Today I wanted to let you know about a free website where you can discover all the latest free offers, voucher codes and flash bargains.

Gratisfaction UK is updated daily, every day, with all the latest UK offers, contests and giveaways. The main menu at the top of the screen has five tabs titled Home, Freebies, Flash Bargains, Voucher Codes and Hot. These are pretty self-explanatory, but here is a screen capture of the Freebies section at the time of writing.

As you can see, items are added on an hourly basis. If a particular offer appeals to you, clicking on Get Freebie will take you to a web page where you can apply for the deal in question.

If you don’t want to miss anything, you can also sign up to a free daily email newsletter. Just enter your first name and email address in the box at the top left of the screen. You can, of course, cancel at any time if you decide it’s not for you.

There are lots of great freebies at Gratisfaction UK. Some that particularly caught my eye included a free McDonalds activity pack for kids (perfect with the Easter holidays fast approaching!), a competition to win one of 20 free jars of the new Marmite Peanut Butter, and another competition to win one of five luxury Belazu food hampers. Just be sure to check they are still open, as many of the offers are time-limited and may close suddenly or expire. You snooze, you lose, as the expression goes!

In summary, if you like saving money and getting freebies, do check out Gratisfaction UK – and if you like what you see, sign up for their free email newsletter as well.

Disclosure: This is a sponsored post on behalf of Gratisfaction UK.

If you enjoyed this post, please link to it on your own blog or social media:

Stop me if you’ve heard this before, but I just realised that I have been paying well over the odds for another of my home insurance policies. This time it is my Home Emergency Cover.

To put you in the picture, soon after I moved into my current home with my now-deceased partner Jayne in March 1995, we decided to take out emergency plumbing and drainage insurance with a company called Homeserve.

We were strongly influenced at the time by a promotional leaflet enclosed with the water bill which indicated that if there was a problem with the water supply pipe from the mains, the water company wouldn’t be responsible and we could face a large bill to have it fixed.

Homeserve were offering a policy that would cover us in these circumstances and for other plumbing-related emergencies. Rightly or wrongly, we felt at the time it made sense to pay for this, especially as the company seemed to be endorsed by our water supply company (South Staffs Water).

We paid for the policy by quarterly direct debit and each year it rolled over, generally with a small increase. I looked after our household finances but never really thought much about this. The sums involved weren’t huge, and I assumed it was worth paying them for the peace of mind. As far as I can remember, we never actually made a claim on the policy.

Fast forward to 2019, and after taking stock of my buildings and contents insurance (and saving over £500 on it), I decided the time had come to put my home emergency cover under the microscope as well and see if there were any savings I could make. And again, there certainly were!

Doing the Sums

In December 2018 Homeserve said my insurance would be going up from £198 to £222 per year, working out as £55.50 per quarter (to be fair to Homeserve there was no extra charge for payment by instalments).

So I went online to see what alternatives there were for plumbing and drainage insurance. I did a search for home emergency cover providers on Top Cashback (a website that provides money back to people buying via merchants listed on the site – see this post for more details).

I could immediately see a few possibilities for saving money. Even allowing for the cashback on offer with TCB, though, the best deal I found was with another company called Home Emergency Assist. HEA offer a wide range of policies, some of which also include gas and electrics, pest removal, boiler servicing, and so on.

Obviously you have to be sure you are comparing like with like. With Homeserve I was on their Plumbing and Drainage Plus policy, which covered me for emergencies with the internal plumbing and external water supply pipes. There was a maximum limit of £4,000 per claim.

With HEA I could have bought water supply pipe and stop cock cover only, for a price (according to their website) from £1.49 a month or just under £18.00 a year. For a policy similar to Homeserve’s which also covered me for internal plumbing problems, I was quoted £42.57 a year. This is obviously a lot less than Homeserve’s price, and there was also a higher maximum limit of £5,000 per claim.

Admittedly Homeserve’s policy included zero excess, whereas the HEA quote mentioned had a £95 excess per claim. I was happy to accept that, but for the purposes of a fair comparison I checked their price for a policy with zero excess as well and this was £87.89 a year – still £134.11 cheaper than Homeserve quoted (and with a larger maximum claim limit).

So I cancelled my Homeserve policy, and (after a few more checks including reading their Trust Pilot reviews) have signed up with Home Emergency Assist instead. As I accepted the £95 excess, I shall be paying £42.57 a year, which as stated above is £179.43 less than I would have been charged by Homeserve.

I have, incidentally, nothing against Homeserve, but for me anyway their offer no longer represented value for money. Neither am I especially endorsing Home Emergency Assist. Although they offered the best price I could find for my needs, you might of course do even better by shopping around.

In any event, the real moral of this story (as I’ve said before) is not to let laziness and inertia ever stop you looking for better deals. Even with something as mundane and relatively cheap as home insurance, you may be as surprised as I was by how much money you can save.

You can search on Top Cashback for home insurance providers (all offering cashback) by clicking on this link (affiliate). If you aren’t already a member you will need to register to get cashback, but this is free and only takes a few moments.

As ever, if you have any comments or questions on this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have another great giveaway to share with you. I’ve joined forces with some of my fellow UK Money Bloggers to put together a giveaway of not one, not two, but three Marks & Spencer Easter Hampers.

These hampers sell for £50 apiece on the M&S website. They contain an assortment of Easter goodies, beautifully presented in a stylish dark brown hamper. The full contents are as follows:

Assam tea (25g/10 bags)

Caramel eggs (120g)

Simnel cake bar (400g)

Cheeky chicks (120g/pack of 6)

Mini luxury hot cross buns (325g/pack of 9)

Hide and seek egg hunt bag (135g)

British strawberry soft set jam (113g)

Chicky choccy speckled eggs (100g)

8 Easter biscuits (200g)

Bubbly bunny (23g) x 4

Presented in a dark-stained wicker hamper with brown faux-leather handle and straps

In the event of supply difficulties, or with discontinued products, M&S say they reserve the right to offer alternative goods or packaging of equal quality and value. If you need to know about any possible allergens in the contents, full information can be found on the M&S website.

Here then are all the details you need to enter, provided by my colleague Emma Drew (who is co-ordinating this event). Good luck! It would be great if a Pounds and Sense reader wins one (or more) of the prizes 🙂

This Easter, some of the UK Money Bloggers have come together to offer you the chance to win one of three M&S Easter hampers. Three lucky winners will win an Easter hamper delivered before Easter. Keep reading to find out how you can enter.

Table of Contents

Who are the bloggers behind the giveaway?

The UK Money Bloggers are a group of bloggers, podcasters, and influencers in the UK who are passionate about helping you to improve your finances. Whether you want to make more money, spend less, understand investing or pay off debts, we all contribute something unique to the community. Here’s who we are:

The giveaway is open until midnight on 14th April 2019, when the winners will be chosen.

The giveaway is open to UK residents only.

Winners will be contacted by email from hello@emmadrew.info

Should the Easter hampers be out of stock then a suitable replacement will be found.

How to enter

You can enter by completing as many of the Rafflecopter widget entry options below as you would like. You can also enter daily by tweeting from the Rafflecopter widget.

Comment with your best money saving tip to unlock more entry options.

All of us who wear glasses know how annoying it is when one of the small screws that hold the frames or arms in place comes loose and falls out.

Even assuming you can find the tiny screw, reinserting it is no joke, especially if your eyesight isn’t great (which of course is likely to be the case if you need glasses!).

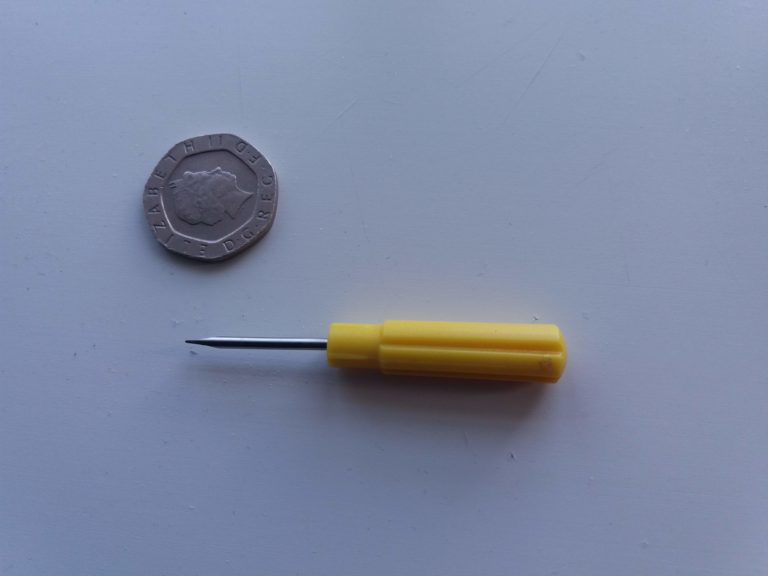

So I was delighted to receive a free review copy of the SnapIt Glasses Repair Kit, pictured below.

The clever thing about this inexpensive kit is that it includes screws with a long ‘tail’ that are easy to insert into the spectacle frame. You then tighten the screw and snap off the protruding tail (hence the name, of course) for a perfect quick repair.

Here’s a step by step illustration of the process. Please excuse the fact that I used an old pair of glasses for this demonstration, so they aren’t exactly in pristine condition!

As you can see, I’m repairing an arm which has come loose. The first step is to insert the screw into the appropriate hole in the frame. You get five different screw sizes to choose from. The long tail on the screw makes doing this a doddle.

Next you use the little screwdriver provided in the kit to screw it in. Here’s a picture with a 20p coin beside it to give you an idea of the size.

It takes just a few moments to tighten the screw, so it looks like this.

Finally you just snap off the tail (easy again). Hey presto, a perfect repair!

Giveaway

As you can tell, I was very impressed with the SnapIt Glasses Repair Kit, so I was delighted to be offered one to give away to my readers. To enter the competition, just follow the steps on the Gleam form below. The more ways you enter, the better your chances of winning!

Good luck in the giveaway. If you have any comments or questions about this article, as always, please post them below.

And if you are a company or agency interested in running a giveaway like this on Pounds and Sense, please do drop me a line.

Disclosure: This is a sponsored post on behalf on SnapIt, who were kind enough to provide a kit to me free of charge and are also providing the prize in my giveaway.

If you enjoyed this post, please link to it on your own blog or social media:

On Pounds and Sense I often talk about the importance of having a diversified investment strategy. And the investment opportunity I am spotlighting today will certainly help you towards achieving that aim!

Raptor is a platform that provides ordinary individuals with the opportunity to invest in the production of gold and precious metal mining. The product on offer is a three-year mini-bond with a tax-free IFISA wrapping. Raptor are currently offering a return of 8 percent per year on a minimum £2,000 investment.

Table of Contents

What Is An IFISA?

For those who may not know, IFISA is short for Innovative Finance ISA. IFISAs allow anyone to invest tax-free in authorized ‘innovative finance’ platforms, including P2P lending and mini-bonds.

You can put any amount into an IFISA up to your annual ISA allowance. In the current 2018/19 tax year this is £20,000, which can be divided however you choose between a cash ISA, a stocks and shares ISA and an IFISA. So, for example, you could invest £10,000 in a cash ISA, £6,000 in a stocks and shares ISA and £4,000 in an IFISA. The ISA allowance for 2019/20 will be £20,000 as well, though after that it could change.

Note that under current rules you are only allowed to invest new money in one of each type of ISA in a tax year. It is though generally possible to transfer money from one type of ISA to another without it affecting your annual entitlement (although there may be platform fees to pay).

How Is Your Money Invested?

The money raised from Raptor IFISA investors is used to provide ‘Stream and Royalty’ finance for mining companies. This is explained in detail in the Raptor IFISA brochure, but briefly Raptor’s investment arm (Raptor Capital International, or RCI for short) makes payments to carefully selected development-stage mining companies to purchase part of their future production at a price below the market level.

The mining company therefore receives much-needed capital through immediately monetizing part of its future production, and investors get the opportunity to make a good return on their investment. Stream and Royalty Finance is still relatively new, and with many high-quality mining projects requiring financing there is an opportunity for investors to capitalize on this.

What Are The Returns?

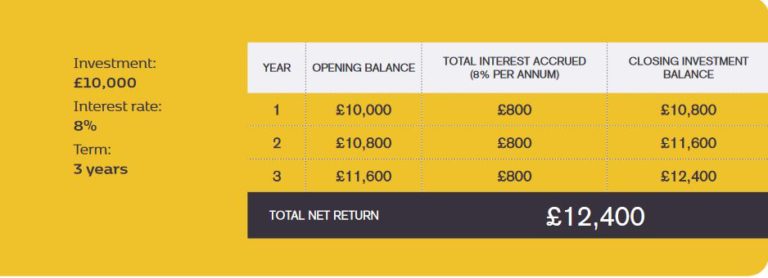

The Raptor IFISA pays 8% interest per year for the three-year term of each bond, with a minimum investment of £2,000. As it’s an IFISA, all profits are paid without any deductions for tax. There is also no charge for investing in the Raptor IFISA.

Returns are paid as simple interest, as shown in the diagram below, which has been copied from the Raptor IFISA brochure. All capital and interest is returned at the end of the three-year term (or earlier if the bond is repurchased/redeemed by Raptor before this point).

What Are The Risks?

All UK IFISA providers have to be authorized by the Financial Conduct Authority (FCA) and HMRC. This doesn’t in itself protect investors against the failure of a platform, however. While savers with UK banks and building societies are covered by the government’s Financial Services Compensation Scheme (FSCS), which guarantees to reimburse up to £85,000 of losses, this does not apply to IFISA platforms (or stocks and shares ISAs, for that matter).

IFISA investors don’t therefore enjoy the same level of protection in the UK as bank savers. This is, of course, a major reason why the returns on offer are significantly higher. It’s therefore important to be aware of the risks and ensure you are comfortable with them before investing this way. It’s also important to invest across a range of asset classes and sectors, and not make the mistake of putting all your eggs in one investment basket.

In addition, the Raptor IFISA is not a liquid investment. Your money will normally be tied up for three years. Raptor say they will assist investors if they want to sell or transfer their bonds to another investor, but there is no guarantee that a buyer will be found. This opportunity is therefore not suitable for funds you might need back quickly and should be regarded as a medium- to long-term investment.

