Today I am sharing some information about National Conversation Week, a collaborative initiative between financial organizations Paymentshield and Defaqto, together with mental health charity Mind.

What is National Conversation Week?

National Conversation Week – which this year runs from 11 to 18 May – aims to get people talking in a bid to improve the nation’s well-being, at a time when we are all facing unprecedented challenges and are separated from one another. This annual awareness week, founded by Paymentshield, is now in its fourth year.

Through safe conversations via phone, video calls, or any other socially-distanced method, people can bring comfort and care to one another during the current crisis. National Conversation Week reminds people to get in touch, and encourages creative ways of connecting with friends, family, neighbours, acquaintances, online communities and professionals, to give and receive much-needed support.

In particular, National Conversation Week hopes to encourage conversations about money, to tackle financial worries. A recent YouGov study of over 1000 GB adults, commissioned by Paymentshield, revealed that finances were the single biggest concern when asked to select from a list of 7, with 32% of respondents admitting that money is the thing that worries them the most – ranking higher than work, family, friends, fitness, housework, and hobbies. This is likely to have increased following the outbreak of coronavirus, with many people facing additional financial difficulty and uncertainty.

Financial Worries and Mental Health

Financial worries have a huge impact on mental health, and talking to someone about the situation can be very helpful. Shockingly, Paymentshield’s research discovered that 41% of people rarely ask for financial advice when they need it.

According to financial experts at Paymentshield, during periods of financial uncertainty, people tend to consider their outgoings and can be tempted to make risky financial decisions based purely on cost. Seeking the help of professionals is especially recommended during these periods, to avoid being left vulnerable if, for example, you cancel an insurance policy and are no longer protected, or swap to a cheaper policy without understanding how to avoid higher compulsory excess fees. National Conversation Week raises awareness of the benefits of talking to financial advisers, so that people can have a better understanding of what they can do if their circumstances have changed.

As part of the awareness week, a variety of free resources and information have been released. This includes mental health information from Mind, which is National Conversation Week’s charity partner for the second year in a row.

Stephen Buckley, Head of Information at Mind, says:

“The coronavirus outbreak will have a long-term impact on our economy – we’re likely to see another recession as the nation attempts to get back on its feet. We know there is a strong link between issues like debt, unemployment, poor housing and poor mental health.

“So, it stands to reason that factors like job insecurity, unemployment, low paid work and redundancy could have a knock-on impact on mental health. Unfortunately, we know these kinds of factors disproportionately affect people who have existing mental health problems. That’s why it’s important that financial support and support with wider social issues are there for people when they need it.

“Speaking about these issues and asking for help may seem daunting but sharing your worries can be a real relief and is often the first step in getting the help you need. We’re supporting National Conversation Week in the hope that it will encourage people to speak to a friend, family member, or another trusted individual about how you’re feeling.”

Jennifer Ripley, Head of Marketing at Paymentshield, says:

“We might not be able to see each other face-to-face, but that doesn’t mean that conversations have to stop. We know that right now is a particularly worrying and challenging time, especially with so much uncertainty, and whilst people are cut off from their usual support networks. It’s more important than ever before that we stay in touch, especially when it comes to financial conversations. Money is one of the biggest contributors to poor mental health. We’re calling on the nation to keep the conversation going – from video calls with a financial expert, to a chat with grandparents – and support each other.”

Independent financial research company Defaqto is also supporting this year’s National Conversation Week. Its independent comparison tools can be used alongside conversation on many websites (such as this one) to gain a better understanding of the overall value and quality of a financial product.

To mark the start of the week, Paymentshield has also launched an online quiz to help people find out more about their financial personality, and how conversation could benefit them. Why not try it out now to see what sort of financial personality you have? I am ‘Budget Bobby’, apparently!

Thank you to my friends at National Conversation Week for sharing the information above and, in particular, raising the very important issue of mental health and financial awareness at this challenging time. I strongly recommend checking out the website resources mentioned. And I’d like to endorse the advice that if you have money worries, don’t bury your head in the sand. Speak to friends and family members, and to a financial expert if appropriate (here’s a link to my blog post about why I have a personal financial adviser).

As so many of us are struggling financially right now, I’ve teamed up with some fellow UK bloggers for a great giveaway. We have over £100 worth of supermarket vouchers to help two lucky winners with their grocery shopping 🙂

The first prize is a whopping £75 voucher. The runner-up will receive a £30 voucher. Both vouchers will be for supermarkets of the winners’ choice. The prizes will be e-vouchers for supermarkets that offer home delivery, including Tesco, Asda, Sainsbury’s, Waitrose and Iceland (subject to availability).

This giveaway has been organised by my fellow blogger Kellie Steed at the comping website Prize Warriors. Do check out her excellent site if you are interested in winning more cash and prizes from consumer competitions!

To enter the Bloggers Together Giveaway, all you have to do is work down (or up) the Rafflecopter widget below. As you will see, for each action you take (e.g. following a blogger on Twitter or visiting their Facebook page) you will receive one entry. The winners will be drawn at random, so the more times you enter, the better your chances of success.

The closing date is 31st May 2020, so get clicking now!

All of the bloggers listed below have contributed towards this giveaway prize. Please check out their blogs via the links below. They are all well worth reading, and many run giveaways of their own too.

I do hope you enjoy taking part in this giveaway, and even if you don’t win a prize you discover some wonderful bloggers to follow in future.

One small point is that if a winning entry comes from following someone on social media, Kellie will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow (or claim to be following when you’re not), as your entry won’t then count.

Good luck if you enter the Bloggers Together Giveaway – it would be great if a Pounds and Sense reader won one (or both) of the prizes!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m focusing on a money-making opportunity that is literally open to anyone. It involves advertising your services on a website called Fiverr.

Table of Contents

What is Fiverr?

Fiverr is a US-based site that lets anyone advertise ‘gigs’ (tasks) they are willing to perform for five dollars – hence the name, of course. You are also allowed to charge more than $5 as you gain positive feedback and experience.

Gigs range from the serious (e.g. write a press release) to the creative (e.g. design a tee-shirt – see cover image) to the downright quirky (e.g. write your message, name or URL in chocolate). Most gigs are services that are delivered electronically, though there is nothing to stop you selling physical products if you wish (you can charge extra for postage).

Fiverr was launched in 2009, and they recently revealed that freelance earnings via the site now exceed a billion dollars. Whatever your skills or interests, there is bound to be a service people will pay you to provide there.

Of course, you may already have noticed one potential drawback. Five dollars is only around £4.03 at current exchange rates. And in fact it’s worse than that, because Fiverr’s fees and charges have to be deducted, meaning that you will only receive about $4, or £3.22, for each $5 gig you complete.

Read on, though, because there are techniques you can use to boost your Fiverr income to something far more substantial. But first, you will need an account…

Getting Started on Fiverr

Joining Fiverr is straightforward (and free).

Navigate to the Fiverr homepage and at the top, click on ‘Join’. A sign-up box will then be displayed.

Fill in the fields for your email address, username, and password (your choice). Read and accept the terms of service, and complete the inevitable captcha form. Then click the Join button. You will see a page displayed with a message that says ‘Activation link was emailed to you’.

Check your email for a message from Fiverr with the subject line ‘Fiverr: Registration Confirmation’ and click the link inside the email message. You should then be taken to a page on Fiverr that says, ‘Account successfully activated. Hey, this is a great time to edit your Profile.’

Congratulations! You’ve completed the registration and sign-up process for Fiverr. Make a note of your user name, password, and the email address you used to sign up so that you can log in again in future.

One other thing you should do as soon as possible is to fill in all the fields in your profile, including a picture of yourself. It’s important to have a completed profile, so that potential clients can see the person they will be dealing with. In addition, your gigs will only be eligible for extra (free) promotion on Fiverr when your profile has all the blanks filled in.

Finally, you will need a Paypal account to receive your fees. If you don’t have one already, you can sign up here. As you will be running a business, you should get a business account rather than a personal one. Note that Fiverr operates primarily in US dollars, but with PayPal it’s very easy to change one currency in your account to another.

Listing Your First Gig

Once you’ve decided what service you are going to offer – spend some time browsing Fiverr for ideas if you’re not sure – you’ll want to list your first gig. Here are six tips for getting off to the best possible start…

Very important – create a high-quality digital image that’s relevant to the gig you’re selling. This will be different from your profile photo. Make the image colourful, vivid, and expressive. It should stand out and draw a potential customer’s eye.

Add keywords to the listing for your ad. This is important, too, as it increases the number of views your gigs will receive. The more views you receive, in general, the more sales you are likely to make.

Write a thorough, easy-to-understand description of your gig. If you’re unsure how to do this, search for other gigs that are generating a lot of ‘stars’ and positive comments.

State a realistic length of time it will take you to deliver the product. Get this wrong, and the negative comments will affect your ability to sell that gig in the future.

Provide clear instructions to the buyer. This will save you hours of answering unnecessary emails from customers. Tell them exactly what they must do, how they should do it, and what they can expect. If you still receive the same questions repeatedly, add another sentence or two to your instructions.

Consider creating a video to introduce your gigs.

The latter is becoming more and more common on Fiverr. For some types of gig nowadays, having a ‘gig video’ is virtually obligatory. In your video you can talk about (and preferably demonstrate) the service you are offering.

As well as adding interest to your listing, using a video will increase the exposure to your gig, not only on Fiverr, but in the search engines as well.

You can also use YouTube to promote your Fiverr videos. As Google owns YouTube, there’s a good chance your Fiverr video will be shown high in Google’s search results for your selected keyword/s.

If you don’t have a dedicated video camera, you can, of course, make perfectly serviceable videos nowadays using a mobile phone, smartphone, or even a webcam.

Another option is to use screencasting software, such as the free web-based Screenr. This will allow you to record a video up to five minutes long showing whatever is on your computer screen with your spoken commentary over it.

And, of course, there is no shortage of people on Fiverr offering to create a gig video for you!

Promoting Your Gig

Fiverr is one of the top 200 sites on the internet and attracts huge amount of traffic – so the very fact of listing your gig there will ensure plenty of people see it.

You should, however, make an effort to promote it yourself as well, especially when you’re just starting out and don’t have much of a track record.

Every Fiverr gig has its own unique web page URL, and you should share this as widely as possible. Put it in your email signature, and post it on Facebook, Twitter and any other social networks you belong to. If you use online forums, include the link in your signature text (most forums will permit this). If you’re a blogger, blog about it too.

As mentioned, it can also be a good idea to create a gig video and post it on YouTube. This is another site that generates huge amounts of traffic, and can provide another route for potential buyers (and search engines) to find you.

Techniques for Boosting Your Income

At first glance the earning potential of Fiverr looks limited. But with a little imagination, you can effectively boost your returns many times over. Here are three top techniques you can use…

Do the Work Once, Sell Multiple Times

This is a technique anyone can use, even if they are brand new to Fiverr. For example, you could write a short report or e-book and sell it through the site multiple times. This is slightly against the spirit of Fiverr, but I’ve seen plenty of people doing it. Here’s one current example…

‘I will list ten great under-appreciated horror movies by cult and old-school movie directors for you and write a brief synopsis for $5.’

I assume this individual has already written his report and simply sends it to anyone who pays the $5 for it.

One top tip here is to make it sound as if you are personalizing your offer for each recipient. As in the example above, refer to the reader as ‘you’ and explain exactly what you (and your report) are going to do for them. Essentially, by this method, you could sell the same report dozens of times, potentially making hundreds of pounds or more from a single short report.

Offer Multiples and Extras

This is really the key to making big money on Fiverr. ‘Multiples’ simply means that a client can buy the same gig from you multiple times (e.g. if you are offering logo design for $5, they could buy five different logo designs for $25).

Extras are additional features you offer on top of your basic gig. For example, someone offering to write a 250-word blog post for $5 might offer a 500 word article for $10, and so on.

As a newbie on the platform you will be quite limited in the multiples and extras you can offer. Currently you can offer just two gig extras ($5, $10 and $20) and five gig multiples

Once you have ten gigs on Fiverr completed with no complaints against you, you will be promoted to what the platform calls Level One. At this point you can add more multiples and extras to your gigs. The most you can charge for extras is $40 at Level One, and $50 at Level Two (for which you require 50 completed gigs).

You can read more about Levels on Fiverr, what is required to achieve them, and the benefits of reaching any particular level on this page of the Fiverr website.

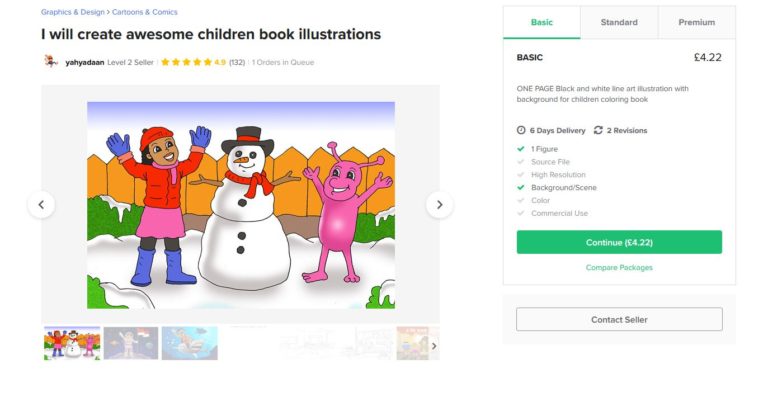

As an example, a Level Two children’s book illustrator by the name of Yahyadaan (see screen capture below) is currently offering to draw a picture in black and white for $5. Paying $15 gets you a colour illustration, and $30 gets you a full colour illustration with ‘high quality detail’ and commercial use allowed. You can also pay an extra $10 for rapid delivery (within a day). The latter is a very common extra, incidentally, and in effect triples your fee for a basic $5 job.

