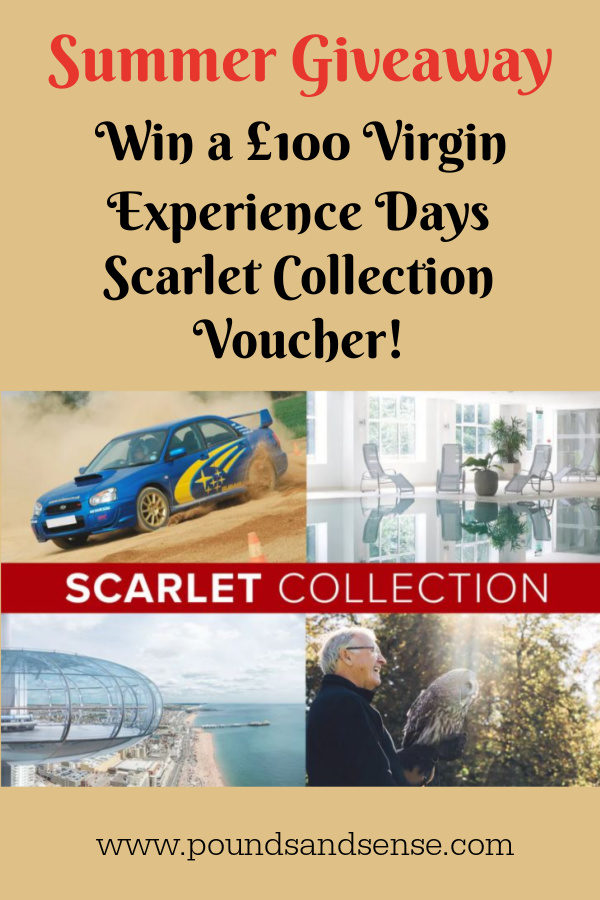

Summer is here, so it’s high time for another exciting giveaway on Pounds and Sense 🙂

I have joined forces with some of my fellow UK money bloggers to bring you the chance of winning a fantastic Virgin Experience Days Scarlet Collection voucher, worth £100. You can use this voucher on any of a huge range of experiences: from an introductory microlight flight to dinner for two at Coombe Abbey; a pamper day with cream tea for two at a Hallmark Hotel to a three-hour oriental cookery class at School of Wok.

After the last eighteen months we all need and deserve a treat, so here’s your chance to grab one for free!

This giveaway has been organized by my colleague Dan from The Financial Wilderness blog, so I should like to thank him very much for this. More details provided by Dan himself, along with instructions on how to enter, can be found below…

The Prize

The wonderful prize on offer today is a voucher allowing a choice of experience from the Virgin Experience Days Scarlet Collection.

This voucher worth £100 gives you the opportunity to choose a variety of exciting experiences, with something for just about everyone. To give you a flavour of the options on offer in the Scarlet Collection:

For the adventurous – A rally or Porsche driving thrill experience

For the foodies – A range of afternoon teas and dinner options

For the sporty – Have a round of golf at some great courses or learn archery

For the relaxed – A collection of overnight breaks around the country

You can view details of all the available experiences with the Virgin Scarlet Collection on the Virgin Experience Days website here.

The Bloggers Taking Part

This giveaway in run in conjunction with some of my fellow UK Money Bloggers – we run these events to help each other out, so please do visit at least some of the excellent blogs concerned 🙂

Enter to Win a Virgin Experience Days Scarlet Collection Voucher!

Use the Rafflecopter Widget below to make your entry. You’ll need to fill out your basic details and click ‘claim 1 entry’ to be in for the competition.

You also have the opportunity to claim bonus entries by performing an action relevant to the above websites, such as following an account on Twitter or visiting an article. You can do as many or as few of these as you like.

1. There is one top prize of a voucher for Virgin Experience Days “The Scarlet Collection.”

2. There are no runner up prizes

3. Open to UK residents aged 18 and over, excluding all bloggers involved with running the giveaway

4. Closing date for entries is midnight on 18.09.21

5. The same Rafflecopter widget appears on all the blogs involved, but you only need to enter on one blog

6. Entrants must log in to the Rafflecopter widget, and complete one or more of the tasks – each completed task earns one entry in the prize draw

7. Tweeting about the giveaway via the Rafflecopter widget will earn five bonus entries into the prize draw.

8. 1 winner will be chosen at random.

9. The winner will be informed by email within 7 days of the closing date and will need to respond within 28 days with their delivery address, or a replacement winner will be chosen.

10. The winners’ names will be published in the Rafflecopter widget (unless the winner objects to this).

11. The prizes will be dispatched within 14 days of the winner confirming their address.

Just a quickie today to share details of a free-to-enter competition from my friends at All Free Stuff. You can win 1 of 1000 Dior J’adore Absolu samples (see cover image). This is a great women’s floral fragrance by Dior.

To enter, all you have to do is sign up to the Free Stuff email newsletter. This daily email contains all the latest freebies, free samples, competitions, and more (of course, you can unsubscribe any time). Entrants must be over 18 and live in the UK. For the full rules and to enter the competition, please click here.

Good luck, and I hope you win one of the 1000 prizes!

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another Coronavirus Crisis Update. Regular readers will know I’ve been posting these since the first lockdown started in March 2020 (you can read my July 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

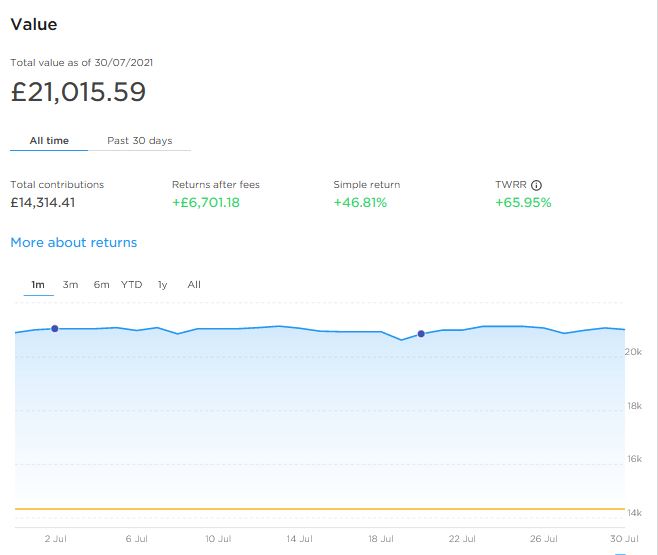

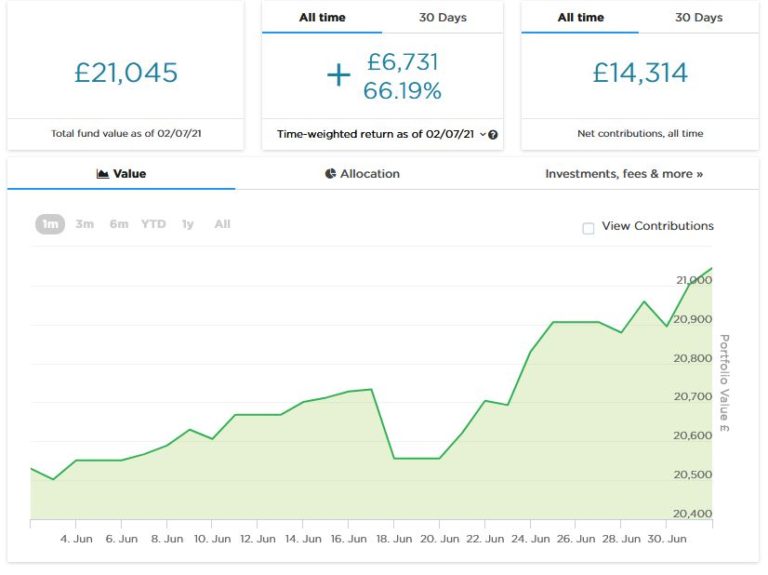

As the screenshot below shows, the value of my main portfolio remained pretty steady in July. It is currently valued at £21,015. Last month it stood at £21,045, so that is a slight drop of £30.

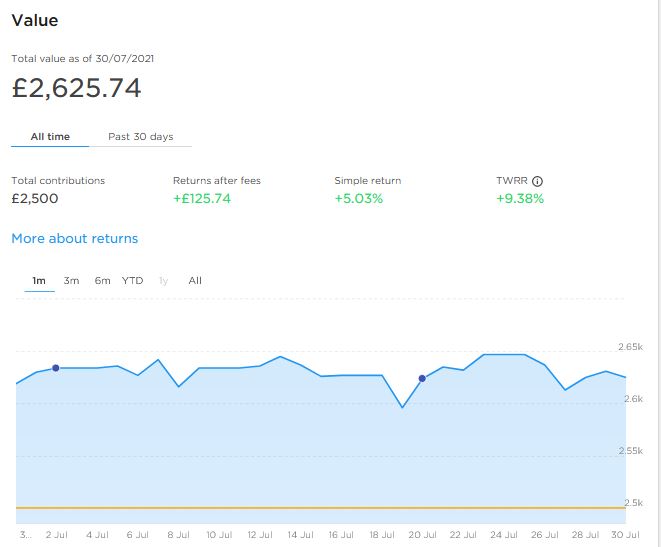

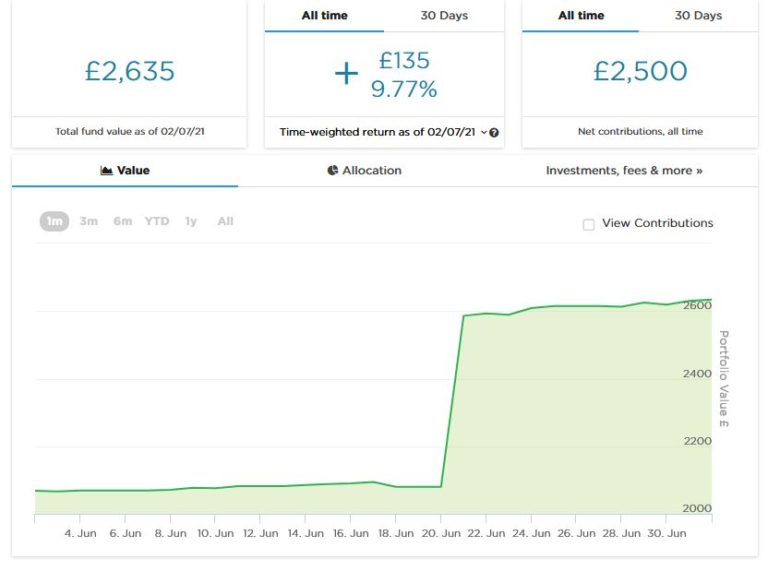

Apart from my main portfolio, I also have a second pot using Nutmeg’s new Smart Alpha option. This pot is now worth £2,625, compared with £2,635 last month, so a small decrease again. Here is a screen capture showing performance in July 2021.

Although it’s a little disappointing both portfolios are down slightly, over the last six months (and longer) both are still well up overall, so I’m certainly not going to lose any sleep over this. This is a long-term investment and some ups and downs are to be expected. In 2021 the overall trend has been mainly upwards, so I hope and expect this to be resumed soon.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering.

If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually amazed by the difference the risk level you choose makes.

.As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Touch wood, everything has been going well, so in June I added another £500, bringing my total investment on the platform up to £1,000.

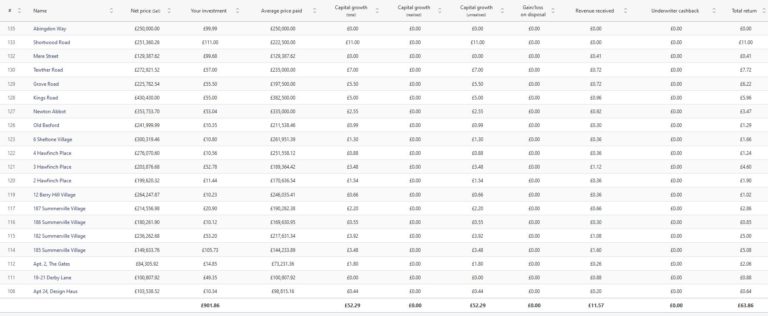

Since I opened my account, my portfolio has generated £11.57 in revenue from rental and £52.29 in capital growth, for a total return of £63.86. Here is my current statement:

As I said last time, to a degree Assetz Exchange has been a victim of its own success. They have had a big influx of new members, meaning all available investments were quickly snapped up. At the same time, some of the new projects that were due to launch were delayed. As a result I still haven’t invested all the money in my holding account. One new project did come on stream last week, so I put £100 into that.

My colleagues at Assetz Exchange assure me that more new projects are coming very soon. They are also limiting how much members can invest in the first few weeks of any new launch, so that everyone has a fair chance to purchase shares. And as time goes on more members may opt to offer their shares for sale on the exchange, opening up additional buying opportunities.

I am investing relatively modest amounts in new projects as they come onto the platform, so I don’t therefore put more than around £100 into any one project. As you can see, I already have a well-diversified portfolio comprising 20 different projects. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

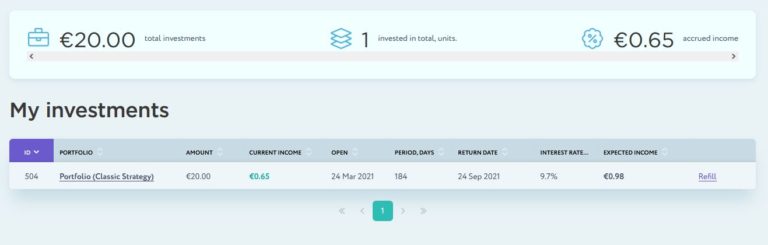

I haven’t mentioned my trial investment on European loan crowdfunding platform Nibble for a while, so thought I should remedy that this month. This has been proceeding without any issues and my initial test investment of 20 euros has accrued income of 0.65 euros, corresponding to an annual interest rate of 9.7 percent (see screen capture below).

I get weekly updates from Nibble confirming how much interest has been added to my portfolio. Based on my experiences to date I am considering investing a more substantial sum with them soon. My full review of Nibble can be found here.

Finally, in July 2021 two more PAS readers signed up with the low-key sideline-earning opportunity mentioned in previous updates. They will have received their initial £100 reward payments about now. I still have a few more invitations available if anyone else would like to take advantage.

This opportunity is based on matched betting, a sideline I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). It doesn’t require any financial outlay and is risk-free and entirely hands-off (once you have set up your account). No knowledge of betting is required and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company.

The company has changed its terms somewhat for new members. You now get a larger £!00 initial reward payment once your account is up and running, and then £25 every month you remain a member. I think this is a good move personally, as setting up the account does involve a little work on your part (though it’s certainly not rocket science). So the £100 in effect compensates you for your time, and once it’s done you continue to get £25 a month for no effort at all. The company is constantly developing its offering, partly in response to feedback from PAS readers. They recently launched a new mobile-friendly website to make it even easier for new members to sign up (once you’re up and running you shouldn’t need to use the website at all). They also recently incorporated an Open Banking app so that members don’t have to provide their online banking info to the company, as some people were concerned about this.

Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more information (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page. And yes, I will receive a reward for introducing you, but this will not affect the service or the rewards you receive.

Finally, in the interests of full transparency, I should say that if you do matched betting yourself, you may be able to make more money than what is being offered by the company. However, you will have to research the techniques in detail, place all bets yourself, and probably subscribe to a matched betting advisory service such as Profit Accumulator [affiliate link]. This opportunity is really for those who want an easy way to make some extra money without the hassle (or expense) of learning/applying matched-betting methods themselves.

Personal

The big news in July – in England at any rate – was that so-called Freedom Day took place as promised on 19th July 2021. Most of the legal restrictions on our lives, including mandatory masks and social distancing, were lifted from that date.

Since then – to the surprise of many experts and pundits (though not me) – new case numbers have been falling steadily week on week. Hospitalizations and deaths were slower to fall, but are now starting to follow the same path.

It is of course far too soon to say that the pandemic is over – and Covid is, in any event, likely to remain with us in some form for the foreseeable future. But it is all very encouraging, especially in the face of predictions from doom-mongers such as Professor Neil Ferguson that daily case numbers could reach 100,000 or even 200,000 as a result of restrictions easing.

In my view it is now high time we got back to something close to normal life and learned to live with the virus. But while out and about I notice that people generally are still being ultra-cautious. That is particularly the case in shops and supermarkets, where I should say that four out of five people are still wearing masks (though the numbers without are slowly increasing). On trains I would say it is about two in three, though on a couple of occasions when I travelled in the evening recently (after 7 pm) mask-wearers were in a minority.

I don’t use buses so can’t comment about them. At my local gym and swimming pool, however, almost nobody is wearing a mask now. Assuming that the numbers keep going in the right direction, I hope that more people will find the confidence to ditch the masks. It is wonderful to be able to see smiles and happy faces again after all this time!

In July I took a rail trip to Swindon to visit my old friend Jeff, who at the start of this year moved to Wiltshire. Unfortunately we chose what was probably the hottest day of the year. The whole round trip involved seven trains from three different train companies. So I can report that by far the best company for aircon, wifi, drinks/snacks service, and general all-round comfort, was Great Western Trains. Second were Cross Country, and last were West Midlands Railway. I travelled on three WMR trains in total and I don’t believe any of them had working aircon (one seemed to have the heating turned on despite the fact that the temperature outside was over 30). WMR had also by far the worst wifi, something I’ve experienced on many occasions before. I think West Midlands Mayor Andy Street should be turning his attention to improving this service rather than indulging in virtue-signalling gestures like offering passengers free masks. That aside, I did of course enjoy seeing Jeff again and also visiting Swindon for the first time. I would happily go back there, but hopefully on a cooler day!

As I said last time, I recently subscribed to Britbox and have been making good use of this. I really enjoyed watching all three series of the original House of Cards trilogy featuring Ian Richardson. I remembered the original series the best, but thought the second series (To Play the King) was equally good. I didn’t like the last series (The Final Cut) quite as much. It was never going to be quite the same without Michael Kitchen or Colin Jeavons, and I thought the ending was a bit of a let-down. But if you haven’t seen them before, I highly recommend watching all three.

Last week Britbox added Dennis Potter’s Lipstick on Your Collar (see image below) to their platform. I am very much enjoying watching this again almost 30 years since it first aired. I am a huge fan of Dennis Potter’s work and think he is probably our greatest-ever TV writer. His masterpiece was undoubtedly The Singing Detective, but Lipstick on Your Collar runs it pretty close. As with The Singing Detective, the series intersperses the action with lip-synched musical numbers, in this case classic 1950s rock ‘n’ roll. It has drama, comedy, great characters and some amazing music. What more could you possibly want?!

As I mentioned last time, now that Freedom Day has happened, this will be my last Coronavirus Crisis Update. I plan to continue with my monthly investment updates, and will also do more personal/general ones as and when the occasion arises.

I do hope you have enjoyed these monthly updates and found them of value. I have enjoyed writing them, and find it interesting looking back over them now as a sort of diary of the pandemic. I have listed them all below for convenience.

I recently returned from a three-day break in Llanbedrog. This is a village on the Llyn (or Lleyn) Peninsula in NW Wales. It was the first time I had been to Llanbedrog, although I have holidayed in North Wales quite often.

This was also the first time I had stayed at an Airbnb property. I did try last year but was scuppered by the pandemic, so had a refund voucher I needed to use up. The place I stayed was a room/apartment attached to a private house, but self-contained with its own front door. I’ll say more about it below.

Llanbedrog itself is by the coast, roughly half way between Pwllheli (famed for its Butlins camp, now run by Haven Holidays) and trendy Abersoch. Here is a map of the area from Google Maps.

Accommodation

As mentioned, I stayed at an Airbnb property in Llanbedrog. Under Airbnb’s rules I’m not supposed to reveal exactly where it was, but the location was certainly convenient. It was about 100 yards from the main road and 150 from one of the two local pubs. The beach was around ten minutes’ walk away.

You can read more about the place I stayed on this page of the Airbnb website (you can also read my post about booking a holiday with Airbnb here). It consisted of a large bedroom-cum-sitting room, along with a bathroom with excellent walk-in shower. There was also a kitchenette area with a toaster, fridge, sink, coffee-making machine and so on, but no actual cooking facilities (there wouldn’t have been room for them). For a short stay that wasn’t a problem, though. On two nights my Airbnb host, Jem, kindly cooked main meals for me for a modest extra fee. And on the other night I went to the local pub, which was very good as well 🙂

My room had a stunning view across the hosts’ beautiful garden with the sea in the background (see photo below). Another thing I enjoyed was that the garden was home to a colony of wild rabbits. They looked very cute and provided an entertaining all-day cabaret!

The apartment had free wifi which worked perfectly during my stay (not always the case in my experience). The location was quiet and peaceful, and I slept very well.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £344.98 for my three-night stay. This was made up as follows:

£91.67 x 3 nights = £275

Cleaning fee £20

Service Fee (which goes to Airbnb) £49.98

I was charged an initial deposit of £112.50, with the balance taken from my card a fortnight before my visit. As mentioned, some of the cost was covered by a refund from a booking I made with Airbnb in 2020 which had to be cancelled.

So the total price worked out to £115 a day. Obviously that’s not cheap, but prices across the board have risen due to Covid and the additional cleaning and other precautions property owners have to take. I thought it was very reasonable bearing in mind the high standard of the accommodation and the convenience of the location.

Things to Do

I won’t give you a blow-by-blow account of what I did while I was there, but here are a few highlights.

Plas yn Rhiw

This National Trust property is about 7 miles from Llanbedrog. It’s pretty remote, and I was glad to have my satnav to guide me. At one point I drove through a tiny hamlet and some children waved at me as I passed. That was a first for me!

Plas yn Rhiw is a 16th century manor house (with Georgian additions) overlooking the sea. Unfortunately due to Covid only the ground floor was open to visitors. This was basically three rooms, all roped off so you had to look at them from a distance. As you may imagine, it didn’t take me very long to go round. I did though have a nice chat with the National Trust lady who was in the kitchen. She told me about the paraffin cooking range from the 1950s (see photo below). There must have been quite a smell in the house when this was going!

The house also has some beautiful formal gardens (see photo below). And, naturally, there is a tea room. I enjoyed an excellent cappuccino with a jam and cream scone here. As I chose to sit inside (it was raining a bit at this point) I had to complete a Covid tracking form. That was no great hardship, of course.

Overall I enjoyed my visit to Play yn Rhiw even though the restrictions were frustrating. I would like to go back there again when things are more normal and see the rest of the house.

Oriel Plas Glyn y Weddw

This gothic-styled mansion built in 1857 is in Llanbedrog and was five minutes walk from where I was staying.

Nowadays the building is used as an art gallery and museum. It also has an excellent cafe attached which I visited twice during my stay. It’s free to enter and certainly worth a visit if you are staying in the Llanbedrog area. The gallery hosts a permanent collection of Welsh porcelain (said to be among the finest in Wales) along with exhibitions of works by local artists.

Oriel Plas Glyn y Weddw also has some beautiful gardens and an outdoor theatre, which had some shows advertised for later in the year (though not during my visit). In the grounds there is also this carriage from the horse-drawn tramway which used to run from Pwllheli to Llanbedrog. Apparently this was a popular tourist attraction until the track was damaged by a heavy storm in the 1930s and subsequently abandoned.

Llanbedrog Beach

As mentioned, the beach (see cover photo) was about ten minutes’ walk from my apartment. It was sandy and quiet, and offered a perfect place for children to play. The beach huts were well maintained and picturesque. There was also a beach bar serving drinks and snacks all day (though not in the evening). I didn’t go here in the end as it was quite small and I felt a bit awkward about taking up a table on my own when families were queuing up. I did hear good reports about it, though, and it was certainly a lovely location (see photo).

Final Thoughts

As you may gather, I enjoyed my short break in Llanbedrog, and am happy to recommend both the town and the accommodation where I stayed for a short break. Llanbedrog is a lovely place to relax and chill out, and with its beautiful beach could also be a good destination for families with young children. Older children and teenagers might find the lack of other entertainments a bit limiting though.

As for me, this was the first time I had been away since last autumn. After many months of lockdown, I really appreciated the sea air and (mostly) sunshine, and of course the much-needed change of scene. I definitely plan to return there before too long.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another Coronavirus Crisis Update. Regular readers will know I’ve been posting these since the first lockdown started in March 2020 (you can read my June 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio performed pretty well in June. It is currently valued at £21,045. Last month it stood at £20,435, so overall it has gone up by £610. I am happy with that, obviously.

Apart from my main portfolio, I also have a second pot using Nutmeg’s new Smart Alpha option. I added another £500 to this in June, bringing the total invested to £2,500. This pot is now worth £2,635, compared with £2,060 last month. Disregarding the extra £500 investment, this pot is therefore now £135 in profit compared with £60 a month ago, an increase of £75. So again I am quite happy with that. Here is a screen capture showing performance in June 2021. As you will see, my £500 investment was credited to the account on 20 June 2021.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering.

If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually amazed by the difference the risk level you choose makes.

Regular readers will know that this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Touch wood, everything has been going well, so in June I added another £500, bringing my total investment on the platform up to £1,000.

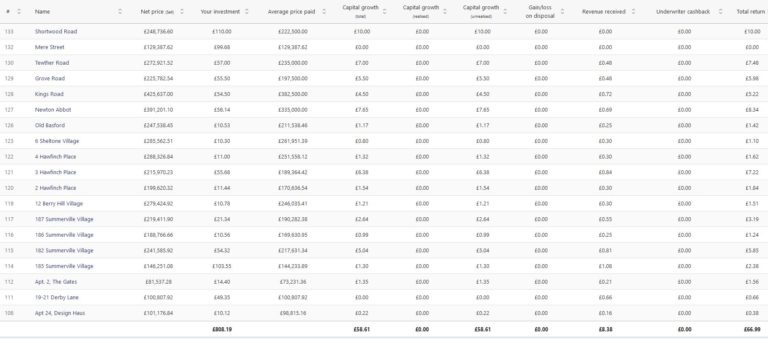

Since I opened my account, my portfolio has generated £8.38 in revenue from rental and £58.61 in capital growth, for a total return of £66.99. Here’s my current statement in case you’re interested:

The eagle-eyed among you may notice that although I have now put £1,000 into Assetz Exchange, only just over £800 of investments are listed above. The balance is still in my account waiting to be invested. The truth is that Assetz Exchange has been, to a degree, a victim of its own success. Over the last few weeks (my contacts at AE tell me) they have had a big influx of new members and all available investments are being quickly snapped up. New projects are coming on stream all the time, however, and AE are limiting how much members can invest in the first few weeks so that everyone has a fair chance to purchase a share. And as time goes on more members may opt to offer their shares for sale on the exchange, opening up additional opportunities for would-be buyers.

I am investing relatively modest amounts in new projects as they come onto the platform and expect to be fully invested by the end of this month. Indeed, I could be already if I chose, but I am following my strategy of diversifying as widely as possible, so don’t invest more than around £100 in any one project. As you can see, I already have a well-diversified portfolio with 19 different projects. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Lastly in this section, I wanted to say that the low-key sideline-earning opportunity I have mentioned in previous updates has reopened for new members, with slightly different terms (see below). About a dozen PAS readers (including my sister Annie) have already signed up to this and are enjoying a hassle-free monthly sideline income.

The opportunity is based on matched betting, a sideline I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). It doesn’t require any financial outlay and is risk-free and entirely hands-off (once you have set up your account). No knowledge of betting is required and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company.

As I said above, the company has changed its terms somewhat for new members. You now get a larger £!00 initial payment once your account is up and running, and then £25 every month you remain a member. I think this is a good move personally, as setting up the account does involve a little work on your part (though it’s certainly not rocket science). So the £100 in effect compensates you for that, and once it’s done you continue to get £25 a month for no effort at all. As a matter of interest, the company is constantly developing its offering and just about to launch a new mobile-friendly site to make it even easier for new members to sign up (once you’re up and running you shouldn’t need to use the website at all),

Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more information (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page. And yes, I will receive a reward for introducing you, but this will not affect the service or the rewards you receive.

Finally, in the interests of full transparency, I should say that if you do matched betting yourself, you may be able to make more money than what is being offered by the company. However, you will have to research this in detail, place all bets yourself, and probably subscribe to a matched betting advisory service such as Profit Accumulator [affiliate link]. This opportunity is really for those who want an easy way to make some extra money without the hassle (or expense) of learning/applying matched-betting methods themselves.

Personal

Of course, the big news this week is that so-called Freedom Day is set to happen on 19th July 2021. Most of the legal restrictions on our lives, including mandatory masks and social distancing, are set to be lifted then.

Regular readers of this blog (and my social media) may not be surprised to hear that I’m in favour of this. Indeed, I think it should already have happened. In particular, I am glad that the mask mandate is being scrapped and the decision to wear one (or not) will be left to individuals. Unsurprisingly this decision has caused some controversy, but personally I have always felt that the harms of masks to people’s physical and mental health greatly outweigh any potential benefits. And despite much hot air being expended on the subject, the evidence they do anything to reduce transmission of the virus in real world settings is – as England’s Deputy Chief Medical Officer has admitted – weak at best.

I also regularly see misuse of masks and other face coverings, which in my view makes them a hazard to both the wearer and those around them. That includes masks being endlessly re-used and kept in pockets and handbags when not required. I have lost count of the number of people I see in shops fiddling with their masks and then touching products on the shelves, potentially passing the virus on. It doesn’t surprise me at all that those US states which stopped mandating masks months ago have all seen dramatic drops in case numbers. There is every chance the same thing will happen here.

And then of course there is the small matter of the billions of tons of plastic pollution from masks (including particles of potentially carcinogenic microplastics) clogging up our oceans and littering our pavements, roads and countryside.

So, as you may imagine, I do not intend to continue wearing a mask or any other form of face covering after the 19th. Even if they worked, which I highly doubt, the benefits are extremely marginal (one study estimated that if infection levels are relatively low, 200,000 people would need to wear a mask to prevent ONE case of the virus being transmitted – and that figure optimistically assumes that masks reduce the risk of transmission by 40%). I have no objection at all to other people continuing to wear masks if it gives them reassurance (or a sense of moral superiority). But even though I am 65 and suffer from a long-term lung condition, I absolutely don’t want or expect anybody to wear one for my supposed benefit.

Moving on, I have just returned from a short break in Llanbedrog in North Wales. I won’t say too much about this now, as I plan to write a separate blog post about it soon. But it was a relaxing and restorative break and I felt much better for it. I stayed in this Airbnb apartment (you can read my post about booking a holday with Airbnb here if you like). I had never been to Llanbedrog before but would definitely like to return before too long. There is a picture of the beach and headland (which I climbed) in the cover image.

Also in June I met up with various friends I hadn’t seen for some time for pub lunches and other social events. I am doing more driving now, and noticing increasing amounts of traffic on the roads. Also, sad to say, I am seeing some very poor driving, including one collision (which thankfully didn’t involve me). I suspect many people have got out of practice at driving during lockdown, so please do be extra careful out there 😮

On the entertainment front, I finally got around to subscribing to Britbox in June. They had a special offer of one month free followed by three months at half price and I decided that was too good to ignore (I think that offer is closed now – sorry).

I haven’t really used it much yet, but have enjoyed watching (or re-watching) some old episodes of The Avengers with Diana Rigg and Patrick Macnee (pictured above). Last night I watched The House That Jack Built, one of the all-time classic episodes (even though it’s in black and white).

I am also planning to watch some of the original Doctor Who stories, and the three series of the political drama House of Cards featuring the inimitable Ian Richardson (“You might very well think that; I couldn’t possibly comment”). I understand that Britbox also have Dennis Potter’s Lipstick on My Collar coming up shortly and am looking forward to watching that too.

Whether I will stick with Britbox once my trial offer is over I am not sure. The big attraction for me is the classic series. While they do have some new material on offer as well, there isn’t much that has really piqued my interest. Still, I have four months before I need to decide about that 🙂

I plan to do one further Coronavirus Crisis Update next month. Assuming Freedom Day does go ahead on 19th July as planned, I think that will be a suitable point to stop. I will probably continue with monthly investment updates, and may also do more personal/general ones as and when the occasion arises.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

I recently saw an interesting survey of the main big-ticket items people have been buying in the UK during lockdown.

The YouGov survey of over 2000 adults was performed by YouGov on behalf of National Conversation Week (see below). The survey was commissioned by insurance services company Paymentshield, who sponsor National Conversation Week.

The top ten items were as follows:

Gadgets or electronics – 22%

TV – 13%

Games console – 11%

Gym equipment – 10%

Jewellery or watch – 10%

Bike – 6%

Expensive equipment to support a hobby (e.g. photography equipment, a musical instrument) – 6%

Pet – 6%

Garden shed – 5%

Art or antiques – 3%

I thought this list made very interesting reading, especially the fact that 1 in 10 people have bought home gym equipment. With gyms closed for many months due to the pandemic, it is no surprise that many of us have been investing in stationary bikes, rowing machines and even treadmills to try to maintain our fitness. I wonder whether people will rejoin clubs in the same numbers now they have this equipment at home.

I am not surprised either to see pets on the list. Certainly in my area I have the impression that many more people now own dogs. I can understand that they provide companionship, especially for those who live alone. Though I do think some of these new owners might benefit from education about how to look after their animals, and in particular the need to pick up after them 😮

I was slightly surprised to see that so many people have been buying jewellery, watches, art and antiques. I guess this may partly reflect that those of us lucky enough to have a continuing income have had fewer ways to spend it, leaving more spare cash available. I just hope the people concerned have checked that they are covered for any expensive items on their home insurance.

Finally, it’s interesting to see garden sheds on the list, with 1 in 20 buying them. I guess this reflects the fact that so many of us are working from home now, for some of the week at least. If you have the space for it, a shed can be a great option for reducing distractions and separating work life from home life. Around here I have also seen one or two mini-pubs created in garden sheds! (See cover image.)

National Conversation Week

National Conversation Week – which this year runs from 7 to 11 June – aims to get people talking in a bid to improve the nation’s well-being, at a time we are all facing unprecedented challenges. In particular, National Conversation Week hopes to encourage frank and open conversations about money. This is especially relevant at the moment, with many people having lost their jobs due to the pandemic and facing stress and hardship as a result.

Above all else, though, be kind to yourself, and don’t suffer in silence. And equally, if you know someone who may be struggling – or you just haven’t seen or heard from them for a while – reach out by phone or at least message them to check they are okay. It may be a cliche, but we really are all in this together. And pretty much everyone is struggling in their own way.

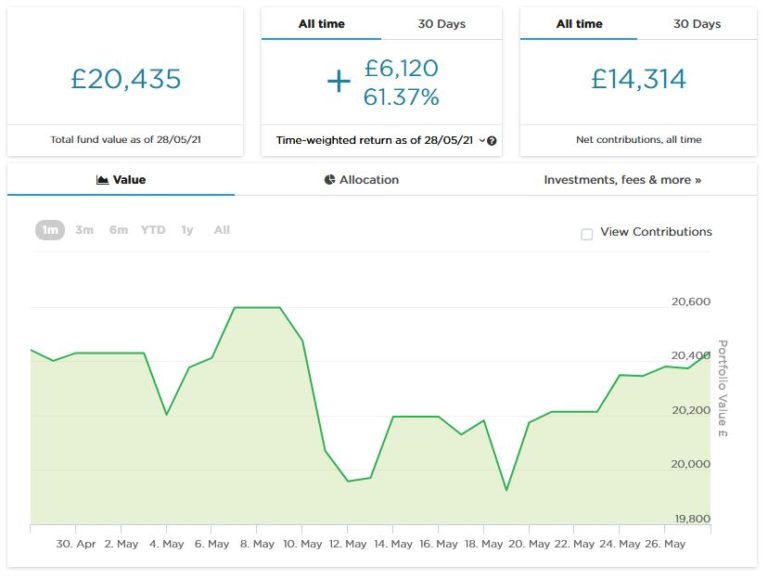

Another month has gone by, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these since the first lockdown started in March 2020 (you can read my May 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio has been on a roller-coaster ride in May. It is currently valued at £20,435. Last month it stood at £20,430, so overall it has gone up by the princely sum of five pounds! Since 20th May it has been on an upward trajectory, so clearly I hope that trend continues 🙂

.

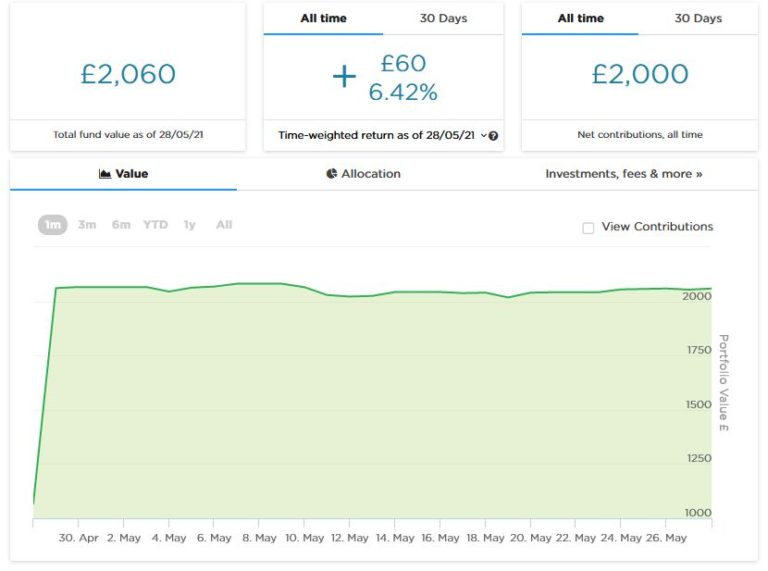

Apart from my main portfolio, six months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This did pretty well, so in April I added another £1,000 from some money returned to me from another investment. This pot is now worth £2,060 (£7 down on last month’s figure). Here is a screen capture showing performance in May 2021.

I updated my full Nutmeg review recently and you can read the latest version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth considering.

If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was truly amazed by the difference the risk level you choose makes.

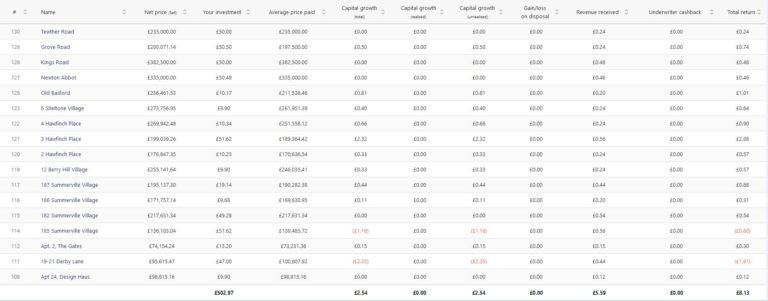

This year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Since then my portfolio has generated £5.59 in revenue received from rental and £2.54 in capital growth for a total return of £8.13. Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio with 17 different projects. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

In May several of the loans I invested in with the P2P property investment platform Kuflink were repaid (with interest) and I duly reinvested the money in other loans.

I have a well-diversified portfolio of loans with Kuflink paying annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often £100 or less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are definitely behind me now!

You can read my full Kuflink review here. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money with them. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year, with built-in automatic diversification. And I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Moving on, if you haven’t seen it yet, you might like to check out this eye-opening post about ‘how much is enough to retire on’ published on the PensionBee blog – I am quoted representing people in their 60s in this article!

You may also like to read my article on the Mouthy Money site in which I reveal why I am not a fan of premium bonds. I was recently hired as a regular contributor for Mouthy Money, so watch out for more articles from me there in the coming months. I also highly recommend reading the articles on the site by other contributors.

And finally, you can read my Q&A on the Lifeline24 blog, in which I talk about Pounds and Sense and share a few financial tips. Lifeline24 is a personal alarm service for older people and people with disabilities. If you’re interested, there is a code to get £10 off their already reasonably priced service at the end of the article. And no, I’m not getting any commission from them!

Personal

In May, as I’m sure you know, more of the government’s lockdown restrictions were eased. In particular, pubs and restaurants were allowed to open inside as well as out. Considering the monsoon-conditions that ensued after the outdoor reopening in April, that was a relief all round!

Last week I enjoyed my first pub lunch since the autumn at the Spread Eagle in Gailey, near Cannock. I met up with my old friend Liz, a former colleague from my days working at Wolverhampton University (the last ‘proper’ job I ever had). It was wonderful to see Liz again and in retrospect I hope I didn’t come across as too demob-happy! The food and service were both excellent. The pub was pretty quiet when we arrived at 12.30 but got busier later. There was still plenty of room inside and out, though.

Also in May I had my second Covid jab. For some reason I wasn’t able to book a slot at Whitemoor Lakes where I had my first jab, so this time I made my way to Great Wyrley Community Centre, another voyage of discovery for me. Everything went well, though bizarrely when I arrived a man at the door offered to ‘fast-track’ me if I took a lateral flow test (I declined). I had no side effects at all from this jab (the Oxford again), not even a sore arm. It is strange how people react so differently. I have friends who have had quite nasty reactions, though generally these lasted no more than a day or two. As for me, I have had (much) worse reactions from my annual flu jab.

With the better weather over the last week or two, I have resumed my habit of going for a breakfast walk. This is by far my favourite time of the day for walks, and I now have a good variety of routes to choose from around the local lanes. The photo in my cover image shows the beautiful Wisteria on Hope Cottage. This is about half a mile from where I live and features on many of my routes 🙂

Also in the last month I got back into the habit of reading again. I know many people say they read more during lockdown. However, I found that my concentration and attention-span were badly affected by the pandemic, so I more or less stopped reading for pleasure.

But in the last few weeks I’ve been feeling a bit more relaxed and that has helped me get back to reading, starting with some short books. Initially I picked up The No. 1 Ladies’ Detective Agency by Alexander McCall Smith. Having enjoyed that I moved on to the follow-up novel, Tears of the Giraffe. which is also very good. I remember that these light-hearted books were made into a TV series a few years ago, so I am thinking of buying the DVD set now.

After that, I moved on to another short novel, The Mountains of Majipoor by US science-fiction/fantasy writer Robert Silverberg.

Silverberg wrote a series of novels set on the giant world of Majipoor. I read most of them around 30 years ago, but for some reason this is the one novel in the series I never got around to.

I did enjoy it, but if you have never read any of the Majipoor novels, I wouldn’t start with this one. The place to begin is undoubtedly Lord Valentine’s Castle, a tour de force of the imagination with a compelling storyline. As a matter of interest, Lord Valentine’s Castle inspired me with the desire to learn to juggle (if you read the book you’ll understand why). But sadly despite many hours of trying I proved to have zero aptitude for it! Here’s an image link (affiliate) to the Amazon UK sales page.

The novel I’m reading at the moment is The Long Way to a Small Angry Planet by Becky Chambers. This is a longer science-fiction novel, which was recommended to me by Amazon as something I might enjoy.

Amazon recommendations can be hit or miss, of course, but I was very glad I acted on this one. The Long Way to a Small Angry Planet is a novel of great wit and charm, and I have been engrossed by it. It is mainly set on a small, commercial spaceship called The Wayfarer, whose job is to ‘tunnel’ wormholes in space. Becky does a brilliant job of bringing the ship and its (mostly) lovable multi-species crew to life.

The story is episodic – you could almost say picaresque – and told from the viewpoints of different crew members – from the reptilian pilot Sissix to the amiable alien chef/doctor called (quite reasonably) Dr Chef. There are some humans too, including the captain, Ashby, and the ship’s clerk and newest crew member, Rosemary Harper, who has a secret that is tearing her apart. There is plenty of humour and emotion alongside the science, so you definitely don’t need to be an SF aficionado to enjoy it. Anyway, I won’t rave on about it any more. If you want to find out more, here’s an image link (affiliate) to the Amazon sales page.

Finally on the subject of books, my nephew Steve (a semi-professional guitarist) has just published his first on Amazon. It’s called Crucial Guitar Basics and was written as a lockdown project. I had a very small input into it and my sister Annie rather more (she edited/proofread it). I’m no guitarist myself but thought it was a well-written and accessible introductory guide. Here’s an image link (affiliate) in case this might interest you. It’s available in both print and Kindle ebook form.

As I write this, the whole UK has just enjoyed its first day since March 2020 without a single Covid death. There is still some concern over the rise in cases of ‘The Indian Variant’, but so far these don’t appear to be causing a significant increase in hospitalizations or deaths. There is some speculation about whether the final stage of the PM’s ‘Roadmap to Recovery’ will take place on June 21st as promised. Personally I think it should, but in my view it’s more likely we will see a partial lifting of restrictions, with others retained for longer. I would particularly like to see an end to mandatory masks, as the evidence in favour of their use is weak (and many US states have done away with them for months now with no calamity ensuing). But we will see, I guess!

I hope that at some point soon I will be able to stop producing ‘Coronavirus Crisis Updates’ as normal life resumes. At that point, I may switch to creating monthly updates about my investments and maybe separate, more personal updates if anyone would be interested to read them. But I will definitely do at least one more full Coronavirus Crisis update next month.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Accountants are trained and experienced in all aspects of the tax system. They have both theoretical and practical knowledge of how the system works and how the (complex) rules are typically interpreted by HMRC. And they have to keep themselves up to date with the endless legal and procedural changes.

Also, unlike HMRC, an accountant is four-square on your side. They will advise you on the best way to organize your affairs to minimize your tax liability. They will answer any questions you may have, e.g. what records you need to keep. When the time comes, they will (if you want them to) compile your accounts and submit the relevant figures to HMRC in your tax return. And if any queries or problems arise, they will act on your behalf to try to resolve them.

A further benefit of having your accounts prepared by an accountant is that HMRC will know that a finance professional – someone who speaks their language – has compiled them. Other things being equal, this is likely to mean they will be more inclined to accept the figures and not dispute them.

Even if you aren’t self-employed or running a business, there may still be a strong case for getting an accountant to help with your taxes. Many older people, for example, have multiple streams of income, from stocks and shares to ISA accounts, property rentals to pensions. Some of this income may be taxable and some not, and varying tax rates and tax-free allowances may apply. Most accountants are more than happy to provide a service to people in this situation as well.

There is, of course, one drawback to engaging an accountant, and that is the cost. This will probably amount to a few hundred pounds a year (maybe more in some cases). Not to pay this, however, is in my view a false economy. A good accountant is likely to save you at least as much in unnecessary tax as they cost you. And the reassurance (and relief) of having a finance professional on your side when any queries with taxation arise is impossible to put a price on (but extremely valuable).

Of course, finding a good accountant who offers a service suitable for your needs isn’t always straightforward. And the amount they charge varies considerably. If you are looking for a keenly priced and easily accessible service, you might therefore like to check out what my friends at Simply Tax have to offer.

The Simply Tax Option

Simply Tax is a service run by professional accountants that provides a simple and inexpensive method for preparing and submitting tax returns to HMRC. They operate mainly online and are therefore able to keep charges to a bare minimum (starting from as little as £90). They say their service is for:

First time tax filers

Sole traders

CIS subcontractors

High earners (£100K+)

Landlords

Investors

Company directors

People living abroad

Anybody who needs a tax return

As the name indicates, Simply Tax aim to make the process of drawing up and submitting a tax return as simple as possible. In a nutshell, they say their procedure is as follows:

Create your free online account (just need your full name and email address)

Once verified, go into your user area and complete your personal information

Select the button to start your tax return (you’ll be taken to a screen to answer a few questions)

Once you’ve paid and been checked for your identification, simply drag and drop the information requested

We will do all the leg work and prepare the tax return for you

We’ll upload a draft tax return for you to review and approve electronically

Once you’ve approved, leave it to us to submit to HMRC

Although all of this is done online, you will be allocated a personal tax adviser whom you can contact at any time with any questions.

Simply Tax say their service will save you lots of time (they estimate between 70-80%) compared with filing your return yourself. They also estimate that their service is up to 50% cheaper than using a traditional high street accountant or tax advisor.

Finally, Simply Tax are fully regulated by the ICAEW (Institute of Chartered Accountants in England & Wales), providing added reassurance.

If you are looking for a straightforward, cost-effective way of preparing and submitting your annual tax return, in my view Simply Tax is well worth checking out. Okay, if you run a multi-million pound business empire it may not be for you. But if you are like most of us and just need a friendly, professional accountancy service who won’t charge an arm and a leg, they could certainly fit the bill.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Simply Tax. If you click through any of the links and make a purchase, I will receive a commission for introducing you. This will not affect the fee you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Almost everyone loves getting something for free, and in this digital age it is easier than ever to get freebies. So why do so few people take advantage of the great opportunities on offer?

In some cases, people simply aren’t aware that such opportunities exist. However, the main reason for people not actively pursuing freebies is that they are suspicious of getting something for nothing – they believe that there is some sort of catch involved. Alternatively, they might assume that the freebies available are cheap, low quality or not worth the effort. Neither is necessarily true.

Whilst some freebies are undeniably low cost or in sample-size proportions, there are a lot of really great products and services available too. The trick is to identify what product niches you are specifically interested in, then target the offers accordingly. This can yield better results than scanning offer websites with no real intent, and is less labour-intensive if hunting for offers is not something you actively enjoy.

Where you should look for freebies will depend on what type of niche you are targeting. For example, if you are a parent looking for baby- or child-related items, simply signing up to a manufacturer’s website will sometimes result in freebies. Occasionally they may provide the items in exchange for consumer feedback or a product review. But often they will give away items for no other reason than to encourage brand loyalty.

Literature is another good niche to target if you love a free gift. Publishing companies are always looking for people, both adults and children, to review newly published books. You have complete control over which books are sent to you, and are only required to review those which truly interest you.

If your interests are broad and you are more motivated by the thrill of receiving something for nothing, there are many websites and forums where people will list opportunities for obtaining free goods and services. The most impressive freebies are normally offered in limited quantities or for a restricted time period, so you will need to check the listings regularly to get the best deals. Signing up for emails or downloading an app which will generate alerts can make the process easier.

Some of the best free products and experiences are available to those people who are willing to put in a little effort. In particular, mystery shopping can produce great results because the company is required to reimburse you for your time. Your assignment may involve a free experience, such as eating at a restaurant or visiting a local attraction, or visiting a specific store and getting financial recompense for shopping there.

However much free time you have, and whatever your interests, you will be able to find freebies which suit you. Companies frequently send out free samples in order to generate interest in their products, and often all you need to do is fill out your name and address. If you are willing to provide something in return such as a review or completing a short survey, the freebies you receive can be even more enticing.

Disclosure: This is a sponsored post on behalf of Free Stuff websites.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my April 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

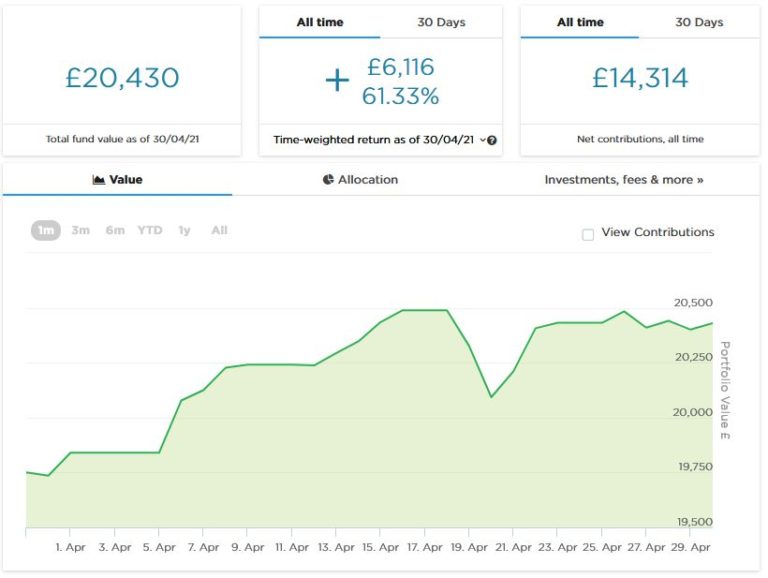

As the screenshot below shows, the value of my main portfolio rose fairly steadily in the first half of April, after which it remained around the same level (apart from a brief dip around the 20th). It is currently valued at £20,430. Last month it stood at £20,078, so overall it has gone up by £352. I am happy enough with that.

Apart from my main portfolio, five months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This has done pretty well, so in April I added another £1,000 from some money returned to me by RateSetter (as discussed in last month’s update). This pot is now worth £2,067. Here is a screen capture showing performance in April.

I updated my full Nutmeg review in April and you can read the new version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

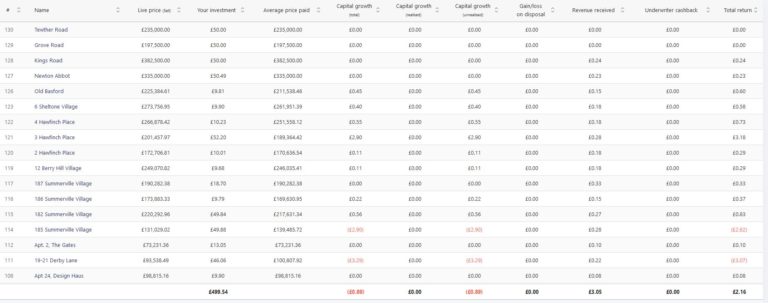

I also added £400 (from RateSetter again) to my initial test investment of £100 with Assetz Exchange. As you may recall, Assetz Exchange is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and (as mentioned) another £400 in April. Since then my portfolio has generated £3.05 in revenue received from rental (equivalent to an annual interest rate of about 10% on my original £100 investment). Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

You may also notice that some of the properties in my portfolio have gone up in value and some have gone down. This makes it a bit harder to judge overall performance compared with an equity-based investment like Nutmeg. The property values quoted by Assetz Exchange represent the best price you can sell at currently on the exchange, which is where all investments on AE are bought and sold. But they are only really relevant if you want to buy or sell that day. By contrast, Property Partner (a somewhat similar P2P property investment platform) quote a value for each property based on an independent surveyor’s valuation every 6-12 months. That means the values displayed on Property Partner are more stable, but of course they are only theoretical as there is no guarantee that this valuation would be achieved if the property was put on the market.

In case you’re not aware, everyone has a generous £20,000 tax-free ISA allowance in the current tax year (2021/22). However, for some reason the government only allows you to invest in one of each type of ISA in any particular.tax year. So you can only put new money into one stocks and shares ISA per year, but you can invest in a cash ISA and/or IFISA as well if you wish – just as long as you don’t exceed the £20,000 total limit. In the 2021/22 tax year I am therefore investing in a Nutmeg stocks and shares ISA and an Assetz Exchange IFISA. This gives me additional diversification compared with investing in just one type of ISA.

Moving on, I heard last month that I will not be eligible for any more SEISS income support payments for the self-employed. Along with many other self-employed people, my income took a hit when the pandemic struck and this money from the government came in very useful (though I do thankfully have a personal pension and other investments as well). However, I have become a victim of the rule that says to receive SEISS your average self-employed income must represent at least half of your total income.

For the first three rounds of SEISS that was indeed the case. However, the latest round of payments incorporates another set of tax returns (2019/20) when calculating average income. Because my income was lower in these accounts (partly due to the pandemic) my four-year average is now less than what I draw from my personal pension. So at a stroke I am no longer eligible for any more support. It’s not the end of the world, but I do find it bizarre that a scheme intended to support self-employed people whose livelihoods have been affected by the pandemic can cut off completely when your average income drops. Commiserations to any PAS readers who may have found themselves in a similar situation 🙁

Personal

In April, as I’m sure you know, some of the government’s lockdown restrictions finally began to be lifted.

I was glad to be able to go for a swim for the first time since Christmas, and have been doing so twice a week since it became possible again. I am a member of the David Lloyd Club in Lichfield which has two pools, one inside and one out. Although I’ve heard that you have to book slots at some swimming pools, that has never been the case at DL Lichfield, and in fact in many ways it feels reassuringly normal. Of course, you have to wear a mask as you enter the building, but thankfully not in the changing rooms or the pool 😀

I have just been told that if the pools get very busy, DL staff ask people to wait in the changing rooms until others have left. I haven’t witnessed this myself and don’t think it happens very often, but am happy to place this info on record.

What I do find bizarre is the rules about buying and consuming refreshments. The club room (aka coffee shop) at DL Lichfield is open for the purchase of drinks and light meals, but you can’t consume them within the building. You are, however, allowed to sit at a table in the club room (no need for a mask) to read and relax or just stare at the four walls. But heaven help you if you try to eat or drink anything.

I was told by a staff member that it was okay to take a drink to the outdoor pool as long as I was going for a swim, but not if I simply wanted to lie on a sunbed. Even though I am fast becoming a connoisseur of strange lockdown rules, this one seems barmy to me and I’d love to know how DL Lichfield plan to enforce it (“Unless you get in that pool in the next five minutes, I’m taking your coffee away.”). I’d like to support the DL club room/coffee shop, but the incomprehensible rules have defeated me. So I’m now taking a flask of tea and a biscuit with me and having that on the poolside or in the changing room after my swim. So far no Covid police have come for me.

I have also been pleased (and relieved) to have my hair cut again, six months after this was last done. Thankfully I didn’t have to queue up, as my hairdresser comes to me and cuts my hair in my conservatory. We have both had Covid jabs and agreed to dispense with masks and just kept the door and window open (thankfully it was quite a warm day). Again, it all felt reassuringly normal.

I haven’t so far taken advantage of the reopening of pub gardens, largely because it has been so cold (and wet) most days. It’s good to see at least some of my local pubs open again, but a shame they still aren’t allowed to open inside as well as out. Last year we had Eat Out to Help Out at a time when there were more Covid cases and deaths then there are now (just one death yesterday, I read). I am looking forward to May 17th when pubs and restaurants can reopen inside as well, but believe this has been delayed too long personally.

I am probably one of the few people who didn’t watch the Line of Duty finale. Indeed, I haven’t watched any of the series, as it didn’t really appeal to me. For one thing it sounded downbeat and depressing, and life has been grim enough recently. But also, it appeared a bit too complicated for my liking. Especially as i grow older, I find following series with large casts and labyrinthine plots increasingly challenging. I can remember laughing (affectionately) at my dad when he expressed confusion at the plot of some TV detective show, but I am obviously going down the same route myself now 😮

I have watched a couple of shows I enjoyed this month, though, so thought I’d share details in case anyone fancies giving them a try.

The first is an Amazon Prime Video series called Upload. This is a dystopian science fiction tale, set in a not-too-distant future when a method has been found for transferring people’s minds at the point of death (or before) to a virtual afterlife. This service is provided by a number of large corporations. They employ minimum-wage ‘angels’ in large warehouse-like offices to monitor these worlds and support the clients who live in them (at least, until their money runs out). It is quite a dark concept, but full of laugh-out-loud moments and some great characters. There is also a mystery in it, and a romance between a female ‘angel’ and one of her (deceased) male clients. It’s well worth a watch if you like something a bit different (and have Amazon Prime Video, of course).

I am also enjoying a US fantasy series called The Librarians (see below). I originally caught a couple of episodes on an obscure Freeview channel and decided I’d like to watch the whole (four) series from the beginning. Doing that proved a bit more challenging than I anticipated, but eventually I managed to track down a DVD box set on eBay.

The Librarians is a tongue-in-cheek fantasy series with a certain retro feel to it. It reminds me a bit of the old Avengers TV show in its heyday (with Diana Rigg as Emma Peel).

The Librarians are a group of misfits who are recruited to work at the mysterious Library, a place where magical artefacts of all kinds are stored. Early in the first series magic is released into the world again, having been suppressed for many centuries. In each episode the Librarians investigate some mysterious incident and try to stop evil individuals deploying magic for nefarious ends, generally using their intelligence rather than violence.

Again, it’s hard to explain in a few words, but you soon get the hang of things. And the characters, while perhaps excessively goofy at times, are all endearing in different ways. The Librarians is really old-fashioned family entertainment (with little if any swearing) and none the worse for that. If you can get hold of it – I’m not sure whether it’s on any streaming services – it offers an enjoyable (and at times hilarious) drop of escapism, something I guess many of us need at the moment.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

.

.