Today I am pleased to bring you a guest post by Araminta Robertson, who blogs at Financially Mint.

Araminta is a university student and she writes from a young person’s perspective. Today she shares some of her top tips for eating healthily on a budget.

One thing many older people have in common with students is that they need to watch the pennies. Araminta has some great advice for all of us on how to eat both frugally and healthily.

Over to Araminta then…

It’s not easy to combine healthy, cheap, delicious and quick. And yet, it is still possible. As a student, I’ve always had to figure out the best combination, and through a lot of practice I’ve realised that the methods I used could also be very useful for anyone in a similar situation.

So – here are four steps get that sweet combination of exactly what you’re looking for when you eat. Here we go:

Table of Contents

1. Plan it

The first step is to figure out your ‘magic number’; how much are you willing to spend? What is your budget for food for one month/week?

Start with that number and work your way back. Then make a list of cheap healthy food that you and your family enjoy. Some examples are:

Beans

Eggs

Tomatoes

Frozen veggies

Pepper + onions

Almonds

Lentils

Squash/pumpkin

Oats

Canned goods

Yoghurt and cheese

Quinoa

Carrots

Aubergine

Kale

Sweet potatoes and potatoes

Now you’ve got your magic budget number, some general ingredient ideas. What’s missing? A recipe. And it’s at his point that I whip out Google and simple type in ‘ingredient recipe’, so ‘carrot recipe’ for example. I do a bit of research, look for something simple and cheap to make. Some great websites to find these are BBC Good Food and All Recipes UK.

Do a bit of a rough plan – find some ingredients, do some research and pick some recipes you’d like to try out during the week. Then write down the list of ingredients you’ll need to complete that plan. It’s always fun to try some exciting recipes and do some experimenting. More on this later 😉

2. Shop it

Time to do some exploring! If you want to stick to a small budget, go to discount supermarkets such as Aldi, Asda and Lidl. Bring your ingredients and grocery list and do the shopping!

A little tip: Don’t go shopping when you’re hungry, you’ll probably end up buying unnecessary stuff

What I normally do is one big shopping day a week and then some additional stuff from time to time. Pick a day to do your shopping for the week and buy it all at once. You’ll see batching is a huge productivity booster – no need to do mini shopping trips anymore! It’s also easier to budget week by week, this way it’s easy to know how much you spent on the shopping trip.

3. Cook it

Now to the exciting part.

What prevents most people from cooking is the ‘I’m rubbish at cooking’. We were all rubbish at cooking at one point, and you get better by doing more of it. The first pie you make might be a disaster, but the tenth one will be pretty tasty.

Once again, batching: pick a day to do all the cooking for the week (I like Sundays). Make it a fun activity; include the kids, the family, the dog, even. A proper event, an afternoon where everyone gets together to prepare meals for the week. Of course, if that’s not possible then simply cook it yourself – but an event is always nice.

Have your meal plan ready and then cook and freeze stuff for the week. Soup, rice and beans can last the week – whereas meat and potatoes aren’t very good at that. As you cook more and more you’ll figure out what can be stored and what can’t, and you’ll also end up preparing some more delicious recipes.

I normally produce large quantities of rice/pasta/sauce/ and freeze it or leave it in the fridge. Then when it’s time to eat I just have to make the meat/veggies

4. Try it

The most important when improving your cheap/delicious/healthy meals is to keep experimenting (I even do fancy Money Experiments). Try new ingredients (I’ve got an interesting vegetable called a ‘swede’ in my kitchen), new recipes and new dishes. You’ll slowly get better at it. Now I consider myself an expert at making something out of scraps – stir-fry it all.

Here are some examples of cheap budget meals I like to do:

Soup – mushroom soup, pumpkin, lentil, tomato

Curry – could be vegetarian

Pie/quiche

Tacos/wraps/quesadillas

Jacket potatoes

Chili

Fried rice – literally just veggies, eggs and rice

Omelettes/scrambled eggs

Stir-fry

Also keep on the lookout for discounts, sales and chances to save a little bit of money. Here are some good websites to get started: Money Saving Expert, Super Savvy Me and CheckoutSmart.

There you go! Four steps to eating well on a budget. The hardest part is simply sticking to it and being willing to try new things. But if you make it a fun event every week, you can turn it into a family activity and be held accountable to do every week. Next thing you know you’ll be cooking fancy quiches and amazing risotto. Keep trying!

What’s your favourite recipe? Comment below!

Bio: Araminta is creator of Financially Mint, a personal finance blog for university students written by an actual student. She interviews experts, does weird experiments and a ton of research to help her and others graduate financially intelligent.

Many thanks to Araminta (pictured) for an interesting and useful post. Do check out her Financially Mint blog as well!

I guess some of my older readers may be amused by her reference to the “interesting” vegetable called a swede. Swedes are a vegetable many of us baby boomers remember well from childhood, and not always fondly! I must admit I haven’t cooked with swedes for a while, but promise to put them on my shopping list again during the winter months 😉

Like Araminta I enjoy looking for recipes on the internet, and I often use the websites she mentions, and various others. My personal tip would be to take a few moments to read the reviews and comments that are often left by people who have tried the recipes. This feedback is invaluable, especially the ideas for tweaking/improving the recipe.

As always, if you have any comments or questions about this post, for Araminta or me, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

I’ve discussed matched betting a few times on Pounds and Sense. Despite the name it’s not gambling but a genuine way of making a risk-free sideline income.

Matched betting involves (legally) taking advantage of bookmaker special offers. By doing this you can generate a guaranteed profit for no risk, regardless of how the event/s you are betting on pan out.

Although it’s not essential to subscribe to a matched betting advisory service, if you are new to betting in particular it is highly advisable. There are various services, the best known of which include Profit Accumulator and Odds Monkey. Today, however, I want to look at a rival service called Profit Squad, which has its own unique set of tools and features, and in my view is especially suitable for people who already have some knowledge of matched betting. That being said, it also has all the advice, tools and information someone new to matched betting would require.

Profit Squad were kind enough to give me complimentary membership of their service so I could see what they have to offer. Here’s what I found…

Table of Contents

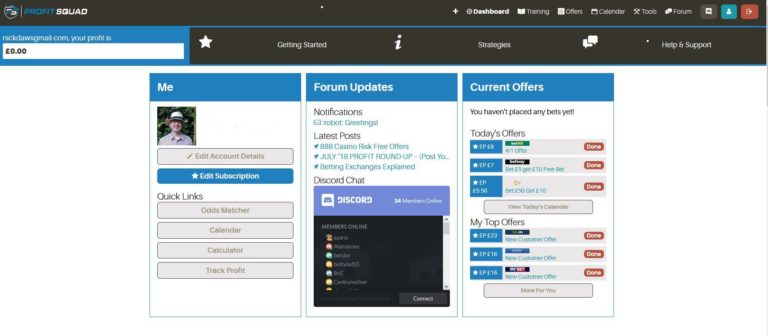

First Impressions

Profit Squad is now owned by the same company that runs MatchedBets.com (which I reviewed here), so you may not be surprised that there are some similarities in appearance between the sites. While MatchedBets.com has a rather garish colour scheme, however, Profit Squad (see below) is more restrained. Personally I prefer this, as it makes the site look more professional, as well as being more readable.

As you will see, the main navigation menu is at the top right of the screen. If you hover the cursor over Offers or Tools, a sub-menu will appear. It’s all quite logical and intuitive.

As with all matched betting advisory services, the site is organized into a number of sections. The main ones are listed below:

Training

Offers

Tools

Calendar

Forum

I’ll look at each of these in a bit more detail below.

Training

This is (of course) the training area of Profit Squad, and is the place where new matched bettors should start. It is neatly and attractively set out. There are 22 articles here, covering everything from how to get started in matched betting to reload offers and advanced strategies (including online casinos)..

The articles consist mainly of text and screen captures, with videos also used in some cases. I found the articles clear and well written. While I am already familiar with the basics of matched betting, I found some of the articles (e.g. on each-way dutching and how to profit from online slots) genuinely eye-opening.

Offers

This is divided into sub-sections, including:

New Customer Offers

Existing Customer Offers

Accumulator Offers

Free Bet Clubs

Horse Racing Offers

Casino Offers

Advanced Casino Offers

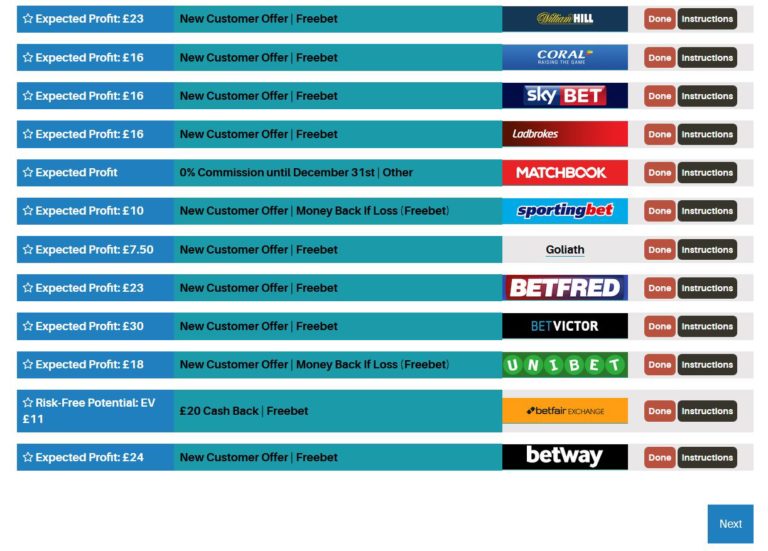

These are all pretty self-explanatory. In New Customer Offers, for example, all such offers are listed in order of expected profit, the highest first (see below).

Clicking on Instructions takes you to detailed instructions on how to apply the offer. These generally include a short video plus written instructions. Again, I thought these were very clear, and I like the way the key points of each offer are set out in checklist form at the top of the page.

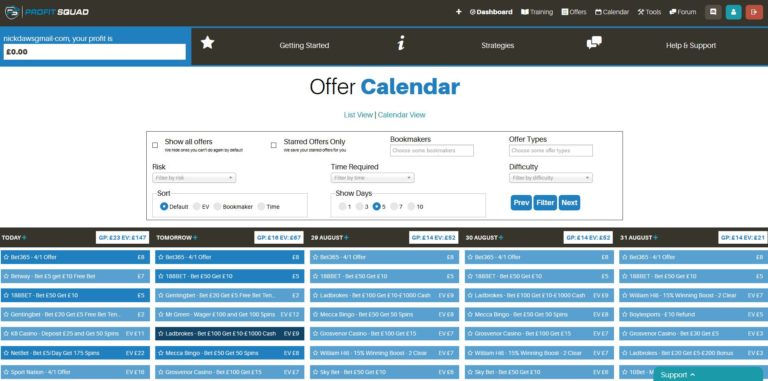

Offer Calendar

This is a feature of Profit Squad I really like. Just by visiting the Calendar page you can see all the day’s recommended offers, along with the expected profit and a link to full instructions for doing them.

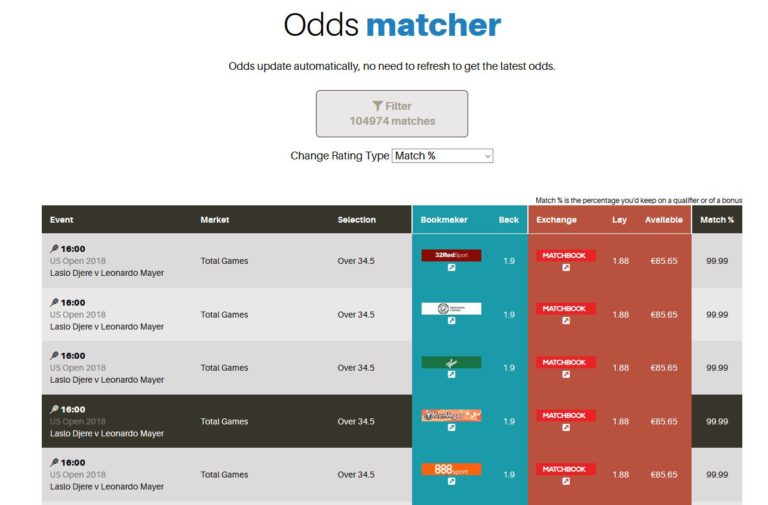

Odds Matcher

Of course, every matched betting service needs an odds-matching tool, which helps you find the best bets for matched betting offers. Here’s a capture of the one provided by Profit Squad.

As you would expect, you can filter results according to sport, odds (minimum or maximum), start time, odds percentage, liquidity available at the exchange, and so on.

One feature I particularly like is that odds are shown in real time, so you don’t have to keep refreshing the screen. This also avoids the situation that can occur using other odds matching software (e.g. on Profit Accumulator) where the information frequently lags behind, so you think you have found a great match only to discover it has already gone.

Acca Backers

As mentioned in this blog post a few months ago, accumulator offers are a particular favourite of mine. These are where you take advantage of bookmakers’ offers to refund your stake if one leg of your accumulator loses. This gives punters an in-built edge and means they should enjoy steady profits so long as they back and lay appropriately.

Profit Squad’s accumulator software offers four different ways to make money from accumulator offers: Lay Sequential, Lay at Start, Lay With Lock-In, and No Lay. All four methods are explained in the Training area, mentioned earlier. This is more advanced than other platforms’ accumulator tools, which typically only offer three options.

As you may have noticed, with Profit Squad by default you see all four types of offer listed according to their expected value (average profit generated). However, if you prefer one particular type of acca (e.g. Lay With Lock In, which I prefer personally) you can set the filter to show only this type.

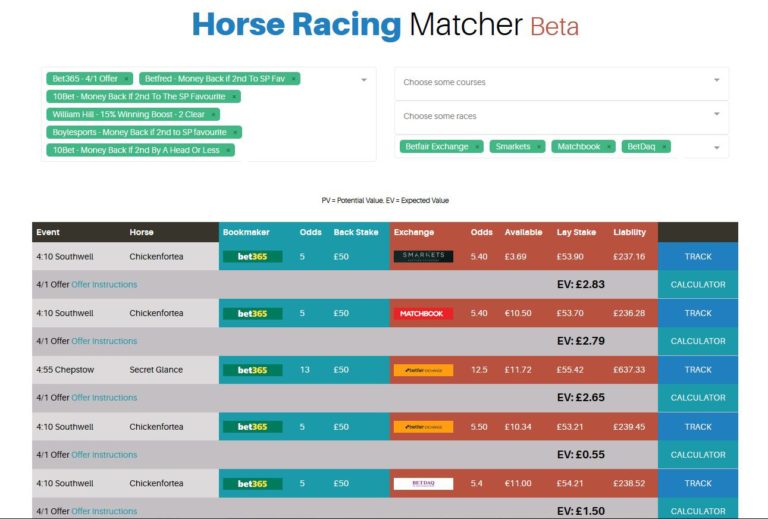

Horse Racing Matcher

This tool is provided for use with horse racing offers, e.g. your money back if your horse is second to the SP favourite. By careful backing and laying you can generate a good return when a refund is triggered and a small qualifying loss otherwise, hopefully producing steady profits overall.

As you will see, the Horse Racing Matcher is still in Beta at the time of writing, but appears to be working well. As with the Odds Matcher and Acca Backers, the odds in this software tool automatically update when they fluctuate on betting exchange and bookmaker sites.

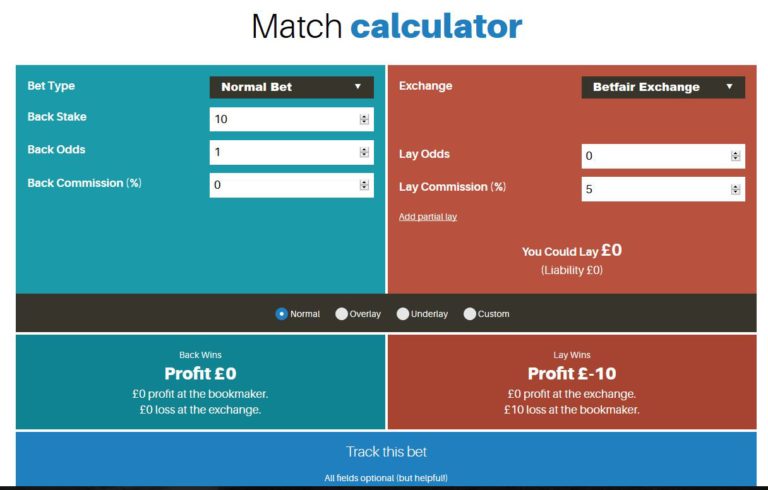

Calculator

This is another standard feature on matched betting advisory service sites, but the one offered by Profit Squad is undeniably impressive. Although it looks simple at first sight (see below), it is actually a very powerful tool.

As well as standard matched betting calculations for qualifying bets and free bets, you can use it to calculate bonus on win, bonus on loss, enhanced odds as free bets, and several more. Pretty much any bonus situation is therefore covered. You can also use the calculator to work out what to do in the event of incomplete lays, and if you want to overlay or underlay a bet.

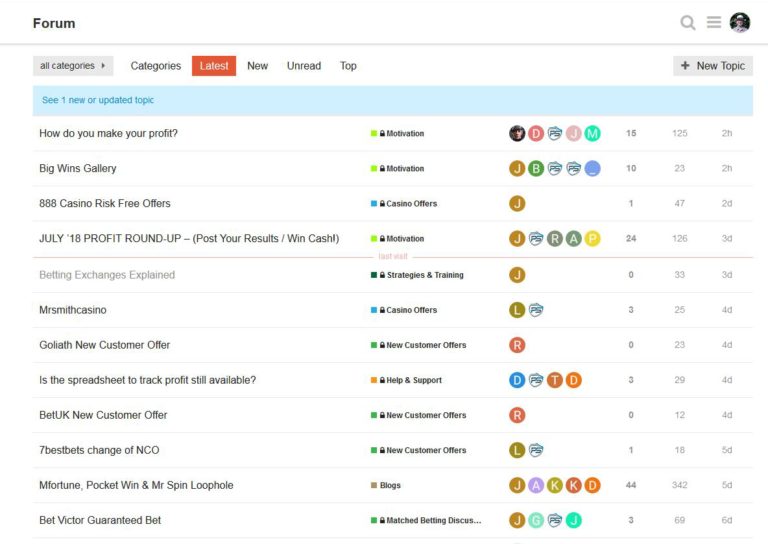

Forum

Likewise, every matched betting service needs a forum, where members can ask questions, share offers and opportunities, or just discuss anything matched betting related (or otherwise).

The Profit Squad forum (see below) is neatly set out and works well. It isn’t as busy as some forums, e.g. the one owned by the market-leading Profit Accumulator. There is plenty of good content, though, and staff are usually around to assist as required.

In addition to the forum, Profit Squad has a discord chatroom for members, which is great for discussing opportunities in real time.

Other Features

Profit Squad has a range of other features as well. If I tried to list them all this review would be at least double its already excessive length!

One tool I should definitely mention, however, is the Each Way Dutching Calculator. Each way dutching is a method of backing multiple or all runners in a horse race (or other event) with different bookmakers at their best prices. With suitable races this method can be more profitable than standard backing and laying, and it is also generally less hassle. Full information about how to use the Calculator is included in the training area, of course.

Another thing I should mention is that Profit Squad tracks all your betting activity automatically. It keeps a record of your profits and bet details, and displays them in your account. This makes it easy to see how you are doing overall, and does away with the need to maintain your own spreadsheets (although personally I still like to do this).

One final comment is that the site is fully mobile optimized – so if you like to bet on your smartphone, you should find using Profit Squad a pleasanter experience than with some rival services.

Pricing

Joining Profit Squad currently costs £15 a month. That is cheaper than most other matched betting advisory services, e.g. Profit Accumulator currently charge £17.99 a month. They don’t have a free trial offer like some other services, but for just £1 you can get a 14-day trial giving you full, unlimited access to the service. In many ways this is a better deal than the free limited membership offered by other services, as you can do as many bookmaker offers as you like (or can fit in) during your 14-day membership.

Closing Thoughts

Overall, I have been very impressed with Profit Squad. It offers high-quality matched betting training, and a comprehensive range of software tools, tips and information..

In my view it is particularly suitable for people who may already have some experience in matched betting, who are now looking for more advanced strategies to keep the money rolling in.

Profit Squad is particularly strong on online casino strategies, including slots, roulette and blackjack. I know from my membership of various matched betting Facebook groups that this is now a very popular approach among experienced matched bettors who have exhausted the bookmaker welcome offers. There are some risk-free casino offers, and others that may not be risk-free but have a positive ev (expected value). That means by the law of averages if you do these offers you will make a long-term profit, but will likely suffer some day-to-day losses. This is all covered in detail in the training, of course.

Profit Squad also have some of the best matched betting software tools I have seen, covering pretty much the entire range of bookmaker welcome and reload offers and more besides. About the only drawback I can see with it compared with a service such as Profit Accumulator is that the forum isn’t as active, but of course this is likely to change in future as more members join the service.

If you are thinking of giving matched betting a go – or are looking for an alternative advisory service featuring more advanced strategies – I strongly recommend checking out Profit Squad. They are adding new tools and features all the time, and joining now will ensure you have access to them at no extra cost. In any event, the 14-day trial for £1 is basically a risk-free opportunity to see everything they have to offer. Do just one risk-free offer during this time and you should cover your £1 outlay multiple times over.

As always, if you have any queries about Profit Squad or matched betting generally, please do post them below.

Disclosure: This review includes tracked affiliate links. If you click through and sign up with Profit Squad, I will receive a commission for introducing you. This will not affect the service you receive (or the price you are charged) in any way.

If you enjoyed this post, please link to it on your own blog or social media:

If you are 50 or over, you will almost certainly at least have heard of Warner Leisure Hotels. The company have 14 country and coastal resort hotels across England and Wales. They have a strict adults-only policy, and appeal mainly to an older clientele (based on my experience, the average age is late sixties or early seventies).

As well as accommodation, they offer a range of leisure activities, including day trips, quizzes, guided walks, archery and bowls, social dancing, swimming, and so forth. Most of these activities are included in the price, as is the evening entertainment.

Accommodation is generally on a half-board basis, including breakfast and evening meal. Guests typically book short stays of two to four days, often focused around a particular headline act. Some of those in the current line-up include Motown, Abba and Franki Valli tribute acts, plus the real Leo Sayer, Paul Young, Russell Watson, Alexander Armstrong, Jane Macdonald, and many others. There are also seasonal breaks, spa breaks (at the Thoresby Hall hotel), bowls breaks, and more.

I have been to two Warner Leisure Hotels, Bodelwyddan Castle in North Wales (pictured above) and Alvaston Hall in Cheshire. I thought I would therefore take the opportunity to share my impressions here for others who might be contemplating this type of short break holiday.

My Review

As my partner passed away five years ago, I went to both venues on my own. I am in my early sixties, and felt very young compared with some of the other guests!

In both cases I found the accommodation spacious and comfortable, with all the facilities you would expect at a good hotel. I was on the ground floor at both, and had a small private terrace with a metal table and chairs, which was pleasant to sit out on. Here’s a picture of the accommodation block in which I stayed at Alvaston Hall.

I thought the food was generally very good. The dining area was large and could be a bit noisy, but the waiters and waitresses did a great job of getting meals out quickly. You are allocated a table at the start of your stay and keep that for the duration. As a solo guest I was offered the opportunity to be matched with another solo male as a dining partner. I declined this, as it seemed a gamble whether I would have anything in common with them.

At Alvaston Hall the evening meal is combined with the entertainment. So, basically, you have your meal followed by a show, all the while sitting at the same table. I liked this idea in theory, but in practice I discovered it had a few drawbacks.

For one thing, if you have been allocated a table towards the back (as I was) it can be quite hard to see what is happening on the stage. In addition, for me anyway it felt a long time to be sitting in one place. Really I preferred the arrangement at Bodelwyddan Castle, where you had your meal in the restaurant then went over to the main hall for the evening entertainment (for which you could sit anywhere).

I must admit I was slightly disappointed by the entertainment programme. The evening entertainment in particular was targeted at an older clientele and I didn’t particularly relate to it, despite being no spring chicken myself!

Both hotels seemed very big on social dancing, with guests being invited to ‘take the floor for the foxtrot’ or whatever. Not my thing at all, I’m afraid. I had been hoping for something more akin to cruise ship entertainment, with song and dance shows and cabaret acts, but perhaps that was asking too much.

There were regular quizzes, though again I felt that they were often oriented towards the older guests. I did one quiz about the 1950s, a decade many of those taking part remembered well. As I was only four years old when the fifties ended, I felt at a bit of a disadvantage!

On the positive side, I went on several guided walks, which I really enjoyed. I also took full advantage of the swimming pools, and at Alvaston Hall went to an interesting demonstration of fruit and vegetable carving (see photo below).

I also enjoyed looking around Bodelwyddan Castle itself (pictured below), which is a National Trust property. Warner guests get free entry during their stay, which is a nice bonus.

Prices

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I thought both the breaks I took were good value for money, bearing in mind that as well as comfortable accommodation you get breakfast and an evening meal, and a range of leisure facilities and entertainment.

When I checked just now, you could book a two-night break at Alvaston Hall for two people this weekend at prices ranging from £219.48 for a standard room up to £315.48 for a luxury suite. In my experience even ‘standard’ rooms are very comfortable, and the price above works out to just over £100 per person per night. By comparison, I have been charged well over £100 per night for bed and breakfast, with no evening meal or entertainment, in some hotels and guest houses.

If you are travelling solo (as I was) you may have to pay an under-occupancy surcharge. However, the hotels do have some single rooms, and there are also ‘no surcharge’ offers for solo travellers on some breaks. It’s definitely worth inquiring about this with the hotel you want to stay at.

Finally, I should mention that Warner Leisure Hotels often offer special deals and discounts. Once you are on their list, you can expect to be mailed regularly about these!

Summing Up

Overall, while I enjoyed my stay at these hotels, I have to say I did feel a bit young for them. The entertainment wasn’t really my cup of tea and I’m not sure it will be even when I’m ten years older. I saw one review that described Warner Leisure Hotels as ‘Butlins for old people’ and have to admit I think that’s quite apt (it’s owned by the same parent company as Butlins and Haven Holidays, incidentally). I don’t mean to sound snobby about this. When I was growing up I enjoyed regular family holidays at Butlins holiday camps and hotels. But the format does seem a little tired and old-fashioned now. In my view the company could learn a few lessons from the range of entertainment offered on cruise ships nowadays and even in tourist hotels in places like the Canary Islands.

I also think Warners could do a lot more to welcome solo guests and get them involved. At times I found staying there surprisingly lonely. Again, my experience with cruises has been that they do a much better job for solo guests, with regular meet-ups, social activities and even dedicated staff members to look after them. It would be nice if Warners did something similar. There are lots of older people who live alone, and I think the company are missing a trick by not reaching out to them.

But to be fair, I do think Warner Leisure Hotels offer an appealing combination of comfortable rooms, good food, a full activities and entertainment programme, and good value prices. I’m not planning on going again soon, but I certainly wouldn’t rule it out in future.

So those are my impressions of Warner Leisure Hotels, but what do you think? Have you stayed at one yourself, or would you even consider it? I’d love to hear your views!

For a wider range of all-inclusive holiday options in the UK and abroad, check out this article on Over 60s Discounts 🏖

Disclosure: This review includes affiliate links, so if you click through and make a purchase I will receive a commission for introducing you. This will not affect in any way the terms you are offered. Neither has it influenced in any way this review!

If you enjoyed this post, please link to it on your own blog or social media:

Some of you may know that for more years than I care to remember I made my living as a freelance writer. Nowadays I am semi-retired but still take on writing work from time to time, alongside running this blog, of course!

I know many people are interested in freelance writing, and it often appeals to older/retired people, as you can do it part-time and it doesn’t require any expensive tools or equipment. Writing is also something you can do even if you have health issues or disabilities.

So today I thought I would share a few of my top tips about freelance writing for money, based on my years of experience. To be clear, I am talking mainly here about writing for editors and other clients, rather than books or ebooks (which I previously covered in this post about books and this one about ebooks).

I hope this article may be of interest to younger people, as well as my core readership of over-50s.

Table of Contents

1. Don’t Worry About Not Knowing Everything

When I was starting my writing career, I worried a lot about what I didn’t know.

Every time I came across a word I hadn’t seen before, rather than view it as an opportunity to learn something new, I took it as a further sign that my vocabulary wasn’t wide enough to succeed as a writer. (In fact, I now realise that while having a good vocabulary is definitely an asset, you could go through an entire writing career without ever knowing the meaning of palimpsest, clepsydra, ursine, and many more…)

It wasn’t just vocabulary either. I worried that I didn’t know whether I should use “toward” or “towards”, “forever” or “for ever”, “continuous” or “continual”, and many more. And I could waste a whole morning agonizing over whether I should use a dash or a colon in my opening paragraph.

What I realise now is that most of these things matter little. Quite often, either choice will be acceptable. My advice to a new writer today would be to get a good dictionary and style guide, and refer to these whenever you’re in doubt. But if you’re still not sure, just make your best guess and move on. The chances are that whatever you choose, your editor will change it anyway!

Our American friends have a very good expression for this: Don’t sweat the small stuff.

2. Specialize

There are lots of other would-be freelance writers out there, so you need to do whatever you can to make yourself stand out. For me, anyway, that has meant specializing.

Specializing has all sorts of advantages for a freelance writer. If you are regarded as an “expert” in your field, editors and publishers will turn to you when they need a writer on the subject in question. In addition, because of your perceived expertise, you may be able to charge a higher rate than an “ordinary” freelance.

Don’t just stop at one specialism, though. Try to develop a number. My specialist subjects over the years have included self-employment, advertising and PR, careers, the Internet, gambling for profit, popular psychology, English grammar, writing for profit, personal finance, and several more. At least then, if there is a fall in demand for one of your specialisms, you have other strings to your bow.

My advice to a new writer would be to start with an area you know a lot about, or have a particular interest in, and make it your business to become an “expert” in that field. Write a few articles about it, perhaps for low-paying markets when you’re getting started. Once you have published some work on your specialism, people will start to regard you as an expert in it, and more work is likely to follow. By researching more articles and talking to “real” experts, you will build up your store of knowledge, until you really are something of an expert in your chosen field. It’s worked for me, anyway

3. Don’t Take Criticism Too Seriously

Don’t get me wrong, I’m not saying you shouldn’t listen to constructive feedback on your work. However, you should evaluate it carefully and be prepared to reject it if you don’t agree with it.

Remember that judgements about quality (or otherwise) are often subjective. There’s a story I tell in my CD course Write Any Book in Under 28 Days (more info here if you’re interested) about a time when I regularly wrote careers information articles for a large UK publishing house. These were basically four-page articles about different jobs.

I submitted my articles to one particular editor at the publishing house. Invariably they came back to me covered in red ink, with insertions, deletions and transpositions all over the place. I tried to learn from her comments and improve, but still every time the articles came back changed almost beyond recognition. She still put the edited articles through, but I honestly felt like a schoolboy whose report card read, “Could do better”.

Then I got a new editor – a man this time, as it happens. I submitted my latest article to him, and waited for it to come back to me covered in red ink as usual. And waited. And waited. So eventually I phoned him up and asked what had happened to my article. “Oh that,” he said, sounding surprised I had even mentioned it. “It was fine, so I put it through for publication.”

The truth is that in writing, as in life, everyone has different views of what is good and what is bad. So listen to criticism by all means, but try to evaluate it objectively, and always feel free to reject it if you think it’s wrong. And never, ever, take criticism personally.

4. Put Yourself About

However good a writer you are, no publisher or editor is going to beat a path to your door. Especially when you are starting out, you must be prepared to send off torrents of query letters, emails, book proposals, and so on. I first connected with one of my longest-standing clients, Lagoon Games, after I replied to an advertisement they placed in the Guardian newspaper twenty years ago. I am still working with Lagoon today, incidentally.

Put yourself about in the flesh too. Join your local writers’ circle, go on writers’ courses and conferences, volunteer to give talks, and run classes in adult education. In the online world, set up a writing homepage and/or a blog, and join at least one writers forum. And sign up at social networking sites such as Twitter, LinkedIn, and Facebook. All of this will help raise your profile as a writer, and make it more likely that potential clients will get in touch with you.

And also under this heading I’d add, build up your network of useful contacts. These can come from all sorts of places: fellow writers you meet, proofreaders and editors you work with, folk you meet on courses, people you interview for articles, people you connect with via online services such as Twitter, and so on. Many of the new writing opportunities that have come my way over the years did so as a result of networking.

5. Don’t Rely Solely on the Internet

Don’t get me wrong, the net is a wonderful thing, and there are lots of great resources on it for writers. However, there was no internet at all when I was starting out, and it didn’t hold me back!

If I was starting today, one thing I would certainly do is approach potential clients directly offering my services, including local companies, agencies and organizations. I would also read the job ads in newspapers and magazines, not only looking for writing jobs, but for businesses who are hiring in the fields of information management, PR, and so forth. They might well be in need of freelance writing assistance as well, and a speculative application could turn up a regular source of writing work. Again, this is a strategy that has worked well for me in the past.

6. Be Reliable

This is one of the most important qualities any client needs in a writer. He (or she) wants to be confident that you will deliver your article (or whatever) by the agreed deadline. If the deadline arrives and your article doesn’t, it can create all sorts of headaches for them.

If you can see you’re going to have problems meeting a deadline, therefore, DON’T just cross your fingers and hope for the best. Tell your client. Given sufficient notice they may be able to make alternative arrangements, e.g. bringing another article forward and postponing yours till next month. But if you don’t tell them in advance, it may be too late for this. Don’t then expect them to offer you any work in future.

7. Be Available

Clients sometimes need to contact writers at short notice, e.g. to check a fact or request a partial rewrite. You don’t have to be always just a phone call away (though that won’t hurt), but it should be possible for an editor to contact you by some means and get a reply within 24 hours. Always aim to have your mobile with you, therefore, and check this and your email regularly, preferably at least twice a day.

And if you’re going away on holiday for more than a day or two, it’s a courtesy to let the editor know, especially if you have just sent them some work!

8. Don’t Argue

OK, this one is a bit controversial. If you disagree with a client’s decision, you can say so. But don’t push it. At the end of the day, it’s her neck on the block, not yours, if she publishes your article and it goes down like a lead balloon with her readers.

Here’s an example from my own experience. In my capacity as a newsletter editor I was pitched an idea by a semi-regular contributor. Normally I liked his ideas, but for various reasons I couldn’t use this one, so I turned it down with a polite explanation. I then received a long, aggrieved email telling me quite forcibly that I was wrong and he was right, concluding with words to the effect, “I think I know our readership by now.” As you might guess, I didn’t commission many more articles from him after that…

9. Be Friendly but Professional

It’s good to build relationships with clients and editors. Over a period of time you will inevitably get to know one another quite well, and genuine friendships often result.

However, remember that the client is also – in effect – your employer, so it’s important to remain professional in all your dealings with them. Don’t assume that because ‘John’ or ‘Mary’ is your buddy, they won’t mind if you palm them off with inferior work or take other liberties with them.

Another example here (all names changed to protect those concerned). A few years ago one of my regular clients, a guy I’ll call Phil, was looking for an additional freelance writer. I recommended a woman named Clare to him, whom I’d worked with on a couple of projects.

All seemed to go well at first, and then I heard that he had dropped Clare quite suddenly. As I knew Phil pretty well, I asked him what had happened. He was a bit reticent at first, but then he told me, “We’re a family company, Nick, and we choose the people we work with very carefully.”

A little more probing finally revealed that he had been on the phone to Clare one day, and she casually dropped the F-bomb into their conversation two or three times. Phil hadn’t said anything to her at the time, but I guess he was a bit shocked by this. Anyway, he decided that he couldn’t work with her any more.

I must admit, I don’t know why Clare did this. Maybe she wanted to show she was “one of the boys”, or maybe she’d just been watching too many Hollywood movies. In any event, it was exactly the wrong tack to take with Phil, who abhors bad language in any form. And so it cost Clare the opportunity of a continuing source of well-paid work.

That’s perhaps an extreme example, but it does illustrate an important point. A good, friendly relationship between writer and editor/client can be very rewarding for both parties, but you should never let it become an excuse for behaving unprofessionally.

10. Be Enthusiastic!

One final thing experience (mine and other people’s) has taught me is that enthusiasm will carry you a long way as a writer. I’m sure it’s true in other fields as well, but clients generally are more inclined to hire writers who are enthusiastic about their work rather than those who seem simply to be going through the motions.

Obviously, you DO need in addition the writing skills and other qualities to deliver a good job. Without enthusiasm, however, you will probably never get the chance to demonstrate that you have these skills and qualities.

Look at it this way. If a client gets two applications, one from someone who is relatively inexperienced but brimming with enthusiasm and ideas, the other from someone with an impressive CV who sounds as though they could barely be bothered to get of bed this morning, nine times out of ten it’s the writer with the enthusiasm who will get the gig, even if they may not have as much experience. It’s human nature that we all respond better to people who radiate a positive attitude themselves.

So before sending off an application for any writing job, ask yourself honestly: Do I really sound as if I want this job? Do I appear excited by the prospect of working with this company? Can the client see that I am bursting with ideas and raring to do a good job for her? Or, conversely, does my application sound half-hearted? Does it sound as though I don’t really expect to get the job, and don’t much care one way or the other? If the latter is the case, hit “Delete” and start again. You MUST, MUST, MUST convey enthusiasm in all your applications and proposals!

I do hope you find these tips helpful. If you have any comments or questions – or any other useful tips for new writers – feel free to add them below as comments.

Happy writing!

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post from Cora Harrison, a UK blogger and vlogger (video blogger) whose website is called The Mini Millionaire.

Cora is a successful ‘comper’ who (as revealed below) has won over £20,000 worth of prizes from free-to-enter consumer competitions. In her article she explains how anyone can follow in her footsteps and shares her top tips and resources.

Over to Cora, then…

Twenty years ago my dad, a former miner, spent most of his night shifts listening to the radio answering tie-breaker questions. He won a number of prizes, his favourite of which was a cash lump sum that allowed him to purchase a greenhouse for our garden.

Twenty years later and in my young adulthood I’ve found myself with the same hobby of entering competitions to win prizes. Albeit, things are slightly different now. That’s of course due to the internet, which has seen radio and postal competitions decline in favour of email and web-based competitions – after all, this is a marketing promotion for businesses, and they are interested in creating product awareness and getting you to buy their product.

While I’ve only been a true ‘comper’ for the past three years, I’ve managed to win upwards of £20,000 worth of prizes, including a television, a number of nights and weekends away, a family trip to Universal Studios in Florida, a games console, and much, much more…

Today I want to present a basic introduction to what I believe to be one of the greatest hobbies ever – comping!

Table of Contents

Where To Find Competitions

Finding competitions has been made much easier since the birth of the internet. That’s thanks to database websites listing competitions, the answers to any questions asked, prizes on offer, closing dates, etc.

As well as checking these websites regularly, I also subscribe to Compers News. For £4.95 a month I get a monthly magazine posted direct to my door with a directory of great competitions, news articles from the world of comping, and an online forum providing me with connections to people who share the same interests as me.

How To Enter Competitions

There are a number of different ways in which competitions can be entered. Prior to the internet the main ways were phone calls and the post. And while these methods of entry still exist, they are much less common now.

Instead, as I mentioned in the introduction, you’ll find many more competitions that are online based. They may require you to sign up for a free account for a website, for example, or even to comment via your social media account.

My favourites are known as ‘creative competitions’. These often require you to make or design something. They can sometimes require a specific skill and take longer to enter than other competitions due to the effort required. But of course this has the effect of reducing the number of competing entries, and gives you the opportunity to use your skills to give your chances of success a big boost.

Here’s my girlfriend’s entry to a recent competition hosted by British Heart Foundation charity shops. This required you to use your sewing skills to upcycle an item of clothing from the store.

Unfortunately, she didn’t win the top prize of a European break for two. However, she had a fantastic time creating the outfit!

Hints and Tips

Now we know where to find competitions and how to enter them, I want to set out some basic hints and tips that should help you to enjoy your new found hobby of comping.

1. Only Enter Competitions For Prizes You Want To Win

Believe me when I say that there are thousands upon thousands of prizes available to win in the UK alone each and every month from competitions. And while some people choose to enter the competition regardless of the prize, I’d advise you to focus instead on a couple of items you’d like to win and enter those competitions specifically.

Spending more time on one entry rather than rushing through to enter as many competitions as possible is certainly going to increase your chances of winning those prizes you really want.

2. Don’t Get Discouraged

It’s easy to get discouraged in comping when you haven’t won a prize in a while. However, remember that everyone goes through a dry spell and absolutely any competition win is a great blessing.

Keep entering competitions for the prizes you want to win even when you’re feeling discouraged, though. You’re only going to win a prize if you enter the competition.

3. Get Creative With Your Entries

As I mentioned earlier, getting creative with your entries is a great way to extend this hobby into other areas of your life. We’ve created some fantastic photo entries, built forts from cardboard boxes, baked cakes, sewn outfits. You name it!

4. Hold ‘Comping Days’ With Friends And Family Members

Comping doesn’t have to be a lonely hobby. There are a number of comping clubs scattered across the UK and some national events hosted by the community. Even if you can’t attend one of the events in person get active within the online comping community in one of the many forums or Facebook groups.

Even consider having ‘comping days’ with your friends and family members. There are competitions exclusively for children that require them to be creative for a chance to win prizes. So consider getting some competitions for the children (or grandchildren) to do the next time they visit, for all the family to join in with.

Many thanks to Cora Harrison (pictured, right) for some great tips and resources.

When I was younger I entered quite a few competitions and won various prizes, including a crate of beer for devising a slogan for a brewing company. I also won third prize in a local radio competition where the top prize was a luxury Mediterranean cruise. Sadly, the third prize was just a leather passport holder and a book of travel tips. So near yet so far!

I do nevertheless think comping is a great sideline earner/hobby for older people. Age or disability are no barriers, and the costs are minimal. You can do it from the comfort of your home with the aid of the internet. It can help keep your grey cells active, and the lure of cash and prizes is hard to resist. So why not check out the resources in the article, including Cora’s own Mini Millionaire site, of course.

Good luck, and happy comping!

As always, if you have any questions about this article, for Cora or myself, please do post them below. And if you have any comping success stories or helpful hints and tips, do share them also!

If you enjoyed this post, please link to it on your own blog or social media:

I recently decided to take the plunge and put my personal pension into drawdown. As I know many Pounds & Sense readers will be thinking about doing this (sooner or later), I thought I would share my experience of the process here.

To give you some background, I am 62 and a semi-retired freelance writer. I still do some writing work – and run this blog! – but that doesn’t in itself produce enough income to live on. I am fortunate to have some savings and investments, but won’t qualify for my state pension until I am 66 (in about three-and-a-half years).

I do have a SIPP (Self Invested Personal Pension) with Bestinvest, though, so I decided I would put this into drawdown to give me another source of income. As you will know if you read this recent post, drawdown is one of the options open to you if you have a defined contribution pension. Once you are 55 or older, you can withdraw a quarter of your pension pot tax-free and (if you opt for drawdown) take a taxable income from the remainder. The balance stays invested until you withdraw it, and hopefully continues to grow.

Mine is not a massive pension pot – it came to about £56,000 – but my financial adviser and I worked out that if I draw £200 a month, assuming average growth of the remaining investments in my portfolio, it should last me until I am well into my 80s. I will also have the option to reduce the amount I draw once my state pension kicks in and/or to top up my pension fund to a modest degree in later years (see below). Yet another option will be to use the balance in my pension pot 10 to 15 years down the line to purchase an annuity, by which point the rate available on this will be higher.

The Process

I have been managing my SIPP online for over 10 years, but there wasn’t much on the Bestinvest website about how to put it into drawdown. So I phoned them up and asked.

The woman I spoke to said they would email an application form. This duly arrived as a PDF. I was pleased to discover that I could complete it on my PC (I use the free Foxit Reader for reading and editing PDFs).

The form had 10 pages. As well as the usual personal information, it wanted to know how much I wanted to draw from my pension and at what intervals. It also asked whether I wanted to take the tax-free lump sum straight away (I said yes).

The other things the form asked were a bit less predictable. There were quite a lot of questions about other pensions I might have. This didn’t apply to me, but they have to ask in order to check that you aren’t exceeding your lifetime allowance of just over a million pounds (I wish!).

The form also asked whether I had taken advice from the government’s Pension Wise service and/or an independent financial adviser. This did strike me as a bit nanny-ish, but as it happened I was able to say yes to both.

Clarifications

There were a few things I wasn’t clear about, so I phoned Bestinvest back and asked them. Here’s what I discovered. I hope this information may be useful to anyone who is in this situation or will be soon, as it doesn’t seem to be widely known.

First of all, I assumed that when paying out from my pension, my provider would simply sell off funds on a pro rata basis (I have about a dozen funds and shares in my pension account). This turned out not to be the case, though.

The woman at Bestinvest explained they don’t do this, as people often have their own views on which funds they want to sell and which they want to keep long term. So she told me I should sell enough funds via the BI website to cover my lump sum and also to cover my monthly payments going forward. To avoid delays she advised me to do this as soon as possible.

I therefore sold around £15,000 worth of funds from my account, to cover the lump sum I was withdrawing and the first few monthly payments. As the months go by I will obviously need to sell more of my holdings, but hopefully the cost will be balanced to some extent by the value of my remaining holdings going up.

I also discovered that my online account would continue to function exactly as it did before going into drawdown. The only difference is that the government imposes a lower limit of £4,000 (including tax relief) for any further investments in a SIPP after you have “crystallised” your pension (i.e. started drawing a taxable income from it). This rule is to avoid people withdrawing large sums and immediately reinvesting them to get another big chunk of tax relief, which I guess is fair enough. In any event, it’s good that I will have the ability to top up my pension from my other savings and investments by a few grand a year in future if my remaining pot starts to shrink too much.

After all this I submitted my form, and everything so far has gone as promised. It took about a month for the tax-free lump sum to appear in my bank account, and around six weeks to get my first monthly payment. I had heard some horror stories about large “emergency deductions” being made from the latter by HMRC to cover any possible tax liability, but discovered they weren’t applying any deductions at source to my payments. Of course, I will have to add this money to my total taxable income for the year, and if it exceeds my personal allowance I will have to pay tax on it.

So that was my experience of putting my Bestinvest SIPP into drawdown. As of August 2018, I can legitimately describe myself as a pensioner! If you have any comments or questions, naturally, please do post them below.

Disclosure: This post includes affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my fellow money blogger Perry Wilson, who blogs at Stupid is the Norm.

Perry has some important advice for anyone over fifty who thinks they have left it too late to boost their income in later life.

Over to Perry then…

Okay. So you’re in your 50s, and while you’re not yet in retirement, if you stand on your tip-toes you can see it from where you are now.

You’ve definitely got more years behind you than you have in front of you. Maybe thinking ‘should have stuck in at school’? Or ‘I really screwed up’? ‘It’s too late now?’

Correct to the first two, wrong to the last one.

Let’s say you’re 55. Average mortality age for males is 79.4, and females 83.1. So, you have another 25 or so years left.

25 years. Hmm. If we go back 25 years, you’d only be 30 years old. Knowing what you know now, what advice would you give your 30-year-old self?

You’d advise yourself to do things differently, wouldn’t you? That’s good, because it means you’re taking responsibility for your current position. It’s an empowering admission because it puts the power of change in YOUR hands. It’s down to you. Master of your own destiny, and all that stuff.

Now, return to the present. You have (on average) 25 years left. There LITERALLY is no time to waste, and tinkering around at the edges is insufficient. You need to take ‘massive action’ (as Tony Robbins would say).

You have to put any pride to one side and do something extraordinary. Work more hours. Try something different. Something unfamiliar. Doing the same thing, something familiar, will get you what to have now – and it’s not enough.

I have a friend who decided to work eight hours overtime per week. That’s equivalent to a 20% pay rise. Extra money which he now invests.

I have another friend who delivers takeaways two evenings per week and makes a whopping £160 per week cash (and a free supper each night). An extra income of £8300 pa!

I do matched betting which regularly makes me £200 per week for half an hour’s work per day.

Be an Uber driver. Sell stuff on eBay. Start a blog and monetize it. Massive action.

Alternatively, do nothing. To do or not to do? That is the question. (Thanks, William).

Thinking and planning are important. But it’s action that changes things. Nothing changes until you take action.

Doing nothing is what normal people do. But that’s not you. If you’re still reading this it means you’re extraordinary. Different. Deserving of better.

Act now.

Don’t be Stupid and don’t be Normal.

Many thanks to Perry for some cogent advice. Do check out his Stupid is the Norm blog for more ideas and inspiration.

I agree absolutely with Perry that it’s never too late to boost your income, whether you are in your fifties, sixties, seventies, or older.

Indeed, there is a lot to be said for creating additional income streams whatever your age. For one thing, the extra cash can help boost quality of life for you and your loved ones. But beyond that, having an extra income source makes you less reliant on your salary or pension, and gives you additional options. It can also help keep your brain sharp and flexible, and provide the opportunity to be creative, meet new people, and learn new skills (or apply old ones).

On Pounds and Sense I regularly feature sideline-earning opportunities such as those mentioned by Perry, and many others too. No matter what your age or background, there are ‘side hustles’ (to use the modern vernacular) you really can make a start on today.

As always, if you have any comments or questions – for me or for Perry – please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Peer-to-peer (P2P) lending involves lending money to people and businesses via a P2P platform (generally web-based) and being paid back with interest by the borrower.

P2P lending has become increasingly popular among savers looking for better interest rates than those offered by banks and building societies. Until quite recently, however, you couldn’t invest in them tax-free.

All that changed in April 2016, though, with the launch of the Innovative Finance ISA, or IFISA for short. IFISAs allow anyone to invest tax-free in P2P lending via authorized platforms.

You can put any amount into an IFISA up to your annual ISA allowance. In the current 2018/19 tax year this is £20,000, which can be divided however you choose between a cash ISA, a stocks and shares ISA and an IFISA. So, for example, you could invest £10,000 in a cash ISA, £6,000 in a stocks and shares ISA and £4,000 in an IFISA.

Note that under current rules you are only allowed to invest new money in one of each type of ISA in a tax year. It is though generally possible to transfer money from one type of ISA to another without it affecting your annual entitlement (although there may be platform fees to pay).

After a slow start when only a very few were available, in 2018 the number and range of IFISAs has grown significantly. As of July 2018 over 40 UK IFISA providers are operating, ranging from well-established P2P lenders such as Zopa to new, upcoming platforms such as The Just ISA (see below). Interest rates paid vary considerably, from around 4% to 15%. Obviously, the higher rates reflect the higher levels of risk involved.

Although all IFISAs involve P2P lending, a number of different types are available. Those currently on offer include lending for all the following purposes:

property development

business loans

personal loans

green energy projects

bonds and debentures

entertainment industry loans

infrastructure projects

An unusual IFISA which certainly lives up to the “Innovative” description is The Just ISA. This is described as a litigation ISA. Lenders’ money is used to help individuals fund the cost of taking businesses, institutions and individuals to court, typically for reasons of professional negligence.

The Just ISA offers five-year bonds paying a gross interest rate of 8% per year (in practice this headline rate will be reduced somewhat due to fees and charges). All cases are underwritten and fully insured, and they say they have a success rate of 90%. There is a minimum investment of £2,000.

What Are The Risks?

All UK IFISA providers have to be authorized by the Financial Conduct Authority (FCA) and HMRC. This doesn’t in itself protect lenders (or savers if you prefer) against the failure of a platform, however. While savers with UK banks and building societies are covered by the government’s Financial Services Compensation Scheme (FSCS), which guarantees to reimburse up to £85,000 of losses, this does not apply to IFISA platforms.

All IFISA providers do offer various safeguards to lenders, though. These vary, but include provision funds to cover potential losses, insurance policies, and so forth. In many cases, also, loans are made against the security of property or other assets, which in the worst case could be sold to pay off any debts.

Even so, IFISA lenders don’t enjoy the same level of protection in the UK as bank savers. This is, of course, a major reason why the returns on offer are significantly higher. It’s therefore important to be aware of the risks and ensure you are comfortable with them before investing this way. It’s also important to lend across a range of platforms and loans, and not make the mistake of putting all your savings eggs in one P2P lending basket.

Summing Up

If you are looking for a home for some of your savings that can offer better interest rates than banks and building societies and won’t incur any tax charges, IFISAs are definitely worth considering.

As well as the higher interest rates, they can add diversity to your investments, helping you ride out financial peaks and troughs. Just be aware of the risks involved in P2P lending, and ensure you invest in IFISAs only as part of a balanced portfolio.

Disclosure: this is a sponsored post on behalf of The Just ISA. All investments carry a degree of risk. Be sure to do your own “due diligence” before investing, and speak to a qualified professional financial adviser if in any doubt before proceeding.

If you have any comments or questions about this post, as always, feel free to post them below.

If you enjoyed this post, please link to it on your own blog or social media:

TaskRabbit puts people who need various sorts of chore performed in touch with those who have the time and skills to do them (for a fee, of course). The company calls the people who work via its platform “taskers”.

A huge range of skills are required, including gardening, flat-pack furniture assembly, household repairs, parcel delivery, cleaning, moving and packing, pet sitting, laundry and ironing, event staffing, and many more. Clients can even hire taskers to queue up for them at product launches, buy theatre tickets, and so on.

Once a tasker has been hired they go and do the job, with payment handled automatically through TaskRabbit. The company takes 30% of the fee charged, with the remainder going to the tasker.

How Do You Become a Tasker?

As mentioned above, currently you have to live in or near London, Birmingham, Bristol or Manchester.

Beyond that, you need to be 18 or over in the UK and able to offer some of the types of skill listed on the TaskRabbit website. In practice the great majority of people should be able to do at least one of these.

You need to have a UK bank account and credit card, and must also have a smartphone. Tasks are allocated and managed via the TaskRabbit app, which is available for both Android and Apple iOS.

If you meet these requirements – and can provide some sort of personal identification – you can apply via the TaskRabbit website. Once your application is approved, you can expect an invitation to a two-hour orientation session where the TaskRabbit system is explained in detail and any questions can be answered.

After that, it is simply a matter of downloading the app, looking for tasks you can do in your area, and applying for them.

TaskRabbit Pros and Cons

Clearly nobody is going to get rich working as a tasker. You will be paid an hourly rate, which for many jobs is likely to be little more than the national minimum wage. You will be competing against other taskers for jobs, which can have the effect of pushing rates down.

In addition, your status will be that of a self-employed contractor. That means you won’t be eligible for holiday pay or sick pay, or any of the other benefits employees routinely enjoy (although this may change in future). Neither is there any guarantee you will have paying work from one week to the next.

For all those reasons, TaskRabbit is unlikely to be a good choice if you need a full-time income. On the other hand, it does have the big benefit of flexibility. You can work at times convenient to you, perhaps to supplement other earnings or save towards a holiday or other major purchase.

Another attraction of TaskRabbit is the variety of the work. Every task is different, and brings with it the opportunity to meet new people and do new things. This can be a welcome contrast for those whose normal jobs may be monotonous and/or solitary.

TaskRabbit can be a great resource for self-employed people, to provide income when other work is scarce. It can also be a good option for those with health problems and/or caring responsibilities who are unable to do a full-time job. Retired and semi-retired people – which of course includes many Pounds and Sense readers – can also supplement their income this way.

And finally, TaskRabbit can open doors for tradesmen/women looking for new clients. You might, for example, tackle a small repair job and mention to the client that you are also available for bigger projects if the need arises in future. Be sure you have a good supply of business cards to hand out!

As already mentioned, TaskRabbit is only available in certain cities. There are, though, many other opportunities in the gig economy if this type of opportunity interests you. Some of these such as Viewber I have talked about in previous posts on Pounds and Sense. Another is Deliveroo, which offers the chance to earn a sideline income delivering meals for restaurants and takeaways. You can learn more about Deliveroo here if you wish.

Summing up, TaskRabbit offers anyone the opportunity to earn extra income doing small jobs of all kinds. If that sounds like something that might interest you, visit the TaskRabbit website for further information and to sign up.

As ever, if you have any comments or questions about TaskRabbit, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Right now the UK is sweltering in a summer heatwave that shows no sign of ending any time soon.

Many people are enjoying the warm sun, but when it goes on for days/weeks on end it can become tiring and debilitating. And for older people and those with chronic health conditions especially, it can be extremely uncomfortable and have a harmful effect on health. Heat exhaustion and (especially) heat stroke are potentially very serious conditions.

So today I thought I’d share some tips on keeping cool and healthy in the heat. I also asked some of my fellow UK bloggers for their top tips as well, so I’ll be sharing them here too.

I’ll start with my own tips, though…

1. Drink plenty of fluids, preferably water. It’s a well-known fact that in older people the sense of thirst doesn’t always work so well and it’s easy to get dehydrated without realising it. Aim to top up your fluids regularly, and have a bottle, jug or at least a glass of water beside you at all times.

2. Sprinkle water over your skin and/or clothes to help stay cool.

3. In the hot weather, fans can be lifesavers. There are plenty of different models on sale in shops and supermarkets and online stores such as Amazon. If you can, get one with variable speeds, so you can adjust it according to conditions. You can even get fans with remote controls, like this one:

4. If you work at a computer, consider buying a USB fan. I bought one for just £4 from my local Morrisons and it is keeping me cool while I write this blog post! They are also available very cheaply on Amazon – like the one below, for example.

5. Air conditioning is wonderful in this weather. But in the UK few people have it in their homes, as it’s bulky, expensive to buy and run, and would only be useful occasionally. A cheap and cheerful alternative is to freeze bottles of water (plastic not glass) and put them in front of a fan – this will help cool the air passing through. You can also buy personal air coolers such as the one below which work on the same principle. They are cheap enough, although not having tried one I can’t vouch for how effective they would be!

6. Shut windows and draw the curtains or blinds when it is hotter outside. This will help keep hot air and radiant heat from the sun out. You can open the windows for ventilation when it is cooler.

7. Check up regularly on friends, relatives and neighbours who may be less able to look after themselves.

More Cool Tips!

As mentioned above, I also asked some of my UK blogging colleagues for their tips and ideas. Here is a selection. I have put my own comments in italics after them where relevant.

That’s a great idea! I found a similar one on Amazon (see image link below).

Laura Dempster from Thrifty Londoner wrote: “I like to keep hydrated in the hot weather (like we all do!). If I’m going out and about sometimes I will put a water bottle in the freezer overnight. Since it’s so hot, as soon as I go outside the ice begins to melt and it means my drink stays that little bit cooler for longer.”

That’s a nice, easy tip! Just be sure to use plastic bottles rather than glass.

Nicola Kaye from Mum on a Budget wrote: “I have filled up an empty spray bottle with a mixture of water and Aloe Vera gel (shake well) – I have been spraying it on my face and neck a few times a day, it is really cooling.

Yep, great idea. It would of course work with plain water too.

Mel Trudgett of Mel’s Money Mindset commented: “When I was in my early 20s I went to Spain in the middle of August and stayed in a cheap hotel with no air-con! It was well over 45 degrees in our room overnight. I found that the only thing that helped me was putting a cold, damp cloth on my feet and one on my head. This really helped to cool me down and I was able to sleep. I still do this if my daughter has a fever. I also run cold water on my wrists (or put a frozen bottle of water on them) and that cools me down very quickly.

Claudia Vogt from Retro Claude said: “It makes your house look like a squatter’s den, but if you tape the reflective blankets that athletes use at the end of races to your windows it really helps to keep the heat out. They are only about £3 from Amazon. I know lots of mums do this with babies’ bedrooms in the heat.

Here’s an image link to the sort of thing Claudia means (I assume) on Amazon.

Victoria Elizabeth Currell of Our Life on Sea said: “I keep my blinds drawn upstairs and the windows only open a fraction during the day in the heat. Then as soon as it gets a little cooler in the evening I open my windows wide. This way it keeps the hot air out during the day and allows the cooler air in for the evening. I’ve started that this year and it has totally changed the temperature of the upstairs of my house.”

Michelle Rice of Utterly Scrummy Food for Families wrote: “I put four wet face cloths in a bag in the freezer for my children to cool down after school. I also freeze their water bottles for packed lunches.”

Natalie Ray of Plutonium Sox suggested “Open water swimming! I swim in the river every Monday morning. Great for cooling down and the perfect way to start the week. It’s free too!

Appealing as it sounds, open water swimming probably isn’t for everyone, but even swimming in a pool can be a great way to cool down. I belong to the Virgin Active club in Lichfield which has both indoor and outdoor pools. I make as much use as I can of the latter!

Jane Hanson of Lady Janey wrote: “Drink lots of tea! Scientific studies have shown that hot beverages can actually cool you down on a hot day.”

I do like a nice cup of tea 🙂 The science behind this is described in this article on the Huffington Post site. Apparently it works by making you lose more heat through sweating. This won’t work so well on muggy, humid days, though.

Amanda Shortman of The Family Patch offered two suggestions: “(1) Cool down the pulse points (wrists, neck, etc) by either running under water or using a cool pack. I find this cools me down far more effectively than anything else. And (2) drink things like coconut water to try and help keep a good balance of electrolytes. I have only just started this, but I am already finding that it helps reduce some of the more extreme fatigue and dizziness I experience in this heat as opposed to simply drinking water all day. I get the small 330ml cartons and have one of those a day along with plenty of water.”

Lynn James who blogs as Mrs Mummypenny said: “Get a diddy paddling pool (we were sent a foldaway one from Aldi and it’s perfect) and cool your feet down in it. If your feet are cool the rest of your body will cool down as well. Drinks tons of water, and I mean three litres a day. Hydration is so important in this weather

Sue Foster from Suefoster.info wrote: “When I can’t sleep at night I wet a towel and wring it out, then lay it over me. This cools the body down, so I can get some sleep.”

Thanks to everyone who contributed suggestions, and apologies to those whose tips I wasn’t able to use, mainly because they were too similar to others listed.

As always, feel free to leave any comments or questions below. And of course, if you have any other suggestions for keeping cool in the heat, please do post them also.

Disclosure: This article includes affiliate links to some Amazon products. If you click through these and make a purchase, I will receive a small commission. This will not affect the price you are charged by Amazon in any way.

If you enjoyed this post, please link to it on your own blog or social media:

Many thanks to Cora Harrison (pictured, right) for some great tips and resources.

Many thanks to Cora Harrison (pictured, right) for some great tips and resources.