Today I’m pleased to bring you a guest post from my friend and near-neighbour Sally Jenkins, a successful published fiction and non-fiction author (check out her latest novel Out of Control – a later-life romance perfect for summer holiday reading!).

Many older people (in particular) harbour an ambition to write a book and make money from it. If that includes you, I hope you will find Sally’s article of interest. In it she sets out the main options for getting your book published, and shares some valuable resources she has found.

Over to Sally then…

Everyone has at least one book in them, or so the saying goes. It might be a thriller, a memoir, a collection of poems or short stories, a ‘how-to’ non-fiction manual or something completely different. Finishing that manuscript is a laudable achievement in itself but don’t stop there. It takes guts to send any literary work out into the public arena; however, doing so can lead to an additional passive income stream in the form of royalties that continue to hit your bank account long after you’ve finished writing.

There are three main routes to publication that you might like to consider:

Traditional Publishing

Traditional publishers come in all shapes and sizes, from the giants like Penguin and Hachette to far smaller, less well-known companies who publish in e-book format only.

Traditional publishers bear all the costs of publishing a book, meaning there is no financial risk for the author. These costs may include editing, proofreading, cover design, marketing and the printing of physical copies. The author contributes nothing to these costs and receives a small royalty for each copy of the book sold.

The competition to be signed by a traditional publisher is fierce and only a very small number of authors are taken on. The larger companies will only accept manuscript submissions via a literary agent but it is possible for authors to submit directly to many of the small publishing houses. There is nothing to lose by trying this traditional route but be prepared to develop a thick skin to deal with the probable rejections. A good place to start is an up-to-date copy of the Writers’ and Artists’ Yearbook, which contains a comprehensive list of publishers and literary agents.

Partnership Publishing

In the partnership publishing model, the publisher and the author share the financial risk of publishing the book. This means the author will be asked to make a financial contribution towards the publishing costs. What proportion and how much this means in monetary terms will vary from company to company, so it’s worth approaching more than one partnership publisher and requesting explicit information about their offering. In return for contributing to the publishing costs, the author can expect to receive a higher percentage of royalty payments than under the traditional model.

However, care is needed when choosing a partnership company to work with – there are many rogue or ‘vanity’ publishers out there who will publish anything and charge a lot of money for very little service. Ensure that the company you choose has a manuscript selection process – even if this means you might face rejection as in the traditional model. A true partnership publisher will only publish books that it thinks have merit and will sell. Even so, there is no guarantee that you will recoup all or any of your publishing costs via royalties. Do not spend more than you can afford to lose.

Authors who self-publish carry all the financial risk themselves but retain all the royalties (bar the amount taken by distribution platforms such as Amazon). It is possible to self-publish on Amazon at no cost or you might choose to spend hundreds of pounds depending on what services you buy in. The main services requiring financial outlay will be:

Cover Design – don’t attempt this yourself unless you are a graphic designer with a knowledge of the book covers currently selling in your genre. An amateur cover design will be obvious and off-putting to potential readers.

Editing – a novel (particularly a first novel) may benefit from a full structural edit. This will advise on plot, character development, pace etc. You might also want to consider a sentence level copyedit and/or proofread.

Formatting – some authors pay for this but, with a little patience, anyone who can use Microsoft Word can do this themselves.

Printing – there is no need to pay for a print run of books and hold them in stock.

Amazon (and other companies) use print-on-demand (POD) technology. This means that when someone orders a copy of your book it is printed individually and sent direct to the customer. Authors can also order copies at a reduced rate to sell direct to friends, family or the public at large.

The Alliance of Independent Authors has a directory of reputable editors, cover designers, proofreaders, etc. The directory also lists companies who can offer a complete self-publishing service for authors who don’t want to do any of the leg work – but this can be very expensive. As with partnership publishing, never spend more than you can afford to lose.

If you would like to know more about low-cost self-publishing via Amazon, the e-book Kindle Direct Publishing for Absolute Beginners (pictured, left) offers a good introduction. If you don’t currently read on Kindle, download the free Kindle app to your laptop, tablet or smartphone.

Whichever publishing route you choose, enjoy the journey and the royalties!

Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher Choc Lit (part of Joffe Books). She has also had a novel published in partnership with The Book Guild and has self-published several books via Amazon KDP. When not at the keyboard, she feeds her addiction to words by working part-time in her local library and running two reading groups. Sally can also be found walking, church-bell ringing and enjoying shavasana in her yoga class. Follow her writing blog at https://sally-jenkins.com/.

If you enjoyed this post, please link to it on your own blog or social media:

Having fallen out of favour for a while due to a lack of suitable opportunities, the sideline-earning system of stoozing is back in the spotlight again!

Stoozing is a financial strategy that allows individuals to profit by leveraging 0% interest credit card offers. By using the interest-free periods, you can earn interest on borrowed funds without incurring additional costs.

Here’s a guide to effectively implementing a stoozing strategy…

1. Understanding Stoozing

Stoozing involves borrowing money through a credit card offering a 0% interest period and depositing that money into a high-interest savings account. The goal is to earn interest on the borrowed funds and repay the credit card balance before the interest-free period ends. This method requires careful planning and discipline to ensure profitability.

2. Steps to Implement Stoozing

Select a Suitable 0% Interest Credit Card

Begin by researching credit cards that offer a 0% interest period on purchases or balance transfers. Opt for cards with the longest interest-free durations to maximize potential gains. Ensure you understand any associated fees, such as balance transfer fees, which could impact your overall profit. A useful resource for tracking down cards with 0% interest-free offers can be found on the popular MoneySavingExpert website.

Use the Credit Card for Everyday Purchases

Instead of using your debit card or cash, utilize the 0% interest credit card for daily expenses. This approach allows your regular income to remain in your bank account. This money can then be transferred to a high-interest savings account. Note that you should never withdraw cash directly from your credit card as you will be charged interest on this and it may also adversely affect your credit score (see below).

Deposit Funds into a High-Interest Savings Account

Transfer the money that would have been used for purchases into a high-interest savings account. This strategy enables you to earn interest on funds that would otherwise have been spent. Regularly monitor interest rates using a platform such as MoneySuperMarket to ensure you’re getting the best possible return on your savings.

Make Minimum Monthly Payments

It’s essential to make at least the minimum monthly payments on your credit card to maintain the 0% interest offer. Setting up a direct debit can help prevent missed payments, which could result in losing the interest-free benefit.

Repay the Full Balance Before the 0% Period Ends

Before the end of the 0% interest period, ensure you repay the entire credit card balance using the funds in your savings account. The difference between the interest earned and any fees paid represents your profit.

3. Example of Potential Earnings

Let’s say you obtain a 0% interest credit card with a 24-month interest-free period and a credit limit of £5,000. You deposit the full £5,000 into a high-interest savings account offering an annual interest rate of 5%.

Year 1 Interest: £5,000 x 5% = £250

Year 2 Interest: £5,000 x 5% = £250

Total Interest Earned Over 2 Years: £500

Assuming there are no fees and you meet all minimum payments on time, your profit from stoozing would be £500, simply by leveraging the 0% interest period.

4. Calculating Potential Profits

To assess the potential gains from stoozing, you can use online calculators designed for this purpose. These allow you to enter details such as the balance to be transferred, the introductory period, balance transfer fees, and minimum monthly payments to estimate your profit. One such calculator is available at stoozing.com.

5. Risks and Considerations

While stoozing can be profitable, it’s important to be aware of potential risks:

Discipline Required: Failure to make minimum payments or repay the balance before the 0% period ends can lead to interest charges that outweigh your earnings.

Credit Score Impact: Applying for multiple credit cards can affect your credit score. It’s advisable to check your credit report before proceeding. And it may be best to avoid stoozing if you plan to apply for a mortgage or business loan in the near future.

Changing Interest Rates: Savings account interest rates can vary, potentially reducing your anticipated profits.

Fees: Be mindful of any fees associated with the credit card or savings account, as they can erode your gains.

6. Closing Thoughts

Stoozing offers a method to earn additional income by strategically using 0% interest credit card offers and high-interest savings accounts.

Success in stoozing hinges on careful planning, disciplined financial management, and a thorough understanding of the terms and conditions associated with the financial products involved. Always ensure that the interest earned exceeds any fees incurred to achieve a net profit.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2024, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

Thank you for being a valued Pounds and Sense reader. Just a reminder that you can get notifications every time the blog is updated via the Subscribe box on the right (or scroll down on mobile devices). You can also follow PAS on X/Twitter and Facebook and now on BlueSky as well 🙂

If you have any comments or questions about this post, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

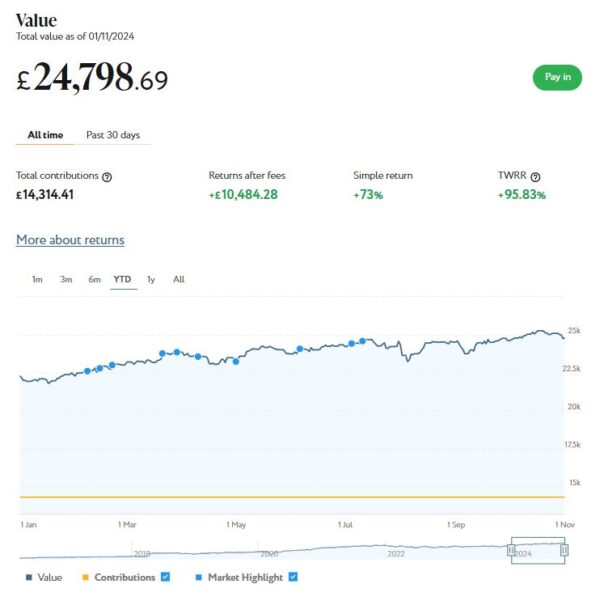

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,799 (rounded up). Last month it stood at £24,625, so that is an increase of £174.

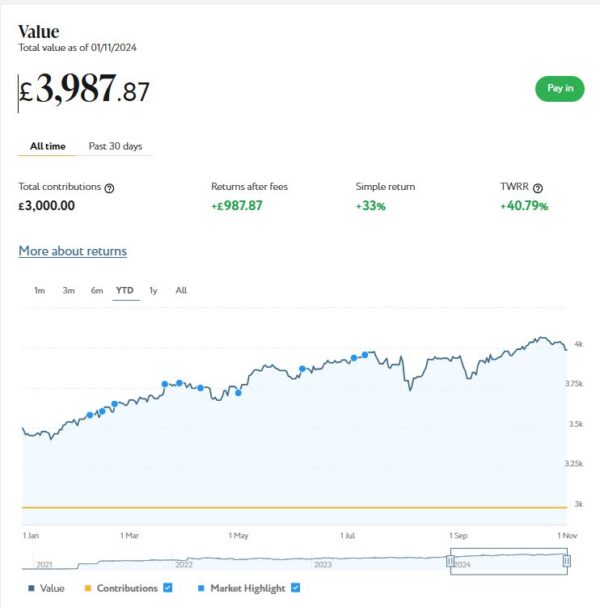

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,988 (rounded up) compared with £3,954 a month ago, a rise of £34. Here is a screen capture showing performance over the year to date.

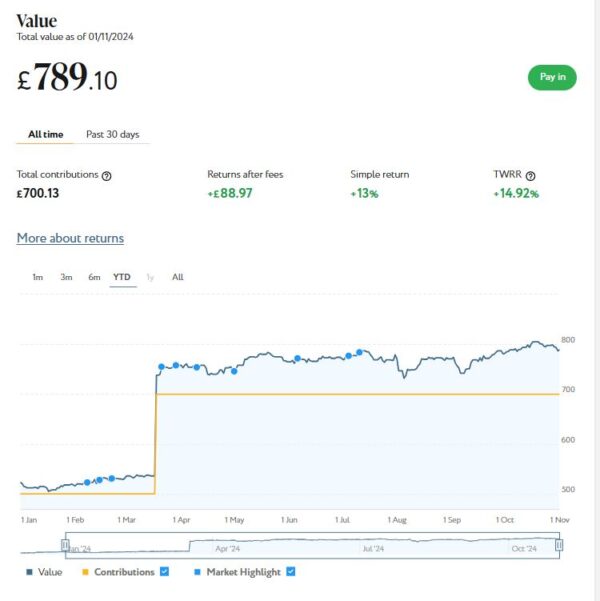

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £789 compared with £781 last month, a small rise of £8.

As you can see, October was another decent month for my Nutmeg investments, though the last few days saw a bit of a dip. The overall value has risen by £216 or 0.75% since the start of October. They are also up by £3,261 or 11.62% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024. Despite some predictions to the contrary, you still have a full £20,000 tax-free ISA allowance for 2024/25. As from this year, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Note that after this month I will not be including Kuflink in my monthly updates. I am gradually winding down my portfolio with them, as part of the de-risking process for my investments as i get older. As I’ve said above, I have no particular issue with Kuflink, though I do think increasing their minimum investment was unfortunate for the reasons stated above. But I still recommend them if their offering suits your investment strategy and risk appetite.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £215.02 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 17 are showing losses. My portfolio of 34 properties is currently showing a net decrease in value of £43.61, meaning that overall (rental income minus capital value decrease) I am up by £171.41. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

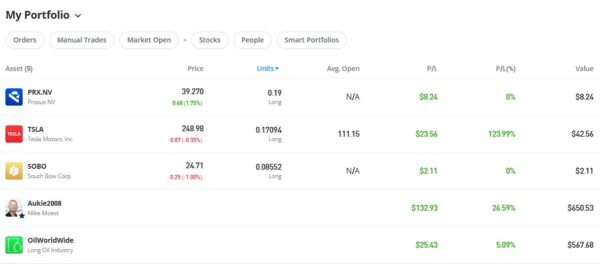

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,271.89 an overall increase of $249.63 or 24.42%.

As you can see, my Oil WorldWide investment is showing 5.09% profit. That’s a bit underwhelming, but at least it’s a profit! Obviously my copy trading investment with Aukie2008 has been doing much better.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in October on the excellent Mouthy Money website. The first is How to Cut Your Energy Bills This Winter. With the coldest winter months fast approaching, energy bills can quickly become a significant financial burden. So in this article I set out some tips to help you reduce your energy costs and keep your home warm without breaking the bank.

Also in October Mouthy Money published my article Always Wanted to be in the Movies? Let TV Studios Use Your Home for Money. As I explained in this, you definitely don’t need to live in a stately home to profit from this opportunity. A huge range of properties is required, so wherever you live there’s a chance it could be the perfect location for an upcoming project.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in October, I particularly enjoyed How to Prepare for a Frugal Winter by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published (or republished) several posts on Pounds and Sense in October. Some are no longer relevant, but I have listed the others below.

In Here’s Why I’m Not Doing EDF Energy’s ‘Sunday Saver’ Challenge I set out my reasons for being dubious about this particular money-saving opportunity. This post has actually generated more comments than any before from readers sharing their experiences. If you’re considering doing this challenge (or a similar one from another energy company) I strongly recommend reading what others are saying about it. I must admit that having seen all the comments (those from Harry especially!) I am now more enthusiastic than I was originally, and will be giving it a try in November. Watch this space!

My post on How to Prepare for Winter Blackouts revealed my reasons for believing winter blackouts are increasingly likely in the UK, from government energy policies to the conflicts in Ukraine and the Middle East. I set out a range of tips to ensure that you and your family are well-prepared should the worst happen.

In Will You Get the Warm Home Discount? I discussed this scheme which provides people on low incomes and/or certain means-tested benefits with a discount of £150 on their electricity bill. This is a one-off payment that will be credited to your electricity account by March 2025 (you won’t receive it in cash). The 2024/25 scheme has recently launched, and in this post I revealed who may be eligible.

In my post Should You Take a Lump Sum From Your Pension Now? I looked at the pros and cons of taking a tax-free lump sum from your pension. Retirees can typically withdraw 25% of their pension pot as a tax-free lump sum once they reach the age of 55. At the time I wrote this there was much speculation whether this tax-free allowance would be removed or reduced by Chancellor Rachel Reeves in her budget. That didn’t happen, but you might still find this article informative if taking a lump sum from your pension is on your agenda sometime soon.

My Review of the Simba Orbit Weighted Blanket was a sponsored post. I was sent this product free of charge by my friends at Simba Sleep. In this post I revealed what I thought of it.

And in Twelve Great Christmas Gift Ideas for Older People (That Aren’t Socks) I set out 12 suggestions for presents for older friends and relatives that – based on my experience as an older person myself – should put a smile on their faces! If you’re struggling for ideas for gifts for older friends and relatives, check this out 🙂

Lastly – as referred to earlier – in October we had Labour Chancellor Rachel Reeves’ first budget. This seemed a very long time coming and was the subject of much speculation – and no small amount of dread – beforehand.

My initial reaction was that it wasn’t as bad as it could have been. Several of the possible measures that had been touted didn’t happen. That includes cuts to the £20,000 annual tax-free ISA allowance, the ending of the old person’s bus pass, and the scrapping of the 25% council tax discount for single-person households. The last two in particular would have been very bad news indeed for older people on top of losing (in many cases) their Winter Fuel Payment. Thankfully these things haven’t happened (yet).

Also on the plus side, the additional investment in the NHS is obviously welcome, though in my view this does need to be accompanied by structural changes to boost efficiency and productivity.

On the minus side, although Reeves presented this as a budget for growth, the rise in employers’ National Insurance contributions and other changes brought in by Labour seem more likely to have the opposite effect. They will discourage investment in the UK and potentially lead to job losses as well. Farmers were particularly hard hit by inheritance tax changes. These will potentially generate huge tax bills for family farms and may result in thousands having to sell up. Any farmers among my readers have my sympathy and support.

We will obviously see how things pan out over the coming months and years, but I can’t say I am particularly optimistic over the direction in which this country is heading. In particular – as regular readers will know – I have serious concerns over the effect the government’s reckless pursuit of ‘Net Zero’ will have on our energy security and standard of living. In my view, far more effort should be put into adapting to the effects of climate change, rather than wasting billions on pie-in-the-sky virtue-signalling schemes such as carbon capture machines and giant flywheels. Okay, I’ll get off my soapbox now!

As always, if you have any comments or queries about this update, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m featuring a way you can get a free share worth up to £100 by signing up with an online share trading platform called Trading 212.

Trading 212 is unusual in that it offers commission-free and fee-free share trading. As a special offer, until Wednesday 6th November 2024 they are offering people new to the platform a free share just for signing up via a referral link (such as the links in this post). The share you will get is chosen at random, but could be worth up to £100. You can either keep this share or sell it.

How to Sign Up

Signing up with Trading 212 is pretty straightforward. Just visit the Trading 212 website via any of the (referral) links in this post and follow the on-screen instructions to register. Note that you will be required to provide various items of information, including your date of birth, National Insurance number, annual income, employment status, and contact details. I understand that this is to meet their legal ‘Know Your Customer’ duty.

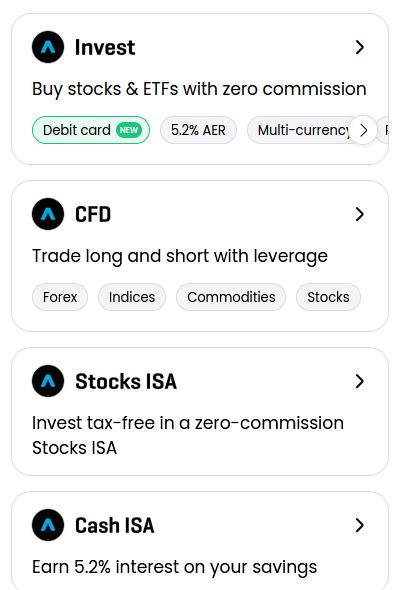

You will also need to indicate the type of account you want from the options available (see screen capture below).

As you will see, the four account types on Trading 212 are Invest, CFD, Stocks ISA and Cash ISA. You can apply for any or all of these if you like.

CFD stands for Contract for Difference. CFDs are quite complex financial instruments, and unless you know what you’re doing I recommend giving them a miss.

If you just want the free share my suggestion would be to tick the Stocks ISA box. An ISA is, of course, a tax-exempt Individual Savings Account. As from April 2024 you can open any number of ISA accounts in a year as long as you don’t exceed your annual £20,000 allowance.

If you have already used up your entire £20,000 this year, you should choose Invest instead to open a general investment account without any tax benefits. Obviously if you don’t want a Stocks ISA with Trading 212 for any reason, you can choose this option as well.

For more information about the new Trading 212 Cash ISA, see my review here. Be aware that you must open either an Invest account or a Stocks ISA account to qualify for a free share. Of course, there is nothing to stop you opening a Cash ISA account as well, but my recommendation would be to open an Invest or Stocks ISA account first.

Getting Your Free Share

There is one more step you will need to take in order to get your free share. You will need to deposit a minimum of £1 into your account. There are various ways you can do this, but i just used my debit card. There is no obligation to invest the £1 (or whatever you choose to deposit) and if you wish you can withdraw it once your free share has been credited.

The next business day you should receive an email confirming that a free share has been added to your account. As mentioned above, this is allotted at random. If you’re lucky you might get one worth up to £100. Even if you get a less valuable one, though, it’s still a share for free. If you choose to keep it, it may rise in value. There may also be dividends payable in future (and credited to your account).

Already have a Trading 212 account? You can also get a free ETF share worth up to £200 (and now guaranteed to be worth at least £10) with new DIY wealth-building app Wealthyhood. A minimum investment of £50 is required to get the free share (although if you’re not bothered about this you can start investing on the platform with as little as £20). Click through here for more info.

Selling Your Share

You can’t sell your share immediately. You have to wait three business days before doing so, but it is then just a matter of clicking the Sell button on your member’s dashboard.

The money will be credited to your Trading 212 account but you will have to wait 30 days before withdrawing it. So there may be a case for waiting to see if your share’s value goes up in that time. Of course, it could also go down!

In my case, I received a free share in the Ford Motor Company worth just under £8 at the time. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort 😀

How Safe Is Trading 212?

Trading 212 is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £85,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks and shares, which can go down as well as up. All investments carry a risk of loss, although in the case of your free share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Trading 212 member can also refer new members. In this case, both you and the person concerned will receive one free share worth up to £100. Obviously, the links in this blog post include my referral code – so if you register and get a free share, I will receive one also. Under the terms of the current offer you can get up to five free shares in this way. Five is the limit per person. Although you can still refer new members who will get a free share after this, as a referrer you won’t receive one as well.

Final Thoughts

I first heard about Trading 212 a while ago, but wasn’t initially sure whether it was legit and here for the long term. And I thought the free share offer was, frankly, too good to be true. However, my own experiences have been entirely positive. My original free share in the Ford Motor Company was credited the next business day as promised and I received an email notifying me about it.

I can log in to my Trading 212 account any time to see how my Ford share is doing. I have also collected a few other shares from referrals as well. These include a share in AMD (the semiconductor company), which is currently worth £117.92, and one in Nike, which is worth £105.83. I still have my original Ford Motor Company share and it has risen in value to £8.16. I also received an annual dividend payment from them a while ago. I haven’t sold any of my free shares yet but could of course do so any time I choose. I am not in any rush, as Trading 212 do not impose any platform or inactivity fees.

Although in this post I have focused on the free share offer, Trading 212 is worth considering as a share-dealing platform too. In particular, the fact that it’s fee-free and commission-free means it is well suited for people who are dipping a toe in stocks and shares investment for the first time. By contrast, the dealing fees and commissions charged by some other share-trading platforms can make small share purchases prohibitively expensive. This review by Money Savvy Daddy looks at the pros and cons of Trading 212 as a share-dealing platform in a bit more detail.

It’s also worth bearing in mind that Trading 212 pays interest on any uninvested funds in your ISA or Invest account, currently at a rate of 5.1% AER. You can also make money allowing your shares to be lent out. Rates on offer for this vary according to investor demand, with the process handled automatically by Trading 212 once authorized. You can read more about share lending on Trading 212, including the risks and safeguards provided, here.

In conclusion, I hope this post has inspired you to consider registering with Trading 212 to claim your free share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And, as always, any other comments or questions are very welcome too.

Don’t forget, the current free share offer ends on Wednesday 6 November 2024.

Disclosure: The links in this post include my referral code. If you click through and register as described above, I will receive a free share (as will you). Please note also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss (although not in the case of free shares, obviously).

This is an update of my original post about this special offer.

If you enjoyed this post, please link to it on your own blog or social media:

For the sake of completeness, though, I thought I should publish (or more accurately republish) a post about matched betting. This is something I did for several years and earned about £3,000 (tax-free!) from. I am not doing it as much these days, for reasons I’ll explain below. But if you’ve never done it before, I do still recommend matched betting as a way of making some quick tax-free cash.

So Why Am I Doing Less?

There are two main reasons. The first is that since I started matched betting around six years ago I have had my account restricted (or gubbed, as we say in the business) by many online bookmakers. That obviously makes it harder to take advantage of the offers matched bettors need in order to generate their guaranteed profits.

My second reason is that during the pandemic, with many sporting events cancelled, there were far fewer matched betting opportunities. Thankfully that is behind us now and normal life (more or less) has resumed. Even so, the bookies are more cautious than they once were, and offers are somewhat thinner on the ground.

I still do a small amount of matched betting but keep it very low-key. There are only a few good online bookmakers I can now use, and I’d like to go on flying under their radar for as long as possible before they ban me!

If you are new to matched betting – or have let it fall by the wayside – then as stated above I do still recommend it. But be aware that it may not be quite as profitable as it was pre-Covid.

But let’s start with a recap of the basics…

What is Matched Betting?

Matched betting is a method for making risk-free profits by taking advantage of offers made by online bookmakers.

The best offers are those made to attract new clients. Here’s an example. The bookmakers Sky Bet offer £30 in free bets (3 x £10) for new online customers. To get this, you have to open an account with them and deposit a minimum of £5. You then have to place a minimum 5p bet at odds of evens (2.0) or better. Once you have done this, Sky Bet will immediately credit you with £30 worth of free bets.

So how do you turn this into a guaranteed profit? Well, that’s the clever bit. You make use of a website called an exchange (Smarkets and Betfair are two of the better known). These sites allow anyone to lay a bet (i.e. bet that the outcome in question won’t happen). By backing with a bookmaker and laying the same bet at an exchange you can ensure that however the event pans out, you will only make a small loss or occasionally a tiny profit (depending on the odds available).

With a normal bet this is obviously of limited value, as the two bets more or less cancel each other out. But when your first bet qualifies you for a second (and in Sky Bet’s case much larger) free bet, it suddenly becomes a lot more interesting. Here’s an example…

Let’s say Wolverhampton Wanderers are about to play Spurs in the Premier League. You can back Wolves to win with Sky Bet at 4.75 (15/4 in the more traditional but less useful fractional style) and lay them with Smarkets at 4.80. If you put £5 on Wolves with Sky Bet and at the same time lay Wolves to the appropriate stakes (something I’ll come to shortly) you can ensure that whether they do or don’t win, your net loss will be just 13p (allowing for Smarkets’ standard 2% commission charge). The lay bet covers you for the draw as well, as in effect you are betting that Wolves won’t win – so if Spurs win or the match ends in a draw, the lay bet will pay out.

But now, because you are a new member, Sky Bet will give you £30 worth of free bets. You can back and lay these again to generate a guaranteed profit. For the sake of simplicity let’s say you use the same market, Wolves v. Spurs, although you certainly don’t have to. At the odds mentioned, and backing to the correct stakes, if you use all three £10 free bets you can guarantee yourself a net profit of £23.05 however the match pans out. Subtract the 13p loss from your qualifying bet, and once the dust has settled you will have made a risk-free (and tax-free) £22.92. If your bet loses with the bookie, your profit will be in the exchange (remember, this is a free bet so it hasn’t cost you anything). If the bet wins at the bookie, you will lose money at the exchange, but your winnings with the bookie will exceed this, giving you the same net profit either way.

Those are the bare bones of matched betting. Of course, there’s more to it than that, but most matched betting opportunities boil down to this. You place an initial qualifying bet and lay it to ensure (at worst) a small net loss, and then back and lay the free bet you receive to make yourself a guaranteed profit.

One or two people have asked me whether matched betting is legal. The answer is a clear yes. It’s fair to say the bookies don’t like it, though. And if they suspect you are doing it, they may close or limit your account. As mentioned above, this is called ‘gubbing’ and it is an occupational hazard for matched bettors. As a matter of interest, I had to change the example used at the start of an earlier version of this blog post after being threatened with legal action by the bookmaker in question.

How Do You Get Started?

You can, of course, do all this yourself, researching opportunities and comparing odds to find the most profitable matched betting opportunities. When you are starting out, though – and especially if you are new to online betting – it obviously helps a lot to get some instruction and guidance.

Fortunately there are some excellent online services that will do all this for you and provide step-by-step instructions. You can apply these even if you have never placed a bet in your life before. Here’s the service I recommend for beginners to matched betting…

Outplayed

Outplayed (formerly Profit Accumulator) is a dedicated matched betting website. You can get a 7-day free trial which gives you access to over 60 welcome offers of the type mentioned above. If you wish to continue, you can then pay a fee (currently £39.95 a month) to become a ‘Platinum’ member and get access to Outplayed’s full range of betting offers and services.

As well as detailed instructions on offers, Outplayed also provide various online tools you can use. Their oddsmatcher, for example, helps you find markets where the back and lay odds are as close as possible, so you can minimize your losses on qualifying bets and maximize the value of your free bets. They also have calculators where you enter the back and lay odds and how much you want to bet at the bookmaker. The calculator then reveals how much you need to lay at the exchange to guarantee a set profit (or qualifying loss) with either outcome.

A further advantage of joining Outplayed is that you get access to the members-only community forum, where you can get any questions you may have answered by more experienced members and/or the Outplayed team.

For more information about Outplayed and its different membership levels, just click through this link [affiliate].

If you are at all sceptical about the Outplayed service, you might like to check out the reviews on the independent Trust Pilot website. They currently average 4.7 out of 5 stars, with 89% of respondents awarding them a five star (‘Excellent’) rating. That is among the highest average ratings I can recall seeing on Trust Pilot.

What Happens When You’ve Exhausted the Welcome Offers?

This was something I wondered about before I started, and I know other people do as well.

First of all, it will take you quite a long time to work through all the offers on the Outplayed website. Not all are as simple and straightforward as the Sky Bet offer mentioned above, but nonetheless if you follow the step-by-step instructions they can all generate a healthy profit for you.

After that, you can move on to ‘reload’ offers. These are offers made by bookmakers for existing members to encourage them to keep coming back and using their service. Reload offers work in a wide range of ways. Some provide a guaranteed profit if you apply them correctly, while others may sometimes make a small qualifying loss but other times produce a much larger profit, generating a good net profit overall. Reload offers are also listed on the Outplayed website and updated every day.

Is Matched Betting for Everyone?

In principle anyone can do matched betting, but it is probably more suitable for some people than others. In particular, it will help if you have a small amount of capital to get started – at least £50, preferably £100 or more.

If you have less you can still do it, but it will take longer to build up your earnings. Remember that you will need money to fund your qualifying bets at the bookmaker sites and also your exchange account. You don’t lose this money – it simply moves between bookie and exchange according to how events pan out – and you can always withdraw it if required. But to operate as a matched bettor you do need to have some ‘working capital’.

Another requirement to make a success of matched betting is that you need to be organized and methodical. Matched betting is not difficult once you grasp the basic concept, but if you make a mistake it is possible to lose money doing it. Initially at least it’s important to take it slowly and steadily and follow the instructions on Outplayed (if you have signed up with them) to the letter. It helps to be reasonably numerate as well, although the actual calculations are done for you by the oddsmatching tool and calculators.

And finally, if you think you might get drawn in to gambling through matched betting, you may be better giving it a miss. This applies especially if you have ever had a gambling problem in the past. To emphasize again, matched betting is NOT gambling if you do it properly and follow the correct procedures. But if you are tempted to go off-piste and start placing random bets, the likelihood is that you WILL lose money overall.

Final Thoughts

If you are looking for a tax-free sideline earning opportunity, matched betting can certainly fit the bill. Done properly it is risk free, and (as mentioned earlier) I have made around £3,000 from it myself.

For reasons discussed in this blog post I don’t recommend matched betting as a substitute for a full-time job. In these challenging times, however, if you need another tax-free string to your money-making bow, it can certainly perform that role. But be aware that the first few months are likely to be the most profitable. After that, as you run out of welcome offers (and are perhaps ‘gubbed’ by some bookies) it will get harder.

As always, if you have any comments or questions about this post or matched betting more generally, please do leave them below.

This is a fully updated version of an earlier post.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

In a recent post I talked about tax-free ways to boost your finances. It occurs to me that I omitted an important one, however – entering prize draws and competitions. In the UK anyway, cash and prizes acquired this way are normally tax-free.

In recent years the internet has opened up a host of opportunities for entering (and winning) competitions from home. Whether you’re a seasoned ‘comper’ or a newbie eager to try your luck, I hope you will find the tips, resources and advice in this post useful…

1. Finding the Right Competitions

The first step towards winning is finding the competitions themselves. Here are some ways to discover them:

Social Media: Follow brands, influencers (e.g. Superlucky Di) and competition-focused groups on Facebook, Twitter/X and Instagram. Search for relevant hashtags, e.g. #competition #prize #giveaway. Many businesses also run exclusive competitions for their social media followers.

Email Newsletters: Subscribe to newsletters from your favourite brands and competition websites to receive alerts about the latest contests.

2. Setting up Dedicated Comping Accounts

It’s best to set up dedicated email and social media accounts for your comping. Inevitably you will receive growing volumes of promotional material and even (regrettably) spam. Using separate, dedicated accounts will ensure your personal accounts don’t get cluttered up.

Check Email Regularly: To save time, you can search for relevant words and phrases like Congratulations, Winner and Runner-up.

Set up Accounts on Facebook, Instagram and Twitter/X just for Comping: Some competitions require you to ‘like’ or follow a particular brand on social media in order to enter.

Don’t Sign Up for Further Info: Avoid ticking the box to receive more information when entering a competition, unless you are really sure you want this. Doing so can result in your inbox swiftly being overrun.

3. Understanding the Rules

Each competition has its own set of rules and regulations. Carefully read the terms and conditions to understand:

Eligibility: Ensure you meet the requirements (e.g. age, location).

Entry Limits: Some competitions allow multiple entries, while others are strictly one per person.

Closing Dates: Note the end date to ensure you don’t miss out.

4. Crafting Winning Entries

Certain types of competition require more than just luck. Here’s how to stand out:

Skill-based Competitions: These might ask for a slogan, recipe, or photo. Be creative and original. Research past winners to understand what judges are looking for.

Tie-breakers: If there’s a question to answer, put some thought into it. A unique and clever response can be your ticket to winning.

5. Maximising Your Entries

To increase your chances, enter as many competitions as possible. Here’s how:

Set a Schedule: Dedicate time each day or week to entering competitions.

Use Autofill Tools: Tools like RoboForm can save time by automatically filling out your details for you.

Keep Track: Maintain a list or (preferably) spreadsheet of entered competitions to avoid duplicates and track deadlines.

6. Avoiding Scams

While many competitions are legitimate, some are not. Protect yourself by:

Verifying the Source: Only enter competitions from reputable websites or brands.

Not Paying Fees: Genuine competitions won’t ask you to pay to enter.

Checking Reviews: Look up the competition and the company running it to ensure they have a good reputation.

7. Networking with Fellow Compers

Join online communities and forums such as MoneySavingExpert or dedicated Facebook groups (such as this one) where members share tips, winning stories and new competition finds. Networking with other compers can provide valuable insights and motivation.

8. Celebrating Wins, Big and Small

Not every prize will be a jackpot, but every win counts. Celebrate all victories, whether it’s a small voucher or a large cash prize. Sharing your wins on social media or competition forums can also encourage others and attract positive attention.

9. Staying Persistent

Winning competitions requires patience and perseverance. Don’t get discouraged if you don’t win straight away. Keep entering regularly, and your persistence will eventually pay off.

Closing Thoughts

Winning cash and prizes through online competitions is a fun and potentially rewarding hobby. By keeping organised, being creative, and staying wary of scams, you can significantly boost your chances of success. So get out there, start entering, and who knows? You might just land that dream holiday or big tax-free cash prize sooner than you think 😎🍾🏖

Happy comping, and may the odds be ever in your favour!

If you enjoyed this post, please link to it on your own blog or social media:

Although the rate of inflation has fallen in recent months, for many the cost of living crisis continues to bite.

So today I thought I would set out some ways you may be able to make a few pounds extra to boost your finances. None of these is likely to make you a fortune, but together they can certainly help keep your bank balance ticking over.

I have linked to relevant posts on Pounds and Sense for further information where appropriate. I have direct experience of all the methods set out below and therefore know that they work and are not scams.

1. Prolific Academic

Prolific Academic is a platform used by academic researchers world-wide to recruit participants for online studies/surveys. These are varied and often surprisingly interesting. They require anything from two minutes to an hour to complete, with payments based on how long (on average) they take. I’ve earned over £600 to date from Prolific. For more information, see my blog post Make Money and Help Academic Researchers With Prolific Academic.

2. MobileXpression

If you have a smartphone, this is an easy way to make money from it. Just install this app (which tracks your browsing anonymously) and every few weeks you will receive a £20 Amazon voucher for your trouble (Amazon vouchers are pretty much as good as money, as you can of course buy almost anything there). You can read my full review of the MobileXpression app in this post.

3. Shop and Scan

Shop and Scan is a market research programme run by Kantar Worldpanel. Anyone can apply to become a panelist, and when you are accepted (which may be immediate or after a few weeks) you receive a barcode scanner and guidebook in the post. You are then required to scan all your shopping when you bring it home (or it’s delivered) and scan and submit your receipts. For doing this you get points. When you have enough, these can be converted into vouchers for a wide range of online stores (again, I normally pick Amazon). You can earn extra points by performing other tasks such as completing online questionnaires, so it doesn’t take long to earn enough points for a £10 voucher. For more information, see my blog post Make Money From Your Shopping With ShopandScan.

4. The Viewers

The Viewers is another market research company always looking for new members for its (paid) audience panel. As the name suggests, they research people’s TV viewing habits via surveys and focus groups. They pay participants in cash (via PayPal) or Amazon vouchers. They run ‘real world’ focus groups in large cities, and online studies of various types. For more information, see my blog post Make Money Watching TV With The Viewers.

5. People for Research

This is another opportunity to make money taking part in consumer research. People for Research are constantly recruiting people to take part in studies. Some of these take place in large cities (London and Bristol especially) but many are done remotely via the phone or the internet. The studies cover a huge range of topics and are for the most part interesting and enjoyable. But the best thing is that they are fairly (and sometimes generously) recompensed – usually in cash, though sometimes Amazon vouchers. For more information, see my blog post Earn a Sideline Income with People for Research.

6. Y Live

Y Live (previously called Populus Live) is a survey website that wants your opinions and pays cash for them. You can sign up free of charge and will then receive email notifications any time they have a survey you may be eligible for. Each survey is worth a set number of points. Once you have accrued 50 points you will be paid £50 (each point is worth £1, in other words). Admittedly it can take a little while to reach the payment threshold, but £50 is undoubtedly a useful sum when you receive it. For more information, see my blog post Make Extra Money From Y Live.

7. Selling on eBay

One great way to generate quick extra cash is to have a clear-out of things you no longer need and put them up for sale on eBay. All sorts of things sell here, and if you have never tried selling via the site you will be pleasantly surprised by how easy it is. What’s more, as long as you are selling your own possessions (and not buying stuff to resell) it’s tax-free too. For more tips about this, see Twelve Top Tips for Selling on eBay, a guest post on PAS by my money blogging colleague Luci Olivia.

8. Matched Betting

In the last year or two matched betting has undoubtedly become harder, partly due to the pandemic and partly to bookmakers becoming less generous with their offers. If you haven’t yet tried matched betting, though, there is still money to be made.

For those who don’t know, matched betting involves taking advantage of online bookmaker offers (especially welcome offers) to generate a guaranteed profit. It is emphatically not the same as gambling (which I don’t recommend at all). As per my blog post Can You Make Money from Matched Betting? if you are new to this field I recommend starting with the matched betting support and advisory service Outplayed [referral link] previously called Profit Accumulator. You can earn up to £45 (tax free) by taking advantage of the offers available to free members. You could then leave it at that or sign up as a full member with unlimited profit potential.

9. Free Share Offers

Various online share trading platforms offer free shares to anyone opening an account with them. One of my favourites is Trading 212, which periodically offers anyone who signs up and deposits a minimum of £1 a free share. This is chosen at random but could be worth up to £100. You can sell this after three days if you wish and withdraw the proceeds (including your initial deposit) after 30 days. For more information on Trading 212, including how to get your free share when the offer is open, see my blog post Get a Free Share Worth Up to £100 With Trading 212. Another service offering free shares is the online wealth-building platform Wealthyhood. Learn here how you can get a free ETF share worth up to £200 by signing up with Wealthyhood.

10. Selling Your Old Tech

Most of us have old gadgets we no longer use that are just gathering dust. They include mobile phones, tablets, laptops, cameras, games consoles, and even desktop computers. They may still work, but we have replaced them with new and (hopefully) better products. If that sounds like you, there are lots of ways you can make money from your old tech, even if (in many cases) it doesn’t work any more. Check out my blog post How to Make Money From Your Old Tech for a range of methods for doing this.

11. Freelance Writing

This is a subject close to my heart, as for many years I was a full-time freelance writer (I’m semi-retired now). It’s a competitive field, but there is still lots of money to be made. You don’t need to be Shakespeare either, just have a reasonable grasp of written English and be willing and able to write what the market wants. Check out my blog post My Top Ten Tips for Making Money as a Freelance Writer here. You can also read my posts Should You Write a Book? and How to Publish Your Own E-book on Kindle.

12. Cashback Websites

I’ve mentioned cashback sites a few times on PAS. These are sites such as Top Cashback and Quidco, where any time you make a purchase with a certain online store, if you go via the cashback site, you get some money refunded to your account. Obviously you aren’t actually making money in this case – but if you were going to make the purchase anyway you get some money back, and over time this can add up to a tidy sum. In addition, there are some offers listed on the sites where you can get ‘cashback’ without actually making a purchase. For more information, see my blog posts Save Money With Cashback Sites and Six Ways to Make Money With Cashback Sites.

13. Comping

Okay, comping, or entering consumer competitions, isn’t a guaranteed way of making a sideline income. Nonetheless, there are stacks of cash and prizes on offer at any time, and somebody has to win them. There’s no reason it couldn’t be you! There are lots that you can enter online – just check out competition listing website Loquax, for example. For hints and tips on getting started, see How to Win Cash and Prizes in Consumer Competitions, a guest post on PAS by Cora Harrison. I also highly recommend the book Superlucky Secrets by my UK blogging colleague Di Coke (also known as Superlucky Di). You can read my review of this in-depth guide to comping here.

14. Free Online Lotteries

This is obviously another opportunity where returns are not guaranteed. Nonetheless, there are various online lotteries you can enter free with a chance of winning (in most cases) cash prizes. Typically you have to return to the lottery site every day to see if you are a winner. My favourite such site is Pick My Postcode [referral link]. This site offers multiple chances to win every day, with prizes ranging from £10 to over £1,000. I have a particular soft spot for PMP, as back in the days when it was called Free Postcode Lottery, I was lucky enough to win £614.53 on it. You can learn more in my blog post titled How to Cash in on Free Lottery Websites.

15. Website Testing

If you enjoy trying new apps and websites and putting them through their paces, there are various sites that will pay you for doing this and reporting back. One such site site with a strong community angle is Crowdville. For more information about this, see my blog post Make Money Testing Apps and Websites with Crowdville. Other sites you might like to check out include Testing Time and Respondent.

16. Blogging

I make money this way, and there’s no reason you couldn’t as well. Blogging is by no means a get-rich-quick opportunity. But if you are prepared to put some time and effort in, the rewards will come. You can blog about any subject you like (though some subjects are easier to make money from than others). Once your blog is up and running you can earn from it in various ways, including advertising, affiliate marketing, sponsored posts, and so on. To get an idea how this works, check out this guest post by Ruth Hinds titled Five Things You Really Need to Know About How to Make Money from Blogging.

17. Online Design and Print

This is a great home-based sideline earning opportunity. No special skills are needed beyond a little imagination; although if you do have art and design skills, so much the better. I’m talking here about designing and selling clothes and other products, from tee-shirts to tote bags, hoodies to coffee mugs. By designing I mean coming up with slogans and/or graphics to adorn these products that will appeal to a particular target market. This opportunity has been opened up by web-based companies such as TeeMill that allow you to design and sell your products online. They provide all the back-end services, including taking payments and fulfilling orders. They charge you a set fee for this, which is covered from the fee paid by your customer. You charge your customers a bit more, and your profit is (of course) the difference between the two. For more information, see my blog post How to Make Money with Online Design and Print.

18. Virtual Assistant Work

There is a steady demand for virtual assistants who can perform a wide variety of tasks from home via the internet. The sorts of things VAs do may include research, writing, proofreading and editing, graphic design, publicity, data entry, programming and other technical tasks, and much more. Social media management is another very popular area. You can read my in-depth blog post on how to make money as a virtual assistant here.

19. Fiverr.com

As you may know, Fiverr is US-based site that lets anyone advertise ‘gigs’ they are willing to perform for five dollars (hence the name, of course). Gigs range from the serious (e.g. write a press release) to the creative (e.g. write a customized solo piano track) to the downright quirky (e.g. write a message, name or URL in chocolate). Most gigs are services delivered electronically, though there is nothing to stop you selling physical products if you wish (you can charge extra for postage). Obviously $5 isn’t a lot, but if you can perform your gig in just a few minutes it can still work out as a decent hourly rate. It’s also possible to charge additional amounts for ‘extras’ such as rapid delivery or upgraded features. See my blog post How to Make Money on Fiverr for much more information about this.

20. Investing for Income

This is obviously a different angle from the preceding ideas. If you have money in the bank earning a derisory rate of interest (or nothing at all), however, you might like to consider investing some to provide an additional income stream for you.

This is obviously a huge subject and I can’t go into detail about it here. There are lots of possibilities, though. One would be to invest some of your money in dividend-paying shares. This subject was covered in an excellent guest post for my blog by Lewys Lew titled How to invest For Income From High Yield Share Dividends.

Of course, you should research any possible investment carefully and be prepared to lose money in the short term at least (see below). Note also that some companies – e.g. the big banks and oil companies – cut their dividends during the Covid crisis, so it’s important to pick your sectors carefully.

Regular readers will know I am also a big fan of the robo-adviser investment platform Nutmeg. They are primarily aimed at helping people build a savings (or pensions) pot rather than providing an income, but you can of course withdraw money from your account as and when you wish. You can read my full review of Nutmeg here. You can also get six months free of any management charges when you invest in Nutmeg via my referral link.

Of course, all investment carries a risk of loss, so you should always do your own ‘due diligence’ and take professional advice if in any doubt before deciding to invest. You should also ensure you have enough cash and/or easily accessible savings to get you through a period of three to six months in case of emergencies.

As always, if you have any comments or questions about this post, please do leave them below. And keep reading Pounds and Sense for more money-saving and money-making ideas in the weeks and months ahead.

Disclosure: Some of the links in this post (and elsewhere on PAS) include my referral links. That means if you click through and make a purchase (or perform some other defined action) I may receive a commission for introducing you. This will not affect the price you pay or the products/services you are offered.

This is an update of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a survey website that wants your opinions and pays cash for them 🙂

The site in question is Y Live. It was previously called Populus Live. You can sign up free of charge, and will then receive email notifications any time they have a survey you may be eligible for.

Each survey is worth a set number of ‘points’. Once you have accrued 50 points you will be sent a cheque for £50 (each point is worth £1, in other words).

The notification emails state how long the survey is expected to take and how many points it is worth. In general, you get 1 point for a five-minute survey, 2 points for a ten-minute one, and so on.

Bear in mind, though, that the timings are Y Live’s estimates, and may not correspond with how long they actually take to complete. For example, I find that ‘five-minute’ surveys can sometimes take ten minutes or longer. Of course, that does reduce the effective hourly rate you receive.

On the other hand, the surveys are generally straightforward and easy to do (though watch out for the attention-checkers). It’s quite possible you will be quicker to complete them than I am.

On occasion you may find yourself screened out of a survey, e.g. if you are not in the target group they are interested in. In that case you won’t be awarded any points, but will get one entry in their monthly prize draw for £250.

Clearly nobody is going to earn a fortune from Y Live, but in my view (and experience) it can make a very worthwhile addition to your sideline-earning portfolio.

As always, if you have any comments or questions about Y Live, please do post them below.

Note: This is an update of an earlier post.

If you enjoyed this post, please link to it on your own blog or social media:

As you may have heard, from January 1, 2025, digital platforms like eBay, Etsy and Airbnb will be required to collect additional information from sellers, including number of sales and amount of income generated.

This data will be automatically shared with HM Revenue & Customs (HMRC) by January 31, 2025, covering the 2024 calendar year. HMRC will then compare this against their records to see if any tax may be due.

This news has caused some consternation on messageboards and social media, with many who have ‘side hustles’ to help pay the bills worried they may be hit by an unexpected tax demand. Some of this concern may be justified, but (thankfully) much of it isn’t.

So today I thought I’d explain what’s actually happening and how you can minimize your tax liability from side hustles and reduce the risk of unwanted attention from the taxman (while staying within the law, of course).

So What’s Happening?

Digital platforms will automatically share seller information with HMRC if a seller has made 30 or more sales a year or earned over €2,000 (approximately £1,700).

The reporting threshold is set in Euro as this is a multi-national initiative by the Organisation for Economic Co-operation and Development (OECD) which aims to tackle tax evasion globally. The new rules apply to various digital platforms, defined as any app, website or software connecting sellers to consumers of goods and services.

It’s important to understand that this is a reporting change and not a change in tax law. If you didn’t have to declare certain earnings or pay tax on them before, that remains the case now. In particular, if you are selling personal possessions you no longer want/need – as opposed to items you bought with a view to selling them for profit – that wouldn’t normally count as trading and no tax would be due.

The other important exemption is that everyone in the UK has an annual trading allowance of £1,000. This means you are allowed to make up to £1,000 (gross) per year from self-employed work including side hustles. If your total annual income by this means is below £1,000, there is no need to declare it to HMRC or pay tax on it (even if you have a separate day job). Note, however, that in the case of online auction trading, that £1,000 is income before any platform fees and other selling costs are deducted.

If your taxable earnings from a side hustle are over £1,000 a year, you will need to notify HMRC via a self-assessment tax return. You will then be required to pay income tax on this, unless your total taxable earnings from all sources are below the personal tax-free allowance (currently £12,570).

Top Tips

As promised, here are some tips to help you negotiate the rules surrounding side hustles, minimize any potential tax liability, and reduce the chances of attracting unwanted attention from HMRC, all while staying within the law.

Keep careful records of all your business activities. That includes activities that you don’t believe count as trading, e.g. selling your unwanted possessions. You may need this info if you are challenged by HMRC.

In particular, keep a running record of total sales and number of transactions on platforms such as eBay. If you’re having a clear-out, it won’t be hard to exceed the 30-item or €2,000 limit that will trigger a report to HMRC. As mentioned above, if you’re just selling your old stuff, there shouldn’t be any tax liability. But you might understandably prefer to avoid having to field queries from HMRC about your selling activities.

It might therefore be a good idea to use a variety of platforms for selling your stuff rather than just one. So instead of just eBay, use other similar sites such as Facebook Marketplace, Gumtree, Vinted, Craigslist, Ziffit, eBid, and so on. Aim to keep your total sales on any one platform to under 30 and under €2,000 in total.

If you are selling items you have made yourself (e.g. clothing or jewellery) on websites like Etsy, be aware that this will also usually count as trading and any profits may be taxable. Again you can claim the £1,000 trading allowance, though.

If you think what you are doing counts as trading, monitor when your gross annual income (or turnover if you prefer) is approaching £1,000. At this point you might prefer to ‘shut up shop’ until the following year. Otherwise you will need to declare your earnings to the taxman and (if required) pay tax on them.

Be aware that cashback earned through websites such as Quidco and Top Cashback is not taxable. Neither is the cashback paid with certain bank accounts.

Note also that lottery and competition prizes are not generally taxable in the UK. Neither are gambling wins (not that I recommend this) or any profits made through matched betting.

I hope this article will have clarified the situation for you if you’re pursuing a side hustle or considering doing so. As I said earlier, the tax rules haven’t changed, but with the new reporting regime it’s more important than ever to understand what the tax and trading rules are and ensure you stay within them.

If you have any comments or queries, as always, feel free to leave them below. Please note that I am not a tax professional, however, and cannot answer detailed questions about your personal financial circumstances. As I said in this blog post a while ago, if you need advice with tax matters, in my view a qualified accountant should always be your first port of call.

If you enjoyed this post, please link to it on your own blog or social media:

If you would like to know more about low-cost self-publishing via Amazon, the e-book Kindle Direct Publishing for Absolute Beginners (pictured, left) offers a good introduction. If you don’t currently read on Kindle, download the free Kindle app to your laptop, tablet or smartphone.

If you would like to know more about low-cost self-publishing via Amazon, the e-book Kindle Direct Publishing for Absolute Beginners (pictured, left) offers a good introduction. If you don’t currently read on Kindle, download the free Kindle app to your laptop, tablet or smartphone. Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher Choc Lit (part of Joffe Books). She has also had a novel published in partnership with The Book Guild and has self-published several books via Amazon KDP. When not at the keyboard, she feeds her addiction to words by working part-time in her local library and running two reading groups. Sally can also be found walking, church-bell ringing and enjoying shavasana in her yoga class. Follow her writing blog at https://sally-jenkins.com/.

Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher Choc Lit (part of Joffe Books). She has also had a novel published in partnership with The Book Guild and has self-published several books via Amazon KDP. When not at the keyboard, she feeds her addiction to words by working part-time in her local library and running two reading groups. Sally can also be found walking, church-bell ringing and enjoying shavasana in her yoga class. Follow her writing blog at https://sally-jenkins.com/.