It can hardly have escaped your notice that in the last week or so shares generally have plunged in value due to economic fears sparked by the coronavirus outbreak.

If you have a pension pot, stocks and shares ISA, or any other equity-based investment/s, this is obviously a worrying time. It’s very important to avoid knee-jerk reactions, though.

In particular, unless you really need the money urgently now, you should think very carefully before selling up. By doing so you will be locking in any losses. Even though it’s true that shares may have further to fall, this advice still applies. All share prices are cyclical, and rises and falls are to be expected. That is why stock market investments should always be regarded as long term.

Luckily, there are a few apps that offer you experts’ advice on safe long-term investments. You can check some of the best on the market at BestStockTradingApp.com.

A further consideration is that if you sell up now, you won’t receive any dividends due from your shares further down the line.

Should You Top Up?

With share prices currently falling, should you take the opportunity to ‘top up’? That is actually a difficult question to answer, as it’s impossible to know for sure how much further the markets will fall before they recover. Timing the market is notoriously difficult, and many investors in the past have had their fingers burned by thinking they could second guess it.

Nonetheless, if you are currently investing monthly into a stocks and shares ISA or other fund, I would say you should almost certainly continue to do so. One consequence of the fall in share prices is that you will get more shares for your money now. This will actually boost the value of your portfolio in the longer term when the markets recover. This phenomenon is called pound-cost averaging. It is one reason why making regular smaller investments rather than one-off lump sums can be such a good option for investors.

Otherwise, it is really a matter of personal judgement. If you think that a certain share or fund is good value at its current price there may be a case for investing in it. Inevitably, though, this will be a bit of a gamble. I am not personally planning to top up my equity portfolio until the present crisis appears to be well on the way to being resolved.

Beware of Pound-Cost Ravaging

If your pension is already in drawdown – especially if you are early into your retirement – pound cost ravaging is a risk you need to be aware of right now.

If the value of your pension pot is falling and you are also drawing money from it, those two things together have the potential to deplete it rapidly. You are then increasing the risk of running out of money later into your retirement.

If you have other sources of cash, therefore, it may make sense to reduce or even suspend entirely withdrawals from your pension pot during this time. This will help preserve its value. You will be able to resume withdrawals when – as will inevitably happen at some point – the markets recover. The great majority of pension providers will be happy to do this for you if you request it.

Consider P2P and Other Non-Equity Investments

If you have money to invest, in my view there is a good case right now for considering other types of investment such as P2P.

Regular readers will know that I am a fan of this type of investment (if approached sensibly and selectively) and have a fair-sized portion of my own portfolio invested in it. I won’t go through all the possibilities now as this is a subject I discuss regularly on Pounds and Sense. But if you are looking for a couple of ideas to start you off, I recommend checking out RateSetter – a relatively low risk P2P lending platform which I reviewed in this post – and Bricklane, a REIT (Real Estate Investment Trust) which offers a highly tax-efficient Property ISA (reviewed in this post).

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

In February 2017 I wrote this post about premium bonds explaining why I was withdrawing a large amount of the money I had invested in them.

To recap, at that time the interest rate paid on premium bonds (from which the monthly prize fund is calculated) had been cut eight months earlier in June 2016. This led me to sell the majority of my holding, as the amount I was earning in prizes had fallen considerably. The rate was cut again a few months later in May 2017, which led me to sell nearly all my remaining bonds. I now have just £5 left, to avoid closing my account completely.

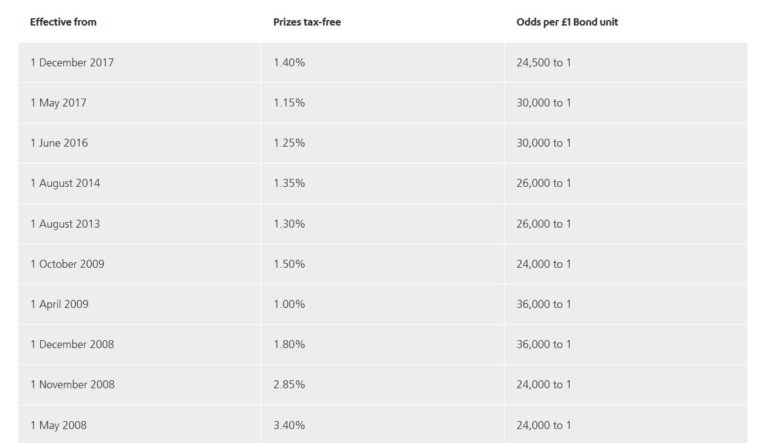

So what has happened since then? The good news for bond owners was that from December 2017 the prize fund was raised by 0.25% to 1.40%. This improved the odds of an individual bond winning a prize in any monthly draw from 30,000 to 1 to 24,500 to 1 (although it still didn’t tempt me to reinvest).

The not-so-good news is that from May 2020 the rate is being cut by 0.1% to 1.3%. As a matter of interest, here is a table copied from the NS&I website showing the changes in prize rates and the odds of winning a prize over the last twelve years. The new rate from May 2020 isn’t shown on the table.

From May 2020 the chances of winning a prize with a single bond will be reduced to 26,000 to 1. Over 170,000 fewer prizes are set to be given out in May 2020 than in February as a result of this change, with less than half the number of £100 and £50 prizes expected to be awarded (source: MoneySavingExpert).

My Thoughts

A first glance you might think that an interest rate of 1.30% percent still isn’t so bad in these days of (very) low interest savings accounts. It’s much the same as the current top paying easy-access savings accounts. Premium bond prizes are tax-free and you can withdraw your capital any time if you need it within a few days. Your money is protected by the UK government and you have an outside chance of winning a life-changing sum. So what’s not to like?

Well, quite a lot in my opinion. Most importantly, although the interest rate is currently 1.40% (reducing to 1.30% in May) in practice most people won’t make this amount. The interest rate is a mean (average) figure and this is skewed by the two one-million pound prizes (which statistically you are highly unlikely to win – see below) and the small number of other other high-value prizes. For these big prizes to be paid out, a lot of people have to win nothing. The more bonds you have, the closer to the average your prize earnings are likely to be. But the reality is that most premium bond owners won’t earn the interest rate quoted (and they may make nothing at all).

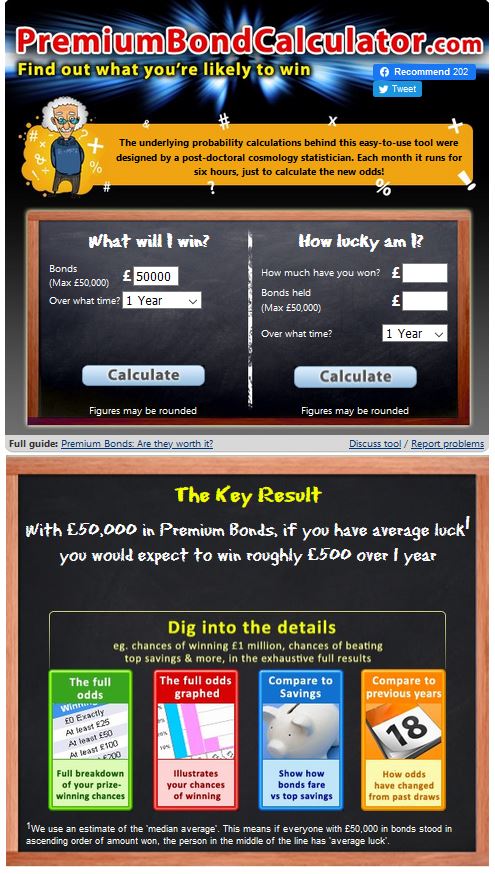

A better measure of what you are likely to make over a year is the median average. The way to think about this is that if you lined up all premium bond-holders with a certain number of bonds (e.g. £50,000) in order from those earning the least in a year (probably nothing) to the most (a million pounds plus), the median is the person right in the middle of the line. Half of all holders will earn more than this person (or the same) and an equal number will earn less. The median in this context is therefore a measure of what you can expect to earn from your premium bonds in a year with ‘average luck’. The clever folks at MoneySavingExpert have built a Premium Bond probability calculator which uses this metric to indicate how much you are likely to win per year, with average luck, with any given holding.

With the £50,000 maximum, the calculator reveals that with average luck you will win just £500 of prizes a year, equivalent to an interest rate of just 1.0 percent (see screen capture below). And that is at the current (February 2020) interest rate. From May 2020 that figure will inevitably go down. Obviously you might have better than average luck, but (as stated above) around half of all bond-holders will have worse. You can read a much more detailed explanation about this on this page of the MSE website.

The calculator also reveals that with £5,000 in premium bonds you could expect to win £50 a year with average luck, and with £1,000 nothing at all. Only about one in three people with £1,000 worth of bonds will win a prize in any one year, so the median (‘average luck’) winnings are zero. Over a two-year period, however, about five out of nine holders of £1,000 will win at least one prize, so the median earnings over two years with £1,000 in bonds are £25 (the lowest and by far the most common prize). This does I guess demonstrate that the ‘average luck’ method used in the MSE calculator has its limitations as a way of estimating likely earnings (although it is still likely to be more accurate than applying the headline interest rate to your investment).

Clearly the longer you hold your bonds, the better are your chances of winning a larger prize, so over a period of years average annual earnings may edge up slightly. Even so, the large majority of bond-holders won’t ever earn the headline rate.

At one time the tax-free status of premium bond prizes would have been a significant attraction, but nowadays that doesn’t apply to nearly the same extent. All basic rate taxpayers now benefit from a Personal Savings Allowance of £1,000 worth of tax-free savings interest every year (higher rate taxpayers get £500 and top rate taxpayers nothing at all). In practice 95% of people now pay no tax on their savings interest. If you are in the 5% who do, premium bonds become a more attractive option. Even so, a typical return of 1% or less, even if it is tax free, isn’t going to set many pulses racing.

Finally, you do of course have a chance of winning a big prize, but it’s important to be realistic about what that chance is. Even with the maximum £50,000 holding, MoneySavingExpert calculate that your chances of winning the million pound top prize in any one year are 1 in 69,876. To put this into perspective, if you had held £50,000 in premium bonds since the year 68000 BC (assuming of course they existed then) with average luck at the current interest rate you could have expected to win the jackpot just once. I looked this up, and 68000 BC is the middle of the Stone Age!

Overall, then, I cannot recommend premium bonds as a home for your savings, especially with the coming rate cut in May 2020.

I can understand why premium bonds are a popular investment, as they offer a bit of excitement every month checking whether you have won and how much. But the fact remains that overall, for most people, the total prize money received is likely to average little more than 1 percent a year at current rates. It may very well be less than this, especially after May 2020 when – as already mentioned – the number of lower value prizes (£25 to £100) will be cut substantially. I look forward to checking on the MSE calculator then to see how much a person with average luck might expect to make in a year.

If you are lucky enough to have £50,000 burning a hole in your pocket, my first advice would be to put enough into an easy-access savings account such as the Post Office Online Saver (currently paying 1.30% including a fixed 0.8% bonus for the first 12 months) to cover your outgoings for up to three months in the event of emergencies. After that, you could invest the balance in a low-cost tracker fund, or a portfolio of investment funds, or a robo-advisory platform like Nutmeg. You could perhaps put a proportion of the money into P2P lending or property crowdfunding as well. Over several years, for the great majority of people, this will outperform an equivalent premium bond portfolio many times over.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Please be aware that this is a historical post. Bricklane is now closed to new investors and is winding down. Please see the comments below for the latest updates about it.

Today I am looking at another property investment platform, Bricklane.

Unlike Kuflink and Ratesetter, both of which I have discussed previously on this blog, Bricklane is not a platform for peer-to-peer loans. Neither does it arrange crowdfunded investments in specific properties like Crowdlords and Property Partner.

Bricklane is structured as a Real Estate Investment Trust, or REIT for short. For those who don’t know, REITs are property funds that use investors’ money to buy (and manage) property and provide returns in the form of rental income plus capital appreciation.

In order to qualify as a REIT in the UK, companies have to meet certain requirements. The most important are as follows:

At least 75% of their profits must come from property rental.

At least 75% of the company’s assets must be involved in the property rental business.

They must pay out 90% of their rental income to investors.

In exchange for operating within these rules – and to encourage investment in UK real estate – REITs are not required to pay corporation or capital gains tax on their property investments. That helps make REITs profitable for the companies running them, and is how they are able to generate attractive returns for investors.

Normally rental income from REITs is treated as taxable income and taxed at your highest marginal rate. However, if you invest through an ISA or SIPP (Self Invested Personal Pension) no tax is due. You therefore get the best of both worlds – your money isn’t subject to taxation while invested in the REIT, and when it comes back to you in the form of income distributions and profits on sales of shares, you don’t have to pay tax on these either.

Types of Investment

You can invest in Bricklane as a stocks and shares ISA or a SIPP, or failing that in a standard investment account, where you will be liable for tax.

To maximize the benefits from investing in a REIT, I highly recommend going down the SIPP or ISA route, if you haven’t already used up this year’s allowance. As a reminder, everyone has a £20,000 annual ISA allowance (for 2019/20) and you are also only allowed to invest in one cash ISA, one stocks and shares ISA and one Innovative Finance ISA (IFISA) in any one tax year. I invested in a stocks and shares ISA with Bricklane myself.

Bricklane has two property portfolios you can invest in. These are Regional Capitals, which includes properties in Birmingham, Manchester and Leeds. and London, with a portfolio of properties in the capital. The Regional Capitals portfolio has generated a return of 19.3% since it was launched in September 2016 and the London portfolio 8.9% since its launch in July 2017 (figures from the Bricklane website).

As a Bricklane investor, you can choose to invest in either or both portfolios, in any proportion you choose. I opted to put all my money into Regional Capitals, as I believe this is where the biggest growth potential lies. In addition, rental income in this portfolio is higher, and I am also concerned about the possible impact of Brexit on London. You might see this differently, of course!

Bricklane Pros and Cons

Based on my experiences so far – and some online research – here is my list of pros and cons for the Bricklane property investment platform.

Pros

1. Fast, easy sign-up.

2. Well-designed, intuitive website.

3. Low minimum investment of £100.

4. Bricklane take care of all the work involved in buying and managing properties. You just choose which portfolio/s to invest in.

7. Possibility to access your money at any time (though this does depend on another investor being willing to buy your shares).

8. Customer service (in my experience anyway) is fast, friendly and helpful.

9. Charges are reasonable, comprising an initial 2% fee (though see my comment below on how you may be able to offset this) and 0.85% annual management fee.

10. Potential to profit through both capital appreciation and rental income.

11. Rental income is paid into your account every three months. You can either withdraw it or reinvest it to compound your returns.

12. Up to £1,500 cashback is available for new investors of £5,000 or more via my referral link (see below).

Cons

1. No detailed information provided about the properties your money is invested in.

2. Can’t invest in an ISA if you have already put money into another stocks and shares ISA this year.

3. 20% tax deduction from rental income at source if you don’t invest via a SIPP or ISA (and additional liability if you are a higher rate taxpayer).

4. Minimum £10,000 investment for a SIPP.

5. Returns over the last few months have been disappointing (see below)

6. No absolute guarantee you will be able to sell your shares when the time comes.

My Experiences

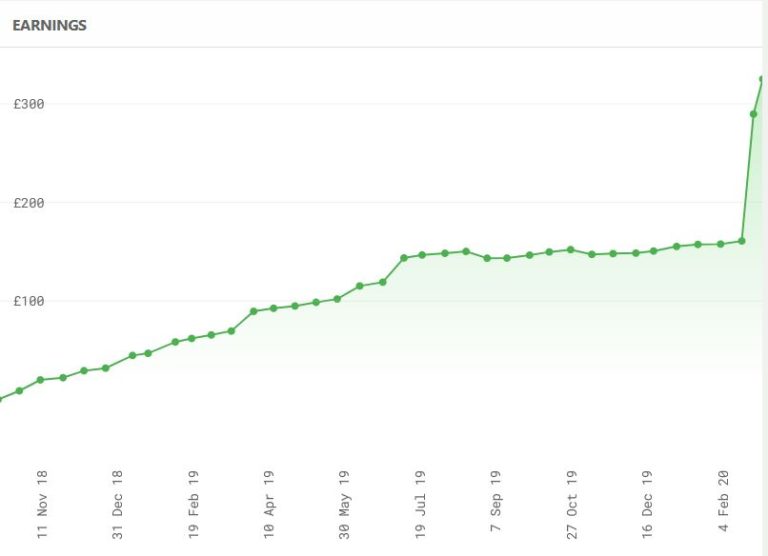

I put £5,000 into a Bricklane Stocks and Shares ISA in October 2018. As mentioned above, I chose to invest in the Regional Capitals rather than the London portfolio. The graph below – taken from my member’s page – shows the earnings generated since I opened my account.

As you will see, initially my investment performed pretty well. In the first nine months I made about £150, which equates to an annual interest rate of 4% (tax-free). That’s not spectacular, but it still beats most bank and building society accounts by a considerable margin. It is similar to the top rate currently on offer with P2P platform RateSetter in their Max account, although in their case you have to pay a fee equivalent to 90 days’ interest if you wish to withdraw. There is no withdrawal fee with Bricklane.

Since July/August 2019, however, returns have diminished considerably. My earnings between August 2019 and February 2020 were only just over £7, which is clearly a very low percentage rate. Of course, a large part of this is down to the depressed state of the property market caused by uncertainty over Brexit. I am hoping that now this is definitely happening – for better or for worse – my investment will get back on an upward trajectory again. Although recent results have been disappointing, at least the overall value of my portfolio hasn’t gone down (which has happened with some of my other property-related investments).

One other thing I should mention is that in October 2019 I withdrew £1,000 from my account to help fund a new central heating boiler after the old one packed in. This has therefore also reduced my returns a little. Although even if I still had the full £5,000 invested, earnings over the last few months would still have been nothing to write home about.

I should add that the withdrawal in question proved straightforward, although it wasn’t instant. I received the money in my bank account about a fortnight after putting in my request.

Conclusion

Clearly the performance of my Bricklane portfolio since last August has been disappointing, though overall I am still better off than I would have been if I had kept my money in a bank or building society.

I am hoping that things will start to improve in the property markets now that the Brexit issue has been resolved. There are some signs of this, although it remains to be seen whether the recovery in property prices will be sustained. For the time being, then, I am sticking with what I have in Bricklane, though I am not planning to top up my investment with them currently.

More generally, my experiences with Bricklane have been good. The sign-up process was fast and simple, and my £125 referral bonus (see below) was credited to my account instantly, completely offsetting (with a bit to spare) the initial 2% charge.

I also like the fact that any investment with Bricklane is automatically diversified across a range of properties, thus reducing volatility and risk. By contrast, with many P2P loan and property crowdfunding platforms, you invest in one loan or property at a time.

It’s also reassuring that you can ask to withdraw your money at any time – this can be an issue with property crowdfunding platforms in particular. As mentioned earlier, this does depend on someone else being willing to buy your shares, but Bricklane say that to date there hasn’t been a problem for anyone wanting to sell. As I said above, I had no issues when I wanted to release £1,000 from my own investment with them.

It is important to note that this is an investment rather than a savings account, and it does not therefore enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme (FSCS).

Clearly, no-one should put all their spare cash into Bricklane (or any other investment platform). Nonetheless, in my view it is worth considering as part of a diversified portfolio. Not only are the rates of return (other than the last few months) higher than those offered by most banks and building societies, they are less affected than shares by ups and downs in the stock market. Property investments aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

In addition, the tax treatment of REITs make them a highly tax-efficient investment, especially if you can invest in the form of a SIPP or an ISA.

Welcome Offer

As an existing Bricklane investor, I can offer a special cashback deal for anyone signing up and investing on the platform via my link. If you click through this special invitation link, sign up and invest a minimum of £5,000, you will receive £125 in cashback (and I will get £100). With a £5,000 investment this bonus will cover your initial 2% charge and still leave you £25 in profit 🙂

If you invest more, you will get even more cashback, as follows:

Over £10,000 – £250

Over £20,000 – £500

Over £50,000 – £800

Over £100,000 – £1,500

Not only that, once you are an investor with Bricklane, even if you only start with £100, you will be able to offer the same cashback bonus to your friends and relatives and earn commission yourself as well. There is no limit to the number of people you can introduce through this scheme.

Obviously, this is a generous promotional offer by Bricklane and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

If you have any comments or questions about this Bricklane review, as always, please do leave them below.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed.

Note: This is a fully revised and updated version of my original Bricklane review from October 2018

UPDATE15 March 2020: Having said that my earnings from my Bricklane ISA over the last 6-8 months were disappointing, since the start of February they have shot up by over 100% (see below).

This doesn’t exactly cancel out the recent falls in my equity-based investments due to the coronavirus, but it does demonstrate the value of having a well-diversified portfolio. And I am obviously feeling more positive about Bricklane as an investment platform now 🙂

One other thing to note is that until the end of April 2020 Bricklane are waiving all investment fees for both new and existing investors. Visit the Bricklane website for more information.

If you enjoyed this post, please link to it on your own blog or social media:

PLEASE NOTE: This welcome offer has now changed. Details of the new ‘Invest £1,000, Get £100’ free welcome offer can be found in my fully updated RateSetter review.

As I said then, RateSetter is one of my favorite lower-risk P2P lending sites. It lets you save via a tax-efficient IFISA and/or an ordinary (taxable) Everyday account. Although their rates aren’t the highest (currently 3% to 4%) I like the fact that risk is spread across all loans on the platform, with a provision fund to cover any defaults.

In my previous articles I mentioned their welcome offer of a £100 bonus for anyone investing £1000 for a year or longer. This offer is now closed, though if you took advantage and are waiting for the £100 bonus to be credited twelve months on, that will (of course) still be honoured.

What RateSetter do have now is an enticing (and much lower cost) Invest £10, Get an Extra £20 offer.

New Welcome Offer

Currently if you are new to RateSetter you can get £20 added to your account for free just by signing up and depositing £10. Full terms of the offer are reproduced below, and you can also find them on the RateSetter website.

You can take advantage of this offer so long as you

have not previously registered with RateSetter;

register after 23rd January 2020; and

deposit a minimum of £10 through the RateSetter ISA or Everyday account within 56 calendar days of registering.

Your bonus will be credited to your Everyday Account and invested in RateSetter’s Access (instant access) product at the going rate (currently 3%) within 30 working days of qualifying. From here you can transfer it to your ISA account if you like or simply withdraw it.

My Thoughts

This is a great offer from RateSetter if you are wary about P2P investing and want to dip a toe without risking any significant money. It is also good if you only have very small amounts available to invest, or you just like the idea of getting your hands on a free twenty pounds! It will also give you a chance to see how the RateSetter P2P platform works for yourself.

Although the bonus is ‘only’ £20 as opposed to the £100 on offer before, you only have to invest £10 to get it rather than £1,000. In addition, your bonus will be credited within 30 working days of qualifying for it, rather than having to wait a full year as before.

Clearly, this is a generous promotional offer by RateSetter and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

As always, if you have any questions or comments about this post, please do leave them below.

Disclosure: This post includes my referral link. If you click through and make an investment for this offer, I will receive a bonus for introducing you. This has no effect on the terms or benefits you will receive. Please be aware also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. You should do your own ‘due diligence’ before making any investment, and take professional advice if at all unsure how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

One question I get asked fairly frequently as a money blogger is what I think are the best current investment opportunities.

I have to be very careful when responding to this sort of question (and always tell people this). For one thing, I am not a qualified financial adviser, so it would be against the law for me to offer personalized investment advice. And even if I were, I still wouldn’t be allowed to give one-to-one advice without first doing an in-depth fact-find on the person in question.

Of course, this is exactly as it should be. For one thing, everyone’s circumstances are different, and what represents a good investment for me might not be the same for you. It depends on a wide range of factors, including your income and expenditure, your family responsibilities, how much you want to invest, the timescale (and purpose) you are investing for, your age and health, and so forth.

Another important consideration is your attitude to risk. Other things being equal, higher returns come with higher risks. If you’re comfortable with this and willing to accept it in exchange for the chance of better returns, that is of course your decision. On the other hand, if riskier investments would cause you sleepless nights, you are probably better off seeking a safer – if possibly less exciting – home for your money.

In addition, anything I say here is inevitably based on my own experience, and there is no guarantee yours will be the same as mine. I might, for example, have great success with one platform and suffer losses on another. But there is no way of knowing whether your experiences if you invest will be the same as mine. This applies especially if you have to choose specific investments on the platform (as with many P2P/property crowdfunding platforms) rather than putting your money into a pooled fund of some kind.

And, of course – as the financial services ads always say in the small print – past results are no guarantee of future performance…

I don’t want to come across as too negative. I am, after all, a money blogger and investor myself. So what I can – and will – do is talk about my own investing experiences and share information about what has worked well for me this year. It’s then up to you to decide if you want to investigate these opportunities any further. If so, you will need to do your own ‘due diligence’ before deciding how to proceed, perhaps taking professional advice from a qualified financial adviser as well (which I strongly recommend if you are new to investing or at all uncertain).

Although I count myself as a reasonably experienced investor, I do still have an independent financial adviser (Mike from Integrity Wealth Solutions). He oversees about half my investments, while the other half I look after myself. He also advises me on my financial situation more generally and answers any questions I can’t answer satisfactorily myself. i will talk more about this in another post. But I wanted to mention it here to show that I am not at all opposed to using a financial adviser and in general recommend it, particularly when starting out in investing.

My Best Investments of 2019

Below I have listed some of my investments that have performed best this year and/or caused me the least stress and hassle! I have included a few lines about each one, and links to any blog posts I have written about them for further info.

(1) Nutmeg

Nutmeg is a robo-advisory platform. I have used it for my Stocks and Shares ISA investments over the last three years. My investment pot has grown steadily, albeit with a few ups and downs, as is to be expected with equity-based investments. At the time of writing my Nutmeg pot has grown by about 40% since i started investing in April 2016, which is certainly a lot better than I could have achieved with a bank savings account. Of course, you shouldn’t normally invest in any equity-based product with anything less than a five-year timescale.

Nutmeg use exchange-traded funds (ETFs) as their investment vehicle. These are discussed in more detail in my in-depth Nutmeg review, which also includes details of what I invested with them and when. Note that my investment has grown by a further £1,100 since that article was published.

(2) Ratesetter

Ratesetter is a P2P lending platform. They don’t pay the highest rates, currently ranging from 3% for instant access to 4% for their Max account (where you pay a release fee of 90 days’ interest if you wish to withdraw). Though better than most bank savings accounts, those rates are clearly nothing spectacular.

One thing I particularly like about Ratesetter, though, is that they have a provision fund that effectively covers investors against defaults. That means you don’t have to worry about diversifying your investments across a range of loans, as is the case with some other P2P lending platforms. Of course, if the whole platform were to collapse the provision fund wouldn’t necessarily save you, but Ratesetter has been going for ten years now and appears professionally and competently run. It has delivered the promised returns to me with no stress or hassle, and I am happy to recommend it based on my experience.

In addition, if you check out my Ratesetter review you can discover how to get a free £20 bonus if you invest a mere £10 with them.

(3) Buy2Let Cars

I took a long time before deciding whether to invest with Buy2Let Cars, as it is quite an unusual investment. Basically what you are doing is putting up the money to buy a car for someone in a responsible job who can’t afford to buy one outright themselves. You then receive monthly repayments over a three-year period, and a final repayment of capital plus interest at the end of the loan. The minimum investment is £7,000, so this is obviously not going to work for everyone. Personally I bought one new car at a price of £14,000 in March 2018. Since then I have been receiving £250 per month in repayments, with a final payment of £8,429 due in month 37. That will give me a total net profit of £3,429 based on an annual interest rate of 10% (the rates on offer can vary but once you have signed an agreement the rate is fixed for the duration of the contract).

There are – of course – various safeguards and protections in place, fully discussed in my Buy2Let Cars review. Buy2Let Cars say that to date they have a 100% repayment record to investors, which appears to be confirmed by their Trust Pilot reviews. This investment has been working very well for me, with payments turning up in my bank account every month like clockwork. I am currently semi-retired, so it is providing a useful extra monthly income for me, with a large lump sum due in 2021, just a few months before I qualify for the state pension 🙂 If you think it might work for you, I recommend checking out my Buy2Let Cars review and speaking to my contact there, Brett Cheeseman, who helpfully answered all the questions I had at the time I invested.

(4) Kuflink

Kuflink offer the opportunity to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage.

Kuflink don’t pay the highest rates in this field – their loans are typically at an interest rate of around 7% – but in my view they offer a fair balance between risks and rewards. One thing I like about them is that interest is paid into your account monthly on all loans. I only have a relatively small amount invested, but so far everything has been going well with just the occasional short delay in repayment of capital.

Kuflink currently have a generous welcome offer, with cashback of up to £4,000 for new investors. Take a look at my Kuflink review for more information about this.

(5) Crowdlords

Crowdlords is a property crowdfunding platform. I have been investing with them almost since their launch and have made a good overall profit. Crowdlords pay competitive interest rates (over 20% in some cases) and offer a choice of equity and debt investments. Equity investments are higher risk than debt ones, but offer the potential for bigger returns if all goes well.

My only reservation about Crowdlords is that I currently have two overdue investments with them. In both cases, though, I have received full and reasonable explanations for the delays, and have been told that the money should be in my account within the next few months. Obviously, if that doesn’t happen, I will let Pounds and Sense readers know.

Crowdlords doesn’t have a welcome offer as such, but they do have a Refer a Friend scheme. If you sign up quoting my code, I will share the commission I receive 50:50 with you. Please see my Crowdlords review for more information about this.

So those are the investments that have given me the best returns and/or least stress during 2019. I do have others as well, including Primestox, ZOPA, Bricklane, The Lending Crowd, The House Crowd and Property Partner. Most of these have still made some money but none has really set the world alight.

Only Primestox actually lost me money. This is (or was) a premium food investment platform. They started promisingly and I made good returns on my early investments, but then they were hit by a series of delays and defaults. This happened with three projects I invested in. In the case of two I have received partial repayments with more promised, but in the third I have probably lost my £500. Primestox are no longer advertising investment opportunities, and I assume are re-evaluating their business model.

Property Partner is an interesting case. I have made modest returns on my portfolio this year, partly due to the fact that the property market in general has been in a slump. That said, there haven’t been any issues with delays or defaults, and dividends have been credited to my account every month as promised. It will be interesting to see what happens in 2020 as properties come up to their five-year anniversary and investors have the opportunity to exit at the current market price. As I noted in this recent blog post, this has the potential to create opportunities for both buyers and sellers.

I haven’t included certain other investments in this article. These include my Bestinvest SIPP, which is now in drawdown and holding up well in value. Neither have I included money invested via my financial adviser. This is mostly in funds from Prudential, which again are doing pretty well.

Lastly, I haven’t included the money I ‘invested’ in Football Index. My portfolio has more than doubled in value over 18 months, so in some ways it is my most successful investment of 2019! I am sure luck has played a significant part in this. Nonetheless, if you want to know more about Football Index – and read how you can get a risk-free £50 when signing up – you might like to check out this recent blog post.

I hope you have enjoyed reading this article, which has run on a bit longer than I expected. I hope also it may have given you a few ideas to investigate further if you are in the fortunate position of having money to invest.

As always, if you have any comments or questions about this article, please do post them below.

Disclaimer: As stated above, I am not a professional financial adviser, and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

If you’re looking for a home for your savings (or some of them), a friendly society might not be the first thought that occurs to you. Nonetheless, it may well be worth considering.

Friendly societies are one of a number of UK institutions called ‘mutuals’. These were originally set up by groups of people for a common financial or social purpose. Before modern insurance and the welfare state, friendly societies provided financial and social services to individuals, often according to their religious, political, or trade affiliations.

Friendly societies today typically provide a range of savings and insurance services. Along with other mutuals, they are regulated by the Financial Conduct Authority (FCA).

Why Save With a Friendly Society?

One big attraction of friendly societies is that they are owned by the members themselves. This means any profits generated go to members (directly or indirectly) rather than shareholders, as is the case with banks.

A good example is Shepherds Friendly, which offers a range of savings, investments and insurance products. These include a highly rated Stocks and Shares ISA. There is a minimum investment in this of £30 a month or a minimum lump sum of £100.

The Shepherds Friendly Stocks and Shares ISA is an actively managed fund and rated medium to low risk. The fund invests in a mixture of UK and overseas company shares, property, government and company bonds, and cash deposits. Most of the fund is normally invested in stocks and shares for greatest growth potential, but at times of economic turbulence some may be switched to safer investments such as bonds and deposits.

Investors in the Shepherds Friendly ‘With Profits’ Stocks and Shares ISA receive an annual bonus based on how the fund has performed in the year in question. Shepherds Friendly say that this has worked out at 3% for the last five financial years after all management fees and costs are deducted. Members may also receive a final bonus when they exit their investment. Note that annual and final bonuses depend entirely on how well the fund has performed, and are not guaranteed.

As with all ISAs, any profits are free of income tax and capital gains tax. Everyone has an annual ISA allowance, which is currently a generous £20,000 a year. This may be divided as you wish among a Stocks and Shares ISA, a Cash ISA and an Innovative Finance ISA (IFISA). However, you may only invest in one ISA of each type per financial year.

A major attraction of the Shepherds Friendly ISA is that it is covered under the Financial Services Compensation Scheme (FSCS) up to £85,000 per person. That means if the society were to collapse in a worst-case scenario, your capital would be protected and returned to you by the FSCS.

Bonus Fund

A further benefit of saving with a friendly society is that because of their special status they can offer additional tax-free savings over and above the ISA limit. In the case of Shepherds Friendly, you can save from £10 a month to £25 a month tax-free in their Tax Exempt Bonus Fund. This is also an alternative option if you have already invested in another Stocks and Shares ISA in the current tax year and are therefore excluded from the Shepherds Friendly ISA.

Voucher Offer

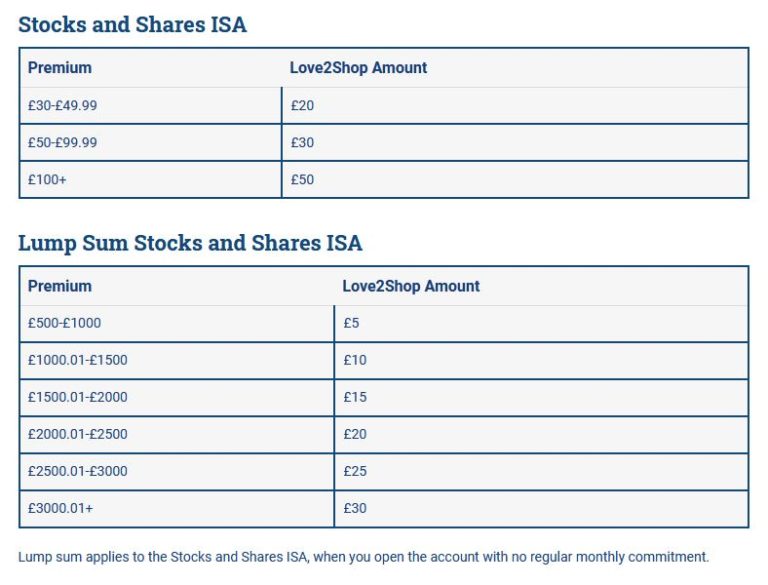

Shepherds Friendly are currently offering investors in their Stocks and Shares ISA a Love2Shop voucher worth up to £50 once you’ve made your first deposit. I’ve copied the actual amount you would receive for Stocks and Shares ISA investments below from the Shepherds Friendly website:

Many of the other financial products sold by Shepherds Friendly include a Love2Shop voucher as well – see this Terms & Conditions page on their website for more info.

Closing Thoughts

If you are looking for a home for some of your savings, Shepherds Friendly offers an interesting option. The society has over 100,000 members, so it is also one that is very popular.

The potential returns from the Shepherds Friendly Stocks and Shares ISA are higher than those currently on offer from banks, though not as high as the potential returns from P2P lending and property crowdfunding (among others). But those investment opportunities do of course tend to be riskier, and your money may not be as easy to access in an emergency. They are also not generally covered by the FSCS guarantee.

As with all stock-market-based investments, there are still risks involved, and past performance is no guarantee of what will happen in the future. Shepherds Friendly is at the lower-risk end of the spectrum, but you should still regard it as a medium to long-term investment (five years at least). With the Shepherds Friendly Stocks and Shares ISA, however, you can at least access some or all of your money at any time if you need it. As stated above, this is not the case with many P2P/property crowdfunding platforms.

As always, if you have any comments or questions about this post, please do leave them below. I’d also be interested to hear from anyone who has invested with a friendly society – be it Shepherds Friendly or another one – what your experience has been and whether you would recommend this method of saving to others.

Disclosure: This is a sponsored post on behalf of Shepherds Friendly. If you click through one of the links in it and make an investment, I may receive a commission. Please note that I am not a qualified financial adviser and nothing in this article should be construed as individual financial advice. You should always do your own ‘due diligence’ before investing, and take professional advice if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

I have mentioned P2P lending platform Ratesetter a few times on Pounds and Sense – most notably in my Ratesetter review.

Ratesetter is one of my favorite lower-risk P2P lending sites. It lets you save via a tax-efficient IFISA and/or an ordinary (taxable) Everyday account.

Although their rates aren’t the highest – currently 3% to 4% – I like the fact that risk is spread across all loans on the platform, with a provision fund to cover any defaults. This means that if someone you have lent money to via the platform defaults, it shouldn’t affect your returns. It also means that – unlike some other P2P lending platforms – there is no need to diversify your lending across the platform in order to control risk.

The Changes

Originally you could invest in Ratesetter in a choice of three different products: Rolling Market, One Year and Five Year.

The Rolling Market was the closest to an ordinary savings account, letting you withdraw some or all of your money any time without penalty. With the 1-year and 5-year products you could still request withdrawals before the full term of the loan, but in those cases a percentage charge was applied. This was 0.3% with the 1-year product and 1.5% with the 5-year product.

Under the new system, loans are spread across all three types of product. What was called the Rolling Market is now an Access account. As before, you can withdraw money from this at any time without penalty. There is just a ‘fair usage’ clause, which prevents investors from lending new money for 14 days after a withdrawal.

Instead of the 1-year and 5-year products, there are now the Plus and the Max. The Plus product pays more interest, but if you want to withdraw you have to pay a ‘release fee’ of 30 days’ worth of interest based on Going Rate at the time of release. And with the Max product, which pays more still, you are charged a release fee comprising 90 days of interest, again based on Going Rate at the time of release.

The Going Rate is the current interest rate for loans in the three product categories. Previously this was set by the market, based on supply and demand. That meant it could fluctuate, sometimes considerably, from day to day and even hour to hour. The interest rate you received could therefore vary a lot.according to when you invested (and when any returns were reinvested).

Under the new system, interest rates are set by Ratesetter themselves. This makes Ratesetter feel more like an ordinary savings provider. Currently the Going Rates are as follows:

Access: 3.0%

Plus: 3.5%

Max 4.0%

If you are already a Ratesetter investor, you may therefore want to reassess the type of product in which your money is held.

If – like me and many others – you put your money into a Rolling Market (now Access) product, you may want to think about transferring some to a Plus or Max account to take advantage of the higher interest rates. There is no greater risk in these accounts, and the only downside is that you will lose 30 or 90 days’ interest if you withdraw early. Doing this is likely to deliver better overall returns, so long as you remain in for at least six months in the case of a Plus account and a year in the case of a Max account. (These are only very approximate figures, as the interest rates paid can change.)

If you want to do this, you can’t (unfortunately) transfer money directly from one type of product to another. Rather – and I have confirmed this with Ratesetter – you will need to start by withdrawing your money from the product it is in currently (e.g. Access) so it goes into your holding account. You can then invest from your holding account into the new product (e.g. Max) that you want. Bear in mind though the 14-day rule mentioned above.

My Thoughts

Overall, I like these changes to Ratesetter. The new Going Rates are admittedly a little lower than the previous market rates. However, I think the greater stability and certainty over the interest rate you will be getting more than make up for this. I also like the new, simpler terms for withdrawing money from your account. I will continue to invest in Ratesetter and regard it as one of the safer (if less exciting) components of my portfolio.

As I’ve noted before on Pounds and Sense, P2P lending does not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme (FSCS). Nonetheless, the rates on offer at Ratesetter are significantly better than those from most banks and building societies. And the existence of a substantial across-the-board provision fund with a strong record of protecting investors from losses clearly offers reassurance.

It’s also reassuring that with all three products you can access your money if needed at any time, even though in the case of Plus and Max you will be charged a release fee for this. Obviously, you shouldn’t therefore put money into the Plus or Max products if you think there is any likelihood you will need it back within a month or two.

Clearly, no-one should put all their spare cash into Ratesetter (or any other P2P lending platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P lending isn’t a way of hedging your equity-based investments directly, but it does definitely help spread the risk.

If you would like more information about Ratesetter, please see my original Ratesetter review (which I will be fully updating soon).

Welcome Offer

Currently if you are new to RateSetter you can get £100 added to your account for free just by signing up and depositing £1,000. Full terms of the offer are reproduced below, and you can also find them on the RateSetter website.

You can take advantage of this offer so long as you

have not previously registered with RateSetter;

register after 27th March 2020; and

deposit a minimum of £1,000 through the RateSetter ISA or Everyday account and this is matched within 56 calendar days of opening an account.

Your bonus will be credited to your Everyday Account and invested in RateSetter’s Access (instant access) product at the going rate (currently 3%) within 30 working days of qualifying. From here you can transfer it to your ISA account if you like or simply withdraw it.

My Thoughts: This is a great offer from RateSetter if you are new to the platform. If you invest £1,000 and keep it there for a year, then including the £100 welcome bonus you will get a total return of between 13 and 14 percent for the first year (depending on whether you opt to invest your money in the Access, Plus or Max product). As a matter of interest, this is the same welcome offer I took advantage of when I signed up with RateSetter two years ago, and my bonus £100 was credited without any issues (or prompting from me) twelve months later.

Obviously if you need your £1,000 at any time, you can withdraw it (normally within 24 hours). This will though mean you don’t receive the £100 welcome bonus at the end of the first year.

Clearly, this is a generous promotional offer by RateSetter and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

If you have any comments or questions about this post, as always, please do leave them below.

Disclosure: As stated above, this post includes my referral link. If you click through and make an investment, I will receive a bonus for introducing you. This has no effect on the terms or benefits you will receive. Please be aware also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. You should do your own ‘due diligence’ before making any investment, and take professional advice if at all unsure how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you by my fellow money blogger Simon from Financial Expert.

In his post, Simon examines the pros and cons of investing in active versus passive funds. This is (of course) a subject of much debate among both pundits and investors. I will share a few thoughts of my own about it at the end.

Over to Simon, then…

For people who are enjoying their retirement or approaching it, choosing the right investments is clearly crucial.

With less time to correct mistakes, a bad investment choice is likely to have a major impact on quality of life in retirement. Many older people therefore struggle to make decisions given the number of investment choices available.

But before picking any particular trust or fund, all investors must first navigate a fork in the road. They must decide whether to follow an active or passive investment strategy.

Active Versus Passive

A fund manager following an active strategy has the discretion to hand-pick shares that they believe represent a superior investment opportunity. They do so in an attempt to deliver a return higher than the market average – for example, the return on the FTSE 100 index of large companies listed on the London Stock Exchange.

Funds that follow a passive strategy, on the other hand, use a mechanical approach of buying most of the shares which form indexes such as the FTSE 100. The objective of replicating the index is to provide a return which mirrors it as closely as possible.

Of these two approaches, which is the more successful? There are many arguments on each side of the debate. Below, I pull out the key pros and cons to help you decide.

In Support of Active Investing

Detailed research is valuable in opaque markets

In emerging markets and other less developed economies, quality financial information is a scarce resource. For example, emerging-market companies are less covered by investment analysts, and the quality of their financial reporting may be lower.

This creates a research deficiency which can be exploited by any active fund with a research team. Any insights generated by the boffins can be used to guide trades and improve the performance of the fund.

This is one of the key reasons why investors opt for active funds over passive funds in the emerging market equities asset class.

Moreover, the higher returns of high-risk markets such as emerging markets helps to cover the premium fees charged by active funds.

Absolute return strategies

Active funds are free to engage in investment strategies which seek to provide a positive absolute return regardless of whether the market is rising or falling.

They can do so by either short selling a company, by switching between asset classes, or by investing for relative value. Relative value investing is where fund managers seek out under-priced securities. They buy under-priced securities and sell over-priced peers. In theory this strategy will deliver a profit regardless of the overall direction of the market, as long as the pricing anomaly corrects itself over time.

These funds seek to provide a lower level of volatility compared to an ordinary equity investment, and similar returns over the long term.

However, the recent performance of large absolute return funds has been underwhelming. In the three years to the end of November 2018, the flagship absolute return fund managed by Standard Aberdeen’s has returned only -6.6% compared to 42% for an average investment trust.

In fact, only 12 of 102 similar funds reported a positive return over the same period. This implies that while active strategies might work on paper, they are difficult to execute in practice, particularly when so much money is chasing the same strategy.

The Drawback of Active Investing

Active managers are losers… most of the time

The track record of active funds highlights their biggest drawback: after fees, active funds tend to under-perform the market average.

Fund managers and research staff are expensive. This translates into higher annual ongoing charges. The higher the fees, the higher the bar is lifted on the returns needed to meet investor expectations.

Simple logic can provide a hint at why active funds disappoint:

Worldwide, the lion’s share of assets are still owned by active funds.

By definition, only half of the market participants can perform ‘better than the average’.

Of the winning half, some of these winners will have significantly outperformed, while many will have only incrementally outperformed.

Because of the premium fees they charge, any active fund that beats the benchmark only slightly will still come out as a loser after fees are taken into account.

Therefore we can conclude that theoretically, only a small proportion of fund managers (those that beat the benchmark by a good margin) can deliver the return that investors expect.

The second issue that plagues active managers is the difficulty of repeating the performance in subsequent years.

A fund manager may have enjoyed a particularly strong year because of sheer luck alone. Perhaps the fund happened to simply be in the right asset at the right time. This doesn’t guarantee that the fund will enjoy remarkable success in the future.

The temporary and unrepeatable nature of fund success explains why the fraction of fund managers that fail to meet their benchmark rises to the ‘Nine out of Ten’ statistic reported by the Financial Times when their performance is measured over a long time frame.

In Support of Passive Investing

Passive strategies deliver what they promise

Followers of passive investment strategies understand this logic and are prepared to accept an ‘average’ market return, in exchange for the assurance that they will not under-perform it.

Passive funds, which create portfolios which closely resemble the indexes they track, carry much lower fees as no research analysts or star fund managers are needed on the payroll.

With fees as low as 0.06%*, trackers give investors the best chance to achieve as close to the ‘average market return’ as possible. As stated above, this will beat active funds, which typically trail behind the same benchmark.

* Vanguard FTSE 100 Index Trust

The Drawback of Passive Investing

An unhealthy concentration

Indexes are created mechanically by companies such as FTSE and Standard & Poor’s. Each company in the index is weighted by its size, among other factors.

This formulaic approach has the unintended side effect of creating unhealthy levels of concentration.

Vanguard’s Emerging Market Stock fund is a good example. 31% of the fund value is invested in a single country; China. In contrast; India, Brazil and Russia take up just 8%, 8% and 4% of the fund respectively.

Indexes can also be skewed by industry. Financial companies form 24% of the same fund. This vastly outstrips banking’s share of the global economy. Even in the UK, which of course contains London, a global financial capital, banking and finance only contribute 6.9% of economic output.

The result of these distortions is that ‘diversified’ passive investors can find themselves exposed to country-specific, sector-specific or even company-specific risks. They may have no clue that such a large proportion of their portfolio is invested in such specific areas, given the global nature of the fund.

Therefore, while passive funds appear to give retirees the best opportunity to achieve average market returns over the long term, investors should be wary. Any potential index fund should be reviewed to discover whether they have an unintended concentration in a particular region or sector.

Many thanks to Simon for an illuminating article on an important topic for all investors.

Anyone who is considering investing in funds or trusts needs to bear in mind the distinction between passive and active management . For new investors, low-cost passive tracker funds, such as those run by Vanguard and mentioned by Simon above, could certainly be worth considering. But bear in mind the point Simon raises about the risk of unintentionally creating unhealthy levels of concentration in a single country, sector or even company.

Personally I have some money in tracker funds, but quite a lot more in funds that are actively managed. This is partly due to the fact that having no living dependants I can afford to take a slightly more adventurous approach in pursuit of better returns. Nonetheless, I do of course aim to diversify my investments as widely as possible, so that a downturn in one particular market or sector doesn’t impact too badly on the value of my overall portfolio.

I would also comment that most investment funds and trusts incorporate quite a bit of diversification already due to the range of investments they hold. Although they do of course come with a degree of risk, other things being equal this is likely to be a lot less than investing in individual company shares. And for older investors, careful risk management is key to ensuring a comfortable retirement, no matter how long this may prove to be 🙂

As always, if you have any comments or questions on this article, for me or for Simon, please do post them below.

Disclaimer: Nothing in this article should be construed as individual financial advice. All investments carry a risk of loss. Be sure to do your own ‘due diligence’ before making any investment and consult a qualified independent financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

On Pounds and Sense I often talk about the importance of having a diversified investment strategy. And the investment opportunity I am spotlighting today will certainly help you towards achieving that aim!

Raptor is a platform that provides ordinary individuals with the opportunity to invest in the production of gold and precious metal mining. The product on offer is a three-year mini-bond with a tax-free IFISA wrapping. Raptor are currently offering a return of 8 percent per year on a minimum £2,000 investment.

What Is An IFISA?

For those who may not know, IFISA is short for Innovative Finance ISA. IFISAs allow anyone to invest tax-free in authorized ‘innovative finance’ platforms, including P2P lending and mini-bonds.

You can put any amount into an IFISA up to your annual ISA allowance. In the current 2018/19 tax year this is £20,000, which can be divided however you choose between a cash ISA, a stocks and shares ISA and an IFISA. So, for example, you could invest £10,000 in a cash ISA, £6,000 in a stocks and shares ISA and £4,000 in an IFISA. The ISA allowance for 2019/20 will be £20,000 as well, though after that it could change.

Note that under current rules you are only allowed to invest new money in one of each type of ISA in a tax year. It is though generally possible to transfer money from one type of ISA to another without it affecting your annual entitlement (although there may be platform fees to pay).

How Is Your Money Invested?

The money raised from Raptor IFISA investors is used to provide ‘Stream and Royalty’ finance for mining companies. This is explained in detail in the Raptor IFISA brochure, but briefly Raptor’s investment arm (Raptor Capital International, or RCI for short) makes payments to carefully selected development-stage mining companies to purchase part of their future production at a price below the market level.

The mining company therefore receives much-needed capital through immediately monetizing part of its future production, and investors get the opportunity to make a good return on their investment. Stream and Royalty Finance is still relatively new, and with many high-quality mining projects requiring financing there is an opportunity for investors to capitalize on this.

What Are The Returns?

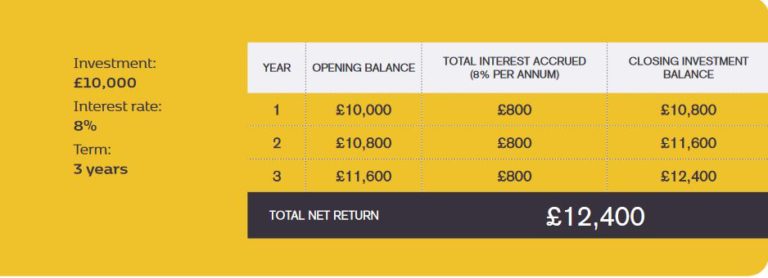

The Raptor IFISA pays 8% interest per year for the three-year term of each bond, with a minimum investment of £2,000. As it’s an IFISA, all profits are paid without any deductions for tax. There is also no charge for investing in the Raptor IFISA.

Returns are paid as simple interest, as shown in the diagram below, which has been copied from the Raptor IFISA brochure. All capital and interest is returned at the end of the three-year term (or earlier if the bond is repurchased/redeemed by Raptor before this point).

What Are The Risks?

All UK IFISA providers have to be authorized by the Financial Conduct Authority (FCA) and HMRC. This doesn’t in itself protect investors against the failure of a platform, however. While savers with UK banks and building societies are covered by the government’s Financial Services Compensation Scheme (FSCS), which guarantees to reimburse up to £85,000 of losses, this does not apply to IFISA platforms (or stocks and shares ISAs, for that matter).

IFISA investors don’t therefore enjoy the same level of protection in the UK as bank savers. This is, of course, a major reason why the returns on offer are significantly higher. It’s therefore important to be aware of the risks and ensure you are comfortable with them before investing this way. It’s also important to invest across a range of asset classes and sectors, and not make the mistake of putting all your eggs in one investment basket.

In addition, the Raptor IFISA is not a liquid investment. Your money will normally be tied up for three years. Raptor say they will assist investors if they want to sell or transfer their bonds to another investor, but there is no guarantee that a buyer will be found. This opportunity is therefore not suitable for funds you might need back quickly and should be regarded as a medium- to long-term investment.

Finally, there is of course a risk that the underlying mining investments will not pay off. However, Raptor and RCI’s Advisory Committee say they will undertake extensive due diligence and engage third-party providers to assist in determining whether or not projects meet and qualify for financing in accordance with set criteria, for example:

There has to be at least a 200,000 ounce gold resource (or gold equivalent ounces).

Uncomplicated metallurgy, allowing simple, conventional, traditional extraction.

Payback of initial capital and interest within three years of production.

Access to mining company financial records.

Allow an RCI agent on site to oversee operations.

With all that said and done, there is no guarantee that you will receive the advertised returns. It is important that you understand and are comfortable with the risks involved.

Summing Up

If you are looking for a home for some of your money that can offer better interest rates than banks and building societies – and won’t incur any tax charges – the Raptor IFISA is worth considering.

As well as higher interest rates, Raptor bonds can add diversity to your saving and investment portfolio, helping you ride out peaks and troughs in the financial markets. The bonds provide an opportunity to profit directly from the returns to be made in precious metal mining, a sector under-represented in many people’s portfolios. The relatively low minimum investment of £2,000 and absence of any charges are further attractions. Just be sure that you are aware of the risks involved, and that you invest only as part of a diversified portfolio.

For more information, please visit the Raptor IFISA website. You can find out more about the investment opportunity there, and also download an informative 14-page brochure.

Disclosure: this is a sponsored post on behalf of the Raptor IFISA. All investments carry a risk of loss. Be sure to do your own ‘due diligence’ before investing, and speak to a qualified professional financial adviser if in any doubt before proceeding.

If you have any comments or questions about this post, as always, feel free to post them below.

If you enjoyed this post, please link to it on your own blog or social media:

In just a few weeks (5th April 2019) it will be the end of the financial year. And that means if you want to make the most of your 2018/19 ISA allowance, you will need to take action soon.

As you may know, ISA stands for Individual Savings Account. ISAs are saving and investment products where you aren’t taxed on the interest you earn or any dividends you receive or capital gains you make. An ISA is basically a tax-free ‘wrapper’ that can be applied to a huge range of financial products.

With ISAs you don’t get any extra contribution from the government in the form of tax relief as you do with pensions. But – except in the case of the Lifetime ISA – you can withdraw your money at any time (subject to any rules about the term and notice period required) and you won’t be taxed on it.

Everyone has an annual ISA allowance, which is the maximum amount you can invest in ISAs in the year concerned. In the current financial year (2018/19) this is a generous £20,000.

There are four main ISA categories: Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA. You can divide your £20,000 ISA allowance among these in any way you choose, but you are only allowed to invest in one ISA in each category per year. Let’s look at each type in a bit more detail…

Cash ISA

Cash ISAs are like standard savings accounts except the interest you receive doesn’t incur income tax.

Unfortunately interest rates are very low at the moment. According to price comparison sites, the best rate for an instant-access cash ISA is currently 1.45% with Virgin Money. With inflation at 1.8% (January 2019) that means even in the best paying cash ISA your money will still be losing spending power when invested this way.

What’s more, the new Personal Savings Allowance (PSA) means most people can get up to £1000 in savings interest without paying tax anyway. As a result of these things, cash ISAs have lost much of their appeal, though if interest rates rise they may become more attractive again.

It is also worth bearing in mind that money invested in a cash ISA remains tax-free year after year. So if in the years ahead interest rates on cash ISAs rise, the benefit of having one will increase as well.

Nonetheless, I have decided not to invest any of my ISA allowance in a cash ISA this year, as I have (in my view) better uses for my money. You might see this differently, of course!

Stocks and Shares ISA

Stocks and shares ISAs are a good choice for many people saving long term. Over a longer period the stock market has outperformed bank savings accounts, often by a considerable margin. You do, though, have to expect some ups and downs in the value of your investments in the short to medium term.

You can opt for a standard stocks and shares ISA offered by a wide range of financial institutions and let them choose your investments for you. Alternatively you can use self-investment platforms such as Hargreaves Lansdown or Bestinvest to choose your own investments from the wide range of shares and funds available.

IFISAs are on offer from a small but growing range of peer-to-peer (P2P) lending platforms. P2P platforms allow people to lend money to businesses and private individuals and get their money back with interest as the loans are repaid. If you invest in the form of an IFISA all the interest you receive from P2P lending is paid tax-free, otherwise it is taxed as income (though interest from P2P lending does qualify for the Personal Savings Allowance of up to £1,000 a year, mentioned above).

Peer-to-peer platforms generally offer more attractive interest rates than bank and building saving accounts (or cash ISAs) – from around 4% to 10% or more. They aren’t covered by the same guarantees as the banks and are therefore riskier, though. And if you need your money back urgently there may be delays and/or extra charges to pay.

Nonetheless, in the current climate of low-interest savings accounts and volatile stock markets, more and more people are looking to IFISAs as a home for at least some of their savings.

Some leading peer-to-peer lending platforms which offer IFISAs include Ratesetter – which I have invested in myself and reviewed in this post – and Funding Circle, which lends to businesses.

Lifetime ISA

Lifetime ISAs or LISAs are a new-ish initiative from the government to encourage younger people to save. They do have one big drawback for older people: you have to be under the age of 40 (though over 18) to open one.

LISAs are designed for two specific purposes: buying your first home and saving for retirement. How they work is that you can pay in up to £4,000 a year (lump sums or regular contributions) and the government will top this up with another 25%. As long as you open your LISA before the age of 40 you will continue to receive the bonuses on your contributions until you reach 50.

So if you pay in the maximum £4,000 in a year, the government will top this up to £5,000. If you pay in the full £4,000 every year from the age of 18 to the upper limit of 50, you will therefore get a maximum possible bonus from the government of £32,000.

LISAs are therefore somewhat different from the other types of ISA mentioned above, but nonetheless any money you invest in one comes out of your annual ISA allowance (currently £20,000). So if you pay the maximum £4,000 into a LISA this year, that comes out of your £20,000 ISA allowance, leaving you with ‘just’ £16,000 to invest in other sorts of ISA.

Your money will grow without any tax deductions in a LISA, and you can also withdraw without having to pay tax. However, there are certain restrictions. In particular, you can only use the money in your LISA for one of two purposes: paying a deposit on your first home or saving for retirement. While you can access your money for other reasons, you will then lose 25% of the total, including your own contribution and the government bonus along with any investment growth. That means in many cases you will get back less money than you put in.

The 2018/19 ISA allowance is a generous £20,000 and offers the potential to save a lot of money on tax assuming you are lucky enough to have this amount to save or invest. But, very importantly, it cannot be rolled over. So if you don’t use your 2018/19 ISA allowance by 5th April 2019 at the latest, it will be gone forever. It is therefore important to attend to this now and ensure you get as much value as possible out of this valuable tax-saving concession.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser and cannot give personal financial advice. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media: