As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2020, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a happy, Covid-free Christmas, and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a Q and A for you with my fellow money bloggers at MoneyNerd.

MoneyNerd is a UK personal finance blog that aims to help people learn to manage their finances and tackle debt. I asked a number of questions about personal finance and debt, and added my own thoughts as well. Our answers are also being shared separately on the MoneyNerd blog. I hope you find them interesting and informative.

Table of Contents

What’s your number 1 financial tip?

MN: It’s hard to give advice that would apply for everyone, because everyone’s finances are different. But I would suggest ‘write it down’, as a fairly universal and important financial tip. Start with your financial goals, then write down the steps you’ll take to get there according to your budget. A lot of people have good financial intentions, but without having clear goals on paper, it’s easy to get led astray.

PAS: Agreed. I would also say, keep on top of your money. Know what’s going in and what’s going out every month, and budget accordingly. Always be on the lookout for ways you can maximize your income and minimize your expenditure. And try to put some money aside for the proverbial rainy day. Everyone should really have at least three months’ worth of income set aside in case of emergencies. Sorry, that’s at least three tips, I know!

What do you think are the main causes people find themselves in financial difficulty?

MN: I think financial difficulties are mainly caused by unforeseen life-events, such as bereavement, unemployment, and relationship breakdowns. These kinds of bumps-in-the-road can severely throw people off course, particularly if their financial situation was fragile in the first place. Unfortunately, all three of these examples have sky-rocketed due to the pandemic, and many people in the UK will be facing financial difficulties over the coming year.

PAS: Not much I can add to that. Although sometimes failing to monitor your income and expenditure closely enough can lead to debts mounting up before you realise it.

What personal finance tools do you currently use to track and manage your money?

MN: I’m quite old-school and still use spreadsheets for a lot of money-related things! There are some good apps out there though – Money Dashboard is a particularly good one.

PAS: I am the same and use spreadsheets a lot. I started with Microsoft Excel, but these days mainly use Google Sheets. As regards personal finance tools, I like Snoop [referral link], a relatively new app that helps you keep track of your finances and suggests easy ways you can make savings.

Any tips for people coming to financial management later in their lives?

MN: It might be a little harder to undo old habits and reinstate new ones if you’re approaching financial management from an older perspective. So start by setting simple goals, and work at them consistently. It’s probably worth taking a little time to assess what’s important to you right now, too: what range of outgoings does your money need to cover in later life that you didn’t need to consider before?

PAS: I am 64 and have friends in their seventies and eighties, so I have seen the sorts of problems older people can face. In particular, so many aspects of our personal finances are dealt with online now, from banking to applying for state benefits. The pandemic has probably accelerated this trend.

Many older people struggle with the technology and it’s often not as intuitive as it should be, especially for those whose eyesight isn’t as good as it once was. So I would say to any older people, try not to get left behind by technology, and ask younger friends and relatives for help when needed. Last year a group of us clubbed together and bought a friend (a retired builder) a Chromebook for his 80th birthday. He had never engaged with computers or the internet before and I must admit I was expecting him to struggle at first. However, he took to it like a duck to water, and was soon ordering tools and components online from a local builders merchant. So even old dogs can definitely learn new tricks!

2021 is going to be tough for many. Do you have any advice on how to keep things under control?

MN: I’d start with the obvious – plan as much as possible, in order to save as much as possible. This is so that when those ‘bumps-in-the-road’ come along, you have some kind of safety net, however small. Unfortunately, however, I imagine a lot of people will do everything right this year and still fall into difficulty. As and when that happens I would say be proactive in reaching out and seeking help. There are plenty of free services and helplines to reach out to, before matters spiral.

PAS: Yes, definitely. As I said earlier, everyone should have a financial safety net to tide them over when life throws you a curveball.

In my earlier career I worked as a debt counsellor at a citizens advice bureau, so I know that there is lots of help out there if you ask for it. And friends and family can be a good source of practical and emotional support too. Just don’t bury your head in the sand and pretend to everyone that nothing is wrong.

What would be your top tip for someone who is worried about a debt (or debts) they can’t repay?

MN: I have two tips: the first is don’t panic, the second is be proactive. If you can’t afford the repayments for a loan or credit card, contact the company and explain your situation. If you’re struggling to meet the repayment amounts, you may also need to look at whether a debt solution is appropriate for you. Having unaffordable debt can be a scary place in which to find yourself, but by taking action you can dissipate some of that anxiety by feeling you are doing something about the problem.

PAS: Yep. It’s worth bearing in mind also that if you have a debt you can’t repay, it’s not just your problem, it’s a problem for whomever you owe the money to as well. It is therefore in their best interests to work with you to find a method for paying down the debt.

What are some good ways of boosting your income?

MN: Ask yourself: do I own anything I could rent? A parking spot, a vehicle, a garden shed, even a room in your house if you own it. Then ask yourself: do I own anything I could sell? Old clothes, a bicycle, old furniture, anything in storage. Then finally, ask yourself what you could do with your spare time: dog-walking, Uber-driving, delivering takeaways/parcels, painting and decorating,completing online surveys, match betting, free-lancing, etc. I have a whole blog post which goes into this very topic in more detail: Making Money – Tips and Tricks.

PAS: Lots of great ideas there. Like MoneyNerd, I also have a section of my blog devoted to ideas for boosting your income. I like online surveys, with Prolific Academic (a website needing people to take part in academic research) a particular favourite. And I do matched betting as well, though not as much as I used to, as I’ve been restricted (or gubbed as we say in MB’ing) by many of the leading bookmakers!

What is the best way you can help a friend or family member who has debt problems?

MN: Honestly, I don’t think there’s a one-size fits all here. Everyone and everyone’s debt problems are different. But that seems like a cop-out! So I think showing genuine, non-judgemental support, and ensuring they have all the right resources (StepChange, CitizensAdvice, etc.) to hand are two good places to start.

PAS: I agree with this. But based on personal experience with a friend a few years ago, I would also advise thinking hard before lending them money, as this seldom solves the problem and may simply exacerbate it. With my friend, who lived alone, I found that acting as a lender to him changed the nature of our friendship, and not for the better. I also felt that by constantly bailing him out, I was allowing him to avoid addressing his money management issues. Eventually we had a difficult telephone conversation when he asked me to lend him money again and I refused. He took it better than I expected and our friendship actually returned to something more normal after that. He got his finances under better control, although I did on a couple of occasions afterwards send him supermarket vouchers to ensure he had enough to get food. I didn’t expect to be repaid for these, obviously!

If you had a sudden, unexpected windfall of £5,000, what would you do with it?

MN: Firstly I’d pay off any loans or outstanding credit card debts. Then I’d take my family out for a nice meal, and put what’s left-over into a tax-free ISA.

PAS: Paying off debts would be my first priority as well, though I am fortunate not to have any at the moment. I would put most of the rest in my Nutmeg stocks and shares ISA, and some in my Kuflink property loan investment account (from which I have had good results over the last three years) to provide a bit of diversification. Going out for a nice meal with family and friends sounds good too, although as I live in a Tier 3 area I might have to wait a while for that!

What was your best-ever financial decision, and what was your worst?!

MN: My best financial decision was investing in a tech based stocks and shares ISA which has done really well over the last 5 years, although don’t know if I’d recommend the same investing approach in the current economic climate.

On the other hand my worst financial decision was living in London for 10 years where rent and cost of living is exorbitant.

PAS: My best financial decision was probably paying off the mortgage when I had a windfall a few years ago. At a stroke one large item of monthly expenditure was gone, giving me greater financial flexibility as well as saving me a lot in future interest payments.

My worst decision was investing too much in property crowdfunding a few years ago when it was still new and exciting. I had money to invest at the time and liked the idea of owning stakes in a portfolio of properties across the UK. Some of my investments worked out but others didn’t, and I am currently sitting on a number I can’t access because the properties in question can’t be sold for one reason or another. The money is still there in bricks and mortar but I have no idea when or how I will be able to access it. That said, I do still believe in the property crowdfunding concept, but I do it a lot more selectively now.

About MoneyNerd

MoneyNerd.co.uk is a personal finance blog that was set up with one aim in mind: to help people learn how to manage their finances and tackle debt. The blog includes a variety of straight-talking articles that cover personal finance topics from credit card guides to mental well-being tips. These can help you understand exactly how financial products work, as well as what your rights are when dealing with debt. We want to offer authentic and truthful information that can help you deal with your situation, whatever that may be.

Many thanks again to MoneyNerd for their insights. Please do check out the MoneyNerd site for much more information about tackling debt and getting your finances under control.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

December is here, so it’s time for another of my monthly coronavirus crisis updates. Regular readers will know I have been posting these updates since the first lockdown started (you can read my November update here if you like).

As ever, I will start by discussing financial matters and then life more generally over the last few weeks.

Financial

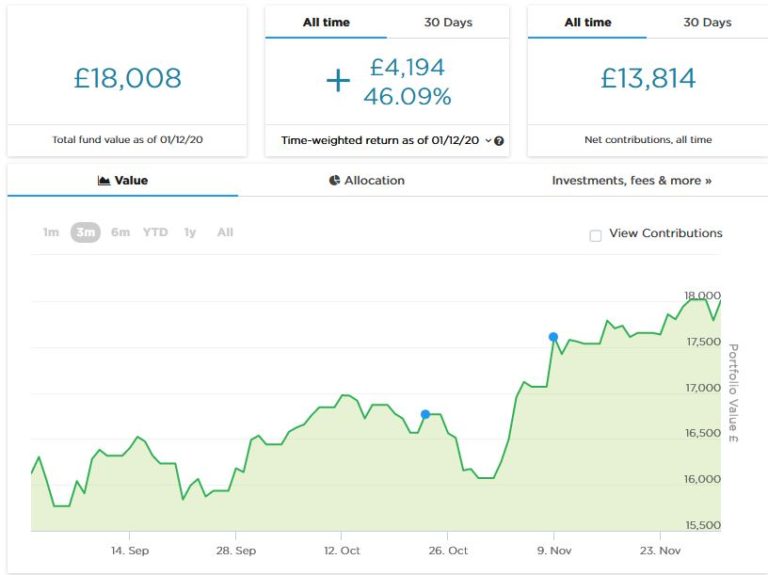

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to follow this.

As the screenshot below shows, since last month’s update my portfolio has been on a generally upward trajectory and is currently valued at £18,008. Last month it stood at £16,955, so it has gone up over £1,000 in value since then. Considering national and world events at the moment, I am more than happy with this.

As you may recall, I recently put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. It is too early to comment on this yet, but I will include an update about it next time.

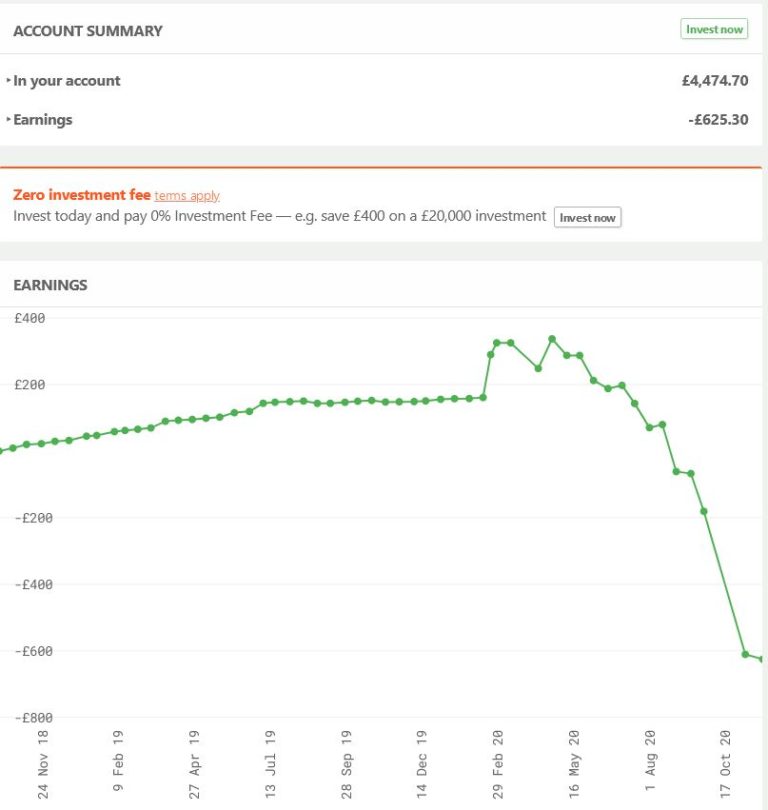

The news hasn’t been so good with my Bricklane Property ISA, which I talked about last time. As stated in in my blog review, Bricklane – not be confused with Brickowner – is a REIT (Real Estate Investment Trust). Investors’ money is pooled to purchase properties. Rental income is then distributed to investors, who also stand to benefit if the value of the REIT goes up. Last month I was down by about £80 on my £5,000 investment, but this month – as you can see from the screen capture below – the figure is over £600.

This is obviously disappointing, though not unexpected. As I said last time, the pandemic has hit property investors hard, especially investors in large commercial properties (as are most in the Bricklane portfolios). But, in addition, the current price factors in the liability of Bricklane and its investors to assess and where necessary replace exterior cladding in some buildings in light of the Grenfell Tower tragedy. I understand that almost half of the properties in the Bricklane Regional Capitals fund (in which I invested) fall into this category.

About the only good thing to be said is that right now Bricklane’s price reflects its liabilities in the worst case scenario. In particular, it has been argued that lease-owners should not bear sole responsibility for paying for this work, as the rules were only changed after Grenfell and it isn’t the owners’ fault that some properties were built to different specifications which were regarded as perfectly safe (and legal) at the time. If the government accepts that argument, in whole or in part, then Bricklane will not have to set aside large sums of money for remedial work, and the share price will rise accordingly. I have written to my MP about this, of course 🙂

As I said last time, if I was braver and had a longer investment horizon, I might look at Bricklane as a value opportunity just now. As it is, I am leaving my money where it is but won’t be investing any more with them for the foreseeable future. I am not planning to sell up as I don’t currently need the money and that would only crystallize my losses. i just hope there will be some better news on this front soon.

I also wanted to say a word about Kuflink this month. This property loan investment platform is still performing well and returning the promised monthly dividends. A couple of loan terms have been extended due to the pandemic but interest continues to be paid and I am not unduly concerned about this. I also had a couple of investments repaid after the loans in question were paid off. So I decided to reinvest in a new six-month loan to help finance the construction of a children’s day nursery in Chorley. Some details of this project from my Kuflink dashboard are shown below…

As you can see, the interest rate being paid is 6.80%. When I invested yesterday the offer had only just launched, so it’s interesting to see it is already up to almost 42% funded now. Although the loan hasn’t gone live yet, as is Kuflink’s normal practice I will received cashback equivalent to the interest on offer until it does, so I am already making money from this loan 🙂

Incidentally, I am not saying this project has any special merit compared with others on the Kuflink platform. But I decided to invest on the basis that it looks reasonably secure with a loan-to-gross-development-value ratio of 36%. And from a more personal perspective, wherever possible I like to invest in projects that will have a socially beneficial outcome, and a new children’s day nursery certainly ticks that box.

i did want to mention as well that I recently updated my full Kuflink review. You can read it here if you like. I’d particularly like to draw your attention to their new and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can actually earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive this!).

My two Buy2LetCars investments are still delivering the promised monthly returns without any issues. As you will remember, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website.

Otherwise, there is nothing especially notable to report on the financial front this month, so let’s move on to the more personal stuff…

Personal

Since my last monthly update England has been mostly in lockdown, so I haven’t been doing anything especially exciting 🙁

I went for my latest checkup at the eye clinic at Burton Hospital in the first few days of the new lockdown. As you may remember, I was diagnosed with a perforated retina after a routine eye test at my optician’s.

I wasn’t allowed to drive, as they put drops in your eyes which blur your vision for a few hours. The trip to Burton involved a bus ride, two train journeys and a one-mile walk, so it took up a whole day. The train journeys in particular felt odd and at times almost post-apocalyptic. I was literally the only person on Lichfield Station waiting for a train to Birmingham, and had the whole carriage (and possibly train) to myself. The train to Burton was a little busier, but you do start to wonder how long the railway network can go on with such minuscule passenger numbers.

It was very quiet at the hospital too, so I was seen straight away. The doctor seemed happy with what he could see, though it’s not easy to tell when he – and everyone else – was wearing a mask. I was told I will have to go back again in January, and if everything is still okay then, they will discharge me. So I guess that’s good news, although they did say that last time as well…

During the lockdown month I aimed to go for a walk every day, and apart from a couple of days of foul weather I achieved that. I have been wearing my new music hat – described in this recent post and pictured below – and enjoying listening to my choice of music. My preferred genre is prog rock (classic and current) but I enjoy jazz and blues as well. I do just find I have to be a bit careful when walking on the narrow country lanes where I live, as with my music playing I don’t always hear cars coming up behind me. Still, I haven’t had any really close calls yet!

I was pleased to be able to go for a swim again this week at my local David Lloyd leisure centre. It was very quiet, and all the staff, including those at reception, are now wearing masks. I suppose some people would find that reassuring. I just find it rather sad and dispiriting. Still, I really enjoyed my swim, and it was great to see a couple of members I know and exchange a few words with them. Even small social interactions like that offer a welcome morsel of normal life in these strange times.

Afterwards I ordered my usual hot drink from the centre’s coffee shop, but because I’m in a Tier 3 area I was told I couldn’t sit down to drink it. I was afraid I might be forced to take it to the freezing cold car park to consume, but was informed there was no objection to me drinking it while standing up in the centre, so long as I didn’t stay in one place for too long. You might think this is barking mad – I couldn’t possibly comment.

There has of course been some good news on the virus front in the last few weeks. As I said last time, new cases (in England anyway) are on a clear downward path. The government are of course trying to spin this as a success for lockdown, but I am sceptical about that. As I said in my November update, cases were already starting to decline pre-lockdown, so what we are seeing now is simply a continuation of that welcome trend.

It’s also interesting that the – admittedly shorter – Welsh lockdown appears to have failed totally, with cases there on the rise again. So they are now imposing even harsher restrictions, including a total ban on pubs and restaurants serving alcohol. I would therefore like to extend my sincere commiserations to Welsh readers (and especially those working in tourism or hospitality) at this time. It is a shame that the four nations of the UK couldn’t have come up with a more coherent, co-ordinated policy to combat the virus – although in my view lockdowns shouldn’t ever be a part of this due to all the collateral damage they cause.

There has been good news about vaccines this week, with the first one from Pfizer/BioNTech receiving regulatory approval in the UK and due to start rolling out next week. I am not an anti-vaxxer and will (probably) accept the vaccine when it is offered. There are, though, some reasons to be sceptical about some of the claims being made for vaccines, nicely summed up in this cautionary blog post by my old friend John ‘Platinum’ Goss. In particular, we still don’t know about any possible long-term side-effects of the vaccines. And with case numbers dropping dramatically in England, you have to wonder how much Covid will still be around in a few months’ time anyway…

In my view, this pandemic will only end when some sort of herd immunity has been achieved. That will be partly through growing numbers of people achieving immunity through contracting the virus, and in addition (hopefully) people acquiring immunity through vaccination. If that is the case, the virus will have nobody left to infect and will ultimately die out (though maybe returning occasionally in milder variants, as happens with other cold and flu viruses). That’s the best-case scenario, anyhow, and I hope it plays out that way.

Before leaving this topic, I would just like to include a quick shout-out for the excellent Lockdown Sceptics website. This site is updated daily and is the first thing I look at when I switch on my computer in the morning. It includes articles from a wide range of academics and other commentators, and offers a sceptical slant on official policies and announcements that is often missing in the mainstream media. Even if you don’t agree with all the views expressed, it’s well worth a read.

As for Christmas, I am expecting to have an even quieter one than usual. I don’t normally socialize a lot at this time anyway. My only remaining close family consists of my three sisters, but they are all in different parts of the country and have their own families and social circles. I have put up my lights and decorations, though, and am looking forward to receiving plenty of cards and letters. I shall also ensure I have a good stock of box-sets to watch!

Well, I guess that’s it for now. I do hope you and your loved ones are staying safe and well and looking forward to the festive season. As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers of PAS will know that I am a fan of the Nutmeg robo-adviser investment platform, and have a good portion of my own money in a Nutmeg stocks and shares ISA. You can read my in-depth review of Nutmeg here.

I was interested to hear that Nutmeg had launched a new investment style for their ISA, Lifetime ISA, Junior ISA, SIPP (personal pension) and general investment account customers. Previously such customers had a choice of three options: Fixed Allocation, Fully Managed and Socially Responsible.

All Nutmeg portfolios are managed by human experts, but the Fixed Allocation ones are altered annually, whereas the others are managed more actively. The Socially Responsible portfolio aims to optimize your investments according to various environmental, social and governance (ESG) factors. So it focuses on companies with a good track record and proactive strategy in such areas as water use, pollution, greenhouse gas emissions, proportion of female board members, and so on. Currently my own stocks and shares ISA is in the Fully Managed category (which was the only option available when I originally invested with Nutmeg).

Whilst all three of these investment styles remain available, a new one was launched in 2020…

Smart Alpha Portfolios

Nutmeg’s Smart Alpha portfolio range is powered by J.P. Morgan Asset Management. It includes five risk-rated portfolios, each holding between 10 and 14 passive and active exchange traded funds (ETFs). They are run by J.P. Morgan’s multi-asset solutions team, giving Nutmeg clients access to the investment giant’s experience and expertise. Writing on the Nutmeg blog, their Chief Investment Officer James McManus explained the benefits of this approach as follows:

The name recognises the intelligent way these portfolios are designed with the potential to achieve alpha (returns above the market) for our clients in three ways.

Firstly: The use of J.P. Morgan Asset Management’s multi-asset specialists, a team with a 50-year history of investing for institutions and professionals worldwide. These specialists inform Smart Alpha portfolios’ long-term (strategic) asset allocation.

Secondly, Smart Alpha portfolios have the ability to be flexible around this long-term asset allocation, allowing us to manage risk and capture opportunities at different stages of the market cycle.

Thirdly: Nutmeg and J.P. Morgan Asset Management have added to these capabilities a means to make smart security selections within active exchange traded funds (ETFs). These smart selections are made based on the insights of J.P. Morgan Asset Management’s research analysts with the aim being to capture returns in excess of the market benchmark (alpha).

How do these smart selections seek to gain alpha? The active ETFs we use allow us to move overweight in certain positions that J.P. Morgan Asset Management’s analysts expect to perform well and underweight in those positions they expect to perform poorly. This gives us the ability to move above and below market benchmark positions, delivering greater potential returns with similar risk to the overall market.

As well as allowing Nutmeg investors to tap into the expertise of J.P. Morgan Asset Management, these portfolios are ESG integrated, meaning that (as mentioned above) environmental, social and corporate governance considerations are factored into every research and investment decision. These portfolios are therefore suitable for the growing number of investors for whom ethical considerations are particularly important.

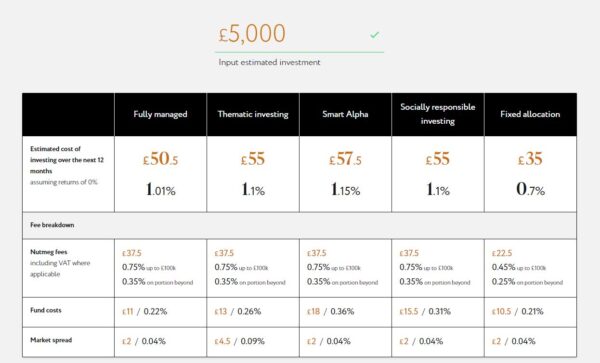

The terms and conditions for the new Smart Alpha portfolios are copied below, alongside the other portfolio types.

The above is correct as at 16 November 2023, but may have changed subsequently. Please note also that Nutmeg has also recently introduced a new ‘thematic’ investment style. More information about this can be found about this in my full Nutmeg review and on the Nutmeg website. Remember that all investing carries a risk of loss.

My Thoughts

This is undoubtedly an interesting move by Nutmeg and gives investors the opportunity to benefit from having their portfolio actively managed by a leading investment house at no extra cost. If you are a Nutmeg investor already, you can start by investing as little as £500 to test the water. You can either use ‘new money’ from your bank account or another ISA, or you can transfer money from another pot within your Nutmeg ISA account.

Personally I am very happy with the way my Nutmeg ISA has performed during this tumultuous year and don’t want to rock the boat too much. On the other hand, I am curious to see how the new Smart Alpha portfolios perform in comparison. So I have created a new £1,000 pot within my ISA and have selected Smart Alpha as the investment style. The risk level is 4/5, which roughly corresponds with the 9/10 risk level in my Fully Managed portfolio.

I will of course report back on Pounds and Sense about how my investments perform. Obviously, if my Smart Alpha pot seems to be doing significantly better than my Fully Managed one, I will switch some or all of the latter to Smart Alpha as well. It is one of the attractions of Nutmeg that you can have multiple pots within a single ISA with different investment styles and risk levels attached to them.

Capital at risk. Tax treatment depends on your individual circumstances and may change in the future.

In Conclusion

I am obviously a fan of Nutmeg and – as stated above – have a significant proportion of my investments with them.

Of course, I am not a qualified financial adviser and everyone should do their own ‘due diligence’ (and/or take professional advice) before deciding to invest. In addition, you shouldn’t consider investing with Nutmeg (or anyone else) unless you have paid off any interest-charging debts and have at least three months of easily-accessible savings in case of emergencies.

Based on my personal experiences with Nutmeg, though, I am happy to recommend them. They provide a simple, easy-to-understand investment platform, the customer service is excellent, and certainly in my case the results to date have exceeded my expectations.

If you have any comments or questions about this post or Nutmeg in general, please do leave them below.

PLEASE NOTE:As with all investing, your capital is at risk. Tax treatment depends on your individual circumstances and may be subject to change in the future. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest.

Note also that I am not a qualified independent financial adviser and nothing in this review should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any way uncertain how best to proceed. All investing carries a risk of loss.

Please note also that this review includes affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the terms you are offered or any fees you may be charged.

If you enjoyed this post, please link to it on your own blog or social media:

2020 has been a stressful and difficult year, but here’s a chance to end it on a positive note. I’ve joined forces with some of my fellow UK bloggers to put together a giveaway with a Samsung 50-Inch Smart UHD TV for the lucky winner.

Read on to find out how you could win this amazing prize in time for Christmas. And please do check out the other talented bloggers who have collaborated on this giveaway.

One lucky winner will win themselves a Samsung 50 Inch UE50TU7100 Smart Ultra HD TV worth a whopping £400! This smart TV is compatible with the following smart apps: Now TV, Disney+, Netflix, BBC iPlayer, Amazon Prime and YouTube. It also has its own built-in Internet browser. To quote from the sales page:

Experience crystal clear colour HDR powered by HDR10+ as the film-makers intended. Crystal Processor adapts to provide the very best 4K picture and targeted sound based on what you are watching. Works with Alexa and Google Assistant. Slim design with very narrow bezel.

How to Enter

To enter simply complete all or any of the Rafflecopter entry options below. The more you complete the more chances you have of winning.

The competition ends at midnight on Sunday 13th December and a winner will be drawn on Monday 14th December. If for any reason the chosen prize is out of stock at the time of the draw, the winner will be able to select an alternative prize up to the same value.

For full entry terms and conditions please see the Rafflecopter widget below.