The ability to offer multiples and extras greatly boosts the money-making potential of Fiverr, so it’s well worth putting in a bit of extra effort with your first few gigs to ensure you get good feedback and are quickly promoted to the higher levels.

Ask for a Tip

Buyers on Fiverr generally realise they are getting a good-value service, and many are happy to pay a bit extra to recognize this. This applies especially with US clients, as tipping there is pretty much a way of life!

There is an etiquette to asking for a tip on Fiverr, and you shouldn’t just demand one. The preferred approach is to set up a separate ‘tip gig’. This is just like any other gig, except you don’t have to do anything in return.

Just include a link to your ‘tip gig’ when delivering your gigs and let clients decide whether to pay. If you have given good service, there is every chance they will. As an example, here is a link to a tip gig for a Fiverr member I worked with a few years ago, although I see that her account is on hold (maybe she has moved on to bigger and better things by now).

By using the techniques set out here, you should realistically be able to generate a substantial part-time or even full-time income on Fiverr, while doing something you enjoy from the comfort of home.

Although in this post I have focused on making money from Fiverr, of course it can also be a great way of getting assistance with a wide range of entrepreneurial and personal projects. I have hired other Fiverr members on various occasions for tasks ranging from designing a banner ad to removing malware from this blog after it was hacked. In general I have received excellent service for keen prices. And while on the subject, I highly recommend the WordPress specialist named Zerotech who came to my rescue in the aforementioned hacking attack and got my blog back to normal within 48 hours 🙂

Good luck, and if you have any comments or questions, as always, please do post therm below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting another survey site that offers the opportunity to generate a sideline income.

You may well have heard of YouGov already, as they often run opinion polls on political preferences and other current issues.

YouGov are always on the lookout for new people to join their panel and complete surveys via their website. Naturally, they provide financial incentives for doing this.

How Does It Work?

For each survey you complete on YouGov, you are allotted points. For a typical survey taking 10 to 15 minutes you will get 50 points. Of course, the longer the survey, the more points you will receive.

You can complete surveys on a computer, smartphone or tablet. You will be notified by email of new surveys you are eligible for, though it’s also worth logging on regularly to see the full range of surveys currently available.

Once you have accumulated 5000 points you can redeem them for a £50 fee. YouGov refer to this as a ‘cheque’, but the money is actually paid direct to your bank account.

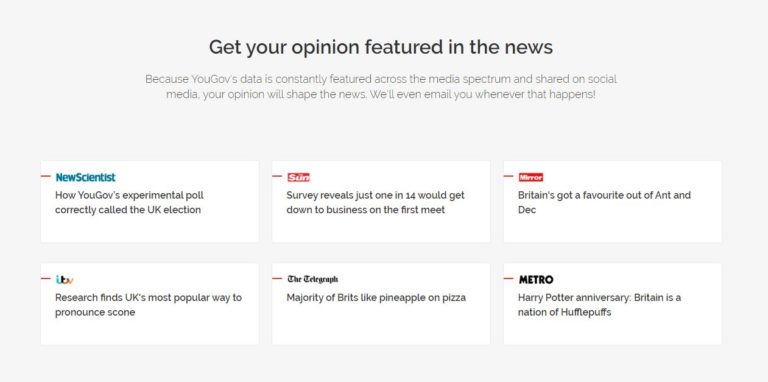

To get 5000 points you would need to complete 100 fifty-point surveys, so this is clearly not a get-rich-quick opportunity. Nonetheless, the surveys are generally interesting and not too demanding to complete. And you will also have the satisfaction of knowing that your responses will ultimately influence decision-makers in government and the private sector. You can see some example media coverage of YouGov surveys in the screen capture from the website below.

How Do You Join?

Joining the YouGov panel is very simple. Just click on this referral link (see below) and complete the short online application form. Acceptance is normally automatic, and you can start earning points immediately.

Disclosure: if you join YouGov via my link I will get 200 points credited to my account (worth £2). If you join YouGov you can also refer other people and earn extra points as well. It all helps get you closer to that next £50 payment!

As always, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

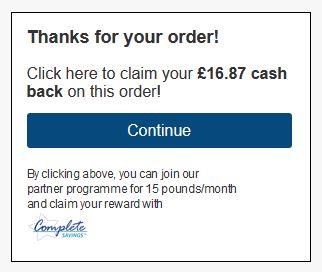

I had a phone call last week from an elderly friend wanting advice. She had just bought some medical supplies on eBay and an ad had come up offering her money back plus a cash bonus. She was keen to know whether this was genuine or not.

Unfortunately I had to tell her that it wasn’t as good an offer as it appeared. This ad – which I have seen many times myself – appears when you have made a purchase at any of a range of online stores, including eBay. Here’s what it looks like…

As you may be able to see from the (tiny) logo at the bottom, this ad comes from a company called Complete Savings. They describe themselves as a cashback site, but as the smaller message below the eye-catching headline reveals, they charge your credit or debit card £15 a month for membership until you cancel.

So Is This a Scam?

I would hesitate to describe Complete Savings as a scam, but the fact remains that – as this Which? article from 2018 confirms – a lot of people are being caught out by it. If you’re in a hurry, it’s easy just to see the eye-catching headline and click straight through to the application form. One lady mentioned in the Which? article didn’t notice she was being charged for five months and ended up £90 out of pocket.

Or you might be like my elderly friend. Her eyesight is poor and she can’t easily read the small print in ads, especially on her mobile phone. She is also relatively new to online shopping (while having to do much more as she is self-isolating). It isn’t hard to see how people such as her could be inadvertently drawn in.

I should make clear that you aren’t automatically signed up just by clicking on the ad. An online application form will appear, and this will hopefully alert you to the fact that you are registering for a subscription-based service. But if you’re in a hurry, or confused, or misunderstand what’s on offer, you could complete the form without realising what exactly you’re signing up for. According to the Which? article mentioned above, they receive a steady stream of complaints from people who have done exactly this.

So Is It Worth Joining?

For your £15 a month, Complete Savings offer discounts from a range of online retailers, including Superdrug, Wickes, B&Q, Hermes, and eBay. Judging from the Complete Savings homepage the standard discount seems to be 10%, although the website says this is the minimum.

To get discounts, you first have to go to the Complete Savings site and click through to the merchant concerned from there. The merchants pay commission to Complete Savings for people buying via their link. All being well, a share of this will be credited to your account as cashback in due course. You can then withdraw this to your bank account once you have earned at least £5.

If you shop online a lot, the cashback could potentially cover the £15 a month fee and be worth your while overall. If you just buy the odd thing online that’s unlikely to be the case, though.

My Thoughts

In my view there are many better ways to get discounts/cashback than Complete Savings (or its sister site Shopper Rewards & Discounts)

As mentioned in this blog post, popular cashback sites such as Quidco and Top Cashback are free to join and offer cashback from a huge range of merchants – in many cases at better rates than Complete Savings. I recommend signing up with all three, and also checking out Cashback Angel, which lets you compare which free cashback platform is offering the best deal for any particular merchant.

Overall, then, my advice is to be very wary of this offer and don’t click on the ads unless you really want to pay £15 a month for a cashback programme when better, free ones are available. And if you know any elderly people or people new to online shopping who may be tempted, warn them it’s not as great a deal as may at first appear. Do them a favour and recommend they sign up with a free cashback site instead!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Right now it’s difficult for savers and investors to know which way to turn. World stock markets have been in free fall, while bank and building society interest rates are at an all-time low.

Regular readers will know that I’m something of a fan of property crowdfunding and have invested through a number of such platforms (notably The House Crowd, Property Partner, Crowdlords and Kuflink). For anyone seeking half-way decent rates of return, I believe they represent an opportunity worth considering at least, especially in the current uncertain economic climate.

But before I come to that, a few words for those new to this field…

Table of Contents

What Is Property Crowdfunding?

As the name says, in property crowdfunding a number of investors pool their money to invest in property and share in the returns pro rata to the size of their investment.

In the last ten years a number of property crowdfunding platforms have been launched to facilitate this. As well as publicizing such opportunities, these companies typically identify suitable properties, advertise and administer projects, and manage properties once they have been purchased. They also distribute payments due to investors from rent received and (eventually) from selling up. Unlike ordinary buy-to-lets, property crowdfunding projects are typically hands-off, passive investments.

There are various methods of property crowdfunding. The traditional method (if you can describe something that’s been around for under ten years as traditional) is equity crowdfunding. Here investors’ money is pooled to buy a house or larger property. Investors then (usually) receive rental income in proportion to the amount they invested plus a share of any capital gains when the property is sold.

The other main method is debt crowdfunding. Here investors lend money to a landlord or property developer so that they can complete a particular project. The money might be used for a bridging loan, or to make improvements to a property prior to selling or remortgaging it. In this type of crowdfunding, the investors never actually own the property. They play a role similar to a bank, lending money and (all being well) being repaid with interest once the project is concluded.

There are also development projects, where investors’ money is used to fund larger-scale property developments. This might involve building a new property (or properties) from scratch, or perhaps converting existing buildings to a new use. Either way, if all goes well, at the conclusion of the development the investors get their capital back along with interest. Development crowdfunding is riskier than equity crowdfunding, but the profits to be made can be bigger.

Property crowdfunding is a form of investment, and like all investments it carries risks. Clearly it’s not as safe as bank or building society savings (which are covered up to £85,000 by the Financial Services Compensation Scheme). All investments are though secured against bricks and mortar, so in the event of a borrower defaulting you should still get your money (or most of it) back once the property concerned has been sold.

The rates of return with property crowdfunding are significantly higher than those from banks and building societies, and they’re also relatively unaffected by fluctuations in the stock market. Property crowdfunding isn’t a way of hedging equity-based investments directly, but it does help spread the risk.

Property and the Coronavirus

These are undoubtedly challenging times for property investors, be they traditional buy-to-let landlords or property crowdfunders.

Even before the virus struck, property prices were at best steady or going down. And measures taken by the government in the last few years, including progressive cuts in mortgage interest tax relief and an additional 3% stamp duty on buy-to-let properties (dubbed ‘The Landlord Tax’) considerably reduced the attraction of buy-to-let for private landlords especially.

The coronavirus crisis has added a whole new layer of difficulty. In particular, measures taken by the government to mitigate the worst effects of the crisis have hit both tenants and property owners hard. Many tenants are obviously suffering financial hardship, and may therefore be having difficulty paying their rent (and other bills). Tenants are, though, currently protected from eviction, and landlords are required to provide rent holidays where appropriate. These measures are sensible and humane, but at a stroke they have reduced or cut entirely many landlords’ income streams, and there is no government scheme to assist them. Obviously I don’t expect many tears to be shed for landlords, but life has undoubtedly become a lot more challenging for them.

In addition, due to social distancing and the lockdown, only limited construction work is continuing. It’s also difficult (or impossible) for surveyors and valuers to do their jobs, or for potential buyers to visit and inspect homes and other properties. All of this means that to a great extent the UK property market has currently ground to a halt.

Despite that, it’s not all bad news. At some point – maybe quite soon – the lockdown restrictions will be eased. The government is (rightly) keen to get the economy moving again as soon as possible. And there are still plenty of people looking to move home, buy property, begin new development projects, and so on. Much as the depressed state of the stock market has presented opportunities for those willing to take a chance on buying now while prices are low, there is certainly a case that property will bounce back in the coming months and years too, rewarding those who invest in the sector now.

Property Crowdfunding Opportunities

Clearly property crowdfunding investors are not immune to the effects of the coronavirus crisis. Developments and sales have been delayed, and in some cases at least rental income has been reduced. It’s quite possible – likely even – that in the longer term the rate of defaults on loans will go up too.

Nonetheless, property crowdfunding investors are unlikely to be as badly affected as private landlords. For one thing, if they are sensibly diversified across a range of properties (and platforms) they won’t be as susceptible as someone with a single buy-to-let. And like all property investors, their money is secured by bricks and mortar, so they will get it back (or most of it) eventually – though in the current crisis, that might take some time. For most property crowdfunding investors at the moment, sitting tight is likely to be the best (or only) option.

As I said above, the crisis is also creating opportunities for those who believe that property will prove to be the resilient investment it has generally been in the past. Rather than prolong this post too much, I will focus my attentions on the four platforms I am currently invested in, and which I am therefore most familiar with.

Property Partner

Property Partner is an interesting case. They have just announced that they are suspending all dividend payments for the next three months (potentially longer). This is, of course, mainly money from rent received, which (for reasons stated above) is likely to take a hit in the coming months. Property Partner say they are taking this action to ensure that investors are protected in the longer term and all properties have sufficient cash reserves to cover any necessary expenditure.

As I said in this post a few months ago, many of the properties on Property Partner are coming up to their five-year anniversaries. This is a significant milestone, because after a property has been owned for five years, all investors have the chance to exit at a fair market price (determined by an independent surveyor). Property Partner have said they are suspending this process until June at the earliest.

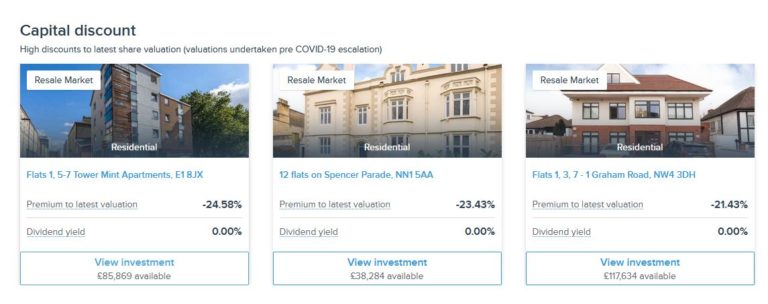

You can still buy and sell properties on Property Partner’s secondary market, and on the face of it there are some good-value buying opportunities here, with properties listed at up to 25% off their current valuations (see screen capture below).

In theory, you could buy shares in these properties on the secondary market at a big discount, and sell them at their current valuation for a good profit when the five-year sale process is reinstated.

Unfortunately it’s not quite a straightforward as that, though. For one thing, the current valuations were made before the coronavirus crisis hit, so they may no longer be an accurate reflection of a property’s value. In addition, the five-year exit mechanism depends on other investors wanting to buy the shares at the valuation stated. Failing that, the property will be sold on the open market, but that could take a long time in the current economic climate. Neither is there any guarantee what price would be achieved.

My personal view is that I do believe property prices will bounce back but it may not be for quite a while. I am looking seriously at some of the buying opportunities on Property Partner’s secondary market where I think they represent good value in the medium- to long-term, but I am not rushing to invest at the moment.

Kuflink is another property crowdfunding platform I have a soft spot for. Although I don’t have huge amounts invested with them, so far all of my investments have paid out as promised, with just a short (one-month) delay in one case.

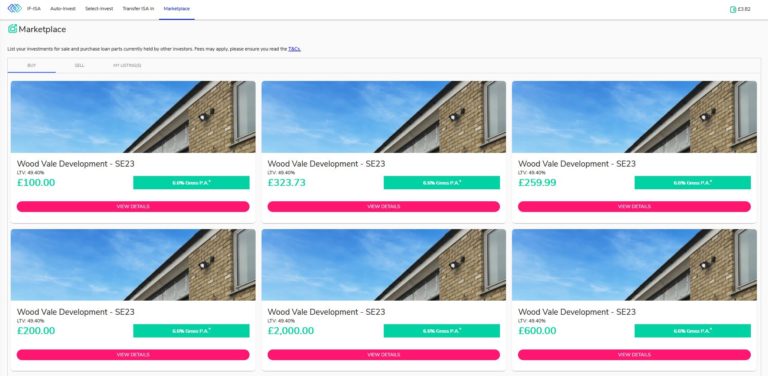

Kuflink is a property loans platform. So far anyway I have not heard of any defaults, although the longer the crisis continues, the greater the risk this may happen. Nonetheless, based on my experiences to date, I am continuing to invest (cautiously) with them. In particular, I like their new secondary market, where you can buy loan parts from other investors who want to sell up early (see screen capture below)

As you may imagine, this has been happening a lot recently, as many investors have wanted (or needed) to access their capital urgently. This has created short-term buying opportunities which I have been busily taking advantage of. These loan parts typically have only a few months to run, so you can expect to get your capital back quite quickly (and can then reinvest it). Only loans in good standing with monthly repayments up to date may be listed on the secondary market, so that offers some reassurance against default – though of course it is by no means a guarantee.

Secondary market aside, Kuflink also still has a steady stream of new investment opportunities coming to the table. Of all the property platforms, they appear to be the ones least affected by the current crisis. I am not exactly sure how they have achieved this, but obviously I hope they continue to do so!

If you haven’t invested in Kuflink before, it’s also worth mentioning that they have a generous welcome offer which is still operating. You can earn up to £4,000 in cashback with this. See my Kuflink review for full details.

The House Crowd

The House Crowd is actually the first property crowdfunding platform I invested with. My experience with them has generally been good, although as mentioned in my House Crowd review there have been some delays and defaults.

Although they started as a traditional crowdfunding platform, The House Crowd have increasingly moved towards development projects, and these have inevitably been hit by the current crisis. THC say that at present they are following a strategy of ‘prudently maintaining The HouseCrowd platform to ensure its continued and efficient operation as we see our way out of the other side of the lock down.’

That means there are fewer investment opportunities on THC at the moment. You can though if you wish still invest in their automatically diversified ‘Auto-Invest’ products, with target interest rates of 5% (Cautious) to 7% (Bold), or the new THC Fusion account, which offers even greater diversification with a target interest rate of 4% to 4.5%. More information about these can be read on the House Crowd website.

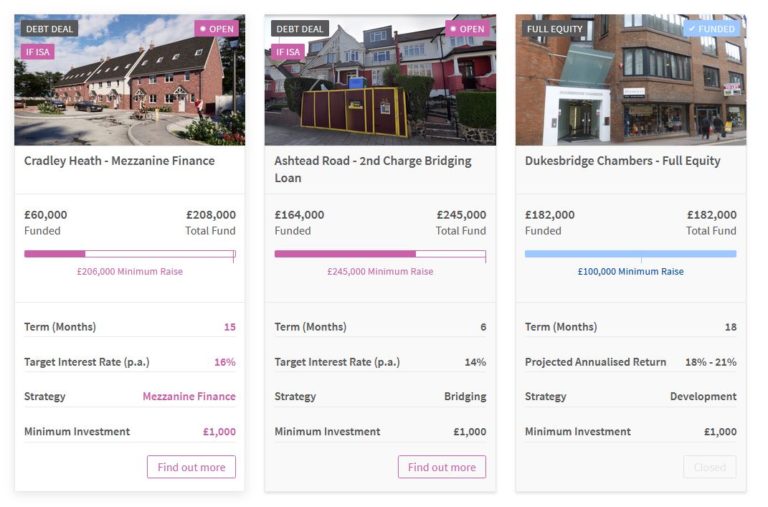

At the time of writing THC also have a couple of development projects open for investment, including their flagship project The Downs in Altrincham town centre, paying a target rate of 10% per year (see screen capture below).

Finally, Crowdlords say they have experienced a significant reduction in investment levels since February, which they put down to uncertainty caused by the pandemic. They do still have a couple of lending opportunities listed (see capture below), but not much else. I guess like The House Crowd they are hunkering down and waiting for the current restrictions to be lifted and the property market to start moving again.

Again, I am not currently planning to invest any more in Crowdlords, but am keeping an eye on any opportunities that may crop up in the months ahead. You can read my full review of Crowdlords here.

Final Thoughts

I thought I’d close by sharing a couple of nuggets of information I found while researching this post.

First, the ratings agency Fitch has downgraded the rating of UK debt to AA-. However, Fitch estimated growth next year would bounce back to 3 percent if the UK can begin to unwind the measures to tackle the health crisis in the second half of the year. The UK’s Coronavirus Job Retention scheme – a three-month programme to support employees hit by the pandemic – will cost about 1.3 per cent of GDP, according to Fitch estimates.

Second, estate agents Knight Frank have predicted that many house sales will be lost this year and the UK’s property market will see little to no growth in 2020. However, a sharp recovery has been predicted for 2021. Liam Bailey, global head of research at Knight Frank, said, “We expect a revival in activity to continue, with volumes next year expected to be 18 per cent above the level seen in 2019.”

All of this (and other sources) suggests that while property markets are in the doldrums now and probably for most of 2020, there is every chance that by next year we will see a recovery. There are undoubtedly good opportunities on offer in property investment now if you agree with this evaluation and are able to be patient in the shorter term.

In any event, if you’re looking for better returns than the banks and lower volatility than the stock markets, then property generally – and property crowdfunding in particular – remains in my view well worth considering as part of a balanced investment portfolio.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I am not a regulated financial adviser and nothing in this post should be construed as individual financial advice. You should always do your own ‘due diligence’ before investing, and seek independent financial advice if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

With Britain in near-lockdown at the moment, and many jobs and businesses under threat, big energy bills are the last thing any of us want to worry about right now.

So Dorset-based energy supplier Utility Point has come up with an innovative solution. Their new UP Support tariff credits customers with half (yes, half!) of the cost of their gas and electricity bills for their first three months on the tariff.

It’s a fixed tariff, so customers have the added reassurance of knowing that prices won’t increase through till next winter and beyond.

The UP Support tariff is open to everyone, though it may appeal especially to those who are seeing their income reduce but energy usage increase while self-isolating or working from home. It’s available now to both new and existing Utility Point customers. You can sign up on the Utility Point website, where further information is also available.

About Utility Point

Based in Poole, Dorset, Utility Point is one of the UK’s fastest growing domestic energy suppliers. Founded in 2018, the company has already grown to over 100 employees, and more than 245,000 customers.

They say their mission is to increase energy efficiency, provide a dedicated, personalized service and work together with customers to save money. These values have brought the company not only commercial success but also widespread public recognition. In March 2020, Utility Point was named in the prestigious Sunday Times Top 100 Small Companies to Work For list, the Top 75 Companies to Work For in the South West list, and awarded the highest available three-star Best Companies rating. The company is co-owned by Ben Bolt and Simon Yarwood.

My Thoughts

Right now money is a major worry for many people. And the next two or three months will be critical, with the lockdown (presumably) continuing and many people waiting for furlough payments and government aid to come through. So halving your energy bills for three months should help considerably, along with the added reassurance of knowing that your tariff won’t rise for at least a year.

In addition, though, it’s clearly important that the tariff itself is competitive once the three-month initial period is over. Utility Point say that their average price for a non-Economy-Seven dual-fuel customer is £76.60 per month, based on a typical medium user (3100 kWhs electricity and 12000 kWhs gas). That looks pretty competitive to me. But of course you can request a free quote on the Utility Point website and compare this with your current supplier, and I would strongly recommend doing this.

I also like the fact that Utility Point has a strong customer-service ethos, and that despite only launching in 2018 it has already earned a reputation as an excellent company to work for.

Finally, it’s worth mentioning that all Utility Point customers automatically get access to a free benefits programme called Utility Point Rewards. The programme includes a range of special offers, including significant discounts (up to 20%) at a host of high street stores, restaurants and websites. These include such big names as Sainsbury’s, Boots, Asda, Wilko, Halfords, Samsung, and more. The savings you can make from this over a year could be substantial, in addition to the money you will be saving on your energy bills.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Utility Point.

If you enjoyed this post, please link to it on your own blog or social media:

I thought today I’d share a more personal post about how the coronavirus, and the measures to prevent it spreading, have affected me personally.

First of all – as many of you will know – I live on my own since my partner, Jayne, passed away a few years ago. I am fortunate to live in a fairly large house with a good-sized garden, so being mostly confined to barracks hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am used to working from home, having done this for the last 30 years or so.

Of course, that doesn’t mean the coronavirus crisis hasn’t affected me in a variety of ways. As Pounds and Sense is a money blog, I thought I should start off with that…

Financial

One hard thing for me (and many other people, of course) has been seeing my equity-based investments – and in particular my pension fund – tumble in value. I’m 64 and semi-retired and my SIPP is in drawdown, so I have been particularly concerned about this. But I have tried to follow my own advice and avoid panicking. In the longer term I am sure that the markets will recover, even if this could take years rather than months.

In general my P2P/crowdfunding investments have been holding up better, with my Bricklane property ISA up substantially over the last few months. Admittedly I am hearing stories about some P2P platforms such as RateSetter struggling to process the large volume of withdrawal requests at the moment, but again I am sitting tight for now, so this isn’t affecting me directly. I have reinvested some of my returns from maturing investments on Kuflink on their new secondary market (see screen capture below), so will be interested to see how this works out.

I did decide to invest £7,000 – the proceeds of another maturing investment – in another vehicle for Buy2LetCars. As regular readers will know, I’ve had one (new) car with this car loan investment platform for about two years now, and the monthly repayments have been coming through like clockwork. So I decided to invest my £7,000 (the minimum investment with Buy2LetCars) in another car – a pre-owned one this time, of course.

I particularly liked the idea of investing again with Buy2LetCars, as they lease vehicles to key workers such as nurses and other NHS staff (along with teachers, prison officers, police, and so on). These people all need cars for their (essential) work. They are responsible individuals, and have every incentive to look after the vehicles (though as they are fully insured, investors don’t bear any risk from accidents themselves).

Unfortunately Buy2LetCars don’t tell you who has leased ‘your’ car, but I like to think the ones I have bought are providing transport and security for two hard-working NHS nurses at this moment 🙂

The only other investment I have made recently is a modest top-up to my Nutmeg Stocks and Shares ISA. This is obviously a bit of a gamble, but with equities having fallen so much in such a short time, I hope to take advantage when the markets start to rise again. Of course, there is no guarantee that the markets won’t fall further in the short term, but based on my experiences to date I am confident that the Nutmeg team will do their utmost to protect my investment and soon enough start it growing again.

I am also waiting to hear if I will be eligible for the government scheme to support self-employed workers. I think I should be, as I appear to meet all the criteria. Indeed, as they are basing payments on profits earned in the tax years 2016/17, 2017/18 and 2018/19, this should actually work in my favour. I earned quite a lot more in 2016/17 and 2017/18 than I am earning now, as I glide serenely into retirement (lol). I won’t turn down any money I am offered as it will provide welcome added financial security. But I appreciate that my needs are probably not as acute as many self-employed people right now.

Personal

On a personal level, the crisis has also affected me in a range of ways. Some of these are predictable, others less so.

Thankfully I have managed to avoid contracting the virus so far (as far as I know). I do, however, have good friends who (probably) have it. Fortunately they haven’t had to go into hospital, though. I am following all the guidelines about social distancing and self-isolating and really hoping to avoid catching it myself (at least until better treatments and hopefully a vaccine are available).

Like most people I have had to contend with the results of panic buying, which have left the supermarket shelves bare of certain items. Here’s a photo of the toilet roll shelves in my local Morrisons a couple of weeks ago when panic buying was at its peak…

On another occasion when I went to Waitrose the only fresh vegetables left in the shop were baby courgettes (I bought a pack – they were very nice in a stir fry).

On my recent shopping trips the situation seems to be getting better. I have been able to buy most things I needed, including eggs, which had disappeared for a while. There is still no flour or pasta, but as it happened I have enough in stock to keep me going for a while yet.

I am taking a daily walk (as mandated by the government) for exercise. In fact there is nothing new about this for me, as working from home I have always tried to fit a walk into my daily schedule. But suddenly I am seeing a lot more people (and families) out and about on the roads and back lanes. People seem a little friendlier generally, more willing to say ‘good morning’ or some such greeting as they pass. I am also becoming accustomed to zigzagging from one side of the road to the other to avoid breaching social distancing rules!

I do miss being able to go for a swim. I used to go twice a week if possible to my local David Lloyd Leisure club, but that is now closed for the foreseeable future. Daily walks are good, but not really a substitute for this. I am not a natural exerciser, but am making an effort to be a bit more active in other ways at home. Having a large garden which needs a lot of attention at this time of year helps!

One online resource I have been finding very helpful is the local community website NextDoor (which I wrote about in this blog post). When last week I was despairing about ever seeing eggs again, I posted there asking if anyone knew where they might be obtained. Within a couple of hours I had over a dozen replies, including suggestions of several local shops I hadn’t even realised were still open.

A side benefit is that I am discovering shops and businesses around my area I wasn’t previously aware of, even though I have lived here for over twenty years. That includes several farm shops, including one that is barely a mile away. Also via NextDoor I learned that my town (Burntwood) is host to a fruit wine making company, and they even deliver free to local residents. I plan to order from them once I have decided whether to get damson or gooseberry 🙂

I am making good use of technology to keep in touch with friends and family (even though it’s obviously not the same as meeting face to face). My Skype skills have improved, and I even took part in an online pub quiz via Skype last week (though I’m told by younger friends that Skype is ‘old hat’ and I need to get on Zoom now!). I have also watched a couple of concerts livestreamed from the living rooms of the musicians concerned.

I was going to sign up for the NHS Volunteer Responders programme, but was a bit slow off the mark. By the time I got around to it, they had closed to new applications. If they reopen I will certainly apply though. In the meantime I am shopping for an elderly couple – old friends of mine – who are self-isolating and have been unable to get online shopping slots with any supermarket despite being officially ‘vulnerable’..

If there is one good thing that has come out of this, it is that in general people are looking out for one another a bit more. I was on the receiving end of this myself recently. The doorbell rang and when I opened it I saw a young man whose face seemed vaguely familiar. I was rather embarrassed when he explained he was my neighbour from over the road, come to check if I needed any help. It’s definitely not like Ramsay Street around here! But it’s good to know people are thinking of others at this time. And if I see that neighbour again in future, hopefully I will remember who he is now!

So that has been my experience of the coronavirus crisis to date. Not great, but I am dealing with it and trying not to get too stressed out. I do of course appreciate that I am in a fortunate position compared with many other people. I hope you and your family are coping in these strange and worrying times as well. I’d love to hear your thoughts and experiences. If you have any comments or questions, as always, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Around two years ago I invested some money in the Ratesetter P2P lending platform, partly – I admit – to take advantage of their welcome offer (the current welcome offer is discussed below). So today I thought I would share my thoughts about it.

Ratesetter is a P2P platform that puts would-be lenders and borrowers together, obviously taking fees for doing so. It is one of the longest-running P2P lending platforms, having launched in 2010. They are one of the ‘Big Three’ P2P lending platforms, which also include Zopa and Funding Circle.

In this post I am looking at Ratesetter from a lender’s (or investor’s) point of view, but of course anyone can apply to borrow via Ratesetter too.

Table of Contents

Types of Investment

Although investors lend money to borrowers via RateSetter, the actual lending is done behind the scenes. So from an investor’s point of view, RateSetter looks and works much like a bank or building society. Importantly, though, investors with RateSetter don’t benefit from the protection bank and building society savers receive by law in the UK via the Financial Services Compensation Scheme. More about this shortly.

There are three main investment products available on RateSetter. They are named Access, Plus and Max.

The Access product, as the name indicates, aims to offer quick access to your funds without any fee. The Plus and Max products pay more interest but you have to pay a ‘release fee’ of 30 or 90 days’ interest respectively if you wish to withdraw from them.

The terms and conditions for each account are summed up in the screen capture below.

Note that the interest rates on Ratesetter can vary, and the rates on offer when you read this may be different from those shown above.

The Access product is the closest equivalent to an ordinary savings account. You can ask to withdraw some or all of your money at any time without penalty. It’s important, however, to note that this is NOT the same as an instant saver account with a bank or building society. Withdrawing does depend on there being other investors willing to take over your lending on the platform. Ratesetter say that to date investors have received their withdrawn investments within 24 hours on average, which does offer some reassurance.

There is also a ‘fair usage’ clause, which prevents investors from lending new money for 14 days after a withdrawal.

With the Plus and Max products you can also request withdrawals at any time. As stated above, however, in these cases a release fee is applied.

Provision Fund

As with all P2P lending, your money does not enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme.

Ratesetter does, however, have a provision fund which provides a safety net in the event of a borrower defaulting. In the ten years since it was launched no investor has lost money from defaults on RateSetter, which is pretty impressive (although obviously it doesn’t guarantee it couldn’t happen in future). The provision fund is paid for by a ‘credit rate fee’ which is paid by all new borrowers.

It’s worth mentioning also that provision fund protection extends equally across all loans. There is therefore no particular need to diversify your investments on Ratesetter, although you should of course diversify across other platforms and investment types.

The IFISA Option

You can also invest in Ratesetter through an IFISA (Innovative Finance ISA). This type of ISA for P2P lending gives you the same tax advantages as a cash or stocks and shares ISA, i.e. you don’t have to pay any tax on the profits you make.

Everyone has a generous annual ISA allowance of £20,000 (in the current 2019/20 tax year). This can be divided any way you like among the three types of ISA. So if you open a Ratesetter IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. You can also only invest money in one of each type of ISA in any one financial year.

If you have maxed out your ISA allowance – or have invested in another IFISA in the current tax year – you still have the option of opening an Everyday Account. You can invest any amount in this, but of course the profits you make will be taxable.

2020 Interest Rate Cut

Due to the coronavirus crisis and the current febrile economic environment, RateSetter announced on 4th May 2020 that there would be a temporary reduction in interest rates for the remainder of 2020. During this time, investors will receive only 50% of their interest, with the other 50% going to the Provision Fund, for the protection of all investors. At current rates. that means the actual interest rates paid during this time will be 1.5% for Access accounts, 1.75% for Plus accounts, and 2% for Max accounts.

I have also heard (and confirmed with Ratesetter) that currently repayment requests are taking three to six months to process. If that changes I will update the information here.

Ratesetter Pros and Cons

Based on my experiences so far – and the results of some online research – here is my list of pros and cons for the Ratesetter P2P lending platform.

Pros

1. Fast, easy sign-up.

2. Low (£10) minimum investment.

3. Choice of investment terms

4. Quick and simple investment process.

5. Tax-free IFISA option available.

6. Provision fund protects lenders against loss (no investor losses at all to date).

7. Ability to access your money at any time (though with a fee when exiting the Plus and Max products)..

8. Customer service (in my experience anyway) is fast and helpful.

9. NEW! A free £100 added to your account for new users who invest £1,000 and keep this invested for a year (see below).

Cons

1. Rates paid aren’t the highest in P2P lending.

2. Website isn’t always as intuitive to use as it should be.

3. Withdrawals are taking longer than usual to process due to increased demand following the coronavirus outbreak.

4. Temporary interest rate reduction by half to help boost the Provision Fund (see above)

Conclusion

Overall, my experiences with Ratesetter so far have been good. My initial deposit was matched within 24 hours and has been generating the promised returns ever since. I reinvested my bonus payment into the platform and this is earning interest as well.

As mentioned earlier, P2P lending does not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates on offer at Ratesetter are significantly better than those from most banks and building societies. And the existence of a substantial provision fund with a strong record of protecting investors from losses clearly offers reassurance. Based on its past record and the protections in place, Ratesetter appears to be one of the safer P2P lending platforms.

It’s also reassuring that you can access your money any time – this can be an issue with property crowdfunding platforms in particular, as liquidity in these platforms can be limited. With the Plus and Max products you will be charged for exiting early, though, so invest in these only if you are pretty confident you won’t be needing the money within the next few months.

On the negative side, the current three to six month delay in withdrawals, and the halving of the rate paid to investors, is clearly disappointing. I understand that RateSetter are doing this to protect the business in the longer term, but it obviously it reduces the attraction of investing with them currently (though see Welcome Offer, below)

Clearly, no-one should put all their spare cash into Ratesetter (or any other P2P lending platform). Nonetheless, it is worth considering as part of a diversified portfolio. Not only are the rates of return higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P lending isn’t a way of hedging your equity-based investments directly, but it does help spread the risk.

Welcome Offer

Currently if you are new to RateSetter you can get £100 added to your account for free just by signing up and depositing £1,000. Full terms of the offer are reproduced below, and you can also find them on the RateSetter website.

You can take advantage of this offer so long as you

have not previously registered with RateSetter

deposit a minimum of £1,000 through the RateSetter ISA or Everyday account and this is matched within 56 calendar days of opening an account

keep a minimum of £1,000 invested for 1 year

Your bonus will be credited to your Everyday Account and invested in Ratesetter’s Access product within 30 working days of qualifying. You can ask to withdraw your money at any time, but you must keep a minimum of £1,000 invested for 1 year to qualify for your £100 bonus.

My Thoughts: This is a great offer from RateSetter if you are new to the platform. If you invest £1,000 and keep it there for a year, then including the £100 welcome bonus you will get a total return of at least 12 percent for the first year, even allowing for the temporary 50% rate cut. As a matter of interest, this is the same welcome offer I took advantage of when I signed up with RateSetter two years ago, and my bonus £100 was credited without any issues (or prompting from me) twelve months later.

Clearly, this is a generous promotional offer by RateSetter and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

As always, if you have any questions or comments about this post, please do leave them below.

Note: This is a fully revised and updated relist of my original (2018) RateSetter review.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive.

If you enjoyed this post, please link to it on your own blog or social media:

…that’s the question I was asked recently by a Pounds and Sense reader after I mentioned in this blog post that I had a financial adviser.

Of course I replied to her directly at the time, but on reflection I thought it would be good to provide a more in-depth answer to this question on the blog.

To recap, my financial adviser is called Mike and he works for a company called Integrity Wealth Solutions. I was recommended to Mike by my accountant, and he has been advising me for over three years now.

Mike actually looks after about half of my portfolio. He advised me about this initially and set up the recommended investments on my behalf, making maximum use of my tax-free allowances. He continues to monitor my investments and makes any recommendations for adjustments as required. I see Mike once a year in person to review how things are going (both with the investments and me personally). But of course, I can also speak to him by phone (or email) any time if required.

The other half of my portfolio I look after myself, and it is fair to say it is well diversified! As regular readers of PAS will know, I have investments in property crowdfunding, P2P lending, the robo advisory platform Nutmeg, and various others.

Why then do I need Mike? Here are just some of the reasons…

1. Mike is a trained and experienced independent financial adviser/planner who works full-time in this field. I am a money blogger and obviously have a special interest in financial matters, but I have no professional training or direct work experience in this field. I can ask Mike for his professional opinion on any investment-related matters, and while I am not obliged to follow his advice I do of course take it very seriously.

2. Mike has a backup team in his office and access to specialist investment research services and software. He uses these resources to inform his advice, and also to provide in-depth reports (with snazzy-looking charts and spreadsheets!) regarding how my investments are performing.

3. As a regulated financial adviser, Mike has to follow all the correct protocols and ensure that all advice he gives follows best professional practice and is appropriate for my needs and circumstances. He cannot cut corners, invest on a whim or hunch, or let himself be distracted by the latest ‘bright shiny object’ in the investment world. I have to admit that I have been guilty of all of these things myself in the past!

4. As a professional financial adviser Mike also has access to certain investment opportunities or platforms that are not easily accessible to the general public. I won’t go into detail about this here, but it is certainly something I have had occasion to be grateful for in the current coronavirus outbreak.

5. Mike is able to provide personalized but objective advice about my finances, based on information I give him. Money and investment can be emotive subjects, and it’s great to have a sympathetic – but at the same time sensible and detached – professional advising you. I am sure Mike sometimes sighs inwardly at some of my more exotic investments, but he is always interested in what I have been doing with ‘my’ half of my portfolio and happy to offer his thoughts as appropriate.

Are there any drawbacks to having an adviser? Well, of course, you have to pay them! In the case of Mike I paid an up-front fee initially and now pay a small monthly commission. Hand on heart I can say that Mike is well worth his fee, and even in the current exceptional circumstances his charges have been more than covered by the amount by which my investments have grown.

So that is why I have a personal financial adviser. If you are fortunate enough to have money to invest, I strongly recommend you consider engaging one too.

If you would like to find out more about the service offered by Mike and his colleagues at Integrity Wealth Solutions, you can check out their website and contact them on 02476 388 911, or email them at advice@integritywealth.co.uk. They are friendly and not at all pushy, and will be delighted to talk you through the service they offer without obligation. If you do get in touch, please mention that you were recommended by Nick Daws of Pounds and Sense blog. If you end up becoming a client they have said that they will pay me a small fee to say thanks. This will help to cover my costs and ensure I am able to go on sharing tips and advice to Pounds and Sense readers.

As always, if you have any comments or questions about this post, just let me know.

If you enjoyed this post, please link to it on your own blog or social media:

The ability to offer multiples and extras greatly boosts the money-making potential of Fiverr, so it’s well worth putting in a bit of extra effort with your first few gigs to ensure you get good feedback and are quickly promoted to the higher levels.

The ability to offer multiples and extras greatly boosts the money-making potential of Fiverr, so it’s well worth putting in a bit of extra effort with your first few gigs to ensure you get good feedback and are quickly promoted to the higher levels.