Is This a Good Chance to Profit with Property Partner?

I have discussed Property Partner a few times on this blog, most notably in my Property Partner review.

In brief, Property Partner is a property crowdfunding platform. For the most part they specialize in ‘traditional’ property crowdfunding rather than loan or development finance.

Properties are bought and managed by Property Partner on investors’ behalf. Investors then receive a share of the rental income as dividends, and a share of any profits (plus return of their capital) when the property is sold.

Property Partner launched in January 2015. That date is significant, because after a property has been on the platform for five years, all investors get the chance to exit at a fair market price (determined by an independent surveyor). Due to the pandemic the five-year anniversary process was temporarily put on hold, but it is now proceeding again, albeit with delays as they work through the backlog.

How it operates is that in the run-up to the fifth anniversary of a property, all investors have the opportunity to say if they want to exit their investment at the valuation price or stay on for another five-year term (less than this if they subsequently exit via the resale market, of course).

All investors who have opted to leave will then have their shares pooled and put up for sale on Property Partner at the price stated. New investors are then able to buy these shares.

So long as all shares are sold, the original investors get their money (including any net profits) and the property continues under Property Partner’s management. If all shares don’t sell, however, Property Partner offer the property for sale on the open market. Investors then have to wait until the property is sold before getting their money back. As anyone who has been involved with buying or selling property will know, this is likely to take several months (quite possibly longer in the current circumstances).

The Opportunity

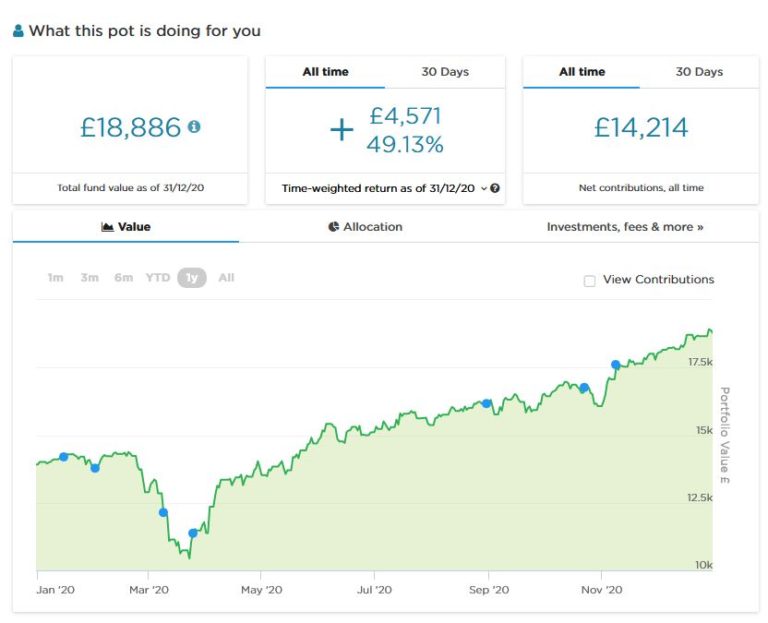

As Property Partner themselves have been pointing out, a number of properties that are coming up to their fifth anniversary are currently trading on the resale market at well below their latest valuation. Here is just one example:

This property in Tower Hill, London (not one I own shares in myself) is due to go through the fifth-anniversary process in April 2021 (or possibly a bit later due to the backlog). At the time of writing shares are available on the secondary market at a price of 91p, which is 28.28% below the latest valuation of £126.88. In theory, then, you could buy shares now and in the next few months sell up for a substantial short-term gain.

Of course, in practice it’s not as simple as that. Here are some reasons:

- Nobody knows yet what the final five-year valuation will be. If it is lower than the current valuation (which is perfectly possible in the current economic climate) the net profit will be reduced, perhaps substantially.

- There is no guarantee that the shares of all investors who wish to exit will actually sell on the platform. If they don’t, as mentioned, you could have a long wait before the property is sold on the open market. In addition, if this happens there is no guarantee that the property will sell at the valuation price. If it goes for less than this, your returns will be reduced accordingly.

- There are platform fees to take into account. In particular, there is a 1% fee for buying on the secondary market and a further 0.5% stamp duty reserve tax charge. Thankfully there are no exit fees, though.

- And finally, the number of shares available for any property on the secondary market is limited. Obviously the number you can buy depends on how many shares other investors want to sell at the price in question.

On the plus side, for the length of time you hold the shares you may receive monthly dividends at a rate between 1.5% and 6% per year (though dividend payments on some properties are currently suspended due to Covid). This will offset the fees mentioned above; but if you only intend to hold the shares for a few months it probably won’t cover them completely. Bear in mind that an Assets Under Management (AUM) fee is now deducted from dividends as well.

You can read more about the five-year exit mechanic on this page of the Property Partner website.

My Thoughts

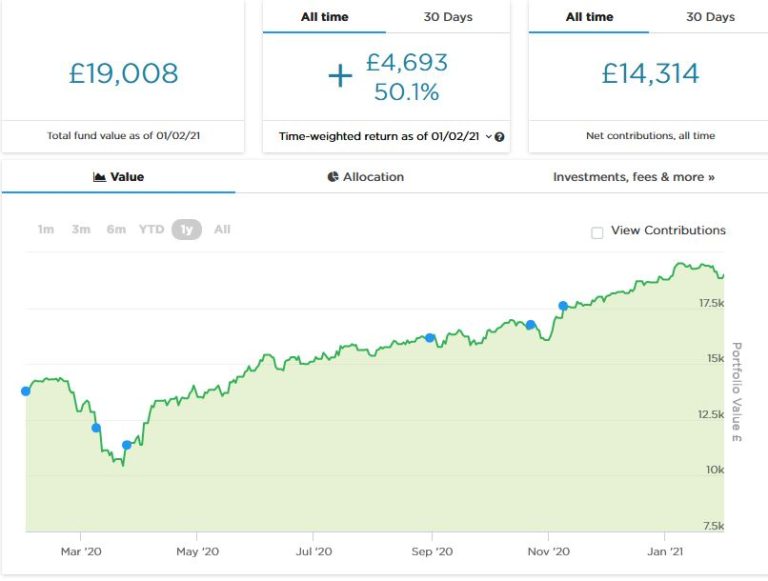

As an investor with Property Partner since almost the beginning (the cover image shows a property in Torquay I own shares in – I plan to retire there one day 😀 ), I am awaiting the five-year exit for my investments with considerable interest.

My personal circumstances have changed since I started investing with the platform, so I intend to take the opportunity to offload at least some of ‘my’ properties. Indeed, I have already voted to sell my shares in the first property I ever invested in with Property Partner (20 Phillimore Close) and am waiting to see how this pans out. I will update this post in due course once I know.

Nonetheless, I am still considering investing short term on the resale market to take advantage of the opportunity the five-year anniversary presents. In particular, I have already topped up my investments in some of the properties I already hold but am planning to dispose of.

I will, though, be cautious until I have a better idea how the first few five-year anniversaries have passed, so I can see if all shares put up by investors sell on Property Partner, or if they have to sell the properties concerned on the open market. As mentioned earlier, the latter route will clearly take longer and there is no guarantee what price would be achieved.

Would I recommend someone who is currently an investor in Property Partner to look into this? Yes, certainly. Whatever your current circumstances, you need to be aware of what is going on with any properties you hold with Property Partner. And if you wish to sell, you should definitely consider taking advantage of the five-year exit mechanic. Equally, if you have money available to invest, you could check out the opportunities buying now on the resale market – though do bear in my mind my cautionary comments above.

If you haven’t joined Property Partner, and you like the idea of investing some of your portfolio in property, the platform is certainly worth a look. As older properties come back on the market for new investors, there will be no shortage of opportunities in the months ahead. And my understanding is that, as the original costs of acquisition have been amortised, there will be less costs to cover from investors, thus boosting the potential returns from the properties in question.

In addition, as these properties have a five-year history already, you will be able to check how they have been performing in terms of dividends generated and capital appreciation. This is no guarantee of how well or badly they will do in the future, of course.

Take a look at my Property Partner review for much more information about the platform and how it works. Also, if you do decide to invest in Property Partner, there is a welcome bonus offer. For convenience I have copied details below from my review.

Welcome Offer

As an existing Property Partner investor, I can offer a special bonus for anyone joining via my link. If you click through this special invitation link, sign up and invest a minimum of £2,000 within 60 days, you will receive an extra bonus as follows (and so will I):

£2,000 – £30

£10,000 – £150

£20,000 – £300

£50,000 – £750

Not only that, once you are an investor with Property Partner, you will be able to offer the same bonus to your friends and relatives and earn commission yourself. There is no limit to the number of people you can introduce through this scheme.

If you have any comments or questions about this post, as always, please do leave them below.

Note: This is a fully updated version of a post published in 2019.

Disclosure: this post includes referral links. If you click through and make an investment, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. Be aware that all investments carry a risk of loss.