I’m a bit off-topic today, I know. But these are – to put it mildly – exceptional times, and we all have to respond as best we can.

I know many people are having to self-isolate right now, or at least spend a lot more time at home. So I thought I would make a small contribution towards making life more bearable by offering both of my Kindle ebooks free of charge.

My ebook The Festival on Lyris Five is a tongue-in-cheek science fiction novella featuring illustrations by the talented Louise Tolentino. You can download it free (until Thursday 26 March) by clicking here or on the ad below. I hope you enjoy reading it. If you do, a review would be appreciated (though certainly not a requirement!).

My other ebook is called Three Great Techniques for Plotting Your Novel or Screenplay. As you’ll gather, this is aimed at writers and aspiring writers. If you are in that group, I hope you will find the tips and advice it contains helpful. Again, here is a link or you can click on the display ad below.

As you may know, you don’t need a Kindle device to read Kindle e-books. You can also read them on your mobile phone, tablet or PC using the free Kindle app available via Amazon at https://www.amazon.co.uk/kindle-dbs/fd/kcp

And since one of these titles is aimed at writers, I thought I would also include a plug here for Best Writing Forum, which I helped set up a couple of years ago. BWF is free to join and has members all over the world. If you are looking for support or feedback with your writing, you will find it here. Equally, if you are just seeking online companionship from fellow writers during these most stressful of times, you can find that here as well.

As ever, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a pension advisory service called AdviceBridge that may be of interest to any Pounds and Sense readers who are planning for their retirement.

There is no doubt that in recent years retirement planning has become more challenging. The pension reforms introduced by George Osborne in 2015 gave people much more freedom over how and when they can access their retirement savings. There are many benefits to those reforms – and I’m a fan of them myself – but it does mean most people now have big decisions to make over how to finance their retirement.

A further factor is the decline of ‘defined benefit’ pensions. These guaranteed a certain pension usually based on how long you had worked for an employer and how much you earned during your career. The great majority of working age people nowadays have ‘defined contribution’ pensions, where you build up a pension pot over the course of your working life. This then provides you with an income (alongside the state pension and any other investments) when you retire. Anyone with a pension of this type will have important choices to make over how, when and where to save for their pension, and what to do with it once they reach retirement age. Many people who are not financial services professionals understandably struggle with this and need some expert help (I did myself).

Getting professional financial advice can be expensive – typically pension advisers in the UK charge £2,000-£3,000 up front and then 0.5% a year. But a new service called AdviceBridge promises a personalized, affordable retirement planning service. Indeed, they say they can do this for as little as a tenth of the average adviser fee, partly by running the service online and over the phone (no face-to-face meetings required).

Although it is a low-cost service, AdviceBridge is staffed by fully trained and regulated financial advisers, and the company is authorized and regulated by the Financial Conduct Authority (FCA). AdviceBridge never holds investors’ money, even when they assist in the implementation of a retirement plan. The advice they give is though covered by the Financial Services Compensation Scheme (FSCS), which means clients can claim compensation of up to £85,000 if they receive bad advice.

Table of Contents

Who Is AdviceBridge For?

In order to keep their charges low, AdviceBridge say that at the moment they are only able to help clients who meet the following criteria:

You are resident and domiciled in the UK.

You are generally in good health.

You do not have any unsecured loans.

You are not currently contributing to pensions with safeguarded benefits such as a final salary pension.

You do not own any buy-to-let property or any non-standard investments.

You do not receive any means-tested benefits.

You would like to plan individually, not as a couple.

How Does It Work?

Assuming you meet the criteria above, you start by filling in an online questionnaire and completing some electronically-signed compliance documents.

As well as the usual contact information, the questionnaire covers such matters as:

your age

your employment status

your annual income

any existing private or company pensions

whether you will qualify for a full state pension

other savings and investments

your target retirement age

how much income you hope to have in retirement

any major outgoings in future you need to plan for

and so on

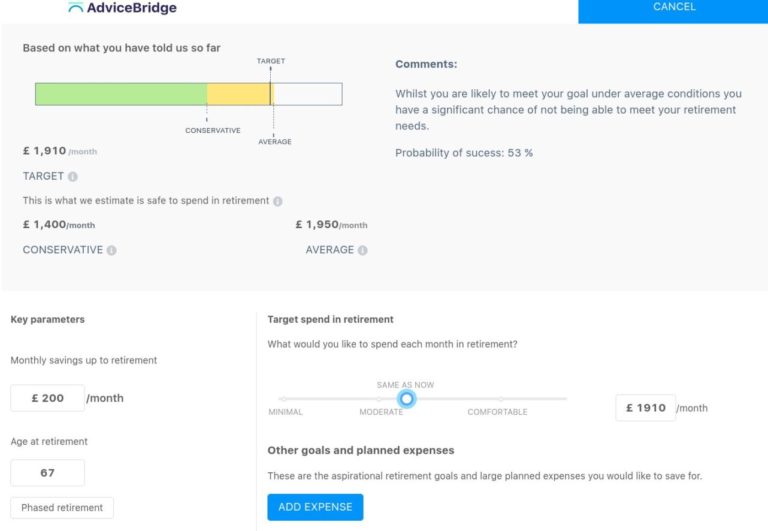

Once you have entered this information, you can create and log in to your account to see an overview of your financial situation. You can adjust the parameters in order to achieve a realistic and sustainable level of retirement income. Here is a screen capture showing part of this (an example account, not mine personally!).

Personalized Plan

Naturally, the above is just the first stage of the process. Once you have provided this information and set up your account, the AdviceBridge advisers will crunch the numbers and (with the aid of their specialist software) produce a personalized plan for you.

This is obviously a key document. The sample plan I saw came to 39 pages in PDF form. It was divided into three sections: About You, Our Recommendations and Advice, and Appendices.

About You sums up the information you have provided to AdviceBridge via the questionnaire. It covers your personal circumstances, your retirement savings and investments, and your progress so far towards achieving your retirement goals.

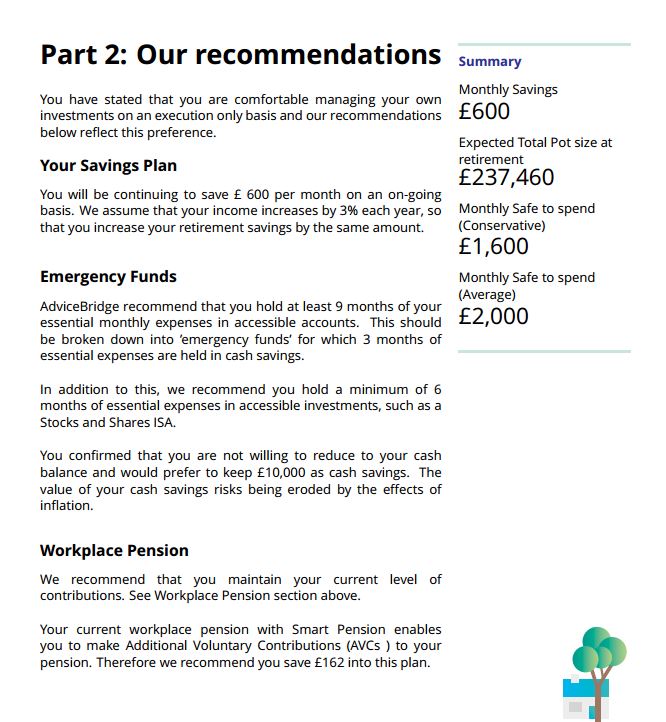

Our Recommendations and Advice is the longest section of the plan. It presents recommendations on every aspect of managing your finances for retirement, including restructuring your investment portfolio if required (with specific recommendations for low-cost personal pensions and ISAs). It also examines the likely outcome of following the recommendations, including both average and conservative projections. A sample page from this section of the plan is shown below.

Finally, the Appendices section includes a range of supplementary information, including more detail about the UK state pension, rules about annual pension allowances and taxation, your options for accessing your pension (drawdown, annuities, etc), and more.

It doesn’t end there, though. Once you have had a chance to read and digest your plan, you can arrange a call with a personal financial adviser from AdviceBridge to talk through the advice and recommendations and help you decide how to proceed. The advisers are not paid commission on product sales, so they are able to give unbiased advice about what investments may be best for you based on your specific circumstances.

So What Does It Cost?

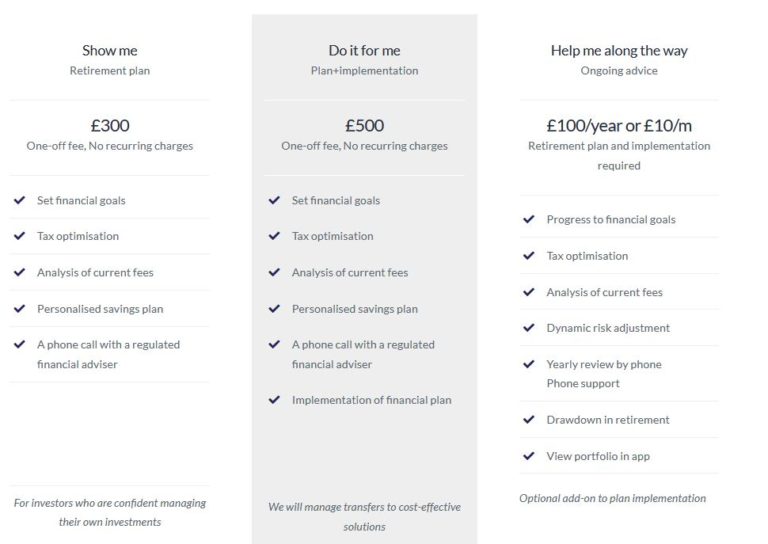

For the basic AdviceBridge service as described above, there is a one-off fee of £300 with no recurring charges. This service will suit people who are happy to arrange their own investments based on the advice given and the telephone call with an adviser.

If you want AdviceBridge to set up the recommended investments for you – to implement your financial plan, in other words – they will do this as well for an inclusive fee of £500, again with no recurring charges.

Finally, if you opt for the Plan+Implementation service and want ongoing support and assistance too, including dynamic risk adjustment, an annual telephone review, ongoing telephone support, assistance putting your pension into drawdown, and the opportunity to monitor your portfolio online using a dedicated app, AdviceBridge offer all this for an additional £100 a year or £10 a month.

All of the above is summed up in the table below which I have copied from the AdviceBridge website.

My Thoughts

Overall, I have been very impressed by AdviceBridge, both in terms of what they are offering and the prompt and friendly support they provided while I was writing this article. Here are some of the main things I like about their service:

much lower fees than traditional financial advisers

all fees quoted include any taxes due – what you see is what you pay

range of options according to how much (or little) work you want to take on yourself

non-commission-based advisers, so unbiased advice on what investments will suit you best

advisers are free to recommend across the entire range of investment opportunities

all digital process – no need for personal visits or face-to-face meetings

fully FCA authorized company and advisers

advice is covered up to £85,000 under the Financial Services Compensation Scheme (FSCS)

all personal information is securely encrypted

in-depth written advice and recommendations on your retirement finances backed up by telephone support

Any negatives? Well, the only real one I could find is that various groups are currently excluded from the service, e.g. buy-to-let landlords and holders of ‘non-standard investments’. I guess the latter might include me, as I have a proportion of my portfolio in P2P lending and property crowdfunding.

I do of course appreciate that to keep their service so inexpensive AdviceBridge have to streamline their service, but it is a pity if this excludes a significant proportion of people who could benefit from it. I understand that this is something that AdviceBridge keep under review and in future they may remove some of these restrictions. In the mean time, if you aren’t sure whether you are eligible, it is well worth giving them a ring or contacting them via the website to ask (without obligation).

In my opinion, if your circumstances match their criteria, AdviceBridge are well worth checking out. I particularly like their £500 Plan+Implementation service, which covers not only researching and producing a retirement plan for you but implementing it as well. I would also seriously consider paying the extra £100 a year (or £10 a month) for the ongoing service. Obviously that brings the price up a bit further, but it is still far less than you would pay a traditional financial adviser for a similar service.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: This is a sponsored post for which I am receiving a fixed fee (but no commission). Please note also that I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and take professional advice as appropriate. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’ve joined forces today with some of my fellow UK Money Bloggers to put together a giveaway of FIVEM&S Easter Family Hampers. That means five lucky winners will receive a hamper in time for Easter 2020 🙂

These hampers sell for £50 apiece on the M&S website. The full contents are as follows:

Gold label teabags (250g/ 80 bags)

Caramel eggs (120g)

Hide and seek egg hunt bag (135g)

Simnel cake bar (460g)

Chicky choccy speckled eggs (90g)

8 Spiced Easter biscuits (200g)

Bubbly bunny (23g) x 4

British strawberry soft set jam (113g)

Easter fried eggs whips (180g)

4 golden hot cross buns (260g/pack of 4)

Presented in a dark stained basket with brown faux leather strap

In the event of supply difficulties, or with discontinued products, M&S say they reserve the right to offer alternative goods or packaging of equal quality and value. Full information about the hamper and its contents can be found on the M&S website.

Here then are all the details you need to enter, provided by my colleague Emma Drew (who is co-ordinating this event). Good luck! It would be great if a Pounds and Sense reader wins one (or more) of the prizes 🙂

Meet the Bloggers Taking Part

The bloggers taking part in this fantastic giveaway are as follows…

There are five M&S Easter Hampers up for grabs, worth £50 each.

If the hamper is no longer available when the winners are drawn then the winners will be offered an alternative hamper from M&S worth £50 each.

Enter to Win

To enter simply complete any or all of the Rafflecopter entry widget options below.

The competition closes at midnight on 29th March 2020. If the hamper selected is sold out then we will offer an alternative M&S hamper worth £50. You can see the widget for the full terms and conditions of this giveaway.

One final small point is that if a winning entry comes from following someone on social media, Emma will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and I really do hope you win a hamper!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I am something of an enthusiast for property investment (and specifically property crowdfunding). Among other things, I like the fact that you can make money from both rental income and capital growth. And investing in property can be a good way of spreading risk when you have equity-based investments.

The House Crowd was actually the first property crowdfunding company I invested with, starting in 2014. So I thought I would say a few words today about my experiences with the company and the investment opportunities they offer.

Table of Contents

History

When I started investing with The House Crowd, they were offering mainly shares in specific properties. Investors pooled their money to buy a property and received a share of the rental income (distributed annually) with their money back – and hopefully a good profit – when the property concerned was sold. Typically a five-year timescale was specified, with investors then able to vote on whether to sell and take their profits or continue for another year (or more).

I still have shares in seven House Crowd properties. There haven’t been any disasters, though in certain cases rental income has been lower than forecast. This was typically due to voids (tenants leaving and not being replaced). There were also a few cases of tenants failing to pay their rent and absconding. And there was one ‘tenant from hell’, who apparently threatened other tenants with a knife so they all left, caused serious damage to the property, and left owing six months’ rent. Reading about this made me glad I invest via property crowdfunding platforms (and REITs) and am not a landlord myself.

One drawback of this type of investment is that it is quite illiquid. If you want your money back before a property is sold, The House Crowd will try to sell your share to another investor. There is no guarantee a buyer will be found, however, and even if one is you will only get the price you paid for your share. There is currently no formal secondary market, as on some other platforms such as Property Partner.

On the plus side, this sort of investment has its attractions from a tax perspective. Rental distributions are paid as dividends. There is currently a £2,000 annual tax-free dividend allowance which many people don’t otherwise use. And even if your dividend income exceeds £2,000, as a basic rate taxpayer you will only pay 7.5% tax on the balance above this. Gains when selling are – of course – treated as capital gains, and again there is a generous annual tax-free CGT allowance (£12,000 in 2019/20).

New Types of Investment

In recent years, recognizing that some investors were being deterred by the lack of liquidity, The House Crowd have introduced other types of investment. One of these is secured loans. Here money is lent to developers (or THC’s sister company, House Crowd Developments) for short- to medium-term projects, typically between 6 and 18 months.

Obviously you don’t get rental income with these, but you get your money back with interest once the loan is paid off. Interest rates vary, but are typically in the region of 7 to 12% per year. The rate paid generally depends on the LTV (loan to value). The higher the LTV (the loan amount compared with the property value), the riskier the loan, and the higher the interest rate on offer as a result. Some example projects open for investment at the time of writing can be seen in the cover image at the top of this post.

I have invested in loans with The House Crowd as well. The majority have gone well. For example, I invested £5,000 in a development loan for a Welsh property called Croesyceiliog Farm. I got this back with £461.99 interest ten months later.

Other loan investments haven’t gone as smoothly. For example, in 2016 I invested £1,000 in a loan for a property called Caverswall Castle. This was meant to be 12-month loan, but the borrower defaulted and legal action is now being taken to sell the property and repay investors. I still expect to get my money back eventually, but legal proceedings move at a glacial pace. How much interest I will get after all costs are covered I don’t know. At this stage, if I just get my £1,000 back, I will be more than happy.

Secured loans have various attractions for investors, and many property crowdfunding platforms as well as The House Crowd are now offering more opportunities of this nature. They have the advantage of shorter timescales than direct investment and decent rates of return (assuming the borrower doesn’t default). One drawback is that the interest paid when the loan is redeemed is treated as income, so you will have to pay tax on it at your highest marginal rate.

Auto-Invest and IFISA

In recent years The House Crowd have introduced an Auto-Invest product which you can (optionally) hold as an Innovative Finance ISA (IFISA).

As you may know, IFISAs offer the opportunity to invest in P2P lending and get tax-free returns. Everyone has a generous annual ISA allowance of £20,000 (in the current 2019/20 tax year). This can be divided any way you like among the three types of ISA. So if you open a House Crowd IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. Note that you can also only invest in one ISA of each type per financial year.

The House Crowd Auto-Invest product allows you to invest in one of three investment portfolios: Cautious, Balanced or Bold. Each of these comprises a basket of bridging and development loans, providing automatic diversification. The Cautious product has a target return of 5%, the Balanced 6%, and the Bold 7%. Note that these are target rates and they are not guaranteed. I have copied a summary table about the three products from the House Crowd website below .

As you can see, the more ‘adventurous’ the product, the higher the average LTV and the higher the maximum LTV. As mentioned earlier, the higher the LTV (other things being equal) the riskier the loan, and the higher the interest rate on offer as a result.

There is a minimum investment of £1,000 and a minimum 12-month term. After that you can withdraw by giving 30 days’ notice. Your money is protected by a legal charge secured against the borrower’s land/property, which can be possessed and sold in the event of the borrower not repaying.

It is possible to transfer another ISA to the House Crowd IFISA free of charge if it is over £5,000 (there is a £50 transfer fee for ISAs valued from £1,000 to £4,999).

Pros and Cons

As usual, here is my list of pros and cons for The House Crowd.

Pros

1. Well-established property crowdfunding platform with a good track record.

2. Customer service is fast, friendly and helpful.

3. Choice of investment types.

4. Tax-free IFISA option available.

5. Competitive rates of interest.

6. Attractive, user-friendly website.

7. Detailed information provided about loans and investments.

Cons

1. Limited liquidity with no formal secondary market.

2. Rental income (where applicable) only distributed annually.

2. Minimum £1,000 investment.

3. Some loans are currently in default.

4. Can’t open an IFISA if you have already put money in another IFISA this year.

Conclusion

For the most part I have been happy with my experiences with The House Crowd to date. Although (as mentioned above) there have been ups and downs, overall I have still made a good net return from my investments with them.

I like the new Auto-Invest/IFISA option, which is automatically diversified across a range of loans (thus reducing volatility and risk). The minimum 12 month term and withdrawal on 30 days’ notice thereafter is attractive as well. It is, however, important to be aware that the target rates of return quoted are not guaranteed.

You should also bear in mind that investments with The House Crowd do not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme. All investments are though secured against bricks and mortar, so in the event of a borrower defaulting you should still get your money (or most of it) back once the property has been sold. But obviously, this may take a while.

The lack of liquidity with property investments generally – and the absence of a formal secondary market with The House Crowd – means you should only invest money you are unlikely to need at short notice. This should be regarded as a medium- to long-term investment, therefore.

Clearly, no-one should put all their spare cash into The House Crowd (or any other investment platform). Nonetheless, it is worth considering as part of a diversified portfolio. Not only are the rates of return significantly higher than those offered by banks and building societies, they are relatively unaffected by fluctuations in the stock market. Property investments aren’t a way of hedging your equity-based investments directly, but they do help spread the risk

A further consideration is that with world stock markets in chaos at the moment due to the coronavirus outbreak, now is probably not an ideal time for the average individual to be investing in stocks and shares. P2P lending of the type offered by The House Crowd represents an alternative investment approach that may be less susceptible to the wild ups and downs (mostly downs) on stocks and shares right now..

Welcome Offer

Unfortunately at present there is no welcome offer (or referral scheme) for new investors with The House Crowd. If a welcome offer is launched in future, I will of course post full details here.

If you plan to open an account with The House Crowd after reading this review, I’d still be grateful if you could let me know by sending a message via my contact form or leaving a comment on this post. This may help me persuade THC to set up a referral scheme and/or welcome offer in future 🙂

And of course, if you have any comments or questions about this review, as always, please do leave them below.

Note: This is a fully revised and updated version of my original 2017 review.

Disclosure: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. All investments carry a risk of loss. Finally, in the interests of full disclosure, I should reveal that as well as being an investor with The House Crowd, I also own shares in the company.

If you enjoyed this post, please link to it on your own blog or social media:

For many older people the free bus pass (officially known as the older person’s bus pass) is a valuable concession. It helps them get about and maintain their independence without eating into their often limited income.

Holders typically get free bus travel within their local authority area between 9.30 am and 11 pm on weekdays and all day at weekends.

The rules for when you qualify for a free bus pass vary according to where in the UK you live. In Scotland, Wales and Northern Ireland, it’s straightforward. You qualify once you reach your 60th birthday.

Those living in England are not as fortunate. In this case, you won’t qualify until you reach the current state pension age. This is currently 66 for both men and women. The state pension age will start to increase again from 6 May 2026, and will reach 67 by 6 March 2028.

Once you have reached the qualifying age in whichever country of the UK you live, you can apply via the government’s Apply for an Older Person’s Bus Pass page. You will see a box on this page in which to enter your postcode. Clicking through this should take you to the website for your local authority (though you may have to navigate to the page for travel concessions from there). You can then apply online for your bus pass. Requirements can vary from one local authority to another, but in general you will be required to upload a passport-style photo, proof of identity, and proof of residency in the area concerned (e.g. a council tax bill). For info about how to renew your bus pass online, please click here.

If you don’t want to apply online, most authorities also offer an option to apply in person, e.g. at a public library. Your local authority website should have more information about this.

