If you’re looking for a home for your savings (or some of them), a friendly society might not be the first thought that occurs to you. Nonetheless, it may well be worth considering.

Friendly societies are one of a number of UK institutions called ‘mutuals’. These were originally set up by groups of people for a common financial or social purpose. Before modern insurance and the welfare state, friendly societies provided financial and social services to individuals, often according to their religious, political, or trade affiliations.

Friendly societies today typically provide a range of savings and insurance services. Along with other mutuals, they are regulated by the Financial Conduct Authority (FCA).

Why Save With a Friendly Society?

One big attraction of friendly societies is that they are owned by the members themselves. This means any profits generated go to members (directly or indirectly) rather than shareholders, as is the case with banks.

A good example is Shepherds Friendly, which offers a range of savings, investments and insurance products. These include a highly rated Stocks and Shares ISA. There is a minimum investment in this of £30 a month or a minimum lump sum of £100.

The Shepherds Friendly Stocks and Shares ISA is an actively managed fund and rated medium to low risk. The fund invests in a mixture of UK and overseas company shares, property, government and company bonds, and cash deposits. Most of the fund is normally invested in stocks and shares for greatest growth potential, but at times of economic turbulence some may be switched to safer investments such as bonds and deposits.

Investors in the Shepherds Friendly ‘With Profits’ Stocks and Shares ISA receive an annual bonus based on how the fund has performed in the year in question. Shepherds Friendly say that this has worked out at 3% for the last five financial years after all management fees and costs are deducted. Members may also receive a final bonus when they exit their investment. Note that annual and final bonuses depend entirely on how well the fund has performed, and are not guaranteed.

As with all ISAs, any profits are free of income tax and capital gains tax. Everyone has an annual ISA allowance, which is currently a generous £20,000 a year. This may be divided as you wish among a Stocks and Shares ISA, a Cash ISA and an Innovative Finance ISA (IFISA). However, you may only invest in one ISA of each type per financial year.

A major attraction of the Shepherds Friendly ISA is that it is covered under the Financial Services Compensation Scheme (FSCS) up to £85,000 per person. That means if the society were to collapse in a worst-case scenario, your capital would be protected and returned to you by the FSCS.

Bonus Fund

A further benefit of saving with a friendly society is that because of their special status they can offer additional tax-free savings over and above the ISA limit. In the case of Shepherds Friendly, you can save from £10 a month to £25 a month tax-free in their Tax Exempt Bonus Fund. This is also an alternative option if you have already invested in another Stocks and Shares ISA in the current tax year and are therefore excluded from the Shepherds Friendly ISA.

Voucher Offer

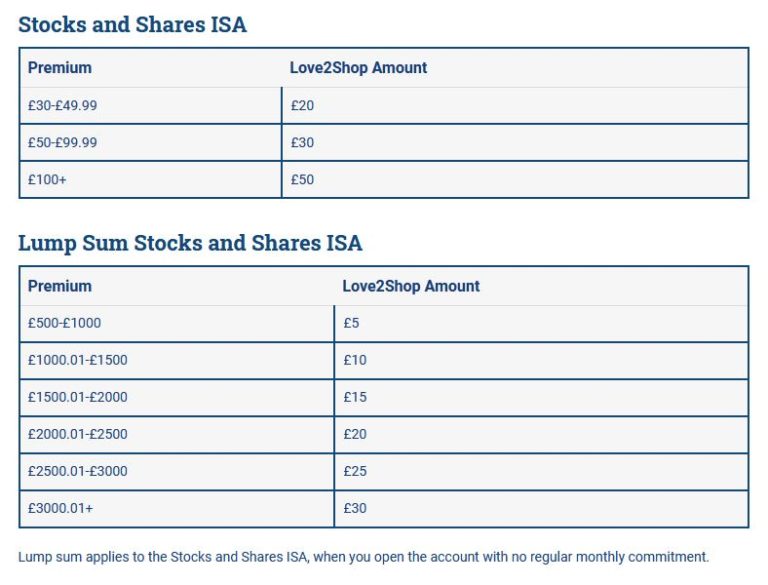

Shepherds Friendly are currently offering investors in their Stocks and Shares ISA a Love2Shop voucher worth up to £50 once you’ve made your first deposit. I’ve copied the actual amount you would receive for Stocks and Shares ISA investments below from the Shepherds Friendly website:

Many of the other financial products sold by Shepherds Friendly include a Love2Shop voucher as well – see this Terms & Conditions page on their website for more info.

Closing Thoughts

If you are looking for a home for some of your savings, Shepherds Friendly offers an interesting option. The society has over 100,000 members, so it is also one that is very popular.

The potential returns from the Shepherds Friendly Stocks and Shares ISA are higher than those currently on offer from banks, though not as high as the potential returns from P2P lending and property crowdfunding (among others). But those investment opportunities do of course tend to be riskier, and your money may not be as easy to access in an emergency. They are also not generally covered by the FSCS guarantee.

As with all stock-market-based investments, there are still risks involved, and past performance is no guarantee of what will happen in the future. Shepherds Friendly is at the lower-risk end of the spectrum, but you should still regard it as a medium to long-term investment (five years at least). With the Shepherds Friendly Stocks and Shares ISA, however, you can at least access some or all of your money at any time if you need it. As stated above, this is not the case with many P2P/property crowdfunding platforms.

As always, if you have any comments or questions about this post, please do leave them below. I’d also be interested to hear from anyone who has invested with a friendly society – be it Shepherds Friendly or another one – what your experience has been and whether you would recommend this method of saving to others.

Disclosure: This is a sponsored post on behalf of Shepherds Friendly. If you click through one of the links in it and make an investment, I may receive a commission. Please note that I am not a qualified financial adviser and nothing in this article should be construed as individual financial advice. You should always do your own ‘due diligence’ before investing, and take professional advice if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

If you ever buy anything online, you can almost certainly save some money by signing up with cashback sites.

In this post I’ll be discussing the top two UK cashback websites, Quidco and Top Cashback, both of which I have belonged to for some years and can vouch for.

You might also like to check out My Money Pocket, a new UK cashback website I reviewed here recently.

The idea behind cashback sites is that they are free to join (although premium membership may be available at a small cost) and provide links to a range of online retailers. When a member clicks through one of these links and buys something (or performs some other action) the cashback site receives a commission from the retailer. Rather than keep all this for themselves, the sites return some or all of the commission they get to the member in question.

So if, for example, you need home insurance, you could click through to a broker’s website from the cashback site. If you then buy a policy from that broker, some or all of the commission paid to the cashback website is credited to your account. You can then withdraw it to your bank account, PayPal or even as vouchers for your favourite merchant.

As mentioned, I have been a member of the two sites mentioned above for several years now, and have made hundreds of pounds from both. Via Quidco, for example, I made £110 when I clicked through their link to the Nutmeg financial services website and opened an investment account with them. Although described as cashback, really this was more like a bonus, as the money I invested with Nutmeg does of course remain mine and I can get it back at any time. My Nutmeg investment has actually risen in value by over £2,600 since I invested, so this has clearly been a worthwhile investment in more ways than one! You can read my full review of Nutmeg here, incidentally.

With Top Cashback I recently pocketed a more modest £40 cashback by switching my gas/electricity provider using a comparison service listed on the website (the cashback came from the comparison service rather than the energy provider). I shall be saving around £500 a year by switching provider, so again the cashback feels more like a bonus than the return of any money I have spent.

You don’t always have to spend money to benefit from cashback sites either. Both Quidco and Top Cashback list offers where you can get money simply asking for a quote or some other action. On Quidco you can earn 50p just by signing up for free with SearchLotto and making 25 internet searches (which also gets you a free National Lottery entry). And on Top Cashback you can get £7.35 if you order and activate a new SIM card from Giffgaff.

You can also make money by introducing friends and family to these sites. Offers change from time to time, but typically you are paid between £5 to £10 when someone joins via your link and earns cashback themselves. The links in this post are referral links, of course.

As you can tell, I’m a big fan of cashback websites. I highly recommend signing up with both Quidco and Top Cashback, as they compete feverishly with each other to offer the best deals.

My money blogging colleague Will Pointing from GreatDealsMadeEasy.com is a fan of Airtime Rewards, a different type of cashback app. He says: ‘I use the Airtime Rewards app as it automatically lets high street retailers pay towards your smartphone bill (in the form of cashback) when you buy items. It is very similar to Top CashBack and Quidco, but you don’t need to manually select the retailers – it is all done automatically (you can also get two separate cashback amounts for a single transaction, essentially getting double cashback). All you have to do is download the app, register your card and then buy as you normally would. For example, if you bought some eye-drops at Boots for £4, you would get 5% back, so 20p. Once you get to £10 in cashback funds, you can select to pay this towards your phone bill – so free money!’

Do Cashback Sites have any Drawbacks?

Not drawbacks exactly, but there are certain things to be aware of.

For starters, you only get paid by the cashback site when they receive payment from the merchant concerned. Sometimes this happens within a week or two but other times it can take a lot longer.

Also, the system depends on your visit to the merchant being tracked by the software, and this doesn’t always work as it should. This happened to me recently when I made a groceries purchase from Asda. It didn’t track for some reason, so I had to open a claim via Top Cashback. Eventually I did get my money, but it took over three months.

So one thing to remember is not to rely on your cashback arriving quickly (or indeed at all). You should only make a purchase via a cashback site if you genuinely want- or preferably need – the item in question and believe it is good value. The cashback then will be a welcome bonus when it arrives.

For Readers Outside the UK

Finally, if you live outside the UK, there are cashback websites in many other countries as well (for example, Top Cashback now has a US operation, Top Cashback USA). Just do a Google search for “cashback website” plus your country’s name and see what results come up. Or check out this article on the MakeUseOf website which lists a number of such sites serving the US. Read the comments section below the MakeUseOf article for a range of international cashback sites as well.

As ever, if you have any comments or queries about Quidco and Top Cashback or cashback sites more generally, please do post them below.

Save

Save

Save

If you enjoyed this post, please link to it on your own blog or social media:

I have mentioned P2P lending platform Ratesetter a few times on Pounds and Sense – most notably in my Ratesetter review.

Ratesetter is one of my favorite lower-risk P2P lending sites. It lets you save via a tax-efficient IFISA and/or an ordinary (taxable) Everyday account.

Although their rates aren’t the highest – currently 3% to 4% – I like the fact that risk is spread across all loans on the platform, with a provision fund to cover any defaults. This means that if someone you have lent money to via the platform defaults, it shouldn’t affect your returns. It also means that – unlike some other P2P lending platforms – there is no need to diversify your lending across the platform in order to control risk.

The Changes

Originally you could invest in Ratesetter in a choice of three different products: Rolling Market, One Year and Five Year.

The Rolling Market was the closest to an ordinary savings account, letting you withdraw some or all of your money any time without penalty. With the 1-year and 5-year products you could still request withdrawals before the full term of the loan, but in those cases a percentage charge was applied. This was 0.3% with the 1-year product and 1.5% with the 5-year product.

Under the new system, loans are spread across all three types of product. What was called the Rolling Market is now an Access account. As before, you can withdraw money from this at any time without penalty. There is just a ‘fair usage’ clause, which prevents investors from lending new money for 14 days after a withdrawal.

Instead of the 1-year and 5-year products, there are now the Plus and the Max. The Plus product pays more interest, but if you want to withdraw you have to pay a ‘release fee’ of 30 days’ worth of interest based on Going Rate at the time of release. And with the Max product, which pays more still, you are charged a release fee comprising 90 days of interest, again based on Going Rate at the time of release.

The Going Rate is the current interest rate for loans in the three product categories. Previously this was set by the market, based on supply and demand. That meant it could fluctuate, sometimes considerably, from day to day and even hour to hour. The interest rate you received could therefore vary a lot.according to when you invested (and when any returns were reinvested).

Under the new system, interest rates are set by Ratesetter themselves. This makes Ratesetter feel more like an ordinary savings provider. Currently the Going Rates are as follows:

Access: 3.0%

Plus: 3.5%

Max 4.0%

If you are already a Ratesetter investor, you may therefore want to reassess the type of product in which your money is held.

If – like me and many others – you put your money into a Rolling Market (now Access) product, you may want to think about transferring some to a Plus or Max account to take advantage of the higher interest rates. There is no greater risk in these accounts, and the only downside is that you will lose 30 or 90 days’ interest if you withdraw early. Doing this is likely to deliver better overall returns, so long as you remain in for at least six months in the case of a Plus account and a year in the case of a Max account. (These are only very approximate figures, as the interest rates paid can change.)

If you want to do this, you can’t (unfortunately) transfer money directly from one type of product to another. Rather – and I have confirmed this with Ratesetter – you will need to start by withdrawing your money from the product it is in currently (e.g. Access) so it goes into your holding account. You can then invest from your holding account into the new product (e.g. Max) that you want. Bear in mind though the 14-day rule mentioned above.

