As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2023, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on X/Twitter and Facebook). I’ll therefore close by wishing you a Very Merry Christmas (strikes and cost-of-living crisis permitting) and for all of us a brighter, more prosperous new year 🍾

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

For the second winter in a row, some energy companies are offering incentives to customers to reduce their electricity use during periods of peak demand. Payments are made to those who succeed in doing this.

Most large energy companies – and some smaller ones – are running schemes, though some by invitation only. At the time of writing they include British Gas, EDF, Octopus Energy, E-on, OvoEnergy, Shell Energy, Scottish Power and Utilita. You can see a regularly updated list on this page of the Moneysavingexpert website.

If you aren’t with one of these companies, however, you may still be able to benefit by signing up with an app-based service such as Loop Energy or Power Rewards.

Don’t, though, be tempted to sign up for more than one scheme at a time. That is against National Grid’s rules and could see you being banned from receiving ANY payments.

This programme is part of a broader initiative from the National Grid Electricity System Operator (ESO), the organization responsible for transporting electricity around England, Scotland and Wales and keeping homes and businesses powered. The aim is to balance supply and demand, thus reducing the need to fire-up fossil-fuel plants and (in the worst case) avoiding power cuts.

During cost-cutting events, National Grid ESO pays participating suppliers a certain amount for each unit (kWh) of electricity saved by any of their users signed up to schemes. Suppliers then pass some or all of this payment on to customers.

One thing all schemes have in common is you must have a smart meter capable of sending half-hourly readings. Smart meters are of course somewhat controversial, and for various reasons not everybody wants one. If you wish to benefit from this particular opportunity, however, having a smart meter is essential. For the record I do have a smart meter and believe it has saved me money. But I do of course respect those who have differing views about this.

How It Works

To make money from these schemes you will be asked to reduce your electricity (not gas) consumption during certain periods. This is most commonly around the evening peak time of 4 pm to 7 pm, but exact times vary depending on the supplier concerned and the needs of National Grid.

The duration of events varies but in my experience is typically an hour or 90 minutes. But I understand they could be anywhere between 30 minutes and three hours.

You are unlikely to make a fortune from these schemes, but could earn up to £100 (or more) over the course of the winter. Payments vary from around £2.50 to £4.50 per unit (kWh) saved, the rate depending on what National Grid is paying. The actual rate you receive will also depend on how much of the payments from National Grid your supplier chooses to pass on.

One other important point is that you may be expected to reduce your usage by a certain minimum amount (e.g. 40%) from your average in order to receive a payment. If you cut your usage by less than this, unfortunately you may not qualify for any payment on that occasion.

You will be required to opt in to the scheme run by your energy supplier (or other provider). You will likely also have to opt in to specific energy-saving events, with advance notifications sent via email and mobile phones.

How to Maximize Your Returns

Here are a few tips and ideas for cutting your electricity use during power-saving events and maximizing the returns you receive…

Turn off as many lights as possible, including outside lights (easily forgotten).

Turn off all mains-powered computers, printers and other electronic devices (again, easily forgotten).

Avoid cooking with electricity during events.

Avoid using other high-energy-consumption devices such as dishwashers and washing machines.

Obviously, avoid using electric heating if possible. If there’s no alternative, heat up the room/s you will be in beforehand and close all doors, windows and curtains to keep the warmth in.

Avoid taking electric showers while events are in progress.

Be sure no electrical devices have been left on to charge.

Switch off the TV and watch instead on your laptop/tablet using its internal battery.

Avoid boiling the kettle as this uses a lot of electricity (albeit for a short period). Make a flask of coffee/tea beforehand and drink from that during the event.

Avoid opening fridge/freezer doors during events. But you can also switch off fridges and freezers entirely to save more. This should be perfectly safe for up to three hours.

If it’s feasible, arrange to go out during some or all of the power-saving event. This is the easiest way to save as much electricity as possible!

Create a checklist of things to do at each event to save power. You can also use this after the event to ensure you remember to turn things like fridges and freezers back on again.

One other slightly left-field idea is to use high-energy devices such as washing machines and electric cookers MORE during evening peak times when there isn’t a power-saving event happening. That will boost your average energy consumption at this time, giving you the opportunity to save more when a power-saving event comes along. Obviously you shouldn’t use high-energy devices more than you would overall. But if you can shift your usage to peak times when power-saving events are typically scheduled, this should help you save more when events occur.

I hope this post has given you some ideas for how to maximize your returns from these schemes. As always, if you have any comments or questions, please do leave them below. I’d also be very pleased to receive any other tips for making more money from power-saving events.

Don’t forget, you can also get a FREE £50 credited to your energy account when you switch to EDF Energy via my affiliate link. Terms and conditions apply.

This is a fully updated version of my original 2022 post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

Public speaking can be a good paying sideline for retired and semi-retired people. As well as the financial benefits, it can offer an enjoyable opportunity to talk about your hobbies and interests, or your current or former career. I’ve also known people who have done public speaking as a method of raising money for charities or other causes close to their heart. Although the pandemic and lockdowns temporarily put paid to most public speaking work, as life has returned to normal the opportunities are definitely out there again.

Over to Sally then…

Wouldn’t it be great to make extra money by following your passion? A hobby that pays makes ‘working’ a pleasure. Unfortunately, things like stamp-collecting, rambling and local history rarely turn a profit, but there is a way to make them pay: share your specialist knowledge with others.

Community organisations such as the WI, Probus and independent Leisure and Learning clubs struggle to find speakers for their meetings. I speak about novel-writing at many such groups and am always asked if I know of any other speakers open for bookings. These are paid gigs. How much you charge, how far you travel and what type of bookings you take are all up to you. Depending on the policy of the organisation, these events may also give you the opportunity to sell produce from your hobby. For example, I sell copies of my books, but a creator of conserves might sell jam and marmalade or an artist, his paintings.

Below are some tips for starting a speaking career:

Collate enough material for a 45-minute talk and sort it into a logical sequence. Include stories that will capture the listener rather than a lot of heavy facts.

Refine the material into minimal bullet-pointed notes. It’s important to talk freely around each bullet point rather than read from a manuscript. Reading makes eye contact with the audience difficult and hand gestures to illustrate your words are almost impossible.

Think about any visual aids; these add variety and colour to a talk. When I talk about thriller-writing I produce some ‘murder weapons’ – a rolling-pin, a (blunt) knife and a packet of tablets. The conserve creator might show her jam pan and specialist thermometer. The artist might have a range of brushes to discuss.

Practise! Producing a successful talk is like an iceberg. At least 90% of the work is in the preparation beforehand. However, once you’ve perfected your performance, you can give that same talk many times to different groups.

Don’t be surprised if you are handed a microphone to use. This often happens in large halls or where several audience members are hard of hearing. Hold it at a consistent distance from your mouth and don’t turn your face away from it. Practise at home by holding a wooden spoon – this will give you an idea of what it’s like to talk with only one free hand.

Enquire at your local church hall about community groups who meet there and use speakers.

Do a couple of small bookings for free and ask for feedback from the audience. Once you’re confident, don’t make a habit of speaking for free (unless it’s a charitable cause) because that makes it harder for other speakers to ask for a fee.

Receiving a cheque at the end of a talk is good but public speaking brings other benefits, such as the opportunity to meet new people and share your knowledge. It will improve your everyday confidence as well. When you can speak in front of an audience, complaining in a shop or restaurant is less daunting, putting your point of a view in a meeting is easier and making small talk with strangers at a party is no problem.

Many thanks to Sally Jenkins (pictured) for an interesting and inspiring article. Although as I said to her, I hope she never gets stopped by the police on the way to one of her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!

I have done a bit of speaking myself, both for work reasons (in the long-ago days when I had a proper job) and to talk about writing or blogging. I always get nervous beforehand, but once I start I normally enjoy it and get a buzz from doing it.

I would maybe add one more tip to Sally’s list and that is to compile a list of topics you can speak about (with appropriate visual aids, of course). You can then offer potential bookers a ‘menu’ they can choose from. This has the benefit that if they don’t like one idea, they may well go for another. It also means you can potentially get repeat bookings, maybe on a regular basis, speaking on a different subject each time. This certainly happens with some of the speakers who are booked by my local U3A.

As always, if you have any questions about this article, for Sally or for me, please do post them below.

This is a fully updated version of an original post from 2019.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m sharing a sideline money-making opportunity that – if you’re in a position to do it – can bring in a steady income for very little effort.

The shortage of parking spaces in many towns and cities has created an opportunity for anyone who has a driveway (or garage) they aren’t using all the time.

One of the best-known operators in this field is JustPark. Through their website and mobile app, they put drivers in touch with home-owners and businesses who have parking spaces (and/or EV charging spaces) available near their destination. They say they help over 10 million drivers a year find parking spaces at over 45,000 UK locations.

Listing your space is free and you can set your own price based on how long the driver wishes to stay. JustPark will suggest an appropriate price based on your location and the facilities you are offering, but you aren’t obliged to accept this.

JustPark charges space-owners a 3% fee on one-off bookings (so if you charge £10 they will take 30p, meaning you receive £9.70). For longer term or rolling bookings over two months, they charge space-owners a higher fee of 20% for the first month, with the fee reverting to the standard 3% after that.

JustPark also make money from drivers, adding up to 25% of the space-owner’s asking price to the fee charged. They say, however, that charges to drivers are still typically 30% lower than ad hoc street parking (if you can find it), which makes the service attractive to motorists as well.

One big attraction of JustPark is that they handle all the admin on your behalf. All payments are made via the website, and space-owners can withdraw earnings via PayPal or direct to their bank account. JustPark also ensure you still get paid even if the booker doesn’t turn up.

JustPark say that the money you earn from renting out your parking space is included in the property trading income allowance introduced by the government in April 2017 – so you can make up to £1,000 per year completely tax-free (and no need to declare it to the taxman).

All drivers using the service have to register on the site, so you know exactly who will be using your space on any given day. There is also a rating system so you can see any comments other users of the service have made about them. Space-owners are also rated by drivers, incidentally.

You can offer spaces by the day, week or month, and set any restrictions you wish on when your space is available. Anyone is welcome to advertise spaces on JustPark, but the locations in most demand are those near airports, stations and stadiums, and in major cities. According to one recent article in the Daily Mail, people in such areas are making more than £4,000 a year doing this. Even if that doesn’t apply to you, though, you can still earn from a few hundred pounds a year to £1000 or more by this means.

Obviously the pandemic and working from home reduced demand for parking spaces. But with life returning to normal now, demand for parking spaces is steadily increasing again.

Of course, if you don’t have a suitable space to offer, you won’t be able to benefit from this opportunity. You could still use JustPark to save money on your own parking costs, though. Either way, the service is well worth checking out 🙂

Another option for cheaper parking is Your Parking Space. Over 60s can get an exclusive 10% discount on this service through my friends at Over 60s Discounts.

Disclosure: As well as being a registered user of JustParkI am an affiliate for them and will therefore receive a small commission if you click through any of my links and sign up. This will not affect the money you earn through the site and/or any savings you make if you use them to find parking spaces.

Cover image by courtesy of BingAI.

This is a fully revised and updated version of my original article on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

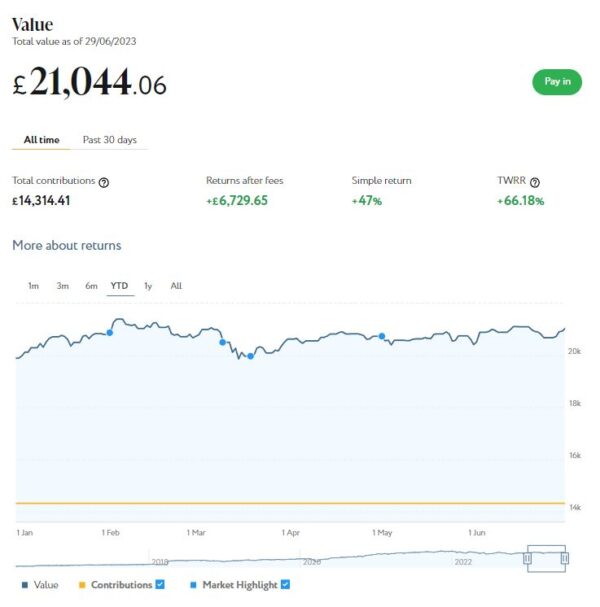

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,044. Last month it stood at £20,419 so that is a rise of £625.

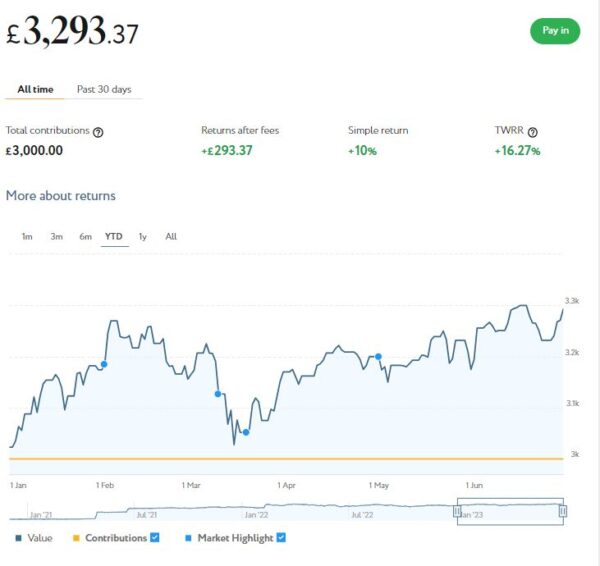

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,293 compared with £3,175 a month ago, an increase of £118. Here is a screen capture showing performance since the start of this year.

This has clearly been a better month for both my Nutmeg pots. Their total value has risen by £743 or 3.15% month on month. Since the start of 2023 the net value of my Nutmeg investments has grown by £1,417 or 6.18%.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £124.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 12 are showing losses. My portfolio is currently showing a net decrease in value of £15.53, meaning that overall (rental income minus capital value decrease) I am up by £109. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is slightly disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

I also spoke to the CEO of Assetz Exchange, Peter Read, recently. He made the point that capital values on the platform simply reflect the latest price at which shares in the property concerned have changed hands on their exchange. They do not represent objective or independent valuations of the properties. If you are investing long term with AE, the annual yield from rentals is really a much more important consideration.

Peter also made the point that the current high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. Assetz Exchange recently published a blog post about this which is worth a read.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching every week. I currently have around £2,500 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 31 July 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 31 July 2023 if the limit is reached. For more information, click here [affiliate link].

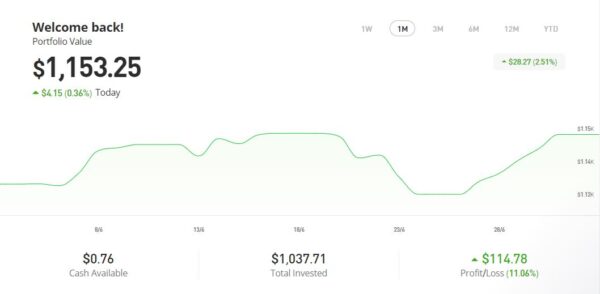

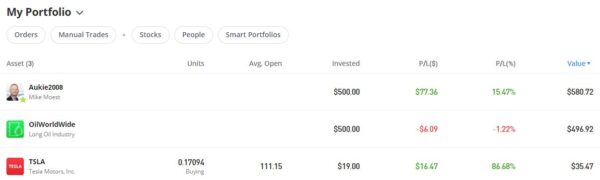

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen capture below, my original investment of $1,022.26 is today worth $1,153.25, an overall increase of $130.99 or 12.81%. in these turbulent times I am very happy with that.

Since last month the price of my Tesla shares has risen substantially and my copy trading portfolio with Aukie2008 has also done well (though less spectacularly). My most recent investment in Oil Worldwide has risen a bit this month but it’s still slightly down on when I invested. The Oil Worldwide portfolio has just been rebalanced by eToro, so I am hoping for better things in the months ahead

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in June on the excellent Mouthy Money website. The first was 10 Great Ways to Save Money on Amazon. Amazon is Britain’s – and the world’s – favourite online store. Prices on Amazon are generally competitive, but over the years I’ve discovered a variety of ways to ensure you get the best value for money from them. So in this article I set out my top ten tips for saving money on Amazon

My other article was Do You Need a Personal Financial Adviser? In this article I discuss the different types of financial adviser and what they do. I also revealed why – despite being a money blogger and considering myself reasonably financially savvy – I have a personal financial adviser myself.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite and I enjoyed reading her recent article concerning how you can Save Money by Reducing Food Waste.

I also published several new posts on Pounds and Sense in June. One of these was My Short Break in Bath. Bath is, of course, a historic city on the River Avon, about 12 miles from Bristol. I went there for three days in June, the first time I had been for over 30 years. In my post I discuss the self-catering apartment where I stayed and reveal some of the things I did and saw. I also share a few top tips for visitors to Bath. The cover image shows the famous Pulteney Bridge, one of Bath’s best-known landmarks.

I also published a post based on a survey of Britons’ investing habits. This addressed questions such as what are the main barriers stopping people investing and where do people get their investment advice from. I thought the results were quite eye-opening. Take a look if you haven’t already.

Finally, I wanted to highlight that the free share offers described in last month’s update are both still open if you haven’t done them yet. The opportunity to Get a Free Share Worth up to £100 with Trading 212 was reopened after closing briefly. It is now on offer till 27 July 2023.

The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is also still open but the terms have changed slightly. To remind you, Wealthyhood is a DIY wealth-building app aimed especially at people who are new to stock market investing. As from 1 June 2023 they changed their fee structure to make it (even) more attractive to small investors. They have now increased the minimum investment to qualify for the free share offer from £20 to £50 – but on the plus side, they guarantee that your free ETF share will be worth at least £10.

That’s all for today. I hope you’re enjoying the summer months and taking the opportunity to get out and about in our beautiful country (or further afield).

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m featuring a way you can get a free ETF share worth up to £200 by signing up for a DIY wealth-building app for investors called Wealthyhood.

Wealthyhood offers a quick and easy method for even complete beginners to start investing in stocks and shares. And currently if you’re new to the platform you can get a free ETF share worth up to £200 just by signing up via any of the referral links in this post and investing at least £50. The ETF share you will get is chosen at random, but could be worth up to £200 (with a minimum value of £10). You can either keep this share or sell it (after 60 days).

For those who don’t know, ETF stands for Exchange Traded Fund. ETFs are a package of shares from a particular section of the stock market. For example, an ‘Asia Pacific ETF’ is a collection of shares from the Asia-Pacific region. ETFs are different to most investment funds in that they don’t usually have a manager running them. Instead, most ETFs are run by computers that regularly balance their portfolios automatically. This helps keep costs low, while still producing respectable returns in most cases. You can learn more about ETFs here if you wish.

How to Sign Up

Signing up with Wealthyhood is pretty straightforward. Just visit the Wealthyhood website via any of the (referral) links in this post and follow the on-screen instructions to register.

You will need to indicate the type (or types) of investment you are interested in. Four broad options are available: stocks, bonds, commodities and real estate. You can choose one or more of these (personally I chose stocks). You will also be invited to indicate whether you want your investments to be global or US only (I opted for global).

You can then choose the actual stocks you want or have this done automatically for you, and indicate the level of risk you are comfortable with. I chose ‘Optimized for Portfolio Weighting’ and then clicked on ‘Create my Portfolio’.

You will then be required to provide various items of personal information, including your address, date of birth, UK National Insurance number, and so on. Once you have entered all the required details, click on ‘Complete Verification’. After a few moments your account should be verified.

In some circumstances the process may take longer. If that happens, Wealthyhood will email you once you’ve been verified.

The next (and final) step will be to deposit a minimum of £100 into your Wealthyhood account and make a minimum £100 investment within seven days. You must do this within seven days of opening your account to qualify for the free ETF share. (If for some reason you’re not bothered about the free share, you can start investing with a minimum of £20.)

Within five days you should receive your free ETF share worth up to £200 (Wealthyhood say that 95% of users get their free ETF share within 1-2 days). You should receive notification about this in the My Account section of the Wealthyhood website when you log in.

You may wish to set a calendar reminder for 60 days, since (as mentioned above) you have to leave your free ETF share in your account for this long before you can sell it and withdraw the proceeds. You can, of course, leave it invested for longer if you wish, but bear in mind that fees may be applied (see below).

What Are The Fees?

Wealthyhood compares favourably with many other share-trading and investment platforms. Deposits and withdrawals are free, and other costs are kept to a minimum.

Until recently Wealthyhood charged all investors a platform fee of £1 a month. That wasn’t excessive (in my view) but for small investors (including those just wanting to take advantage of the free share offer) it was a bit of a deterrent.

As from 1st June 2023, however, the monthly platform charge was scrapped. Instead investors in Beginner accounts (everyone starts off with one of these) pay a small ‘custody fee’ of 0.18% per annum (or 0.015% per month). That works out as an annual custody fee of £1.80 for a £1,000 investment, or just 15p a month. In addition, they have introduced an acquisition charge of 0.45% per order (e.g. £4.50 for £1,000).

These new charges work out much cheaper for investors starting with small amounts and those just signing up for the free share. If you decide to stick with the platform, however, you might in due course want to consider upgrading to the new Wealthyhood Plus plan. This offers fully commission-free investing with no charges per order and no custody fees for £2.99 a month or £35.88 a year. This is obviously not worthwhile for very-small-scale investors, but once your portfolio gets up to around £6,000 (by my calculation) you should save money this way.

How Safe is Wealthyhood?

Wealthyhood is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £85,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks, which can go down as well as up. All investments carry a risk of loss, although in the case of your free ETF share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Wealthyhood member can also refer new members. All you have to do is send them your unique referral link which can be copied from your dashboard. If they join via your link and invest a minimum of £100 (as above), both you and they will then receive one free ETF share worth up to £200 (minimum £5). There is no limit to the number of friends you can refer by this means or the number of free ETF shares you can receive.

Don’t Miss Out!

I do just want to emphasize that in order to qualify for the free ETF share, you MUST click through a special referral link such as those in this article. If you simply go straight to the Wealthyhood website and join there, you won’t receive one.

What’s more, when I was researching this article I found that several other websites who were advertising this offer didn’t have the correct, up-to-date referral links. So even if you had clicked through them and signed up, you wouldn’t have qualified for a free share. To be safe, I strongly recommend clicking through my Wealthyhood referral link. You should then see a banner like this near the top of the page.

If you don’t see this banner, you haven’t clicked through a genuine, working referral link, and sadly will not receive a free ETF share.

Bear in mind also that this offer may be withdrawn any time. If and when I hear of that I will of course amend this post. But I do therefore strongly recommend taking advantage of this offer while you can.

Final Thoughts

Although in this post I have focused mainly on the free ETF share offer, Wealthyhood is also worth considering as an investment platform for the longer term.

Its low charges (especially from 1st June 2023) mean it is well suited for people who are dipping a toe into stock market investing for the first time. By contrast, the dealing fees and commissions charged by some other platforms can make small investments prohibitively expensive.

While you can’t invest in individual company shares through Wealthyhood, a wide range of ETFs is available via the platform. If you have a particular interest in an area such as video games, healthcare or clean energy (for example) you can invest in specific ETFs that track those sectors. This facility for thematic investing is not currently available through most other robo-adviser platforms, including Nutmeg.

I also like the simple, user-friendly Wealthyhood website. This allows you to easily build a balanced portfolio covering the investment types that interest you and reflecting the level of risk you are comfortable with. You can log in to your account at any time to see how your investments are performing and make any changes you wish to your portfolio, including investing more money or withdrawing.

In conclusion, I hope this post has inspired you to consider registering with Wealthyhood to claim your free ETF share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And if you like Wealthyhood you may of course wish to consider investing long term via the platform as well.

As always, any comments or questions are very welcome.

Disclosure: Posts on Pounds and Sense may include my referral links. If you click on one of these and make a purchase or perform some other defined action on the website in question, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive. Please note also that I am not a registered financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a professional financial adviser if in any doubt how best to proceed. All investment carries a risk of loss. Past performance is not a guarantee of future returns. Capital is at risk.

If you enjoyed this post, please link to it on your own blog or social media:

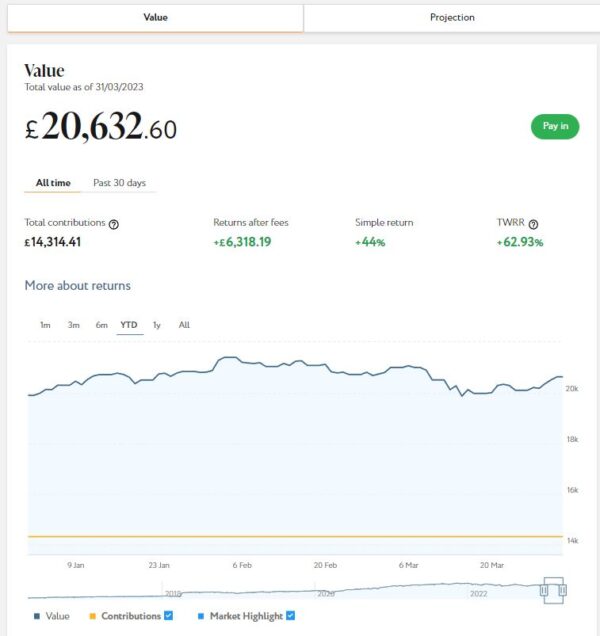

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension), from which I recently started withdrawing again.

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £20,632. Last month it stood at £20,680 so that is a modest fall of £48.

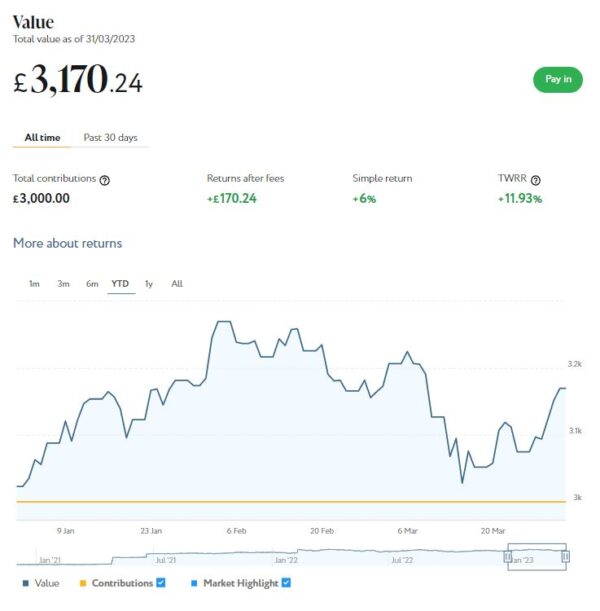

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,170 compared with £3,162 a month ago, a (very) small increase of £8. Here is a screen capture showing performance since the start of this year.

As you can see, this has been a roller-coaster month for both my Nutmeg pots, though overall the dial hasn’t moved very much. My Smart Alpha portfolio has done a bit better than my main portfolio and I might be tempted to switch more of my money into it, though there clearly isn’t a massive difference in performance between them.

The net value of all my Nutmeg investments has fallen this month by £40 or 0.17% month on month. That is obviously a little disappointing, but both pots are still comfortably up on where they were at the start of the year. And their total value has risen by £1,890 (7.77%) since mid-October last year.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not be the smartest strategy. The one exception is if you plan to withdraw your money shortly and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £108.37 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 6 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 16 are showing (small) losses. My portfolio is currently showing a net decrease in value of £26.97, meaning that overall (rental income minus capital value decrease) I am up by £81.40. That’s still a reasonable rate of return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is a little disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 18 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 31 May 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 31 May 2023 if the limit is reached. For more information, click here [affiliate link].

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios. I also invested a small amount I had left over in Tesla shares. My original investment of $1,022.26 is today worth $1,113.72, an increase of $91.46 or 8.95%. in these turbulent times I am very happy with that.

As I said last time, my big success was investing in Tesla at the right time, as their share price has risen by over 86%. If only I had put more than $19 into this!

My copy trading portfolio with Aukie2008 is well in profit. My most recent investment in Oil Worldwide, having started well, is still down fractionally (some might say this serves me right for investing in fossil fuels!). But I am certainly not going to worry about that at the moment.

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in March on the always-excellent Mouthy Money website. One is Some Ways to Save Money on Council Tax. Along with fuel bills and mortgages, council tax is many families’ single largest item of expenditure. There are various ways you may be able to reduce this bill (or even avoid it altogether), though. In this article I go through a range of methods, including household-based, income-based and property-based.

My other piece was Always Wanted to be in the Movies? Let TV Studios Use Your Home for Money. Clearly this opportunity won’t work for everyone. But if you live in a place with features that might be in demand by a TV or film production company, you can potentially make hundreds or even thousands of pounds. And as I say in the article, you definitely don’t need to live in a stately home. Studios need all types of properties – from two-bed terraces to penthouse flats, country cottages to 1970s-style bachelor pads!

Speaking of Mouthy Money, you might also like to read my in-depth blog post about this personal finance website which I wrote in March. It’s called (without any great originality, I know) Have You Seen Mouthy Money?

As you may know, I am nowadays contributing two articles a month to Mouthy Money, so you’ll understand that I have good reason for wanting to promote it 🙂 But that aside, it is an excellent resource for anyone interested in money-making and money-saving. I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite of mine. With Easter on the horizon, I highly recommend her latest article, How to Have a Frugal Family Easter.

Several of my other Pounds and Sense blog posts from March are no longer relevant due to deadlines passing so I won’t bother listing them here. You might perhaps like to read Two Places You Really Shouldn’t Turn for Tax Advice (and One You Definitely Should), though. This is an update of an article I wrote a while back, but it’s on a subject I feel quite strongly about and is still 100 percent relevant.

Finally, as I write this update there are just two days left to the end of the financial year on 5 April 2023. That means you have just two days remaining to make use of your 2022/23 tax-free ISA allowance before it is gone forever. With other tax-free allowances already set to be slashed in the years ahead, it’s more important than ever to make the most of this one while you can. Here’s a link to my recent blog post on this subject.

That’s all for today. I hope you and your family are coping in these challenging times. Don’t forget to check out the government’s Help for Households website, which sets out various types of financial assistance you may be entitled to and is regularly updated.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I have mentioned Mouthy Money a few times on Pounds and Sense. Some of you will be aware I’m a regular contributor to this UK personal finance website.

But while I’ve talked about it in passing a few times, I have never really discussed Mouthy Money properly on PAS. So I thought I should rectify that today!

What Is Mouthy Money?

Mouthy Money is a website dedicated to helping people understand financial matters and make the most of their money. It is run by a small, dedicated team from an office in London. Their efforts are supplemented by a team of freelance writers, researchers and bloggers, including myself.

Every week new articles are added to the website. They are in four main categories, as follows:

Earning covers boosting your income, e.g. by starting a side hustle. Saving is all about reducing your outgoings, while Spending is about getting the best value for your money, e.g. on your weekly groceries shop. Your Questions answers specific questions sent in by readers, e.g. What happens if I can’t pay my tax bill?

The main menu runs across the top of the page. You can scroll down to see the latest articles in the order in which they were added. Alternatively, you can click on any of the four category titles to see the latest articles in the category concerned.

If you scroll further down the Mouthy Money homepage, you will see brief biographies of all the regular contributors, including myself. They include my fellow bloggers and writers Shoestring Jane, Finance Dee, Tolu Frimpong, Jordon Cox, Dana Raer, and so on. There are also bios of the site’s co-editors Paul Thomas and Edmund Greaves. Clicking on any of these will take you to a page listing all articles on Mouthy Money by the person in question.

Example Articles

Here are just a few of my favourite articles from Mouthy Money. I hope this will give you a flavour of the breadth and quality of the content:

I hope you enjoy reading these and many other articles on Mouthy Money and will add the site to your list of finance websites to visit regularly (along with Pounds and Sense, of course!). You can also follow Mouthy Money on Facebook and on Twitter.

As with Pounds and Sense, you can also subscribe to receive emails from Mouthy Money notifying you about the latest posts. The blue sign-up box can be found near the top of most articles on the site (not in the sidebar as on PAS).

One final thing is that if you run a personal finance blog yourself, Mouthy Money are always on the lookout for additional (paid) contributors. You can find out more and apply via this page of the MM website.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I have always had a feature on Pounds and Sense allowing readers to sign up to receive updates any time a new post is published.

It recently came to my attention, however, that these updates, which were meant to be sent automatically, have not always been going out. Although I’ve looked into this, with my admittedly limited technical skills I’ve been unable to figure out why it was happening or how to put it right.

I have therefore taken the ‘nuclear option’ and signed up with an alternative mailing list service called MailPoet. This has worked perfectly in my initial trials.

I don’t just want to import the old list of subscribers to MailPoet. I suspect many people will have forgotten they signed up for updates and I don’t want to be accused of spamming. So if you’d like to receive – or continue receiving – updates every time a new post is published (and other very occasional emails) please could I ask you to sign up to the new service? All you have to do is go to any page on Pounds and Sense and enter your email address in the box near the top right. Click on Let’s Keep in Touch and confirm when requested. Of course, you can cancel any time via the link at the bottom of every email.

I do apologize to existing subscribers that this service hasn’t been working as it should, but hopefully with the new service that will be a thing of the past now.

Finally, just a very quick reminder that you can also follow PAS on Facebook and on Twitter.

Thanks again for being a valued reader of Pounds and Sense 🙂

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2022, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a Very Merry Christmas (strikes and cost-of-living crisis permitting) and for all of us a much better new year 🍾

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!

her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!