Some local authorities have their own schemes and concessions for older (and/or disabled) people. Again, your local authority website should tell you if there are any special concessions for older people in your area, or you can ask at your local library.

In London, once you reach the female state pension age you can apply for an Older Person’s Freedom Pass. This entitles you to 24-hour free travel across Transport for London’s networks (except for some river boats where travel is half price). You can check your eligibility for a Freedom Pass and apply here.

Cards and Discounts

Even if you don’t yet qualify for a free bus pass, there may be other ways you can get free or discounted travel.

If you live in London and are 60 or over, you can apply for a 60+ Oyster card. This provides free travel on the London Underground, Overground, trams and buses, as well as some TfL Rail and National Rail services, but you can’t use it outside London. The card has a one-off £20 administration fee. You can apply online from two weeks before your 60th birthday. For more information about the application process see the TfL website.

Also once you are 60 or over, you can apply for a Senior Railcard. This currently costs £30 a year and gets you a third off most rail journeys, local and national. You can get more information and apply here.

Or if you’re 60 or over and make regular use of National Express coaches, you can buy a Senior Coachcard which costs £12.50 (plus 2.50 p&p) and offers a third off travel throughout the year. With this card you can also buy a £15 day-return on Tuesdays, Wednesdays and Thursdays to anywhere in the UK (excluding airports) as long as you book three days in advance. You can apply for a Senior Coachcard via the National Express website.

As always, if you have any comments or questions about this post, please leave them below. Happy travels!

If you enjoyed this post, please link to it on your own blog or social media:

It can hardly have escaped your notice that in the last week or so shares generally have plunged in value due to economic fears sparked by the coronavirus outbreak.

If you have a pension pot, stocks and shares ISA, or any other equity-based investment/s, this is obviously a worrying time. It’s very important to avoid knee-jerk reactions, though.

In particular, unless you really need the money urgently now, you should think very carefully before selling up. By doing so you will be locking in any losses. Even though it’s true that shares may have further to fall, this advice still applies. All share prices are cyclical, and rises and falls are to be expected. That is why stock market investments should always be regarded as long term.

Luckily, there are a few apps that offer you experts’ advice on safe long-term investments. You can check some of the best on the market at BestStockTradingApp.com.

A further consideration is that if you sell up now, you won’t receive any dividends due from your shares further down the line.

Should You Top Up?

With share prices currently falling, should you take the opportunity to ‘top up’? That is actually a difficult question to answer, as it’s impossible to know for sure how much further the markets will fall before they recover. Timing the market is notoriously difficult, and many investors in the past have had their fingers burned by thinking they could second guess it.

Nonetheless, if you are currently investing monthly into a stocks and shares ISA or other fund, I would say you should almost certainly continue to do so. One consequence of the fall in share prices is that you will get more shares for your money now. This will actually boost the value of your portfolio in the longer term when the markets recover. This phenomenon is called pound-cost averaging. It is one reason why making regular smaller investments rather than one-off lump sums can be such a good option for investors.

Otherwise, it is really a matter of personal judgement. If you think that a certain share or fund is good value at its current price there may be a case for investing in it. Inevitably, though, this will be a bit of a gamble. I am not personally planning to top up my equity portfolio until the present crisis appears to be well on the way to being resolved.

Beware of Pound-Cost Ravaging

If your pension is already in drawdown – especially if you are early into your retirement – pound cost ravaging is a risk you need to be aware of right now.

If the value of your pension pot is falling and you are also drawing money from it, those two things together have the potential to deplete it rapidly. You are then increasing the risk of running out of money later into your retirement.

If you have other sources of cash, therefore, it may make sense to reduce or even suspend entirely withdrawals from your pension pot during this time. This will help preserve its value. You will be able to resume withdrawals when – as will inevitably happen at some point – the markets recover. The great majority of pension providers will be happy to do this for you if you request it.

Consider P2P and Other Non-Equity Investments

If you have money to invest, in my view there is a good case right now for considering other types of investment such as P2P.

Regular readers will know that I am a fan of this type of investment (if approached sensibly and selectively) and have a fair-sized portion of my own portfolio invested in it. I won’t go through all the possibilities now as this is a subject I discuss regularly on Pounds and Sense. But if you are looking for a couple of ideas to start you off, I recommend checking out RateSetter – a relatively low risk P2P lending platform which I reviewed in this post – and Bricklane, a REIT (Real Estate Investment Trust) which offers a highly tax-efficient Property ISA (reviewed in this post).

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

In February 2017 I wrote this post about premium bonds explaining why I was withdrawing a large amount of the money I had invested in them.

To recap, at that time the interest rate paid on premium bonds (from which the monthly prize fund is calculated) had been cut eight months earlier in June 2016. This led me to sell the majority of my holding, as the amount I was earning in prizes had fallen considerably. The rate was cut again a few months later in May 2017, which led me to sell nearly all my remaining bonds. I now have just £5 left, to avoid closing my account completely.

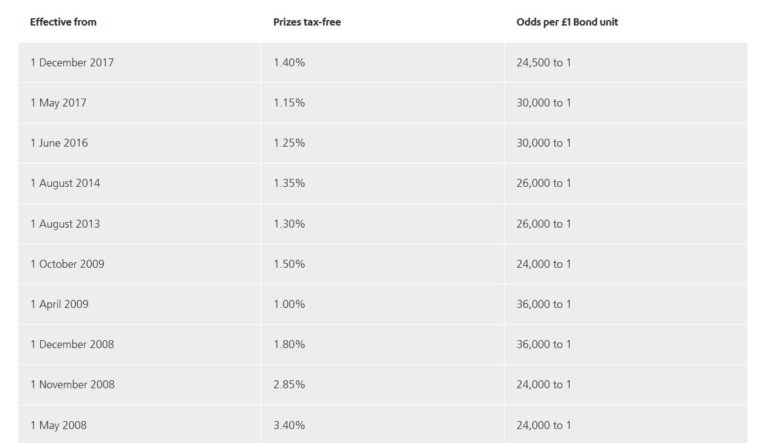

So what has happened since then? The good news for bond owners was that from December 2017 the prize fund was raised by 0.25% to 1.40%. This improved the odds of an individual bond winning a prize in any monthly draw from 30,000 to 1 to 24,500 to 1 (although it still didn’t tempt me to reinvest).

The not-so-good news is that from May 2020 the rate is being cut by 0.1% to 1.3%. As a matter of interest, here is a table copied from the NS&I website showing the changes in prize rates and the odds of winning a prize over the last twelve years. The new rate from May 2020 isn’t shown on the table.

From May 2020 the chances of winning a prize with a single bond will be reduced to 26,000 to 1. Over 170,000 fewer prizes are set to be given out in May 2020 than in February as a result of this change, with less than half the number of £100 and £50 prizes expected to be awarded (source: MoneySavingExpert).

My Thoughts

A first glance you might think that an interest rate of 1.30% percent still isn’t so bad in these days of (very) low interest savings accounts. It’s much the same as the current top paying easy-access savings accounts. Premium bond prizes are tax-free and you can withdraw your capital any time if you need it within a few days. Your money is protected by the UK government and you have an outside chance of winning a life-changing sum. So what’s not to like?

Well, quite a lot in my opinion. Most importantly, although the interest rate is currently 1.40% (reducing to 1.30% in May) in practice most people won’t make this amount. The interest rate is a mean (average) figure and this is skewed by the two one-million pound prizes (which statistically you are highly unlikely to win – see below) and the small number of other other high-value prizes. For these big prizes to be paid out, a lot of people have to win nothing. The more bonds you have, the closer to the average your prize earnings are likely to be. But the reality is that most premium bond owners won’t earn the interest rate quoted (and they may make nothing at all).

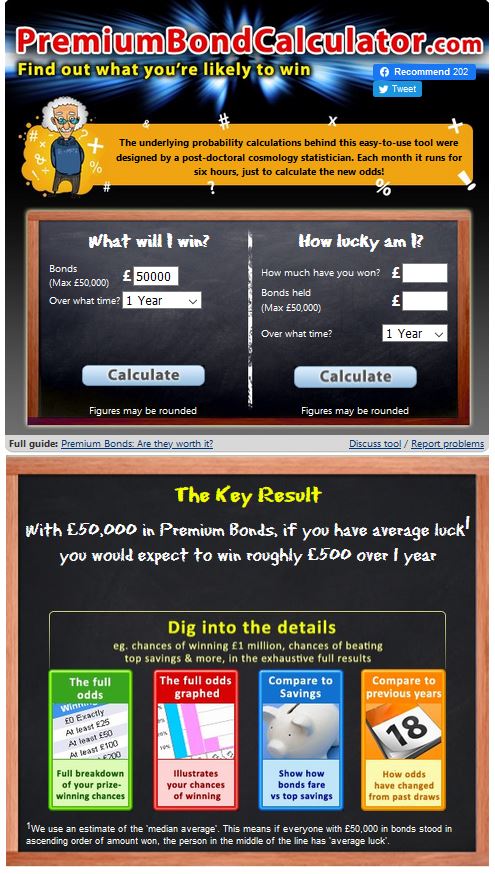

A better measure of what you are likely to make over a year is the median average. The way to think about this is that if you lined up all premium bond-holders with a certain number of bonds (e.g. £50,000) in order from those earning the least in a year (probably nothing) to the most (a million pounds plus), the median is the person right in the middle of the line. Half of all holders will earn more than this person (or the same) and an equal number will earn less. The median in this context is therefore a measure of what you can expect to earn from your premium bonds in a year with ‘average luck’. The clever folks at MoneySavingExpert have built a Premium Bond probability calculator which uses this metric to indicate how much you are likely to win per year, with average luck, with any given holding.

With the £50,000 maximum, the calculator reveals that with average luck you will win just £500 of prizes a year, equivalent to an interest rate of just 1.0 percent (see screen capture below). And that is at the current (February 2020) interest rate. From May 2020 that figure will inevitably go down. Obviously you might have better than average luck, but (as stated above) around half of all bond-holders will have worse. You can read a much more detailed explanation about this on this page of the MSE website.

The calculator also reveals that with £5,000 in premium bonds you could expect to win £50 a year with average luck, and with £1,000 nothing at all. Only about one in three people with £1,000 worth of bonds will win a prize in any one year, so the median (‘average luck’) winnings are zero. Over a two-year period, however, about five out of nine holders of £1,000 will win at least one prize, so the median earnings over two years with £1,000 in bonds are £25 (the lowest and by far the most common prize). This does I guess demonstrate that the ‘average luck’ method used in the MSE calculator has its limitations as a way of estimating likely earnings (although it is still likely to be more accurate than applying the headline interest rate to your investment).

Clearly the longer you hold your bonds, the better are your chances of winning a larger prize, so over a period of years average annual earnings may edge up slightly. Even so, the large majority of bond-holders won’t ever earn the headline rate.

At one time the tax-free status of premium bond prizes would have been a significant attraction, but nowadays that doesn’t apply to nearly the same extent. All basic rate taxpayers now benefit from a Personal Savings Allowance of £1,000 worth of tax-free savings interest every year (higher rate taxpayers get £500 and top rate taxpayers nothing at all). In practice 95% of people now pay no tax on their savings interest. If you are in the 5% who do, premium bonds become a more attractive option. Even so, a typical return of 1% or less, even if it is tax free, isn’t going to set many pulses racing.

Finally, you do of course have a chance of winning a big prize, but it’s important to be realistic about what that chance is. Even with the maximum £50,000 holding, MoneySavingExpert calculate that your chances of winning the million pound top prize in any one year are 1 in 69,876. To put this into perspective, if you had held £50,000 in premium bonds since the year 68000 BC (assuming of course they existed then) with average luck at the current interest rate you could have expected to win the jackpot just once. I looked this up, and 68000 BC is the middle of the Stone Age!

Overall, then, I cannot recommend premium bonds as a home for your savings, especially with the coming rate cut in May 2020.

I can understand why premium bonds are a popular investment, as they offer a bit of excitement every month checking whether you have won and how much. But the fact remains that overall, for most people, the total prize money received is likely to average little more than 1 percent a year at current rates. It may very well be less than this, especially after May 2020 when – as already mentioned – the number of lower value prizes (£25 to £100) will be cut substantially. I look forward to checking on the MSE calculator then to see how much a person with average luck might expect to make in a year.

If you are lucky enough to have £50,000 burning a hole in your pocket, my first advice would be to put enough into an easy-access savings account such as the Post Office Online Saver (currently paying 1.30% including a fixed 0.8% bonus for the first 12 months) to cover your outgoings for up to three months in the event of emergencies. After that, you could invest the balance in a low-cost tracker fund, or a portfolio of investment funds, or a robo-advisory platform like Nutmeg. You could perhaps put a proportion of the money into P2P lending or property crowdfunding as well. Over several years, for the great majority of people, this will outperform an equivalent premium bond portfolio many times over.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I recently booked my first ever break with Airbnb.

Of course, I’ve been aware of this person-to-person accommodation booking platform for some time, but till now I’ve avoided using it myself. In the back of my mind were stories I read years ago about people renting out sofas in their living room to make a bit of extra cash. At my age that prospect – the sofa in the living room, I mean – definitely didn’t hold any appeal!

Times change, though, and it’s important to keep up with them. In my case I wanted to book a short break in a part of North Wales that isn’t well served by hotels, the Lleyn Peninsula. Okay, I could have stayed at the Haven Holidays Park (formerly Butlins) in Pwllheli, but I was pretty sure that wouldn’t be my cup of Welsh tea either.

So after researching the relatively few hotels in the Abersoch area where I wanted to stay using Booking.com (affiliate link), I decided it might be time to give Airbnb a try. In recent years, as regular readers will know, I have become more accustomed to booking self-catering accommodation for short breaks, and have realised that in some ways I prefer this to staying in hotels.

In this blog post I thought I’d share my experience of registering with Airbnb and finding and booking accommodation. I hope this might inspire you to try it yourself if you haven’t yet taken the plunge with Airbnb.

Of course, you can also become an Airbnb host and make money that way. I haven’t tried this myself, but did cover the subject in another blog post titled Boost Your Income by Renting Out a Room.

Registering with Airbnb

Before you can make a booking with Airbnb, you have to be registered on the website. You can still browse without joining but (as I found out) if you find somewhere you like available on the dates you want, you will have to go back and register and then start the whole process again. This is a frustrating waste of time. It’s free to register and doesn’t take long, so if there is any chance you might want to book through the platform, my advice would be to do this first.

Registering with Airbnb is similar to registering on other booking websites. One thing to be aware of, though, is that as well as your personal details, as proof of ID they also ask you to upload a scan of an official document such as your passport or driving licence with your photo on it. Once you have done this, you have to wait for your ID to be approved. In my case this happened within 15 minutes and I received notification by email.

Once you’ve done all that, you can start searching for your perfect holiday retreat!

Searching Airbnb

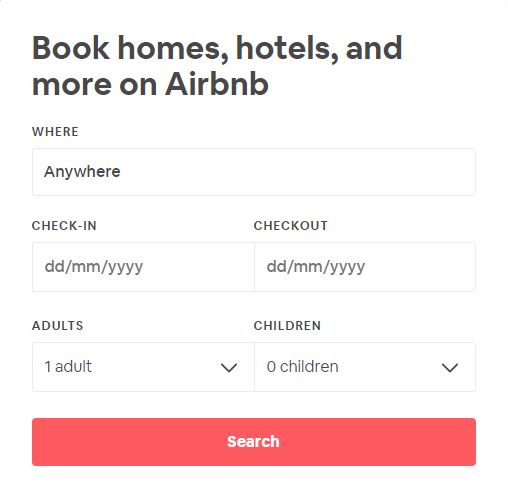

Once you are logged in, you can start your search using the box on the Airbnb front page (see below).

As you can see, you have to enter where you wish to go and the dates you want to arrive and depart. You have to choose specific dates, even if (as I was) you are flexible about this. Once you have found somewhere you like, you will be able to see what other dates that accommodation is available. If you want to check all possible places in the area, though, you may need to do a few searches using different dates.

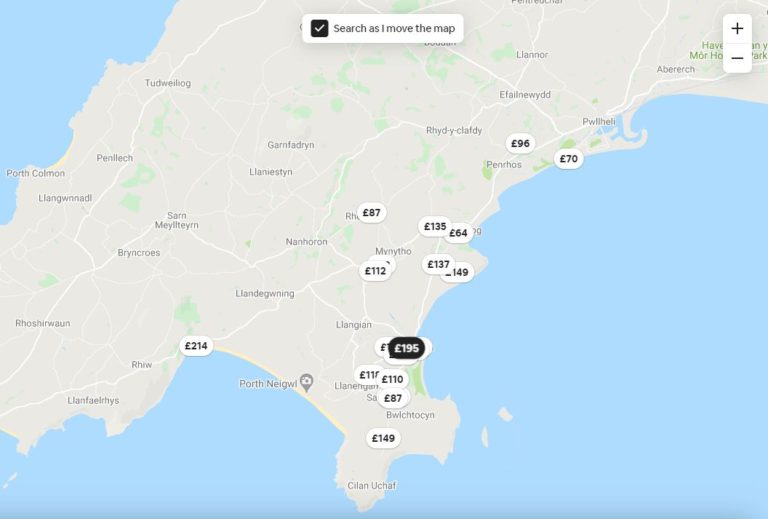

Anyway, once you have entered the relevant details and clicked on search, a new page will open showing you a map of the area in question. Here’s what I got when I searched just now for accommodation near Abersoch in early May (not actually when I am going).

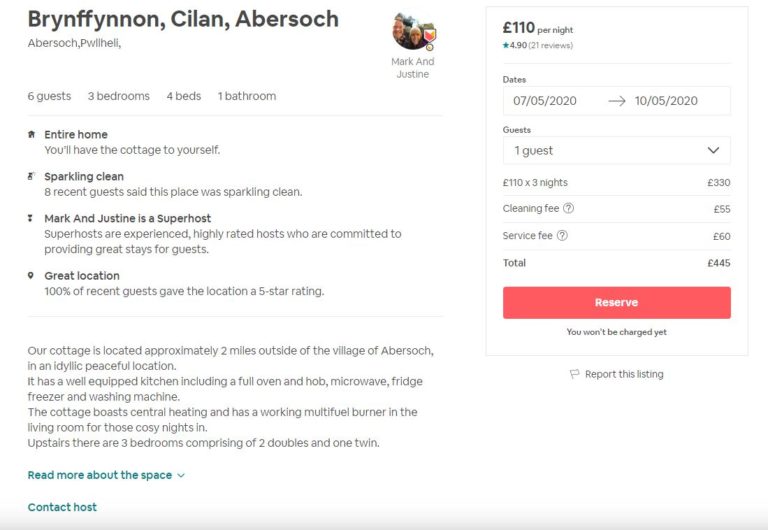

As you may gather, each of the prices in a small oval represents an Airbnb place with availability on the dates in question. The price is the cost per night. Clicking on any of these will bring up brief info about the accommodation in question. If you like the look of this, clicking again will bring up a new page with photos and more. Here’s the top of the page for a cottage I like the sound of, though it would be too large for me alone.

Also on this page are full details about the accommodation and a reservation form – see below.

As you can see, for your money you are getting considerably more than a sofa in someone’s living room 😀 £110 a night seems very reasonable to me for a cottage that can accommodate a family of six.

As you may have noticed, there are some additional charges. Many Airbnb properties – though by no means all – charge a cleaning fee. In addition, you will always be charged a service fee. This goes to Airbnb, and is one way they make their money (they also charge a fee to the property owners).

If you scroll down you will see various other items, including visitor reviews and a calendar showing when the property is (and isn’t) available. Also towards the bottom of the screen you will find the cancellation terms. These are set by the hosts and vary considerably, so be sure to study them carefully. Often you will be able to cancel free of charge until a certain date. After that, you may have to pay the service charge and perhaps part or all of the booking fee as well.

Making Your Booking

If you want to proceed, clicking on Reserve will take you to a new page where you can confirm your booking and provide payment information. This is pretty standard, although one thing you don’t normally have to do on hotel booking sites is write a message of introduction to the property owners (your hosts).

Airbnb provide a ready-written message you can use by default. This is pretty bland, however. I think it’s best to take a few minutes to write something more personal about who you are, why you want to visit the area, and so on. This is especially important if you are new to Airbnb and don’t have any history on the site or reviews written about you (yep, Airbnb hosts review guests as well as vice versa). In theory a host can decline your booking if they don’t like the sound of you, so it’s good to reassure them that you are a normal human being and will treat their property with respect.

And that’s it, basically. When I made my booking it all went through smoothly and I received a thank-you message from the hosts within an hour. I haven’t been on the holiday yet, but will post a review on this blog after my return.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Please be aware that this is a historical post. Bricklane is now closed to new investors and is winding down. Please see the comments below for the latest updates about it.

Today I am looking at another property investment platform, Bricklane.

Unlike Kuflink and Ratesetter, both of which I have discussed previously on this blog, Bricklane is not a platform for peer-to-peer loans. Neither does it arrange crowdfunded investments in specific properties like Crowdlords and Property Partner.

Bricklane is structured as a Real Estate Investment Trust, or REIT for short. For those who don’t know, REITs are property funds that use investors’ money to buy (and manage) property and provide returns in the form of rental income plus capital appreciation.

In order to qualify as a REIT in the UK, companies have to meet certain requirements. The most important are as follows:

At least 75% of their profits must come from property rental.

At least 75% of the company’s assets must be involved in the property rental business.

They must pay out 90% of their rental income to investors.

In exchange for operating within these rules – and to encourage investment in UK real estate – REITs are not required to pay corporation or capital gains tax on their property investments. That helps make REITs profitable for the companies running them, and is how they are able to generate attractive returns for investors.

Normally rental income from REITs is treated as taxable income and taxed at your highest marginal rate. However, if you invest through an ISA or SIPP (Self Invested Personal Pension) no tax is due. You therefore get the best of both worlds – your money isn’t subject to taxation while invested in the REIT, and when it comes back to you in the form of income distributions and profits on sales of shares, you don’t have to pay tax on these either.

Table of Contents

Types of Investment

You can invest in Bricklane as a stocks and shares ISA or a SIPP, or failing that in a standard investment account, where you will be liable for tax.

To maximize the benefits from investing in a REIT, I highly recommend going down the SIPP or ISA route, if you haven’t already used up this year’s allowance. As a reminder, everyone has a £20,000 annual ISA allowance (for 2019/20) and you are also only allowed to invest in one cash ISA, one stocks and shares ISA and one Innovative Finance ISA (IFISA) in any one tax year. I invested in a stocks and shares ISA with Bricklane myself.

Bricklane has two property portfolios you can invest in. These are Regional Capitals, which includes properties in Birmingham, Manchester and Leeds. and London, with a portfolio of properties in the capital. The Regional Capitals portfolio has generated a return of 19.3% since it was launched in September 2016 and the London portfolio 8.9% since its launch in July 2017 (figures from the Bricklane website).

As a Bricklane investor, you can choose to invest in either or both portfolios, in any proportion you choose. I opted to put all my money into Regional Capitals, as I believe this is where the biggest growth potential lies. In addition, rental income in this portfolio is higher, and I am also concerned about the possible impact of Brexit on London. You might see this differently, of course!

Bricklane Pros and Cons

Based on my experiences so far – and some online research – here is my list of pros and cons for the Bricklane property investment platform.

Pros

1. Fast, easy sign-up.

2. Well-designed, intuitive website.

3. Low minimum investment of £100.

4. Bricklane take care of all the work involved in buying and managing properties. You just choose which portfolio/s to invest in.

7. Possibility to access your money at any time (though this does depend on another investor being willing to buy your shares).

8. Customer service (in my experience anyway) is fast, friendly and helpful.

9. Charges are reasonable, comprising an initial 2% fee (though see my comment below on how you may be able to offset this) and 0.85% annual management fee.

10. Potential to profit through both capital appreciation and rental income.

11. Rental income is paid into your account every three months. You can either withdraw it or reinvest it to compound your returns.

12. Up to £1,500 cashback is available for new investors of £5,000 or more via my referral link (see below).

Cons

1. No detailed information provided about the properties your money is invested in.

2. Can’t invest in an ISA if you have already put money into another stocks and shares ISA this year.

3. 20% tax deduction from rental income at source if you don’t invest via a SIPP or ISA (and additional liability if you are a higher rate taxpayer).

4. Minimum £10,000 investment for a SIPP.

5. Returns over the last few months have been disappointing (see below)

6. No absolute guarantee you will be able to sell your shares when the time comes.

My Experiences

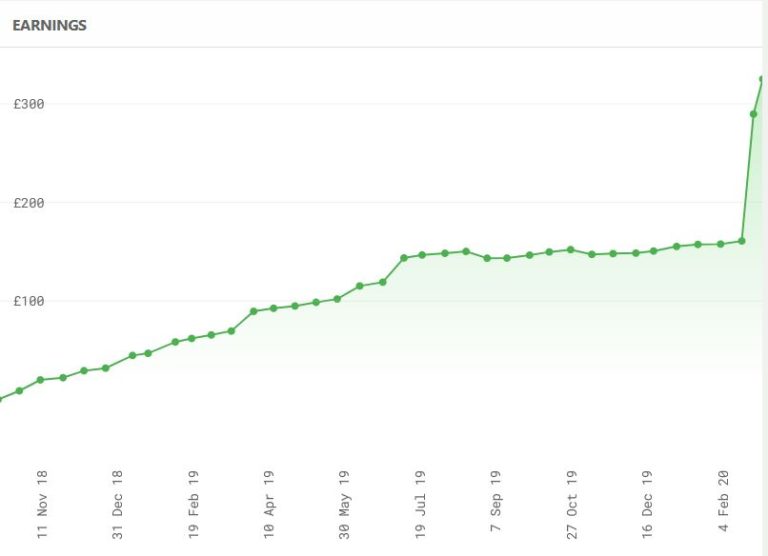

I put £5,000 into a Bricklane Stocks and Shares ISA in October 2018. As mentioned above, I chose to invest in the Regional Capitals rather than the London portfolio. The graph below – taken from my member’s page – shows the earnings generated since I opened my account.

As you will see, initially my investment performed pretty well. In the first nine months I made about £150, which equates to an annual interest rate of 4% (tax-free). That’s not spectacular, but it still beats most bank and building society accounts by a considerable margin. It is similar to the top rate currently on offer with P2P platform RateSetter in their Max account, although in their case you have to pay a fee equivalent to 90 days’ interest if you wish to withdraw. There is no withdrawal fee with Bricklane.

Since July/August 2019, however, returns have diminished considerably. My earnings between August 2019 and February 2020 were only just over £7, which is clearly a very low percentage rate. Of course, a large part of this is down to the depressed state of the property market caused by uncertainty over Brexit. I am hoping that now this is definitely happening – for better or for worse – my investment will get back on an upward trajectory again. Although recent results have been disappointing, at least the overall value of my portfolio hasn’t gone down (which has happened with some of my other property-related investments).

One other thing I should mention is that in October 2019 I withdrew £1,000 from my account to help fund a new central heating boiler after the old one packed in. This has therefore also reduced my returns a little. Although even if I still had the full £5,000 invested, earnings over the last few months would still have been nothing to write home about.

I should add that the withdrawal in question proved straightforward, although it wasn’t instant. I received the money in my bank account about a fortnight after putting in my request.

Conclusion

Clearly the performance of my Bricklane portfolio since last August has been disappointing, though overall I am still better off than I would have been if I had kept my money in a bank or building society.

I am hoping that things will start to improve in the property markets now that the Brexit issue has been resolved. There are some signs of this, although it remains to be seen whether the recovery in property prices will be sustained. For the time being, then, I am sticking with what I have in Bricklane, though I am not planning to top up my investment with them currently.

More generally, my experiences with Bricklane have been good. The sign-up process was fast and simple, and my £125 referral bonus (see below) was credited to my account instantly, completely offsetting (with a bit to spare) the initial 2% charge.

I also like the fact that any investment with Bricklane is automatically diversified across a range of properties, thus reducing volatility and risk. By contrast, with many P2P loan and property crowdfunding platforms, you invest in one loan or property at a time.

It’s also reassuring that you can ask to withdraw your money at any time – this can be an issue with property crowdfunding platforms in particular. As mentioned earlier, this does depend on someone else being willing to buy your shares, but Bricklane say that to date there hasn’t been a problem for anyone wanting to sell. As I said above, I had no issues when I wanted to release £1,000 from my own investment with them.

It is important to note that this is an investment rather than a savings account, and it does not therefore enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme (FSCS).

Clearly, no-one should put all their spare cash into Bricklane (or any other investment platform). Nonetheless, in my view it is worth considering as part of a diversified portfolio. Not only are the rates of return (other than the last few months) higher than those offered by most banks and building societies, they are less affected than shares by ups and downs in the stock market. Property investments aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

In addition, the tax treatment of REITs make them a highly tax-efficient investment, especially if you can invest in the form of a SIPP or an ISA.

Welcome Offer

As an existing Bricklane investor, I can offer a special cashback deal for anyone signing up and investing on the platform via my link. If you click through this special invitation link, sign up and invest a minimum of £5,000, you will receive £125 in cashback (and I will get £100). With a £5,000 investment this bonus will cover your initial 2% charge and still leave you £25 in profit 🙂

If you invest more, you will get even more cashback, as follows:

Over £10,000 – £250

Over £20,000 – £500

Over £50,000 – £800

Over £100,000 – £1,500

Not only that, once you are an investor with Bricklane, even if you only start with £100, you will be able to offer the same cashback bonus to your friends and relatives and earn commission yourself as well. There is no limit to the number of people you can introduce through this scheme.

Obviously, this is a generous promotional offer by Bricklane and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

If you have any comments or questions about this Bricklane review, as always, please do leave them below.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed.

Note: This is a fully revised and updated version of my original Bricklane review from October 2018

UPDATE15 March 2020: Having said that my earnings from my Bricklane ISA over the last 6-8 months were disappointing, since the start of February they have shot up by over 100% (see below).

This doesn’t exactly cancel out the recent falls in my equity-based investments due to the coronavirus, but it does demonstrate the value of having a well-diversified portfolio. And I am obviously feeling more positive about Bricklane as an investment platform now 🙂

One other thing to note is that until the end of April 2020 Bricklane are waiving all investment fees for both new and existing investors. Visit the Bricklane website for more information.

If you enjoyed this post, please link to it on your own blog or social media:

I recently helped an elderly friend submit an application for Attendance Allowance, so in this post I thought I would set out how the application process works and share some tips and advice based on my (thankfully successful) experience of claiming it.

But first, let’s deal with the basics…

Table of Contents

How Much Is It?

Attendance Allowance is paid at two different rates according to how much help and care you need.

The lower rate (currently £58.70 a week) is paid to people who need frequent care throughout the day OR night

The higher rate (currently £87.65 a week) is paid if you need frequent care throughout the day AND night, or if you are terminally ill.

Payments are normally made every four weeks direct to your bank account. The money is yours to spend as you wish to make your life a bit easier.

It is worth noting that you do not need to have someone currently caring for you in order to claim. Eligibility is based on your need for care rather than whether you are actually receiving it.

Another important point is that Attendance Allowance is not means-tested – eligibility is based purely on your care needs. Also, it is not taxable and will not normally affect your entitlement to other welfare benefits. Indeed, you may also be eligible for extra Pension Credit, Housing Benefit or Council Tax Reduction if you receive Attendance Allowance.

How Do You Apply?

Attendance Allowance is administered by the Department for Work and Pensions (DWP) rather than local councils. In Northern Ireland the Department for Communities (DfC) has responsibility for it.

The bad news is that there is a long (31 pages) and complicated application form. You can either download this from the government website or you can phone them on 0800 731 0122 and ask for a form to be sent to you. In Northern Ireland you can download the form from this site or phone the Disability and Carers Service on 0800 587 0912. You can apply yourself or someone else can apply on your behalf (with your permission, of course)..

Whether to download the application form or request it by phone needs careful consideration, as both methods have their pros and cons.

If you download the form it will be as an editable PDF. That is the option I used for my friend’s application. It has the advantage that you can complete it on screen rather than by hand. If is therefore easy to edit and amend your answers. Then when you are ready you can print it, sign it where required, and submit it. As a matter of interest, I used the free Foxit Reader program to complete and edit the form on my PC.

On the other hand, if you request a printed application form, as long as you return it within six weeks (a deadline date will be marked on the form) the benefit – if awarded – will be backdated to when the form was sent out. If you download the form from the website, it will only be backdated to the date they receive it from you. So you could lose out on several weeks’ money you might otherwise have had.

One compromise would be to request the form by phone and download it from the website as well. You can then use the downloaded version to create and edit your answers on screen. Once you have a finished version you are happy with, you can copy this manually on to the paper form and submit it within the six-week deadline.

Top Tips for Filling in the Form

Based on my experiences helping my friend – and some additional research online – here are my top ten tips for completing the Attendance Allowance application form.

1. Don’t rush at it like the proverbial bull in a china shop. If you do, you will almost certainly make mistakes and forget things. If you requested the form by phone you have six weeks to complete and return it without any financial penalty, so take advantage of this.

2. Read the notes that come with the form before you start to complete it. This will help you understand what the assessors are looking for to determine whether you are eligible for the benefit (and at what rate).

3. Keep a diary for a few days at least (ideally a week). Record in this all the occasions on which you need help and support. For example, if you need help getting dressed or washing, note down when this happens and how many times a day.

4. Be honest about your care needs when completing the form. Bear in mind, though, that Attendance Allowance is awarded to people who need help with their personal care. Washing, showering, eating, getting dressed and going to the toilet would all be things to mention if you need help with them. On the other hand, things like washing clothes, cooking, washing-up, dusting and hoovering may not be viewed in the same light. While these tasks clearly have to be performed by someone, they probably wouldn’t be regarded as personal care needs. Neither does the allowance cover mobility needs.

5. In the relevant section (Question 25) you should list any aids and adaptations you need/use. These might include bath or stair rails, a hoist, a shower seat, a commode, a walking stick, a wheelchair or walking frame, and so on. If you have eyesight problems, they could also include a magnifying glass or an extra-bright daylight bulb. You should also write about these things in the relevant ‘care needs’ questions. For example, if you use a grab rail to get in and out of the shower, you should also mention this in Question 29, ‘Do you usually have difficulty, or do you need help with washing, bathing, showering or looking after your appearance?’ Don’t worry if you end up mentioning the same thing twice (or more) over.

6. Bear in mind that you don’t have to require continuous support to receive the benefit. The term used on the form is frequent, although this isn’t defined precisely. One question (in Q38) asks how long you can safely be left unsupervised. My friend and I decided that the honest answer to this was two to three hours, although the latter would only apply with careful advance preparation. We answered 2-3 hours maximum and this appeared to be acceptable.

7. In addition, it doesn’t matter who is providing your care currently. My friend was concerned that because her husband was her primary carer, she would not be eligible for Attendance Allowance, as this would be expected from a spouse anyway. That is emphatically not the case. No matter who is caring for you – or even if nobody currently is – that will not affect your eligibility for the benefit.

8. The form gives you the opportunity (in Q49) to include a statement about your care needs from someone who knows you well. It is obviously good to include this if you can. As a close family friend I filled in this part of the form myself, but other options might include a doctor, a nurse, a care assistant, a family member, a priest or chaplain, or even a neighbour. Obviously it is important that whoever does this understands what the form is for and the sort of care needs the assessors are looking for.

9. You can also include a letter (or letters) from a medical professional backing up your need for care and support. In the case of my friend, we included a copy of a letter from her main (respiratory) consultant regarding her latest appointment. Fortuitously this also listed all her other health conditions and included a brief medical history. If you don’t have something like this available, ask your GP or consultant if they will provide something for you.

10. Remember that care needs can be psychological as well as physical. If you need support to combat loneliness and depression (or worse), you can and should mention this on the form.

Submitting the Form

Once you have completed the form, you will need to send it by post (email is not acceptable). As I completed my friend’s form online, I printed it out and put it in a clear plastic wallet, then sent this is a large padded envelope.

The address to send it in England, Wales or Scotland is Freepost DWP Attendance Allowance. The address for Northern Ireland will be on the form.

Don’t expect a quick response to your application. It is likely to be six to eight weeks before you hear anything, though you can if you wish phone to check that they have received it.

As mentioned, if your application is successful your benefit will be backdated to the date the form was received or (if you originally requested it by phone and are within the six-week deadline) the date the printed form was sent out to you.

Thankfully my friend’s application was approved without any further investigation and she is now receiving the allowance. In some cases applicants are required to attend for a personal assessment. Information about this will be sent by letter.

If you are unsuccessful in your application, you can submit an appeal. Information about how to do this will be included with the letter informing you that your application has been unsuccessful. You will need to appeal in writing to the address given in the letter. Normally you have to submit your appeal within a month of being turned down.

Other Resources

This has inevitably been a concise article, based on my experience of applying for Attendance Allowance on my friend’s behalf. If you need more information and guidance, there is plenty more online. Here are some useful websites to check out…

If you – or an elderly relative, friend or neighbour – may be eligible for Attendance Allowance, I hope this post has encouraged you to apply. The application form can appear daunting at first, but if you take your time and approach it in a calm and systematic way, it is perfectly do-able. The money is set aside for people in your situation, and it really can help make your life a little more comfortable.

I do, though, recommend enlisting some help with it if possible. Even if you are confident about completing the form, someone who knows you well may be able to suggest ways you need care and support that you might not have thought to mention yourself. And two heads are always better than one, of course! If you don’t have a suitable friend or relative, you can contact your local Citizens Advice Bureau and ask if they have someone who can assist you in completing the form.

As always, if you have any comments or questions (though bear in mind I make no claim to being an expert about Attendance Allowance!), please do leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media: