architecture in Europe”, and it is classed as a World Heritage Site.

Admission to Harlech Castle costs £8.30 for adults or £7.70 for seniors (over 65). You can also buy a family ticket for two adults and up to three children for £27.40. Children under 5 receive free entry, as do people with disabilities and their companions. All prices are correct as at September 2022.

Harlech Castle is impressive and well worth a visit. You can climb the stone staircases in several of the towers and walk along the battlements (obviously you need to be reasonably fit to do this). From up here you can enjoy spectacular views across the sea and towards the mountains of Snowdonia. At ground level there is a room with some information about the castle and its history. I was glad to have this, as the ticket office had run out of guidebooks in English and only Welsh language ones were available.

I should maybe also mention that Harlech Castle has an excellent cafe with plenty of seating inside and out. I enjoyed a very nice cappuccino and cake here!

Portmeirion

Portmeirion is a beautiful Italianate village created by the architect Clough Williams Ellis. These days it is probably best known as the location for the 1960s cult TV series The Prisoner, starring Patrick McGoohan. I drove here in the afternoon after spending the morning in Harlech. It’s a wonderful place to while away a few hours.

There is an admission fee to get into Portmeirion, At the time of writing (September 2022) this is as follows:

Adult £17.00

Concessions £13.50 (this applies to anyone aged 60+ or a student with a valid student ID)

Children £10.00 (5-15 years)

Children (under 5 years) Free

There are also discounted family tickets for various permutations of adults and children.

You can also get free admission (in the afternoon) by booking a minimum two-course lunch at Castell Deudraeth; this is part of the Portmeirion estate, a short walk from the village itself. Free admission to the village is also available if you book a spa treatment or afternoon cream tea there.

More information is available on the Portmeirion website. One thing you may need to know is that they don’t allow dogs (other than guide dogs) into the grounds.

Fairbourne Railway

The Fairbourne Railway is a miniature steam railway. It’s a bit of a drive to get there from Barmouth, as you have to cross the estuary, which entails driving several miles inland and back again. However, you can get a ferry (actually a motorboat) from Barmouth seafront that takes you to the far end of the Fairbourne Railway in under ten minutes. This costs the princely sum of £2.50 (September 2022 price) and provides some wonderful views of Barmouth and the railway bridge. Highly recommended!

If you are energetic you can also walk from Barmouth to Fairbourne via the railway bridge (which isn’t open to cars). On this visit I ended up walking to the Fairbourne Railway and then getting a ferry back.

A one-way trip on the Fairbourne Railway costs £7.60. Alternatively you can buy a Day Rover ticket for £11.50 which entitles you to go up and down the line as many times as you like. This is obviously better value! You can choose whether to travel in an open or closed carriage (it all costs the same). There is a small museum at the Fairbourne end of the line with information about the railway’s history and some exhibits. There is also a separate room housing a large model railway. This is free to enter, but you have to insert a coin to watch the train go round 🙂

The ticket office at Fairbourne incorporates a cafe selling drinks, sandwiches and snacks (no cooked meals though). At the Barmouth Ferry end of the line there is also a cafe but this is only open during the peak summer months.

Final Thoughts

I enjoyed my short break in Barmouth and am happy to recommend both the town and the hotel where I stayed for a short break.

As mentioned above, Barmouth is a traditional Welsh seaside resort, and none the worse for that. It has a clean, attractive promenade and a beautiful sandy beach which goes out a long way to the sea. It is hard to imagine it getting overcrowded!

There is plenty to do for families with children, including a funfair and amusement arcades. There are various restaurants and fast food outlets along the seafront. There is also a railway station with regular trains to Pwllheli in one direction and Aberystwyth and beyond in the other. Road connections are good as well.

Also worth checking out while you are there are Ty Crwn, a 19th century lockup for drunks and petty offenders (picture below). There is also a small museum near the seafront dedicated to the town’s maritime history. Entry to this is free, though donations are appreciated.

Finally, as mentioned above, I recommend taking a stroll across the half-mile-long railway bridge over the Afon Mawddach river. This is the longest timber viaduct in Wales and one of the oldest in regular use in Britain (it opened in 1867). It offers some stunning views across the estuary. You can also walk on to Fairbourne and the Fairbourne Railway (see above).

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold, incidentally, to avert the risk of pound-cost ravaging.

As the screenshot below of performance last month shows, my main portfolio is currently valued at £19,292. Last month it stood at £20,344 so that is a fall of £1,052.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,921 compared with £3,091 a month ago, another fall of £170.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

There is no denying that these falls are disappointing, especially with my Smart Alpha portfolio now worth less in total than I have contributed to it. As I’ve noted previously on PAS, however, you do have to expect ups and downs with equity-based investments. And this year there has been no lack of volatility, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

About my only consolation is that things could have been even worse if – paradoxically – I’d opted for a lower-risk level with my investments. In their latest blog update, Nutmeg reveal that low and medium-risk portfolios actually performed worse overall last month than high-risk ones. I have copied below their explanation for this:

By design, Nutmeg’s low- and medium-risk portfolios have more exposure through ETFs to assets that are priced in sterling and with limited foreign currency exposure. As you will have seen in the headlines this week, the pound hit an all-time low against the dollar with markets initially placing little faith in the chancellor’s tax-cutting and pro-growth agenda.

This year it has been rewarding to hold foreign currency with sterling particularly weak versus the dollar. Some of our high-risk portfolios have benefited from currency moves, while low- and medium-risk portfolios have not. They haven’t lost money from having low foreign currency exposure, they just haven’t benefited from it.

Secondly, low- and medium-risk portfolios by design have more exposure – again through ETFs – to government bonds, which in ‘normal’ times are considered something of a safe haven and have much lower volatility than equities. After all, it is still highly unlikely that the UK government would default on its debts.

In a nutshell (no pun intended) low- and medium-risk Nutmeg portfolios hold a higher proportion of investments in pounds sterling and UK government bonds. These are normally regarded as lower risk, but last month both took a particular hammering. So in comparison nominally higher-risk portfolios like mine actually performed somewhat better.

This is one more reason I’m glad I opted for higher risk levels with my Nutmeg portfolios (9/10 for my main one and 5/5 for my Smart Alpha). If you haven’t yet seen it, you might also like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was actually pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

Since I started investing with Nutmeg in 2016 – and despite everything that has happened this year – I have still made a total net return on capital of £4,977 (35% or 52.35% time-weighted) on my main portfolio. So I can afford to be philosophical about the recent falls. Indeed, I am considering topping up my Nutmeg investments again now while asset values are depressed.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £76.51 in revenue from rental and £63.58 in capital growth, a total of £140.09. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled My Odd Smart Meter Story and Why Despite This I Still Recommend Them. In the article I discuss my rather strange experiences with a smart meter, which stopped working after I switched supplier and then rather mysteriously started again two years later! As per the article title, I do still recommend getting a smart meter, especially in these times of soaring energy bills.

Also in September I enjoyed a final (probably) short break of the year in Barmouth in Wales. I stayed at a Victorian Gothic hotel called Tyr Graig Castle. I was lucky with the weather, and enjoyed visiting nearby Harlech and Portmeirion (see cover image) as well as Barmouth itself.

I shall be publishing a full review of my short break in Barmouth soon. In the meantime, here is a photo of a rather splendid sunset taken from the hotel restaurant…

Finally, I know a lot of people are extremely anxious about the cost-of-living crisis. As I said last time, though, it’s important not to panic. I recommend a three pronged-approach of maximizing your income, minimizing your expenditure, and budgeting carefully (using your resources as effectively as possible, in other words).

Bear in mind, also, that a range of government support measures have been announced to mitigate the worst effects of the crisis. This government Help for Households website has a useful summary of all the help available and is regularly updated.

In the meantime, please do check out some of the other posts on Pounds and Sense for additional advice and resources, especially in the Making Money and Saving Money categories.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

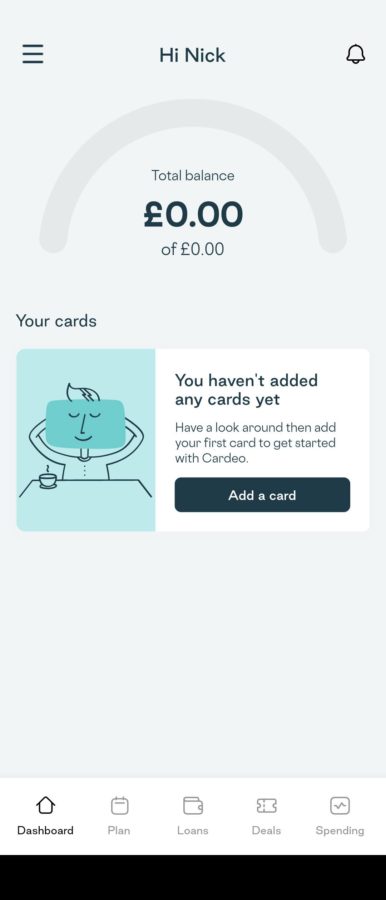

Today I’m looking at Cardeo, a new, free credit card management app. It is designed to help save you money on your credit cards.

