Today I have a guest post for you about something many of us in icebox Britain would no doubt love to do at the moment.

Buying a Spanish holiday home, both for your own enjoyment and as a potential investment, has many attractions. But there are various important matters to consider before signing on that dotted line.

Learn more below 🏖

If you and your partner have spent many happy years holidaying in Spain, perhaps you’d like to consider investing in a Spanish holiday home?

Not only would a stunning sun-kissed property provide a wonderful place to enjoy your retirement years, but you could also let it out while you are not there and make some additional income. After all, Spain is a highly popular vacation spot with much to recommend it, so you would certainly never be short of guests.

Whatever you would like to use your Spanish holiday property for, there are a few important things you need to be aware of before you start house-hunting on the Costa Blanca…

Many Stunning Locations To Choose From

As you surely already know if you relish a vacation in Spain, the country has a plethora of gorgeous locations to choose from. While on the one hand this is clearly a good thing, on the other, it could make deciding on a particular location rather tricky.

If you’re struggling to settle on one spot, take some time to think about your requirements for the property. For example, if you’re planning to purchase a home solely for your own use, it makes sense to choose a property in a location you particularly love. Alternatively, if you’re buying a home as an investment, you may prefer to think about the locale that draws the biggest number of visitors and has the highest rental prices.

Insurance Is Important

Insuring your Spanish holiday home is of the utmost importance, even if you won’t initially be spending a great deal of time there. After all, you never know what might go wrong – from fire and theft to flood damage or structural damage caused by extreme weather. If you don’t have cover then you could be liable for some truly hefty repair bills.

Fortunately, finding the right holiday home insurance for Spain should be a breeze, thanks to Quotezone.co.uk’s helpful comparison service. You can compare and contrast quotes from a range of UK providers and potentially save yourself a lot of time and money along the way.

You Will Need An NIE

When you buy a property in Spain as a foreigner, you will be required by law to have an NIE number. The authorities will be able to use this number to work out how much tax (if any) you owe each year.

Your NIE number can be applied for at the Spanish Consulate in your country of residence or in Spain itself. You will need to fill out forms and provide various supporting documents. The process can take anywhere between two weeks and two months.

Factor In All The Costs

Before you take the plunge and commit to buying your Spanish holiday home, it’s a good idea to dedicate some time to running through all the potential costs you are likely to incur.

After all, you won’t just be paying the asking price of the home itself. You will also have to pay various associated fees, not to mention mortgage payments, lawyers’ fees and surveyor charges.

There will also be additional annual costs, as you will have to keep the property maintained to a good standard, particularly if you’re letting it out.

To ensure a Spanish holiday home is the right choice for you and won’t prove to be too big a drain on your retirement savings, take some time to pause and reflect on the various costs involved. This will help ensure you choose the option that works best for you.

Thank you to my friends at Quotezone.co.uk for an informative article. If you have ever dreamed of owning a holiday property in Spain, I hope it will give you food for thought.

As always, please feel free to leave any comments or questions below as usual. I would be particularly interested to hear from any readers who have gone ahead and bought a property in Spain or are actively considering it.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my fellow money blogger Bilquis, whose blog you can read at http://getmoneysaving.com.

In the article below, Bilquis sets out ten work-from-home jobs that can be done without large amounts of training or experience. Whether you’re looking for part-time or full-time work, there may be something suitable for you here.

Over to Bilquis then…

The pandemic has changed how we do many things. A big one is how we work. A lot of companies now prefer the work-from-home (WFH) method. This saves money for the business as they don’t have to pay as much for office space. For employees it means they don’t have to spend time and money commuting and can stay in the comfort of their own home and work there.

While working from home can have drawbacks as well as benefits, it can’t be denied there are lots of opportunities. In this post I will set out ten jobs you may be able to do on a WFH basis.

Sales

If you’re good at selling, this is perfect for you. With improved technology and cloud-based software, having a home-based sales job is a realistic possibility for many. You can sell anything from carpets to pet food. And the great thing about sales jobs is that most pay commission for every sale you make.

There are plenty of businesses looking for salespeople. Check out job boards like Indeed and search for “work from home sales” – plenty of jobs will come up! If you want to brush up your sales skills then I suggest going on YouTube and watching videos from experts like Zig Ziglar.

Customer Service

As with sales, customer service is now in many cases fully remote. Many companies are looking for home-based customer service reps to help with enquiries from customers. These jobs are generally very flexible, so if you can only manage a certain number of hours a week, employers will often be happy work around that.

Again, the best place to find customer service roles is job boards like Indeed.

Admin

If you are well organized and good at creating reports and spreadsheets then you might like working as an administrator. This might include other duties as and when required. Look on job sites like Indeed or WeWorkRemotely.

Social Media Management

Do you like using social media platforms like Instagram and Facebook? Businesses are willing to pay good money for people who can help them grow their business through social media. After all, millions of people use social media and the numbers are increasing every day. Many businesses are clueless when it comes to social media and don’t know how to make the most of it.

That’s where you come in. As a social media manager you will manage and grow their social media by adding interesting content and responding to queries from clients and potential clients. If you don’t know anything about growing social media accounts, you can always learn. Go to Udemy and take one of the many courses available there.

As a social media manager you can either take the freelance route applying for opportunities on Upwork and Fiverr, or you can start your own business. You could also get a job with a company, working in their marketing department.

To start your own business as a social media manager it might help to offer to work free for the first few clients, to gain reviews and social proof.

Audio Transcription

Audio transcription involves preparing a written version of spoken content such as a video or podcast. Podcasts are a very popular way to consume information but some people prefer to read a transcript or at least have it available for reference.

So if you have good typing speed and enjoy listening to podcasts this job could be for you. There are plenty of companies in this field like Happy Scribe, Rev.com and Accuro. Some of these companies do require you to be a native English speaker. According to Happy Scribe, their top earners are making $3,000 (£2,400) a month.

Voiceover Artist

If you have a good voice and enjoy speaking, doing voiceovers can be a great stay-at-home job. The work may involve creating voiceovers for videos and courses. You may also work on audiobooks and other projects.

A good website to get started is Mandy. Others include Voices.com, Voquent and Backstage. Companies or individuals post jobs on these sites and you can apply for them by submitting a short audition.

Top earners can earn over $50,000 (£40,000) per year

Teacher

High speed internet and software like Zoom and Skype has made it easy and convenient to teach online from home. If you are knowledgeable about a particular subject, you can set your own hours and work as many or few as you want. There is also a big demand for native English speakers who can teach the language and/or help learners practise their conversational skills.

All you need is a laptop, internet connection and a working webcam/microphone. Some websites you can try are Preply, Cambly and SkimaTalk. Some of these do require you to have qualifications and/or experience.

If you are looking to boost your income you can create online courses. Using platforms like Skillshare or Udemy you’re able to create online courses that people can sign up to and you can profit from each sign up.

Paralegal

As a paralegal you will be helping solicitors and barristers by preparing legal documents, researching, providing quotes to clients, going to court and performing admin work, all based from home.

Most paralegal jobs will not require you to have a law degree, but some do require you to have some legal training or experience.

You can find WFH paralegal jobs on Indeed, TotalJobs or even social networking site Linkedin.

Virtual Assistant

This WFH job involves helping businesses with any task they may have such as data entry, admin, email, research, simple bookkeeping, and so on. The job can be varied and interesting. You can find jobs for virtual assistants on Upwork, Freelancer, and so on.

Web Developer

Businesses need an online presence and can’t afford not to be online. If a business isn’t online and doesn’t have a website, their competition most likely will. As a home-based web developer, you can use your programming skills to build websites for business clients. You can also enjoy a continuing income maintaining and updating the site for them.

Conclusion

With high-speed internet connections and ever-improving technology, working from home is now commonplace. For many of these jobs you do not need any special experience or qualifications. And because you will be working from home, you – and your clients – can be based anywhere in the world.

If you want to work from home, opportunities have never been better, whether you want to work for an employer or become self-employed and seek out clients yourself.

Good luck, and enjoy your new WFH career!

Thank you again to Bilquis for an eye-opening article. Please do check out his blog at http://getmoneysaving.com.

As Bilquis says, there has never been a better time to seek work from home. And as someone who has done this himself for over 30 years, I do highly recommend it! But it must be said that it can have certain drawbacks as well. You might enjoy reading my blog post The Pros and Cons of Working From Home in which I discuss this in much more detail.

As always, if you have any comments or questions about this post, for me or for Bilquis, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my colleague Richard Winstone (not pictured above). Richard has just launched a new, diary-style blog called Financially Fat about his quest to achieve ‘financial fitness’.

I thought Financially Fat could be of interest to many Pounds and Sense readers, so I invited Richard to create a guest post about it. He was happy to oblige, so here is his article.

Hi everyone. I’m Richard Winstone and I write a blog called Financially Fat.

I want to start this post by thanking Nick for allowing me to guest blog on Pounds and Sense. I appreciate the feedback he has given on my blog and am really proud to have this opportunity to showcase Financially Fat to the Pounds and Sense community.

What is Financially Fat?

“If financial fitness is the aim, then I am Financially Fat.” This is the tag-line of the Financially Fat blog.

Being financially fat isn’t supposed to paint the image of a fat, wealthy man. It’s meant to imply that my finances are out of shape, which they are.

I’ve decided to take a no-holds-barred approach to financial honesty in my blog: the good, the bad and the ugly. So, in the second post I wrote down my complete financial position. I left nothing to the imagination and fully revealed my “financial nakedness”. I did this because I wanted my readers to know that I’m not another rich guy giving quick tips to save a few quid (not that there’s anything wrong with that), but that I’m actually financially struggling and that I’m taking action to improve my financial fitness.

Financially Fit is written as a diary, in which every Friday I comment on how I did with the previous week’s targets and set new targets for the following week. There are also a couple of sections of me rambling about my thoughts from the previous week, which I hope are insightful but may just be the ramblings of a mad man 😉

The purpose of the blog is two-fold. First, I want to chronicle my journey from being financially fat to being financially fit. I think this is easier to do weekly while I’m on the journey rather than try to remember what I did after (I hope) I’ve become financially fit. And second, I’m hoping to provide a step-by-step guide for others to follow to help improve their financial fitness. I write and post my blog to the over50smoney.com website and email it out to our over50smoney community each week.

So, below is a quick summary of how my blogging journey has gone so far, now that I’m five weeks in…

This is another introductory post, but it goes into much more detail. I start by detailing what I hope to gain from Financially Fat and then move on to set out my starting financial position, including my salary, savings, debts, shares, assets and anything else I could think of. It’s a complete works of my financial position, which I’ve committed to reviewing monthly in a similar format so I can see how my financial position improves month-to-month (the next review is this Friday and I’m nervous!).

Right, Week 2 is when it starts getting more interesting and where the format of the blog really starts to become clear. I started this post by highlighting three things I did that were bad for my finances over the previous week, which were:

Moving home (kind of unavoidable)

Working from Costa far too often

Dining out

I then came up with the idea of setting targets for the following week to address things that I’ve done wrong in the previous week, with the hope that I’ll eventually move away from bad habits that cost me way too much money. This seems to be working to be honest, at the moment I’m down to working from Costa only once or twice a week and usually only for a couple of hours each time rather than full days.

Continuing the development of the blog format, Week 3 is where I started titling the blog posts a little more nicely, and where I started summing up my financial savings from following the targets on my previous week.

In this post, I point out how working from Costa only once a week instead of five times a week can save me around £50 per week, over £200 per month! I also discuss setting yourself targets as you follow the blog. Reading it is (I hope) interesting, but for the blog to be useful you need to follow the thought processes I go through and make sure you’re applying them to your own life. So, if you have a small, seemingly inexpensive habit that you do frequently, then I recommend reviewing how much that habit has actually cost you over a month and see how much you could save by cutting down.

In Week 4 I discussed the target of reviewing my standing orders and direct debits. After just one review, which took about 45 minutes, I was able to save just under £600 per year! Which is insane. I continued to review into the following week but was only able to save an additional £1 per month by changing my gym membership.

This is also the week I formalised my “Ramblings” as an introduction to the blog, I hope you enjoy reading them and please feel free to email me any time to comment, ask questions or provide suggestions (I’ve been getting some great tips from readers!).

By this point, I’ve started getting really into the money-saving game. I’m also discussing things like increasing income to ensure I’m not reliant only on my salary.

But, as the title indicates, I talk about tackling my biggest challenge yet, which is currently destroying my finances – smoking! I know, it’s a horrible habit and I’m obviously very aware of the negative health affects as well as the impact it’s having on my bank balance. So, I’ve set out a five-week plan to quit (which I can say I’m currently doing okay on, but it has only been four days).

Cutting out smoking could save me around £2,400 per year, which means from the Financially Fat blog I would have saved around £3,200 a year in disposable income just in the first five weeks, and there’s still so much more work to do!

Follow the Financially Fat Blog

That’s it for the summary of my first six blog posts. I hope you will click through and give them a read as there’s a lot more information in there and some interesting views, I like to think.

If you’re interested in following my blog, please head over to over50smoney.com and sign-up for our newsletters. Or, if you’d rather not receive emails, you could just follow us on Facebook. I write and post every Friday and put links on our Facebook page, so please consider liking and following this. Thank you 🙂

I want to thank Nick again for letting me write this short summary of Financially Fat. I really hope you find it as useful as I am. If you have any questions or comments, or just fancy a chat about finances, please feel free to reach out to me directly at richard@over50smoney.com. I sometimes take a few days to reply, but I promise I get back to every email I receive.

I’m Richard Winstone and I am Financially Fat.

Many thanks to Richard Winstone (pictured, right) for this article. I hope you will take a moment to check out Financially Fat.

I particularly admire the honesty with which Richard sets out his financial position. I try to be honest about my finances on PAS as well, but not in nearly as systematic a way as he is doing!

If you are also ‘financially fat’ (as Richard defines it) I hope you may find the info and advice on the new blog inspires you in your own quest to achieve financial fitness.

As always, if you have any comments or questions about this post (for me or for Richard), please do share them below.

If you enjoyed this post, please link to it on your own blog or social media:

Tourism in many parts of the UK is booming right now.

As we come out of the pandemic some people are venturing abroad again. But many others (perhaps deterred by the remaining restrictions and long queues and cancellations at airports) have been discovering (or rediscovering) what this country has to offer. This in turn has led to a growing demand for holiday rentals. That is only likely to increase as overseas visitors start to return as well.

There is undoubtedly money to be made from holiday lets, so in my post today I shall be looking at this subject in more detail. The article is written in association with my friends at the Suffolk Building Society and I shall be quoting from their detailed research on this subject (and using some of their graphics!).

Let’s start with the most crucial consideration for would-be holiday let landlords…

Setting

A recent study by the Suffolk Building Society found that the setting of a property was more important for potential landlords than other factors such as renovation potential or proximity to amenities. The key aspects for would-be landlords when considering buying a holiday let were:

A property that is in or near beautiful scenery (31%)

A property that is near the beach or coast (30%)

A property that is easy to manage and doesn’t require much upkeep (28%)

A property that is in an area that the landlord already personally knows or loves (27%)

A property that is in a popular tourist or holiday destination (23%)

This is summed up in the graphic below.

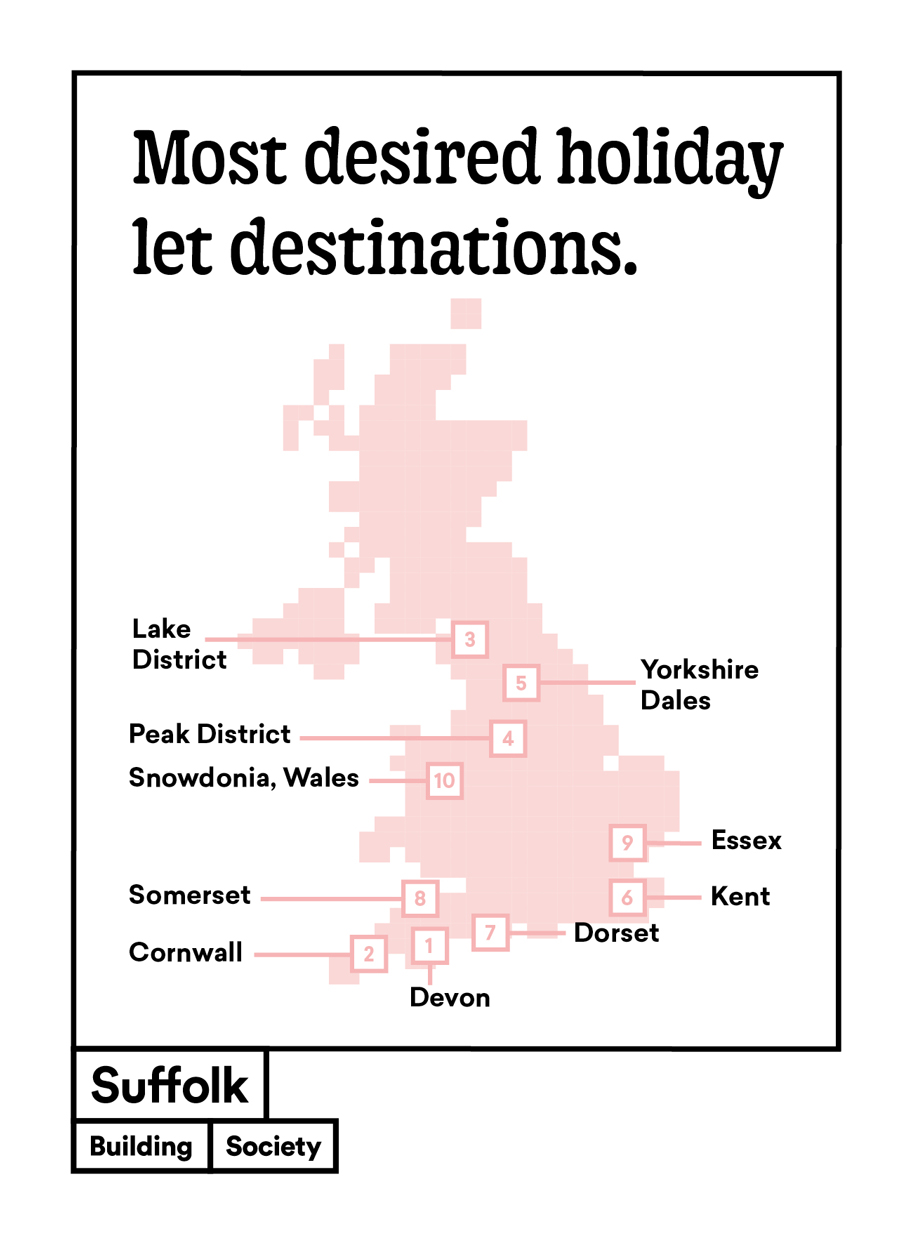

Location

As you can see in the graphic below, Devon and Cornwall were the locations most aspiring holiday let landlords were considering, followed by the Lake District, Peak District and Yorkshire Dales.

How Much Can You Make?

Being a holiday let landlord has many attractions, including significantly higher returns than are achievable from residential lets.

An apartment in a popular tourist area, for example, can generate £1,000 a week or more (in peak season at least). A recent report in Which? found that the average annual yield on a holiday let was just over 10%. This compares favourably with residential buy-to-lets, where around 7% a year is more typical. The Which? article mentioned above forecasts holiday let yields rising in future to 14% or more.

According to Sykes Holiday Cottages, the average holiday let owner is earning approximately £21,000 per year. You can also enjoy cheap holidays staying at the property yourself. And there are tax advantages too, as running a furnished holiday let (FHL) is considered a trade rather than an investment. This means you can offset mortgage interest costs against your income, as well as council tax and other bills.

On the downside, being a holiday let landlord is likely to be more hands-on. New tenants will move in every few days and the property will need to be cleaned, tidied and restocked on a regular basis. Covid precautions have added an extra dimension to this (though rules are now easing). There will be more admin dealing with a steady stream of enquiries and visitors. You will need to budget for advertising too, or risk ‘voids’ when your property is empty and you are losing rather than making money. And finally, any garden at the property will need tending as well.

You can of course outsource some (or all) of this work to a management agency, but naturally there will be a cost to this, impacting your bottom line

Tips for Would-be Holiday Let Landlords

If you are planning to buy a holiday let property with a mortgage (as most people do), there are some important things to bear in mind. Buying a holiday let differs in some significant ways from buying a home to live in or even a traditional buy-to-let.

Be aware that many holiday let mortgages require a landlord to have a mortgage, own their main residential property first, or have buy-to-let properties already – and in some instances, a combination of these.

Understand that some lenders also have age restrictions for first time landlords, even if they are already residential home owners.

Affordability assessments for holiday-let properties are usually calculated on the property’s rental potential rather than personal income and outgoings, but the lender will still want to understand the applicant’s financial position.

Applicants may have to demonstrate a minimum income set by the lender, but this income can often be from a combination of employment, self-employment, investments, pensions, and so on.

Be prepared to show third-party evidence of rental value in low, mid and high seasons from a verified lettings agent – even if not planning on using an agency to manage the property.

Expect that the property will also be assessed by the mortgage lender. Properties in holiday parks, caravans or lodges, and those of unusual construction method may not always be accepted.

Applicants should not assume they can market their property on short-term lettings sites such as Airbnb and Vrbo – some mortgage lenders have rules that prohibit this.

Check the amount of personal use allowed so as not to breach terms and conditions. Mortgage companies will always allow the owner a certain amount of personal use but this can vary.

Check whether the mortgage lender has a limit on the number of holiday let and/or buy to let properties that the landlord is allowed to own.

Specialist holiday letting insurance must be arranged with public liability cover (typically minimum £1 million) included.

Suffolk Building Society’s Head of Mortgages, Charlotte Grimshaw, says: ‘Before jumping on the [holiday let] bandwagon, potential owners should do their due diligence; consider the financial commitments of not just the purchase but the maintenance, taxes, and other expenses such as cleaners and gardeners. It’s also worth taking the time to understand the market, and check out the competition before falling in love with a property that isn’t viable in terms of lettings.’

And she adds: ‘Applying for a holiday let mortgage can be a little more complex than applying for a traditional residential property or buy to let, so it can be helpful to approach an independent mortgage adviser to ensure the application has the best chance of success. A mortgage adviser will also have a good understanding of the different criteria that mortgage companies request, helping landlords find the most suitable product.’

Final Thoughts

Thank you again to my friends at Suffolk Building Society for their help with this article. I hope it has opened your eyes to the money-making potential of holiday lets. And if you are among the 17% of UK adults who (according to the SBS survey) considered buying a holiday let property during the pandemic, I hope it has given you some points to think about.

Regular readers of PAS will know I have a particular interest in P2P/crowdlending investment. Such platforms offer the opportunity to invest in loans to businesses or individuals and profit from the interest charged to borrowers.

With savings account interest rates still very low, many investors are understandably looking for better returns on their savings and investments. If that applies to you, European crowdlending platform Nibble is worth a look.

What is Nibble?

Nibble is a crowdlending platform launched in 2020 by IT Smart Finance, a company with over five years’ experience developing innovative products in financial technology.

Nibble’s business method involves investing in P2P loans to businesses made through Joymoney (the flagship product of the ITSF group). Private investors can then invest in these loans to take advantage of the interest paid by borrowers.

What Are the Benefits?

Probably the biggest attraction of Nibble to investors is that it offers returns on investment of up to 14.5%. As you will doubtless know, this is well above the average in the collective financing industry.

The minimum investment with Nibble is just €10 (about £8.40 at current exchange rates). The platform has an auto-investment tool, allowing trading to be fast and straightforward. You aren’t required to choose individual loan investments, as this is handled by the company. You simply choose one of three investment strategies (see below) based on the timescale over which you wish to invest and the level of risk you are comfortable with.

Other attractions include a minimum investment period of as little as one month, with interest credited to your account weekly. You can withdraw the interest if you wish or reinvest it in an existing or new portfolio.

In addition, if you want to withdraw money from your account early, Nibble say they will find a new investor for your portfolio for a small commission fee.

What Are the Risks?

Obviously no investment is without risk, but Nibble have gone to some lengths to keep this as low as possible. You can read a detailed article about this on this page of the Nibble website (warning: it is quite long!).

For investors opting for the lowest-risk Classic Strategy (see below) a Buyback Guarantee applies. That means that if a borrower defaults on payment, the company will return your money, including interest earned, for the time you held the loan.

For the other two, higher-paying strategies, the risk is shared between the investor and the platform in the form of a variable interest rate. The rate paid is decided by the Risk Committee, which meets monthly to assess how loan portfolios are performing and set rates accordingly. The actual rates paid therefore vary from month to month.

Obviously the other risk is that the lending company itself will go bust. For various reasons set out on the Nibble website this appears unlikely, but of course it is not impossible. If that were to happen, you would not be covered by the Financial Services Compensation Scheme (FSCS) which covers deposits in registered UK savings institutions up to £85,000. Nibble say that in the worst case scenario ‘a management company will be assigned to help the investor to recover funds in accordance with the rights of claim against the borrower. In addition, there is always a reserve fund which serves as an additional “safety airbag” for the investor.’

Finally, as loans are currently all in euro, UK investors will of course have to contend with exchange rate fluctuations, which could work for or against you.

How Do You Get Started?

If you wish to invest via Nibble, the first thing you will need to do is set up an account via the Nibble website.

As Nibble is a European operation, you will need to invest in euro and your returns will be paid in this currency. That obviously adds a layer of extra complexity for UK citizens, but there are various ways round this. If you have a UK bank account you will normally be able to make (and receive) payments in euro, but may be charged a NSTF (Non-Sterling Transaction Fee).

You could use your own bank to fund your account initially, but if you become a regular investor with Nibble you might want to use a service or account that charges lower fees. You could use a money transfer service such as Paysera or Wise (formally TransferWise). These will enable you to transfer funds between Nibble and your own bank account with lower charges (and potentially a more favourable exchange rate). Another option would be to open a Euro account with a provider such as Starling. This will allow you to receive and make payments in both sterling and euro, again at a lower overall cost.

Nibble offers investors a choice of three investment strategies according to income and risk preferences. They call this approach Flexible Investment. The three strategies are called Classic, Balanced and Legal. They differ in the level of income on offer, the degree of risk, and how those risks are distributed between the platform and the user. Each strategy is described below using screen captures from the Nibble website.

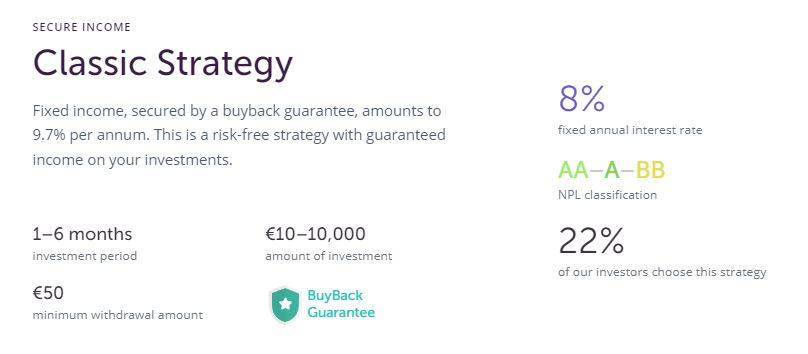

Classic Strategy

As you can see, this strategy offers the lowest level of risk and also the lowest rate of return (though still a respectable 8% at time of writing and up to 9.7% if you reinvest every time your investment matures). You can start with as little as 10 euro for a minimum period of just one month, so this may be a good way to test the water initially. Be aware that the minimum withdrawal is 50 euro though.

An important thing to note here is the BuyBack Guarantee. As mentioned above, this means that if a borrower defaults on their payment, the company will return your money, including interest earned, for the time you held the loan. That significantly reduces the risk of investing.

Balanced Strategy

As you will see, the Balanced Strategy offers higher potential returns than the Classic Strategy but without the safety net of the Buyback Guarantee. The minimum investment amount is 100 euro and the minimum period seven months. According to Nibble this is the most popular strategy among investors, with almost 2/3 opting for it.

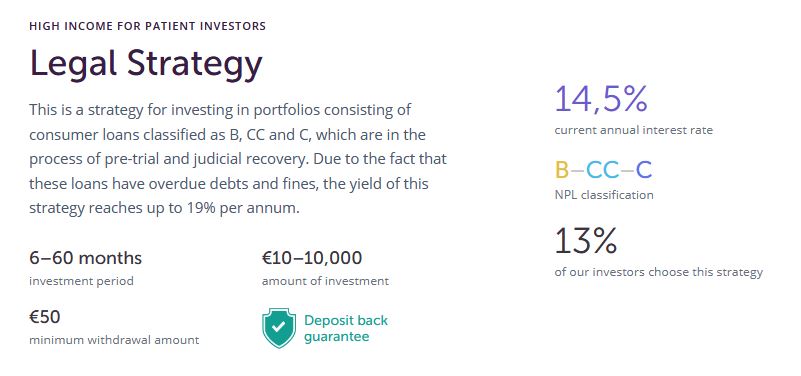

Legal Strategy

The Legal Strategy offers the highest potential returns. The loans in question are in default and facing legal action (hence the name). Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the amount owed. The minimum investment amount is 10 euro and the minimum period is six months.

As you can see, the Legal Strategy comes with a deposit back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per annum. The actual yield paid will depend on how successful recovery efforts prove, so you may end up with a return of anywhere between 9% and 14.5%.

According to Nibble 13% of their investors choose this strategy, which is a fairly new one.

My Experience

I wanted to try out Nibble myself,so I set up an account with them. The process was quick and straightforward. You just click on Create Account at the top of the Nibble homepage and follow the online instructions.

You are required to complete a short verification process before opening your account. This involves taking a photo of your passport, driving licence or some other form of ID, along with a selfie. You may use your mobile phone camera for this. It all worked smoothly and seamlessly in my case, and within a couple of minutes my application had been verified and approved.

After that, it is just a matter of making your initial deposit and deciding which of the strategies mentioned above you want to use. I chose the Classic Strategy as a low-risk test and so far everything has gone as promised. Interest is credited to my account every week, and so far at the end of each investment period I have reinvested all the capital and interest received.

I plan to try out the new Legal Strategy myself and will report in due course how this goes.

Closing Thoughts

If you are looking for a more exciting home for some of your cash that allows you to take advantage of the higher interest rates on offer in Spain (and other countries soon), Nibble is worth checking out.

I like the low minimum investment for the Classic Strategy and the fact that the minimum loan period for this is just a month. That allows you to try out the platform without risking too much or tying up your funds for too long. The BuyBack Guarantee provides additional reassurance. The other strategies offer higher rates of interest, though it is important to note the longer investment periods and the fact that rates paid may vary from month to month.

The website’s ease of use is another attraction, as is the fact that Nibble doesn’t impose any fees or charges on investors. As mentioned above, you do just need to bear in mind the need to switch between pounds and euro and the importance of minimizing the costs associated with this.

As a Spanish-based company NIbble doesn’t have too many UK reviews, but those that I have seen are almost entirely positive. On the popular independent Trustpilot website, they get an average score of 4.2 (‘Great’) with 75% of reviewers awarding them a maximum five star rating.

My advice if you want to try Nibble would be to start by investing modestly using the Classic Strategy (as I have). This will allow you to see how the platform works and get your capital returned with interest in as little as 30 days. You can then move on to the other investment options (Balanced and Legal) for bigger potential returns if you wish.

I have just made a small additional investment in the Nibble Legal Strategy, so will be saying more about this soon.

Obviously, nobody should put all their money into Nibble, but it is worth considering within a diversified savings and investments portfolio, especially in the current low-interest savings environment. As stated above, you should also bear in mind that your money won’t be protected by the Financial Services Compensation Scheme (FSCS), which protects deposits of up to £85,000 in most UK bank accounts. Of course, P2P/crowdlending platforms in the UK are not generally covered by the FSCS either.

I will, of course, continue to report on Pounds and Sense how my Nibble investments fare.

As always, if you have any comments or questions about this post, please do leave them below.

Note: This is a fully updated version of my original Nibble review from 2021.

Disclaimer: I am not a qualified independent financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if unsure how best to proceed. All investing carries a risk of loss. Note also that this review includes my affiliate (referral) links, so if you click through and end up investing with Nibble, I may receive a commission for introducing you. This will not affect the price you pay or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

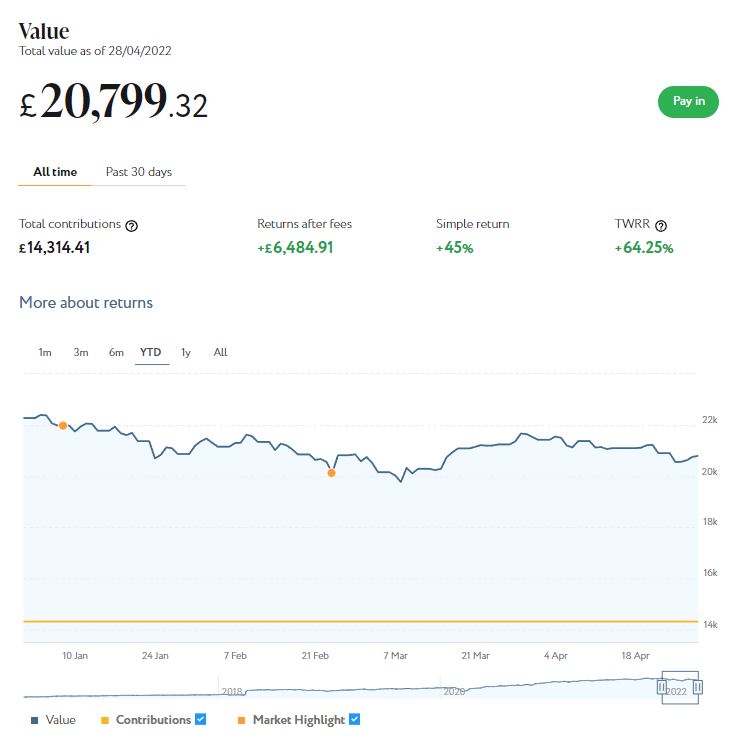

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below shows, my main portfolio is currently valued at £20,799. Last month it stood at £21,646, so that is a fall of £847.

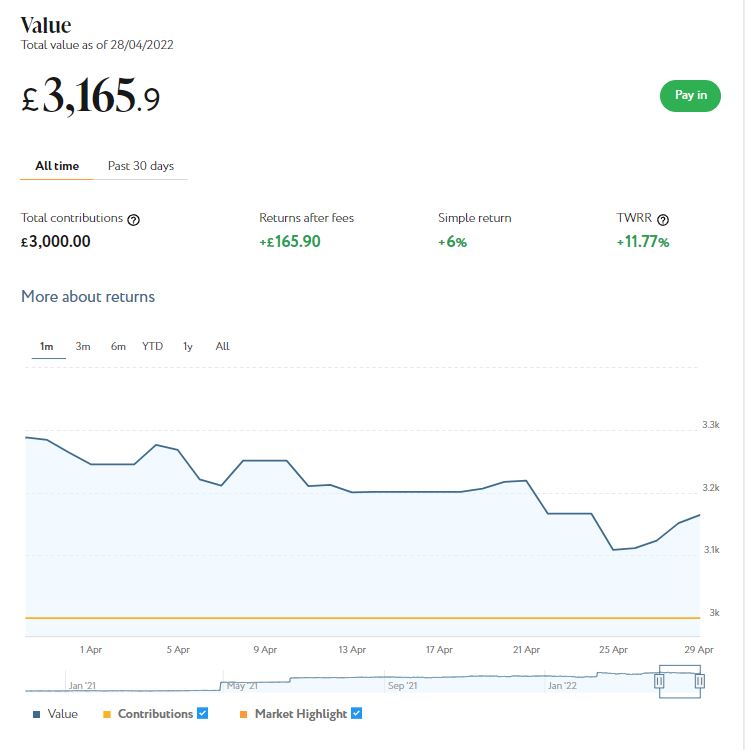

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,166 compared with £3,286 last month, a fall of £120

Here is a screen capture showing performance over the last month.

Obviously the falls are disappointing (although they come after broadly similar rises the month before). As I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments, and certainly over the last few months there has been no shortage of volatility in world markets. And it’s also worth noting that since I started investing with Nutmeg in 2016 I have still enjoyed a total return on my main portfolio of 45% (or 64.25% time-weighted).

I should also mention that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls last month.

If you also have a Nutmeg portfolio and plan to withdraw from it in the next few months, there is certainly a case for switching to a lower risk level right now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

I won’t go into detail about my Assetz Exchange investments this month. Briefly, though, regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000. Since I opened my account, my AE portfolio has generated £51.50 in revenue from rental and £82.29 in capital growth, a total of £133.79. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have over £2,150 invested with them, a significant proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, although some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present all my Kuflink loans are performing to schedule, with several due to mature in the next few months.

Kuflink recently announced that they were ending their cashback incentive for new members. This used to pay up to £4,000. I know several PAS readers availed themselves of this offer. It’s obviously disappointing it’s now ended, but in a way it’s good news as well. It demonstrates that Kuflink is thriving and they don’t need to offer ‘bribes’ to bring in new investors. As they themselves said in a recent email, ‘We feel now is the right time for us to move away from these campaigns [cashback and refer-a-friend] and utilise the funds within the business to make further enhancements to our products and the platform.’

Even without the cashback incentive, I do still recommend Kuflink and will continue to invest with them. You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

Another platform in which I have a modest investment is the European crowdlending platform Nibble. This has continued to perform as promised. Several of the loans I invested in have matured and each time I have reinvested the proceeds.

Nibble recently added a new loan category to their offering. This is in the debt collection market; Nibble describe it as their Legal Strategy. This involves investing in loans that are overdue and facing legal action for recovery. Nibble buy these loans at a fraction of their value and then attempt to recover as much of the outstanding debt as possible.

Nibble investors can buy portions of these loans for prices starting at 100 euro (about £84). The company say that investors will receive annual interest rates of between 8 and 14.5% according to how successful their recovery efforts prove. But in any event they offer a ‘buyback guarantee’ that even in the worst case you will receive 8% interest and return of your original investment. I will be trying this out myself soon and also updating my original review, which you can read here if you wish. You can also sign up directly on the Nibble website if you like [affiliate link].

Also this month I wanted to mention that the under-the-radar matched betting opportunity I have described a few times on PAS has closed. My contact there tells me the bookies have tightened up so much on their offers that it is no longer feasible to go on running a free service that makes money for both clients and the company. Final payments went out by the end of April to all existing members (which of course include a number of PAS readers). Again this is obviously disappointing, but I have seen myself that it is getting harder and harder (though not yet impossible) to generate profits from matched betting, especially once you have exhausted the welcome offers.

Anyway, the better news is that the guys behind the business have a new project in the pipeline that will make use of the clever software they developed for the matched betting service. It will work a bit differently from the original programme, but again will be free to join and entirely risk-free for members. They say they expect it to work over a three-month period and generate a one-off payout of between £500 and £1500 per person. In addition, because the new programme will work differently, it will also be open to people who do matched betting themselves (or have done in the past). I will share more details on PAS when I have them – but for now if you would like to be put on my priority list for info, just drop me a line with your email address via my Contact Me page.

Another bit of news is that I have temporarily suspended withdrawals from my Bestinvest SIPP, which is now in drawdown. This is partly in response to volatility in world markets caused by the war in Ukraine and inflation fears (among other things). But also I don’t need the money as much at the moment, as I am now receiving the full state pension. With my other income streams as well, continuing to draw an income from my SIPP would have generated a tax liability, so I thought it better to let the money grow tax-free in my pension fund until I really need it. My personal financial adviser Mike agrees and approves, incidentally 🙂

Lastly, I enjoyed my short break in lovely Llandudno a week ago. I was reasonably lucky with the weather, although it was quite windy. But it was great to see the resort almost back to normal after the lockdowns and other disruptions of the last two years. There were plenty of people out and about enjoying the spring sunshine, as this photo taken at the end of the pier shows 🙂

One other thing that struck me in Llandudno was how widely cash was accepted and indeed welcomed. In the Midlands town where I live most businesses don’t seem to want cash any more and insist on payment by card. I actually had to go to a cashpoint in Llandudno to draw more money. I can’t remember the last time I did that at home!

That’s enough for now, so I’ll sign off till next time. I hope you are keeping safe and well, and making the most of the better weather and lifting of Covid restrictions. If you’re planning any UK holidays yourself, don’t forget I have a list of places I have visited and recommend here 🙂

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

This is the second in a three-part series of collaborative posts about equity release. This article looks at the likely effect of rising interest rates on the equity release market.

The equity release industry is booming. Homeowners from across the UK may find the financial freedom they desire by unlocking one of these attractive products.

If you’re a homeowner over 55 and haven’t heard of equity release, you need to do your research. These products allow you to access cash tied up in your property for any purpose you wish. No tax is payable on this money, and you will never be obliged to move out of your home.

John Lawson from SovereignBoss has done extensive research on the future of the equity release interest rates. He has discovered that after reaching an all-time low in March 2021, equity release interest rates are rising. The big question is, how significant will the rate increase be, and will this have a short-term effect on the industry as a whole? Let’s take a look at what Mr Lawson has to say.

Interest Rate Increase

When interest rates rise, the equity release sector is inevitably impacted as well. In March 2021 interest rates hit a historic low, with some homeowners having the opportunity to unlock equity with fixed rates as low as 2.3%. This unprecedented rate drop was exciting because it wasn’t much more expensive for a homeowner to opt for an equity release than it was to have a traditional mortgage. Plus, with no repayments required in one’s lifetime, retired homeowners could save a fortune by eliminating monthly mortgage payments. (1)

Recently interest rates have increased slightly but are still quite low. Current rates range between 2.9% and 6.4%. The interest rates you achieve will be lender-dependent, but they will also be determined by your age, health condition and property value.

Experts predict that interest rates are set to rise until 2024. And with the latest announcement by the Equity Release Council (see below), now could be the cheapest opportunity to access the cash tied up in your property through an equity release mortgage.

New Compulsory Optional Repayments

In addition to interest rates rising but still being stable, on 31st March 2021, the Equity Release Council enforced guidance on lenders to offer all their lifetime mortgage clients the option for penalty-free voluntary repayments. This means that homeowners can now repay up to 40% of the amount borrowed each year.

The exact offer you receive will depend on the lender you select. But in principle, if you have the means to do so, you could pay off your equity release plan within three to 10 years, restoring your property’s value.

But that’s not all. Once you’ve released equity, there is no risk of foreclosure. You can stop and start making repayments whenever you wish. Voluntary repayments are a great idea if you can afford them, as they reduce the overall cost of your loan by preventing compound interest.

So How Badly Will the Industry Be Affected?

With interest rates still reasonable and the above announcement by the Equity Release Council, the industry is set for another record-breaking year. Eighty percent of experts agree that the industry’s value is rising, and we at Sovereign Boss are excited to see further innovation from lenders and the Equity Release Council.

In Conclusion

Whether now is the best time to opt for an equity release product is very personal. You will need to consult a financial advisor who will help you determine the best course of action for your needs. If it’s in your interest to unlock equity at this stage, however, you’re likely to find a fantastic deal, with product flexibility better than ever.

So, while interest rates are rising, they’re not too much of an issue at this stage. And there is certainly no indication that there will be any short-term impact on the equity release industry. On the contrary, we are set for another record-breaking year.

That being said, it’s too early to predict the long-term impact that interest rates increase will have on the industry. But SovereignBoss considers it their responsibility to keep you updated with the latest industry trends.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at P2P property investment platform Kuflink.

I have been investing with Kuflink for five years now, so this is a fully updated repost of my original review.

What is Kuflink?

Kuflink is an online platform offering opportunities to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage.

Kuflink offer three types of investment, as follows:

Auto Invest and IFISAs both automatically invest your money across a number of loans and pay a fixed interest rate, typically between 7 and 9%. You can choose a 1-year, 2-year or 3-year term, and interest is paid annually (it is automatically reinvested at the end of each year with the two-year and three-year products). The Auto-Invest product is basically the same as the IFISA, but without the tax-free wrapper.

At one time only the Auto-Invest option was available for IFISAs, but nowadays you can choose your own investments if you prefer. The great majority of Self-Select loans on the Kuflink platform are IFISA-eligible. If you check out the Self-Select listings on the Kuflink website (see image below), this will tell you whether any particular loan is IFISA-eligible or not.

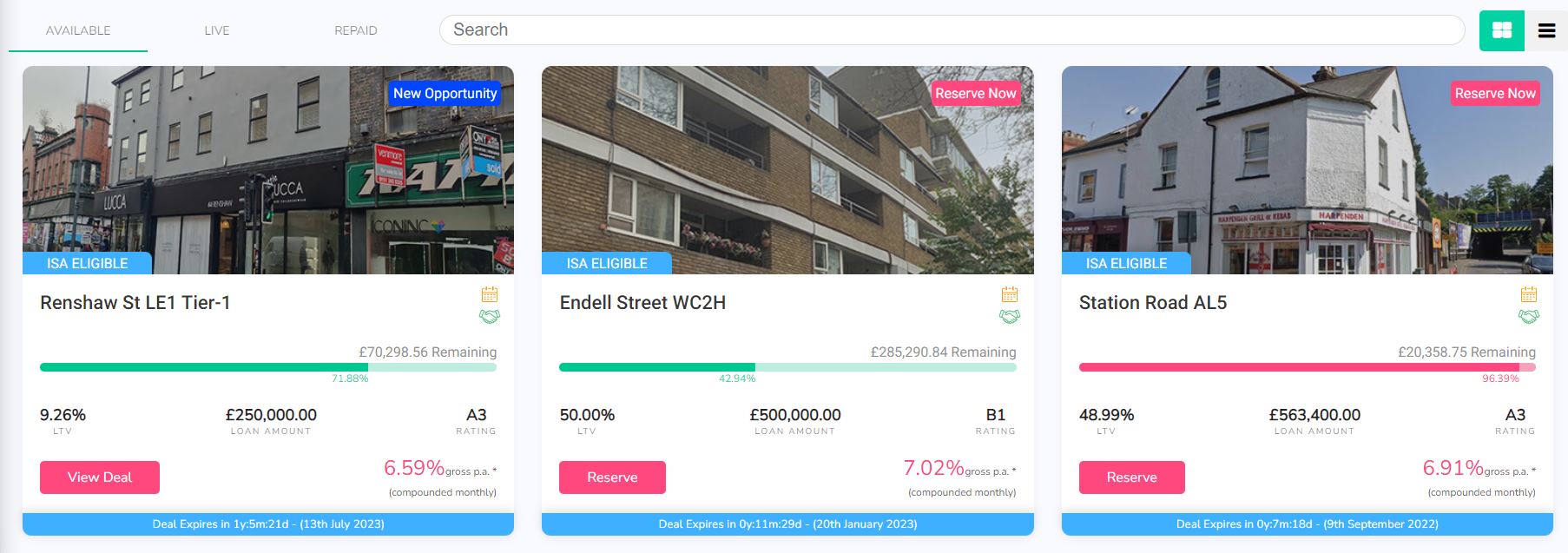

Individual Select-Invest loans pay interest rates varying between about 6 and 7.2%, depending largely on the LTV of the loan (loan to value, a measure of how secure the loan would be in the event of a default). The higher the LTV, the riskier the loan, and – other things being equal – the higher the interest rate paid in consequence. You can see a screen capture below of three Select-Invest loans available on the platform at the time of writing.

As a reasonably experienced P2P investor, I put my money into Select-Invest loans. These typically have a duration of six months to a year and (as mentioned above) pay interest from around 6 to 7.20 percent. That obviously isn’t as much as some P2P property platforms (e.g. BLEND), but I think it represents a fair balance between risk and reward. Kuflink also invest in every loan themselves up to 5% of the value of each loan – so, as the expression goes, they have skin in the game.

My Kuflink Review

I found signing up with Kuflink a quick and easy process. They do the obligatory money-laundering checks, but in my case anyway this was all done electronically behind the scenes. I uploaded a copy of my passport and was approved almost immediately. I started by depositing £500, but you can start with as little as £100 if you like.

Initially I put my money into a 12-month loan paying 7% annual interest. One good feature I didn’t grasp initially is that with Select-Invest loans interest is paid monthly. So once a month I receive interest payments on all the loans I am currently invested in. This is paid into a wallet, from which you can either withdraw to your bank account or reinvest.

Kuflink recently introduced an option to have monthly loan repayments automatically reinvested rather than paid into your account as cash. This effectively boosts your interest rate by the power of compounding, as you then receive interest on the reinvested payments as well. Currently this option is available for most, but not all, loans on the platform. You can see which of your loans compounding is available for via your Kuflink dashboard.

I have continued to invest in Kuflink, and have also reinvested in new loans when the original ones were paid off. Another good feature is that money invested in a loan but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

There have been no defaults so far on any of my loans, and Kuflink say on their website that to date nobody has lost a penny on their platform. I have experienced short delays with loans being repaid, but in such cases you continue to earn interest, of course.

Secondary Market

A new feature on Kuflink I like is the Marketplace (secondary market). Here you can buy loan parts from other investors who want to sell up early. You can also put up for sale any (or all) of your own loan parts.

The number of loan parts listed in the Marketplace went up in the early months of the pandemic, as many investors understandably wanted (or needed) to access their cash. This created short-term buying opportunities which I was happy to take advantage of. Loan parts offered via the Marketplace typically have only a few months to run, so you can expect to get your capital back quickly (and can then reinvest it if you wish). Only loans in good standing with monthly repayments up to date may be listed on the Marketplace, so that offers some reassurance against default – though of course it is by no means a guarantee.

In recent months the number of loan parts listed on the Marketplace has reduced considerably. And those that are tend to be snapped up quickly. As a would-be investor this is slightly disappointing, but it does indicate that people are keen to take advantage of the opportunities on offer. It also means that if you want (or need) to exit a loan early, accessing your money should be a quick and easy process.

Pros and Cons

Based on my experiences, here is my list of pros and cons for the Kuflink investment platform.

Pros

1. Easy sign-up process.

2. Low minimum investment.

3. All loans secured against property.

4. Choice of investments and approaches.

5. Manual and auto-invest options.

6. Kuflink invest in all loans themselves, so they have a strong incentive to ensure they are safe and secure.

7. They also cover the first 5% of losses on any loan before investors are affected (although this has never happened yet).

8. Money invested but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

9. In-depth information is provided on the website about all loans, so you can see exactly how your money will be used (and by whom).

10. There have been (according to Kuflink) no investor losses to date.

11. Customer service (in my experience anyway) is fast, friendly and helpful.

12. There is a 14-day cooling off period for new investors.

13. Marketplace (secondary market) for buying and selling loan parts.

14. No charges to investors lending on the primary market and only a 0.25% fee if you resell a loan part on the secondary market.

15. On most loans you can opt to reinvest monthly repayments to boost your net interest rate.

16. Tax-free IFISA option available.

Cons

1. Rates paid aren’t the highest in P2P lending.

2. Delays with some loans being repaid (although investors do earn extra interest if this happens).

3. No mobile app [UPDATE FEB 2023 – An app is now available.]

Conclusion

Overall, my experiences with Kuflink so far have been entirely positive and my investments have been generating the promised returns. I started cautiously with them, but have gradually built up the amount I have invested on the platform. Although – like all property P2P platforms – they were adversely affected by the pandemic, they appear to have come through it strongly, with new loans now being added almost daily.

As mentioned above, although Kuflink don’t pay the highest rates in P2P lending, I think the returns on offer are realistic and sustainable. The steady expansion of the platform seems to testify to this, as does the fact that they have received several industry awards. These include Best Alternative Business Funding Provider in the Business Moneyfacts Awards in both 2018 and 2019 and Best Service From an Alternative Funding Provider in 2020.

Kuflink are also highly rated on the independent TrustPilot website, with an average 4.6 out of 5 (‘Excellent’). At the time of writing 82% of reviewers award them the maximum five-star rating, which is among the highest figures I have seen for a financial services platform.

As with all P2P lending, your money does not enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates of return on offer are significantly better than those from most financial institutions. And the fact that all loans are secured against bricks and mortar – and Kuflink themselves have cash invested in them – clearly offers some reassurance.

From my experience, Self-Select loans tend to fill up quickly. On the positive side, this shows investors have confidence in Kuflink and want to invest through the platform. On the minus side, it means there are typically no more than two or three new loans open for investment at any time.

Clearly, no-one should put all their spare cash into Kuflink (or any other P2P investment platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return much higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P loans aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

If you have any comments or questions about this review or Kuflink in general, as always, please do leave them below.

Disclosure: As stated above, I am an investor with Kuflink myself, and if you invest £500 or more via my link above I will receive a bonus for introducing you. Money is at risk. You should always do your own ‘due diligence’ before investing, and seek advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2021, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a very merry Christmas (Covid and the government permitting), and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

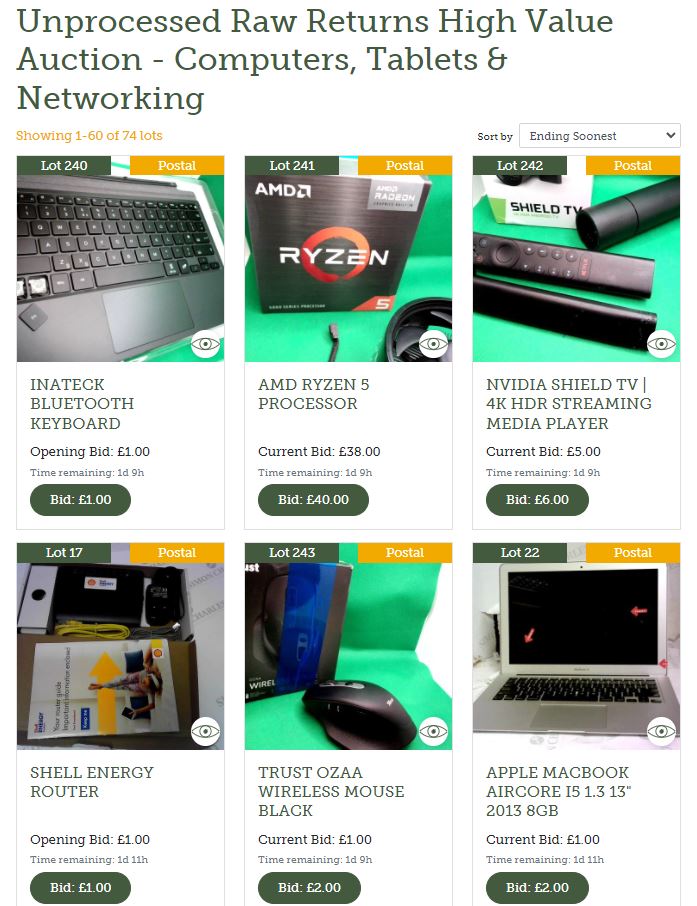

If you like saving money – at this expensive time of the year especially – have you considered shopping at an online auction house?

To be clear, I am not talking about eBay here (much as I love them). Rather I’m talking about more traditional auction houses, who nowadays conduct much or even all of their business online.

An example is Simon Charles. They have four auction centres in the Greater Manchester area and are one of the largest auction houses in Europe. Partly in response to Covid, they now conduct all of their auctions online. Anyone in the UK (or further afield) can therefore bid on them.

Disclosure: I have received assistance with this article from Simon Charles Auctioneers, but don’t have any other connection with them, commercial or otherwise.

Of course, auctions are typically associated with expensive art at one extreme and complete tat at the other. This is not invariably the case, though. While these types of auction houses do exist, there are many that specialize in other areas.

Simon Charles Auctioneers specializes in new, used and returned goods provided to them by high-end retailers. Many of these items are in excellent condition, often still in their original packaging. And with very low or no reserve prices, they can often be snapped up for ridiculously low prices. Here is a screen capture from the Simon Charles website showing some examples…

As you will see, all of the items above have a ‘Postal’ tag at the top right. This means they can be sent by post for a small additional fee. In practice most items sold at SC auctions can be sent by post within the UK. Those that can’t, typically because of their size or weight, are marked for collection only.

In common with other auction houses (and eBay) Simon Charles do impose some additional charges. All lots sold with them are subject to a 18.5% + VAT buyers premium, all lots sold online are subject to 5% + VAT internet fee, and all lots unless otherwise specified are subject to 20% VAT on the hammer price of the item. So it is important to bear these charges in mind when bidding on an item, along with postal costs if you aren’t able to collect your purchase/s in person.

It’s also important to remember that lots sold this way may not be brand new. The products sold at Simon Charles come from high street and online retailers, wholesalers and distributors across the UK. They are in a range of different conditions, from brand new to customer-returned or faulty. They say they don’t always have the chance to test and check items and all products are therefore ‘sold as seen’. But they do have viewing times available to come and check the condition (these times can be found by clicking the Book Viewing button on the auction catalogue or lot page). In these times of Covid, social distancing and masks are required for viewings, which must be booked in advance.

If it’s not possible for you to view in person, they also have an ‘Ask a Question’ feature on each item, so you can gain a better understanding of the product before bidding.

I asked my contact at Simon Charles why they believe buying this way can be better than eBay. Here’s the reply I received: ‘The main benefit of buying from auction over eBay is that our stock tends to be cheaper than eBay. The fact that we’re selling all the stock ourselves means that if you were to buy several lots you could combine shipping, decreasing overall costs. Also, at Simon Charles we work with several large retailers to bring their overstock and returns to auction. These goods aren’t influenced by a price point and can therefore be offered from a much lower amount than someone on eBay might be willing to sell.’

Final Thoughts

I must admit that I had never really thought about buying this way before, but can certainly see the attraction. There are undoubtedly bargains to be had if you are looking for Christmas/birthday gifts or just want to save some money. But I can also see that this method might particularly appeal to small traders looking for stock to resell on market stalls or even on eBay and similar websites. Obviously, if you are a trader registered for VAT, you would be able to reclaim this part of the cost.

In any event, I should like to thank my friends at Simon Charles Auctioneers for bringing this opportunity to my attention. If you have any comments or questions, as always, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

tic a way as he is doing!

tic a way as he is doing!