One final small point is that if a winning entry comes from following someone on social media, the organizers will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and here’s hoping we can all look forward to a happier Christmas!

If you enjoyed this post, please link to it on your own blog or social media:

The number of people applying for Universal Credit has surged to record levels as a result of the Coronavirus pandemic and the numbers are set to rise further with the ongoing economic uncertainty.

In addition to a loss of income, households could also be facing a rise in energy-bills due to more time spent at home and cold weather approaching. Many will be coming to grips with the benefits system for the first time and starting to understand the rules, regulations and complexities around making a claim.

However, there is a little known silver lining for these claimants. Anyone who has claimed Universal Credit successfully will also be eligible for home improvements under the Government’s Energy Company Obligation (ECO) scheme.

This current scheme, called ECO3, targets people that have high energy costs comparative to household income. The scheme has a list of ‘qualifying benefits’ for eligibility. Universal Credit is on that list.

Plus, there are no savings or income-tests for the qualifying benefit part of the application, so if you receive any benefit on the list below (excluding Child Benefit, as that has an income cap), it’s likely you’ll be eligible.

According to Ofgem (who administer the ECO scheme), claimants will still be eligible for a period of 18 months following the date of the letter for the Universal Credit award (page 44 of the Ofgem ECO3 guidance has full details).

So if, say, you were awarded your Universal Credit in April but you got a job last week and came off Universal Credit today (for example), you still have a significant period of time (a year and a half) to apply for and install the measure, as you would still be classed as eligible even when you return to work. While you can wait to apply, it’s advisable to apply sooner rather than later, as funding rules can change at any time.

Even if you have returned to work or are planning to return to work, you will still be eligible, providing you have had at least one award for Universal Credit.

And it isn’t just Universal Credit recipients who are eligible for grants. Also on the ‘qualifying benefits’ list are the following:

Armed Forces Independence Payment

Attendance Allowance

Carer’s Allowance

Child Benefit*

Child Tax Credit

Constant Attendance Allowance

Disability Living Allowance

Income Support

Pension Credit (Guarantee)

Employment and Support Allowance (income-related)

Jobseeker’s Allowance (Income-based)

Income Support

Industrial Injuries Disablement Benefit

Mobility Supplement

Personal Independence Payment

Severe Disablement Allowance

Universal Credit

War Pension Mobility Supplement

Working tax credit

* Note: If Child Benefit is the only qualifying benefit you receive, you will also need to meet additional income rules detailed here.

You will still be eligible if you return to work as you can claim for a period of 18 months after claiming benefits.

What Grants Are Available?

There are a range of energy-efficiency measures that can be installed under the Energy Company Obligation (ECO) scheme, including boiler upgrades, home insulation and heating upgrades. The Scheme is funded by the major energy companies and if you claim benefits, you are entitled to this funding.

Table: Measures Available Under the Energy Company Obligation Scheme

Measure

Homeowners

Private Tenants

Housing Association Tenants

Landlords

Council Tenants

Air Source Heat Pump (ASHP)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Boiler Upgrade or Repair

✅

❌

❌

❌

❌

Cavity Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Electric Heating Upgrade

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

First Time Central Heating (FTCH)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Internal Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Underfloor Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

How Much Could You Get?

The amount of funding available depends on a range of factors, including property type, your existing heating, wall type and potential energy savings from proposed work.

The first step in working out what you could get is to check your eligibility online. There’s a quick form on the Energy Saving Genie website where you can enter your details to see if you are eligible.

If you meet the criteria, you can choose to apply and once your application has been submitted, it will be passed to a Registered Installer.

The Registered Installer will arrange a free survey of your property. You can choose to proceed ASAP with a survey taking place following strict health and safety guidelines or you can choose to wait until after Covid-19.

Once the survey has taken place, the surveyor will report back to the Registered Installer, who will talk you through the grants that are available towards energy-efficiency measures at your property.

The grant is paid directly to the installer and they are awarded on lifetime savings (LTS) scores. Currently electric heated properties and larger properties tend to receive the most funding. But even if your home isn’t large or heated by electricity, it is worth applying as you could still receive a significant grant towards home improvements.

So if you are one of the many million new Universal Credit claimants due to Covid-19, you can start the process of applying for a home improvement grant that will knock £££s of your energy bills for years to come, well after the pandemic has passed.

Check your eligibility here!Disclosure; This is an adapted reblog of an original post by Energy Saving Genie. It is also a sponsored post. If you click through and end up taking advantage of this government scheme, I will receive a fee for introducing you. This will not affect any products or services you may receive or the value of any grants you may be awarded.

If you enjoyed this post, please link to it on your own blog or social media:

Another month, another coronavirus crisis update. Regular readers will know I have been posting these updates since the first lockdown started (you can read my October update here if you like).

As always, I will discuss what has been happening with my finances and my life generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as from feedback received I know many of you like to follow this.

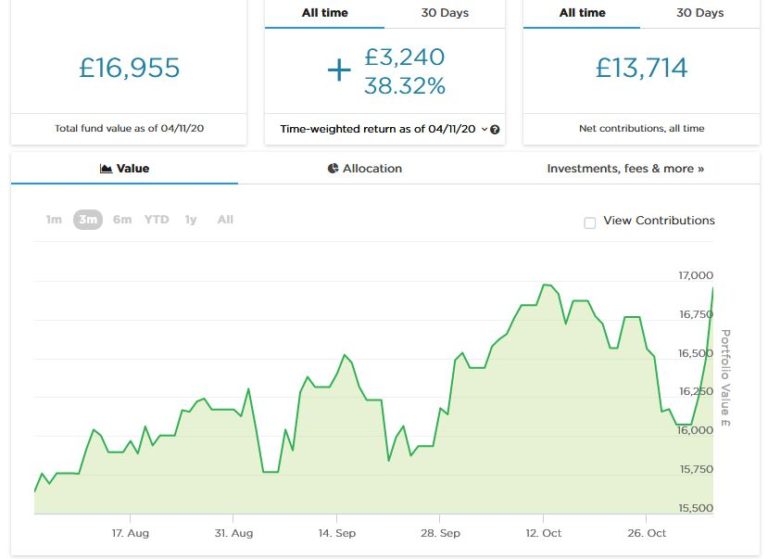

As the screenshot below shows, my portfolio has been on a roller-coaster ride over the last few weeks but is currently valued at £16,955, about £500 up on last month. Considering national and world events at the moment I am very happy with this. You can read my in-depth Nutmeg review here (including a special offer for PAS readers).

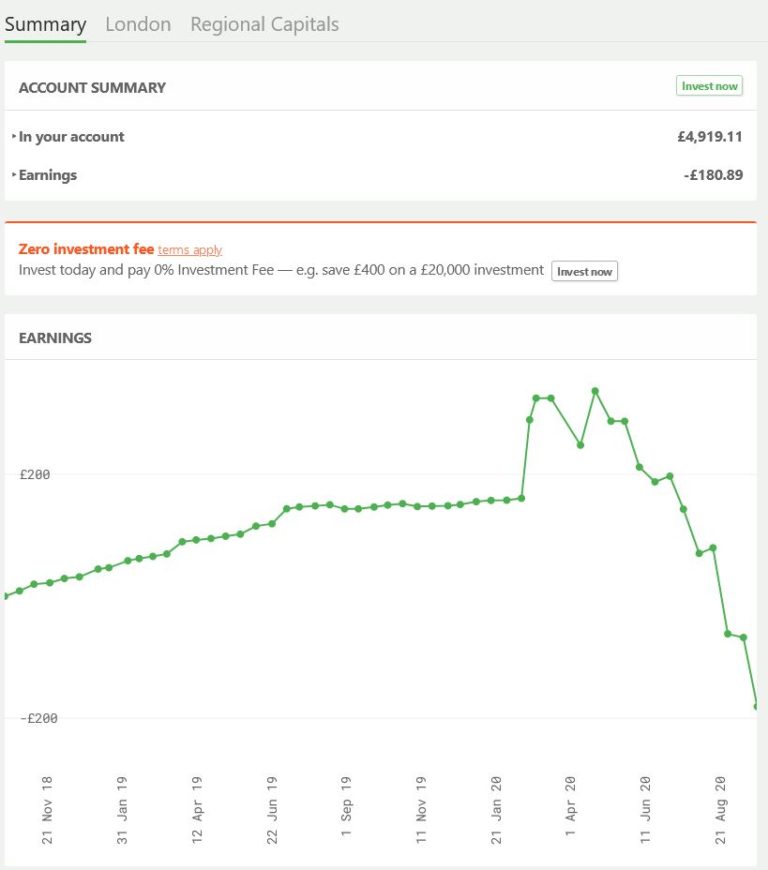

I haven’t mentioned my Bricklane Property ISA for a while, so I thought I should rectify that this month. As discussed in my blog review, Bricklane – not be confused with Brickowner – is a REIT (Real Estate Investment Trust). Investors’ money is pooled to purchase properties. Rental income is then distributed to investors, who also stand to benefit if the value of the REIT goes up. As you can see from the chart, though, this year the trajectory has been largely downward.

.

At first glance this looks alarming, but of course it’s important to note that the vertical axis of the graph goes from minus £200 to plus £200, so in reality the losses aren’t as bad as that scary-looking precipice might suggest. Allowing for the fact that I received a £100 welcome bonus when I signed up with Bricklane, overall I am about £80 down on my £5,000 investment. Of course, that’s not what you would hope for, but this has been a particularly tough year for anyone investing in property. Among other things, rising unemployment, company failures, more people working from home, and rising defaults on loans and mortgages (along with mandatory payment holidays) have all affected demand and reduced rental returns and property values.

A recent email from Bricklane gave further insight into the problems they are facing. It turns out that the Regional Capitals fund (in which I am invested) includes a number of properties that may need extensive refurbishment in light of the Grenfell Tower tragedy. As I understand it, they have cladding which needs assessing by specialists and may have to be removed and replaced. This is a time-consuming and costly business. Of course, the owners (who include me as an investor) have no option but to undertake this, and inevitably this is having an impact on the value of the fund.

This does of course illustrate that any investment in a single asset class such as property carries additional sector-specific risks compared with broader-based investments, and you may see greater volatility as a result. On the plus side, when investing in property your money is secured by bricks and mortar, so it’s very unlikely you will lose your shirt.

I guess if I was braver and had a longer time horizon, I might look at Bricklane as a value-investing opportunity just now. As it is, I am leaving my money where it is but won’t be investing any more with them for the foreseeable future. I am not planning to sell up as I don’t currently need the money and that would only crystallize my losses.

Otherwise there is nothing dramatic to report on the financial front. My two Buy2LetCars investments are still delivering the promised monthly returns without any hassle. To recap, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. I heard from the company today that they are allowed to continue trading in England’s second lockdown and are already experiencing an upsurge of enquiries from key workers needing transport. So if you are looking for an income-producing investment with a substantial lump sum payment after three years, they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website.

My Property Partner and Kuflink investments are still both ticking along satisfactorily. Unsurprisingly there have been delays in repaying some of my Kuflink loans, but I continue to receive monthly interest payments on them and am not unduly concerned. As regards The House Crowd, I assume that the sales of the two properties in which I hold £1,000 shares are progressing, but can understand that it is a slow process. As with Kuflink, rental payments are still accruing, which should help to defray some of the selling costs.

There has been no further word either regarding my investments with Crowdlords. As I said last month, I have two remaining investments with them, Kennington Road eco-houses and Trent House. I was told they hope to have exit options for these properties by the end of the year, but I’m not holding my breath. On the plus side, they are paying 6 percent interest on my Trent House investment, which is quite generous in these days of ultra-low interest rates.

Personal

Thankfully this month has been less eventful for me than the previous one. Touch wood my left eye is recovering well after the laser treatment (thank you to those who have asked and/or sent me good wishes about this). I am going back to Burton Hospital in a week’s time for what I hope will be a final check-up.

I still have floaters in both eyes – worse in the left – but that is not unusual for people of my age. It’s annoying but not dangerous in itself, and there isn’t really any treatment (I understand lasers can be used in extreme cases to ‘blast’ them, but it’s rare to do this as it risks causing other damage). I did read online about a Chinese study which found that eating pineapple can help reduce floaters, so I was happy to have an excuse to eat more of this delicious fruit!

As I write this, England is going into its second lockdown. I am dubious about the wisdom of this and worried for people whose physical and mental health is likely to suffer, especially as it appears the second wave has already peaked and new case numbers are starting to fall.

I am at least thankful that the schools have been exempted this time. I live quite near a secondary school, and it lifts my spirit when I see the young people bursting out of the school gates at the end of the day. chatting to their friends, larking around, and generally doing all the things young people do. And not a mask in sight!

Today I am off to see my accountant to discuss my annual accounts. He works from home and neither of us was sure what rules applied in this situation, so in the end we agreed to meet outside on his front drive. At least this will help to ensure that the meeting doesn’t go on a minute longer than it needs to 🙂

I had a winter flu jab last month (the first time I’ve qualified for a free one as I reach 65 later this year). It seemed a sensible thing to do, especially as it may give some protection from Covid too. I did have a reaction to it, though. I woke up at around 2 am shivering violently, and then I started to get nausea as well. By morning I was feeling a lot better, apart from having had almost no sleep. Apparently these are quite common side effects of the vaccine, though two friends (both older than me) didn’t get any effects at all.

I went for my last pre-lockdown swim on Tuesday. The centre was busier than usual, so I guess I wasn’t the only one who decided to take the opportunity while it was still available. I am very disappointed that pools have been made to close again as there is no evidence the virus is spreading this way and many people (me included) depend on swimming for our physical and mental health. I just hope they reopen at the start of December and the lockdown isn’t extended. Personally I expect the numbers of new cases to continue falling over the next few weeks, not due to the lockdown but simply because that is the trend now. If that is the case, there will be no excuse for prolonging the lockdown. But I guess by the time of my December update we will know one way or the other!

Finally I am still dutifully completing the UCL Virus Watch weekly questionnaire saying whether I have any possible Covid symptoms (none so far). And I am still waiting to hear when I will be able to take the blood test to see if I have any antibodies or other natural resistance to the virus. But I gather they wouldn’t be able to do that until a few weeks have elapsed after the flu jab anyhow, so it may be just as well I’ve heard nothing yet.

So that’s it for this month really. I hope you and your loved ones are staying safe and well. As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

For many of us, our mortgage is our biggest monthly outgoing. So it’s important to keep a close eye on it and check regularly whether you could save money by switching to another provider.

That’s exactly what a new online service called Dashly aims to do. They evaluate your current mortgage deal against the whole market, taking into account your specific personal circumstances as well. If they find a better deal for you they let you know and – if you choose to proceed – assist you with the switching process.

How Does Dashly Work?

Dashly is available as a desktop site, with mobile apps for iOS and Android coming soon.

You start by registering and entering some details about your current mortgage and your personal circumstances. The latter is important, as things such as your income, employment type, credit score and age can all affect the deals you could be eligible for. This process takes 10-15 minutes. Dashly then compares your mortgage against an average of 10,000 products to find the best deal for you.

If they find a better deal than your present one, they send you a notification. You can then evaluate this and decide whether you want to switch. If you do, the team at Dashly will assist you with the switching process.

In addition, Dashly will continue monitoring your mortgage every month. If they find you could save money by switching again, they’ll let you know. It’s worth noting that the equity you have in your property changes on a monthly basis due to ever-changing house values and your decreasing mortgage balance. As your LTV (loan-to-value ratio) decreases, your mortgage may qualify for better, cheaper deals. Again, Dashly checks this on your behalf.

You receive a detailed personal report from Dashly about your mortgage every month. In addition, your dashboard will show you all the key facts at any time, from the changing value of your property to the amount of equity in it, any current deals that would save you money to your next payment date. It’s all there on one easy-to-read web page.

How Much Could You Save?

The savings can be substantial. Dashly say that on average their users save £2,620 (see footnote).

Of course, in practice savings will depend on a number of things, including the balance outstanding on your mortgage, the competitiveness of your current deal, the term left to run, and the effect of any early repayment penalties. Dashly takes all of these things into account in determining whether you could save money by switching to a new lender (and by how much).

Are There Any Costs?

Using Dashly is free. There are no hidden charges and Dashly say they will never hit you with advertisements or email campaigns to try to make money from you. They get paid out of mortgage provider fees, and are authorized and regulated by the Financial Conduct Authority.

Dashly are also founding members of Finance For Good, a charity run by social impact fintechs who put consumers first. They say that their security rivals that of the world’s leading banks.

In Conclusion

If you have a mortgage, in these uncertain times it’s more important than ever to ensure that you aren’t paying over the odds for it.

Dashly offers a free service that not only checks whether you are getting the best deal currently but also continues monitoring your situation month by month and recommends switching again if a new and better deal arises.

By using Dashly you could painlessly save hundreds or even thousands of pounds on the cost of your mortgage. There is never any obligation to switch or any fee to pay for the service. So you really have nothing to lose and everything to gain by registering for an account today.

Footnote: Your individual savings may vary and will depend on personal circumstances. £2,620 per year is the average amount based on research Dashly has conducted on the mortgage market. Find out more at www.dashly.com/reference-index.

Disclosure: This is a sponsored post on behalf of Dashly. If you sign up and make use of the service, I may receive a referral fee for introducing you. This will not affect in any way the service you receive or the deals you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Life insurance isn’t the most exciting of subjects, but in these uncertain times it’s something we all need to think about.

Not everyone requires life insurance. If you are single with no dependants and/or on a very low income, it may not be necessary or appropriate for you. But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death.

Table of Contents

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

What Doesn’t It Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

Other things being equal, the younger and healthier you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Bespoke Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It is therefore important to establish what is the most appropriate option for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Bespoke Financial. They are independent insurance and mortgage brokers, and will take the time to establish your exact requirements and design a ‘bespoke’ package to suit you and your family’s needs. Their trained advisers will visit you in your home (with all necessary Covid precautions) or you can speak on the phone to them. They can arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on.

To get an initial personalized quote, click through to the Life Insurance page of their website and answer six quick questions. You can then discuss this with an adviser to ensure you will be getting exactly the right type and level of cover for your needs.

And as an added bonus for readers of my blog, you can get a free will just by asking for a quotation. You can’t say fairer than that, now can you?

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Bespoke Financial. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

2020 has been a year like no other. And while the first vaccine has just been approved, for many of us this winter still looks like being a long, hard and stressful one.

There is no doubt many people’s mental health has been impacted both by the threat of the virus and the measures taken by government to try to control it. Add to that, many people have seen their income reduced or lost their jobs altogether, causing financial hardship as well.

Clearly we all need to find methods for getting through this difficult time. So I asked some of my fellow bloggers to share any tips they might have, including things they are doing to help them (and their families) cope. I have listed their answers below, with my own reactions in italics afterwards where relevant. I will then say a bit about how I am planning to get through the Covid winter myself.

Bloggers’ Tips

Jo Jackson who blogs at Tea and Cake for the Soul says, ‘List your outgoing payments and see what can be got rid of or reduced. List all of your utility accounts, insurances and entertainment packages then look at comparison sites to see if you can get better deals elsewhere.’

Always a good idea and can save you a lot of money. Check out cashback websites as well, as they may offer cashback if you switch to a new supplier.

Sally Allsop of Life Loving says, ‘Buy yourself a big thermos or two and fill them with hot drinks and homemade soup. Then you can still go for days out without having to worry about mingling and queuing at eateries/cafes. You’ll also be able to keep yourself warm on theoretically safer outside winter activities.’

Hayley Muncey, who blogs as Miss Manypennies, says, ‘I’ve applied for the 30 hours’ free childcare funding for my 3-year-old. Normally I love taking her out and about to playgroups, the library and meeting to play with her little friends, but since everything is cancelled, closed and we’re not allowed to meet anyone (local lockdown), preschool is basically the only social activity she’ll have, so I’m going to up her hours. I think she’ll have more fun there than stuck at home! Plus it gives me more time to concentrate on working from home, so hopefully I can bring in a bit more money.’

I didn’t know anything about this scheme, but there are more details on this government website if you may be eligible. In England you need to have a child who is 3-4 years old. Other schemes apply in different parts of the UK.

Jennifer Graudenz of Monethalia says, ‘Sign up at your local library. Many libraries let you take out eBooks, so you will always have something to read, no matter how many lockdowns we have.’

Good idea. You can still borrow ordinary print books as well but special Covid precautions are likely to apply. Ask at your library for more info.

Ryan Maley who blogs at A SIngle Step says, ‘Try to keep some sort of routine, even if you are stuck in the house all day. If you’re working from home, make sure you stick to set hours with a lunch break, and have a separate space in which to work. Organise calls, video calls, quizzes and virtual catch-ups with friends and family. Try to get fresh air or exercise whilst following the rules. A run after work or exploring some local countryside can do wonders. Or even dancing along to a YouTube video in your bedroom. Most of all, if you are struggling, make sure you speak to friends or family. A problem shared really is a problem halved.’

Claire of Stapo’s Thrifty Life Hacks writes, ‘We are a family of three and a few weeks ago we invested in waterproofs for the whole family. We started walking a lot at the start of lockdown and as things ramp up again, we know that we will want to get out and explore where we can. As we now have all the right gear, we are hopeful that the rain and wind won’t put us off getting out there as autumn turns into winter.’

Fiona Hawkes who blogs at Savvy in Somerset says, ‘We’ve started planning at-home Christmas activities, as trips to visit Father Christmas and big family gatherings won’t be happening this year. I’m making my daughter an activity advent calendar for us to enjoy during December which includes things like Christmas story books, festive cake making, writing letters and cards to family we won’t see and making lovely decorations for our home.’

Human Carley, who blogs at the wonderfully named Unicorn Puffs and Rainbows, says, ‘Make your house as cosy as you can. Clear out anything you can now whist charity shops and recycling centres are open. Having as much usable space as possible will be important, as we will have much less time outside.’

You could sell anything you no longer need on eBay or similar sites to boost your income as well. There are some great tips about selling on eBay in this guest post by Lucy Olivia.

Anisa Alhilali who blogs at Two Traveling Texans says, ‘Feed your travel wanderlust. Even if you can’t travel there are ways to have “travel-like experiences” from home. You can take a virtual tour, have a travel-themed night, read a travel book, and more.’

Love this idea. You could start planning for future post-Covid adventures.

And Anisa also has a blog called Origami Expressions. She writes: ‘Take advantage of the time at home and learn origami. It is great for mindfulness and you will be amazed at all the things that you can make with just a sheet of paper!’

And it costs almost nothing as well. I may just try this myself!

Victoria Sully who blogs at Healthy Vix says, ‘Make sure you have ways to relax and chill at home to reduce the stress. This year I have just invested in a bath pillow, fluffy bath mat, candles and some soothing bath foam to indulge in some some luxurious baths this winter to take the stress away! Even something as simple as lighting candles in the evening can be calming and help to reduce stress.’

Anne Fraser who blogs at The Platinum Line says, ‘My lifesaver at the moment is our local leisure centre. Although a lot of classes have been cancelled they are still hosting an over 60s lane swim twice a week. I think it is important to find an indoor activity you enjoy and if it makes you healthier so much the better.’

Absolutely. I love swimming and was so relieved when my local leisure centre and pool reopened.

Vicky Smith of More Than A Mummy says, ‘For Christmas we will only buy gifts for the kids in the family. Will save valuable cash at a time when our business has been hit hard by the pandemic. We actually started doing this last year and it saved me hundreds as our family is huge!’

Jenny Tate of The Life Stuff says, ‘Check with your current suppliers to see if you can make any savings i.e. gas, electric, TV, internet providers. My internet bill was put up last week to £54/month so I called up the provider and got the exact same package for £26!’

Shelley Whitaker who blogs at Wander & Luxe says, ‘We are preparing at home by making sure we have plenty of things to entertain ourselves and our toddler. For example, crafts, puzzles, things to cook and DIY bits for around the house. We are also purposely not watching too many movies or TV shows so we have things we want to watch if needed. For now I am trying to get out each day and do normal things that I am able to (restrictions permitting), and basically just take each day as it comes.’

Sarah Bailey of Life in a Breakdown says, ‘Think about making some family time using a video calling service. Some of them cost after so long but some don’t, so shop around and don’t just use the one most spoken about. It will allow you to keep in touch with family during this time should the worst happen!’

Emma Reid who blogs at Emmareid.net says, ‘Just because it’s chilly doesn’t mean you can’t still go exploring and get outdoors. We are doing 1000 hours outside challenge and we still have a bit of a way to go to hit it so I am making the most of the days we have left to get outside whatever the weather. As long as you have the right gear, you can still have fun.’

Finally, Emily Jane of Emily Underworld says, ‘While winter means Christmas and the season of giving, don’t forget to practise self-care. This can be anything from rest to time alone for meditation. As my budget for Christmas this year is low, I’ll be supporting small UK businesses, as well as making some gifts myself. Getting creative is great for self-care, and it’s also great for my bank balance.’

Yes, as well as being kind to others we also need to be kind to ourselves at this difficult time. And I do agree as well with supporting local businesses, many of whom are having a very tough time of it.

My Own Thoughts

I have also been thinking a lot about how to stay sane and well over the coming months.

As you probably know, I’m semi-retired and live alone. Nowadays blogging is my main source of earned income. It doesn’t make me a fortune – far from it – but I’m lucky enough to have savings and investments and a small personal pension as well to keep my finances ticking over.

As well as being a source of income, working on the blog gives my days a bit of structure, which we all need at the moment. I typically spend a few hours each morning on it, then do other things (e.g. going for a swim or a walk) later. I feel as though once I have got my ‘work’ out of the way I have earned the right to do other things I enjoy. Though I do enjoy writing and blogging as well, of course!

I am planning other activities as well. Some friends told me recently that over the winter they intend to get on with some decorating projects. While that doesn’t appeal so much to me, there are a number of jobs around the house and garden that I really do need to tackle. I plan to make a list of them and see how many I can tick off before the spring!

I am also considering getting into video gaming – though as I spend a lot of time anyway at a computer or watching TV, I am not entirely sure I should be lining myself up for more hours staring into a screen.

I’m also thinking of teaching myself a musical instrument – possibly tenor ukulele, as I have heard they are among the easiest instruments to learn, although I am open to other suggestions 😀

I am also trying my best to keep some sort of social life going, even in the face of mounting restrictions. I don’t live in an area under lockdown (yet) so am hoping and planning to go on meeting friends for pub lunches. I am also keeping in touch with friends/relatives as much as possible using video calling and traditional phone calls. It has been particularly good to be in more regular touch with my sister Annie, who also lives alone. We speak on the phone most weekends now, and it’s been great to hear what’s been going on in her life and her job (she works as a librarian).

I agree with my fellow bloggers who pointed out the importance of staying active even in the cold winter months. I aim to go swimming at least once a week and really enjoy this, not least because it’s something normal I can still do at a time when our freedom of action is increasingly limited. I also try to go for a walk every day, though as the weather worsens I suspect I won’t be doing this quite as often.

Finally, although I did say I’m wary of spending any more time than I do already staring at a screen, I’m considering taking out a Britbox subscription for the long winter nights. They have a lot of classic BBC and ITV series that I would enjoy watching (or re-watching). And I must admit I wouldn’t mind giving the new Spitting Image a try as well!

I’d like to close this post by thanking my fellow bloggers for their varied and thought-provoking suggestions for surviving this Covid winter. I hope you may want to check out at least some of their blogs.

And, of course, if you have any comments or questions about this post, or any other suggestions for coping over the coming months, I’d love to hear them. Please leave a comment below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

.

.