A quickie today to let you know that the price of stamps is rising again on Monday 7 October 2024. That is the second price rise this year, after they also went up in April.

On this occasion a standard first class stamp is going up from £1.35 to £1.65, an inflation-busting 22%. The price of sending a large letter is going up even more, from £2.10 to £2.60. That’s an increase of 50p or 24%.

One bit of good news is that the price of sending a standard or large letter by second class post is not increasing this time. That remains at 85p and £1.55 respectively.

Standard letters can weigh up to 100g and measure a maximum of 24cm x 16.5cm x 5mm. Large letters can measure 35.3cm x 25cm x 2.5cm but still have to weigh under 100g. If they weight over 100g, higher rates apply, and if they weigh over 750g they have to go at parcel rates.

The cost of many of Royal Mail’s ‘Signed For’, ‘Special Delivery Guaranteed’ and ‘Tracked’ services will also rise from 7 October, as will the price of sending parcels first and second class. You can see a full list of prices by clicking here (PDF).

Saving Money on Stamps

So is there anything you can do to mitigate the impact of the latest price rises?

Well, my number one recommendation is to stock up now while stamps are still at the old price. Standard and large-letter stamps don’t have values printed on them and will still be valid after the October price rise comes in. If you can afford to buy (say) 100 standard first-class stamps and 100 large letter first class stamps, that will save you an impressive £80 in total.

The best bet for buying stamps is – of course – your local post office. If you don’t have one near at hand, however, you can also buy in bulk from The Royal Mail Shop (minimum order £50 for free delivery)..

Amazon also sell postage stamps, though costs vary and when I checked some prices were significantly higher than at post offices. But they may be worth a look, especially if you are an Amazon Prime member.

Another option you could consider is the online auction site eBay (search for “new UK stamps”). There can be good savings to be made here, but check reviews and ratings carefully and be wary of offers that are clearly too good to be true.

For the sake of completeness, though, I thought I should publish (or more accurately republish) a post about matched betting. This is something I did for several years and earned about £3,000 (tax-free!) from. I am not doing it as much these days, for reasons I’ll explain below. But if you’ve never done it before, I do still recommend matched betting as a way of making some quick tax-free cash.

Table of Contents

So Why Am I Doing Less?

There are two main reasons. The first is that since I started matched betting around six years ago I have had my account restricted (or gubbed, as we say in the business) by many online bookmakers. That obviously makes it harder to take advantage of the offers matched bettors need in order to generate their guaranteed profits.

My second reason is that during the pandemic, with many sporting events cancelled, there were far fewer matched betting opportunities. Thankfully that is behind us now and normal life (more or less) has resumed. Even so, the bookies are more cautious than they once were, and offers are somewhat thinner on the ground.

I still do a small amount of matched betting but keep it very low-key. There are only a few good online bookmakers I can now use, and I’d like to go on flying under their radar for as long as possible before they ban me!

If you are new to matched betting – or have let it fall by the wayside – then as stated above I do still recommend it. But be aware that it may not be quite as profitable as it was pre-Covid.

But let’s start with a recap of the basics…

What is Matched Betting?

Matched betting is a method for making risk-free profits by taking advantage of offers made by online bookmakers.

The best offers are those made to attract new clients. Here’s an example. The bookmakers Sky Bet offer £30 in free bets (3 x £10) for new online customers. To get this, you have to open an account with them and deposit a minimum of £5. You then have to place a minimum 5p bet at odds of evens (2.0) or better. Once you have done this, Sky Bet will immediately credit you with £30 worth of free bets.

So how do you turn this into a guaranteed profit? Well, that’s the clever bit. You make use of a website called an exchange (Smarkets and Betfair are two of the better known). These sites allow anyone to lay a bet (i.e. bet that the outcome in question won’t happen). By backing with a bookmaker and laying the same bet at an exchange you can ensure that however the event pans out, you will only make a small loss or occasionally a tiny profit (depending on the odds available).

With a normal bet this is obviously of limited value, as the two bets more or less cancel each other out. But when your first bet qualifies you for a second (and in Sky Bet’s case much larger) free bet, it suddenly becomes a lot more interesting. Here’s an example…

Let’s say Wolverhampton Wanderers are about to play Spurs in the Premier League. You can back Wolves to win with Sky Bet at 4.75 (15/4 in the more traditional but less useful fractional style) and lay them with Smarkets at 4.80. If you put £5 on Wolves with Sky Bet and at the same time lay Wolves to the appropriate stakes (something I’ll come to shortly) you can ensure that whether they do or don’t win, your net loss will be just 13p (allowing for Smarkets’ standard 2% commission charge). The lay bet covers you for the draw as well, as in effect you are betting that Wolves won’t win – so if Spurs win or the match ends in a draw, the lay bet will pay out.

But now, because you are a new member, Sky Bet will give you £30 worth of free bets. You can back and lay these again to generate a guaranteed profit. For the sake of simplicity let’s say you use the same market, Wolves v. Spurs, although you certainly don’t have to. At the odds mentioned, and backing to the correct stakes, if you use all three £10 free bets you can guarantee yourself a net profit of £23.05 however the match pans out. Subtract the 13p loss from your qualifying bet, and once the dust has settled you will have made a risk-free (and tax-free) £22.92. If your bet loses with the bookie, your profit will be in the exchange (remember, this is a free bet so it hasn’t cost you anything). If the bet wins at the bookie, you will lose money at the exchange, but your winnings with the bookie will exceed this, giving you the same net profit either way.

Those are the bare bones of matched betting. Of course, there’s more to it than that, but most matched betting opportunities boil down to this. You place an initial qualifying bet and lay it to ensure (at worst) a small net loss, and then back and lay the free bet you receive to make yourself a guaranteed profit.

One or two people have asked me whether matched betting is legal. The answer is a clear yes. It’s fair to say the bookies don’t like it, though. And if they suspect you are doing it, they may close or limit your account. As mentioned above, this is called ‘gubbing’ and it is an occupational hazard for matched bettors. As a matter of interest, I had to change the example used at the start of an earlier version of this blog post after being threatened with legal action by the bookmaker in question.

How Do You Get Started?

You can, of course, do all this yourself, researching opportunities and comparing odds to find the most profitable matched betting opportunities. When you are starting out, though – and especially if you are new to online betting – it obviously helps a lot to get some instruction and guidance.

Fortunately there are some excellent online services that will do all this for you and provide step-by-step instructions. You can apply these even if you have never placed a bet in your life before. Here’s the service I recommend for beginners to matched betting…

Outplayed

Outplayed (formerly Profit Accumulator) is a dedicated matched betting website. You can get a 7-day free trial which gives you access to over 60 welcome offers of the type mentioned above. If you wish to continue, you can then pay a fee (currently £39.95 a month) to become a ‘Platinum’ member and get access to Outplayed’s full range of betting offers and services.

As well as detailed instructions on offers, Outplayed also provide various online tools you can use. Their oddsmatcher, for example, helps you find markets where the back and lay odds are as close as possible, so you can minimize your losses on qualifying bets and maximize the value of your free bets. They also have calculators where you enter the back and lay odds and how much you want to bet at the bookmaker. The calculator then reveals how much you need to lay at the exchange to guarantee a set profit (or qualifying loss) with either outcome.

A further advantage of joining Outplayed is that you get access to the members-only community forum, where you can get any questions you may have answered by more experienced members and/or the Outplayed team.

For more information about Outplayed and its different membership levels, just click through this link [affiliate].

If you are at all sceptical about the Outplayed service, you might like to check out the reviews on the independent Trust Pilot website. They currently average 4.7 out of 5 stars, with 89% of respondents awarding them a five star (‘Excellent’) rating. That is among the highest average ratings I can recall seeing on Trust Pilot.

What Happens When You’ve Exhausted the Welcome Offers?

This was something I wondered about before I started, and I know other people do as well.

First of all, it will take you quite a long time to work through all the offers on the Outplayed website. Not all are as simple and straightforward as the Sky Bet offer mentioned above, but nonetheless if you follow the step-by-step instructions they can all generate a healthy profit for you.

After that, you can move on to ‘reload’ offers. These are offers made by bookmakers for existing members to encourage them to keep coming back and using their service. Reload offers work in a wide range of ways. Some provide a guaranteed profit if you apply them correctly, while others may sometimes make a small qualifying loss but other times produce a much larger profit, generating a good net profit overall. Reload offers are also listed on the Outplayed website and updated every day.

Is Matched Betting for Everyone?

In principle anyone can do matched betting, but it is probably more suitable for some people than others. In particular, it will help if you have a small amount of capital to get started – at least £50, preferably £100 or more.

If you have less you can still do it, but it will take longer to build up your earnings. Remember that you will need money to fund your qualifying bets at the bookmaker sites and also your exchange account. You don’t lose this money – it simply moves between bookie and exchange according to how events pan out – and you can always withdraw it if required. But to operate as a matched bettor you do need to have some ‘working capital’.

Another requirement to make a success of matched betting is that you need to be organized and methodical. Matched betting is not difficult once you grasp the basic concept, but if you make a mistake it is possible to lose money doing it. Initially at least it’s important to take it slowly and steadily and follow the instructions on Outplayed (if you have signed up with them) to the letter. It helps to be reasonably numerate as well, although the actual calculations are done for you by the oddsmatching tool and calculators.

And finally, if you think you might get drawn in to gambling through matched betting, you may be better giving it a miss. This applies especially if you have ever had a gambling problem in the past. To emphasize again, matched betting is NOT gambling if you do it properly and follow the correct procedures. But if you are tempted to go off-piste and start placing random bets, the likelihood is that you WILL lose money overall.

Final Thoughts

If you are looking for a tax-free sideline earning opportunity, matched betting can certainly fit the bill. Done properly it is risk free, and (as mentioned earlier) I have made around £3,000 from it myself.

For reasons discussed in this blog post I don’t recommend matched betting as a substitute for a full-time job. In these challenging times, however, if you need another tax-free string to your money-making bow, it can certainly perform that role. But be aware that the first few months are likely to be the most profitable. After that, as you run out of welcome offers (and are perhaps ‘gubbed’ by some bookies) it will get harder.

As always, if you have any comments or questions about this post or matched betting more generally, please do leave them below.

This is a fully updated version of an earlier post.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

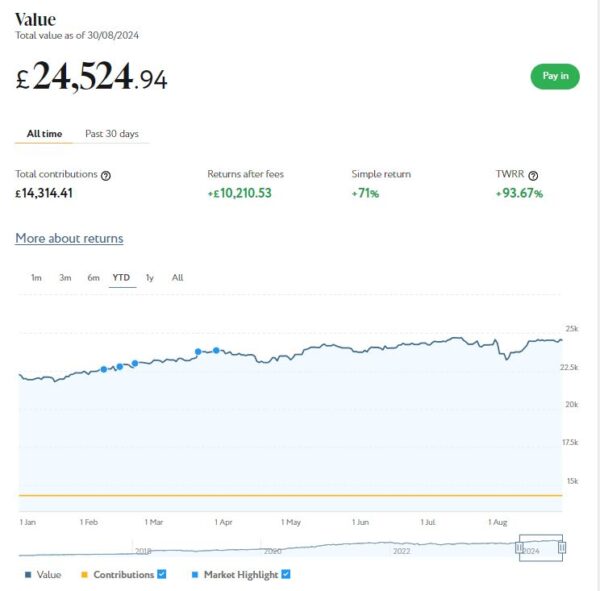

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

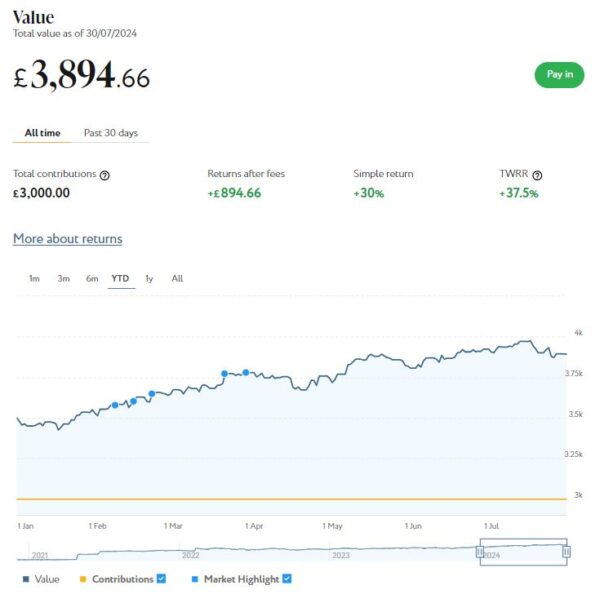

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,525 (rounded up). Last month it stood at £24,237, so that is an increase of £288.

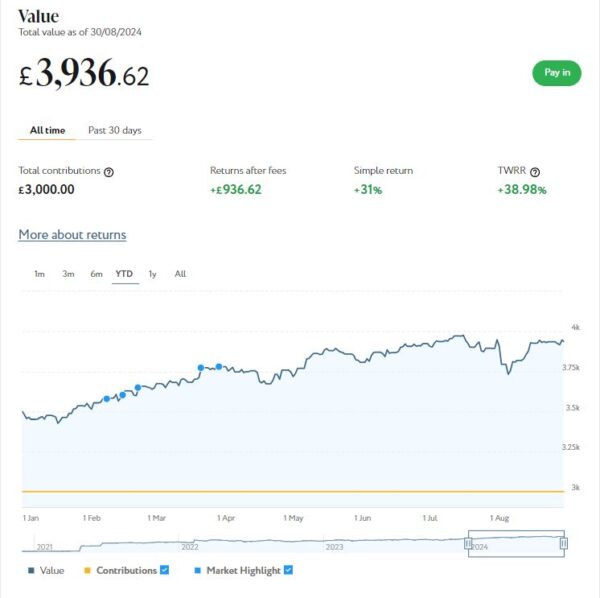

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,937 compared with £3,895 a month ago, a rise of £42. Here is a screen capture showing performance over the year to date.

