Today I’m spotlighting another survey site that offers the opportunity to generate a sideline income.

You may well have heard of YouGov already, as they often run opinion polls on political preferences and other current issues.

YouGov are always on the lookout for new people to join their panel and complete surveys via their website. Naturally, they provide financial incentives for doing this.

How Does It Work?

For each survey you complete on YouGov, you are allotted points. For a typical survey taking 10 to 15 minutes you will get 50 points. Of course, the longer the survey, the more points you will receive.

You can complete surveys on a computer, smartphone or tablet. You will be notified by email of new surveys you are eligible for, though it’s also worth logging on regularly to see the full range of surveys currently available.

Once you have accumulated 5000 points you can redeem them for a £50 fee. YouGov refer to this as a ‘cheque’, but the money is actually paid direct to your bank account.

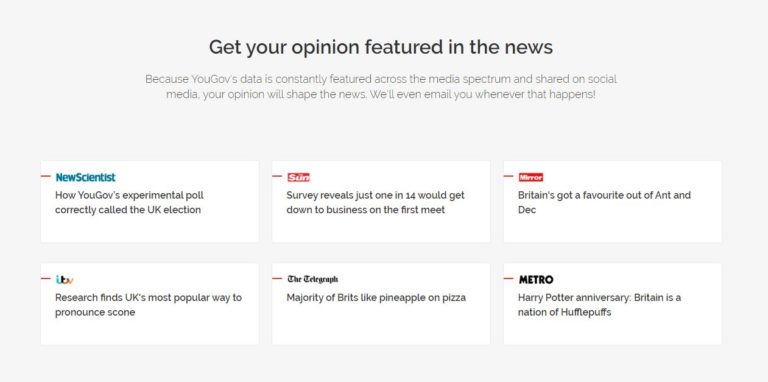

To get 5000 points you would need to complete 100 fifty-point surveys, so this is clearly not a get-rich-quick opportunity. Nonetheless, the surveys are generally interesting and not too demanding to complete. And you will also have the satisfaction of knowing that your responses will ultimately influence decision-makers in government and the private sector. You can see some example media coverage of YouGov surveys in the screen capture from the website below.

How Do You Join?

Joining the YouGov panel is very simple. Just click on this referral link (see below) and complete the short online application form. Acceptance is normally automatic, and you can start earning points immediately.

Disclosure: if you join YouGov via my link I will get 200 points credited to my account (worth £2). If you join YouGov you can also refer other people and earn extra points as well. It all helps get you closer to that next £50 payment!

As always, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Right now it’s difficult for savers and investors to know which way to turn. World stock markets have been in free fall, while bank and building society interest rates are at an all-time low.

Regular readers will know that I’m something of a fan of property crowdfunding and have invested through a number of such platforms (notably The House Crowd, Property Partner, Crowdlords and Kuflink). For anyone seeking half-way decent rates of return, I believe they represent an opportunity worth considering at least, especially in the current uncertain economic climate.

But before I come to that, a few words for those new to this field…

What Is Property Crowdfunding?

As the name says, in property crowdfunding a number of investors pool their money to invest in property and share in the returns pro rata to the size of their investment.

In the last ten years a number of property crowdfunding platforms have been launched to facilitate this. As well as publicizing such opportunities, these companies typically identify suitable properties, advertise and administer projects, and manage properties once they have been purchased. They also distribute payments due to investors from rent received and (eventually) from selling up. Unlike ordinary buy-to-lets, property crowdfunding projects are typically hands-off, passive investments.

There are various methods of property crowdfunding. The traditional method (if you can describe something that’s been around for under ten years as traditional) is equity crowdfunding. Here investors’ money is pooled to buy a house or larger property. Investors then (usually) receive rental income in proportion to the amount they invested plus a share of any capital gains when the property is sold.

The other main method is debt crowdfunding. Here investors lend money to a landlord or property developer so that they can complete a particular project. The money might be used for a bridging loan, or to make improvements to a property prior to selling or remortgaging it. In this type of crowdfunding, the investors never actually own the property. They play a role similar to a bank, lending money and (all being well) being repaid with interest once the project is concluded.

There are also development projects, where investors’ money is used to fund larger-scale property developments. This might involve building a new property (or properties) from scratch, or perhaps converting existing buildings to a new use. Either way, if all goes well, at the conclusion of the development the investors get their capital back along with interest. Development crowdfunding is riskier than equity crowdfunding, but the profits to be made can be bigger.

Property crowdfunding is a form of investment, and like all investments it carries risks. Clearly it’s not as safe as bank or building society savings (which are covered up to £85,000 by the Financial Services Compensation Scheme). All investments are though secured against bricks and mortar, so in the event of a borrower defaulting you should still get your money (or most of it) back once the property concerned has been sold.

The rates of return with property crowdfunding are significantly higher than those from banks and building societies, and they’re also relatively unaffected by fluctuations in the stock market. Property crowdfunding isn’t a way of hedging equity-based investments directly, but it does help spread the risk.

Property and the Coronavirus

These are undoubtedly challenging times for property investors, be they traditional buy-to-let landlords or property crowdfunders.

Even before the virus struck, property prices were at best steady or going down. And measures taken by the government in the last few years, including progressive cuts in mortgage interest tax relief and an additional 3% stamp duty on buy-to-let properties (dubbed ‘The Landlord Tax’) considerably reduced the attraction of buy-to-let for private landlords especially.

The coronavirus crisis has added a whole new layer of difficulty. In particular, measures taken by the government to mitigate the worst effects of the crisis have hit both tenants and property owners hard. Many tenants are obviously suffering financial hardship, and may therefore be having difficulty paying their rent (and other bills). Tenants are, though, currently protected from eviction, and landlords are required to provide rent holidays where appropriate. These measures are sensible and humane, but at a stroke they have reduced or cut entirely many landlords’ income streams, and there is no government scheme to assist them. Obviously I don’t expect many tears to be shed for landlords, but life has undoubtedly become a lot more challenging for them.

In addition, due to social distancing and the lockdown, only limited construction work is continuing. It’s also difficult (or impossible) for surveyors and valuers to do their jobs, or for potential buyers to visit and inspect homes and other properties. All of this means that to a great extent the UK property market has currently ground to a halt.

Despite that, it’s not all bad news. At some point – maybe quite soon – the lockdown restrictions will be eased. The government is (rightly) keen to get the economy moving again as soon as possible. And there are still plenty of people looking to move home, buy property, begin new development projects, and so on. Much as the depressed state of the stock market has presented opportunities for those willing to take a chance on buying now while prices are low, there is certainly a case that property will bounce back in the coming months and years too, rewarding those who invest in the sector now.

Property Crowdfunding Opportunities

Clearly property crowdfunding investors are not immune to the effects of the coronavirus crisis. Developments and sales have been delayed, and in some cases at least rental income has been reduced. It’s quite possible – likely even – that in the longer term the rate of defaults on loans will go up too.

Nonetheless, property crowdfunding investors are unlikely to be as badly affected as private landlords. For one thing, if they are sensibly diversified across a range of properties (and platforms) they won’t be as susceptible as someone with a single buy-to-let. And like all property investors, their money is secured by bricks and mortar, so they will get it back (or most of it) eventually – though in the current crisis, that might take some time. For most property crowdfunding investors at the moment, sitting tight is likely to be the best (or only) option.

As I said above, the crisis is also creating opportunities for those who believe that property will prove to be the resilient investment it has generally been in the past. Rather than prolong this post too much, I will focus my attentions on the four platforms I am currently invested in, and which I am therefore most familiar with.

Property Partner

Property Partner is an interesting case. They have just announced that they are suspending all dividend payments for the next three months (potentially longer). This is, of course, mainly money from rent received, which (for reasons stated above) is likely to take a hit in the coming months. Property Partner say they are taking this action to ensure that investors are protected in the longer term and all properties have sufficient cash reserves to cover any necessary expenditure.

As I said in this post a few months ago, many of the properties on Property Partner are coming up to their five-year anniversaries. This is a significant milestone, because after a property has been owned for five years, all investors have the chance to exit at a fair market price (determined by an independent surveyor). Property Partner have said they are suspending this process until June at the earliest.

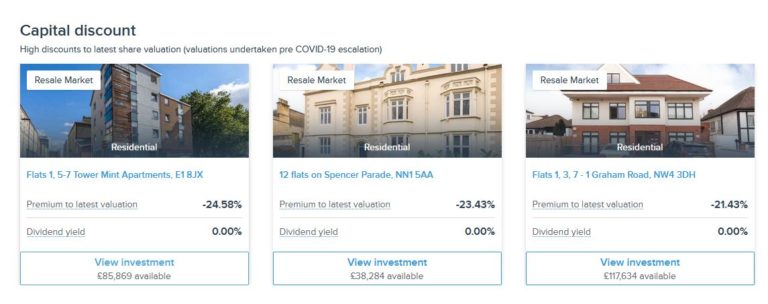

You can still buy and sell properties on Property Partner’s secondary market, and on the face of it there are some good-value buying opportunities here, with properties listed at up to 25% off their current valuations (see screen capture below).

In theory, you could buy shares in these properties on the secondary market at a big discount, and sell them at their current valuation for a good profit when the five-year sale process is reinstated.

Unfortunately it’s not quite a straightforward as that, though. For one thing, the current valuations were made before the coronavirus crisis hit, so they may no longer be an accurate reflection of a property’s value. In addition, the five-year exit mechanism depends on other investors wanting to buy the shares at the valuation stated. Failing that, the property will be sold on the open market, but that could take a long time in the current economic climate. Neither is there any guarantee what price would be achieved.

My personal view is that I do believe property prices will bounce back but it may not be for quite a while. I am looking seriously at some of the buying opportunities on Property Partner’s secondary market where I think they represent good value in the medium- to long-term, but I am not rushing to invest at the moment.

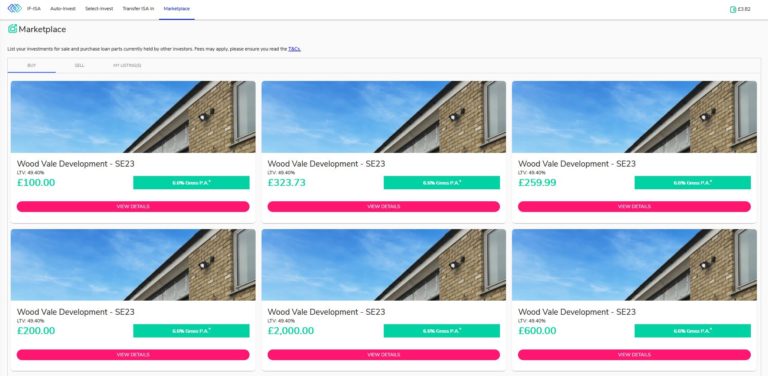

Kuflink is another property crowdfunding platform I have a soft spot for. Although I don’t have huge amounts invested with them, so far all of my investments have paid out as promised, with just a short (one-month) delay in one case.

Kuflink is a property loans platform. So far anyway I have not heard of any defaults, although the longer the crisis continues, the greater the risk this may happen. Nonetheless, based on my experiences to date, I am continuing to invest (cautiously) with them. In particular, I like their new secondary market, where you can buy loan parts from other investors who want to sell up early (see screen capture below)

As you may imagine, this has been happening a lot recently, as many investors have wanted (or needed) to access their capital urgently. This has created short-term buying opportunities which I have been busily taking advantage of. These loan parts typically have only a few months to run, so you can expect to get your capital back quite quickly (and can then reinvest it). Only loans in good standing with monthly repayments up to date may be listed on the secondary market, so that offers some reassurance against default – though of course it is by no means a guarantee.

Secondary market aside, Kuflink also still has a steady stream of new investment opportunities coming to the table. Of all the property platforms, they appear to be the ones least affected by the current crisis. I am not exactly sure how they have achieved this, but obviously I hope they continue to do so!

If you haven’t invested in Kuflink before, it’s also worth mentioning that they have a generous welcome offer which is still operating. You can earn up to £4,000 in cashback with this. See my Kuflink review for full details.

The House Crowd

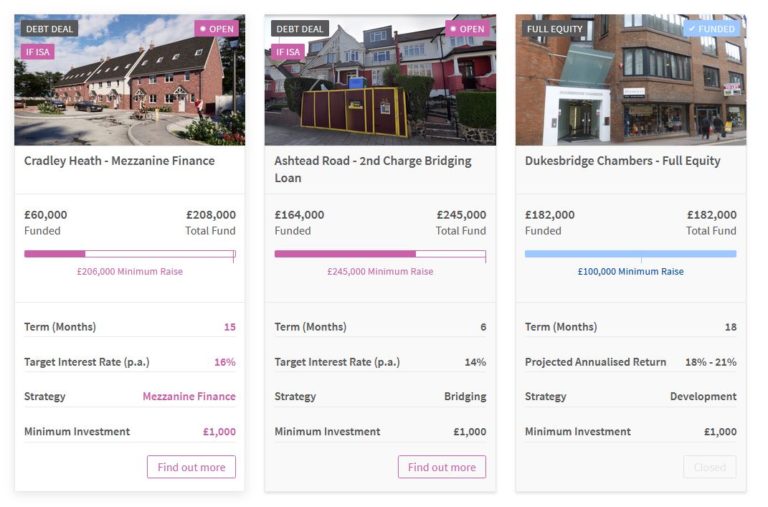

The House Crowd is actually the first property crowdfunding platform I invested with. My experience with them has generally been good, although as mentioned in my House Crowd review there have been some delays and defaults.

Although they started as a traditional crowdfunding platform, The House Crowd have increasingly moved towards development projects, and these have inevitably been hit by the current crisis. THC say that at present they are following a strategy of ‘prudently maintaining The HouseCrowd platform to ensure its continued and efficient operation as we see our way out of the other side of the lock down.’

That means there are fewer investment opportunities on THC at the moment. You can though if you wish still invest in their automatically diversified ‘Auto-Invest’ products, with target interest rates of 5% (Cautious) to 7% (Bold), or the new THC Fusion account, which offers even greater diversification with a target interest rate of 4% to 4.5%. More information about these can be read on the House Crowd website.

At the time of writing THC also have a couple of development projects open for investment, including their flagship project The Downs in Altrincham town centre, paying a target rate of 10% per year (see screen capture below).

Finally, Crowdlords say they have experienced a significant reduction in investment levels since February, which they put down to uncertainty caused by the pandemic. They do still have a couple of lending opportunities listed (see capture below), but not much else. I guess like The House Crowd they are hunkering down and waiting for the current restrictions to be lifted and the property market to start moving again.

Again, I am not currently planning to invest any more in Crowdlords, but am keeping an eye on any opportunities that may crop up in the months ahead. You can read my full review of Crowdlords here.

Final Thoughts

I thought I’d close by sharing a couple of nuggets of information I found while researching this post.

First, the ratings agency Fitch has downgraded the rating of UK debt to AA-. However, Fitch estimated growth next year would bounce back to 3 percent if the UK can begin to unwind the measures to tackle the health crisis in the second half of the year. The UK’s Coronavirus Job Retention scheme – a three-month programme to support employees hit by the pandemic – will cost about 1.3 per cent of GDP, according to Fitch estimates.

Second, estate agents Knight Frank have predicted that many house sales will be lost this year and the UK’s property market will see little to no growth in 2020. However, a sharp recovery has been predicted for 2021. Liam Bailey, global head of research at Knight Frank, said, “We expect a revival in activity to continue, with volumes next year expected to be 18 per cent above the level seen in 2019.”

All of this (and other sources) suggests that while property markets are in the doldrums now and probably for most of 2020, there is every chance that by next year we will see a recovery. There are undoubtedly good opportunities on offer in property investment now if you agree with this evaluation and are able to be patient in the shorter term.

In any event, if you’re looking for better returns than the banks and lower volatility than the stock markets, then property generally – and property crowdfunding in particular – remains in my view well worth considering as part of a balanced investment portfolio.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I am not a regulated financial adviser and nothing in this post should be construed as individual financial advice. You should always do your own ‘due diligence’ before investing, and seek independent financial advice if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Around two years ago I invested some money in the Ratesetter P2P lending platform, partly – I admit – to take advantage of their welcome offer (the current welcome offer is discussed below). So today I thought I would share my thoughts about it.

Ratesetter is a P2P platform that puts would-be lenders and borrowers together, obviously taking fees for doing so. It is one of the longest-running P2P lending platforms, having launched in 2010. They are one of the ‘Big Three’ P2P lending platforms, which also include Zopa and Funding Circle.

In this post I am looking at Ratesetter from a lender’s (or investor’s) point of view, but of course anyone can apply to borrow via Ratesetter too.

Types of Investment

Although investors lend money to borrowers via RateSetter, the actual lending is done behind the scenes. So from an investor’s point of view, RateSetter looks and works much like a bank or building society. Importantly, though, investors with RateSetter don’t benefit from the protection bank and building society savers receive by law in the UK via the Financial Services Compensation Scheme. More about this shortly.

There are three main investment products available on RateSetter. They are named Access, Plus and Max.

The Access product, as the name indicates, aims to offer quick access to your funds without any fee. The Plus and Max products pay more interest but you have to pay a ‘release fee’ of 30 or 90 days’ interest respectively if you wish to withdraw from them.

The terms and conditions for each account are summed up in the screen capture below.

Note that the interest rates on Ratesetter can vary, and the rates on offer when you read this may be different from those shown above.

The Access product is the closest equivalent to an ordinary savings account. You can ask to withdraw some or all of your money at any time without penalty. It’s important, however, to note that this is NOT the same as an instant saver account with a bank or building society. Withdrawing does depend on there being other investors willing to take over your lending on the platform. Ratesetter say that to date investors have received their withdrawn investments within 24 hours on average, which does offer some reassurance.

There is also a ‘fair usage’ clause, which prevents investors from lending new money for 14 days after a withdrawal.

With the Plus and Max products you can also request withdrawals at any time. As stated above, however, in these cases a release fee is applied.

Provision Fund

As with all P2P lending, your money does not enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme.

Ratesetter does, however, have a provision fund which provides a safety net in the event of a borrower defaulting. In the ten years since it was launched no investor has lost money from defaults on RateSetter, which is pretty impressive (although obviously it doesn’t guarantee it couldn’t happen in future). The provision fund is paid for by a ‘credit rate fee’ which is paid by all new borrowers.

It’s worth mentioning also that provision fund protection extends equally across all loans. There is therefore no particular need to diversify your investments on Ratesetter, although you should of course diversify across other platforms and investment types.

The IFISA Option

You can also invest in Ratesetter through an IFISA (Innovative Finance ISA). This type of ISA for P2P lending gives you the same tax advantages as a cash or stocks and shares ISA, i.e. you don’t have to pay any tax on the profits you make.

Everyone has a generous annual ISA allowance of £20,000 (in the current 2019/20 tax year). This can be divided any way you like among the three types of ISA. So if you open a Ratesetter IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. You can also only invest money in one of each type of ISA in any one financial year.

If you have maxed out your ISA allowance – or have invested in another IFISA in the current tax year – you still have the option of opening an Everyday Account. You can invest any amount in this, but of course the profits you make will be taxable.

2020 Interest Rate Cut

Due to the coronavirus crisis and the current febrile economic environment, RateSetter announced on 4th May 2020 that there would be a temporary reduction in interest rates for the remainder of 2020. During this time, investors will receive only 50% of their interest, with the other 50% going to the Provision Fund, for the protection of all investors. At current rates. that means the actual interest rates paid during this time will be 1.5% for Access accounts, 1.75% for Plus accounts, and 2% for Max accounts.

I have also heard (and confirmed with Ratesetter) that currently repayment requests are taking three to six months to process. If that changes I will update the information here.

Ratesetter Pros and Cons

Based on my experiences so far – and the results of some online research – here is my list of pros and cons for the Ratesetter P2P lending platform.

Pros

1. Fast, easy sign-up.

2. Low (£10) minimum investment.

3. Choice of investment terms

4. Quick and simple investment process.

5. Tax-free IFISA option available.

6. Provision fund protects lenders against loss (no investor losses at all to date).

7. Ability to access your money at any time (though with a fee when exiting the Plus and Max products)..

8. Customer service (in my experience anyway) is fast and helpful.

9. NEW! A free £100 added to your account for new users who invest £1,000 and keep this invested for a year (see below).

Cons

1. Rates paid aren’t the highest in P2P lending.

2. Website isn’t always as intuitive to use as it should be.

3. Withdrawals are taking longer than usual to process due to increased demand following the coronavirus outbreak.

4. Temporary interest rate reduction by half to help boost the Provision Fund (see above)

Conclusion

Overall, my experiences with Ratesetter so far have been good. My initial deposit was matched within 24 hours and has been generating the promised returns ever since. I reinvested my bonus payment into the platform and this is earning interest as well.

As mentioned earlier, P2P lending does not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates on offer at Ratesetter are significantly better than those from most banks and building societies. And the existence of a substantial provision fund with a strong record of protecting investors from losses clearly offers reassurance. Based on its past record and the protections in place, Ratesetter appears to be one of the safer P2P lending platforms.

It’s also reassuring that you can access your money any time – this can be an issue with property crowdfunding platforms in particular, as liquidity in these platforms can be limited. With the Plus and Max products you will be charged for exiting early, though, so invest in these only if you are pretty confident you won’t be needing the money within the next few months.

On the negative side, the current three to six month delay in withdrawals, and the halving of the rate paid to investors, is clearly disappointing. I understand that RateSetter are doing this to protect the business in the longer term, but it obviously it reduces the attraction of investing with them currently (though see Welcome Offer, below)

Clearly, no-one should put all their spare cash into Ratesetter (or any other P2P lending platform). Nonetheless, it is worth considering as part of a diversified portfolio. Not only are the rates of return higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P lending isn’t a way of hedging your equity-based investments directly, but it does help spread the risk.

Welcome Offer

Currently if you are new to RateSetter you can get £100 added to your account for free just by signing up and depositing £1,000. Full terms of the offer are reproduced below, and you can also find them on the RateSetter website.

You can take advantage of this offer so long as you

have not previously registered with RateSetter

deposit a minimum of £1,000 through the RateSetter ISA or Everyday account and this is matched within 56 calendar days of opening an account

keep a minimum of £1,000 invested for 1 year

Your bonus will be credited to your Everyday Account and invested in Ratesetter’s Access product within 30 working days of qualifying. You can ask to withdraw your money at any time, but you must keep a minimum of £1,000 invested for 1 year to qualify for your £100 bonus.

My Thoughts: This is a great offer from RateSetter if you are new to the platform. If you invest £1,000 and keep it there for a year, then including the £100 welcome bonus you will get a total return of at least 12 percent for the first year, even allowing for the temporary 50% rate cut. As a matter of interest, this is the same welcome offer I took advantage of when I signed up with RateSetter two years ago, and my bonus £100 was credited without any issues (or prompting from me) twelve months later.

Clearly, this is a generous promotional offer by RateSetter and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

As always, if you have any questions or comments about this post, please do leave them below.

Note: This is a fully revised and updated relist of my original (2018) RateSetter review.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post from Cora Harrison, a UK blogger and vlogger (video blogger) whose website is called The Mini Millionaire.

Cora says she loves to explore new ways of making money, both online and offline. She has a particular interest in online selling (and reselling) and there are many posts on this subject on her blog.

In her guest post today she reveals how anyone with an interest in creating arts and crafts can boost their profits – potentially many times over – by selling their work online.

Over to Cora, then…

If you love creating arts and crafts products, you can of course sell them at local markets or craft fairs. If you are looking to sell more and make (much) more money, however, you should definitely consider selling online as well.

There are various ways you can display and sell your work online. Here are some of the most popular.

Your Own Website

Selling arts and crafts on your own website is probably the single best way to sell your hand-made items online.

Having your own website will allow you to contact customers directly, grow your brand, and avoid the fees charged by third-party platforms like Etsy and eBay. In addition, you will not be competing directly with other craftspeople selling similar items to the same pool of customers on the platform.

For this to work, however, you will need to create an attractive, professional-looking website. You will then need to drive traffic to it, using techniques such as search engine optimization (SEO) and perhaps paid advertising. You can use online website building tools such as Wix or Shopify to create your site or hire a professional website designer.

Selling on Etsy

Etsy is an online marketplace dedicated to hand-crafted items. It is known for vintage, unique and custom-made items. It is easy to use, so you can set up your store and sell your crafts online in no time. Many would-be buyers of hand-made products look on Etsy before going anywhere else. Customers can pay by various methods, including PayPal and Google Pay.

On the minus side, many other artists and craftspeople also use the platform. This means it can be hard to sell common items. In addition Etsy charge about 5% of the sales value as a transaction fee every time you make a sale. You also pay about $0.20 for each item you sell. PayPal (the most popular payment method on the platform) also charge a fee for processing payments. All of these fees and charges will eat into your profits.

Facebook Marketplace

Facebook Marketplace is a prime location for selling hand-made crafts products locally. Given that Facebook has a massive user base, you can reach many potential buyers in your area by posting your items there. Posting items is free and you can add up to 42 images of your product in every sales post. The post will also include a description of the product, your location, and the price of the item.

While there is no limit to the number of posts you can make in a day, Facebook may limit posting to avoid spamming the page with similar ads. You have the option of sharing posts on your wall so that your friends may see the posts you have shared in local buying and selling groups. Potential customers will message you for more information and selling terms. The Marketplace is available on the web-based version of Facebook and as an app.

Selling on eBay

eBay is of course primarily an auction marketplace where sellers post items and sell them to the highest bidder. However, you can also create fixed-price listings. It is therefore a good platform to sell hand-made crafts online. The platform uses PayPal as the payment provider for all transactions. Both eBay and PayPal have various fees that you will encounter.

You will also be required to pay a final value fee. The fee is applied at the end of the transaction after making a sale. The fee is a percentage of the purchase price. There are also shipping and handling fees. Shipping fees are based on the method chosen by the buyer unless for domestic shipping, where the fee is calculated from the cheapest shipping method.

You will pay the final value fee whether or not the client pays for the item. If the sale is unpaid, you can cancel the sale or report it as unpaid. Note that eBay will give you credit for this rather than a cash refund.

Why Selling Online is Beneficial

There are several reasons you should consider selling your hand-made crafts online compared with selling in person at craft fairs and so on (though you can of course do both).

First, as stated above, online selling exposes you to a much larger audience than in the case of a market stall. You can sell your items to potential buyers across the country – and further afield – with ease.

In an online store, there are no opening time restrictions. The store runs around the clock and customers can place orders at any time of the day or night, as opposed to a local venue with set opening hours. In addition, you can operate the business from anywhere and target potential buyers who are far away from your location.

An online store also requires less time and effort. Once you have set up your online store and posted your hand-made items, they will be seen whether you are online or not. This allows you to sell your crafts even if you are otherwise engaged.

An online store also has lower running costs than an off-line one. There are no utility bills, rent or other premises costs to pay. You can run your online store from your kitchen, living room or bedroom. All you need is a laptop or desktop computer with an internet connection.

Effectively Selling Your Items Online

The Quality of Photos Matters

Just like in an off-line store, in an online store your hand-made crafts need to look good to appeal to customers. It is therefore vital that you take clear, sharp photos of your items. You can take them from different angles to give the customer an all-round view.

A modern smartphone should produce good-quality images in ambient light, but place your items on a white surface to give them a professional look. You can also use image-editing software to make the image ‘pop’.

Give Your Items a Perfect Description

Since you will not be there to explain the features of your product in person, it is important to provide a good description alongside your image. Ensure that the customer gets a mental image of the item without getting too sales-y. Most platforms have a character limit within which you can write a description. Use this opportunity to explain all the features that might be of interest to a potential buyer.

Keep Checking Your Site Regularly

Keep checking the platform where you have posted the item regularly for customer queries or orders. If the account is linked to your email address, you can have ‘push notifications’ set on your phone so that you know when there is activity relating to your item. The ability to respond quickly to queries will boost your reputation and prevent you from losing customers.

You may wish to post on more than one platform to increase your exposure. Try to estimate the return versus the cost of placing ads on multiple platforms. Having many items listed rather than just a handful will increase your overall selling rates as well, so aim to build up your inventory as quickly as possible.

Good luck, and I wish you every success selling your hand-made arts and crafts online!

Many thanks to Cora Harrison (pictured, right) for some great tips and ideas.

Selling arts and craffs (online or off-) isn’t something I have ever tried myself, but I know it will interest many of my readers, so I was delighted to receive Cora’s article.

Obviously, you need some artistic talent to do this, but you definitely don’t need to be Leonardo (da Vinci, I mean, not DiCaprio). For example, using inexpensive software you can create attractive printables, which could sell well on Etsy and similar websites. You can read my blog post on this subject here.

But if you really don’t feel that selling arts and crafts online is your thing, you can still make good money selling and reselling products of all sorts online, from DVDs and collectables to Lego bricks! Check out Cora’s Mini Millionaire site for much more information about this..

As always, if you have any questions about this article, for Cora or myself, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Over the last few weeks I’ve received several queries about 20 COGS. I’ve also seen people asking about it on Facebook. Some of my fellow UK money bloggers have been promoting it as well.

I did try 20 COGS myself about 18 months ago. I didn’t like it and have therefore never written about it or promoted it (and I’m not now, so there are no affiliate links in this post). As it still seems to be generating a lot of interest, however, I thought I’d share my experiences (and opinions) about it here.

I guess I’d better start with a word of explanation, though…

What is 20 COGS?

For those who don’t know, 20 COGS is a home money-making opportunity. The way it works is that you undertake a set of twenty online tasks. Once you have completed all twenty as specified – and not before – you receive a cash reward. This is generally between £150 and £200, but you are likely to incur some costs in completing the tasks (e.g. paying for trial subscriptions) and these will need to be deducted from your reward to calculate your net profit.

The tasks are, of course, the twenty COGS in the name. COGS stands for Competitions, Offers, Gaming, Surveys. A typical task might involve signing up with an advertiser for a free or low-cost trial subscription (which you have to remember to cancel before they start charging the full monthly amount). Or it might involve signing up to an online casino site and wagering a set amount of money on their slot machines. It might also just involve filling in a (long) survey, but quite a few tasks do involve some financial outlay (with the risk of more if you don’t cancel in time).

My Experience

I saw 20 COGS recommended by a few bloggers I generally trust, so decided to give it a go. Unfortunately I didn’t prepare as well as I could have done, which was my first big mistake. In particular, I made the rookie error of giving out my own email address and mobile phone number.

I soon discovered that this was a serious mistake, as after the first few tasks I began getting spammed mercilessly. The spam emails weren’t so bad, as they were generally filtered out by my email program. However, my mobile phone became unusable due to the torrent of marketing calls and text messages I received. In the end I had no alternative but to bite the bullet, cancel my mobile number and get a new one. In my defence, I naively assumed that this wouldn’t happen due to GDPR and data protection rules – but when you sign up with 20 COGS these appear to go out the window.

I also had problems with some of the tasks. To start with, I couldn’t do quite a few of the gaming ones due to previously being a matched bettor. This meant I had already signed up with many of the websites concerned so I wasn’t eligible for the tasks in question. In those circumstances you can ask for a substitute task but this all takes time and in my case there weren’t enough replacement tasks available (although over time new ones do of course get added). As I mentioned earlier. this was about 18 months ago, so it’s possible there are more alternative choices available now.

I also had major reservations about the amount of personal information some of the survey-related tasks asked for – from holiday plans to dates of renewal for home and car insurance. Pretty obviously, this information was likely to be used for (unwanted and intrusive) marketing purposes.

Eventually, after completing about half a dozen cogs, I decided enough was enough and closed my account. That didn’t stop the spam, but at least I could breathe a sigh of relief that I didn’t have to do any more tasks. Of course, I got no money for the ones I had done, which I assume is one major way 20 COGS make their profits.

My Recommendations

As I said at the start, based on my experiences I don’t recommend signing up with 20 COGS at all.

It is an awful lot of hassle to go through for a probable net profit of £100 or so after costs are deducted. And you can easily end up with less than this if you forget to cancel a subscription (which is very easy to do).

If, despite all this, you are still tempted to give it a try, here are my recommendations…

1. Sign up via the link on Top Cashback. This will earn you an extra £1.20 cashback (at the time of writing).

2. Before starting, create a disposable email address and use this for all tasks. You could set up a new email address on Gmail or use a free disposable email service like ThrowAwayMail.

3. In addition, don’t use your real mobile number. You could use a pay-as-you-go SIM, or pick a number from https://fakenumber.org/united-kingdom. They have a list of UK mobile numbers that are not in use currently.

4. Keep detailed records of everything you do and when you do it. To avoid unwanted charges, it is clearly essential to cancel subscriptions before you have to pay the full amount (but after the qualifying period required by the advertiser). You might also want to set up automated reminders on your phone or computer to do this.

5. Read and follow all instructions carefully. Every advertiser on 20 COGS has its own specific requirements and you need to follow these carefully or you may not be credited for the task in question.

6. Take screenshots as you complete your tasks. If an advertiser disputes whether you completed a task correctly, you will then have visual proof that you did.

Finally, bear in mind that 20 COGS is a once-only scheme. After you have completed it, you won’t be able to do it again. It is not an ongoing money-making opportunity like matched betting or Prolific Academic, to take two random examples from the many I have covered on Pounds and Sense.

In Conclusion

As I said above, based on my experiences with 20 COGS I am not a fan and don’t recommend it.

It’s an awful lot of hassle to go through in order to earn £100 or so. And there is a very real risk of earning less than this if you make a mistake such as forgetting to cancel a subscription. There are also privacy issues, and you are potentially opening the door to a torrent of spam emails, texts, phone calls and more (though using fake/disposable mobile numbers and email addresses as recommended can reduce this).

Of course, this is just my opinion. I do know of people who have completed 20 COGS and (eventually) received a payout. If you are still on the fence about it, I recommend reading this comprehensive 20 COGS review by my colleague Adam who blogs at Money Savvy Daddy. Adam did actually complete 20 COGS and says he made about £100 from it. He is honest in his review about the time it took and the obstacles he faced along the way, however.

As always, if you have any comments about this post – or 20 COGS more generally – please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Many of us have old gadgets that we no longer use and are just gathering dust. These include mobile phones, tablets, laptops, cameras, games consoles, and even desktop computers. They may still work, but we have replaced them with new and (hopefully) better products.

There is a natural tendency to hang on to the old products for a while, just in case we need a backup if our shiny new replacements fail. Modern brands are generally very reliable, however. And once you have established that a new product isn’t faulty, there isn’t really much reason to hang on to the old one – certainly not for months or years on end.

You might think the only thing to do with an old gadget is take it to the tip – sorry, household recycling centre. Before doing that, though, it’s worth noting that there are various ways you can make money from your old tech, even if (in some cases) it’s no longer working.

The High Street

There are various shops that will pay for old technology of all kinds. For example, CeX (who also have a website) will pay for smartphones, satnavs, cameras, speakers, headphones, laptops, games consoles, and even TVs in some cases. The device needs to be working but doesn’t have to be in its original packaging. Buy-and-sell stores like Cash Converter and Cash Generator will buy your old tech too.

eBay

Whatever the product you want to sell, the online auction house eBay is worth considering. It has a huge audience, and there will always be potential buyers looking for any item you want to dispose of.

Of course, you will have to spend a little time preparing your auction listing, taking photos, writing a description, and so on. However, eBay make this as easy as possible for sellers by showing you similar items that have sold on the site recently. This will help you prepare your own listing and assess the likely amount you may be able to get. Bear in mind that eBay does impose charges for sellers, which will reduce the amount you receive.

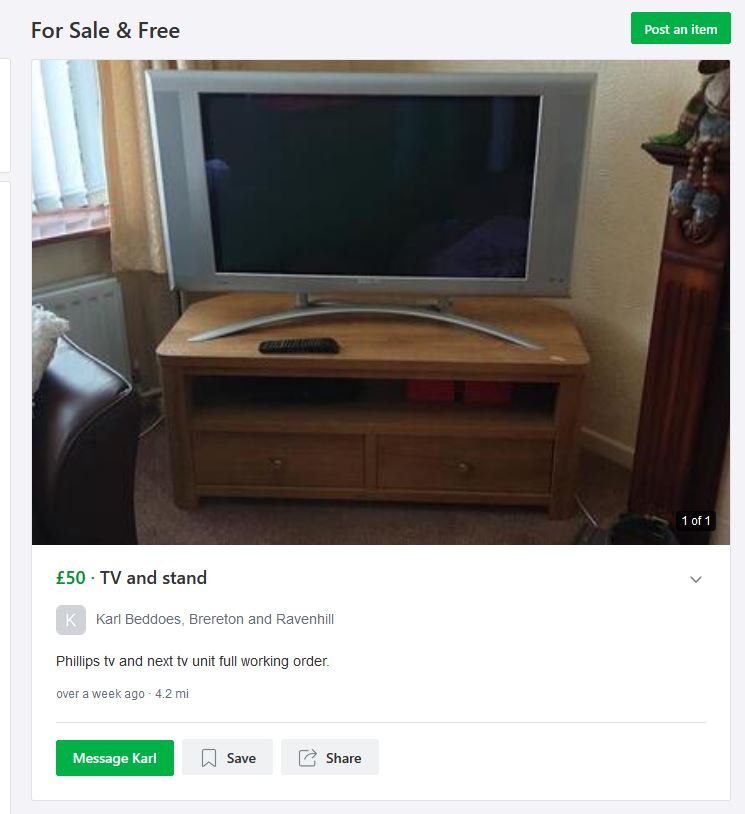

Facebook and Other Community Sites

Facebook local pages can be a great way of selling larger items in particular that may not be easy to post. You will need to include a photo and write a description stating the price you want. With a bit of luck someone living nearby will want the item and collect it from you for the price asked.

There are also other local community websites that may be worth trying. One I belong to myself is NextDoor. This is primarily a forum for the discussion of local news, seeking/sharing recommendations, publicizing local events, and so on. However, you can also advertise items for sale on the site. Here’s a typical example…

Specialist Sites

There are also specialist websites that want your old tech and will pay you for it. This can be a quick and hassle-free solution, with the advantage that you know exactly what price you will be getting (the sites quote a price online and it is up to you whether or not to accept this). Most will also accept products that are no longer working, though of course they will pay a lower price for them.

One such site I used recently and recommend is Cash in Your Gadgets. I sold them my seven-year-old Samsung Chromebook. The item in question was still working but by modern standards it was slow and the display wasn’t great. I went to the Cash in Your Gadgets website and spent a minute or so entering some details. I received an instant offer of £18 for the Chromebook, which I accepted.

Okay, I know £18 isn’t a fortune, but I was pleased to have the money and get the device off my hands. Cash in Your Gadgets arranged collection by courier, who arrived the next day, put the item in a box, sealed it, and gave me a receipt. A few days later I got the promised £18 in my bank account.

Cash in Your Gadgets pay for laptops, Chromebooks, Macbooks, iMacs and desktop PCs, though not smartphones or tablets. If you have one of those to dispose of, there are various other options.

One well-known site that buys phones and tablets is MusicMagpie. They also buy consoles, tablets, smartwatches, Kindle e-book readers, and more. If you use my referral link you can get an extra £5 when you sell your first product to them (and so will I) 🙂

Other options include Mazuma and Sell My Mobile. My best advice is to try these and similar sites and see who offers the best price. When I wanted to dispose of my old Samsung J5 (2016) smartphone, I was surprised by how much the offers I received varied. I was offered between £25 and £40, and naturally opted for the £40 (which happened to come from MusicMagpie).

.When using these services you will need to send the item to them in a padded envelope or a box. You will have to provide this yourself, but the postage is normally free.

Data Security

Before disposing of any item that may contain sensitive information it’s important to erase any personal data, ideally by performing a factory reset. All the specialist companies perform a data wipe on receipt anyway, but it’s clearly advisable to do this yourself as well. If you are selling privately – perhaps via eBay or Facebook – it is essential to ensure that any personal data on the device is permanently erased and can’t be restored.

I hope this article has inspired you to gather together any old tech you no longer need and turn it into useful cash. As always, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Cashback sites give you money back when you shop with a wide range of online retailers. In the UK the two best known are Quidco and Top Cashback, but there are others as well.

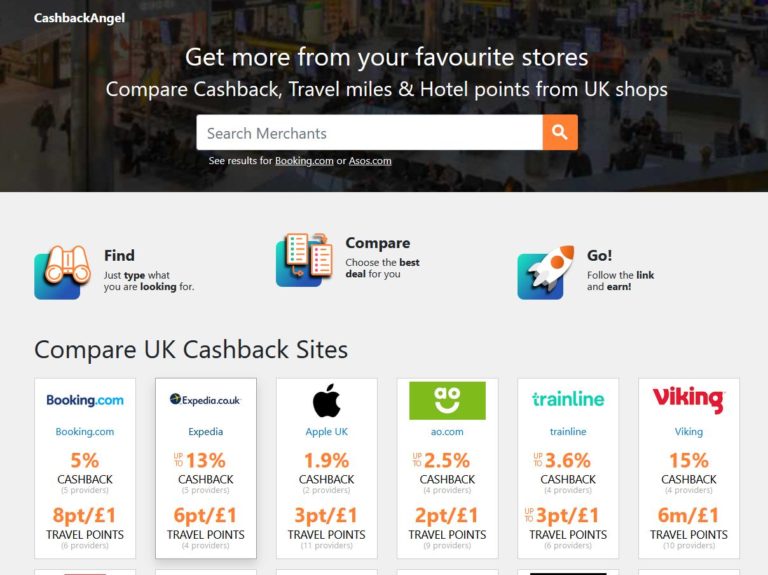

All cashback sites offer different deals which change frequently, so it can be hard to assess which has the best offer at any time. However, a new comparison website called CashbackAngel promises to make this task much easier.

CashbackAngel

CashbackAngel allows you to quickly check and compare deals on offer from cashback sites for any online retailer you may be planning to purchase from. It is therefore much more than just a website that lists and compares cashback sites.

I have posted a screen capture of the CashbackAngel front page below.

The main search box is at the top of the screen and lets you search for any merchant. Below this are example merchants showing the best deal currently available for each one, both in terms of percentage cashback and travel points (should this interest you).

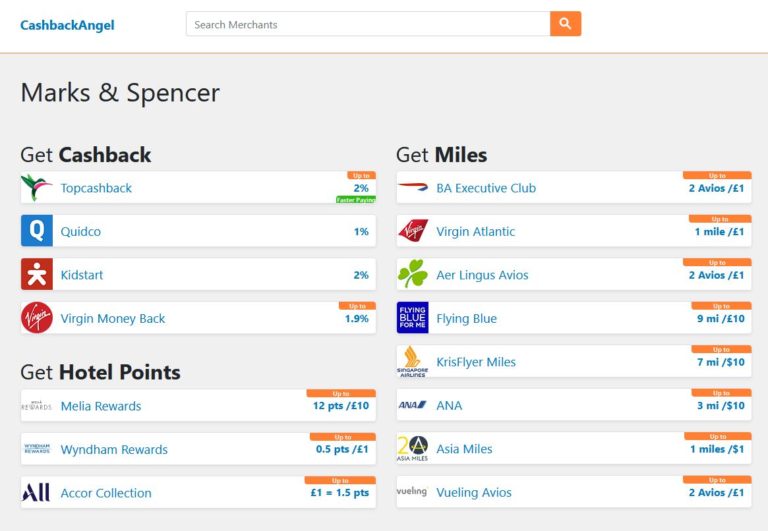

Let’s say you want to find which cashback site offers the best deal for purchasing from Marks & Spencer. Enter the retailer’s name in the search box and click on the search icon. When I did this, the results below were displayed.

As you will see, in this instance CashbackAngel displays results from four different cashback websites: Top Cashback, Quidco, Kidstart and Virgin Money Back (If you’re not familiar with Kidstart – I wasn’t – it’s a site that pays cashback into a dedicated children’s savings account).

In this example, Top Cashback (along with Kidstart) looks as though it might offer the best deal, with cashback of up to 2%. Obviously you would need to check on the Top Cashback site to find out their exact terms. You can do this by clicking through the link on the CashbackAngel results page (shown above). When I did this myself, I found that new M&S customers arriving via Top Cashback get 2%, returning customers 1%.

As you can also see from the screenshot above, cashback is by no means the end of it. If you are collecting Air Miles, CashbackAngel lists a number of providers who are offering these in exchange for shopping with the retailer in question. And you can also earn Hotel Points for various hotel chains if that is your preference.

My Verdict

Overall, I was impressed with CashbackAngel. In particular, I like the way it compares offers in real time, so you can always see which cashback site has the best deal at the time of asking.

It is also good to see a wide range of cashback and rewards sites included – though slightly disappointing that the new My Money Pocket website (which I reviewed here) doesn’t appear to be included currently. Hopefully this will be added soon. [UPDATE: I just heard from CashbackAngel that they intend to add My Money Pocket by the end of January 2020.]

If you use cashback sites – and in my view everyone should! – CashbackAngel is well worth checking out and adding to your online bookmarks.

As ever, if you have any comments or queries about this post, please do leave them below.

Disclosure: Some links in this article include my affiliate code. If you click through and make a transaction, I may receive a commission for introducing you. This will not affect any rewards you receive or terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing another great sideline-earning opportunity.

Crowdville started in 2014 in Italy, where they built up a thriving online community of over 30,000 members. In the last year or two they have launched in the UK and other countries as well.

Crowdville pay members to test digital products (both existing and upcoming) and report back on what they find. Members are paid for their feedback, their opinions about the user experience, and their bug-finding skills. The YouTube video below provides a quick introduction to the platform.

Joining Crowdville

Joining Crowdville is free of charge. All you need is a smartphone and an email account. Click through any link in this post to Crowdville and you will be presented with a registration form. This should only take a minute or so to fill in. Accept the terms and conditions and click on Register. And that’s it – you’re in!

Once you have joined Crowdville, you can sign up for ‘Missions’. These range from simple surveys to more complex bug-finding challenges. Payment for successfully completing a Mission is guaranteed.

You can also access Crowdville using a laptop, PC or tablet, and provide feedback via the website – but as most Missions involve testing mobile phone apps, you will need a smartphone in order to do this.

Crowders – as the company calls its members – are paid by bank transfer or Amazon vouchers. As long as you successfully complete a Mission – either by submitting a survey, sending screenshots or finding bugs – you are guaranteed to be paid.

Anyone is welcome to join Crowdville. However, it’s an ideal platform for technology enthusiasts, as you are able to test out a range of digital products and services before anyone else. You get an exclusive preview of upcoming app releases, put them through their paces, and then get paid for giving your feedback about them.

The work you are offered will depend on your location and other personal info, but you can always turn down Missions if for some reason they don’t appeal to you.

Community

One big attraction of Crowdville is that – as the name implies – it is community-based.

Through a private social media platform called Otium, you can meet and interact with other Crowders and Crowdville managers. This provides you with an opportunity to learn from others, and as you gain experience to offer support and advice to new Crowders yourself. This social aspect makes working as a Crowder more enjoyable and less stressful, especially when you are first starting out.

Additionally, once you’ve been accepted to a Mission, you are automatically placed in that Mission’s group. You can discuss the Mission here with others who are also doing it, and ask about any problems you may be having. As well as making the process easier and less stressful, this allows the community as a whole to learn from one another and improve.

Finally, there is even a reward for being a helpful Crowder. If you complete Missions and help other members, you can become a SuperCrowder. This allows you to earn more money and access other, higher-paying opportunities.

Summing Up

If you’re looking for a new sideline-earning opportunity – and especially if you enjoy testing and evaluating apps and websites – Crowdville is well worth a try. It’s free to join, and you can earn a steady stream of cash and vouchers. You can also make more money by introducing friends and colleagues and giving them the opportunity to earn from the platform as well. In any event, there really is nothing to lose by signing up for free and trying out Crowdville for yourself.

As always, if you have any comments or questions about this post, or Crowdville in general, please do leave them below.

Disclosure: I am a Crowdville member myself and the links in this post are referral links. If you click through and sign up, I may receive a commission for introducing you. This does not affect in any way the benefits you will enjoy as a Crowdville member.

If you enjoyed this post, please link to it on your own blog or social media:

For about three years now I have been a panelist with ShopandScan. This is an ongoing market research programme run by a company called Kantar Worldpanel.

I got an invitation to join ShopandScan in the post, but you can also apply directly if you wish (see below). I now receive £10 reward vouchers every few weeks just for scanning my shopping and my till receipts.

How it Works

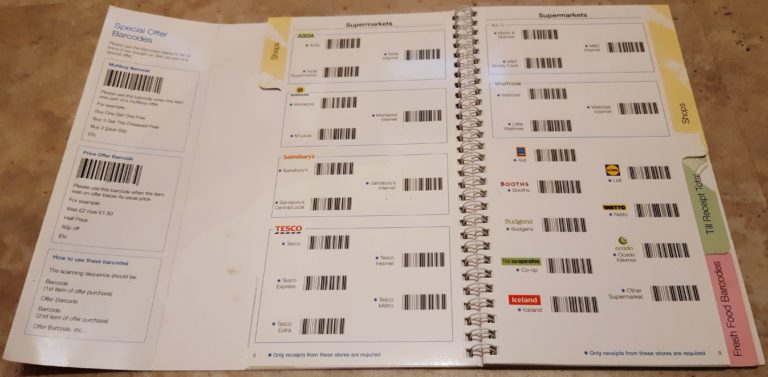

After accepting the invitation to join ShopandScan, you receive a membership pack in the mail. This includes a User Guide and a barcode scanning device or ‘clicker’ (see picture above).

As a panelist, you use this to scan all shopping with barcodes coming into your home. You also scan barcodes in the User Guide to indicate who in your household did the shopping, the store concerned, and how much was spent.

There are also barcodes to scan for items that don’t have codes themselves, e.g. loose fruit and vegetables. Finally, there are barcodes to scan when an item is on special offer or part of a multi-buy offer. You can see a sample page of the User Guide below…

You have to upload the scanned data via the ShopandScan website once a week (at least). Full instructions are provided, but it isn’t rocket science. Basically you plug the clicker into a USB port on your computer and follow the instructions in the User Guide.

For doing this, you receive points. You get 1100 points a week for uploading the data from the clicker. In addition, you get 500 points a week for uploading scans of all your till receipts (unfortunately you don’t get points for each individual receipt). So each week that you do these things, you earn a total of 1600 points. Occasionally (e.g. at Christmas) they award extra points, to allow for the fact that it’s easy to forget at busy times of year.

The points accumulate in your account and once you get to 10,000 you can redeem them for a £10 electronic gift voucher. These are available for a variety of online retailers. I normally choose Amazon, as I buy stuff there all the time. However, you can also get vouchers for Waterstone’s, Halfords, W.H. Smith, and many more.

As well as getting points for uploading your data and submitting till receipts, you can get them in various other ways. One is by completing questionnaires about some aspect of your shopping.

Recently, I was offered a questionnaire regarding my purchase of own-brand almond milk from Morrison’s. They wanted to know why I bought it and when and how I intended to consume it. It only took a few minutes to complete and I got 300 points for this (equivalent to 30p).

There are other point-earning opportunities as well. Right now I am signed up to another project which involves allowing access to the browsing history on my smartphone. I know not everyone would feel comfortable about this but I don’t object personally (all data is anonymised) and it means I get an extra 500 points every week for no effort (it’s all done via an app).

You may also be offered the opportunity to take part in other studies. I did one a few months ago that involved completing a food diary listing everything I ate and drank for a week. Although I got points for this I found the task rather tedious, and declined when they offered me the opportunity to do it again. There is never any problem if you decide to turn down an invitation in this way.

How to Apply

As I said earlier, I got my invitation to join ShopandScan in the mail. I don’t know how they chose me or got my name and address.

However, you don’t have to wait for an invitation. If you wish to join ShopandScan, you can register for free at https://www.volunteer4panels.com. There is no guarantee that your application will be accepted immediately, as they aim to keep the panel balanced across age groups, locations, domestic circumstances, and so on. From what I have heard, though, once you have applied there is a good chance you will receive an invitation within a few weeks, or months at most..

Closing Thoughts

Clearly nobody is going to make a fortune from ShopandScan but it can be a great addition to your portfolio of sideline-earning opportunities. Once you get used to scanning your shopping before putting it away, it really isn’t much of a hassle. If you do some questionnaires and so forth as well, you can easily make over £100 a year.

As always, if you have any comments or questions about this post (or ShopandScan in general), please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I recently received an email telling me about a new (free) cashback site called My Money Pocket. As a fan of cashback sites I was very happy to check it out.

My Money Pocket is a UK site. It is therefore entering an arena currently dominated by what might be called the Big Two here, Quidco and Top Cashback.

As with those two sites, My Money Pocket offers members the chance to earn cashback by following links to a variety of online retailers. These are affiliate/referral links, and My Money Pocket receives commission for any purchases made by people clicking through them. My Money Pocket then shares this commission with the member concerned.

Getting Started

Before you can use My Money Pocket to get cashback, you do (of course) need to register on the site. All they require for this is your email address and a password. On the plus side, that makes signing up very quick and easy. On the minus side, I find it slightly odd that they don’t ask for your name, which means you can’t see this when you are signed in. That could be problematic if you share your computer with other family members, as you may not know which of you is actually logged in!

I did ask My Money Pocket why they don’t ask for a name when registering, and they said it was to avoid privacy issues. Personally, though, I would much sooner see “Welcome, Nick” (or whatever) at the top of the screen to reassure me that I am actually signed in to my own account.

Once you are logged in you can start earning cashback by clicking through the links provided to a wide range of online stores. Most of these are also available with Top Cashback and Quidco, but the cashback rates (and terms) are different – better in some cases, worse in others. As with all things shopping related, it really does pay to shop around!

The website looks bright and welcoming, but a large area at the top is taken up by an offers carousel, which personally I find a bit obtrusive. I thought the site navigation was okay, but not quite as intuitive as the Big Two. I would prefer a traditional tabbed navigation menu of the sort that is used on Top Cashback and Quidco (and many other websites), but maybe I am just being a bit old-fashioned.

There is a drop-down Categories menu at the top left of the screen. This takes you to cashback offers in the following categories:

Fashion

Food and Drink

Health and Beauty

Electricals

Travel

Broadband

Entertainment and Leisure

Utilities

Gifts

Mobile

Home and Garden

Free Cashback

Gaming

Shopping

Office and Business

Sport

Gambling

Within most of these categories there are sub-categories as well. Incidentally, ‘Free Cashback’ lists offers where you don’t have to spend money to get cashback – for example, you might just have to request a quotation for your car insurance.

As with Top Cashback and Quidco, once you have made a purchase with one of the merchants on My Money Pocket, you will then have to wait for your cashback to be tracked, approved, paid and credited to your My Money Pocket account. You will then be able to withdraw this money, either to your bank account (through BACS) or via PayPal.

One other feature is that you can refer other people to My Money Pocket and receive £5 cashback yourself when they have earned a minimum of £10 in cashback. Note that all links in this blog post include my referral code 🙂

Final Thoughts

It’s early days for My Money Pocket and the site is still to some extent a work in progress. Nonetheless, there is nothing to lose by signing up for free now and checking out the deals on offer. As I said earlier, I would recommend checking and comparing My Money Pocket, Top Cashback and Quidco to see which site is currently offering the best terms for any retailer you intend to buy from.

As always, if you have any questions or comments about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media: