My Investments Update – April 2025

Here is my latest monthly update about my investments (slightly earlier than usual due to other commitments). You can read my March 2025 Investments Update here if you like.

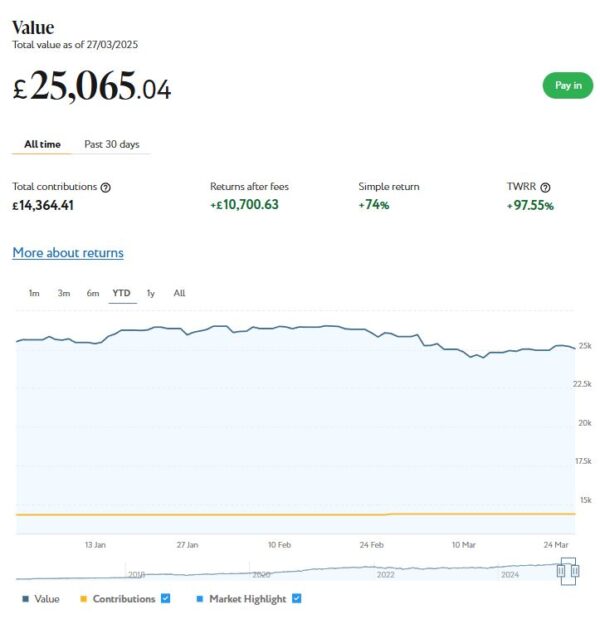

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

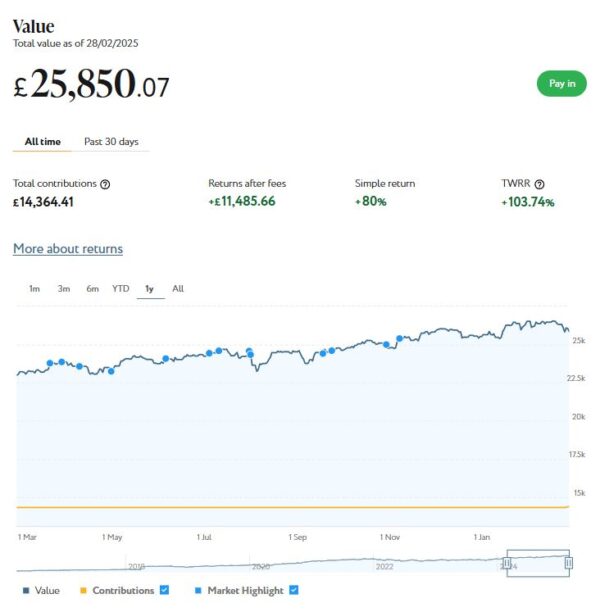

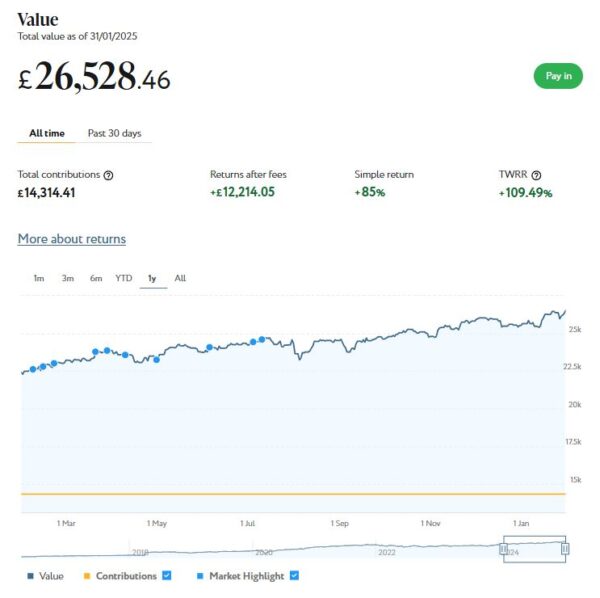

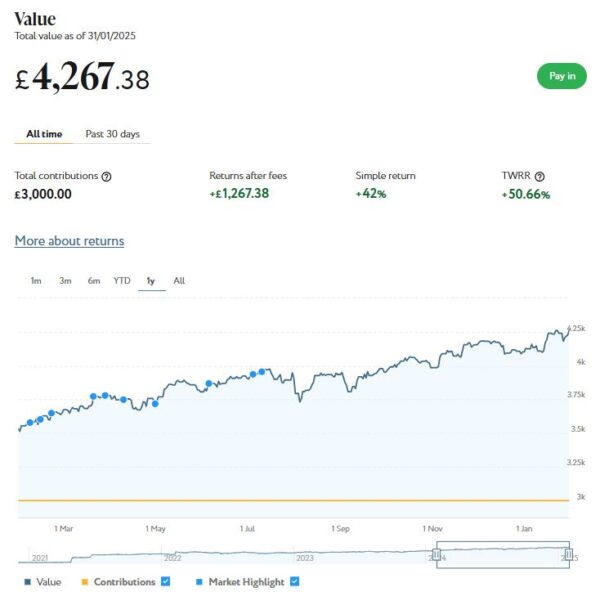

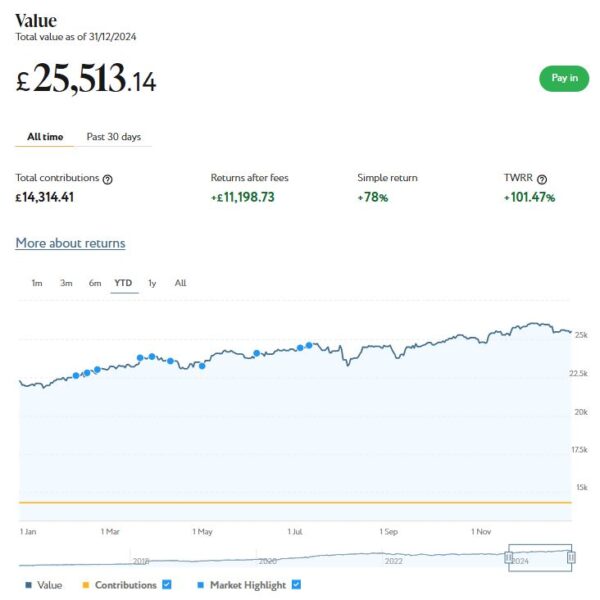

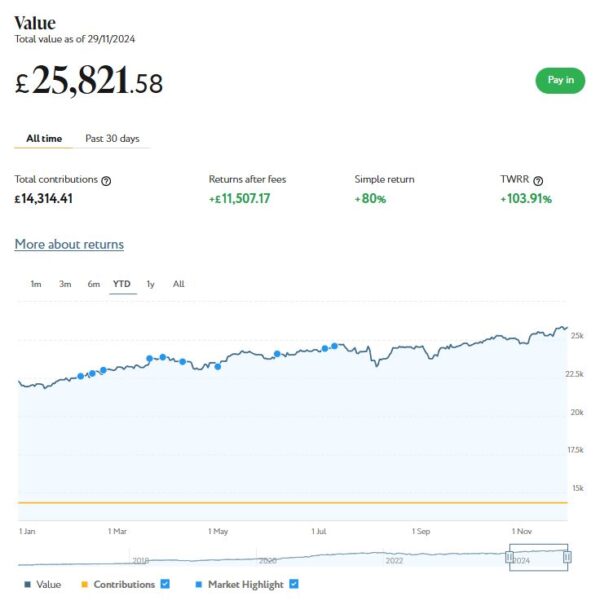

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,065. Last month it stood at £25,850, so that is a drop of £785.

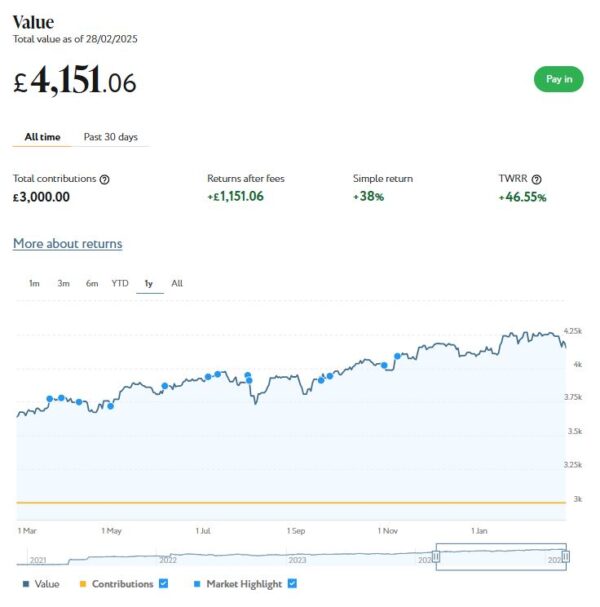

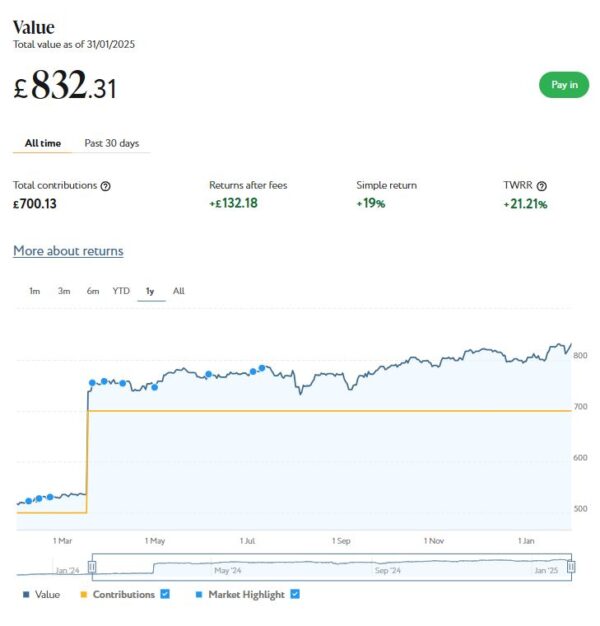

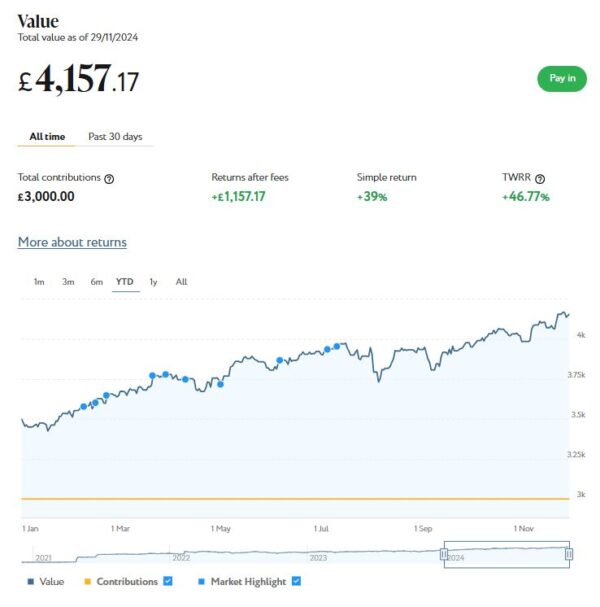

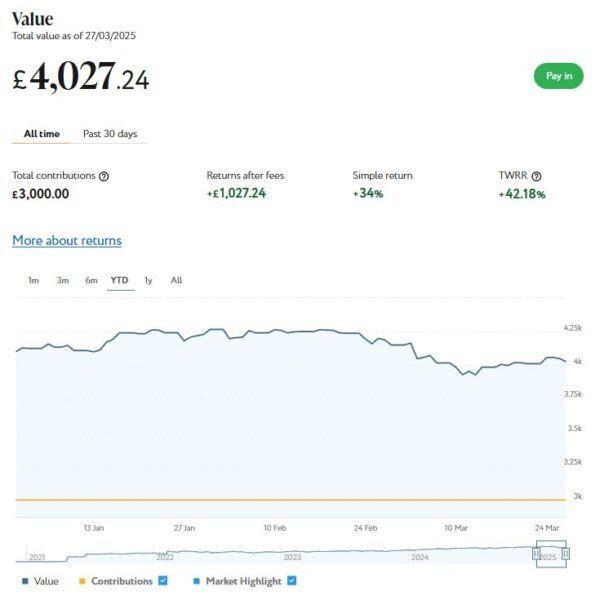

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,027 compared with £4,151 a month ago, a fall of £124. Here is a screen capture showing performance for the year to date.

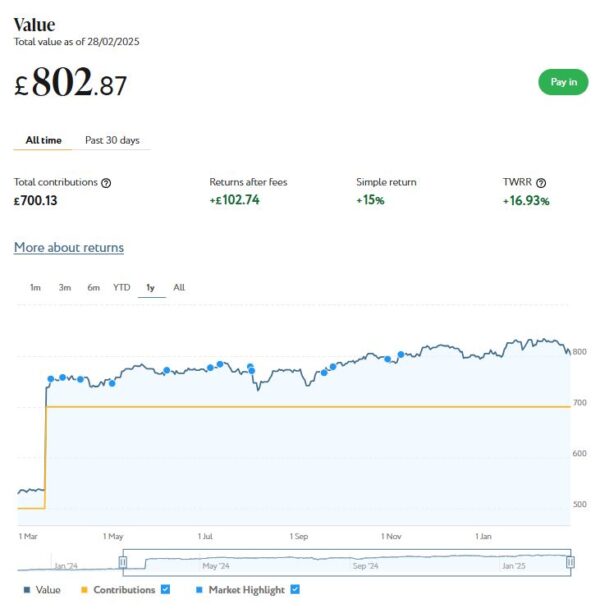

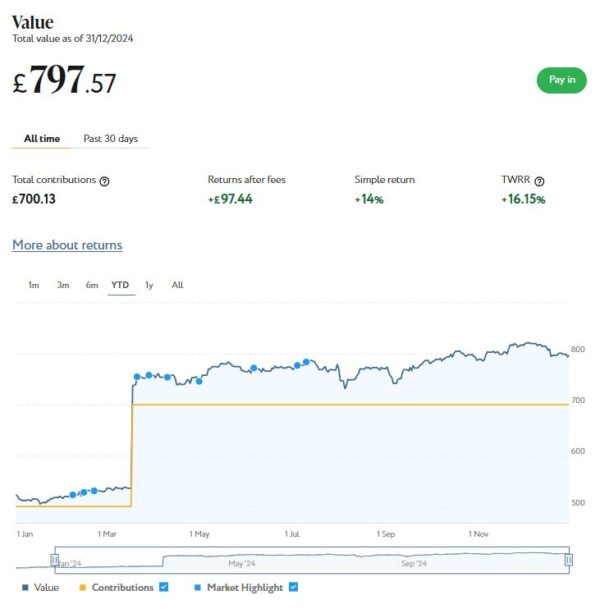

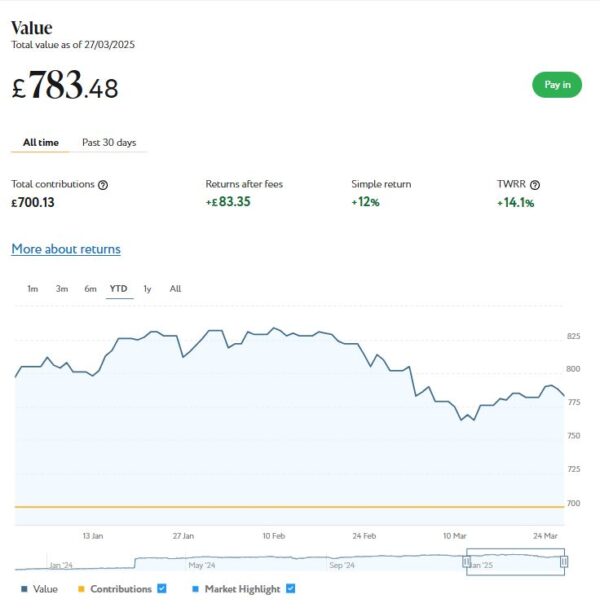

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £783 compared with £803 last month, a fall of £20.

As you can see, March has been another disappointing month for my Nutmeg investments. Overall I am down by £929. This is mostly due to the continuing instability in world markets, caused by the the trade tariffs imposed by US President Donald Trump and other economic and social factors.

Nonetheless, the value of my Nutmeg investments is still up £1,477 in the last twelve months. And their value has increased by £3,559 or 13.52% since the start of January 2024. So the recent falls do need to be taken in context. Ups and downs are always to be expected with stock market investments, and over time they tend to even themselves out. In general the worst thing you can do is panic and sell up when downturns occur, as you are then crystallizing your losses. Indeed, I am considering topping up some of my investments now while values are depressed. That’s just how I’m thinking, of course, and doesn’t constitute investment advice!

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £238.70 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 15 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 19 are showing losses. My portfolio of 36 properties is currently showing a net decrease in value of £52.78, meaning that overall (rental income minus capital value decrease) I am up by £185.92. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

- As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange/Housemartin here and my article about the rebranding to Housemartin here. You can also sign up for an account directly via this link [affiliate].

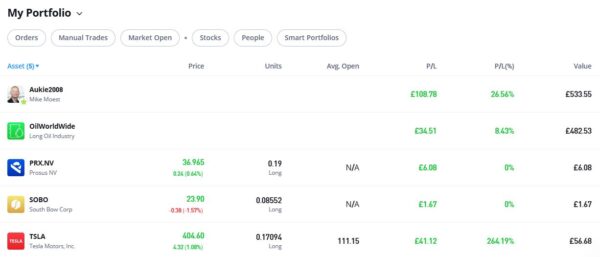

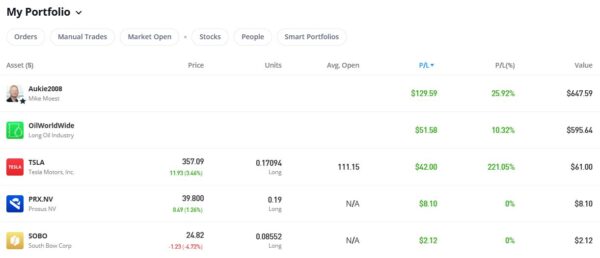

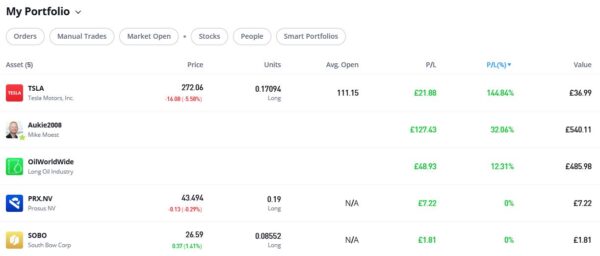

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

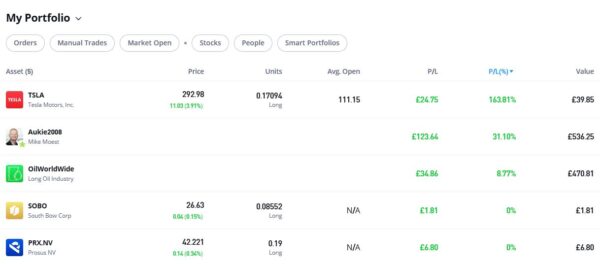

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,072.80, an overall increase of £184.44 or 20.76%.

- Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

You can read my full review of eToro here. You may also like to check out my more in-depth look at eToro copy trading. I also discussed thematic investing with eToro using Smart Portfolios in this recent post. The latter also reveals why I took the somewhat contrarian step of choosing the oil industry for my first thematic investment with them.

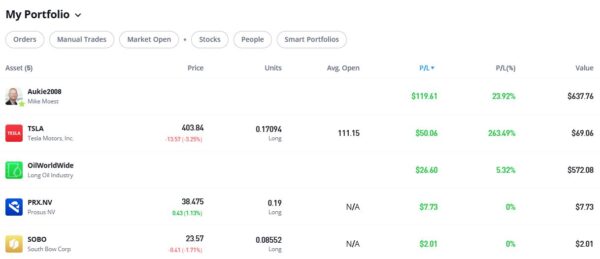

As you can see, my Oil WorldWide investment is currently showing a profit of 12.31%. That’s a welcome improvement since the portfolio was rebalanced by eToro. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 32.06% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 144.84%. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

- eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

Moving on, as I said last time, I am no longer writing for the Mouthy Money website, as they have decided to take their content creation in-house. From a personal perspective I am obviously disappointed about this, but I had a good run with them and wish them every success going forward. You can still read all the articles I contributed to Mouthy Money over the years by visiting my profile page on the website. How long they will keep this in place I really can’t say!

I also published several posts on Pounds and Sense in March. Some are no longer relevant, but I have listed the others below.

In Beat the Postage Stamp Price Rise!, I pointed out that stamp prices are rising again on 7th April 2025. This will actually be the the SIXTH rise in the price of first class stamps in just three years. See what prices are going up, along with my recommendations for mitigating the effects of the increases.

And in From Saving to Spending – The Retirement Mindset Shift I discussed a subject that has been on my mind recently as I enter my 70th year. This is how to negotiate the mindset shirt from saving to spending in retirement, and how (hopefully) to get the balance right.

The Pros and Cons of Investing for Dividends discusses a strategy that has been growing in popularity with older investors particularly. Dividend investing offers the potential for generating income combined with capital appreciation. In this post I examine the pros and cons of a dividend investing strategy and set out a few tips and guidelines for those new to this.

Finally, in Spotlight: The Mintos P2P European Investing Platform I take a closer look at Mintos, Europe’s largest P2P investment platform. As well as the ability to generate above-average returns by investing in loans to businesses world-wide, they have added new diversification options, including bonds, ETFs and real estate. And until the end of April they have a bonus offer for anyone investing €1,500 or above on the platform. In my blog post I look at the pros and cons of investing with Mintos and provide more details about their April bonus offer.

One other thing is that we’re currently just over a week away from the end of the 2024/25 financial year. If you still haven’t used all of your 2024/25 £20,000 tax-free ISA allowance, you have just a few days left before it’s gone. It is more important than ever to use all your tax-free allowances while you can, as the government looks set to reduce some of these allowances later in the year. See my recent blog post for more information.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

- I am also on the BlueSky social media network under the username poundsandsense.bsky.social. For the time being anyway, Twitter/X will remain my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!