Right now – as you can see on the official UKHSA website – flu and other respiratory viruses (though not Covid) are soaring.

Of course, winter often brings a surge in colds, flu and other seasonal illnesses. But while not unexpected, these infections can be a nuisance at least. And – in the case of older people especially – they can sometimes be life-threatening.

While a balanced diet, regular exercise and adequate sleep remain the cornerstones of good health, certain supplements can provide an extra layer of protection. Here’s a guide to the best supplements to support your immune system during the colder months.

1. Vitamin D

Why it’s essential: With limited sunlight during UK winters, many people experience a drop in their vitamin D levels. This nutrient plays a crucial role in immune function and helps reduce the risk of respiratory infections.

How to take it: Public Health England recommends everyone consider a daily supplement of 10 micrograms (400 IU) of vitamin D during the autumn and winter months. Higher doses may be necessary for those with deficiencies, but consult a healthcare professional first.

2. Vitamin C

Why it’s essential: Vitamin C is known for its immune-boosting properties and its ability to reduce the duration and severity of colds. It’s also a powerful antioxidant that helps protect cells from damage.

How to take it: A daily dose of 500–1,000 mg is generally safe for most people. You can also pair supplementation with dietary sources like oranges, kiwi fruit and bell peppers.

3. Zinc

Why it’s essential: Zinc is vital for immune cell function and has been shown to shorten the duration of cold symptoms when taken early. It also helps your body fight off viruses more effectively.

How to take it: Lozenges containing 10–15 mg of zinc can be taken at the onset of a cold. Long-term supplementation should not exceed 25 mg daily unless advised by a healthcare professional.

4. Probiotics

Why it’s essential: A healthy gut microbiome supports immune function, and probiotics help maintain this balance. Some strains, like Lactobacillus and Bifidobacterium, are particularly effective in reducing the risk of upper respiratory tract infections.

How to take it: Look for a high-quality probiotic supplement with at least 1 billion CFUs (colony-forming units). Yogurt and fermented foods like kimchi and sauerkraut can also be excellent natural sources.

5. Elderberry Extract

Why it’s essential: Elderberries have been traditionally used to fight colds and flu. They are rich in antioxidants and may reduce the severity and duration of symptoms.

How to take it: Elderberry syrup or capsules are common forms. Follow the recommended dosage on the product label, and avoid taking it if you have an autoimmune condition without consulting a doctor.

6. Echinacea

Why it’s essential: Echinacea is a popular herbal remedy that may help prevent and reduce the severity of colds by boosting immune activity.

How to take it: Look for standardised extracts and follow the manufacturer’s dosage guidelines. Echinacea is best taken at the first sign of illness.

7. Omega-3 Fatty Acids

Why it’s essential: Omega-3s, particularly EPA and DHA found in fish oil, have anti-inflammatory properties that support immune function and overall health.

How to take it: Aim for 250–500 mg of combined EPA and DHA daily. Vegetarian or vegan options include algae-based supplements.

8. Garlic Supplements

Why it’s essential: Garlic contains allicin, a compound with antimicrobial and immune-boosting properties. Regular garlic intake has been associated with fewer colds and flu.

How to take it: Opt for aged garlic extract supplements or incorporate fresh garlic into your diet for the best benefits.

Final Tips

Consult a GP or pharmacist: Always check with a healthcare professional before starting new supplements, especially if you’re pregnant, nursing or on medication.

Choose quality brands: Look for products that are third-party tested for purity and potency. A wide range of supplements and vitamins is available from Amazon.

Maintain healthy habits: Supplements work best when combined with a balanced diet, regular exercise, good hygiene and adequate sleep.

By supporting your immune system with the right supplements, you can give yourself a better chance of staying healthy this cold and flu season.

This blog post was created with the aid of AI.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2024, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

Thank you for being a valued Pounds and Sense reader. Just a reminder that you can get notifications every time the blog is updated via the Subscribe box on the right (or scroll down on mobile devices). You can also follow PAS on X/Twitter and Facebook and now on BlueSky as well 🙂

If you have any comments or questions about this post, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

Christmas is coming, so here’s a chance to make it extra special for one lucky winner!

I’ve joined forces with some of my fellow UK bloggers in this festive mega-giveaway with prizes valued at over£500 in total.

Entering the giveaway is free of charge and full instructions can be found below. There are multiple ways to enter, and the more you do, the better your chances of winning. You may also like to use the prize list as a source of ideas for Christmas gifts.

Note that where an entry requires following a social media account, you will need to continue following this account until the winner has been drawn after the closing date of 22 December 2024. Before the winner is announced the organisers will check that they are still following the account in question. If not, they will be disqualified and another winner drawn.

This giveaway has been organised by my fellow blogger Rowena Becker, who blogs at My Balancing Act. Please check out her blog and those of the other talented bloggers taking part (listed below). And read on for full details from Rowena of all the prizes on offer and how you could win this mammoth bundle!

The Bloggers Mega Christmas Giveaway!

Win Big This Christmas! Some of the UK’s top bloggers have come together to offer one lucky winner a collection of incredible prizes that are sure to bring smiles to every face in your household.

From thoughtful treats to exciting surprises, this bundle has everything you need to make this Christmas extra special. Entering couldn’t be easier—simply head over to our Rafflecopter link at the bottom of this post for multiple chances to win.

Don’t miss out—this could be the perfect way to surprise and delight the whole family!

This giveaway is open to over 18 only and age verification will be required. The winner will be chosen at random and contacted via email. Terms and conditions apply.

The Bloggers

In order to be able to bring you this incredible giveaway, some of the UK’s top bloggers got together. A massive thank you to our bloggers! The bloggers taking part are:

The Perfect Gift for Foodies: FinaMill Rechargeable Gift Set

Upgrade your loved ones’ cooking game with the festive FinaMill Rechargeable Gift Set. This set not only adds a pop of colour to any kitchen in its Sangria shade, but it also takes cooking to the next level with its innovative design and features. Whether you’re shopping for experienced chefs or kitchen newbies, this gift set is sure to impress.

The rechargeable grinder allows for fast charging and has a long-lasting battery, making it the perfect addition to any busy kitchen. And with its eco-friendly design, you can feel good about reducing your carbon footprint while cooking up delicious meals.

Not only does the gift set come with the FinaMill grinder, it also includes 3 different types of FinaPods: 2 FinaPod Pro Plus for everyday spices and 1 FinaPod MAX for larger spices and dried herbs. With a sleek and modern tray exclusive to this gift set, your loved ones will have all the tools they need to elevate their dishes in one convenient package.

As well as being a practical and unique present, this will also show your loved ones how much you care about their passion for food. Don’t wait—enter our giveaway now!

Ocoopa HotPal PD Quick Charge Rechargeable Hand Warmer

The Ocoopa HotPal PD Rechargeable Hand Warmer is the perfect addition to our prize bundle, making it an ideal gift for anyone who loves spending time outdoors during the colder months. This hand warmer not only keeps your hands warm and toasty during chilly morning hikes or outdoor activities, but it also has adjustable heat options so you can customise the warmth level to suit your needs.

But that’s not all! The Ocoopa HotPal PD Hand Warmer also serves as a backup portable charger using the PD protocol, making it a convenient and versatile gadget to have on hand. It can charge various devices such as lights, earbuds, and smartphones – with lightning-fast speed. In fact, it can charge an iPhone to 50% in just 30 minutes, perfect for those who are always on-the-go. This means you’ll never have to worry about your devices running out of juice during your outdoor adventures.

So whether you’re gifting this hand warmer to a friend or family member who loves camping, hiking, or simply enjoys being outdoors, or even treating yourself to one, the Ocoopa HotPal PD Rechargeable Hand Warmer is a must-have accessory for any winter adventure. Don’t miss your chance to win this amazing prize and make someone’s Christmas extra warm and special with our ultimate giveaway bundle!

Opinel Cheese Knife & Fork Set

Looking for a unique and practical gift for the foodie in your life? Look no further than the Opinel Cheese Knife & Fork Set. This set is not only stylish and beautifully designed, but also functional for any cheese lover.

Opinel, known for their iconic French design and quality craftsmanship, brings their expertise to this must-have set for any cheese plate or charcuterie platter. Made from sustainably harvested European wood, the beechwood handles add a touch of elegance to the knife and fork.

But don’t let the sleek design fool you, these tools are made to last. The stainless steel blade of the knife is sharp, durable, and easy to maintain, ensuring that it will be a staple in any cheese lover’s kitchen for years to come. Plus, the fork serves a dual purpose as a holder for the knife and for easily serving slices from the platter.

This set is not only perfect for holiday gatherings and dinner parties, but also makes a great gift for any occasion. Give the gift of style and functionality with Opinel’s Cheese Knife & Fork Set this Christmas!

Opinel Art Deco 4pc Kitchen Knife Set

The Opinel Art Deco 4pc Kitchen Knife Set is the perfect addition to our prize bundle this Christmas. With its simple, versatile and efficient design, these knives make everyday cooking much easier. The set includes four high-quality knives with unique and stylish designs that are sure to impress any recipient.

Each knife in the set has a Sandvik 12C27 stainless steel blade with a high carbon content, ensuring excellent cutting quality and resistance to corrosion. The handles are made from tinted hornbeam and covered in a protective varnish, making them resistant to water for long-lasting use.

The set contains four essential kitchen knives: No.112 Paring knife in purple, No.113 Serrated knife in soft grey, No.114 Vegetable Knife in emerald green and No.115 Peeler in white. These knives are perfect for various tasks such as peeling, slicing, and dicing fruits and vegetables, cutting bread or meat, and even preparing sushi.

The Opinel Art Deco 4pc Kitchen Knife Set is not only practical but also adds a touch of elegance to any kitchen with its Art Deco design. It’s an ideal gift for anyone who loves to cook or wants to upgrade their kitchen essentials.

Note: Age verification will be required for all prize winners. Open to UK residents over 18 only.

The Perfect Gift for Coffee Lovers: RISE 26oz Tumbler by Klean Kanteen

As part of our amazing Christmas prize bundle, we are excited to offer the RISE 26 oz tumbler with flip lid in Sea Spray. This sleek and stylish tumbler is not only a great addition to any coffee lover’s collection, but also an eco-friendly choice.

Made from certified 90% post-consumer recycled stainless steel, this durable tumbler is perfect for enjoying hot or cold drinks on the go. Its Climate Lock™ insulation keeps drinks at the desired temperature for hours, making it ideal for busy mornings or long commutes.

Christmas Negroni Cocktail Prize Pack

Are you looking for a sophisticated and festive cocktail to add to your Christmas celebrations? Look no further than the Award-Winning Christmas Negroni, crafted by Bottle Bar and Shop.

This twist on the classic Negroni is perfectly balanced with warm seasonal spices and premium ingredients, providing an effortless way to indulge in the holiday spirit. Whether you’re hosting a festive gathering or enjoying a cosy night in, this Christmas Negroni will elevate your experience with its rich flavours and festive flair.

Enter now for a chance to win this as part of our prize bundle. Please note that this prize is only available for those who are 18 years or older. Cheers to the holiday season with our Christmas Negroni Cocktail Prize Pack! Disclaimer: Must be 18 years or over to enter.

Disney Stitch Drink Flask from Thermos

Looking for a practical and fun gift for the little ones in your life? Look no further than the Direct Drink Flask 470ml Disney Stitch Signature from Thermos. This flask not only features cute images of everyone’s favourite mischievous alien, Stitch, but also keeps drinks hot for up to 10 hours and cold for up to 24 hours.

Whether they’re off on an adventure or just need a cool drink at school, this direct drink flask is perfect for kids (or adults!) who love Disney and staying hydrated. And with its durable design and reliable insulation, it’s sure to be a gift that will last beyond the holiday season.

Brainstorm Toys Outdoor Adventure Metal Detector

As part of our Christmas prize bundle, we are excited to offer the Brainstorm Toys Outdoor Adventure Metal Detector. This fun and innovative STEM toy is perfect for young detectorists who love to explore and discover hidden treasures. With its easy-to-use design and light and sound alerts, kids will be entertained for hours as they search for buried gems and coins. Not only does this gift encourage curiosity, but it also provides an exciting outdoor activity that will keep kids active and engaged during the holiday season. Lightweight and versatile, the Brainstorm Toys can be used in handheld mode or attached to a pole for an even more thrilling treasure hunt experience. Don’t miss your chance to win this amazing gift for the little ones in your life!

Doll Smash Glass Lip Oil: The Ultimate Hydration and Shine for Her Lips

This Christmas, give the gift of hydrated and shiny lips with Doll Smash Glass Lip Oil. Its lightweight, vegan formula is perfect for anyone looking for a quick and easy way to add some moisture to their lips. Say goodbye to sticky residue and hello to soft and supple lips with just one glide. With its instant boost of hydration and shine, this lip oil is the perfect addition to any winter skincare routine. So why not treat your loved ones (or yourself!) to beautifully moisturised lips this holiday season?

Age-Defyers Discovery Set from Evolve Organic Beauty

Looking for the perfect gift for her this holiday season? Look no further than the Age-Defyers Discovery Set from Evolve Organic Beauty. This giftable collection of 3 travel-sized skincare products is suitable for all skin types and is specifically designed to help smooth, plump, and give a younger-looking appearance.

Included in this set are 3 samples from Evolve’s award-winning range of organic skincare products, so you can try out some of their best-selling items before committing to full-sized versions. The Gentle Cleansing Melt (30ml) will leave her skin feeling clean and refreshed while the Peptide 360 Serum (10ml) and Multi Peptide 360 Anti-Ageing Cream (30ml) work together to tackle signs of aging. Plus, with the addition of 2 sachet samples, she can continue her journey to youthful skin even after the holidays are over.

Don’t miss out on this amazing gift that will give her the gift of beautiful, radiant skin this Christmas!

New Sprouts® Prep ‘n’ Store Kitchen Island from Learning Resources

As part of our amazing Christmas prize bundle, we are excited to offer the New Sprouts® Prep ‘n’ Store Kitchen Island from Learning Resources! This fantastic play kitchen island is perfect for your little chef to prepare and serve pretend play food and will provide hours of imaginative play. With two rolling wheels on one side and a convenient handle on the other, it’s also easy to move around and store when not in use. Plus, with two storage shelves included, there’s plenty of space to store all kinds of play food—including the six pieces that come with the set! Let your child’s creativity and culinary skills shine this Christmas with the New Sprouts® Prep ‘n’ Store Kitchen Island from Learning Resources.

Numberblocks® Rainbow Counting Bus

The New Sprouts® Prep ‘n’ Store Kitchen Island is not the only exciting educational toy that we have included in our Christmas prize bundle. As part of our commitment to providing quality learning resources, we are also offering a Numberblocks® Rainbow Counting Bus from learning resources! This fun and educational toy is perfect for any young Numberblocks fan who loves imaginative play.

Get ready to embark on exciting adventures in Numberland with the included Seven figure as your driver. With 12 songs and sounds from the series, your child will have a blast counting along and exploring all the numbery features of the bus.

Take a peek at the hidden rainbow by opening the drop-down back, and count all the different colours together. Let this magical toy from Learning Resources be a part of your child’s Christmas celebrations and help them learn and grow while having tons of fun!

Pretend to Bee Postal Worker – 3-5 Years

This fun and interactive costume from Pretend to Bee is the perfect gift for children who love to play pretend and explore different occupations. With a sleeveless jacket, trousers, and post bag, kids can dress up and act out the role of a postal worker, gaining a better understanding of this important job in their community. Not only will they have hours of fun with imaginative play, but they’ll also learn valuable skills such as responsibility and teamwork. Plus, it’s machine washable for easy clean-up after all their adventures! A great addition to any child’s dress-up collection and a fantastic way to encourage creativity and social development. Get ready to deliver some letters this Christmas with the Pretend to Bee Postal Worker costume!

Little Brian Scribble Paint Sticks and Bath Paint Sticks

Add a splash of colour and creativity to your child’s Christmas with the Scribble Paint Sticks by Little Brian, included in our prize bundle! These innovative paint sticks allow kids to unleash their imagination and create intricate designs thanks to their finer tip. With 12 vibrant colours, these paint sticks bring any artwork to life in just under 60 seconds. And the best part? No more messy clean-up afterwards! Watch as your child explores their creativity on paper, card, wood, or glass without worrying about stains or spills.

But wait, there’s more! Also included in our prize bundle are the Bath Paint Sticks from Little Brian. These washable paint sticks make bath time even more fun and colourful as kids can create their own masterpieces on the bath tub or shower walls. With six vibrant colours that easily wash off with water, these paint sticks provide a mess-free and imaginative activity for children of all ages. Make bath time a creative experience this Christmas with the Little Brian Bath Paint Sticks! Don’t miss out on this perfect gift for budding artists this holiday season!

LittleLife Toddler Backpacks

LittleLife’s award-winning range of toddler backpacks come in a plethora of different colourful designs, giving your little ones the perfect amount of storage space this Christmas, whether that’s for their new toys or sweet treats!

What’s more, LittleLife’s toddler backpacks have a built-in safety rein to keep youngsters safe and within reach, whilst still giving them the freedom and independence to explore the outdoors and develop motor skills that are so important for children’s development.

Make festive family walks a cherished tradition, knowing your little ones are secure with LittleLife toddler backpacks!

Browse the LittleLife toddler backpack collection here

Start-Rite Party Shoes

Add some sparkle and fun to little feet this Christmas with Start-Rite’s versatile collection of children’s party shoes! You’ll find classic T-bar styles such as Lottie in Pink Leather and Puzzle in Navy Patent, and festive colours, such as Wiggle in Gold Glitter and Wonderland in Cherry Red Patent. The extensive collection of party shoes and boots from Start-Rite has something for everyone – perfect for family festivities this Christmas.

The FoldLite LX is the perfect solution for making family visits easier this Christmas! With a lightweight, one-of-a-kind fold, the FoldLite LX can be popped up and taken down with ease both home and away. Collapsing to only 26cm wide, you can swiftly tuck the cot into any nook around the house. When travelling, the FoldLite LX can go one step further, folding down even tinier for exceptional portability. Doubling as a playpen and featuring a removable infant bassinet, the FoldLite LX conveniently travels with the family throughout the festive period and beyond.

You can enter the Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collected, and one winner will be randomly chosen via Rafflecopter. Good luck!

The giveaway will run from 8 am 15th December 2024 to 11.45 pm 22nd December 2024.

Prize open to over 18s only. Age verification will be required.

The winners will be notified by email from rowena@mybalancingact.co.uk.

The winner will have 7 days to respond after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, X, YouTube, BlogLovin or Pinterest or any other social media platform.

The prizes may not arrive in time for Christmas.

Some or all of the prizes may take a few weeks to arrive.If any prizes are out of stock then we will do our best to find a suitable replacement but cannot guarantee it.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage.

Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace them.

In the unlikely event that one of the companies withdraws a prize, we cannot offer an alternative.

The winner’s name will be stated on some or all of our blogger’s websites and announced on Twitter and other social media channels. It will also be displayed on the Rafflecopter entry form. By entering this prize draw, you give your permission for this.

Please note the winner may have the same name as you, so if you see your name displayed, be aware that you are not the winner unless you have been notified by us.

There may be some delays in receiving prizes.

Good luck, and I hope a Pounds and Sense reader wins this fabulous prize bundle!

NOTE: Posts on Pounds and Sense may include affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect in any way the product or service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

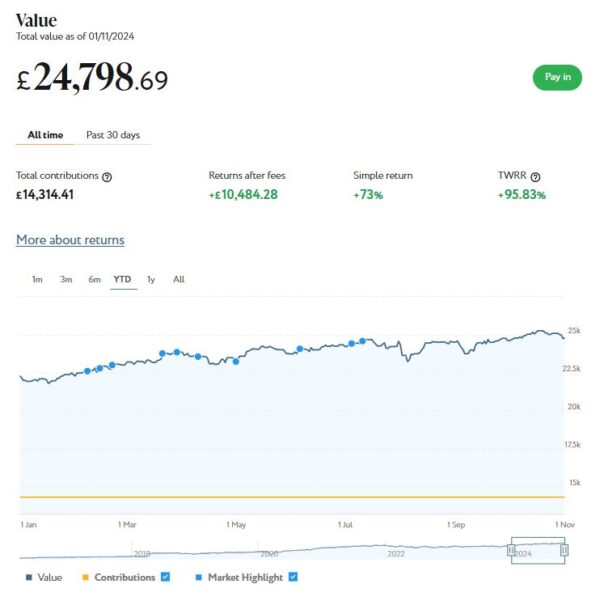

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

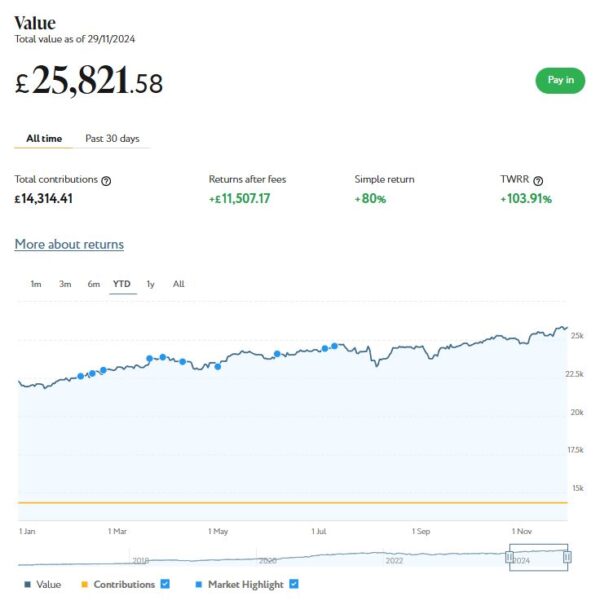

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,822 (rounded up). Last month it stood at £24,799, so that is an impressive increase of £1,023.

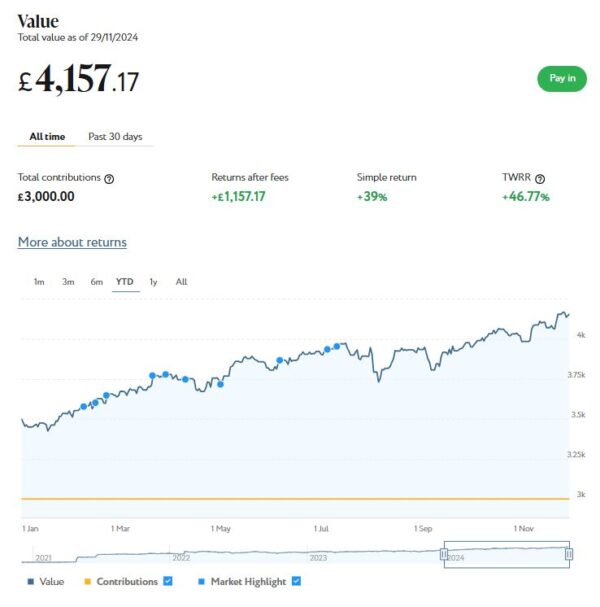

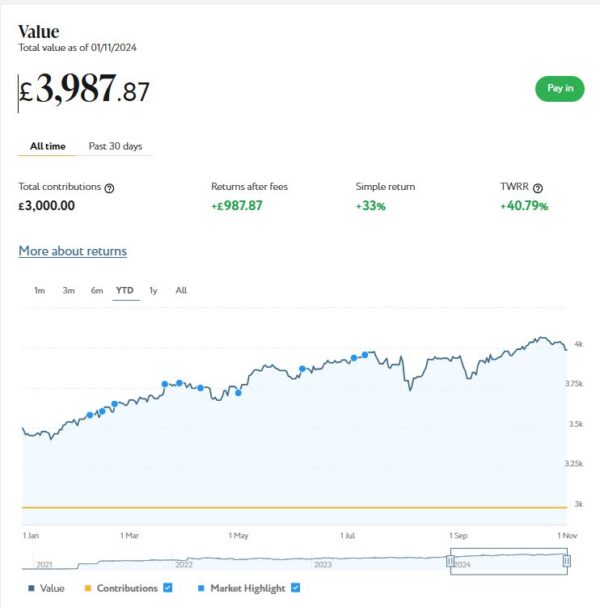

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,157 compared with £3,988 a month ago, a rise of £169. Here is a screen capture showing performance over the year to date.

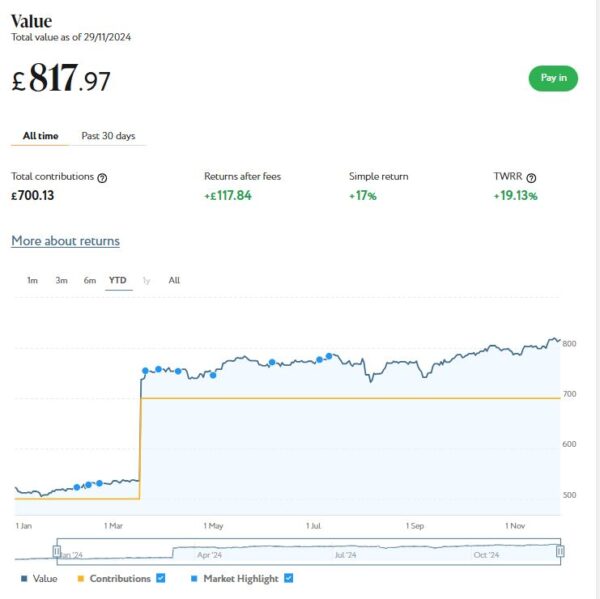

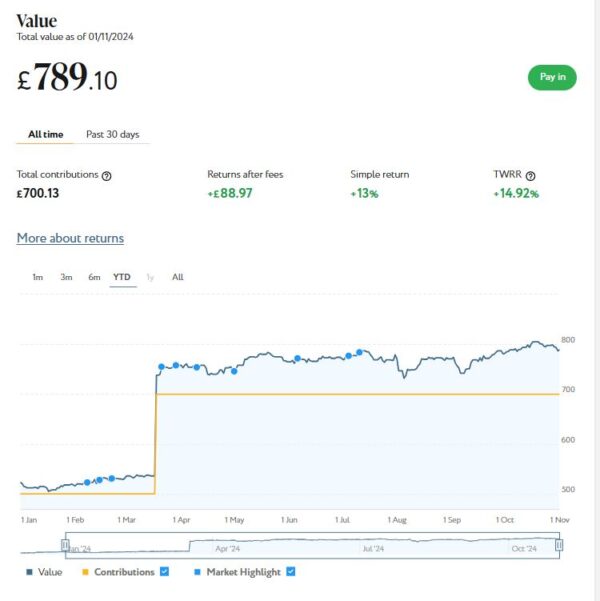

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £818 (rounded up) compared with £789 last month, a rise of £29.

As you can see, November was a good month for my Nutmeg investments. The overall value has risen by £1,221 or 4.13% since the start of November. They are also up by £4,482 or 17.03% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024. Despite some predictions to the contrary, you still have a full £20,000 tax-free ISA allowance for 2024/25. As from this year, you can open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. These continue to generate steady returns. Assetz Exchange focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £220.04 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 18 are showing losses. My portfolio of 34 properties is currently showing a net decrease in value of £44.11, meaning that overall (rental income minus capital value decrease) I am up by £175.93. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this blog post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

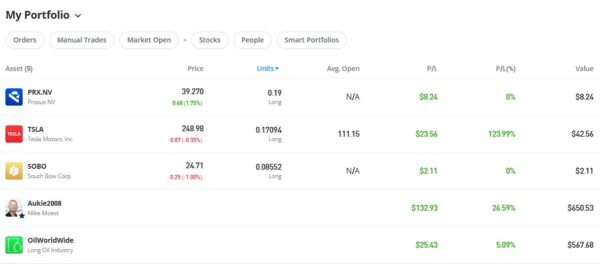

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

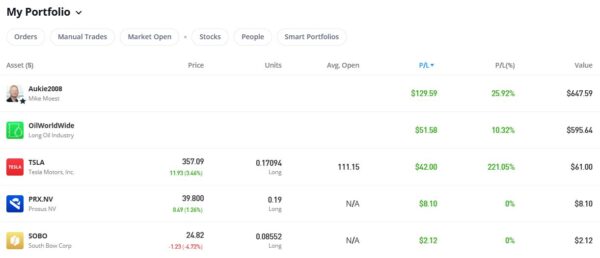

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,315.34, an overall increase of $293.08 or 28.67%.

As you can see, my Oil WorldWide investment is showing a respectable if not outstanding profit of 10.32%. My copy trading investment with Aukie2008 has been doing better, with an overall 25.95% profit. To be fair, I have held the latter investment a bit longer.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in November on the excellent Mouthy Money website. The first is Ten Ways to Boost Your Bank Balance in the Run-up to Christmas. As Christmas approaches, many of us are feeling the pinch, with the cost of gifts, food and festivities adding up. And that’s before you even factor in the cost of living crisis, tax increases, benefit cuts, and so on. So in this article I set out a variety of ways you may be able to boost your income in the weeks leading up to the big day.

Also in November Mouthy Money published my article Get Fit, Make Money – How to Profit from Fitness Apps. In this article I revealed a variety of methods by which you may be able to get fit and boost your bank balance at the same time.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the range of articles published in November, I particularly enjoyed this guide to saving money by selling stuff on eBay and other websites by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published (or republished) several posts on Pounds and Sense in November. Some are no longer relevant, but I have listed the others below.

In Update on my eToro Virtual Portfolio, I brought readers up to date with how my eToro VP has been doing and discussed what lessons could be learned from it. As I say in the article, anyone joining the eToro trading and investing platform automatically gets a $100,000 virtual portfolio in which they can experiment with different investing styles and strategies. I found it very interesting to revisit my VP a year on. I was pleased to discover that since my previous VP update, and despite the fact I hadn’t really paid it much attention, performance had turned around and the port was showing a good profit (unfortunately virtual as well!). As ever there were winners and losers, and these will inform my real-money trading as well.

With Christmas fast approaching, last month I published What Are the Best Video Calling Tools for Older People? For older people (in particular) video calling can provide a great way of connecting with far-flung family and friends if – for whatever reason – they can’t meet in person. In this article I set out the main options available and shared a few hints and tips for making the most of them.

And in Twelve Great Christmas Gift Ideas for Older People (That Aren’t Socks) I set out 12 suggestions for presents for older friends and relatives that – based on my experience as an older person myself – should put a smile on their faces! If you’re struggling for ideas for gifts for older friends and relatives, check this out

Lastly, a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I have also just joined the new BlueSky social media network. My username there is poundsandsense.bsky.social. For the time being at least, Twitter/X will remain my main social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

That’s all for today. I hope you are keeping safe and warm in the current Arctic weather. As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In this post a few weeks ago I discussed EDF Energy’s ‘Sunday Saver’ challenge. I explained why I had some reservations about the scheme and wasn’t therefore taking it up.

The post attracted a lot of interest. It actually generated more comments than any other post I have made on Pounds and Sense. Various people (especially Harry and KenM – thanks, guys!) posted in some detail about their experiences with the scheme. As a result I changed my opinion somewhat and decided to sign up when the opportunity arose the following month.

In this update I thought I would talk about why I changed my mind and the results I have achieved myself over the last few weeks. But first, a word of explanation…

What is EDF’s Sunday Saver Challenge?

This scheme is intended to reward EDF customers for switching some of their energy usage away from peak times.

The way it works is that you’re given targets to shift your electricity consumption on weekdays away from peak hours (4pm-7pm). When you hit your weekly target (which is set individually for each user by EDF), you earn free electricity the following Sunday.

EDF say, ‘The more you shift, the more you earn – reduce your weekly peak usage by 40% and you could earn up to 16 hours of free electricity per week.’ The challenge takes place monthly, starting on the first Monday of each month.

Why Did I Have Reservations?

As I said above, I had various reservations about the scheme prior to signing up. I have copied below the relevant paragraphs from my original post.

To benefit from this scheme you have to cut your daily energy usage every weekday between 4pm and 7pm. That’s quite a long period (three hours), and coincides with when I would normally be cooking my evening meal. To have any realistic chance of cutting my energy use during this time, I would have to eat either ridiculously early or significantly later than normal. For various reasons, including my health, I prefer to eat between 6 and 7 pm and no later. So that in itself is a big ask and would impact drastically on my normal routine.

Free electricity on Sunday sounds great, but the devil is in the detail. EDF say that you will get ‘up to 16 hours’ of free electricity if you meet their targets, but are very vague about what this means in practice. Specifically, they don’t explain how your energy-saving targets are calculated, how any reduction in usage translates to free hours, or when on Sunday you will be able to use the free electricity awarded.

In addition, they say there are ‘fair usage’ limits to how much free electricity you can have. Again, they are vague about what this means in practice. The obvious way to use your free electricity would be to charge your EV, and I strongly suspect limits would be placed on this. As for me, I don’t have an EV and don’t want one, so my options for benefiting from the free electricity would be limited. I could shift use of appliances like my washing machine to Sunday but doubt if I could save more than a few kw/h this way (obviously the exact number would depend on how many free hours I was allocated, which is anyone’s guess). That means my free electricity would likely benefit me by no more than a pound or two.

Lastly, as a solar panel owner I already get some free electricity anyway. My panels obviously generate less in the winter, but during daylight hours they still produce something. That means any benefit from free electricity on Sundays will be reduced, especially if (as is likely) the free hours are in the day rather than at night.

So What Changed?

The comments and info posted by readers who had signed up for the challenge and (in general) had benefited from it changed my views somewhat. They also addressed some of the doubts I had expressed in my original post.

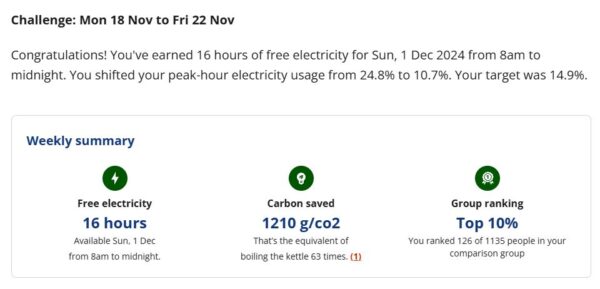

As regards the free hours on Sunday, depending on how much you reduce your usage you can get anything from 4 hours to a maximum of 16. The free hours always start at 8 am and go on until as late as 12 midnight if you achieve the full target saving.

There are indeed ‘fair usage’ limits for the free hours you are awarded. They are as follows: 11.25 kWh with 4 free hours; 22.5 kWh with 8 free hours; 33.75 kWh with 12 free hours; and 45 kWh with 16 hours. EDF say these amounts are subject to change.

I still don’t know how exactly the saving targets are set, but here is a screen capture showing the ones I was set last week and the results I obtained.

As you can see, that was a successful week! I’ll talk more about my personal experiences with the Sunday Saver challenge below.

I also realised that, while I don’t have an EV, I could use a fair-sized portion of my free electricity charging my home storage battery from the grid. This wasn’t something I had done before (I got my battery mainly to store power generated by my solar panels) but obviously I knew it was possible. As things turned out (see below) it wasn’t without its challenges. But without doing this I’m not convinced I could have used enough free electricity to make the scheme worthwhile.

I do, incidentally, still think that EDF should make the terms and conditions of the challenge clearer prior to signing up. But anyway, based on info received from my readers, I felt it was worth giving it a try. So here’s a bit about my experiences with the November challenge.

So What Happened?

When I decided to do the EDF Sunday Saver challenge, I was clear I wasn’t going to cause myseff a ton of hassle cutting my electricity usage to the bone (I live on my own these days, incidentally). I decided I could probably defer starting my (electric) cooking till 7 pm. That was a minor inconvenience, but so far anyway I’ve been getting around it by eating meals that are quick to cook (yesterday I had gnocchi with pesto and spinach, for example). I’ll admit I’ve had a few microwave meals as well. I did also do some healthier batch cooking on one of the Sundays to produce meals I could quickly heat up during the week.

Shifting my main cooking time has undoubtedly done more than anything to reduce my peak-time energy use. Apart from that I have done little. I wouldn’t normally be hoovering or using the washing machine at peak times anyway. I have made a point of turning off my desktop computer by 4 pm (something I should probably have been doing anyway). I’ve also been a bit more careful about switching off lights when I don’t need them. And obviously I don’t use any electric heating during peak hours (thankfully I have gas central heating and a separate gas fire in the lounge). And that’s it really. For the first three weeks of the November challenge I achieved my targets fairly easily, earning the maximum 16 hours for two of them and 12 hours for the other.

I saved all my hoovering and clothes washing for Sundays to make use of the free electricity. In addition, as mentioned above, I set my home battery to charge from the grid that day. Unfortunately because I hadn’t done this before – and the software isn’t as intuitive as it should be – the first time it didn’t work at all. The following Sunday I got it working but somehow must have set it to charge every day in the evening. So on the Monday the battery started charging at the maximum rate (6 kw/h) at 5 pm. Unfortunately I didn’t notice this until around 6 pm, so that drove a coach and horses through my weekly energy-saving target. At the time of writing, my weekly dashboard shows that I am currently using 97.5% of my electricity during peak hours and – unsurprisingly – am ‘not on target’ to achieve the 14.9% set for me. Obviously, then, I will have to write off this week. I just hope that my poor performance will encourage EDF to set me generous targets in December!

Closing Thoughts

Overall, my experiences have been positive enough to want to continue the Sunday Saver challenge. I will have saved some money by doing it, which will be credited to my account in December.

It will be interesting to see what usage targets EDF set me next month, especially after I messed up the final week of the challenge. But in any event, EDF have also let me know that anyone signing up for the December challenge will get an automatic eight hours of free electricity on Christmas Day regardless of any energy savings they make. So that is another incentive to sign up for December (which I have already done),.

So those were my experiences with the EDF Sunday Saver challenge in November. I’d be interested to hear how you got on if you did it too, and whether you will be continuing the challenge. Also, if you are on a similar scheme with another energy company, I’d love to hear how that’s going for you. Please post any comments below as usual, not forgetting to allow me a few hours to approve them.

As I have said before on PAS, I can offer anyone switching to EDF £50 off their bills if they use my refer-a-friend link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 when applying. I will also get £50 off my bill if you do this (£75 till 12 December 2024), which is duly appreciated

If you enjoyed this post, please link to it on your own blog or social media:

I thought PAS readers might be interested to see an update about how my eToro virtual portfolio is doing today and any further lessons to be learned. As you may know, I already publish monthly updates on my real investments and how they are doing, the latest of which you can read here.

Let’s start with the basics, though…

What is eToro?

eToro is a Israeli fintech company based in Cyprus. The company also has registered offices in the UK, US and Australia. It is a hugely popular platform with 25 million customers from over 140 countries across the world.

eToro is regulated and authorised in the UK by the Financial Conduct Authority (FCA) and is covered by the Financial Services Compensation Scheme (FSCS). That means if eToro were to go bust any deposits with them up to £85,000 would be protected. Of course, the FSCS doesn’t protect you if you lose money simply due to your investments performing poorly.

eToro offers a wide range of investment products, from individual shares to cryptocurrencies, commodities to ETFs, currency pairs to copy trading, and thematic investing via smart portfolios. Today, though, I’m focusing on a feature that doesn’t require any outlay at all. This is the facility to operate a $100,000 virtual portfolio on the platform, to familiarize yourself with how it works and test out trading and investing strategies.

I have been an eToro investor for nearly three years now. I started with a virtual portfolio, but I have also invested some real money. I do still use my virtual portfolio, however, and continue to learn valuable lessons from it. So today I thought I’d set out some of these.

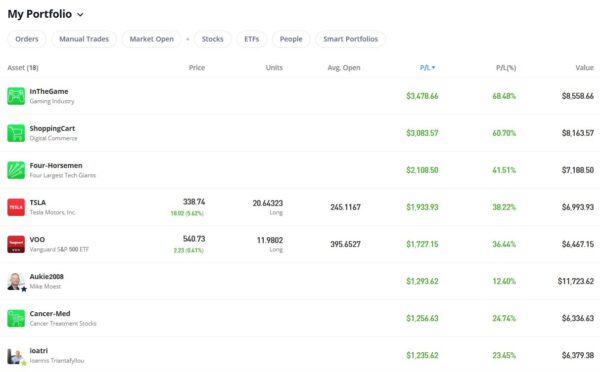

I’ll start by showing you some data on how my virtual portfolio has been performing as of November 2024. As I have quite a lot of different investments in my VP, I have taken two separate screen captures showing first the best performing and then the worst performing. As a matter of interest, I am now up by over $17,000 overall. Obviously I can only wish that was real money!

Table of Contents

Best Performing Investments

Worst Performing Investments

Some Lessons Learned

I hope you found the screen captures of my virtual portfolio interesting. They include most of my current investments apart from one or two in the middle. I can’t discuss every investment in detail here, but as promised here are some of the lessons I have drawn from my experiences to date.

Time in the market really does matter

As my financial adviser, Mike, often reminds me, one of the main keys to successful investing is time in the market. As long as you have a good-quality, well diversified portfolio, over time the inevitable peaks and troughs will even out, and the likelihood of making a good long-term return will increase (though, of course, with all investing there is never any guarantee).

Two years on from when I opened my eToro virtual portfolio, here’s a snapshot of how it’s doing overall…

As you can see, currently my inexpertly-picked portfolio is showing over $17,000 of profit. In my last VP update in July 2023, it was showing a loss of over $3,000. Since then I haven’t made any major changes to the portfolio, but over the last year there has been an impressive turnaround. Apart from my unsuccessful (okay, disastrous) experiments investing in commodities, the profit would be significantly bigger than this. And, as you may have noticed, there has been one other thing holding overall performance back…

Renewable energy companies have performed surprisingly poorly

You might assume that with climate change and the manic quest (in the UK at any rate) to achieve Net Zero, investing in renewables should be a profitable strategy.

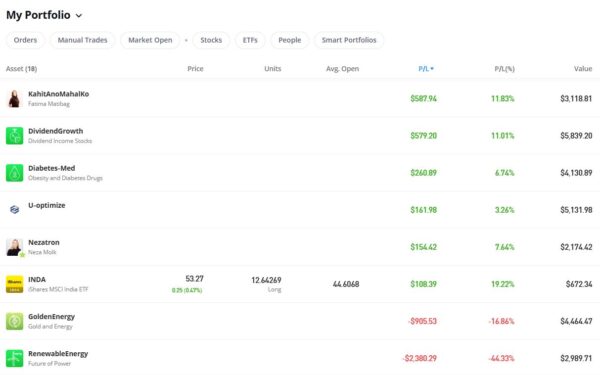

I used to think so too, so in my eToro VP I invested in two smart portfolios in this sector. One is called Renewable Energy and the other Golden Energy. As you can see from my second screen capture, both have performed poorly and are at the bottom of the table. Golden Energy (which invests in gold and energy companies) is down by almost 17%, while Renewable Energy is right at the bottom, having gone down in value by nearly 45%. Obviously I am glad I don’t have any real money in these smart portfolios.

In a somewhat ironic twist, my investment in a smart portfolio called Oil Worldwide is actually showing a profit of around 16%. Regular readers will be aware that I also have some real money in Oil Worldwide.

I don’t really know why companies in the renewable energy sector should be under-performing so badly. But it does make the point that what may appear to be ‘nailed-on’ profitable investments can still end up losing money. As I said earlier, there are never any guarantees!

IT companies generally have done well in the last two years

As you can see from my first screen capture, my top three virtual investments have all been in the information technology field. At the top is In the Game, a smart portfolio focused on the gaming industry. This has delivered a staggering 68% profit. Not far behind is the Shopping Cart smart portfolio, devoted to online shopping technology, which has delivered a 61% return.

And in third place comes the Four Horsemen portfolio, which incorporates shares in the four leading global IT companies, Microsoft, Apple, Amazon and Google. This has generated a 42% profit, partly due to their involvement in the fast-growing AI field.

Obviously there is no guarantee that this trend will continue. But if you are looking for sectors in which to invest, information technology has certainly been delivering impressive returns recently.

Health is another sector worth watching

As you can see, one of the best performing investments in my virtual portfolio was Cancer-Med (25% profit). I had personal reasons for wanting to invest in this, as my partner Jayne died from cancer and I have been treated for prostate cancer myself. Obviously a lot of research money goes into cancer, and successful treatments can prove extremely lucrative for the companies concerned.

I also invested some of my virtual funds in Diabetes-Med. This is a smart portfolio covering companies in the field of diabetes care, treatment and prevention. Again, as someone who has previously been diagnosed prediabetic, I had a particular interest in this. And with diabetes on the rise across the world, it did seem to me it was a sector with good profit potential. It has also delivered a profit for me, albeit a relatively modest 7%.

Copy trading can be profitable

Also among my best-performing investments have been two copy trading portfolios. As you can see, the most profitable has been Aukie2008 (Mike Moest). Following him has generated a profit of around 16% over two years for me. Regular readers will know that I also invested some real money following this trader and have done pretty well from this also.

Also in my VP I am following two other copy traders, Nezatron and ioatri. Nezatron is showing a modest net profit (for me) of around 8%, while ioatri has made a rather more impressive 23% return, putting him in the top section of my performance table.

I am obviously a fan of the copy trading feature on eToro, though naturally some traders do better than others. Please read my blog post about copy trading on eToro for more information about this feature.

Final Thoughts

So those are five more lessons I have learned from my eToro virtual portfolio. I don’t claim any of them are particularly earth-shattering or that they represent deep universal truths. But I have found all of them valuable in different ways and they will certainly inform my investing in future. Obviously bear in mind that the results quoted above are based on my experiences over the last two years since I opened my VP. Over other time periods, the numbers would no doubt be different.

If you are interested in investing and/or trading, I do therefore recommend setting up an eToro virtual portfolio and trying different strategies with it. I shall continue to do so myself, alongside my real investments in eToro and elsewhere.

As always, if you have any comments or questions about this article – or eToro more generally – please do post them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Please note also that posts on Pounds and Sense may include affiliate links. If you click through these and make a purchase or investment, I may receive a commission for introducing you. This will not affect in any way the price you pay or the product/service you receive. In some instances bonuses and other promotional incentives may only be available if you click through my link.

If you enjoyed this post, please link to it on your own blog or social media:

Christmas will soon be here. Touch wood, it looks as though it will be more ‘normal’ than the last few years. But even with memories of the pandemic fading, many older people especially will still be understandably cautious about how much face-to-face socializing they do at this time.

In addition, this year we have a cost-of-living crisis. And many pensioners are even more cash-strapped than usual due to the removal of Winter Fuel Payments for all but the very poorest. Add to that bad winter weather (snow is currently falling here). And, of course, there will be the usual congestion (and worse) on many roads and motorways.

All this means that potentially there may still be less face-to-face socializing this festive season, especially where older people are concerned. Of course, it’s true they are more likely to suffer severe consequences if infected with respiratory viruses such as flu or Covid, so a measure of caution is understandable. But many have been seeing other people less often for several years now. And a lack of human contact – at this time of year especially – can lead to loneliness, depression, and other health issues (physical and mental).

While not a complete solution, video calling can provide a lifeline for older people. In particular, it can provide a means for them to keep in touch with distant friends and family, and especially with children and grandchildren.

So in this post I thought I’d look at some of the main options available. I hope this will help if you are an older person yourself, or if you have older friends and relatives.

Table of Contents

What Do You Need?

At the risk of stating the obvious, if you’re going to make video calls, you will need a device with a camera and a microphone.

The good news is that all modern smartphones, Apple or Android, have good-quality cameras built in. These devices can be great for video calling, as you can hold them comfortably in your hand, move around with them, and point them at yourself or at anything you might want to talk about. The one drawback with smartphones is that the screen is relatively small, but for one-to-one conversations they are perfectly adequate.

Other good options are a tablet, a laptop or a Chromebook. All of these devices generally have a front-facing camera that is ideal for video calling (and indeed designed for it). As the screens are larger you will be able to see the other person (or people) more clearly. And group video calls with two or more other people (should you want to do this) are more feasible.

If you’re using a desktop computer it’s not quite as simple. In this case you will need to activate the built-in webcam or else buy a separate webcam (e.g. from Amazon). Standalone webcams normally plug in via a USB port. They may come with third-party software designed to help you control and make the most of them.

The other thing you will need is a video-calling app. There are lots you can use, but in this post I’ll focus on four of the most popular: Skype, FaceTime, WhatsApp and Messenger. All of these are free to download and use on wifi. If you are using them with a mobile data service they will eat up your allowance and you may end up paying extra, so it’s best to stick with wifi if at all possible.

There isn’t much difference in call quality in my experience, so it really comes down to personal preference which one you choose.

One other thing to note is that the person you are calling will need to use the same app as you are.

1. Skype

Video calls on smartphones? Yes

Video calls on tablets? Yes

Video calls on Windows? Yes

Video calls on a Mac? Yes

Skype was originally designed for making free voice calls over the internet, but then added video calls too. It’s seen as a little old-fashioned in some circles, and isn’t quite as easy to install and configure as some of its newer rivals. Nonetheless, it still works well, and you can use it for one-to-one or group calls.

If you have a modern smartphone or tablet it’s quite likely that Skype will be installed already, but otherwise you can download it from the Play Store (Android), Apple Store (Apple) or Skype website (PC or Mac). You will need to set up an account before you start using it, for which you will need to provide either your mobile number or your email address.

To make a Skype video call to a new contact, use the Search Skype box at the top left to search for the person’s real name, Skype name, or email address. If your friend has a common name, you may find there are a number of people to choose from in the list that pops up. Use the profile pictures to find the person you’re looking for, or click on the name to view their profile information. Anyone you talk to will automatically be added to your Skype contact list. Select your contact and click Call. With your audio call running, select the video camera icon to open the camera. During a call you can mute/unmute your microphone and switch your camera on/off by clicking on or tapping the appropriate icon.

WhatsApp is owned by Facebook. It is primarily used for text chats and sharing photos and videos, but you can make video calls on it as well.

If you have a modern smartphone it’s quite likely WhatsApp will be installed already, but otherwise you will need to download it from the Play Store or Apple Store. To create an account, open the app and work through the set-up assistant. You will need to provide certain permissions to allow the app to access your camera and microphone and to import your existing phone contacts.

WhatsApp then works in a similar way to Skype. To place a video call, tap the contact you want to talk to, and tap the video camera icon next to their name. The other person can answer the call (swipe up the blue button), reject the call (swipe up the red phone button), or reject the call and send a text instead (swipe up the message button). If they answer, you’re good to go. You can toggle between the front and rear cameras on your phone by tapping on the appropriate icon if you wish.

FaceTime comes pre-installed on most Apple devices, so if you and the other person both have devices from Apple, it’s an easy option.

Making a call is (again) very simple. Just open the FaceTime app and tap the ‘+’ button, then type the phone number or email address of the person you want to call. Select audio (the microphone icon) or video (the camera icon) and you’re all set. If you have Apple’s voice assistant Siri you can also just say ‘Contact [Name]’. You can also tap ‘Recents’ to call people you have called recently and/or add your regular contacts to a Favourites list.

Messenger is owned by Facebook but it is a separate app. If you don’t have it on your device already you will need to download it from the Play Store or Apple Store or via the website for PC or Mac.

To use Messenger you will need to have a Facebook account, but this does have the advantage that you won’t need to register the app separately and can start using it straight away. Messenger will automatically connect with all your Facebook friends.

To make a Messenger video call, tap the pencil icon at the top right of the app screen. Enter the name of whomever you want to contact and tap on their picture. You can then tap on the video camera icon to start a video call.

All the apps above also allow you to make group calls. These can be great for connecting with multiple friends and/or family members. The number of contacts you can have in a call varies between apps. I have put details for the four services discussed in this post below.

Skype: Up to 100 contacts. In an ongoing conversation click the ‘+’ icon to add more contacts.

WhatsApp: Up to 32 contacts. In an ongoing call, select ‘Add Participant’.

FaceTime: Up to 32 contacts. During a FaceTime call, select ‘Add Person’.

Messenger: Up to 50 contacts. In an ongoing video call, tap on the ‘+’ icon.

Note that video calling apps compete fiercely for dominance, so the maximum numbers set out above may increase.

Finally, you will probably have heard about the group video-calling app Zoom. This is really a meetings app for businesses, but in the last few years it has become very popular with younger people especially. You don’t need any special software to take part in a Zoom chat – just click on the link you receive by text or email and the Zoom (meeting) will open in a browser window.

Zoom is very easy to use, and its Gallery View in particular has made it very popular. You can have up to 100 participants on a free call (there are also paid options for larger meetings of up to 1000 people). Concerns have, however, been raised about some privacy/security issues. One other drawback is that the free version only allows you to chat for 40 minutes at a time, although you can then reconnect in a new chat if you wish. You can read more about Zoom here.

Using a Smart Speaker

Another increasingly popular option is to use a smart speaker with a video display, e.g. the Amazon Echo Show [affiliate link]. In fact both parties don’t even need an Echo Show device, as you can make and receive calls to an Echo Show using a smartphone.

To make a video call using the Echo Show, first ensure the person you want to speak to has the Alexa app set up on their mobile phone or also owns an Echo Show. Then say, ‘Alexa, video call [contact name].’ You may be asked to confirm details of the person you’re trying to reach. Then wait for the person to answer. If you can’t see yourself on the screen, check the camera shutter on your device isn’t closed, or the ‘camera off’ icon isn’t selected. All being well, you can then start chatting to your friend or relative. At the end of the call click the red hang-up button or say, ‘Alexa, end video call.’

For more detailed information about using an Echo Show to make a video call, click through to this useful article on the popular Tom’s Guide website.

I hope you have found this article helpful. As always, if you have any comments or questions about this post, please do leave them below.

Note: this is a fully revised update of an annual article.

If you enjoyed this post, please link to it on your own blog or social media:

Amazon’s Black Friday Sale is almost with us. This year it extends over 12 days, from Thursday 21 November to Monday 2 December.

Black Friday itself is on Friday 29 November, with the final day, Monday 2 December, being known as Cyber Monday.

Amazon say they will be offering 12 days of epic deals from leading brands including Philips, Tefal, Fossil, Logitech, Oral-B, Braun, Ghd, Bose, Microsoft Surface, Bosch, Shark, and more.

1. Early Deals and Extended Sales

Amazon often kicks off its Black Friday sales early, sometimes starting a week or two before the big day. This year is no different, as early deals have already begun appearing at the time of writing. More will no doubt launch in the coming days, leading into Black Friday itself and extending through till Cyber Monday. Keep an eye out for daily flash deals and special discounts leading up to the main event.

2. Discounts Across Popular Categories

Amazon’s Black Friday sale usually includes heavy discounts across a wide range of categories, including:

Tech and Electronics: Expect significant price cuts on Amazon devices (such as Echo speakers, Fire tablets, and Kindles), as well as popular brands in laptops, smartphones, and TVs.

Fashion: From top brands to Amazon’s own Essentials line, you can expect deals on clothes, shoes, and accessories for every season.

Home and Kitchen: Look for discounts on everything from coffee makers to robot vacuum cleaners.

Toys and Games: With Christmas around the corner, Black Friday is a great time to pick up gifts at a discount.

Tips for Making the Most of Black Friday

1. Prepare Your Wish List

Creating a wish list is a great way to stay organized and track items you’re interested in. Go through your list the week before Black Friday to see if items are already on sale, then you can quickly check back on the day to see if the discount has increased.

2. Use Amazon’s ‘Watch This Deal’ Feature

For time-sensitive deals like Lightning Deals, the ‘Watch This Deal’ feature lets you get notifications when items you’re interested in go on sale. This can help you grab limited stock items before they sell out.

3. Compare Prices with CamelCamelCamel or Keepa

Websites like CamelCamelCamel and Keepa track price history on Amazon, which can help you see if the Black Friday price truly is the best deal. This is especially useful for high-ticket items where discounts may vary.

4. Sign Up for Amazon Prime

Amazon Prime members often get early access to some Black Friday deals. Plus, Prime includes fast delivery, which is ideal if you’re ordering gifts. You get a range of other benefits too, including Amazon Prime Music and Amazon Prime Video. If you’re not already a member, you can take advantage of Amazon’s 30-day free trial. You can always cancel once the Black Friday sale is over if you don’t want to pay for a subscription.

5. Be Ready to Check Out Quickly

Some deals, especially on popular items, sell out fast. To avoid missing out, make sure your payment information and delivery addresses are updated before the sale begins. If you’re ready to check out as soon as you find the deal you want, you’ll have a better chance of securing it.

6. Set a Budget

With so many discounts, it’s easy to get caught up in the excitement and overspend. Set a budget before you start shopping and prioritize items that you’ve planned for.

7. Keep an Eye Out for Coupons and Vouchers

Amazon sometimes offers additional savings through coupons, which are either applied automatically or appear as check-boxes on product pages. Using a coupon can help you save even more.

Key Dates to Remember

Early Deals Begin: from mid-November

Sale Officially Starts: November 21st 2024

Black Friday: November 29th 2024

Cyber Monday: December 2nd 2024 (final day of sale)

Whether you’re looking for electronics, fashion or Christmas gifts, Amazon’s Black Friday sale is an excellent time to find deals on popular products. By preparing beforehand and keeping the above tips in mind, you can get the very most from your Black Friday shopping.

As always, if you have any comments or questions about this post, please do leave them below. I am always delighted to hear from Pounds and Sense readers!

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,799 (rounded up). Last month it stood at £24,625, so that is an increase of £174.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,988 (rounded up) compared with £3,954 a month ago, a rise of £34. Here is a screen capture showing performance over the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £789 compared with £781 last month, a small rise of £8.

As you can see, October was another decent month for my Nutmeg investments, though the last few days saw a bit of a dip. The overall value has risen by £216 or 0.75% since the start of October. They are also up by £3,261 or 11.62% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024. Despite some predictions to the contrary, you still have a full £20,000 tax-free ISA allowance for 2024/25. As from this year, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Note that after this month I will not be including Kuflink in my monthly updates. I am gradually winding down my portfolio with them, as part of the de-risking process for my investments as i get older. As I’ve said above, I have no particular issue with Kuflink, though I do think increasing their minimum investment was unfortunate for the reasons stated above. But I still recommend them if their offering suits your investment strategy and risk appetite.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £215.02 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 17 are showing losses. My portfolio of 34 properties is currently showing a net decrease in value of £43.61, meaning that overall (rental income minus capital value decrease) I am up by £171.41. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,271.89 an overall increase of $249.63 or 24.42%.

As you can see, my Oil WorldWide investment is showing 5.09% profit. That’s a bit underwhelming, but at least it’s a profit! Obviously my copy trading investment with Aukie2008 has been doing much better.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in October on the excellent Mouthy Money website. The first is How to Cut Your Energy Bills This Winter. With the coldest winter months fast approaching, energy bills can quickly become a significant financial burden. So in this article I set out some tips to help you reduce your energy costs and keep your home warm without breaking the bank.