Table of Contents

How Does Cardeo Work?

Cardeo brings together data from all your credit cards into a single app using open banking.

It then gives you insights into your borrowing and spending. Their payment plan works out how long it will take to pay off your cards. You can set a repayment target, decide how to get there, and repay all your cards through a single monthly payment (you can also use it with just a single credit card). Reminders make sure that you never miss a repayment.

You can change the payment plan as much as you like: edit the date, target or the monthly amount, make extra one-off payments, and pause/restart the plan as it suits you.

Cardeo works with most (though not yet all) UK credit cards. You can view the entire list here. All the most popular credit card providers appear to be covered, including Barclays, HSBC, Santander, MBNA, Virgin Money, and so on.

How Can Cardeo Save You Money?

First and foremost, payment reminders from Cardeo help you pay your cards on time each month. That way you avoid extra interest and late payment fees from your card provider. If – like me – you are prone to forget these payments on occasion, this is a valuable money-saving feature in its own right.

The Cardeo payment plan offers a choice of repayment strategies, including the so-called avalanche method. This repays the highest interest rate cards first (after minimum payments are covered). By this means you will minimise interest charges and pay off your cards in the shortest possible time.

Cardeo gives you insights into your credit card usage, helping you make smarter decisions about your spending and saving. Finally, Cardeo also offer deals from other parties which are designed to save you money.

How Does Cardeo Make Money?

As already mentioned, the Cardeo app is free to download and to use, with no in-app purchases or charges.

Cardeo say they make a small amount of money from deal providers each time a customer takes up a deal from the Cardeo app (e.g. a low-interest loan).

My Experience

I found downloading and installing the Cardeo app straightforward – I got mine from Google Play as I have an Android phone.

When you first open the app you have to put in certain details, including your full name and address, phone number (for log-in purposes), and so on. You may also be required to enter an email invitation code. All this took me maybe five minutes at most. I then saw the screen below…

After that, I clicked on ‘Add a Card’ and selected the name of my credit card provider, MBNA. I then had to follow a link to their website and log in with my usual online security credentials to authorize open banking.

Frustratingly, this took me a few attempts. MBNA required me to answer an automated call from them and enter a four-digit code on the telephone keypad to complete the process. Initially it told me I had got the code wrong, despite the fact that I had copied it from the MBNA site. I persevered, however, and eventually the card was linked to my Cardeo account 🙂

As a side note, I am probably not the ideal candidate for Cardeo, as these days I only have one credit card and use it just once or twice a year. The rest of the time, I use my bank debit card instead. I am in the fortunate position of having enough income/savings that I don’t need to borrow on my credit card. On the odd occasion I do use it, it is typically for larger purchases to take advantage of the extra legal protections you get with credit card purchases over £100.

Nevertheless, I am happy to confirm that everything in the Cardeo set-up process went smoothly for me, with the sole exception of the hiccup regarding authorizing open banking with MBNA. The latter wasn’t Cardeo’s fault, and has in fact happened to me before with MBNA. Hopefully you will be luckier!

My Thoughts

If you’re a regular credit card user, and especially if you pay interest on an outstanding balance (or balances), in my view Cardeo offers a great way to minimize the charges you pay and help reduce your debts as quickly as possible.

As I have noted before on Pounds and Sense, credit card borrowing can be very expensive, especially over a long period. So if you are in debt on your cards, it is important to take all possible steps to pay this off as quickly as possible, and Cardeo will certainly help you with this. It can also help build your credit score by ensuring you don’t miss any payments.

A further benefit is that Cardeo will save you administrative time and hassle. You simply make one monthly payment and this is automatically allocated by the app across all your credit cards.

I know some people are uneasy about open banking, and if this is a major concern then Cardeo may not be for you. Open banking is, however, now a well-established option allowing consumers to gain an overview of their financial products. If you’re trying to get (and keep) your finances under better control, this can only be beneficial. Cardeo require your permission to use open banking and you can remove this at any time. Your data is encrypted and your login details are kept hidden. You can read more about the security and privacy protections here if you wish.

As always if you have any comments or questions about this post, or Cardeo more generally, please do leave them below.

Disclosure: This post includes affiliate links. If you click through and download the Cardeo app or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive in any way.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at Buy Now Pay Later (BNPL). This is a retail payment option that has grown massively in popularity over the last year or two. It is most often used online but is also available at some physical stores (e.g. New Look).

Most people’s first contact with BNPL comes when they are shopping online and it appears in the list of payment options.

As the name suggests, BNPL allows you to buy a product (or products) now and pay later. This typically involves paying a deposit followed by a short series of instalments. You may also be offered the opportunity to pay the entire sum after 30 days with no initial deposit.

So if – for example – the product/s in your basket cost £90, with BNPL you may be able to purchase with a down payment of just £30 and two further instalments of £30 at 30-day intervals.

One big attraction of BNPL compared with credit cards is that generally if you pay your instalments on time, you will not be charged interest. The BNPL firms make money by taking a commission from the retailer, which means they don’t need to charge anything to customers.

Another possible attraction of BNPL is that you won’t normally be required to complete a formal (‘hard’) credit check. You will just be asked a few quick questions and will be told there and then if you are eligible. The fact that you applied for BNPL won’t generally appear in your credit file or affect your personal credit score (whereas applying for a credit card certainly will).

This is likely to change in future, however, with greater regulation coming to the sector from 2023. Hard credit checks may be required from then on, in response to fears that BNPL is encouraging some people to spend more than they can afford.

BNPL is offered by a range of financial services companies, the best known of which in the UK are Klarna, Clearpay and LayBuy.

Who Uses BNPL and For What?

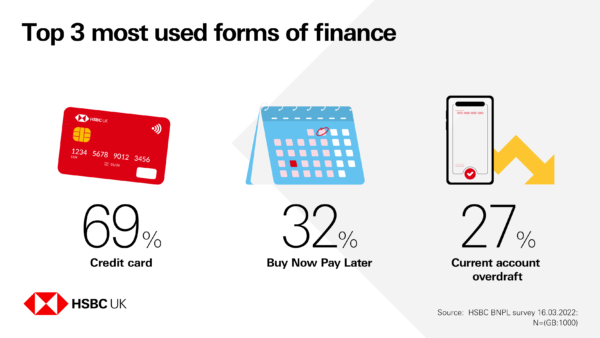

Research from HSBC shows BNPL has become the second most used form of finance behind credit cards (see graphic below). Women are more than twice as likely as men (43% v 21%) to use it.

The HSBC survey found that BNPL was most popular among 25-34-year-olds, with nearly half saying they had used it in the past year (49%), followed by 18-24s (45%) and 35-44s (45%).

As regards what it is used for, the survey found that clothing was the most frequent purchase type with BNPL, followed by food & beverages, shoes, appliances & electronics, and games & toys. This is summed up in the graphic below.

What Are the Pros and Cons of BNPL?

In the HSBC survey, those using BNPL said they valued it over other forms of finance because of the ability to spread payments (20%). They found it quick and easy to use (15%) and more affordable (13%) – with 87% of people who had used it in the past 12 months saying they were likely to use it again in the next year.

BNPL is also popular among people who like to try before they buy (typically with clothing). By buying this way, you may be able to try your purchase without any monetary outlay and return it with no further commitment if you don’t like it.

Sixty percent of BNPL users in the HSBC survey did express some caution, however, saying one of the top three drawbacks was it was too easy to get into debt or overspend. One in five listed lack of availability as a key disadvantage (20%), while one in ten (12%) said the fact it didn’t build their credit score was an issue.

These concerns were also raised by those who hadn’t yet used a BNPL service – with 62% saying one of the main barriers to use was it appeared to be too easy to get into debt or overspend, and nearly one in three (30%) saying that was the primary factor.

Thanks again to my friends at HSBC UK for allowing me to share their survey results and graphics.

With the current cost-of-living crisis, many of us are feeling the pinch at the moment. So it is easy to see the attraction of BNPL for helping budgets stretch a little bit further.

In my view, BNPL can be a sensible option if you need short-term credit and are confident you will be able to repay the money over the period specified. One big attraction is that most BNPL offers do not involve paying any interest as long as you stick to the terms of the agreement. Neither is using BNPL likely to affect your credit score (though it won’t help build it either). And, as mentioned above, payment-in-30-day offers can allow you to try before you buy without any up-front financial outlay.

Some BNPL firms also offer longer-term credit up to 18 months. A hard credit check is required for this and interest will be charged, so this is more like a personal loan. Interest rates tend to be high and you may end up paying back considerably more than you borrowed. I do not recommend going down this route, unless you really don’t have any viable alternative.

Of course, BNPL does have the potential for encouraging overspending and drawing you into debt you then find difficult to repay. If you miss any of the scheduled payments, penalty fees and/or interest may be charged and your credit rating may also be adversely affected. Ultimately, a debt recovery agency may be called in. If you think this is a risk, it may be better to wait and save up before making a purchase in the traditional way.

As always, please feel free to leave any comments or questions about this post below. I would also be very interested to hear from any readers who have used BNPL themselves. What did you use it for and why? And would you do it again?!