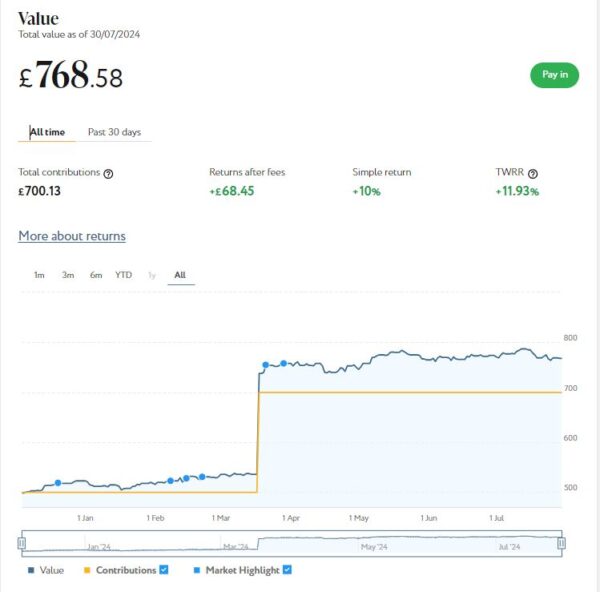

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £772 compared with £769 last month, a small rise of £3.

As you can see from the charts, August was generally a decent month for my Nutmeg investments, despite a hiccup early in the month. Their overall value has risen by £333 or 1.16% since the start of August. They are also up by £2,919 or 11.08% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024 and you have a full £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £200.41 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 6 are breaking even, and the remaining 17 are showing losses. My portfolio of 33 properties is currently showing a net decrease in value of £43.69, meaning that overall (rental income minus capital value decrease) I am up by £156.72. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

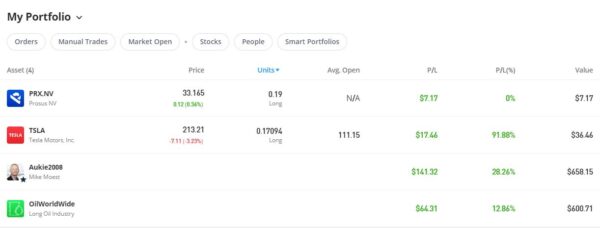

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

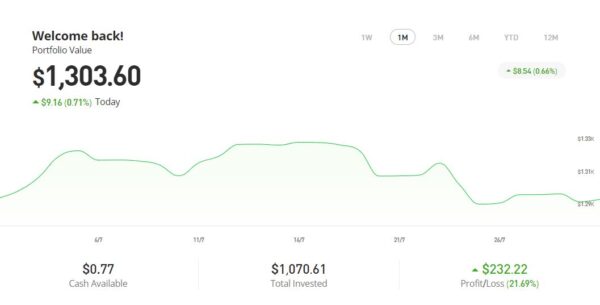

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.27 an overall increase of $281.01 or 27.51%.

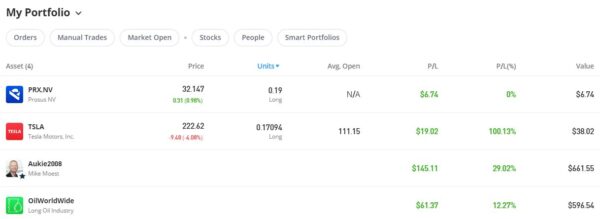

As you can see, my Oil WorldWide investment is showing 12.85% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

You might also notice that I have a small holding in Prosus NV, a Dutch internet group. To be honest I don’t understand how I acquired this, but it may be connected to my copy trading investment with MIke Moest (who is Dutch). In any event, I am happy to have it in my portfolio as well!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in August on the excellent Mouthy Money website. The first is Win Fame and (Maybe) Fortune as a TV Quiz Show Contestant. This can be an exciting and occasionally lucrative pastime. I revealed how to find opportunities and apply for them. I also explained how the auditioning process works, and offered some tips on how to boost your chances of success.

Also in August I revealed my Ten Top Tips for Working From Home. This is something I’ve done for over 30 years now, so in this article I set out my top ten tips based on my experience. If you have recently started working from home, or expect to do so in future, you may find this article helpful.

Finally, I wrote an article titled How Understanding Cognitive Dissonance Theory Can Help Us Manage Our Finances Better. This article drew on my experiences of studying psychology back in the 1970s. Developed by psychologist Leon Festinger in 1957, cognitive dissonance theory explores the discomfort we experience when we simultaneously hold conflicting beliefs or attitudes. By understanding this, we can gain insights into our financial behaviour, helping us make more informed decisions and achieve better financial results.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in August, I particularly enjoyed How to Save Money on Your Home Removal by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in August. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In these challenging times, we all need to ensure our savings stretch as far as possible. So in How to Maximize Your Savings Interest l set out a range of tax-free allowances you can use to help do this. They include the Personal Savings Allowance (PSA), Starting Rate for Savings, Individual Savings Accounts (ISAs), and various others.

I also published How to Win Cash and Prizes in Online Competitions. This can be another tax-free way to boost your finances! In this post I revealed how to find online competitions to enter, why you should set up dedicated ‘comping’ accounts, how to identify potential scams, and more. Good luck if you decide to try this 🤞

As we all know Labour achieved a landslide victory in the general election, and it appears that austerity measures are on the way now. So in How to Reduce the Impact of Tax Rises in Rachel Reeves’ First Budget, I set out some recommended steps to try to protect your finances in the months (and years) ahead. The Chancellor’s first budget is scheduled for 30th October 2024, with tax rises and cuts to public services widely anticipated.

Finally, in August I published What Alternatives Are There to Heat Pumps? The government are currently pushing heat pumps hard in their frantic quest to achieve Net Zero. For a range of reasons, however, they are not suitable for every property. And even if your home might theoretically be suitable, there are good reasons you might not want one (discussed a while ago in this Mouthy Money article). So in this post I set out some possible alternatives you might like to consider instead.

Next, a few odds and ends. I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you decide to invest, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Speaking of energy, a quick reminder that if you switch to EDF via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight the decision by the new Labour government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you have any source of income apart from the state pension, even a tiny one, the chances are you won’t be eligible. I do therefore recommend writing to your MP and asking for this Draconian decision to be reversed. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK. The latter is up to almost half a million signatures now.

That’s all for now. If you have any comments or queries about this update, as ever, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Yes, it’ s time for another exciting giveaway here on Pounds and Sense. This one has a ‘back to school’ theme. In most parts of the UK, of course, this occurs in early September. Scottish schools generally return a bit earlier, around mid-August.

Again I have clubbed together with some of my fellow UK bloggers to provide a plethora of great prizes. And the best news is, it’s entirely free to enter. The giveaway is open now and will close on September 1st 2024.

The prizes have been hand-picked for children and young people returning to school this autumn, so they should be ideal for your children or grandchildren. But if you want to keep any for yourself, we promise we won’t tell!

This event has (again) been organized by Rowena Becker, who blogs at My Balancing Act. No small amount of effort has been involved in arranging and co-ordinating it, so many thanks again to Rowena for her hard work and dedication.

Without further ado, then, I’ll hand you over to Rowena to introduce the giveaway…

Back to School Giveaway

Get ready for an exciting opportunity as some of the top UK bloggers unite to bring you a fantastic back-to-school giveaway! We’ve teamed up to offer one lucky winner a fabulous collection of school essentials that will make heading back to the classroom a breeze.

From stylish lunch bags and durable water bottles, to school shoes and jackets, this giveaway promises to equip you with some great goodies to kick off the school year in style. Join us in this collaborative celebration and enter for your chance to win these amazing prizes. Let’s make this school year the best one yet!

In order to be able to bring you this incredible giveaway, some of the UK’s top bloggers got together. A massive thank you to all involved! The bloggers taking part are:

Start-Rite Shoes is giving one lucky winner the chance to win a pair of school shoes for their child.

The foundation of any school uniform is a quality fitted pair of shoes, but there is nothing uniform about a Start-Rite school shoe! With 12 new styles added to their school shoe collection this season, Start-Rite is more prepared than ever to protect your children’s feet. No one size fits all, as every pair of feet has individual requirements to ensure healthy physical development.

Whether you’re looking to support wide or narrow feet, a high instep, or shoes that double for a special occasion, Start-Rite has a style to suit every child.

EcoSplash Fleece Lined Jacket Navy from Muddy Puddles

Gear up for the ultimate back-to-school season with Muddy Puddles’ in our back-to-school giveaway! Included in the prize bundle is a top-tierkids waterproof jacket that ensures your young adventurers are ready for any weather.

This navy raincoat features an impressive waterproof rating of 10,000mm to keep your child dry during heavy downpours, perfect for rainy days. Crafted from durable, breathable fabric made from recycled plastic bottles, it’s both eco-friendly and long-lasting. The soft fleece lining provides extra warmth, while the jacket’s design makes it easy to layer across various seasons. Fully taped seams offer robust protection against the elements, and reflective details enhance visibility in low-light conditions for added safety. Plus, it’s machine washable at 30 degrees for easy care.

Muddy Puddles has your kids covered for back to school with theirback to school jackets, waterproofs, and more—ensuring every rainy walk to school, puddle-jumping session, and chilly playground adventure is tackled in style and comfort!

Smash lunch bag and water bottle set

Gear up for the school year with an essential lunch bag and water bottle set! TheSmash Lunch Bag is your kids perfect lunchtime companion, designed with full insulation and an antibacterial lining to ensure their meals are as fresh as possible. Made from premium neoprene, this lunch bag is not only fully washable but also brings a splash of personality and fun to every meal.

Stay hydrated in style with theSmash Twin Wall Soda Bottle. Made from durable stainless steel, this sustainable bottle features a sleek design and a removable cap, making it an ideal everyday accessory. It’s BPA-free, food-safe, non-toxic, and offers a smart, twin-walled construction.

Create-a-Space™ Storage Centre from Learning Resources

Introducing a stylish addition to any back-to-school setup: the Create-a-Space™ Storage Centre from Learning Resources, which is part of our exclusive giveaway prize bundle! Perfectly blending modern design with practicality, this white 10-piece set will seamlessly fit into any décor theme, whether at home or in the classroom.

The carousel-style design features 8 removable containers, providing the perfect solution for organising essentials like glue sticks, crayons, pens and more. Keep your workstation clutter-free and enjoy a space that is as functional as it is chic with this versatile storage centre.

LittleLife Flip-Top Water Bottle!

Family active outdoors brand, LittleLife, is giving one person their choice of aflip-top water bottle, perfect for the school day.

Made from impact-resistant Tritan copolyester, a watertight lid and holding 550ml, these bottles are durable and fit fuss-free into your child’s school rucksack or backpack. LittleLife’s water bottles also come with a chew-resistant straw to avoid lingering tastes and odours due to being BPA-free.

Brainstorm Toys Children’s 14cm Desktop World Globe

Discover new horizons with the Brainstorm Toys Children’s 14cm Desktop World Globe, a shining star in our back-to-school giveaway prize bundle! This compact yet high-quality globe is a treasure trove of knowledge, showcasing detailed political boundaries, natural wonders like lakes, rivers, and deserts, as well as capitals and major cities.

Perfect for curious minds, this globe is ideal for home or school, making it a must-have for any aspiring explorer. The sturdy base ensures stability, while its easy rotation allows young adventurers to seamlessly explore different areas of the world. Enhance your child’s learning experience and ignite curiosity with this engaging educational tool.

Little Brian Scribble Paint Sticks

Unleash your creativity withScribble Paint Sticks by Little Brian, a standout addition to our giveaway prize bundle! These innovative paint sticks are perfect for adding intricate details and patterns to your artwork, thanks to their finer tip. Featuring 12 vibrant classic colours, they bring your child’s artistic visions to life with ease. Enjoy a mess-free painting experience where paint twists up and down just like a glue stick and dries in under 60 seconds. Whether you’re working on paper, card, wood, or glass, these versatile paint sticks make it simple to explore your creativity without the clean-up hassle.

How to Enter

You can enter this Back to School Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collated, and one winner will be randomly chosen via Rafflecopter.

The giveaway will run from 4 pm 23rd August 2024 to 8 pm 1st September 2024.

The winner will be notified by email from rowena@mybalancingact.co.uk

The winner will have 7 days to respond, after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, X, YouTube, BlogLovin or Pinterest or any other social media platform.

Prizes open to over 18s only. Age verification may be required to receive some prizes.

Some or all of the prizes may take a few weeks to arrive.

If any prizes are out of stock then we will do our best to find a suitable replacement but cannot guarantee it.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage.

Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace such items.

In the unlikely event that one of the companies withdraws a prize, we cannot offer an alternative.

The winner’s name will be stated on some or all of our bloggers’ websites and announced on Twitter/X and other social media channels. It will also be displayed on the Rafflecopter entry form. By entering this prize draw, you give your permission for this.

Please note the winner may have the same name as you so if you see your name displayed, be aware that you are not the winner unless you have been notified by us.

