My Investments Update – August 2024

Here is my latest monthly update about my investments. You can read my July 2024 Investments Update here if you like.

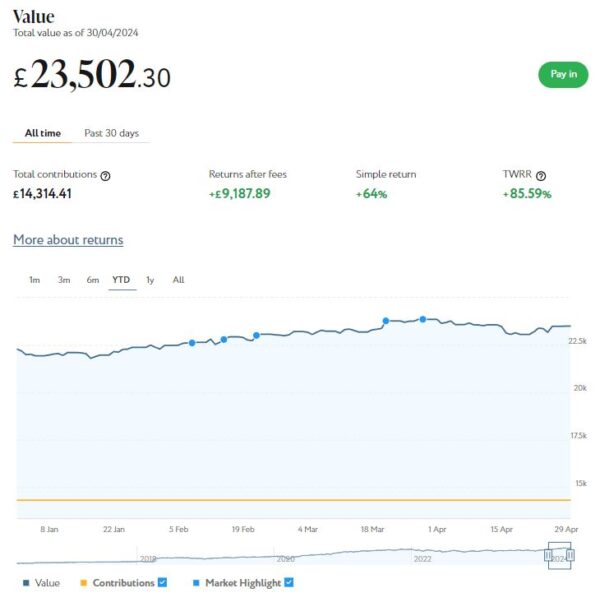

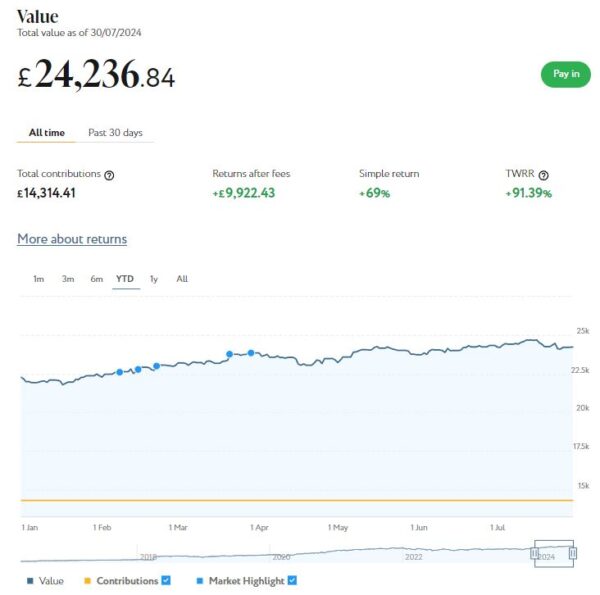

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

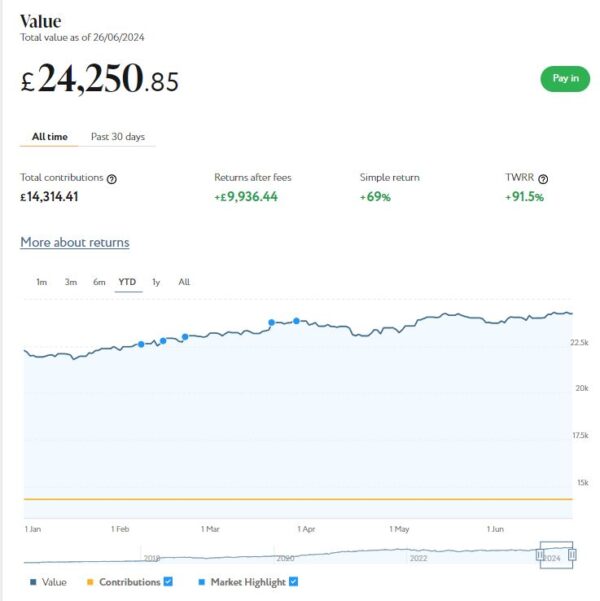

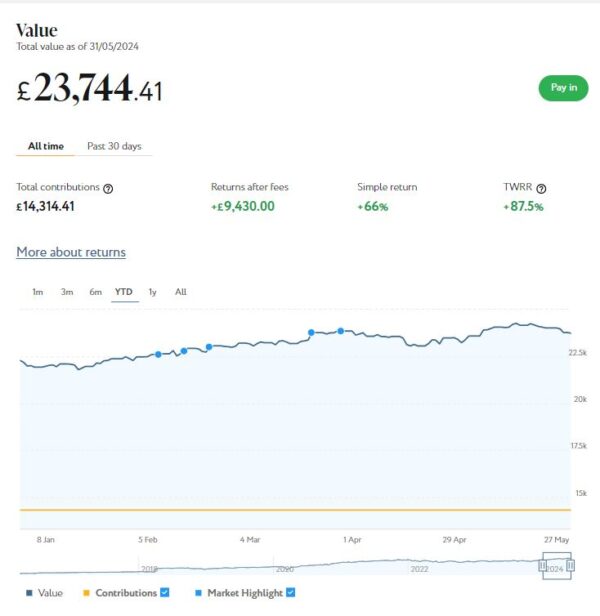

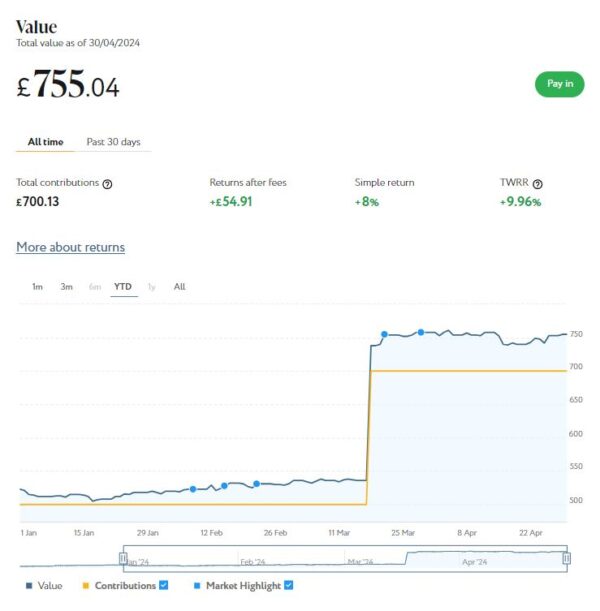

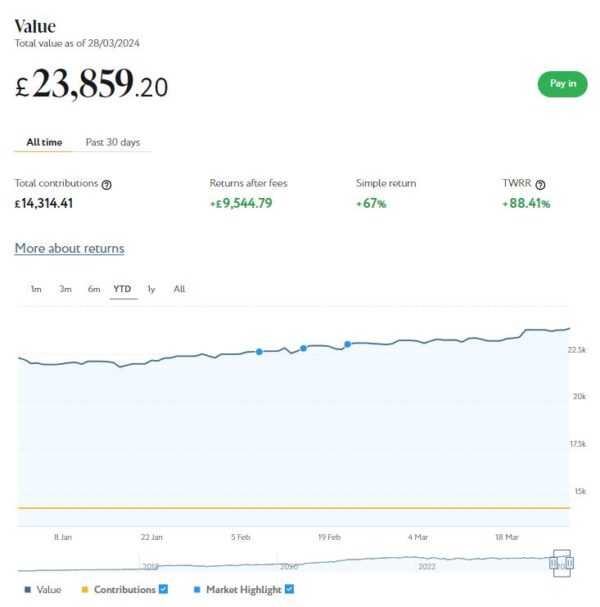

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,237 (rounded up). Last month it stood at £24,250, so that is a small decrease of £13.

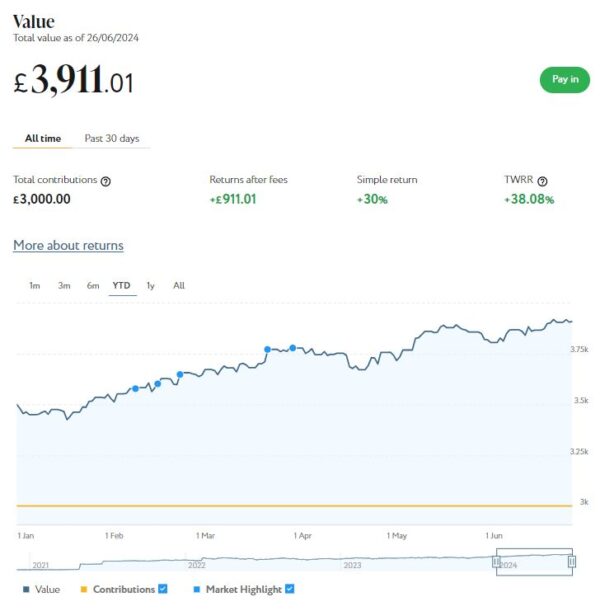

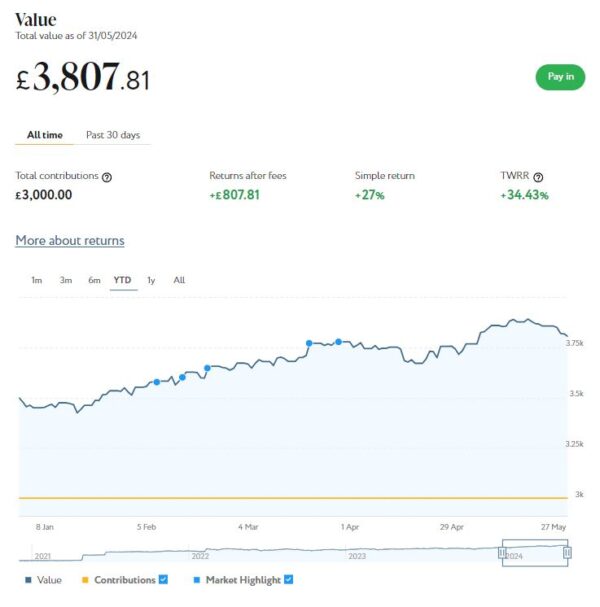

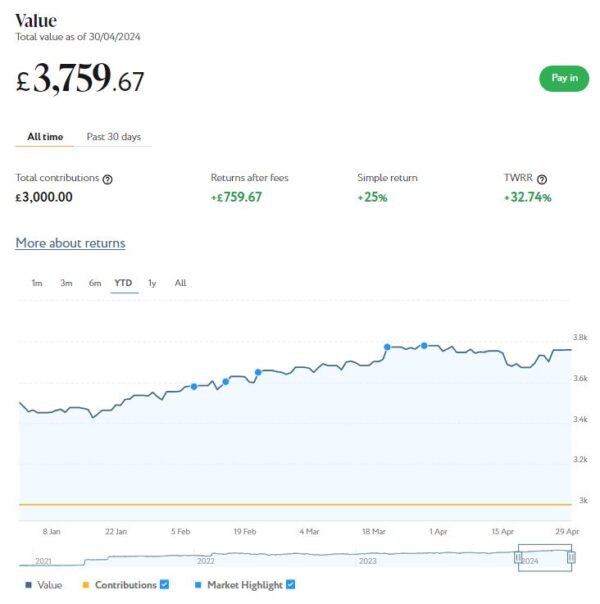

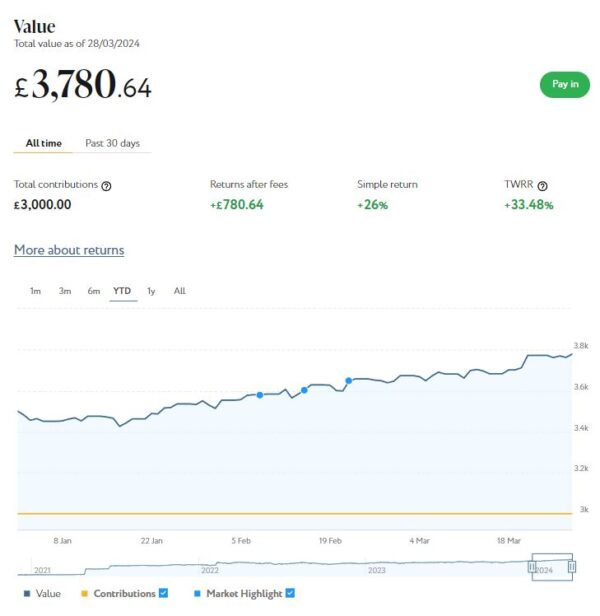

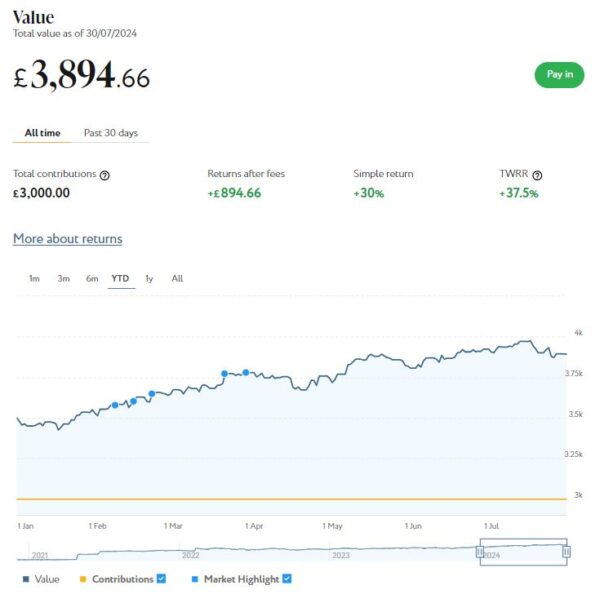

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,895 compared with £3,911 a month ago, a fall of £16. Here is a screen capture showing performance over the year to date.

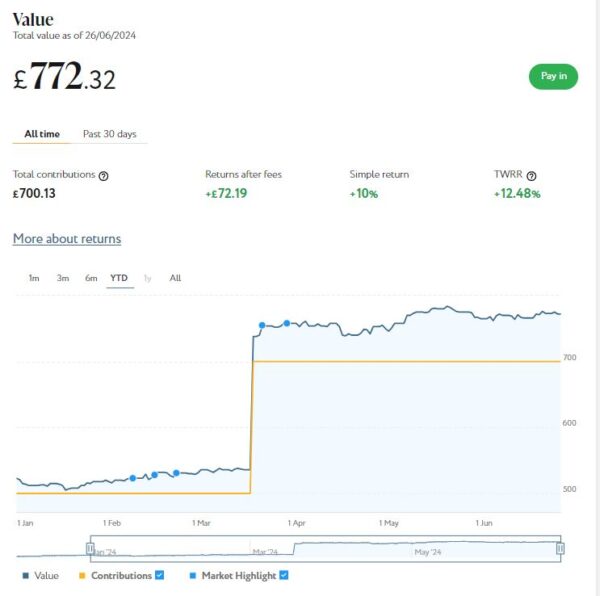

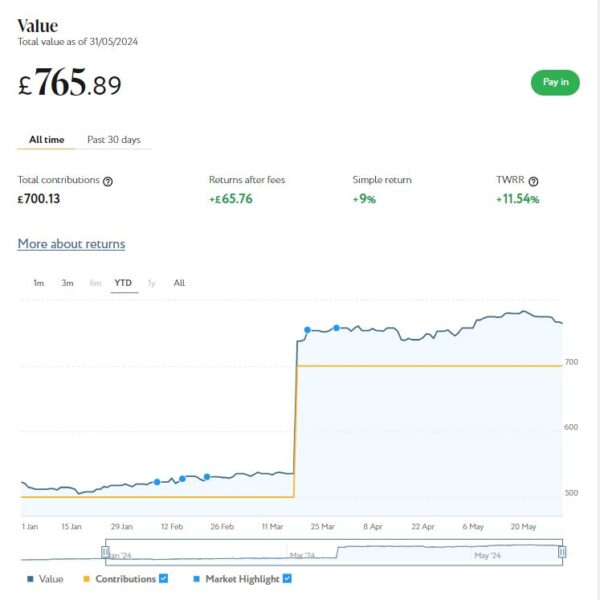

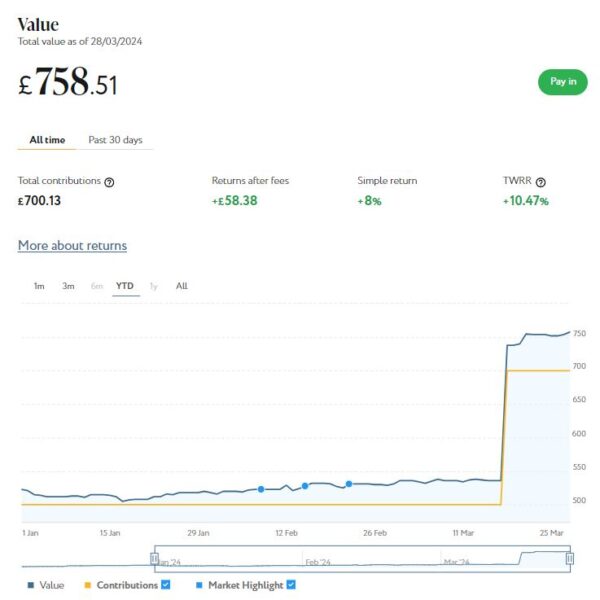

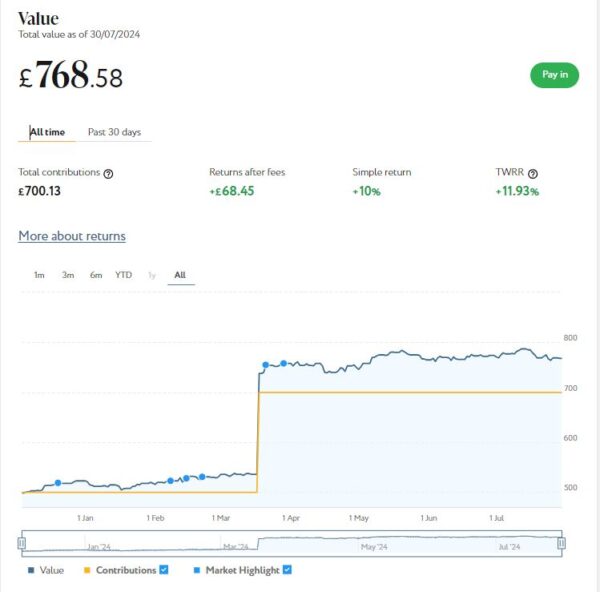

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the all-time screen capture below, this portfolio is now worth £769 compared with £772 last month, a small decrease of £3.

As you can see from the charts, July was an up-and-down month for my Nutmeg investments. Their overall value has fallen by a modest £32 or 0.11% since the start of July.

Although any fall is disappointing, short-term ups and downs are very much very much to be expected with stock market investments. And it is worth observing that the overall value of my Nutmeg investments is still up by £2,586 or 9.82% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

- You may like to note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the new tax year began on 6 April 2024 and and you have a whole new £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you so wish) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. Last month I withdrew £500 from completed loans and now have £40 remaining in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £195.87 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £28.74, meaning that overall (rental income minus capital value decrease) I am up by £167.13. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

- As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Note that as from this financial year (2024/25), you can open more than one IFISA per year.

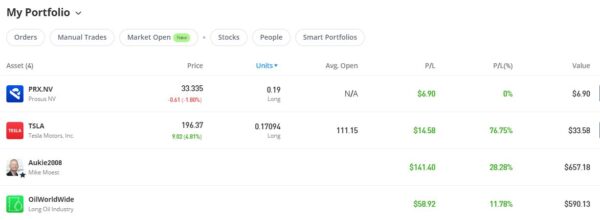

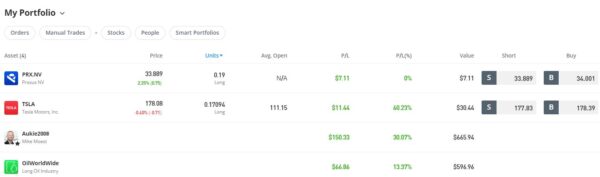

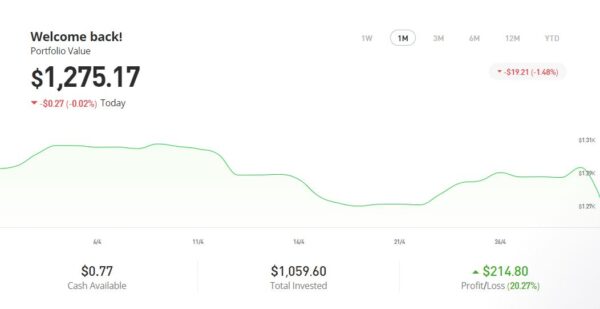

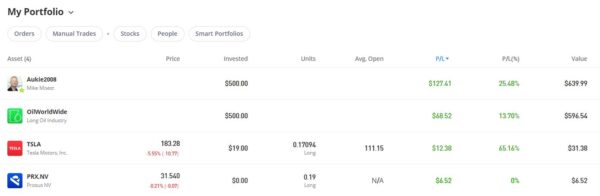

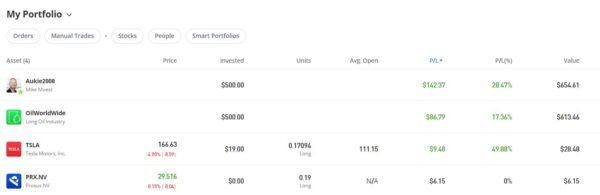

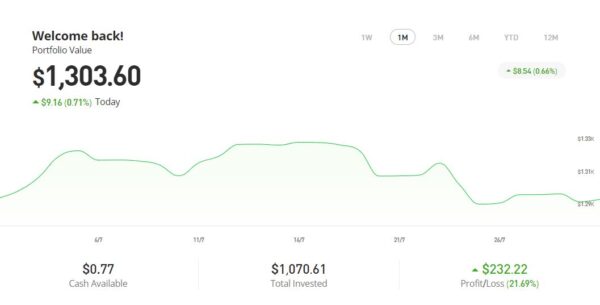

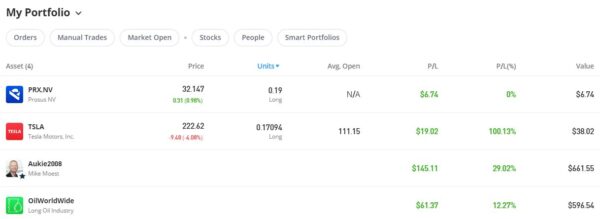

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

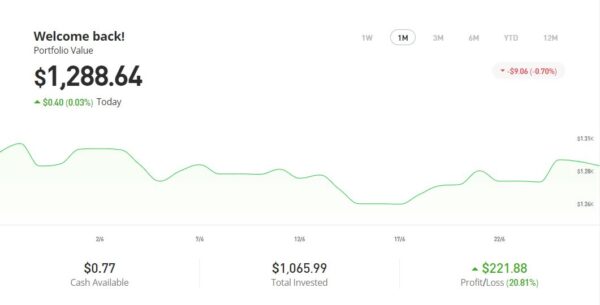

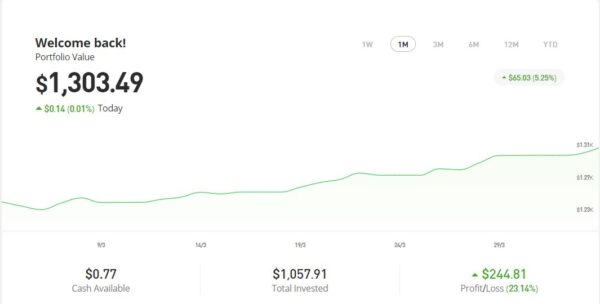

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.60 an overall increase of $281.34 or 27.52%.

You can read my full review of eToro here. You may also like to check out my more in-depth look at eToro copy trading. I also discussed thematic investing with eToro using Smart Portfolios in this recent post. The latter also reveals why I took the somewhat contrarian step of choosing the oil industry for my first thematic investment with them.

As you can see, my Oil WorldWide investment is showing just over 12% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

- eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in June on the excellent Mouthy Money website. The first is Seven Ways to Make Money From Your Garden. In this article I set out seven ways you can make money from your garden (if you’re lucky enough to have one). None of these is likely to make you a fortune, but they can all help your finances stretch further in these challenging times.

Also in July I revealed how you can Make a Sideline Income Renting Out Your Driveway. If you have a parking space or driveway that sits empty most of the day, turning it into a source of passive income is easier than you might think. In this article I explained how you can get started and make the most from this opportunity.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the wide range of articles published in July, I particularly enjoyed Five Ways Tracking Your Spending Can Improve Your Finances by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living, and this article is a good example of her work. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in June. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

How to Protect Your Savings and Investments Under a Labour Government was originally written and published before the general election. I revised and updated it after Labour’s widely anticipated victory, but the advice remains largely the same. A significant part of this involves making the most of tax-free opportunities such as ISAs and (to an extent) pensions, but various other methods and strategies are suggested as well. Nothing that has happened since Labour came into power has suggested to me that the advice in the article needs changing.

Also in July I published Ten Tax-Free Ways to Boost Your Finances. As you may have heard, UK citizens currently bear the highest tax burden since WW2. And with the new government looking to raise more money to pay for its ambitious spending plans, there is no sign of that changing any time soon. So in this article I set out some ways you may be able to boost your finances without increasing your tax liability. As you’ll see, doing this needn’t involve complicated investment strategies or seeking ‘loopholes’ in tax law. The article sets out ten perfectly legal ways you can boost your finances without having to worry about the taxman.

Next, a few odds and ends. I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you then decide to invest yourself, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Speaking of energy, a quick reminder that if you switch to EDF via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight the decision by the new government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it 🙏

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you get the full state pension and/or a private pension (even just a tiny one) the chances are you won’t be eligible. I do therefore recommend writing to your MP and asking for this Draconian decision to be rescinded. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK.

Sorry to end on a downbeat note. At least in this cold, damp, depressing summer we are currently enjoying a few days of warm sunshine, so I hope you have been able to get out and make the most of it. I am sure normal service will be resumed soon!

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!