Finally, there is of course a risk that the underlying mining investments will not pay off. However, Raptor and RCI’s Advisory Committee say they will undertake extensive due diligence and engage third-party providers to assist in determining whether or not projects meet and qualify for financing in accordance with set criteria, for example:

There has to be at least a 200,000 ounce gold resource (or gold equivalent ounces).

Uncomplicated metallurgy, allowing simple, conventional, traditional extraction.

Payback of initial capital and interest within three years of production.

Access to mining company financial records.

Allow an RCI agent on site to oversee operations.

With all that said and done, there is no guarantee that you will receive the advertised returns. It is important that you understand and are comfortable with the risks involved.

Summing Up

If you are looking for a home for some of your money that can offer better interest rates than banks and building societies – and won’t incur any tax charges – the Raptor IFISA is worth considering.

As well as higher interest rates, Raptor bonds can add diversity to your saving and investment portfolio, helping you ride out peaks and troughs in the financial markets. The bonds provide an opportunity to profit directly from the returns to be made in precious metal mining, a sector under-represented in many people’s portfolios. The relatively low minimum investment of £2,000 and absence of any charges are further attractions. Just be sure that you are aware of the risks involved, and that you invest only as part of a diversified portfolio.

For more information, please visit the Raptor IFISA website. You can find out more about the investment opportunity there, and also download an informative 14-page brochure.

Disclosure: this is a sponsored post on behalf of the Raptor IFISA. All investments carry a risk of loss. Be sure to do your own ‘due diligence’ before investing, and speak to a qualified professional financial adviser if in any doubt before proceeding.

If you have any comments or questions about this post, as always, feel free to post them below.

If you enjoyed this post, please link to it on your own blog or social media:

I know quite a few Pounds and Sense readers have an interest in writing, whether for pleasure or profit (or both). So today I thought I would share some information about an invaluable free resource for writers and aspiring writers.

Best Writing Forum is a discussion forum for writers that was set up by my old friend (and former publisher) Karl Moore a year ago. It was created in response to requests from members of My Writers Circle, another online forum I helped set up with Karl and managed for almost ten years.

In the last few years My Writers Circle has changed ownership several times and been rather neglected. So in response to members’ requests, Karl set up the new forum as an alternative place for writers to share their work and get feedback and advice.

Best Writing Forum uses the popular SMF messageboard software. Anyone who was ever a member of My Writers Circle will find it quite familiar, therefore. Of course, the board names and overall design are a bit different, but most people soon get the hang of it. And if you have any problems, there is a dedicated volunteer moderator team on hand to help you out.

If you have any interest in writing, I highly recommend that you check out Best Writing Forum. And if you like what you see, please do sign up. It’s free of charge and only takes a few moments. You will then be able to:

get feedback from fellow writers across the world in Review My Work

Talk about poetry and get comments on your own in Poets Corner

Now is a great time to join Best Writing Forum, as it’s still quite new and you really can play a part in helping guide its future direction. I’ll hope to see you there soon!

Note: this is an updated version of an original article about Best Writing Forum first published on my Entrepreneur Writer blog in December 2017.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my friends at Suttons, a leading seeds, bulbs and horticultural products company.

There is a lot of discussion about saving money before you retire, but not nearly as much about saving afterwards.

But in reality the great majority of us have to survive on a lower income in retirement. While nobody wants to spend their golden years scrimping for every penny, saving money in retirement is important and helps us to afford things such as holidays that can enrich our lives.

So this guest post sets out some great ideas for painless ways of saving money in retirement. I hope you enjoy reading it.

For many of us, we dream of retirement. The ideal age for packing in work is 57, according to studies, with 32% of respondents planning to quit the working world at this age. However, for some, the thought of calling it a day before they’re eligible for their state pension isn’t feasible. It’s been estimated that the British public will need at least £260,000 to retire without money issues. Unfortunately, research has found that the average pot of money held by those aged between 45 and 54 is £71,240 — way off the final required total.

While this final figure sounds extremely high, there are ways to prevent overspending in your later years. Here, we take a look at some great ways to save money after you’ve retired.

Table of Contents

Sell your clutter

We are a nation of hoarders. Whether it’s old equipment or new purchases, we don’t like to get rid. In fact, over half of the UK’s adults claim to have between one and 10 items hanging in their wardrobe which have never been worn. However, one man’s junk is another man’s treasure, right? Therefore, clear out any unnecessary clutter you may have acquired over the years.

Have a huge clear out and you’ll be surprised at how much stuff you don’t actually need if you’re ruthless. This can help to provide extra funds to go towards your retirement pot. It means that you’ll be increasing your income, and you won’t even have to make too many cuts from your lifestyle. You can sell your stuff via online auction houses such as eBay and local Facebook groups.

Grow crops

Growing produce at home has many benefits. We all know that eating fruit and vegetables is good for you due to them being full of vitamins, minerals and nutrients. However, have you ever stopped and thought about how much money you can save if you grow your own veg? If your garden is big enough, you should create a vegetable plot. This can include cabbages, lettuce, onions, sweetcorn, leeks and the likes.

You should also look into companion planting. For example, grow Swiss chard in the same space as onions, beetroot and cabbages and you’ll make the most of your space while also deterring pests. A patio garden can also grow smaller produce, including mange tout, radish and French beans.

Some of the most cost-effective vegetables you should look to grow in your garden include tomatoes. As they don’t require much space to grow, you can even place these on balconies. Usually, they take 12 weeks before they are ready for harvest and each plant can create fresh produce daily for up to six years. Based on a shopper buying one box of tomatoes per week, this can help you save £52 each year.

Potatoes are another money saver. The average Brit eats 429g of potatoes every week and the average four-pack costs £1 in a supermarket. However, for a pack of five seeds, you can grow up to 45 potatoes for as little as £1.50.

Of course, there are many other examples that can save you money, and it all tallies up when put together to make great savings.

Adjust the frequency of luxuries

You don’t have to stop enjoying yourself to save money in retirement. It’s no use retiring just to sit and be bored. However, it’s important that you plan properly and adjust your lifestyle to suit your budget. We all like the occasional blow out — whether that’s on a holiday, fine dining or on new items. However, it’s crucial to live within your means. If you were used to eating out every other night when you were in employment, chances are you won’t be able to once you’ve left the workplace. However, you shouldn’t cut it out altogether. Simply adjust the frequency you do so and you’ll still be able to have that luxury that you long for.

Set priorities

Having a budget doesn’t mean removing the items or adventures that are most important to you from your life. However, it is important to set yourself priorities. Decide what it is that you really want in your life and what are just added bonuses. Doing this can help you to prioritise your money, while ensuring you don’t miss out on what you really want in your life.

The above are all examples of how to save money once you’ve retired. Of course, there are many other opportunities for you to make the most of your retirement, but by focusing on these points, you’ll be well on your way to enjoying your relaxing time after finishing work for good.

Thank you to Suttons for an interesting and thought-provoking guest post.

I definitely agree with the advice to grow tomatoes. I have been doing this for a few years now, in growbags and/or hanging baskets. Despite my distinctly un-green fingers, they never fail to produce a bumper crop of tasty toms, and save me having to buy any from the shops for months on end. Suttons have lots of varieties of tomato seeds available. Or if you prefer you could visit a garden centre such as Dobbies and perhaps take advantage of their Over 60 Meal Deal as well!

As always, if you have any comments or questions about this article, please do post them below.

Today I’m spotlighting an opportunity anyone can use to make a substantial sideline (or even full-time) income.

Deal arbitrage is a relatively little-used approach to online auction trading (although as I’ll explain you don’t necessarily have to use online auctions at all).

While most online auction traders buy in bulk from wholesalers (and hope they aren’t left with crateloads of unsellable products), deal arbitrage is a relatively low-risk method that proceeds (initially at least) one item at a time.

The method involves buying products being sold cheaply in sales and special deals, then selling them on at a higher price once the promotional period is over.

It’s a method that can work particularly well at this time of year, when merchants both online and offline are discounting to improve their balance sheets, make room for fresh lines and boost interest in their stores.

A wide range of popular products can be used for deal arbitrage. Those with the best potential include electronic goods of all kinds, fashion, footwear, jewellery, watches, mobile phones, cameras and computer games. Lower-priced products such as books, CDs and DVDs can also be used, though your profit per deal is (of course) likely to be lower.

I recommend focusing on one particular product category initially as you build your expertise in deal arbitrage, but once you’ve done this there is no reason why you shouldn’t diversify to other areas as well.

Table of Contents

A Four Step Plan

Deal arbitrage is a very simple process. It can be broken down into four main steps. These are: (1) identify suitable deals, (2) check they can be sold at a profit, (3) buy them, and (4) sell them at an online auction site or elsewhere.

Let’s look at each of these steps in turn.

Identify Suitable Deals

There are many places you can find deals. Starting in the real (physical) world, you could simply take a stroll down your local high street and make a note of any good deals you see advertised.

In general you shouldn’t buy there and then, but research the products online when you get home and see what prices they are selling for elsewhere. I will discuss this in more detail when we get to step (2), of course.

If you want to research which stores currently have sales and promotions running, a good place to start is the Money Saving Expert website, run by personal finance guru Martin Lewis. Click on https://www.moneysavingexpert.com/deals/high-st-sales-diary/ and a new page will open listing current (and forthcoming) high street sales, including both online and offline stores.

Other websites with up-to-the-minute information about deals and promotions include Hot UK Deals and Offer of the Day.

Of course, you can also source some great deals from websites directly. Two I especially recommend are Amazon and the UK’s number one online auction site, eBay.

For sourcing potential arbitrage deals on Amazon, click on Today’s Deals near the top of the Amazon homepage. Pay particular attention to the ‘Lightning Deals’ advertised here, as there are some great discounts to be had. When I checked just now they were advertising the Tacklife Digital Tyre Inflator for £8.47, a 79% discount on the normal price of £39.59. Lightning deals only last a day or two, so you won’t have long to wait before you can put your purchase up for resale.

The Amazon Discount Finder on the Money Saving Expert website is another great tool for finding bargains on Amazon. Just enter the product you want to buy and the discount you are looking for and see what it comes up with.

There are lots of great deals to be found on eBay as well. Like Amazon it has its own dedicated deals page, which you can access by clicking on Daily Deals at the top left of the eBay homepage. Some of the discounts on offer here are better than others, but they include some real bargains with great profit potential.

In addition, there many ‘hidden treasures’ on eBay that casual browsers never see. These particular deals are not intentional special offers, but rather the result of errors made by vendors in their listings.

An example is where someone puts an item up for sale but misspells the brand name. This means visitors searching for that brand using the correct spelling won’t find it, and the item is therefore likely to sell for a lower price than it should.

A free tool I recommend for unearthing this type of deal is BayCrazy. This has a range of features to help you find products available on eBay UK at ultra-low prices.

For example, if you select Misspelt from the BayCrazy menu and enter a brand name, the site will display any listings with possible misspellings of that name. So when I entered Accurist, it came up with a listing for a luxury watch where the brand name had been misspelt Acurist. Not surprisingly, there had been no bids on the item in question.

BayCrazy also has search tools for other potential bargains. These include auctions ending soon with no bids, night-time bargains (where auctions end in the middle of the night when nobody is likely to be around), and local offers (where buyers have listed items for collection only, which means only people living nearby are likely to bid).

BayCrazy is an invaluable tool for deal arbitrage. It is well worth taking a little time to explore the site, and adding it to your Favorites list.

Check Items Can Be Sold at a Profit

Before buying any item for deal arbitrage, you should of course check that you will be able to make a profit on it.

As it’s most likely you will be selling your product on eBay, your first step should be to search their current listings using the search box on the homepage.

Check how many results come up, how much interest the auctions generate, and what level the bidding typically reaches. If there are any Buy It Now auctions, make a note of the price being asked. This should help you assess what is considered a reasonable price for this particular product.

Of course, it won’t tell you whether the vendor actually achieves this price, so you should also search completed auctions. This is easy as well on eBay. Start by doing a general search as above, but then scroll down the left-hand menu until you reach the heading Show Only and click the box next to Completed. The results list will change to show completed auctions only.

These searches should give you a good idea of the ‘going rate’ on eBay, but many products can of course be bought elsewhere as well. So in addition it is important to check the best prices currently available to buyers using a shopping comparison tool such as Kelkoo. You can also search on Amazon to see if the item is sold there, and if so for how much.

Ideally, of course, what you want is a product that is in demand and regularly sells at a price which will allow you a decent profit. It should not be available for a cheaper price at Amazon or elsewhere, and neither should there be so many other sellers that it will be difficult to ensure that your own auctions stand out.

Buy Items at the Best Price

If all is looking good, your next step will be to buy the item at the best (i.e. cheapest) price you can achieve.

If you’re buying from a store where the item is on a promotion, this is pretty straightforward, of course. Even so, you may be able to boost your margins a bit more by buying with a cashback credit card, where you get a small percentage of the purchase price back. You could also try haggling, of course.

For many online stores (and some offline) you can also get money back on your purchase by signing up with a cashback site such as Top Cashback and visiting the merchant’s website via a link from the cashback site.

If you’re buying through an auction listing, it’s a little more complicated. Here are a few quick tips to ensure you purchase at the best possible price.

Don’t bid till the last minute.

Work out the most you are willing to pay and bid this amount. You may still get it cheaper than this if nobody else bids.

Add a few pence to your top bid, e.g. £20.15. If someone comes in at the last minute and bids £20, those few pence will ensure that you still win the auction.

Consider using auction sniping software to place your bids at the last possible moment. There are plenty of free or low-cost services you can use. The Goofbid free sniping tool is a personal favourite of mine. You can access it at www.goofbid.com/free_ebay_sniper.html.

Sell Your Purchase for a Good Profit

Finally, of course, you will want to sell your product for the best price you can get, which will hopefully generate a good profit for you.

In most cases your best bet is again likely to be eBay. With popular items especially, a bidding war can develop among buyers which pushes prices up.

Psychology also plays a part in this. Many people hate the thought of ‘losing’ an auction, so they end up bidding more than they could pay if they bought the item elsewhere!

Selling on eBay is a relatively straightforward process, and lots of advice is available on the site itself and elsewhere online. Here are some tips to get you started, though.

Always include a good-quality photo of the product, taken against a plain background.

Write a thorough description of the item (you can research this from other auction and online store listings). Double-check that you don’t misspell the brand name!

Ensure that the auction finishes at a sensible time, so there is plenty of competition among would-be buyers at the end. Early to mid-evening is usually best.

Start the auction at low price. You may think this is a risky strategy, but with popular items it will generate much more interest and potentially start a bidding war. The one exception is specialist items (e.g. antiques) which will only appeal to a small minority of individuals, but these are unlikely to be suitable for deal arbitrage anyway.

As I mentioned earlier, while eBay is likely to be the top choice for most arbitrage dealers, other options do exist.

For books, CDs and DVDs, you may get better prices selling as an Amazon merchant. I won’t go into detail about this here, but it is possible to set up as a merchant on Amazon free of charge, and your products will then be available via the relevant Amazon product page. Obviously, for this to work, you must be able to sell your item cheaper than Amazon and still make a profit.

One other option is to set up your own store and sell directly from that. One service you can use for this is the web-based, drag-and-drop Weebly service. Obviously you will have to work harder to convince buyers you are reputable than if selling via eBay or Amazon, but if you become a regular trader it is worth considering.

If your first few deals work out well, you may want to try buying multiple items while they are on promotion for resale later. This can boost your overall profits considerably.

In summary, deal arbitrage is a great way to make a useful extra income for minimum risk and little hassle. And because you can start with just one item at a time, it is very easy to try out and see if it appeals to you.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This post includes affiliate links. If you click through one of these and go on to make a purchase, I may receive a commission for introducing you. This helps cover the cost of running Pounds and Sense. It has no effect on the terms you are offered by the merchant or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

In just a few weeks (5th April 2019) it will be the end of the financial year. And that means if you want to make the most of your 2018/19 ISA allowance, you will need to take action soon.

As you may know, ISA stands for Individual Savings Account. ISAs are saving and investment products where you aren’t taxed on the interest you earn or any dividends you receive or capital gains you make. An ISA is basically a tax-free ‘wrapper’ that can be applied to a huge range of financial products.

With ISAs you don’t get any extra contribution from the government in the form of tax relief as you do with pensions. But – except in the case of the Lifetime ISA – you can withdraw your money at any time (subject to any rules about the term and notice period required) and you won’t be taxed on it.

Everyone has an annual ISA allowance, which is the maximum amount you can invest in ISAs in the year concerned. In the current financial year (2018/19) this is a generous £20,000.

There are four main ISA categories: Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA. You can divide your £20,000 ISA allowance among these in any way you choose, but you are only allowed to invest in one ISA in each category per year. Let’s look at each type in a bit more detail…

Table of Contents

Cash ISA

Cash ISAs are like standard savings accounts except the interest you receive doesn’t incur income tax.

Unfortunately interest rates are very low at the moment. According to price comparison sites, the best rate for an instant-access cash ISA is currently 1.45% with Virgin Money. With inflation at 1.8% (January 2019) that means even in the best paying cash ISA your money will still be losing spending power when invested this way.

What’s more, the new Personal Savings Allowance (PSA) means most people can get up to £1000 in savings interest without paying tax anyway. As a result of these things, cash ISAs have lost much of their appeal, though if interest rates rise they may become more attractive again.

It is also worth bearing in mind that money invested in a cash ISA remains tax-free year after year. So if in the years ahead interest rates on cash ISAs rise, the benefit of having one will increase as well.

Nonetheless, I have decided not to invest any of my ISA allowance in a cash ISA this year, as I have (in my view) better uses for my money. You might see this differently, of course!

Stocks and Shares ISA

Stocks and shares ISAs are a good choice for many people saving long term. Over a longer period the stock market has outperformed bank savings accounts, often by a considerable margin. You do, though, have to expect some ups and downs in the value of your investments in the short to medium term.

You can opt for a standard stocks and shares ISA offered by a wide range of financial institutions and let them choose your investments for you. Alternatively you can use self-investment platforms such as Hargreaves Lansdown or Bestinvest to choose your own investments from the wide range of shares and funds available.

IFISAs are on offer from a small but growing range of peer-to-peer (P2P) lending platforms. P2P platforms allow people to lend money to businesses and private individuals and get their money back with interest as the loans are repaid. If you invest in the form of an IFISA all the interest you receive from P2P lending is paid tax-free, otherwise it is taxed as income (though interest from P2P lending does qualify for the Personal Savings Allowance of up to £1,000 a year, mentioned above).

Peer-to-peer platforms generally offer more attractive interest rates than bank and building saving accounts (or cash ISAs) – from around 4% to 10% or more. They aren’t covered by the same guarantees as the banks and are therefore riskier, though. And if you need your money back urgently there may be delays and/or extra charges to pay.

Nonetheless, in the current climate of low-interest savings accounts and volatile stock markets, more and more people are looking to IFISAs as a home for at least some of their savings.

Some leading peer-to-peer lending platforms which offer IFISAs include Ratesetter – which I have invested in myself and reviewed in this post – and Funding Circle, which lends to businesses.

Lifetime ISA

Lifetime ISAs or LISAs are a new-ish initiative from the government to encourage younger people to save. They do have one big drawback for older people: you have to be under the age of 40 (though over 18) to open one.

LISAs are designed for two specific purposes: buying your first home and saving for retirement. How they work is that you can pay in up to £4,000 a year (lump sums or regular contributions) and the government will top this up with another 25%. As long as you open your LISA before the age of 40 you will continue to receive the bonuses on your contributions until you reach 50.

So if you pay in the maximum £4,000 in a year, the government will top this up to £5,000. If you pay in the full £4,000 every year from the age of 18 to the upper limit of 50, you will therefore get a maximum possible bonus from the government of £32,000.

LISAs are therefore somewhat different from the other types of ISA mentioned above, but nonetheless any money you invest in one comes out of your annual ISA allowance (currently £20,000). So if you pay the maximum £4,000 into a LISA this year, that comes out of your £20,000 ISA allowance, leaving you with ‘just’ £16,000 to invest in other sorts of ISA.

Your money will grow without any tax deductions in a LISA, and you can also withdraw without having to pay tax. However, there are certain restrictions. In particular, you can only use the money in your LISA for one of two purposes: paying a deposit on your first home or saving for retirement. While you can access your money for other reasons, you will then lose 25% of the total, including your own contribution and the government bonus along with any investment growth. That means in many cases you will get back less money than you put in.

The 2018/19 ISA allowance is a generous £20,000 and offers the potential to save a lot of money on tax assuming you are lucky enough to have this amount to save or invest. But, very importantly, it cannot be rolled over. So if you don’t use your 2018/19 ISA allowance by 5th April 2019 at the latest, it will be gone forever. It is therefore important to attend to this now and ensure you get as much value as possible out of this valuable tax-saving concession.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser and cannot give personal financial advice. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

This is a somewhat embarrassing post to write as a money blogger. However, I recently realised that I have been paying well over the odds for my home insurance for some years. And now that I have addressed the issue, I am actually quite staggered by how much money I will be saving.

To explain, I moved into my current home with my partner Jayne (now sadly deceased) in March 1995. With all the things we had to consider at the time we didn’t pay much attention to home insurance. We took out home contents insurance with Lloyds and buildings insurance with our mortgage lender Britannia. The latter had a special deal for members of the trade union Unison (which Jayne was in at the time), so we thought it must represent good value.

We paid for both policies via monthly direct debit and each year they rolled over, generally with a small increase. I always looked after our household finances but never really thought much about the home insurance. The sums weren’t huge, and I just assumed we were getting a good deal so it wasn’t worth worrying about.

Fast forward to January 2019, and Britannia wrote saying they were no longer offering buildings insurance and I would need to make alternative arrangements. At about the same time I got a letter from Lloyds saying my contents insurance was going up from £147.80 a year to £184.73 (a pretty steep increase in percentage terms). So I decided the time had come to pay my home insurance a bit more attention and see if there were any savings I could make by shopping around. And boy, there certainly were!

Doing the Sums

At the start of this year my buildings insurance premiums were £32.05 a month, which works out as £384.60 a year. Adding that to the latest quote from Lloyds of £184.73 gives a total annual home insurance bill of £569.33.

A bit of online research revealed that nowadays many people get their buildings and contents insurance in a single policy and this generally works out more economical. So I did a search for home insurance providers on Top Cashback (a website that provides money back to people buying via merchants listed on the site – see this post for more details).

To cut a long story short, I wound up buying a combined buildings and contents policy from AA Insurance, with essentially the same cover I had before, for an annual premium of just £100.25. And with that I got £42 cashback via Top Cashback, effectively reducing the price to just £58.25. That represented a massive £511.08 less than I would have been paying in total on my old home insurance policies.

The AA Insurance website said that this was a special new customer deal, so I guess they might push the price up a bit next year. But of course, now that I’ve done it once, I will definitely shop around for prices (and cashback!) again when the time comes.

So the moral of this story is not to let laziness and inertia ever stop you looking for better deals. Even with something as mundane and relatively cheap as home insurance, you may be as surprised as I was by how much money you can save!

You can search on Top Cashback for home insurance providers and price comparison services (all offering cashback) by clicking on this link (affiliate). If you aren’t already a member you will need to register to get cashback, but this is free and only takes a few moments.

As ever, if you have any comments or questions on this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media: