The world is an expensive place, so it’s no wonder many people are obsessed with getting freebies.

However, when entering the freebie-hunting world it is important that you adhere to certain rules in order to make the most of it. This article will set out some top tips for novice freebie-hunters – and you may learn a thing or two as a seasoned freebie-hunter as well.

If It Sounds Too Good To Be True, It Probably Is

The excitement of (potentially) getting a freebie from a favourite brand can easily cloud your judgement.

According to Karen Newman at Mega Free Stuff, the majority of transactions have both an upside and a downside; however, when a transaction is free the downside is temporarily forgotten. ‘Free’ provides people with a strong emotional charge, where the individual perceives the item on offer to be more valuable than it actually is. This basically means that the person will set aside common sense if they are being offered a freebie.

Some companies are willing to give freebies, but fans of a brand are often willing to sell their soul (or at least provide all sorts of valuable personal information) in exchange for a minute sample. This is detrimental, and it is essential that you know how big the sample is and what exactly you will be getting. Be sure the freebie is genuine and always read the terms and conditions before applying for any offers.

If You Do Not Ask, You Will Not Receive

It is always worthwhile writing letters or sending emails to companies asking if they have any samples available for you to try. This may seem obnoxious and pointless to some, but those who complete this task have often received large boxes of free items or discount vouchers from the companies as a means of gaining feedback on their products. Furthermore, if you do not like a product, be honest about this. In many cases companies are happy to offer replacement freebies (plus an extra item) if their products do not meet with the user’s approval.

Do Not Expect Too Much

A full-sized freebie is a rare occurrence, with the majority of free products being delivered in small envelopes or tiny sachets. Of course, the primary goal is not to obtain a full-sized freebie but a free sample to see if you enjoy the product for a future purchase.

Furthermore, do not expect to receive all free items applied for. Even if you have claimed a free sample noted as available online, it is unlikely that you will get a 100% return. In fact, the most you can expect is approximately 70%. Do not give up hope and keep applying, and soon you will be enjoying masses of freebies. Once again, though, be sure to check that any freebie is worthwhile, and always read the terms and conditions regarding the size and number of samples.

Do Not Feel Guilty

While some individuals may feel a degree of guilt about asking for freebies, this is completely unnecessary. The company sending a freebie is not losing millions of pounds on the free products; in fact, they are benefiting from the free item. Think about it – for every sample sent out, there is the potential of a new customer. If you receive a free sample and like it, there is every chance you will make a future purchase of that product and might even become a regular customer.

Set Up a Second Email Address

One important – but often neglected – tip is to set up a second email address. To avoid receiving spam mail to your primary address, use this second address to claim freebies and enter competitions.

We have found an amazing competition here, where you can have the chance to win one of 20 Lindt chocolate Easter Eggs (see picture below). This competition ends on 1st April 2021.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

In brief, Property Partner is a property crowdfunding platform. For the most part they specialize in ‘traditional’ property crowdfunding rather than loan or development finance.

Properties are bought and managed by Property Partner on investors’ behalf. Investors then receive a share of the rental income as dividends, and a share of any profits (plus return of their capital) when the property is sold.

Property Partner launched in January 2015. That date is significant, because after a property has been on the platform for five years, all investors get the chance to exit at a fair market price (determined by an independent surveyor). Due to the pandemic the five-year anniversary process was temporarily put on hold, but it is now proceeding again, albeit with delays as they work through the backlog.

How it operates is that in the run-up to the fifth anniversary of a property, all investors have the opportunity to say if they want to exit their investment at the valuation price or stay on for another five-year term (less than this if they subsequently exit via the resale market, of course).

All investors who have opted to leave will then have their shares pooled and put up for sale on Property Partner at the price stated. New investors are then able to buy these shares.

So long as all shares are sold, the original investors get their money (including any net profits) and the property continues under Property Partner’s management. If all shares don’t sell, however, Property Partner offer the property for sale on the open market. Investors then have to wait until the property is sold before getting their money back. As anyone who has been involved with buying or selling property will know, this is likely to take several months (quite possibly longer in the current circumstances).

The Opportunity

As Property Partner themselves have been pointing out, a number of properties that are coming up to their fifth anniversary are currently trading on the resale market at well below their latest valuation. Here is just one example:

This property in Tower Hill, London (not one I own shares in myself) is due to go through the fifth-anniversary process in April 2021 (or possibly a bit later due to the backlog). At the time of writing shares are available on the secondary market at a price of 91p, which is 28.28% below the latest valuation of £126.88. In theory, then, you could buy shares now and in the next few months sell up for a substantial short-term gain.

Of course, in practice it’s not as simple as that. Here are some reasons:

Nobody knows yet what the final five-year valuation will be. If it is lower than the current valuation (which is perfectly possible in the current economic climate) the net profit will be reduced, perhaps substantially.

There is no guarantee that the shares of all investors who wish to exit will actually sell on the platform. If they don’t, as mentioned, you could have a long wait before the property is sold on the open market. In addition, if this happens there is no guarantee that the property will sell at the valuation price. If it goes for less than this, your returns will be reduced accordingly.

There are platform fees to take into account. In particular, there is a 1% fee for buying on the secondary market and a further 0.5% stamp duty reserve tax charge. Thankfully there are no exit fees, though.

And finally, the number of shares available for any property on the secondary market is limited. Obviously the number you can buy depends on how many shares other investors want to sell at the price in question.

On the plus side, for the length of time you hold the shares you may receive monthly dividends at a rate between 1.5% and 6% per year (though dividend payments on some properties are currently suspended due to Covid). This will offset the fees mentioned above; but if you only intend to hold the shares for a few months it probably won’t cover them completely. Bear in mind that an Assets Under Management (AUM) fee is now deducted from dividends as well.

As an investor with Property Partner since almost the beginning (the cover image shows a property in Torquay I own shares in – I plan to retire there one day 😀 ), I am awaiting the five-year exit for my investments with considerable interest.

My personal circumstances have changed since I started investing with the platform, so I intend to take the opportunity to offload at least some of ‘my’ properties. Indeed, I have already voted to sell my shares in the first property I ever invested in with Property Partner (20 Phillimore Close) and am waiting to see how this pans out. I will update this post in due course once I know.

Nonetheless, I am still considering investing short term on the resale market to take advantage of the opportunity the five-year anniversary presents. In particular, I have already topped up my investments in some of the properties I already hold but am planning to dispose of.

I will, though, be cautious until I have a better idea how the first few five-year anniversaries have passed, so I can see if all shares put up by investors sell on Property Partner, or if they have to sell the properties concerned on the open market. As mentioned earlier, the latter route will clearly take longer and there is no guarantee what price would be achieved.

Would I recommend someone who is currently an investor in Property Partner to look into this? Yes, certainly. Whatever your current circumstances, you need to be aware of what is going on with any properties you hold with Property Partner. And if you wish to sell, you should definitely consider taking advantage of the five-year exit mechanic. Equally, if you have money available to invest, you could check out the opportunities buying now on the resale market – though do bear in my mind my cautionary comments above.

If you haven’t joined Property Partner, and you like the idea of investing some of your portfolio in property, the platform is certainly worth a look. As older properties come back on the market for new investors, there will be no shortage of opportunities in the months ahead. And my understanding is that, as the original costs of acquisition have been amortised, there will be less costs to cover from investors, thus boosting the potential returns from the properties in question.

In addition, as these properties have a five-year history already, you will be able to check how they have been performing in terms of dividends generated and capital appreciation. This is no guarantee of how well or badly they will do in the future, of course.

Take a look at my Property Partner review for much more information about the platform and how it works. Also, if you do decide to invest in Property Partner, there is a welcome bonus offer. For convenience I have copied details below from my review.

Welcome Offer

As an existing Property Partner investor, I can offer a special bonus for anyone joining via my link. If you click through this special invitation link, sign up and invest a minimum of £2,000 within 60 days, you will receive an extra bonus as follows (and so will I):

Not only that, once you are an investor with Property Partner, you will be able to offer the same bonus to your friends and relatives and earn commission yourself. There is no limit to the number of people you can introduce through this scheme.

If you have any comments or questions about this post, as always, please do leave them below.

Note: This is a fully updated version of a post published in 2019.

Disclosure: this post includes referral links. If you click through and make an investment, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. Be aware that all investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m discussing a subject that will be relevant to any of you who have blogs yourself or are thinking of starting one.

I’ve been blogging for almost twenty years now. I started off blogging about freelance writing and moved on to personal finance with Pounds and Sense. I make money from my blog by various means, but the most important (and lucrative) is through collaborations with businesses and agencies on sponsored posts, sponsored links, and so on.

Companies are always on the lookout for ‘influencers’ who can help get their message across to their target audience. They have budgets for this purpose, but before sending any money your way they will almost certainly want to see your blog’s media kit (also known as a press kit). If you don’t have one – or it’s not up to scratch – you can expect to lose out on many paying opportunities.

So What Goes Into a Media Kit?

As a blogger, your media kit is an advertisement for you and your blog and the services you can offer. It will typically consist of one or two pages you can send (or hand out) to anyone enquiring about potential advertising opportunities or collaborations

A good media kit will ensure you create a strong and professional first impression. Everybody’s media kit is different, but here are some things you should consider including in yours…

Biography

In this section you provide a brief account of yourself, including such things as your age, location, occupational background, hobbies and interests, family, and so on. Companies want to know whom they will be working with, to reassure themselves that you and your blog will be a good fit for their target audience. Let your personality shine through, therefore, quirks and all! You should also include a good-quality portrait-style photo of yourself (see the example in the header image).

Blog Description

In this section you talk about your blog itself – the subjects you cover, your target readership, and any other information that may interest potential advertisers. You may also wish to include your blog’s logo.

Stats

Advertisers want to know the size and nature of the audience you can deliver for them. So it’s important to share some key stats, including such things as total unique views, social media following, email newsletter subscribers, and so forth. Clearly you will want to pick the most impressive-looking stats – so if you don’t have many Instagram followers (for example) just leave that out. But don’t exaggerate either. Clients can and will check your stats, and if they don’t appear to correspond with the figures you have quoted, they are unlikely to want to proceed further

Collaboration Options

Here you list ways brands can collaborate or advertise with you. Some possibilities include:

Sponsored Posts

Sponsored Links

Product Reviews

Contests and Giveaways

Banner Ads

Social Media Campaigns

You can also include prices for these services in your media kit if you like. Personally I don’t do this, as I like to leave room to negotiate over price.

Testimonials

If you have worked for business clients before, I would strongly recommend including any testimonials you may have received. And don’t be afraid to ask for testimonials after a successful collaboration. This type of social proof provides invaluable reassurance for would-be clients that you can deliver on your promises and achieve good results for them.

Contact Information

The most important one of all! Don’t forget to include your contact details so that potential clients can get back to you. You will probably want to include your email address, phone numbers (home and mobile), postal address, and so on.

Media Kit Design

As a blogger you aren’t necessarily expected to have an all-singing, all dancing, media kit, but the smarter and more professional it looks, the better. Your kit should work both electronically (e.g. as an email attachment) and when printed out in colour.

Fortunately you don’t need to be a design guru to produce a great-looking media kit. There are lots of free and inexpensive templates available, which you can edit and personalize to your heart’s content. A great place to look for such templates is the Design Bundles website – just put “Media Kits” in the search box on that website.

Win a Design Bundle!

Here’s a great opportunity to win a media kit template and any other design resources you would like too 🙂

My friends at Design Bundles are running a giveaway to win a prize worth £100. This comprises a £50 credit for Design Bundles to use on Media Kit templates and any other products you’d like from them, along with a four-month premium subscription to Canva. As you probably know, Canva is a brilliant design website you can use to create a media kit and other amazing graphics for your blog as well. You can enter via the Rafflecopter widget below.

Anyone world-wide can enter. All fields are optional, so you can choose which ones you’d like to complete. But obviously, the more you do, the better your chances of winning.

The contest is open now and will close at midnight on Tuesday 26th January 2021. The winner will be contacted by the end of that week to arrange their prize.

Good luck in the giveaway, and with creating an attractive and compelling media kit!

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

In the past buy-to-let seemed a relatively easy way to make money.

So long as you had the capital – or were able to borrow it – you could buy a house, put tenants in it, and collect a steady income from rental payments, along with potentially a lump-sum profit if you sold up at a higher price later on.

In recent years, though, tax and regulatory changes have made buy to let less appealing – to a point where many wonder if there is still money to be made this way. So in my post today I want to address this question.

Let’s start, though, by looking at the upside…

The Attractions of Buy to Let

As stated above, property investors get a double benefit. They enjoy rental income from tenants for as long as they own the property, and also have the potential to make a substantial lump sum profit when the time comes to sell.

A further attraction of buy to let is that your tenants effectively pay off your mortgage for you. So if, for example, you are buying a £400,000 property, you might ‘only’ need to find a deposit of £100,000. As long as your tenants’ rental payments cover your mortgage repayments (with a bit to spare), after 25 years or so the mortgage will be paid off. You will then fully own a second property, having originally paid only a quarter of the full property price. And that doesn’t even allow for the prospect of capital growth. If your property eventually sells for £600,000, you’ll have made an additional £200,000 capital gain.

Of course, you don’t have to borrow to fund your buy-to-let. If you already have the capital you need, investing in a buy-to-let property will provide you with a steady income while the capital value of your property (hopefully) appreciates over time.

Buy to let can also be a good way of diversifying your investment portfolio. Rental income is relatively stable, especially if you have a number of properties and tenants. And property values aren’t directly related to the state of the stock market. So while property doesn’t provide a method for hedging your stock market investments directly, it can certainly help spread the risk.

Of course, property prices took a knock in the 2008 credit crunch and subsequent recession, and more recently were affected by the pandemic (though prices generally are on an upward trajectory again now). In the longer term, though, prices have been on a strongly upward trend since the 1970s. On average, house prices have grown faster in the UK than they have in any other European country.

There’s every indication that prices will go on rising in the coming years as well. The UK currently has a serious shortage of housing, caused by various factors. To start with, the UK population is growing rapidly. This inevitably means demand for housing will go on rising, thereby driving up the price of property. According to the Office of National Statistics there will be an annual shortfall of housing in the UK of over 100,000 properties each year for the next decade. This could mean a shortfall of one million properties by 2025 if current trends continue.

Various factors have combined to boost rental demand, including immigration, more people living alone, people moving around the country for work reasons, and rising house prices stopping first-time buyers getting onto the housing ladder. The latter is obviously challenging for young people, but it’s great news for landlords whose buy-to-let properties are being let extremely quickly, while their rental income keeps increasing. All of the above means that residential property can represent a profitable and attractive investment option.

What Are The Drawbacks?

One obvious drawback for anyone wanting to invest directly in property is that it’s expensive! And if you can only afford a single property, you are taking the risk of putting all your eggs in one basket. To mention just a few things…

There may be periods when you don’t have tenants (voids, to use estate agent jargon). At these times your property will be costing you money rather than making it for you.

Bad tenants are all too real and can be a nightmare for landlords. If they don’t pay their rent, it will take time and money to evict them. And that’s not to mention the costly damage to your property a malicious – or just careless – tenant can cause.

There will be maintenance and repair bills to pay. If something expensive goes wrong – the roof or the central heating boiler, say – the cost of the necessary work may wipe out several months of profits for you.

In general, being a landlord – at least, a responsible one – is a hands-on role. While you can outsource some aspects of managing your property to an agency (for a fee) you will still have to keep a watchful eye on your property and tenants to ensure that your investment is protected.

A further drawback is that property isn’t a liquid asset. Yes, putting your money in bricks and mortar gives you a degree of security – but if you need to access your capital urgently this may be difficult or impossible. Even if you’re able to find a buyer quickly, if the timing is bad you could end up selling at the bottom of the market and making only a small net profit or even a loss.

And there’s more bad news for buy-to-let investors. As I said earlier, legal changes over the last couple of years have made the whole buy-to-let process more costly and burdensome. For one thing, from April 2016 anyone buying a residential buy-to-let property (or second home) has had to pay an extra 3% in Stamp Duty. In some quarters this has been dubbed the Landlord Tax.

Another major legal change has affected landlords who use mortgage loans to purchase buy-to-let properties. Before April 2017 landlords were allowed to deduct all of the interest they paid on buy-to-let mortgages from their taxable income. In effect, that meant they paid tax on their net profit from rentals rather than their turnover. The government decided to change the rules, however, arguing they gave buy-to-let landlords an unfair advantage over ordinary homeowners. So from April 2017 landlords were only allowed to claim relief on 75% of their mortgage interest. From April 2018 that dropped to 50%, and it kept falling by 25% a year until it reached 0% in 2020. It was then replaced by a less attractive tax credit equivalent to 20% of mortgage interest (which was particularly disadvantageous to higher rate taxpayers). All of this has meant that borrowing money to fund a buy-to-let has undoubtedly become less attractive (and profitable) than it used to be..

Other changes affecting landlords have come in too. For example, from April 2018 all new tenancies and renewals have had to be rated ‘E’ or better on their Energy Performance Certificates, with fines of up to £5,000 for landlords who don’t comply. Most recently built homes should qualify for this rating, but landlords of older, less energy-efficient properties may have to spend large sums bringing them up to scratch. And, of course, this all adds to the administrative burden for landlords, even if it is ultimately helping to save the planet!

One effect of all this has been that some smaller landlords have decided that buy-to-let is no longer worth the effort for them, and they are selling up and moving out of the sector.

So Is There Still Money to be Made?

My answer to this is a qualified yes.

There is definitely still money in buy to let, but it is no longer the ‘one-way bet’ it might once have appeared. You should therefore research opportunities carefully and adopt a highly professional and businesslike approach to the whole process.

A key consideration here is ‘yield’. This is the net amount (rental minus costs) you can expect to make from a buy-to-let property per year, as a percentage of the purchase price. Yield can be compared with the interest rate paid on a savings account. By this means you can assess how profitable a buy-to-let opportunity is and whether it makes sense as an investment vehicle. Clearly, if the yield is less than you could get by leaving your money in the bank, there is not much point in investing this way.

The website Totally Money recently analysed data from nearly half a million properties across England, Scotland and Wales, to calculate the buy-to-let yield for each postcode. The results were eye-opening to say the least. They found that buy-to-lets in the top 25 postcode areas were still delivering excellent returns. At the top was Liverpool, where landlords can enjoy 10% yields. Falkirk (9.51%) and Glasgow (8.71%), both in Scotland, came second and third respectively. Even postcodes at the lower end of the top 25, such as Lancaster and Aberdeen, were returning respectable yields of over 7%. All of these are clearly far better rates of return than you could get from a savings account, and you will have an asset that is hopefully increasing in value as well (see below).

Location is therefore a key consideration for any potential buy-to-let investment and must be researched thoroughly. In addition, the best area for your investment will depend on whether you intend to put your money into flats for professionals, student accommodation, family homes, etc. At the risk of stating the obvious, there needs to be solid demand in the area from would-be tenants for the type of rental property you intend to buy.

Of course, while it’s very important, yield/income potential isn’t the only consideration for property investors. In the longer term you will likely be hoping for capital growth as well – so ideally you should be looking to invest in properties in up-and-coming areas rather than those in long-term decline.

Getting Started

Having weighed up the pros and cons, if you do decide that buy-to-let is right for you, here are some top tips to get you started…

Speak to a professional independent financial adviser to discuss your plans. They will help you decide how much to invest and the level of return you should realistically be aiming for.

You should also speak to a mortgage broker to find out what deals are available and ideally get approval in principle for a mortgage. This means you will be well placed to make an offer as soon as you find a suitable property.

If there is a particular area you are considering, visit several times to get a feel for the place. That applies especially if it’s a location you’re not already familiar with. Check out the housing stock, public transport, car parking, shopping and schools, hospitals, and so on. Try to speak to other landlords in the area and local letting agents to get an idea of the size and nature of the rental market and the sorts of rentals that may be achievable. Always remember that the bottom line for any buy-to-let investor is return on capital or yield.

Once you find a potential property (with or without existing tenants) research it carefully as well. Obviously before buying you will need to do all the usual searches and a structural survey. As with all property sales, you can expect this process to take several months to complete.

Arrange insurance for your buy-to-let. Along with the usual buildings insurance, you should almost certainly have landlord insurance to protect you from financial losses associated with renting out a property. This will typically cover such things as fixtures and fittings, public and landlord’s liability, subsidence, replacement of windows, locks and keys, and so forth. It will also normally cover malicious damage caused by tenants, along with rent arrears and legal expenses (though the last two may not necessarily be included as standard). You can compare landlord insurance here.

To find tenants you can either go through an agency or do this yourself. Obviously going through an agency will add to your costs but can save you a lot of hassle, especially if you haven’t the time (or inclination) to be too hands-on.

Even if you pick your own tenants – and perhaps already know them personally – draw up a legally-binding contract. That means everyone knows where they stand from the start and can help to avoid potential unpleasantness later on.

Review your buy-to-let mortgage arrangements regularly and be prepared to switch to a better deal when your current one expires.

Ensure that your rental income is declared in a tax-efficient way and set against any allowable expenses. A good accountant will be able to help with this.

Your accountant will also be able to advise you about the pros and cons of running your buy-to-let through a limited company. This comes with additional costs (and paperwork) but for landlords of multiple properties in particular the tax benefits can be significant – not least because you can claim all the interest paid on your buy-to-let mortgage/s against income rather than just 20%.

And finally, once your first buy-to-let is up and running successfully, consider adding more. Multiple properties will give you a bigger income and will also reduce the risk inherent in putting all your eggs in one basket (as discussed earlier).

In Conclusion

If you’re considering buy to let, I hope this article will have helped you make up your mind. There is undoubtedly still money to be made this way, but you do need to choose your location and property carefully, and approach the whole process in a professional and businesslike way. That applies from the initial planning stage right through to the day-to-day – and year-by-year – management of your property.

As ever, if you have any comments or questions about this post, please do leave them below. I would also be very interested to hear from any readers who have invested in buy-to-let themselves, along with any tips (or warnings!) they would like to share.

Disclosure: this is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

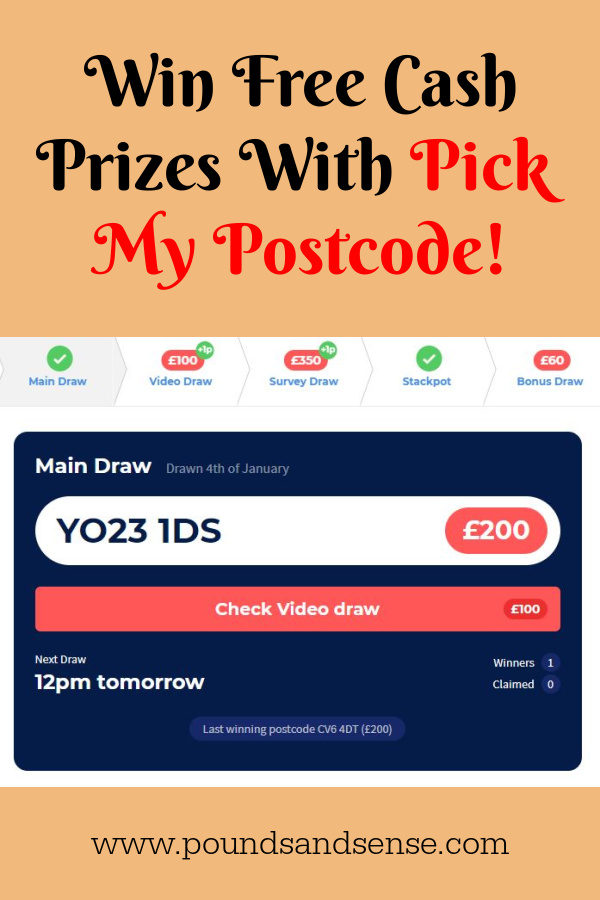

Today I’m highlighting a fun and free way you may be able to boost your income in 2021. And all you have to do is check the website in question once a day to see if your postcode is a winner!

Main Draw Each day one postcode is picked at random for this draw, which has the biggest prizes. The main daily prize – which I was lucky enough to win – can be over £1,000. When I had my own win, the prize was £1,200, though as one other person in my postcode area also claimed, the prize was split between us. So I got £600 plus a small bonus (explained below) – not a life-changing amount, but certainly a day-changing one 😀

Video Draw – To see the winning postcode in this draw, you first have to watch a short video. Though to be honest I find that you just have to watch the ad that plays first and the winning postcode is then displayed – you don’t have to watch the whole of the video unless you want to. This draw pays a minimum of £50, with the prize rolling over to the next day if not claimed. I have seen up to £400 on offer in this draw.

Survey Draw – To see if you have won this draw, you first have to complete a very short survey (generally just one question). As with the Video Draw there is a minimum prize of £50 and it rolls over to the next day if unclaimed. When I checked today there was a £300 prize, so it must have rolled over for a few days previously.

Stackpot – The Stackpot lists a variable number of postcodes with £10 prizes for those claiming them. When I checked this morning there were 14 prizes up for grabs and one that had already been claimed (it is first come, first served with the Stackpot).

Bonus Draw – With the Bonus Draw there is a daily £5 prize, £10 prize and £20 prize. To be eligible you need to have built up a Bonus (see below) equal in value to the prize in question by visiting the site regularly. So to qualify for the £20 Bonus Draw, you need to have accumulated a Bonus worth at least £20 yourself.

All lottery prizes are tax-free, of course, in accordance with UK gambling laws.

One is £5 Flash Draws. These appear at random on advertising spaces around the PMP website. They look like the sample image below. They appear to individual visitors at random. I have never seen one myself, but obviously it’s worth keeping an eye out for them. If you spot one, you just have to click to claim (it doesn’t matter about your postcode). The £5 prize is paid by PayPal as usual.

As for the Bonus, this is a sum of money that is added to your prize any time you win (with the exception of the £5 Flash prizes). It accrues over time as you visit the site. It increases by 1p for every new Main Draw, Survey Draw or Video Draw that you check. That may not sound much, but if you return to the site every day it soon adds up. My Bonus is up to £41.90 now!

If you wish, you can boost your Bonus even more by referring friends and neighbours and taking up some of the offers that appear on the site.

It’s important to note that you can’t withdraw your Bonus until you win a prize. But even £10 in the Stackpot or £5 in the Bonus Draw will qualify. So if I were to win a £10 Stackpot or Bonus Draw prize today, I would actually receive £10 plus £41.90 = £51.90. Another good feature is that your Bonus is added to your winnings every time you win a prize – it doesn’t reset to zero after a win.

I am not normally a great one for lotteries, but I make an exception for Pick My Postcode. As I said above, it’s free to enter, there are loads of prizes on offer, and the longer you go on playing, the bigger those prizes can become. And obviously, having previously won over £600 on the Main Draw myself, I know that it’s genuine and would love to win again!

Finally, if you still need further reassurances about the site, check out the reviews on the independent Trust Pilot website (average 4.8/5 stars, with 94% of people rating it ‘Excellent’).

As always, if you have any comments or questions about Pick My Postcode, please do leave them below.

Disclosure: This post includes my referral link. If you click through and sign up for free, I will receive a small commission for introducing you. This will not affect your potential earnings in any way.

If you enjoyed this post, please link to it on your own blog or social media:

Happy New Year! Here’s hoping it’s a better one for all of us than the year just past 🙁

I shall be continuing my monthly coronavirus crisis updates in 2021, at least till we are clearly over the pandemic and something resembling normal life has resumed. Obviously I very much hope that will be sooner rather than later.

Regular readers will know I have been posting these updates since the first lockdown started in the spring of 2020 (you can read my December 2020 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

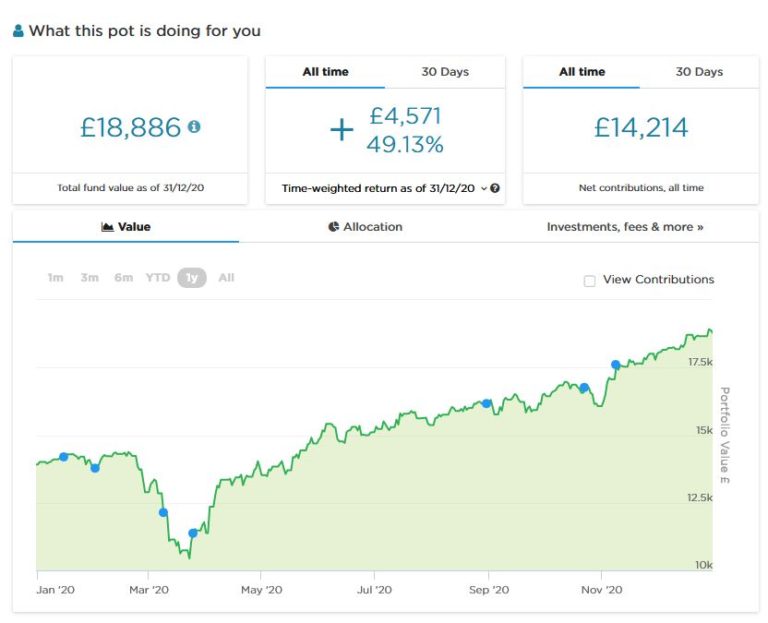

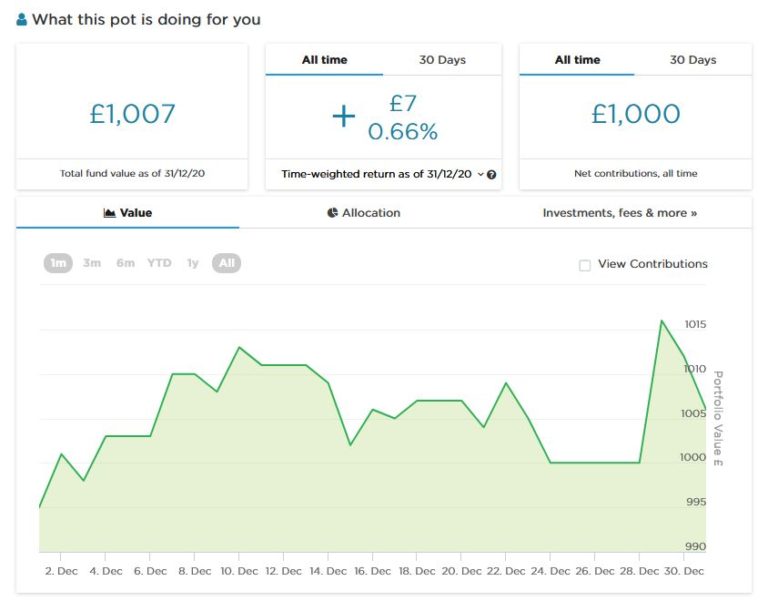

As the screenshot below shows, since last month’s update my main portfolio has continued on a generally upward trajectory and is currently valued at £18,886. Last month it stood at £18,008, so it has gone up by over £800 in value since then. Considering national and world events at the moment, I am more than happy with this.

As you may recall, about a month ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. This pot has risen as high as £1,015 in value and currently stands at £1,007. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

You can see my in-depth Nutmeg review here (including a special offer for PAS readers). As a matter of interest I was recently asked by Nutmeg to contribute an article about my investing journey for their blog. I will add a link to the article here once it is published.

I had some bad financial news last month from Crowdlords, one of the property crowdfunding platforms I invested with. Three years ago I put £3,000 into a development project to build what was originally described as six eco-homes (it has lately been known more prosaically as Kennington Road). An update on the Crowdlords website revealed that due to a ‘perfect storm’ of problems caused directly or indirectly by the pandemic, the development had made a loss and investors would receive no returns. At a stroke I lost £3,000, which was (as you may imagine) a bitter pill to swallow.

I plan to write a more in-depth post about this soon, including lessons learned from the experience. But i will say two things now. One is that property development projects are inherently very risky and you shouldn’t invest in them unless it really is money you can afford to lose in a worst-case scenario. And second, while I don’t blame Crowdlords themselves for the failure of this project, I do think their communications about it could have been a lot better. I also think it would be a nice gesture if they were to offer modest ex-gratia compensation payments from their own profits to investors who have been hit hard (I know some people lost a lot more than I did). Events such as this clearly damage the reputation of property crowdfunding and mean investors are less likely to risk their money this way in future. I know I shall certainly be a lot more cautious now!

In fairness to Crowdlords I should add that I have had other investments on their platform which did deliver the promised returns, However, with the loss described above I am certainly down overall with them.

On a brighter note, a couple of the loans I invested in with Kuflink were repaid (with interest) last month, and I duly reinvested the money in other loans.

Kuflink is primarily a platform for investing in bridging loans, and generally these are safer than development projects such as the one mentioned above. There is still a risk of loss, of course, but as your investment is secured by bricks and mortar, it is unlikely you would lose all your money (though delays in repaying loans can and do happen). I have a diversified portfolio of loans with them paying annual interest rates of 6 to 7.5 percent. These days I generally invest a few hundred pounds per loan at most (and quite often under £100). My days of putting four-figure sums into any single property investment are definitely behind me now!

As you may be aware, I recently updated my full Kuflink review. You can read it here if you like. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money on the platform. I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently.

As you may remember, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website.

Finally, I am still getting a few queries about the low-key matched betting opportunity mentioned in some previous updates. I checked with my contact there and they are still accepting new members, but for reasons related to the pandemic have had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you won’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note though that this opportunity is only open to trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

December was another strange month in a depressing year.

A week before Christmas I had my 65th birthday. Normally reaching that landmark would be cause for celebration, but inevitably in the circumstances it was low key. I did at least manage to meet up with a couple of old friends for a birthday tea (don’t tell Matt Hancock!). It was great to see them and they did their best to make the occasion feel special. We had some laughs and a very nice cake, but it still wasn’t anything like I might have imagined my 65th. I didn’t even have the small consolation of being able to start claiming my state pension, as I am in the cohort of people for whom the age has just been raised to 66.

Work-wise it has remained very quiet (as you probably know, I’m a semi-retired freelance writer/editor). I’ve had very little paid work since the pandemic started and was grateful to receive further financial support from the government’s SEISS scheme. This time round you had to state that your income had been directly affected by the pandemic. I did agonize a bit over this, as it begged the question of how much money I would have been earning if things were normal. I honestly don’t know the answer to that, but it seems to me that the pandemic and government counter-measures have stopped the economy in its tracks, meaning there is less work around generally. Anyway, I applied and was paid without quibble.

The main good news over the last few weeks has concerned the vaccines. Two are now approved, with the Pfizer vaccine being distributed since before Christmas and the Oxford-AZ version coming on stream this week. One benefit of turning 65 is that I have presumably moved up the pecking order to receive it.

The government appears to be pinning all its hopes on vaccines bringing this pandemic to an end by spring/summer. I hope they are right, as the next couple of months in particular look pretty grim. At the time of writing my area has just moved to Tier 4, which effectively means lockdown. So I will have little/no opportunity to see friends or relatives, no more swimming, no more trips away, and the prospect of sporting ‘lockdown hair’ again. But I am still lucky compared to many, I know.

In my blog post Surviving the Covid Winter I mentioned some plans I had for getting through the winter months. In December I started several of these. In particular, I began a couple of DIY jobs I had been putting off. One of these was redecorating the en suite. Initially I planned just to repaint one wall where the paintwork was fading. But the new paint colour didn’t match the old one, so I am now planning to repaint the rest of the room as well. As is so often the case with DIY, what appeared a small job at first has grown into a much bigger one!

I have also taken my first tentative steps in the world of video gaming (my experience prior to this had been limited to Space Invaders/Asteroids and the games bundled with MS Windows such as Solitaire). With some trepidation I signed up with the games platform Steam and downloaded Coffee Talk to my Windows laptop. This was a game I had read about some time ago and liked the sound of. Here’s a typical scene from it…

Coffee Talk is actually more like an interactive movie or novel. You take the role of owner/barista at a late-night coffee shop in an alternative Seattle frequented by a mixture of human beings and mythological characters such as elves.

Mostly your customers chat with you and other customers about their lives and problems, while you prepare coffee and other drinks for them. This isn’t especially taxing, though I was quite pleased when one of the regulars, Freya, returned and asked for ‘the usual’ and I remembered what it was. It’s a pleasant enough way of spending a few hours, though I am thinking I might try something a little more ambitious next time 🙂

On the TV side, I finally finished the box-set of Deep Space Nine, which I very much enjoyed and recommend to any sci-fi fans among you. At the recommendation of my sister Annie (also a sci-fi aficionado) I have now purchased the box-set of Babylon Five. This is also set on a space station, though with quite a different vibe from DS9. With five (long) series, six full-length feature films, a spin-off series called Crusade, and various other extras, hopefully this will see me through to the end of the pandemic 😀

And for a change from sci-fi I also bought the box-set of Agatha Raisin, a tongue-in-cheek detective drama starring Ashley Jensen and set in the Cotswolds. I wasn’t sure about this at first, but after the first couple of episodes I thought it hit its stride, and I recommend it for a bit of amusing escapism with some gorgeous countryside settings. It’s only a shame that all three series are quite short.

Finally, as a Christmas present for myself I bought the DVD of Roger Waters’ Us + Them concert. This is an epic production, featuring a group of hugely talented musicians and some awesome visual effects (at one point a giant model of Battersea Power Station descends into the arena, accompanied – of course – by a flying pig).

Roger and his band play a selection of Pink Floyd classics alongside some of Roger’s solo compositions, all of which are excellent as well (The Last Refugee is particularly poignant). In the video below, though, they perform Time, one of my personal favourite Pink Floyd numbers. Check out Jess and Holly (aka Lucius) supplementing their backing vocal duties with some exuberant drumming!

So that’s it for now. I do hope you are staying safe and sane in these challenging times. Be kind to yourself and to others, and hopefully things will improve before too long. As ever, if you have any comments or questions, please do share them below.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2020, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a happy, Covid-free Christmas, and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a Q and A for you with my fellow money bloggers at MoneyNerd.

MoneyNerd is a UK personal finance blog that aims to help people learn to manage their finances and tackle debt. I asked a number of questions about personal finance and debt, and added my own thoughts as well. Our answers are also being shared separately on the MoneyNerd blog. I hope you find them interesting and informative.

What’s your number 1 financial tip?

MN: It’s hard to give advice that would apply for everyone, because everyone’s finances are different. But I would suggest ‘write it down’, as a fairly universal and important financial tip. Start with your financial goals, then write down the steps you’ll take to get there according to your budget. A lot of people have good financial intentions, but without having clear goals on paper, it’s easy to get led astray.

PAS: Agreed. I would also say, keep on top of your money. Know what’s going in and what’s going out every month, and budget accordingly. Always be on the lookout for ways you can maximize your income and minimize your expenditure. And try to put some money aside for the proverbial rainy day. Everyone should really have at least three months’ worth of income set aside in case of emergencies. Sorry, that’s at least three tips, I know!

What do you think are the main causes people find themselves in financial difficulty?

MN: I think financial difficulties are mainly caused by unforeseen life-events, such as bereavement, unemployment, and relationship breakdowns. These kinds of bumps-in-the-road can severely throw people off course, particularly if their financial situation was fragile in the first place. Unfortunately, all three of these examples have sky-rocketed due to the pandemic, and many people in the UK will be facing financial difficulties over the coming year.

PAS: Not much I can add to that. Although sometimes failing to monitor your income and expenditure closely enough can lead to debts mounting up before you realise it.

What personal finance tools do you currently use to track and manage your money?

MN: I’m quite old-school and still use spreadsheets for a lot of money-related things! There are some good apps out there though – Money Dashboard is a particularly good one.

PAS: I am the same and use spreadsheets a lot. I started with Microsoft Excel, but these days mainly use Google Sheets. As regards personal finance tools, I like Snoop [referral link], a relatively new app that helps you keep track of your finances and suggests easy ways you can make savings.

Any tips for people coming to financial management later in their lives?

MN: It might be a little harder to undo old habits and reinstate new ones if you’re approaching financial management from an older perspective. So start by setting simple goals, and work at them consistently. It’s probably worth taking a little time to assess what’s important to you right now, too: what range of outgoings does your money need to cover in later life that you didn’t need to consider before?

PAS: I am 64 and have friends in their seventies and eighties, so I have seen the sorts of problems older people can face. In particular, so many aspects of our personal finances are dealt with online now, from banking to applying for state benefits. The pandemic has probably accelerated this trend.

Many older people struggle with the technology and it’s often not as intuitive as it should be, especially for those whose eyesight isn’t as good as it once was. So I would say to any older people, try not to get left behind by technology, and ask younger friends and relatives for help when needed. Last year a group of us clubbed together and bought a friend (a retired builder) a Chromebook for his 80th birthday. He had never engaged with computers or the internet before and I must admit I was expecting him to struggle at first. However, he took to it like a duck to water, and was soon ordering tools and components online from a local builders merchant. So even old dogs can definitely learn new tricks!

2021 is going to be tough for many. Do you have any advice on how to keep things under control?

MN: I’d start with the obvious – plan as much as possible, in order to save as much as possible. This is so that when those ‘bumps-in-the-road’ come along, you have some kind of safety net, however small. Unfortunately, however, I imagine a lot of people will do everything right this year and still fall into difficulty. As and when that happens I would say be proactive in reaching out and seeking help. There are plenty of free services and helplines to reach out to, before matters spiral.

PAS: Yes, definitely. As I said earlier, everyone should have a financial safety net to tide them over when life throws you a curveball.

In my earlier career I worked as a debt counsellor at a citizens advice bureau, so I know that there is lots of help out there if you ask for it. And friends and family can be a good source of practical and emotional support too. Just don’t bury your head in the sand and pretend to everyone that nothing is wrong.

What would be your top tip for someone who is worried about a debt (or debts) they can’t repay?

MN: I have two tips: the first is don’t panic, the second is be proactive. If you can’t afford the repayments for a loan or credit card, contact the company and explain your situation. If you’re struggling to meet the repayment amounts, you may also need to look at whether a debt solution is appropriate for you. Having unaffordable debt can be a scary place in which to find yourself, but by taking action you can dissipate some of that anxiety by feeling you are doing something about the problem.

PAS: Yep. It’s worth bearing in mind also that if you have a debt you can’t repay, it’s not just your problem, it’s a problem for whomever you owe the money to as well. It is therefore in their best interests to work with you to find a method for paying down the debt.

What are some good ways of boosting your income?

MN: Ask yourself: do I own anything I could rent? A parking spot, a vehicle, a garden shed, even a room in your house if you own it. Then ask yourself: do I own anything I could sell? Old clothes, a bicycle, old furniture, anything in storage. Then finally, ask yourself what you could do with your spare time: dog-walking, Uber-driving, delivering takeaways/parcels, painting and decorating,completing online surveys, match betting, free-lancing, etc. I have a whole blog post which goes into this very topic in more detail: Making Money – Tips and Tricks.

PAS: Lots of great ideas there. Like MoneyNerd, I also have a section of my blog devoted to ideas for boosting your income. I like online surveys, with Prolific Academic (a website needing people to take part in academic research) a particular favourite. And I do matched betting as well, though not as much as I used to, as I’ve been restricted (or gubbed as we say in MB’ing) by many of the leading bookmakers!

What is the best way you can help a friend or family member who has debt problems?

MN: Honestly, I don’t think there’s a one-size fits all here. Everyone and everyone’s debt problems are different. But that seems like a cop-out! So I think showing genuine, non-judgemental support, and ensuring they have all the right resources (StepChange, CitizensAdvice, etc.) to hand are two good places to start.

PAS: I agree with this. But based on personal experience with a friend a few years ago, I would also advise thinking hard before lending them money, as this seldom solves the problem and may simply exacerbate it. With my friend, who lived alone, I found that acting as a lender to him changed the nature of our friendship, and not for the better. I also felt that by constantly bailing him out, I was allowing him to avoid addressing his money management issues. Eventually we had a difficult telephone conversation when he asked me to lend him money again and I refused. He took it better than I expected and our friendship actually returned to something more normal after that. He got his finances under better control, although I did on a couple of occasions afterwards send him supermarket vouchers to ensure he had enough to get food. I didn’t expect to be repaid for these, obviously!

If you had a sudden, unexpected windfall of £5,000, what would you do with it?

MN: Firstly I’d pay off any loans or outstanding credit card debts. Then I’d take my family out for a nice meal, and put what’s left-over into a tax-free ISA.

PAS: Paying off debts would be my first priority as well, though I am fortunate not to have any at the moment. I would put most of the rest in my Nutmeg stocks and shares ISA, and some in my Kuflink property loan investment account (from which I have had good results over the last three years) to provide a bit of diversification. Going out for a nice meal with family and friends sounds good too, although as I live in a Tier 3 area I might have to wait a while for that!

What was your best-ever financial decision, and what was your worst?!

MN: My best financial decision was investing in a tech based stocks and shares ISA which has done really well over the last 5 years, although don’t know if I’d recommend the same investing approach in the current economic climate.

On the other hand my worst financial decision was living in London for 10 years where rent and cost of living is exorbitant.

PAS: My best financial decision was probably paying off the mortgage when I had a windfall a few years ago. At a stroke one large item of monthly expenditure was gone, giving me greater financial flexibility as well as saving me a lot in future interest payments.

My worst decision was investing too much in property crowdfunding a few years ago when it was still new and exciting. I had money to invest at the time and liked the idea of owning stakes in a portfolio of properties across the UK. Some of my investments worked out but others didn’t, and I am currently sitting on a number I can’t access because the properties in question can’t be sold for one reason or another. The money is still there in bricks and mortar but I have no idea when or how I will be able to access it. That said, I do still believe in the property crowdfunding concept, but I do it a lot more selectively now.

About MoneyNerd

MoneyNerd.co.uk is a personal finance blog that was set up with one aim in mind: to help people learn how to manage their finances and tackle debt. The blog includes a variety of straight-talking articles that cover personal finance topics from credit card guides to mental well-being tips. These can help you understand exactly how financial products work, as well as what your rights are when dealing with debt. We want to offer authentic and truthful information that can help you deal with your situation, whatever that may be.

Many thanks again to MoneyNerd for their insights. Please do check out the MoneyNerd site for much more information about tackling debt and getting your finances under control.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

In my previous article I talked about setting up as a consultant and how this can be a great way to capitalize on your work-related skills and experiences.

I discussed the range of opportunities for self-employed consultants and how to research the market and establish a strong personal brand. This time, I’ll be focusing specifically on how to market your consultancy business.

I’ll start with a time-honoured method…

Using a Mailshot

This is the traditional approach to marketing a service to businesses and still has many attractions. You will need to compile a list of potential clients you wish to target, perhaps using business directories and/or the internet. It is then a matter of putting together a package including a letter and maybe a brochure as well, along with any other enclosures you deem appropriate. A reply-paid envelope, for example, will often boost response rates.

The more modern approach is to use email. This has various advantages, the most important being that it is quicker and cheaper. Email marketing is typically used for establishing initial contact with a prospective client, to be followed up with written information and/or a phone call if any interest is expressed.

This method does have the drawback that you may not be able to find email addresses for all the businesses you want to target. In addition, many business people are inundated with emails, and other things being equal are less likely to read them than messages that arrive in the post (and if they have spam filters, they may not see your email at all). Nonetheless, when you are starting out, an email campaign has much to recommend it, and there is nothing to stop you following up with a mailshot and/or phone call later.

The Seminar Method

This can be a great way of making money as a trainer, and it can also help you land consultancy clients. Right now, due to anti-Covid measures, it is difficult to apply in the traditional way. Sooner or later, however, normal times will return and these measures will be relaxed. So I will set out the bare bones of the seminar method here.

The idea is that you arrange seminars or training sessions in your specialist subject, typically lasting a day or half-day. You book a room in a hotel or conference centre for this purpose and advertise your seminar through emails and/or mailshots sent to likely prospects.

A reasonable target for your first seminar would be 10 to 20 clients. You would need to pay the hotel a room hire fee of £50 to £100, and there would also be some publicity and promotional costs. An initial budget of around £400 would probably cover all of this.

If your clients pay £100 each, with the numbers mentioned you would be looking at a gross return of £1000 to £2000. Assuming – as mentioned above – you spent £400 on setting up and running the seminar, that would leave you £600 to £1600 clear profit.

That’s not a bad return in itself, but the big attraction is that if some clients are impressed by your expertise, there is every chance they will want to engage you for other services as well, from in-house training to mentoring and consultancy. If this becomes an ongoing arrangement you will have a source of regular income, and may be able to charge a monthly retainer for your services as well.

The seminar method is an under-used approach among trainers and consultants, yet it has huge money-making potential. While it would be difficult to apply at the present time, you could certainly adapt it to the online world (see below). For example, you could set up an online seminar using video-conferencing software such as Zoom or GoToMeeting. You could even create a web-based course in your specialist subject using a service such as Teachable.

Either way, in addition to whatever fees you charge, you would be building a pool of potential clients for your consultancy service as well.

Online Marketing

The internet is, of course, a massive boon for entrepreneurs. Used the right way, you can attract a never-ending stream of clients and potential clients by this means.

As I said last time, your website is an essential tool for this. If you take the time to create a good-looking site with quality content, in time you can expect to start attracting search-engine traffic. In other words, people looking for a consultant or trainer in your niche will see your site listed high in their search results and hopefully click through to find out more.

It will take a bit of time for your site to be listed in the search engines, and longer still for it to achieve a high ranking for your target keywords. You can, however, assist this process by using search engine optimization (SEO). This is a huge topic in itself, and I recommend looking online for more information. Search Engine Journal is a good place to start.

Here, though, are a few basic SEO tactics you can use to start boosting your rankings…

Share links to your site on social media such as Facebook, Twitter and Instagram.

Comment on blogs and websites relevant to your field of expertise, with links back to your site. You could offer guest posts to the owners of these sites as well.

Add a blog to your website, in which you talk about relevant issues and share helpful tips.

Join online forums and put a link to your site in your signature text (not all forums allow this, though, so check their guidelines first). Put a link in your email signature as well.

You could also consider self-publishing a short ebook on your specialism and give it away free from your site and/or sell it cheaply as an Amazon Kindle ebook. Again, link from your ebook back to your website. Not only will this assist with your search engine ranking, it may also bring you some clients directly.

SEO can work well over time, but if you want to get up and running faster you could consider paid advertising. One method that can bring results very quickly is Google Adwords. These are the small ‘Ads by Google’ that appear in search engine results and on related websites.

The method generally used to charge for these ads is ‘pay per click’ (PPC). In other words, you pay a set sum to Google every time someone clicks on one of your ads. You can choose the keywords that trigger your ads, and set a maximum you are willing to pay for them. The more you bid, the more prominently your ads will be displayed.

Google Adwords is a powerful tool for bringing targeted prospects to your website. For more information and to sign up, visit www.google.com/adwords.

Finally, there are websites where you can advertise your services and connect with potential clients. Job auction sites such as Guru and Upwork are one possibility, with many thousands of projects posted by would-be clients. You are unlikely to be able to earn top rates via these platforms, however. There is a lot of competition, and as they are international you will be up against people in low-wage economies whose overheads (and fee expectations) may be much lower than yours. If you are looking to gain experience and testimonials they may be worth trying, but they shouldn’t be your first port of call.

A better bet may be sites aimed specifically at connecting consultants with potential clients. One of the more established websites in this field is The Consultant Hub. Joining costs several hundred pounds (tax deductible, of course), but for that you get access to thousands of unadvertised consultancy opportunities, an individual profile page on the website, membership of a private online forum, and access to training and networking events.

More Top Tips

Finally, here are a few more tips for building your training and consultancy business…

Prepare a short pitch that answers the common question, ‘What Do You Do?’ Try to have a core message that can be summed up in one sentence, e.g. ‘I help small business professionals promote their products and services to people who need them.’

Keep up to date with your specialist subject. Join the relevant professional organization/s, read the latest books and journals, and subscribe to authoritative blogs and websites in your niche.

At the end of any training or consultancy session, ask for feedback. Not only will this give you valuable information on areas where you can improve, positive comments may be useful for testimonials (with the client’s permission, of course).

Listen carefully to what clients tell you about their businesses and any areas where they are having problems. This is priceless market research, and may suggest new services you can offer in future.

Build links with consultants and small businesses with expertise in areas related to yours. For example, if your specialism is copywriting, you might want to link up with a graphic design agency. As well as helping your clients by introducing them to other professionals with skills they need, you may be able to negotiate referral fees.

Keep in regular touch with clients, and let them know about any new services you may be offering. Typically 80% of your business will come from repeat clients, so be sure you stay on their radar for the next time they need someone with your particular expertise.

In Conclusion

Selling your skills and knowledge as a mentor, trainer or consultant can be both enjoyable and lucrative. You can work from home, and full-time or part-time as you prefer. This can also be an ideal opportunity for older people who may be looking to reduce their working hours while still earning a decent income.

The work is varied and interesting, and you will have the satisfaction of sharing your skills and experience with people and businesses who can benefit from them. And with many companies relying increasingly on freelancers to help keep overheads low, there has seldom been a better time to get into this field.

Good luck, and happy consulting!

Disclosure: this article includes some affiliate links. If you click through these and make a purchase, I will receive a commission for introducing you. This will not affect the service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

In this two-part article I’ll be looking at a method almost anyone can use to make money, by selling their skills and knowledge as a mentor, trainer or consultant.

I say almost anyone, because clearly you need some skills and knowledge other people would be willing to pay you for. There is a huge range of possibilities, however, and if you have worked in any skilled, professional or managerial position, you almost certainly have knowledge and abilities you could sell – possibly after some polishing up first!

You can offer your services to private individuals (I’ll look at this in a moment) but by far the biggest and most lucrative potential market is businesses (including public sector organizations such as the NHS). They have budgets for training and consultancy, and generally pay well if you can deliver the services their managers and employees require.

To give you a flavour, here are just a few areas for which mentors, trainers and consultants are much in demand…

Health and Safety

Equal Opportunities

Marketing

Business Law

Salesmanship

Accounts and Financial Management

Planning

Copywriting

Computers

Leadership

Communication

Graphic Design

Social Media

One big advantage of working with businesses is that if all goes well, you are likely to be invited back in future, either to follow up your initial session or to train other staff. Also, one type of job can lead to another. For example, you might run a course for a client initially, and then be asked to provide ongoing mentoring or consultancy services.

Although businesses are your most likely clients, in some fields you could work with private individuals as well (or alternatively).

One example is computers. Many people struggle with mastering their home computers, and are willing to pay for help and instruction. If you can combine this with basic repairs and maintenance, you have the basis for a steady part-time or even full-time business. Admittedly it is unlikely to pay as well as working for business clients, but may suit some people better.

Business Basics

If you are going to offer any sort of training or consultancy service, even part-time, you will be regarded by the authorities as running a business. That means you will need to contact the tax authorities (HMRC in the UK) and let them know what you are doing.

You will also need to keep accurate financial records showing all money earned and any allowable expenses (stationery, advertising, phone bills, and so on). You or (more likely) your accountant will use these records in due course to produce annual accounts, which will determine how much tax you have to pay.

My personal advice would be to speak to an accountant early on and get his/her advice on how best to keep your books (financial records). This can save you a lot of hassle – and expense – later.

I don’t have space here to go into detail about the nuts and bolts of setting up in business, but there are many books on this subject available. You might also want to take a part-time college course if any are on offer in your area.

As always, the internet is a great source of information as well. Startups and the government’s business website are two very useful resources, but there are plenty of others. Just enter “Starting your own business” in any search engine to find more.

Marketing Yourself

Marketing is the key to making money in this field, so in the remainder of this post I will concentrate on this subject.

Contrary to what is sometimes believed, marketing isn’t the same as advertising. It is an approach or even a philosophy for doing business.

The marketing method involves finding out what potential clients need, and then setting out to meet those needs. This is important, as what you believe potential clients need may not always correspond with the reality.

Advertising (trying to persuade potential clients you can meet their needs) is therefore one aspect of marketing, but it’s far from the whole story. The first stage of marketing is market research, so let’s start there…

Market Research

If you’re planning to set up as a freelance trainer/consultant, it’s important to spend some time researching your chosen field to discover what exactly potential buyers might be looking for.

This will help ensure you pitch your offer correctly, and may also uncover additional niches you want to target. So it is well worth spending a bit of time on your preliminary research rather than jumping straight in.

There are various ways of doing market research, many of which can be performed from your desk or a library. One is researching what other people working in this field – your potential competitors, in other words – are offering.

This is easy to do on the internet. Put yourself in the position of a would-be client and do the sort of search query you might expect them to use: “leadership training”, for example. That should bring up a range of websites belonging to training and consultancy providers. Spend some time studying what these folk are offering and how they promote themselves. You might also want to make a note of how much they charge, if this information is given.

It’s also good to research what potential clients actually want. This isn’t quite so easy, but one way is to look on job auction sites such as People Per Hour and Guru. Businesses use these sites to post details of services they require, which freelancers then bid on. Look for companies advertising for help in your chosen niche, and see how they describe their requirements and the sort of assistance they are seeking.

It is also well worth contacting at least a few potential clients directly. If you have friends or former colleagues in business, for example, tell them what you are planning to do and ask for any advice they can offer. Most will be delighted to help, and you will also be alerting them to the fact that before long you will be available for work in this field.

Another method I have seen used successfully is to mailshot a range of potential clients with a market research questionnaire, and promise to make a donation to a specified charity for every one that is returned. This will obviously cost you a bit of money, but the information you get back will be valuable to you, and the contacts you make potentially even more so.

Through your market research you should be able to establish the type of client that may be the best fit for your skills, the services they need, and how best to present yourself to them as a potential provider.

Your Business Image

You are now almost ready to start promoting your services to potential clients, but one other thing you should give some thought to is your business image.

As a freelance mentor, trainer or consultant, it is vital that you present an impression of competence and professionalism. This applies even – or especially – if you are working from home.