For better or worse, Britain will have a General Election on Thursday 4th July 2024.

I have seen several articles urging young people to register so they can cast their vote when the time comes. Of course, it is right that in any democracy as many eligible people as possible register and turn out to vote. However, it is just as essential that older people also have their say.

As Pounds and Sense is aimed primarily at over-fifties, I therefore wanted to take the opportunity to encourage you to apply now for a postal vote if this might help you exercise your democratic right to vote.

Having a postal vote means that if ill health, frailty or disability prevent you getting to a polling station, you still have the opportunity to express your political preference. Likewise, you won’t have to worry about obstacles such as bad weather or a lack of transport on the day to get to the polling station.

Any registered voter in the UK can apply for a postal vote. This includes:

British citizens living in the UK

British citizens living abroad (overseas voters)

Commonwealth and Irish citizens residing in the UK

In England, Scotland and Wales (though not Northern Ireland – see below) you will not normally have to give any reason for wanting a postal vote and one should be granted automatically if you apply.

I assume that most readers of this blog will have registered to vote in elections already, but if by chance you haven’t, here’s a link to the relevant website. You must register by 11:59 pm on Tuesday 18th June to vote in the General Election on 4th July.

How to Apply

To get a postal vote for the forthcoming election, you must apply before:

5 pm on Weds June 19th if you live in England, Scotland or Wales

5 pm on Fri June 14th if you live in Northern Ireland

In England, Scotland or Wales, you can obtain a postal vote application form from several sources:

In Northern Ireland, people wanting to vote by post have to fill out a form and send it to the electoral office in Belfast. These forms can be found online here.

The postal vote application form requires the following details:

Your personal details (name, address, date of birth).

Your address where the postal ballot should be sent.

The reason for requesting a postal vote if applicable. Voters in Northern Ireland are always required to give a reason when they apply.

Make sure to fill in all sections accurately to avoid delays or rejections.

Once completed, you must return the form to your local Electoral Registration Office. This can be done by post or hand delivery. It’s important to ensure the form arrives before the deadline, which is usually 11 working days before election day. Late applications will not be accepted.

Receiving and Returning Your Postal Vote

After your application is approved, you will receive your postal voting pack, which includes:

a ballot paper

instructions on how to complete your vote

a postal voting statement, which you must sign and provide your date of birth.

a return envelope

To cast your vote:

Mark your ballot paper according to the instructions.

Seal your ballot paper in the envelope provided.

Complete and sign the postal voting statement.

Place both the sealed ballot envelope and the signed statement in the return envelope.

Post your vote back as soon as possible to ensure it is received in time. It must reach the Electoral Registration Office by 10 pm on election day to be counted.

Tips for Postal Voting

Send your vote early to avoid postal delays and ensure your application is processed in time.

Double-check all details on your application and voting pack.

Follow the instructions carefully to ensure your vote is valid.

If you haven’t received your postal voting pack one week before the election, contact your local Electoral Registration Office immediately.

Be aware that if you have applied to vote by post, you cannot vote in person at a polling station. However, on election day you can return your postal vote to any polling station in your local authority area (before 10 pm) or to the Returning Officer at your local council (before they close) if you don’t want to post it or it’s too late to post it.

Closing Thoughts

The next government, whatever its political hue, will have to address a range of issues that are of great importance to older people. Prominent among these is the cost of long-term care (and who will bear it), but there are many other areas of concern, including pensions and benefits, the NHS, public transport, housing, law and order, immigration, the cost of living, national security and defence, and so on.

So it really is important to ensure that nothing prevents you casting your vote when the time comes. Registering for a postal vote is one way to ensure that ill-health, frailty or disability do not rob you of the opportunity to exercise your democratic right.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a four-night break on the Isle of Man. It was actually the first time I had ever visited the island, so it’s fair to say I was approaching it with fresh eyes!

For this break I went on a heritage-railway-themed holiday with Newmarket Holidays – here’s a link to the package I booked. I paid a single fee, discussed in more detail below. This included four nights half board in a four-star hotel in the island capital Douglas and my flights to and from the island from Birmingham Airport. The fee I paid also covered transfers from and to Ronaldsay Airport on the IOM and various other things, which I’ll discuss shortly.

For those who don’t know, the Isle of Man is in the Irish Sea, about half way between England and Ireland. It is 32 miles long and – at its widest point – 14 miles across. It covers a total area of around 221 square miles, That makes it nearly five times bigger than Jersey, the largest of the Channel Islands. It is a self-governing British Crown dependency. You can read more about the Isle of Man in this Wikipedia article.

Here is a map of the island from Google Maps…

Flights

As mentioned I flew to the Isle of Man from Birmingham, getting a taxi to and from the airport.

I’d have to say my experience at Birmingham Airport on the outward journey was poor. A lot of building work was going on to install new luggage scanners. As a result the usual queuing areas and escalators were unavailable and passengers had to queue for ages, first to get into lifts to the departures area and then to get through security. I spent almost two hours queuing and by the time I was through it was the final call for my flight. So I then had a mad dash to get to the gate in time. Thankfully I just made it; I’m sure others weren’t as lucky.

The flights were with Scottish airline LoganAir and were actually very good. The isle of Man only attracts relatively small numbers of visitors, so they use small planes and boarding is quick and easy. I was also impressed to be offered free refreshments on both the outward and return flights (something I haven’t experienced on a holiday flight for many years). It took around 50 minutes to get from Birmingham to the IOM, so that was quick and easy too. Of course, if you don’t like flying, you also have the option of going to the island by ferry from Liverpool or Heysham.

I should mention that the return flight back to Birmingham was easy in comparison. Because it’s regarded as a domestic destination, passengers returning to the UK from the IOM don’t have to go through security or passport control. I was out of the airport no more than 15 minutes after landing.

Accommodation

I stayed in a four-star hotel called The Mannin in Douglas. The hotel is just off the main promenade and several other Newmarket Holidays guests were staying there as well.

The hotel room had all the amenities needed for a short stay, including a comfortable double bed, a flat-screen TV, a fridge and electric kettle, and plenty of drawer and wardrobe space. It had an en-suite bathroom with a modern power shower that worked well, with plenty of hot water.

One thing the room didn’t have was a window to the outside world. It had a window leading out to a small balcony, but this was actually within the hotel, overlooking the bar and restaurant area. You may not be surprised to hear that I didn’t use this during my stay 😏

As mentioned, I was staying half-board. Breakfasts were buffet-style and included everything you’d expect, including cooked items such as bacon, sausages, tomatoes, mushrooms and fried or poached eggs (no scrambled, though). I was pleased to discover that the evening meals included my choice of starter, main meal and dessert, with even the most expensive items such as steak at no extra cost. My one slight reservation was that, barring the soup and fish of the day, the menu was the same every night . If I had been staying any longer I might have found this a bit limited. That’s only a very small criticism, though.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £1,305 (including VAT) for my four-night visit. That might sound a lot, but as mentioned it included my flights to and from the island, coach transfers, and most meals, along with various other services and amenities. I stayed in a double room with single occupancy, so obviously paid a bit more than a couple would have (pro rata). And finally, I was in a premium four-star hotel. Some other guests were in three-star hotels which I guess would have been a bit cheaper. As a matter of interest, I had to choose the Mannin as it was the only option offered to me when I booked with Newmarket. I guess all the cheaper accommodation had been snapped up already!

The price I paid also included the services of a tour guide, Trevor. He was a local man (from Peel) and extremely knowledgeable about the island. He looked after us very well and even sprang into action when I couldn’t get the top off an ice-cream tub I had bought 🍦😅 Each morning we were picked up by a double-decker bus with Trevor on board. This took us to whatever destination we were visiting first that day (typically a railway station).

Also included in the cost were Isle of Man ‘Go Explore Heritage Cards’. These provided free admission to all the main tourist attractions and also covered travel on the island’s trains and buses. As a result, I actually spent very little extra money during my break – just the odd bit for refreshments during the day and any souvenirs I chose to pick up.

Things To Do

I won’t give you a blow-by-blow account of everything I did on my visit – you can see the full itinerary on the Newmarket Holidays page if you like. I will share some highlights and personal recommendations, though.

1. Douglas: The Capital

This is where I stayed. It is a vibrant, bustling place, with an attractive beach and picturesque promenade you can stroll along. In Douglas you can find the Manx Museum to delve into the island’s history. You can also enjoy a night at the Gaiety Theatre, a beautifully restored Victorian venue offering a variety of performances.

2. Castletown and Castle Rushen

Castletown is the ancient capital of the Isle of Man. Castle Rushen (photo below), one of Europe’s best-preserved medieval castles, is here with its impressive structure and exhibits detailing the island’s past. Also in Castletown you can see the Old House of Keys, the island’s original legislative centre. The trip I was on included admission to the Old House of Keys and an entertaining hour-long interactive presentation there about the island’s history. You would have to book this in advance if not travelling with an organised group.

3. Peel and Peel Castle

The town of Peel is on the island’s west coast and well worth a visit. You can explore the atmospheric ruins of Peel Castle (photo below), and enjoy fresh seafood at one of the local eateries. The House of Manannan museum provides an immersive experience into the island’s Celtic, Viking, and maritime history. You could easily spend a full day here!

4. The TT Mountain Course

For motorsport enthusiasts, the Isle of Man TT (Tourist Trophy) races are legendary. Even outside of race season, you can drive or cycle the 37.73-mile TT Mountain Course, taking in spectacular views and imagining the thrill of the races.

5. Laxey Wheel and Snaefell

The Great Laxey Wheel (see cover image), also known as Lady Isabella, is the largest working waterwheel in the world. If you’re brave (and fit) enough you can go up the spiral steps to a viewing platform at the top. Nearby, the Snaefell Mountain Railway takes you to the island’s highest point. On a clear day it’s said you can see seven kingdoms from here: England, Ireland, Scotland, Wales, the Isle of Man itself, and the kingdoms of Heaven (the sky) and Neptune (the sea). On a more prosaic note, at the top is a nice cafe where you can buy excellent coffee and home-made cake 🍰

6. Isle of Man Steam Railway and Manx Electric Railway

I was on a railway-themed holiday, so naturally this included trips on both of these. The steam railway (photo above) runs through beautiful countryside from Douglas to Port Erin at the southern tip of the island. You get some lovely views of the coast along the way.

The Manx Electric Railway (photo below) also runs from Douglas but in the opposite direction, towards Laxey and then on to Ramsey. The Manx Electric Railway has two carriages, one covered and one open to the elements (referred to colloquially as The Toast Rack!). I went on both during my stay. You get better views from the open carriage but it can be a bit chilly, so remember to wrap up well!

Quick Tips

Here are a few tips for first-time visitors to the Isle of Man based on my own experience and other information gleaned…

1. Plan for the Weather

The Isle of Man has a maritime climate, meaning weather can be unpredictable. It’s advisable to pack layers and waterproofs to stay comfortable regardless of the conditions. That being said, I was extremely lucky on my trip and enjoyed wall-to-wall sunshine.

2. Embrace the Outdoors

With its stunning landscapes, the island is perfect for outdoor activities. Walk a segment of the Raad ny Foillan (Way of the Gull) coastal path, explore glens and waterfalls, or enjoy cycling and bird-watching.

3. Sample Local Delicacies

Don’t miss out on trying Manx kippers, queenies (small scallops), and the island’s renowned ice cream. Local pubs and restaurants often feature these and other regional specialties.

4. Respect Local Traditions

The Isle of Man has a unique culture and traditions, including its own language, Manx Gaelic. You might hear locals using expressions like “Failt Erriu” (Welcome) and it’s appreciated if you can master one or two phrases like this. There are also various superstitions on the island. One of the first I discovered concerned the fairy bridge (quite near the airport). The tour guide told us we must all say “Hello, fairies” as our coach passed over this or bad luck might befall us. Needless to say, everyone complied!

5. Use Contactless Payments

Most places accept contactless payments, but it’s wise to have some cash on hand for smaller vendors and rural areas. Note that if paying by cash you may receive change in Manx notes and coins which are not generally accepted outside the Isle of Man. UK banks will usually exchange Manx banknotes but not coins, so if you get any in your change you will have to keep them as souvenirs, donate them, or hold on to them for your next visit. You can ask retailers if they have UK money available as change, but that is not guaranteed 🙂

Closing Thoughts

As you may gather I enjoyed my holiday on the Isle of Man and am happy to recommend both the island itself and the Newmarket Holidays tour I went on.

The Isle of Man is verdant and charming, with a long and interesting history. Obviously the heritage railways are a particular attraction (for me at any rate!), but so too are the castles at Peel and Castletown and the Great Wheel at Laxey (a beautiful village with a range of other tourist attractions as well). But it’s also a wonderful place to be out walking or cycling, with quiet roads (outside the TT races obviously) and a dramatic and unspoiled coastline. I would definitely like to return there before too long.

As always, if you have any comments or questions about this post, please do leave them below. Also, if you have visited the Isle of Man yourself and have any additional tips or recommendations, I would love to hear them!

If you enjoyed this post, please link to it on your own blog or social media:

I was recently offered the chance to review the Simba Hybrid Mattress Topper (see cover photo). This is a premium mattress topper from the well-known Simba sleep brand.

I must admit, incidentally, I hadn’t realised the variety of sleep products Simba offer. I knew about their mattresses, of course, but wasn’t aware they also sell quilts, pillows, mattress toppers, and so on.

I currently sleep on a Slumberland king-sized mattress which – despite being barely three years old – is starting to sag. My sleep quality had deteriorated and I was waking up with an aching back and hips. Not good at all 🙁 So when I got the opportunity to test out Simba’s hybrid mattress topper, naturally I leapt at it.

I have tried mattress toppers before, and in fact got a cheap one from Amazon prior to receiving the Simba product. It helped a little but clearly wasn’t going to be the solution for me.

The Simba hybrid mattress topper takes sleep comfort to a whole new level. For starters, it’s deeper and heavier than my previous mattress topper. It came rolled up in a (very) large cardboard box. I wrestled it upstairs and opened it without any help (nobody else being around at the time) but ideally I’d say this is a two-person job.

The mattress topper comes tightly wrapped in a clear plastic bag. Once I removed it from this, it lay flat on the bed without curling. Unlike some sleep products I have ordered in the past, you don’t have to wait for it to expand to its full depth.

From the first night onward I was hugely impressed with the Simba hybrid mattress topper. It is no exaggeration to say that it felt as though I was sleeping on a brand new mattress. It is smooth, cool and comfortable to lie on and (for me anyway) offers just the right medium-to-firm level of support. I am sleeping deeper and longer before waking, and the aches and pains in my back and hips are a thing of the past.

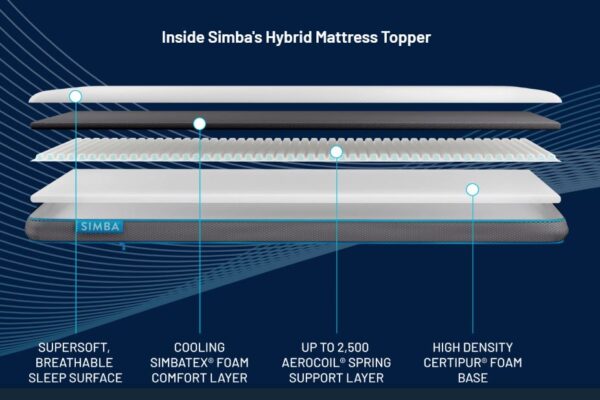

I thought it might be useful to reproduce here the diagram from the Simba web page showing how their hybrid mattress topper is constructed and the different layers it contains…

As you can see, the Simba hybrid mattress topper includes a number of different layers (hence the ‘hybrid’ in the name, I assume). You can read more about this on the Simba web page, but briefly at the top there is a soft, breathable sleep surface, with a foam comfort layer under that. In the middle is a spring support layer (just like in a mattress), with a high-density foam base below that. This is very different from most cheap mattress toppers, which are basically just quilts with a cotton/polyester filling.

Obviously because of its layered structure, you can’t turn the Simba hybrid mattress topper over. You can rotate it from end to end though, and it’s probably a good idea to do so occasionally to even out wear. No instructions are provided about this, however, so that’s purely a suggestion, based on my previous experience with mattresses.

Are there any drawbacks to the Simba hybrid mattress topper? Well, I did notice a slight ‘chemical’ smell which took a few days to disperse. It didn’t bother me, but ideally you might want to let your new mattress topper air for a day or two before starting to use it. I’m afraid I was too impatient to wait, though!

In addition, as this mattress topper contains springs, I wouldn’t recommend trying to wash it (it wouldn’t fit in a standard washing machine anyway!). It does though come with a removable, washable cover. Essentially, you need to treat this product as if it was a mini-mattress in its own right. That isn’t really a drawback to the Simba hybrid mattress topper, just a feature of it.

Overall, I am happy to give the Simba hybrid mattress topper my highest personal recommendation. If – like me – you have an old mattress that is starting to sag, it should prolong its useful life. Also, if you have a mattress that is too hard, it should make it softer and more comfortable for you. It’s not cheap (at the time of writing £219 for the single version or £329 for the king-size I received) – but, as so often in life, you get what you pay for. Easy payment by interest-free instalments (up to 12 months) is also available subject to status.

I should add as well that delivery is free and fast: next working day if you order before 2 pm or two working days if you order after 2 pm. There is also a range of options for buying a Simba double topper.

Many thanks again to my friends at Simba for allowing me to try out their hybrid mattress topper. If you have any comments or questions about this post, as ever, please do post them below as usual.

Disclosure: This is a sponsored post (gifted product).

If you enjoyed this post, please link to it on your own blog or social media:

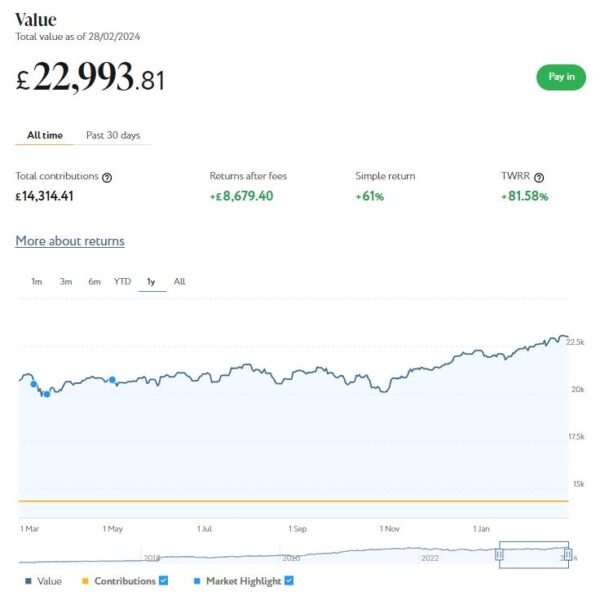

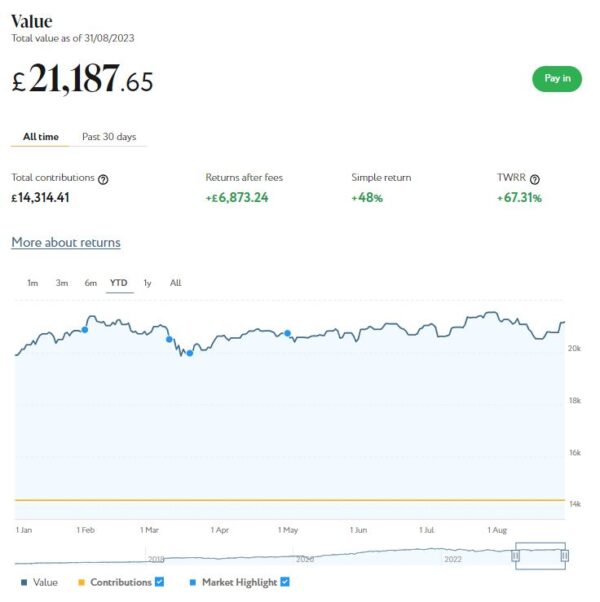

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £ £22,994. Last month it stood at £22,386 so that is a welcome increase of £608.

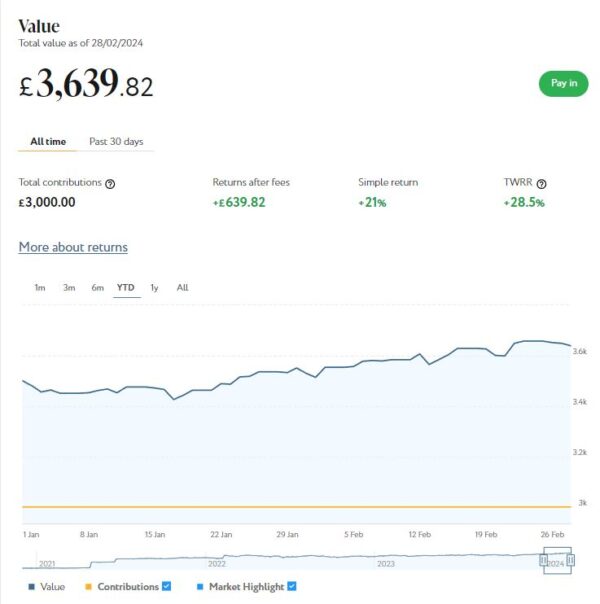

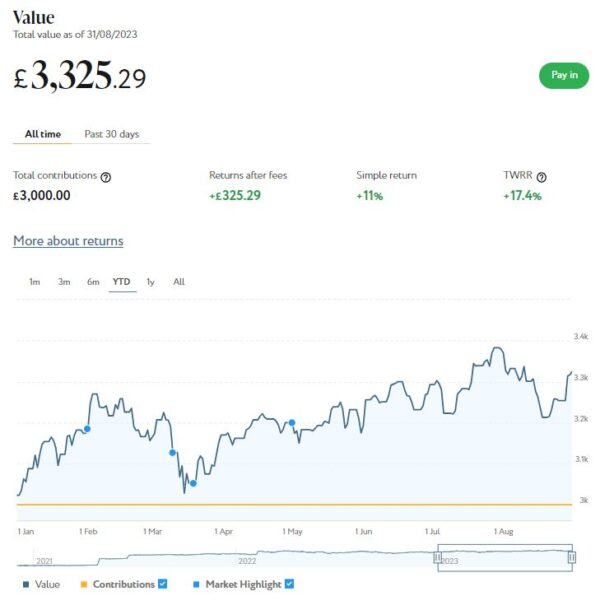

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,640 compared with £3,530 a month ago, a rise of £110. Here is a screen capture showing performance over the last 12 months.

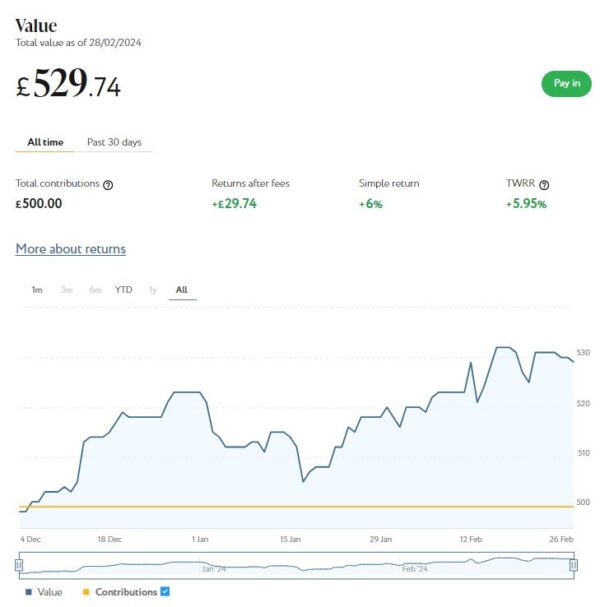

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £530, an increase of £11 since last month and £30 or 6% over the three-month period since I first invested.

February was obviously a good month for my Nutmeg investments. Overall I was up £737 or 2.79%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £168.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £40.01, meaning that overall (rental income minus capital value decrease) I am up by £128.52. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

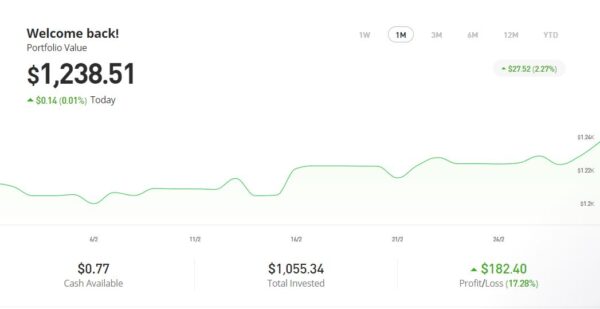

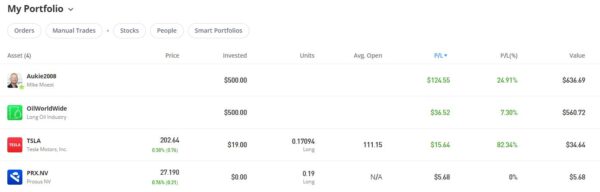

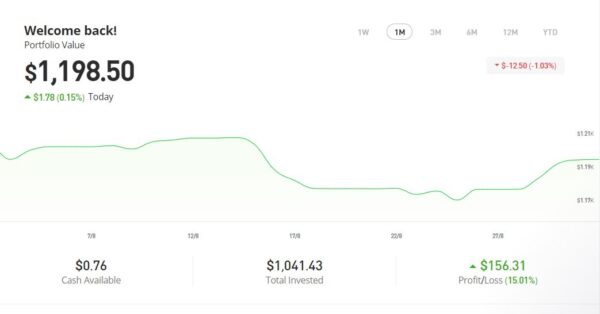

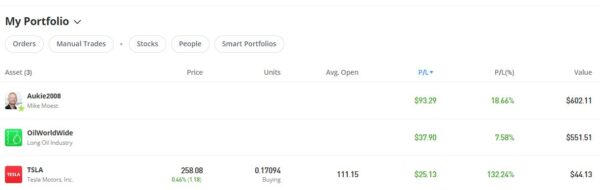

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,238.51, an overall increase of $216.25 or 21.15%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Motoring. Like everything else in life the cost of motoring is going up and up, so in this article I set out a variety of ways – from ride-sharing to driving for fuel economy – you may be able to reduce it.

Also in February Mouthy Money published Are You Making the Most of Your Annual ISA Allowance?. As mentioned earlier, the 2023/24 tax year ends in just a few weeks’ time. And after that the £20,000 tax-free ISA allowance for that year will be gone forever. In this article I describe the different types of ISA – Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA (LISA) – and explain how they work and the differences between them. I also provide some tips and advice for making the most of your annual ISA allowance.

My final article published on Mouthy Money last month was Can You Save Money on Your Shopping with JamDoughnut? Regular PAS readers will know that I am a fan of the JamDoughnut app, which enables you to save up to 20% on purchases with a growing range of retailers. The article also reveals how you can get a £2 head-start by using my referral code.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Frugal Skills to Save You Money sets out a selection of life skills that can save you money (and aren’t hard to learn). You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in February. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Get Your Will Written Free of Charge in March I revealed how you can get your will written (or updated) free of charge during Free Wills Month. This regular event supports a range of leading charities. Obviously the hope is that you will include a bequest to charity in your will, but there is absolutely no obligation to do this. Free Wills Month is now up and running. If you want to take advantage and get your will written free, I recommend acting now as there are only limited spots available.

Also in March I published a guest post titled Building Your Own Home – It’s Not Just for the Super Rich! This post was written on behalf of Suffolk Building Society, who are trying to raise awareness of the self-build option in the UK. As they say in the article, they can provide mortgages to purchase land suitable for self-build projects. SBS emphasize that this option is suitable and available for ‘ordinary people’, not just the super-rich folk you see on TV shows like Grand Designs!

I also published Saving for a Rainy Day or a Stormy Breakup? The Surprising Facts About Secret Savings Accounts. This post is based on some eye-opening research from my friends at Smart Money People, which revealed (among other things) that one in ten people in a serious relationship, including marriage, civil partnerships, or cohabitation, maintain a secret savings account. Find out more in this post.

Also, from January this year I became a regular contributor to the new Over 60s Discounts website. You can read my latest article here: Who Cares for the Carers? This is about help available for unpaid carers in the UK, both financial and practical. I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

One other thing is that this month I switched my Santander 123 Lite current account to a Santander Edge current account. I will try to find time to write a separate post about this soon. But briefly, my main reason was because having an Edge current account allows you to open an Edge savings account, which offers a market-leading 7% interest rate (AER) for amounts of up to £4,000 for one year (it then falls to 4.5% AER).

The Santander Edge account has slightly higher fees (£3 a month as opposed to £2) and the cashback on offer is slightly less. However, when I crunched the numbers, the value of having an Edge savings account easily outweighed this. Though I am fortunate in that I had £4,000 I could put into it immediately from another, lower-paying savings account. If I hadn’t had that, it wouldn’t have been worth switching to the Edge account.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Mother’s Day is coming, so here’s a chance to make it extra special for one lucky winner!

I’ve joined forces with some of my fellow UK bloggers in this giveaway with multiple prizes. Entering the giveaway is free of charge and full instructions can be found below.

There are multiple ways to enter, and the more you do, the better your chances of winning. But note that where an entry requires following a social media account, you will need to continue following this account until the winner has been drawn on Sunday 10th March 2024 (Mother’s Day). Before the winner is announced the organisers will check that they are still following the account in question. If not, they will be disqualified and another winner drawn.

This giveaway has been organised by my fellow blogger Rowena Becker, who blogs at My Balancing Act. Please check out her blog and those of the other talented bloggers taking part (listed below). And read on for full details from Rowena of all the prizes on offer and how you could win this great prize bundle!

Welcome to the ultimate Mother’s Day Giveaway and Gift Guide! This is brought to you by a collaboration of some of the UK’s leading bloggers.

We understand that finding the perfect gift to express gratitude and love for the special women in our lives can be a daunting task. That’s why we’ve come together to curate an exceptional selection of prizes that are sure to delight any mother.

This guide not only aims to make your gift shopping easier but also adds an exciting twist with a giveaway that could win you these wonderful items.

Join us in celebrating motherhood this year by taking part in this fantastic opportunity to spoil your mum – or yourself! Show her just how much she means to you ❤

Meet the Bloggers

In order to be able to bring you this incredible giveaway, some of the UK’s top bloggers got together. A massive thank you to our bloggers! The bloggers taking part are:

Art File Jungle Animals 1000 Piece Jigsaw Puzzle from Gibsons Games

Delight in the vibrant Art File Jungle Animals 1000 Piece Jigsaw Puzzle. A tribute to the diverse beauty of our planet’s wildlife. Crafted with precision and creativity by an award-winning designer from The Art File, this puzzle captures the essence of nature’s splendour. As a joint venture between Gibsons Games and The Art File, two renowned British family businesses, this jigsaw puzzle represents their shared commitment to quality and innovation.

Each of the 1000 pieces contributes to a stunning visual experience, making it not just a puzzle but a piece of art. This makes it an excellent gift for mums who appreciate both the challenge of a jigsaw and the aesthetics of fine art. Plus, it’s part of our exciting prize bundle – a perfect blend of challenge, relaxation, and artistic appreciation.

Liquid Silk Perfect Cleansing Oil (100ml) from DJUSIE

Introducing Liquid Silk Cleansing Oil, the ultimate cleansing oil that will leave your skin feeling smooth and rejuvenated. Designed for all skin types and ages, this luxurious oil delivers a refreshing clean to both oily and dry skin, leaving it perfectly balanced and radiant. Not only is it functional. It also provides a luscious sensory experience with its effortless formula to even remove waterproof makeup.

The refreshing and uplifting scent of lime, red grapefruit, jasmine, and geranium creates a fruity and nuanced aroma that will invigorate your senses. This luxurious blend not only nourishes your skin but also has a positive impact on your mood. The application process is simple. Massage a few drops onto dry skin in circular motions to dissolve impurities and makeup. Then rinse with water. Your mum will be left with soft, supple, and glowing skin that she’ll love. We have one to giveaway to our lucky prize winner!

Pure Shea Butter (180ml) from Aviela

Next up on our pamper list is the 100% pure, highest grade unrefined Shea butter. The perfect choice of gift to show our appreciation and love for the incredible mothers or women in our lives. Packed with essential fatty acids, vitamins A and E, with natural soothing properties, the Shea butter deeply hydrates and nourishes the skin. It quickly absorbs into the skin, leaving it supple and glowing while also creating a protective barrier to prevent moisture loss. This makes it an ideal addition to any skincare routine for all skin types.

The luxurious butter, suitable for use from hair to toe, offers exceptional hydration, outstanding nourishment, and remarkable skin-softening effects for all skin types. It’s particularly effective in combating dryness and soothing irritated skin. As part of our Mother’s Day giveaway, we’re excited to offer one lucky winner the chance to experience these benefits firsthand. Don’t miss out on your opportunity to win this sumptuous treat for your skin!

TIMELESS RENEWAL BIO-RETINOL BODY OIL (100ml) from Evolve Organic Beauty

Evolve Organic Beauty’s latest addition to the age-defying product line, this divinely scented firming body oil is a treat for all skin types, including dry ones. The blend of Retinol analogue Bidens Pilosa, Hyaluronic Acid, Organic Macadamia Oil, and Apricot oils work in harmony to nourish, firm, rejuvenate and smooth your skin while also improving its elasticity and locking in hydration for a youthful glow.

Infused with the organic essential oils of Rose Geranium, Ylang Ylang and Mandarin, the timeless renewal bio-retinol body oil not only pampers your skin but also delights your senses. This Mother’s Day, consider gifting this luxurious body oil to the most important woman in your life. It’s a thoughtful gift that shows you care about her well-being and is part of our Mother’s Day prize bundle. This product is more than just skincare. It’s a chance for her to indulge in a moment of self-care, making it the perfect gift for any occasion.

Paradise Luxury Gloss (Colour: Spell) from Doll Smash Cosmetics

Presenting the Paradise Luxury Gloss from Doll Smash Cosmetics. A luxe lip enhancer that promises brilliant shine, a smooth look, and a luscious feel. This high-quality gloss is designed to elevate your lips while diminishing any imperfections. Its unique formula is far from the sticky or tacky feel of traditional lip glosses. Instead offering a soft, creamy texture that leaves your lips feeling deliciously smooth. The immediate, radiant shine it delivers makes it an instant favourite.

As part of our prize bundle, this gloss makes an excellent gift for mums who appreciate a touch of luxury in their makeup routine. It’s more than just a gloss – it’s a ticket to a pampering experience that every mum deserves.

£50 Amazon Voucher from Make Money Without A Job

Make Money Without A Job is donating a £50 Amazon Voucher to our lucky winner! Check out Make Money Without A Job if you’re looking for ways to earn extra money. Because Make Money Without A Job does exactly what it says. There are over 3,000 articles about making money from side hustles and starting your own business. Whether you want to make £100 a month or £5,000 a month there are ideas for everyone!

What’s more, there’s a free daily draw to win £10, and if it isn’t claimed, the prize rolls over. They’ve given away multiple prizes over £100 to lucky winners. Check out the draw at www.makemoneywithoutajob.com/draw

How to Enter

You can enter the Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collected, and one winner will be randomly chosen via Rafflecopter. Good luck!

The giveaway will run from 8 pm 3rd March 2024 to 8 pm 10th March 2024.

The winners will be notified by email from rowena@mybalancingact.co.uk

The winner will have 7 days to respond after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, X, YouTube, BlogLovin or Pinterest or any other social media platform.

Prize open to over 18s only. Age verification may be required to receive some prizes.

Some or all of the prizes may take a few weeks to arrive.

If any prizes are out of stock then we will do our best to find a suitable replacement but cannot guarantee it.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage.

Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace these.

In the unlikely event one of the companies withdraws a prize, we cannot offer an alternative.

The winner’s name will be stated on some or all of our bloggers’ websites and announced on Twitter and other social media channels. It will also be displayed on the Rafflecopter entry form. By entering this prize draw, you give your permission for this.

Please note the winner may have the same name as you so if you see your name displayed, be aware that you are not the winner unless you have been notified by us.

There may be some delays in receiving prizes.

Good luck, and I hope a Pounds and Sense reader wins this wonderful prize bundle!

If you enjoyed this post, please link to it on your own blog or social media:

SBS are keen to demystify self-build and show it’s not just for wealthy people on Grand Designs!

As part of this, they recently commissioned research which highlights the misconceptions that still exist about self-build. The research was undertaken among 2,000 UK adults by Opinium on behalf of Suffolk Building Society.

Read on to discover how self-build may be more accessible than you think…

According to research from Suffolk Building Society, over two-thirds (69%) of potential self-builders do not know that some mortgage lenders will allow them to borrow to purchase land where planning permission has been granted.

Correspondingly, concern over financing a project was the number one barrier for those interested in self-build: other concerns were around seeking planning permission and difficulties in finding suitable land.

The Society believes the lack of awareness about being able to borrow for land may discourage people from considering self-build. Many incorrectly believe they either need to be sufficiently cash-rich to fund the land themselves before applying for a self-build mortgage, or be gifted a plot from land-owning family members.

Suffolk Building Society is aiming to normalize self-build and, in doing so, wants more people to know that self-build is a viable option for those with modest budgets. Its recent research found that over half (54%) of those who are considering a self-build at some point in the future believe that self-build is still reserved only for the very wealthy.

Richard Norrington, Chief Executive at Suffolk Building Society said: “Self-build television series undoubtedly make for great viewing, but they do set the bar remarkably high. One could easily assume that self-build is only for those with unlimited time and deep pockets.

“Self-build is considered a fairly standard route to home ownership in countries such as Hungary, France, and Sweden, and with better education and awareness, self-build could become more mainstream here in the UK too.”

Who Is Considering Self Build and Why?

The cost of living crisis has not significantly dampened people’s appetite for self-build: a third of people are still considering self-build, which is only a small decrease from 35% last time this survey was undertaken in July 2020.

The propensity to consider a self-build decreases with age: younger people in their 20s (60%) and 30s (56%) are significantly more interested than those in their 50s (16%) and 60s (7%), dispelling the myth that self-build is a project for retirement.

Of those considering self-build, 31% would prefer to go for a completely new build, 27% said they would opt for a knockdown/rebuild project, and 21% said they would undertake a major renovation to an existing property.

The main motivation cited by over a quarter (28%) was the ability to design the layout of their own home, but this is a significant drop from 51% in 2020. There was a broader range of reasons evident in this year’s research, including self-build being a more affordable way of creating an ideal home (15%) and having a home in the right location (12%). One in ten (9%) of those considering a self-build are doing so to create a home suitable for multiple generations under one roof.

Over four in five (83%) want to make eco-friendly decisions about their future property. However, of these, seven in ten would only prioritize this if it was within their budget. This is, of course, reflective of the current economic environment.

Self Build Register Awareness

The Self-build and Custom Housebuilding Act 2015 requires each relevant local authority to keep a register of individuals who are seeking to acquire serviced plots of land in the authority’s area for their self-build project.

Data published on 31 March 2023 showed a decline in individuals joining the Self Build Registers, which tallies with the research from Suffolk Building Society:

Only one in five potential self-builders (21%) are signed up to the Self Build Register and 41% of those considering self-build had not even heard of the Self Build Register.

Richard Norrington said: “The National Custom and Self Build Association campaigned diligently for the Self Build Registers in a bid to facilitate a greater number of self-build homes. But so far, this has not been realized. The Registers need promoting alongside resources that help people understand all that a self-build entails as, despite the current economic uncertainty, there is clearly still an appetite for self-build.

“As a country, we need to normalize self-build, encouraging regular people to build good homes, thus helping to reduce the housing shortage in the process and improving the collective carbon footprint of our housing stock.

“There are undoubtedly more hurdles in this process than in a standard house purchase – particularly at the moment with high labour and material costs. However, being able to design a property that meets your needs both in terms of function and aesthetics is hugely rewarding. We would like more people to know that some lenders are ready and willing to lend on land as well as for the build itself; and secondly, that self-build is more accessible than they might have previously thought.”

Many thanks to Suffolk Building Society for allowing me to reproduce their research – and comments about it – here.

If you would like more info about self-build mortgages from SBS, you can visit the relevant page of their website via this link. SBS say that although 80% of their members are in the east of England, the rest live across the UK.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Christmas is coming, so here’s a chance to make it extra special for one lucky winner! I’ve joined forces with some of my fellow UK bloggers in this festive giveaway with prizes valued at over£700 in total.

Entering the giveaway is free of charge and full instructions can be found below. There are multiple ways to enter, and the more you do, the better your chances of winning.

But note that where an entry requires following a social media account, you will need to continue following this account until the winner has been drawn on 19 December 2023. Before the winner is announced the organisers will check that they are still following the account in question. If not, they will be disqualified and another winner drawn.

This giveaway has been organised by my fellow blogger Rowena Becker, who blogs at My Balancing Act. Please check out her blog and those of the other talented bloggers taking part (listed below). And read on for full details from Rowena of all the prizes on offer and how you could win this mammoth bundle!

The Great Bloggers Holiday Giveaway and Gift Guide

We are back for another Christmas Holiday Giveaway and Gift Guide! Some of the UK’s top bloggers have united to bring you the most incredible holiday bundle of prizes.

Last year’s giveaway proved to be very popular and this year is just as exciting, with so many prizes for one lucky winner to make their family’s Christmas dreams come true. In fact, we have hundreds of pounds worth of holiday goodies and gifts!

The Bloggers

In order to be able to bring you this incredible giveaway, some of the UK’s top bloggers got together and contributed. A massive thank-you to them all! The bloggers taking part are:

Lenovo ThinkPad X13 Gen 1 i5-10210U [Quad] 1.60GHz 13.3″ FHD IPS TOUCH HDMI USB-C 16GB DDR4 256GB NVMe from Tier1

You have a chance to win the powerful Lenovo ThinkPad X13 Gen 1, featuring an i5-10210U [Quad] 1.60GHz processor, a stunning 13.3″ FHD IPS TOUCH screen, HDMI and USB-C ports, a whopping 16GB DDR4 RAM, and a speedy 256GB NVMe storage. This premium laptop is all you need for your work or play!

This prize is brought to you by Tier1, your destination for affordable and eco-friendly tech gifts. Why are Tier1 gifts perfect for Christmas? It’s simple – they’re good for your pocket and good for our planet. With Tier1, you get top-notch tech without breaking the bank, contributing to a more sustainable future. Their products are professionally refurbished, assuring quality and reliability while reducing electronic waste. So if you thought you couldn’t afford to buy tech gifts for your loved ones, head on over to Tier1 for affordable gifts with the wow factor to make your holidays bright and green!

Hairy Biker’s Family-Sized Soup Maker

Get ready for a festive feast with our Christmas Giveaway! Enter now for a chance to win the Hairy Biker’s 1.6L Family Sized Soup Maker with Integrated Scales. This 1000W powerhouse is all you need to whip up delicious, heartwarming soups this holiday season.

Why is this soup maker a must-have in your kitchen? It’s not just about the delicious soups you can create. It’s also about saving time and money. With its integrated scales, you can easily measure ingredients directly into the soup maker – no need for extra dishes. Plus, it cooks up soups quickly and efficiently, giving you more time to enjoy with your loved ones. But that’s not all. Making homemade soup means you control what goes in, helping you avoid the high salt and sugar content often found in canned soups. You can use up leftovers, reducing waste and saving money.

So don’t miss out on this opportunity to make your Christmas cooking easier and healthier. Enter our Christmas Giveaway today and bring home the Hairy Biker’s 1.6L Family Sized Soup Maker as part of your prize!

Life Coaching Sessions Worth £200!

Start the New Year on a high with two life coaching sessions from Lauren Jane Coaching. Lauren helps women invest in themselves, find clarity and balance in their lives, and be at ease with themselves at home and in their careers. She coaches from the inside and allows her clients the space to get truly honest with themselves, helping them to hit the pause button, get more clarity in their lives, move forward with purpose – and feel really good about it! What better way to start 2024?!

Being stressed out, overwhelmed, out of balance, anxious or stuck in any area of your personal, business, or career world can make life feel like hard work, especially following the busy holiday season! Lauren is offering two free sessions to help our winner build on their inner belief, confidence and sense of self-worth until they shift and tune into a new perspective for themselves and their life.

Liiton The Peaks Whiskey Glasses

When you join our special Christmas Giveaway, you will have a chance to win an elegant Set of 4 Liiton The Peaks Whiskey Glasses. This is an incredible gift that’s perfect for the festive season.

The Peaks Whiskey Glasses Set is a dream come true for any whiskey lover. Each glass is crafted using X1 Crystalline and features a true precision glass sculpture of iconic mountains Denali, Mont Blanc, K2 and Mt. Fuji. Weighing in at 1lb each, the glasses have the Patented Chill-Charge System™ which chills down your drink in just 18 seconds. They not only look stunning, but if you swirl the spirits gently around the faces of the Peaks, you will unlock the beautiful whiskey aromas.

This set of 4 glasses ensures you’re always ready to share a toast with friends or family during the holiday season. Made from high-quality materials, these glasses are durable and beautifully crafted, making them a standout addition to any home bar or drinkware collection.

FinaMill

Join our exciting Christmas Giveaway and stand a chance to win a FinaMill! This unique gift is an excellent addition to any kitchen, especially during the festive season.

A FinaMill is more than just a kitchen tool. It’s a game-changer for any home cook or chef. With a Sleek, minimalist design, this mill effortlessly grinds spices and herbs at just a touch of a button, releasing their full flavour and aroma right when you need them. Whether you’re preparing a holiday feast or baking Christmas cookies, this Finamill can help elevate your dishes, making every meal more memorable. Plus, its stylish design adds a touch of sophistication to your kitchen decor.

Don’t miss out on the opportunity to enhance your cooking experience this Christmas. Enter our giveaway now for a chance to win this Finamill in Stone along with other amazing prizes!

Rectangle 3-D Crystal Photo Gift from Forever-Always

Get into the festive spirit with our Christmas Giveaway and stand a chance to win a truly unique gift – the Rectangle 3-D Crystal Photo Gift from Forever-Always in size medium (9cm W x 6cm H x 6cm). This is a special present that’s perfect for capturing cherished memories.

The Rectangle 3-D Crystal Photo Gift is a stunning piece of personalised decor. Your chosen photo is created into a beautiful 3-D image that seems to float inside. It’s a wonderful way to immortalise a precious moment or loved one, making it an exceptionally thoughtful gift. Whether it’s a picture of a family gathering, a beloved pet, or a memorable holiday, this crystal photo gift brings your memories to life in an artistic and beautiful way. Displayed on a mantelpiece, bookshelf, or desk, it adds a touch of elegance and personal touch to any space.

Opinel Folding Saw

As part of our giveaway, we’ve got a prize from Opinel that will delight any outdoor enthusiast. The Opinel Folding Saw is an essential tool for every nature lover. Whether you need to cut firewood for a cosy campfire or prune branches for a clearer path during your forest adventures, this folding saw is your perfect companion. Crafted with Opinel’s signature commitment to quality, it offers durability, precision, and ease of use that makes it stand out in its category.

This Christmas, one lucky winner will have the chance to claim this fantastic tool as their own. So why wait? Enter our Christmas Giveaway now and make this festive season truly unforgettable. With the Opinel Folding Saw, you’ll be fully equipped for your next outdoor adventure. Let the festivities begin!

Graco’s FoldLite LX

As part of our festive Christmas Giveaway, you have a chance to win the perfect item for families on the go – the Graco FoldLite™ LX travel cot.

This travel cot with basinet is perfect for those with little ones, from birth to approx. 3 years (max. 15kg) and the Bassinet from birth to approx. 6 months (max. 9kg).Graco’s FoldLite LX travel cot offers a comfy space for your baby to sleep or play, no matter where your adventures take you. Lightweight and easily foldable, it’s designed for maximum portability for when you are away from home.

Don’t miss this opportunity to win a gift that brings convenience and comfort to the little ones. Enter our Christmas Giveaway now for a chance to win Graco’s FoldLite LX travel cot, among other fantastic prizes!

French Navy Patent Chelsea Boot from Start-Rite

Start-Rite is a British heritage brand that specialises in children’s footwear that enables healthy development whilst creating stylish designs that appeal to parents and children. The French Navy patent Chelsea boot is no exception, and it’s the perfect footwear for your kids over the holiday season.

Whatever the adventure, this stylish boot from Start-Rite will carry little feet through any day in comfort. The inside zip fastening is useful for getting boots on and off quickly and with ease, and the durable sole is ready for any adventure. Crafted in elegant French navy patent with check elastic, the Chelsea French navy patent boots will make any outfit complete. Our winner can choose the size and receive this as part of their prize!

Learning Resources Brainbolt® Genius

Get ready to supercharge your memory this holiday season with our Christmas Giveaway! This year, we’re excited to include the Learning Resources Brainbolt® Genius in our prize bundle. Brainbolt® Genius is a mind-challenging game that tests your memory skills to the max. It lights up different sequences, and your job is to remember and replicate them.

It’s a fun and exciting way to keep your brain active and sharp. Whether you’re playing alone or with friends and family, Brainbolt® Genius keeps the competition lively and the fun rolling. It’s compact and portable, perfect for on-the-go entertainment during holiday travels. So why not give your memory a festive boost? Enter our Christmas Giveaway now and stand a chance to win the Brainbolt® Genius, along with other fantastic prizes. It’s the perfect gift for keeping minds active and engaged over the holiday season!

SAVEUR Selects® Artisan Non-Stick Loaf Pan

Get ready to add a dash of elegance and convenience to your holiday baking with our exciting Christmas Giveaway! This festive season, you stand a chance to win the exquisite SAVEUR Selects® Artisan Non-Stick Loaf Pan – 10″ as part of the prize bundle. This isn’t just a baking essential, it’s a gift that promises to make your kitchen experiences more delightful and your festive goodies more delicious.

The SAVEUR Selects® Artisan Non-Stick Loaf Pan is a coveted item for any home baker. It’s not just a baking tool; it’s a craft of art and functionality combined. This pan, crafted from high-quality, durable materials, boasts a non-stick surface that means your baked loaves slide out perfectly every single time. No more worries about your bread sticking or crumbling!

Whether you’re planning to bake a traditional Christmas fruitcake filled with rich, dried fruits and nuts, a moist and luscious banana bread, or perhaps you’re in the mood to experiment with some new, creative recipes, this loaf pan is your perfect partner. Its generous 10-inch size ensures you can create substantial loaves to share and spread the festive cheer among family and friends.

So why wait? Enter our Christmas Giveaway now for a chance to win this premium Loaf Pan, along with other fantastic prizes! This could be the perfect opportunity to elevate your baking game this festive season. Let the aroma of freshly baked loaves fill your home and hearts this Christmas.

Little Brian’s Paint Sticks Christmas Window Kit

Light up your holiday season with our Christmas Giveaway! This year, we’re thrilled to include Little Brian’s Paint Sticks Christmas Window Kit in our prize bundle. This fantastic kit lets your little ones bring the magic of Christmas right into your home. It includes a range of vibrant, mess-free paint sticks and stencils that make it easy for kids to create festive window decorations. Whether it’s snowflakes, reindeer, or Santa himself, your kids can paint their favourite Christmas motifs directly onto the windows.

The paint sticks are incredibly easy to use and dry quickly, leaving no mess behind. So why not add a dash of creativity to your Christmas celebrations? Enter our Christmas giveaway now for a chance to win the Little Brian’s Paint Sticks Christmas Window Kit [affiliate], along with other exciting prizes. Unleash your child’s artistic talent and fill your home with festive cheer this holiday season!

EUGY Christmas Elf

We’re thrilled to announce that a charming EUGY Christmas Elf is part of our prize bundle. This delightful elf, brought to life by EUGY, is more than just a cute decoration. It’s a symbol of EUGY’s commitment to protecting the planet. Made from recyclable card and printed with natural eco-friendly ink, this little elf is as green as it is adorable. What’s more, it’s assembled with non-toxic glue, making it safe for kids and adults alike. It’s a fun, creative, and sustainable way to add a touch of magic to your holiday celebrations.

So why wait? Enter our Christmas giveaway now for a chance to bring home this eco-friendly EUGY Christmas Elf [affiliate] along with other exciting prizes.

Elf Toy from Elf for Christmas

We’re excited to announce that a delightful Elf Toy from Elf for Christmas is part of our prize bundle.

But here’s the best part – the winner gets to choose their very own elf! These charming elves are not just toys but a wonderful addition to your family’s Christmas celebrations, bringing joy, wonder, and a touch of elfin magic to your home.

So don’t miss out – enter our Christmas Giveaway now for a chance to welcome a new elf friend into your home this holiday season!

Gold Star Costume ‘Shining Light in the Night’

We’re thrilled to include Pretend to Bee’s enchanting Gold Star Costume ‘Shining Light in the Night’ in our prize bundle.

This twinkling costume is perfect for your little star to shine bright during the festive season. It’s more than just a costume; it’s a ticket to a world of imagination where your child can become a shining beacon.

Don’t miss this chance to make your child’s Christmas extra special. Enter our Christmas Giveaway now for a chance to win this magical Gold Star Costume along with other fantastic prizes. Let’s light up this Christmas with joy and imagination!

Family First Aid Kit from LittleLife

The Family First Aid Kit from LittleLife is your must-have companion and proudly a Silver award winner, voted for parents as Best Travel Product for Under £30, in the prestigious Mother & Baby Awards 2024. Whether at home or away, this compact kit ensures peace of mind for you and your loved ones. With everything from Sudocrem, scissors, and tweezers to bandages, dressings, and antiseptic wipes, it’s the ultimate solution for any minor accidents. The Family First Aid Kit is great to take with you for any days out or travelling you do over the holiday season and we have one to give away as part of our prize bundle.

Every Piece of You Puzzle from Gibson Games

The Gibson Games Puzzle, “Every Piece of You,’’ is a captivating 1000-piece jigsaw puzzle that reminds us to celebrate the weird and wonderful pieces of ourselves in a fun and colourful style. Created by Katie Abey, this is not your ordinary jigsaw puzzle.The illustrations of the puzzle represent real people and their stories. Made from 100% recycled puzzle board and with vegetable based inks, this is the perfect gift for any jigsaw lover.

Play-Doh Air Clay Super Colour Bucket

The Play-Doh Air Clay Super Colour Bucket is a fun and colourful part of our Christmas Prize Bundle. Packed with 15 vibrant colours, ten cutter moulds, two handy tools, and an inspirational sculpting guide, it’s perfect for unleashing your kid’s creativity with modelling clay this festive season!

How to Enter:

You can enter the Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collected, and one winner will be randomly chosen via Rafflecopter. Good luck!

The giveaway will run from 7 pm 9th December 2023 to 11.59 pm 19th December 2023.

The winners will be notified by email from rowena@mybalancingact.co.uk

The winner will have 7 days to respond, after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, X, YouTube, BlogLovin or Pinterest or any other social media platform.

Prize open to over 18s only. Age verification may be required to receive some prizes.

Some or all of the prizes may arrive after Christmas and may take a few weeks to arrive. We will do our best to get them to you before Christmas but this is not guaranteed.

If any prizes are out of stock then we will do our best to find a suitable replacement but cannot guarantee it.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage.

Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace these. In the unlikely event that one of the companies withdraws a prize, we cannot offer an alternative.

The winner’s name will be stated on some or all of our bloggers’ websites and announced on Twitter and other social media channels. It will also be displayed on the Rafflecopter entry form. By entering this prize draw, you give your permission for this.

Please note the winner may have the same name as you so if you see your name displayed, be aware that you are not the winner unless you have been notified by us.

There may be some delays in receiving prizes.

Good luck, and I hope a Pounds and Sense reader wins this fabulous prize bundle!

Disclosure: This post includes some affiliate links.

If you enjoyed this post, please link to it on your own blog or social media:

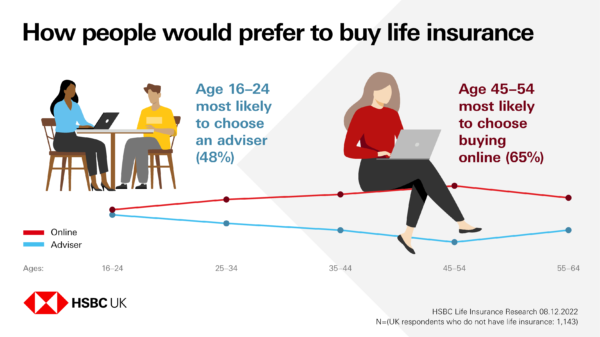

Today I am sharing some interesting data from my friends at HSBC regarding how British people choose life insurance.

This information comes from an online survey of over 2,000 people in the UK conducted on behalf of HSBC Life Insurance. It provides some interesting insights into who is – and isn’t – getting life insurance, and their reasons for doing so.

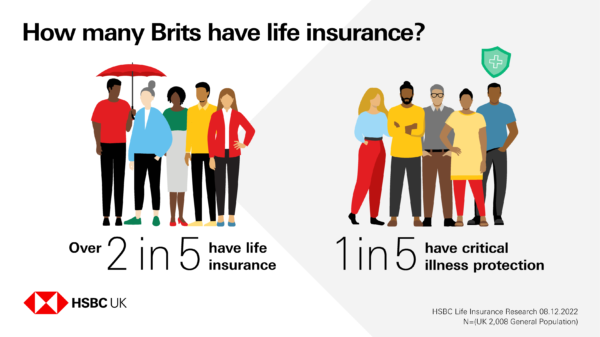

As you can see from the graphic below, the study revealed that more than two in five people in the UK have life insurance (43%), with another one in five (20%) saying they have critical illness protection. The latter provides protection (generally in the form of a one-off tax-free payment) if you become seriously ill or injured. It is typically purchased in addition to life insurance.

Financial worries are a key factor for those Brits who have researched their options but still decided against getting life insurance. One in two (50%) who’ve considered getting a policy but decided not to go ahead say that it’s because they’ve had to tighten their belts.

Reasons for Choosing a Policy and a Provider

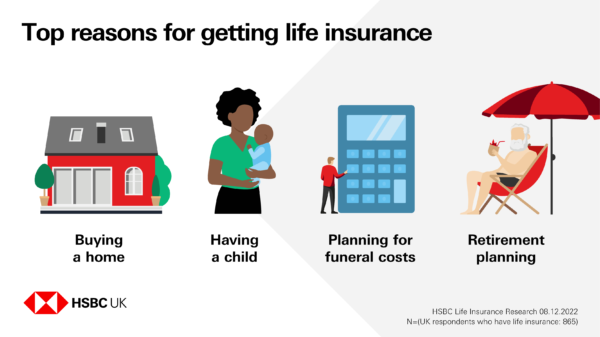

Brits with a policy said the primary reasons they got life insurance were: buying a home (19%), having a child (14%), planning for funeral costs (10%) and retirement planning (9%).

Perhaps surprisingly, people with long-term partners were more likely to say they had a single (54%) than a joint (42%) policy. Those couples who had a joint policy were most likely to say the main reason they chose it was simplicity (37%), followed by “level of cover” (30%) and budget (19%).

The biggest driver for those with life insurance or those who had considered purchasing it in the past two years was price (25%), closely followed by trust in their chosen provider (18%), and confidence that a claim would be paid (13%).

Understanding of Terms

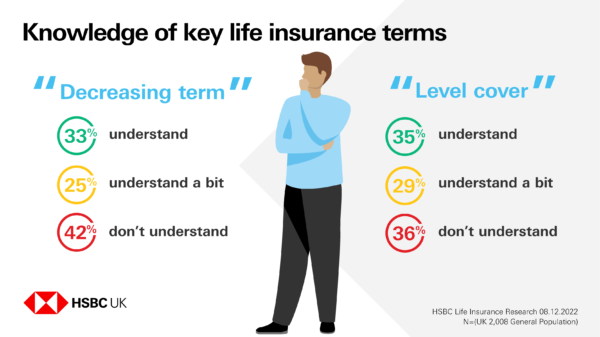

When it comes to key terms relating to life insurance, only around a third of people in the UK say they fully understand the phrases “level cover” and “decreasing term”.

More than two in five Brits (42%) say they don’t know what “decreasing term” means, and more than one in three (36%) don’t fully understand “level cover”.

Most people (53%) say they think “level cover” is the most important consideration when choosing which life insurance policy to purchase, after the terms were explained to them.

Purchase Preferences

People in the UK who have life insurance are pretty evenly split when it comes to how they bought it, with 49% purchasing through an adviser and 47% completing their transaction online.

And overall, those without any cover are more likely to say they’d buy online if they did decide to purchase a policy (58%), compared with through an adviser (40%).

But there are some interesting differences in age – with nearly half (48%) of 16-24-year-olds without insurance saying they’d prefer to use an adviser, more than any other age group. Meanwhile the 45-54 age group were the most likely to say they’d go online (65%).

Closing Thoughts

Many thanks to my friends from HSBC for allowing me to share and discuss their data and graphics.

Nobody would pretend life insurance is an exciting subject, but in these uncertain times it’s something we all need to think about, cost-of-living crisis notwithstanding. Life insurance protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

I discussed this subject in more detail in my blog post Do You Need Life Insurance? (mentioned earlier) and I recommend checking this out if you haven’t already. You may also want to speak to a personal financial adviser to find out more about life insurance and what might be the best option for you.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post on what can become a major issue for parents when making gifts or loans to their married children. Specifically it looks at what you can do to ensure that your wishes are respected should the worst happen and the marriage fails.

The article is by Joanna Toloczko, a partner, family law solicitor and mediator at UK law firm RWK Goodman.

Over to Joanna then…

According to the UK House Price Index in August 2023, the average house price in the UK was £291,000 and in London a whopping £536,000. To put this into context, the average house price back in January 2013 was £167,716, representing an increase of around 73%.

A bank or building society will normally require a minimum deposit of between 10% and 25% of the property value as a term of a mortgage offer, and the more you are able to put down as a deposit, the lower rate of interest you are able to secure. It is not surprising, then, that an increasing number of married couples rely on a contribution from one or both sets of parents for their deposit.

In my work as a family lawyer and mediator I often come across cases where a divorcing couple are at loggerheads about whether such a contribution was a loan or a gift. The party whose parents provided the funds will often argue that the funds were a loan which should be returned to their parents before the remaining funds are distributed between the husband and wife. The other party will usually argue that the funds were a gift and are available for distribution between the parties.

If the couple are not able to reach agreement and the case proceeds to court significant sums of money can be spent on arguing this point as a preliminary issue. Very often the parents will be drawn into the litigation.

Even if the Court accepts that the funds were a loan, it is possible that the Court will take the view that it was a “soft loan”, i.e. a loan where repayment is unlikely to be enforced. In these circumstances, the Court may choose to disregard the liability.

Usually, at the time the funds are made available to the couple no-one has formally addressed the issue of the nature of the advance. Everyone is excited about the new house purchase; no-one anticipates that the marriage may fail.

So, what can be done to ensure that gifts made to married children stay in the family of the parents making the gift, in the event of a divorce?

If the funds are being advanced to assist with the purchase of a property, a Declaration of Trust can be a useful tool. In this situation the married couple are the legal owners of the property and hold the property as “tenants in common”, which means that they have their own distinct share in the property. The Declaration of Trust can be used to set out the beneficial interests in the property, including the interests of third parties. For example, a Declaration of Trust could make it clear that as parents had contributed to the purchase price of the property, they are entitled to a specified share of the equity. Alternatively, the Declaration of Trust could set out that once the property is sold, the parents have to be reimbursed prior to the distribution of the remaining equity between the couple.

If parents are to receive a share of the equity, they need to be aware of a potential Capital Gains Tax liability, should their interest in the property increase in value.

Another alternative would be to use a formal loan agreement or for the parents to take a Legal Charge over the property. A Legal Charge works like a second mortgage. It is secured over the property and registered at the Land Registry. The Charge sets out details of the sum loaned to the couple, whether interest is payable and when/in what circumstances the parents are entitled to call for repayment of the loan.

Nuptial Agreements are also becoming more popular. These can be entered into either before the marriage (Prenuptial Agreement) or during the course of the marriage (Postnuptial Agreement).

These agreements make clear what is to happen to the couple’s assets in the event of divorce or separation.

If parents are gifting money, transferring properties, leaving an inheritance, providing an interest in a business, etc, and they wish to protect those assets in their child’s favour in the event of separation or divorce, a Pre- or Postnuptial agreement can be an extremely useful document.

Although Nuptial Agreements are not legally-binding and can be over-ruled by a judge in the divorce proceedings, if they are prepared in the correct manner, they have good prospects of being upheld or will certainly be heavily influential on the judge.

In summary, when advancing funds to a married child, always be clear about whether the funds are a gift or loan and seek legal advice about how best to ensure that the funds remain in the family in the event of a divorce. It is usually also a good idea to discuss any tax implications of your plans with an accountant or tax adviser.

Joanna Toloczko is a partner, family law solicitor and mediator at RWK Goodman and can be contacted on 07553 058485 or at Joanna.Toloczko@RWKGoodman.com.

Many thanks to Joanna Toloczko (pictured, below) for an informative and eye-opening article. Please do check out her company’s website (linked above).

While nobody likes to think about the marriage of their offspring failing, the reality is that an estimated 42% of marriages in the UK today will end in divorce. So it is vital to be realistic and ensure that, should the worst happen, any money you give or lend is returned or divided in accordance with your wishes.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).