There may be some delays in receiving prizes.

Good luck, and I hope a Pounds and Sense reader wins this fabulous prize bundle!

Note: This post (and others on Pounds and Sense) includes affiliate links. If you click through and make a purchase or perform some other specified action, I may receive a commission for introducing you. This will have no effect on the product or service you receive or the price you pay for it, but it does help me pay my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

The first budget under new Labour Chancellor Rachel Reeves is scheduled for Wednesday 30 October 2024.

Speculation is rife about potential tax rises aimed at addressing the country’s economic challenges. But while tax increases appear inevitable, there is still time to take proactive steps to minimize their impact on your finances.

Here are some tips for how to prepare for and reduce the burden of potential tax hikes.

1. Maximize Tax-Efficient Savings and Investments

One of the most effective ways to protect yourself from higher taxes is by taking full advantage of tax-efficient savings and investment vehicles. These include:

ISA Allowances: The annual ISA (Individual Savings Account) allowance is currently £20,000. Money saved in an ISA grows tax-free, meaning you won’t pay any income tax, dividend tax or capital gains tax (CGT) on any profits made. As well as Cash ISAs, you can invest in Stocks and Shares ISAs and Innovative Finance ISAs (IFISAs).

Personal Savings Allowance (PSA): Basic rate taxpayers can earn up to £1,000 in savings interest tax-free. Higher rate taxpayers get a reduced allowance of £500.

Starting Rate for Savings: For those with a low overall income, the starting rate for savings can be especially beneficial. If your total income (excluding savings interest) is less than £17,570, you may qualify for the starting rate for savings, which can provide up to an additional £5,000 in tax-free interest. This is discussed in more detail in my recent post How to Maximize Your Tax-Free Savings Interest.

Venture Capital Schemes: For those willing to take more risk, schemes like the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) offer significant tax reliefs, including income tax relief and capital gains tax exemption on profits.

2. Diversify Your Investments

Diversification remains a cornerstone of sound investment strategy, especially in times of political and economic uncertainty. By spreading your investments across different asset classes – such as equities, bonds and property – you can reduce the risk of any single investment adversely affecting your portfolio. Consider international diversification as well to hedge against possible downturns in the UK economy.

3. Consider Using a ‘Bed and ISA’ Strategy

If you hold a lot of investments outside an ISA or other tax shelter, this can be a good strategy to reduce your tax liability.

Bed-and-ISA involves selling taxable stocks and shares and then repurchasing them within an ISA wrapper. This allows you to transfer investments into a tax-protected environment, where future gains and income will be sheltered from tax. Note that you cannot transfer taxable stocks and shares directly into an ISA, but Bed-and-ISA performs the same function.

On the minus side, Bed-and-ISA may incur some costs in terms of transaction fees and any difference (spread) between selling and buying prices. You may also become liable for CGT if any profits realized exceed your annual tax-free allowance. The long-term benefits can be substantial, however. This applies especially if – as seems likely – tax-free CGT allowances are reduced and the rates payable are increased. Of course, the Conservatives started doing this when they were in power.

4. Rebalance Your Portfolio Towards Tax-Efficient Assets

Different types of investments are subject to different levels of tax. It’s important to rebalance your portfolio to favour assets that could be less impacted by tax hikes.

Dividends: The tax-free dividend allowance for 2024/25 is £500, and anything above this is taxed at rates of 8.75% (basic rate taxpayers), 33.75% (higher rate), and 39.35% (additional rate). If dividend tax rises further, you may want to limit investments in dividend-paying stocks outside of tax-free wrappers like ISAs and pensions (see above).

Capital Gains: The capital gains tax (CGT) allowance has dropped to £3,000 for the 2024/25 tax year, and there are fears it could be cut further. Consider selling assets to crystallize gains while you can still use your allowance, or shift investments into tax-free vehicles like ISAs using the ‘Bed and ISA’ (or ‘Bed and Pension’) strategy discussed above..You can also offset capital gains with capital losses. If you have investments that have performed poorly, selling them to realize a loss can help offset gains elsewhere in your portfolio. Remember that CGT only applies when a profit (or loss) is actually realised.

Bonds: Government and corporate bonds are often seen as lower-risk investments and may be less vulnerable to tax increases than equity income streams. You might want to consider including more bonds in your portfolio.

Commodities: Gold and other commodities have traditionally been seen as a safe haven in times of economic upheaval. There are risks, however, and it’s important to do your own ‘due diligence’ and seek professional advice before going down this route.

5. Use Your Pension Allowance

Pensions are one of the most tax-efficient ways to save for the future. Contributions receive tax relief at your marginal income tax rate, which means for every £100 you contribute, the government effectively adds £20 for basic-rate taxpayers, £40 for higher-rate taxpayers, and £45 for additional-rate taxpayers.

Consider increasing your pension contributions to mitigate the impact of other tax rises. Just be sure to keep within the current £60,000 annual pension contribution limit. Note that for those earning over £260,000 (adjusted income), the tax-free allowance tapers. More info about this can be found on the government website.

If you’re self-employed, consider setting up or increasing contributions to a private pension or Self-Invested Personal Pension (SIPP) to take full advantage of these benefits.

6. Plan for Inheritance Tax (IHT) Rises

Inheritance tax has long been a controversial topic, and it may well increase under the new government. Currently, the IHT threshold is £325,000, with an additional £175,000 allowance if you’re passing your main home to direct descendants. Anything above this is currently taxed at 40%.

To mitigate IHT risks:

Consider making gifts: You can give away up to £3,000 per year tax-free, with additional allowances for wedding gifts and gifts from surplus income. Gifts between spouses are normally exempt from CGT or IHT, allowing you to transfer assets and take advantage of both partners’ allowances.

Set up a trust: Placing assets in a trust may help reduce IHT liabilities.

Life insurance policies: Some people take out policies specifically designed to cover future IHT bills. Always seek professional advice, however, as trusts and insurance policies can be complex.

7. Review Your Income Structure

Reeves may target income tax thresholds and reliefs, particularly for higher earners. Reviewing how your income is structured could help mitigate the impact.

Salary Sacrifice Schemes: Consider participating in salary sacrifice schemes, where you give up part of your salary in exchange for benefits like pension contributions, childcare vouchers, or cycle-to-work schemes. This will reduce your taxable income.

Dividend Income: If you run a business or own shares, taking income as dividends can be more tax-efficient than a salary, particularly if the dividend tax rates remain lower than income tax rates. Any good accountant will be able to advise you.

Spousal Income Splitting: If your spouse is in a lower tax bracket, transferring income-generating assets to them can reduce your overall tax burden. This is particularly useful for rental income or dividends from jointly held investments.

8. Prepare for Property Tax Changes

Property taxes, including stamp duty and council tax, could see reforms or increases. Here’s how to plan.

Bring Forward Property Transactions: If you’re considering buying (or selling) property, it may be wise to do so before any potential stamp duty increases are announced. Locking in current rates could save you significant costs.

Consider Downsizing: If you anticipate increased council tax rates or other property-related taxes, downsizing to a smaller home could reduce your future tax liabilities and lower your overall living costs. And, of course, doing this should release some of the equity in your property, which you can then use to help maintain your standard of living.

9. Enhance Charitable Giving

If Reeves increases income tax or reduces the thresholds for higher tax rates, charitable giving can become a more attractive option.

Gift Aid: Donations made under Gift Aid are tax-efficient, as charities can claim an additional 25% from the government. Higher-rate taxpayers can claim back the difference between the basic rate and higher rate of tax on their donations.

Donor-Advised Funds: These funds allow you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants from the fund over time. It’s a strategic way to manage charitable giving while benefiting from tax relief.

10. Stay Informed and Seek Professional Advice

Tax planning can be complex, especially in an uncertain economic environment. Staying informed about potential changes in the budget and seeking professional financial advice can help you adapt your strategy to minimize your tax liabilities effectively.

Monitor Budget Announcements: Keep an eye on the budget and any subsequent economic statements to understand how proposed changes might affect you. Quick responses can sometimes yield significant tax savings.

Consult a Financial Adviser: A qualified financial adviser can help tailor a tax-efficient strategy to your individual circumstances, taking into account your income, assets, and long-term financial goals.

Closing Thoughts

While tax rises in Rachel Reeves’ first budget may be inevitable, UK residents have various strategies at their disposal to mitigate the impact.

By taking advantage of tax-efficient investments, restructuring income and staying informed, you can protect your wealth and ensure that any tax increases have a minimal effect on your financial well-being. As always, professional advice tailored to your specific situation is invaluable in navigating these changes effectively.

If you have any comments or questions about this post, please do leave them below. But bear in mind that I am not a qualified tax adviser and cannot provide personal financial advice. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

In a recent post I talked about tax-free ways to boost your finances. It occurs to me that I omitted an important one, however – entering prize draws and competitions. In the UK anyway, cash and prizes acquired this way are normally tax-free.

In recent years the internet has opened up a host of opportunities for entering (and winning) competitions from home. Whether you’re a seasoned ‘comper’ or a newbie eager to try your luck, I hope you will find the tips, resources and advice in this post useful…

1. Finding the Right Competitions

The first step towards winning is finding the competitions themselves. Here are some ways to discover them:

Social Media: Follow brands, influencers (e.g. Superlucky Di) and competition-focused groups on Facebook, Twitter/X and Instagram. Search for relevant hashtags, e.g. #competition #prize #giveaway. Many businesses also run exclusive competitions for their social media followers.

Email Newsletters: Subscribe to newsletters from your favourite brands and competition websites to receive alerts about the latest contests.

2. Setting up Dedicated Comping Accounts

It’s best to set up dedicated email and social media accounts for your comping. Inevitably you will receive growing volumes of promotional material and even (regrettably) spam. Using separate, dedicated accounts will ensure your personal accounts don’t get cluttered up.

Check Email Regularly: To save time, you can search for relevant words and phrases like Congratulations, Winner and Runner-up.

Set up Accounts on Facebook, Instagram and Twitter/X just for Comping: Some competitions require you to ‘like’ or follow a particular brand on social media in order to enter.

Don’t Sign Up for Further Info: Avoid ticking the box to receive more information when entering a competition, unless you are really sure you want this. Doing so can result in your inbox swiftly being overrun.

3. Understanding the Rules

Each competition has its own set of rules and regulations. Carefully read the terms and conditions to understand:

Eligibility: Ensure you meet the requirements (e.g. age, location).

Entry Limits: Some competitions allow multiple entries, while others are strictly one per person.

Closing Dates: Note the end date to ensure you don’t miss out.

4. Crafting Winning Entries

Certain types of competition require more than just luck. Here’s how to stand out:

Skill-based Competitions: These might ask for a slogan, recipe, or photo. Be creative and original. Research past winners to understand what judges are looking for.

Tie-breakers: If there’s a question to answer, put some thought into it. A unique and clever response can be your ticket to winning.

5. Maximising Your Entries

To increase your chances, enter as many competitions as possible. Here’s how:

Set a Schedule: Dedicate time each day or week to entering competitions.

Use Autofill Tools: Tools like RoboForm can save time by automatically filling out your details for you.

Keep Track: Maintain a list or (preferably) spreadsheet of entered competitions to avoid duplicates and track deadlines.

6. Avoiding Scams

While many competitions are legitimate, some are not. Protect yourself by:

Verifying the Source: Only enter competitions from reputable websites or brands.

Not Paying Fees: Genuine competitions won’t ask you to pay to enter.

Checking Reviews: Look up the competition and the company running it to ensure they have a good reputation.

7. Networking with Fellow Compers

Join online communities and forums such as MoneySavingExpert or dedicated Facebook groups (such as this one) where members share tips, winning stories and new competition finds. Networking with other compers can provide valuable insights and motivation.

8. Celebrating Wins, Big and Small

Not every prize will be a jackpot, but every win counts. Celebrate all victories, whether it’s a small voucher or a large cash prize. Sharing your wins on social media or competition forums can also encourage others and attract positive attention.

9. Staying Persistent

Winning competitions requires patience and perseverance. Don’t get discouraged if you don’t win straight away. Keep entering regularly, and your persistence will eventually pay off.

Closing Thoughts

Winning cash and prizes through online competitions is a fun and potentially rewarding hobby. By keeping organised, being creative, and staying wary of scams, you can significantly boost your chances of success. So get out there, start entering, and who knows? You might just land that dream holiday or big tax-free cash prize sooner than you think 😎🍾🏖

Happy comping, and may the odds be ever in your favour!

If you enjoyed this post, please link to it on your own blog or social media:

In these challenging times, we all need to ensure our savings stretch as far as possible. So today I thought I’d set out the range of tax-free allowances you can use to help do this.

Personal Savings Allowance (PSA)

The Personal Savings Allowance (PSA) was introduced in April 2016 and allows you to earn a certain amount of interest tax-free each year. The amount of your PSA depends on your income tax band:

Basic Rate Taxpayers (20%): You can earn up to £1,000 in savings interest tax-free.

Higher Rate Taxpayers (40%): You can earn up to £500 in savings interest tax-free.

Additional Rate Taxpayers (45%): You do not receive a PSA, meaning all interest earned is taxable.

For example, if you are a basic rate taxpayer and earn £900 in interest from your savings in a tax year, this amount is within your PSA and therefore tax-free. However, if you earn £1,200 in interest, £200 of that will be subject to tax at your marginal rate.

Individual Savings Accounts (ISAs)

ISAs are another powerful tool for earning tax-free interest. There are several types of ISA, with varying annual contribution limits and benefits:

Cash ISAs: You can save up to £20,000 per year, and the interest earned is entirely tax-free.

Stocks and Shares ISAs: Also with a £20,000 annual limit, any capital gains or dividends received are tax-free.

Lifetime ISAs (LISAs): Designed for first-time homebuyers or retirement savings, you can contribute up to £4,000 annually to a LISA, with a 25% government bonus on contributions. The interest earned is tax-free.

Innovative Finance ISAs (IFISAs): These allow you to earn tax-free interest from peer-to-peer lending within the £20,000 annual limit.

You can mix and match these ISAs and you can now open as many as you like within a single tax year. But the total amount you contribute in a tax year cannot exceed the overall limit of £20,000.

Starting Rate for Savings

For those with a lower overall income, the starting rate for savings can be particularly beneficial. If your total income (excluding savings interest) is less than £17,570, you may qualify for the starting rate for savings, which can provide up to an additional £5,000 in tax-free interest.

Here’s how it works:

If your non-savings income is below £12,570 (the personal allowance for most people), you can use the full £5,000 starting rate for savings.

For every £1 your non-savings income exceeds £12,570, your starting rate for savings decreases by £1.

For example, if your non-savings income is £15,000, your PSA is reduced by £15,000 minus £12,570 = £2,430. Subtracting £2,430 from £5,000 leaves £2,570. You can therefore earn up to £2,570 in interest tax-free under the starting rate.

If you qualify for both the starting rate for savings and the PSA, you can earn up to £5,000 in interest tax-free under the starting rate, plus an additional £1,000 (or £500 for higher rate taxpayers) under the PSA. For example, if you’re a basic rate taxpayer with £12,000 in non-savings income, you could potentially earn up to £6,000 in interest tax-free (£5,000 from the starting rate and £1,000 from the PSA). Both allowances can be combined to maximize the amount of interest you can earn tax-free.

Premium Bonds provide a chance to win tax-free prizes each month. While the odds of a big win may be slim, any winnings are tax-free. Similarly, some NS&I savings products, like certain Savings Certificates, offer tax-free interest.

Summing Up

By understanding and utilizing these tax-free allowances, you can maximize the interest you earn on your savings without paying tax. Here’s a quick recap:

Personal Savings Allowance: Up to £1,000 for basic rate taxpayers, £500 for higher rate taxpayers.

ISAs: Up to £20,000 per year across various types.

Starting Rate for Savings: Up to £5,000 if your non-savings income is below £17,570.

Premium Bonds and Some Other NS&I Products: Tax-free interest and prizes.

Be sure to review your financial situation regularly and consider using these allowances to optimize your savings strategy. By leveraging these benefits, you can grow your savings more effectively and keep more of your hard-won interest.

Finally, this post sums up the situation currently. The new government is looking to raise extra tax revenue any way it can, however, and tax-free savings allowances certainly aren’t immune. Obviously I will update this article (and/or publish a new one) if the rules are changed in future.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m sharing a post I originally wrote for my friends at Mouthy Money. It’s an important topic so, by agreement with Mouthy Money, I am publishing it here as well.

As you are probably aware, the UK government is currently pushing heat pumps hard in its quest to achieve Net Zero. As I said in my earlier article for Mouthy Money, however, they are definitely not a one-size-fits-all solution for home (or business) heating.

Even the government admits heat pumps are unsuitable for around 4 million UK homes, for a variety of reasons including lack of outside space and planning restrictions. Industry estimates suggest the real number is closer to 8 million [source].

Even if your home is theoretically suitable for a heat pump, there are good reasons why you might not want one. As previously discussed, these include the high initial cost, the potential noise issues, and the fact they work less well in cold weather (just when you need them most!).

For heat pumps to operate effectively, properties must be well insulated, and bigger pipes and radiators are likely to be needed. This can add considerably to the cost, not to mention the disruption caused. In my personal view heat pumps are best suited to new-build homes that can be designed around them.

So today I thought I would set out a range of other home heating solutions you might want to consider. I will also set out some points to take into account before making any decision.

Heat Pump Alternatives

Table of Contents

1. Gas boilers

Gas boilers have been a staple in UK homes for decades, and they remain a very popular choice for heating. They provide reliable and instant heat, making them particularly suitable for homes with high hot water demand. While they rely on fossil fuels, modern condensing boilers are more energy-efficient, helping to reduce carbon emissions (and costs) compared to older models.

2. Oil boilers

For properties not connected to the gas grid, oil boilers offer a viable alternative. They work similarly to gas boilers but use heating oil stored in a tank on the property. While oil prices can fluctuate, modern oil boilers are highly efficient and can provide consistent warmth to homes in rural areas or those without access to natural gas.

In future oil boilers may be converted to run on hydrotreated vegetable oil (HVO), which is a renewable and 100% biodegradable alternative [source].

3. Biomass boilers

Biomass boilers use organic materials such as wood pellets, chips or logs to generate heat. They’re a sustainable option, as wood is a renewable resource.

Biomass boilers can be integrated into existing heating systems and may be eligible for government incentives such as Green Deal, making them an attractive choice for environmentally conscious homeowners.

4. LPG (liquefied petroleum gas) boilers

LPG is a clean-burning fossil fuel typically stored in a tank on the property, providing a reliable source of heating and hot water. LPG boilers function similarly to natural gas boilers, offering instant heat and efficient performance. They’re particularly popular in rural areas where mains gas is unavailable, providing homeowners with a convenient and cost-effective alternative for heating their homes.

5. Electric heating systems

Electric heating systems come in many different forms, including electric radiators, storage heaters and underfloor heating. They also include low-emission infrared panels.

While electricity prices can be higher than gas or oil, advances in technology have led to more energy-efficient electric heating options. They are often easier – and therefore cheaper – to install and require less maintenance compared to traditional boiler systems. They can be a good choice for smaller properties and those with limited space.

6. Air conditioning systems

Traditionally associated with cooling, modern air conditioning systems can also provide heating during colder months through a process known as reverse cycle or heat pump technology.

These systems extract heat from the outdoor air and transfer it indoors, offering both heating and cooling capabilities in a single unit. While more common in warmer climates, air conditioning systems are becoming increasingly popular for heating purposes in the UK due to their energy efficiency and versatility.

7. Electric boiler systems

Electric boilers function similarly to gas or oil boilers but use electricity as their primary energy source. They heat water for central heating and domestic hot water supply, offering a clean and convenient heating solution. They can normally be used with the same radiators as gas boilers, unlike heat pumps which (as mentioned above) typically require the installation of bigger radiators and pipes.

Electric boilers are compact, quiet, and emit no emissions on-site, making them suitable for properties where space or ventilation is limited. While electricity costs may be higher than some other options, electric boiler systems can be an efficient and low-maintenance option.

The MInistry of Defence recently decided to opt for electric boilers rather than heat pumps as a more cost-effective solution for barracks and other military installations [source].

8. Hybrid heating systems

Hybrid heating systems combine two or more heating technologies to optimize energy efficiency and performance. For instance, a hybrid system might pair a gas boiler with a heat pump or integrate solar thermal panels with a conventional boiler. These systems offer flexibility and can adapt to changing energy demands, providing homeowners with both reliability and sustainability.

9. Solid fuel stoves

Solid fuel stoves, such as wood-burning or multi-fuel stoves, provide both warmth and ambiance to homes. They’re particularly popular in rural areas where homeowners have access to firewood or other solid fuels. While they require manual operation and regular maintenance, solid fuel stoves can significantly reduce heating costs and add character to any living space.

10. District heating networks

In urban areas, district heating networks supply heat to multiple buildings from a central source, such as a combined heat and power (CHP) plant or biomass facility. This communal approach to heating can be more efficient and cost-effective than individual heating systems, offering residents a sustainable and reliable heat supply without the need for on-site boilers or heat pumps.

Considerations When Choosing an Alternative

When exploring alternatives to heat pumps, various factors need to be considered.

Cost: Evaluate the initial investment, ongoing maintenance costs, and potential savings (or otherwise) on energy bills.

Space and suitability: Consider the available space for installation and the specific requirements of each heating system.

Energy efficiency: Look for heating solutions with high energy efficiency to minimize running costs and environmental impact.

Fuel availability: Assess the availability and accessibility of fuel sources in your area.

Control options: Explore the available control features, such as programmable thermostats or smart technology integration, for convenient operation and efficient energy management.

Lifestyle factors: Some heating methods (e.g. electric) are good if you are out and about a lot but want rapid warmth when you get home. Other methods (including heat pumps) are better suited to those who are around more in the day and like to keep their home at a fairly constant temperature.

Political and economic factors: Bear in mind that the government is keen to achieve its Net Zero targets, and as a result some heating options may become more costly in future and harder (or even impossible) to access. That applies to fossil fuels in particular; although realistically it is hard to see fuels such as gas being banned entirely any time soon.

Finally, I’d like to sound a note of caution about putting all your home heating eggs in one metaphorical basket, especially that of electricity.

As the UK transitions from fossil fuels towards (supposedly) greener electricity, power cuts are likely to become more frequent and longer. The growing use of heat pumps and EVs will add to the demand for electricity from a distribution network that is already struggling to cope. And renewable energy sources such as solar and wind, while they might be more environmentally friendly, produce significantly less electricity when the sun doesn’t shine or the wind doesn’t blow.

If you’re entirely reliant on electricity for your home heating, this could make you vulnerable in the event of outages (especially relevant if there are older people in the house). In my view there is much to be said for having a backup heating source, e.g. solid fuel, to keep your home warm if the mains electricity fails. Of course, this applies with regard to heat pumps as well, as they require electricity to function.

It’s also worth noting that in Scandinavian countries, where heat pumps are more common, most families have an additional source of heating as well as heat pumps to get them through the coldest months.

A home battery system, as discussed in this recent article, can also reduce your vulnerability in case of power cuts, especially when combined with solar panels.

Closing Thoughts

In summary, while the government and energy companies are pushing heat pumps hard, they are far from the only possible home heating solution, either now or in future.

If you’re considering upgrading your heating, take time to evaluate all the options and don’t be unduly swayed by the heat pump hype (and even misinformation). While these devices can work well for new-builds in particular, they are definitely not the only option.

By exploring alternatives such as gas and oil boilers, biomass systems, electric boilers, LPG boilers, solid fuel stoves, and others, you should be able to find a heating solution to suit your budget, your lifestyle, your priorities and your property size and character.

Good luck, and please do stay warm!

As always, if you have any comments or questions about this article, please do post them below.

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

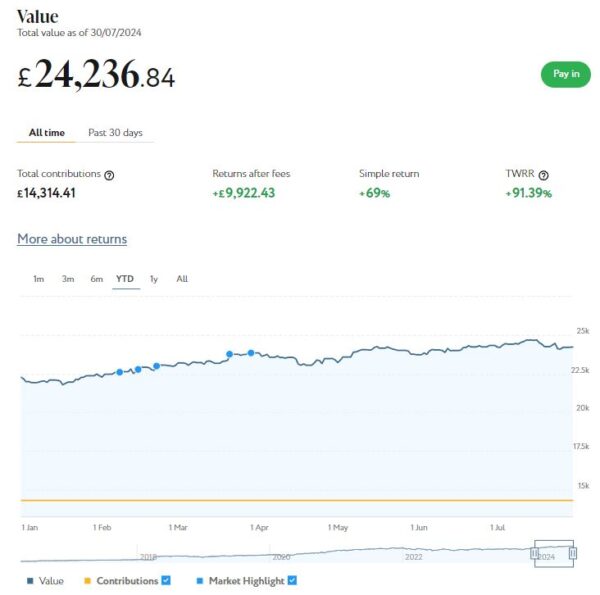

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,237 (rounded up). Last month it stood at £24,250, so that is a small decrease of £13.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,895 compared with £3,911 a month ago, a fall of £16. Here is a screen capture showing performance over the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the all-time screen capture below, this portfolio is now worth £769 compared with £772 last month, a small decrease of £3.

As you can see from the charts, July was an up-and-down month for my Nutmeg investments. Their overall value has fallen by a modest £32 or 0.11% since the start of July.

Although any fall is disappointing, short-term ups and downs are very much very much to be expected with stock market investments. And it is worth observing that the overall value of my Nutmeg investments is still up by £2,586 or 9.82% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

You may like to note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the new tax year began on 6 April 2024 and and you have a whole new £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you so wish) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. Last month I withdrew £500 from completed loans and now have £40 remaining in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £195.87 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £28.74, meaning that overall (rental income minus capital value decrease) I am up by £167.13. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Note that as from this financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.60 an overall increase of $281.34 or 27.52%.

As you can see, my Oil WorldWide investment is showing just over 12% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in June on the excellent Mouthy Money website. The first is Seven Ways to Make Money From Your Garden. In this article I set out seven ways you can make money from your garden (if you’re lucky enough to have one). None of these is likely to make you a fortune, but they can all help your finances stretch further in these challenging times.

Also in July I revealed how you can Make a Sideline Income Renting Out Your Driveway. If you have a parking space or driveway that sits empty most of the day, turning it into a source of passive income is easier than you might think. In this article I explained how you can get started and make the most from this opportunity.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the wide range of articles published in July, I particularly enjoyed Five Ways Tracking Your Spending Can Improve Your Finances by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living, and this article is a good example of her work. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in June. Some are no longer relevant due to closing dates having passed, but I have listed the others below.