My Thoughts

Overall, I like these changes to Ratesetter. The new Going Rates are admittedly a little lower than the previous market rates. However, I think the greater stability and certainty over the interest rate you will be getting more than make up for this. I also like the new, simpler terms for withdrawing money from your account. I will continue to invest in Ratesetter and regard it as one of the safer (if less exciting) components of my portfolio.

As I’ve noted before on Pounds and Sense, P2P lending does not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme (FSCS). Nonetheless, the rates on offer at Ratesetter are significantly better than those from most banks and building societies. And the existence of a substantial across-the-board provision fund with a strong record of protecting investors from losses clearly offers reassurance.

It’s also reassuring that with all three products you can access your money if needed at any time, even though in the case of Plus and Max you will be charged a release fee for this. Obviously, you shouldn’t therefore put money into the Plus or Max products if you think there is any likelihood you will need it back within a month or two.

Clearly, no-one should put all their spare cash into Ratesetter (or any other P2P lending platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P lending isn’t a way of hedging your equity-based investments directly, but it does definitely help spread the risk.

If you would like more information about Ratesetter, please see my original Ratesetter review (which I will be fully updating soon).

Welcome Offer

Currently if you are new to RateSetter you can get £100 added to your account for free just by signing up and depositing £1,000. Full terms of the offer are reproduced below, and you can also find them on the RateSetter website.

You can take advantage of this offer so long as you

have not previously registered with RateSetter;

register after 27th March 2020; and

deposit a minimum of £1,000 through the RateSetter ISA or Everyday account and this is matched within 56 calendar days of opening an account.

Your bonus will be credited to your Everyday Account and invested in RateSetter’s Access (instant access) product at the going rate (currently 3%) within 30 working days of qualifying. From here you can transfer it to your ISA account if you like or simply withdraw it.

My Thoughts: This is a great offer from RateSetter if you are new to the platform. If you invest £1,000 and keep it there for a year, then including the £100 welcome bonus you will get a total return of between 13 and 14 percent for the first year (depending on whether you opt to invest your money in the Access, Plus or Max product). As a matter of interest, this is the same welcome offer I took advantage of when I signed up with RateSetter two years ago, and my bonus £100 was credited without any issues (or prompting from me) twelve months later.

Obviously if you need your £1,000 at any time, you can withdraw it (normally within 24 hours). This will though mean you don’t receive the £100 welcome bonus at the end of the first year.

Clearly, this is a generous promotional offer by RateSetter and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

If you have any comments or questions about this post, as always, please do leave them below.

Disclosure: As stated above, this post includes my referral link. If you click through and make an investment, I will receive a bonus for introducing you. This has no effect on the terms or benefits you will receive. Please be aware also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. You should do your own ‘due diligence’ before making any investment, and take professional advice if at all unsure how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

I recently received an email telling me about a new (free) cashback site called My Money Pocket. As a fan of cashback sites I was very happy to check it out.

My Money Pocket is a UK site. It is therefore entering an arena currently dominated by what might be called the Big Two here, Quidco and Top Cashback.

As with those two sites, My Money Pocket offers members the chance to earn cashback by following links to a variety of online retailers. These are affiliate/referral links, and My Money Pocket receives commission for any purchases made by people clicking through them. My Money Pocket then shares this commission with the member concerned.

Getting Started

Before you can use My Money Pocket to get cashback, you do (of course) need to register on the site. All they require for this is your email address and a password. On the plus side, that makes signing up very quick and easy. On the minus side, I find it slightly odd that they don’t ask for your name, which means you can’t see this when you are signed in. That could be problematic if you share your computer with other family members, as you may not know which of you is actually logged in!

I did ask My Money Pocket why they don’t ask for a name when registering, and they said it was to avoid privacy issues. Personally, though, I would much sooner see “Welcome, Nick” (or whatever) at the top of the screen to reassure me that I am actually signed in to my own account.

Once you are logged in you can start earning cashback by clicking through the links provided to a wide range of online stores. Most of these are also available with Top Cashback and Quidco, but the cashback rates (and terms) are different – better in some cases, worse in others. As with all things shopping related, it really does pay to shop around!

The website looks bright and welcoming, but a large area at the top is taken up by an offers carousel, which personally I find a bit obtrusive. I thought the site navigation was okay, but not quite as intuitive as the Big Two. I would prefer a traditional tabbed navigation menu of the sort that is used on Top Cashback and Quidco (and many other websites), but maybe I am just being a bit old-fashioned.

There is a drop-down Categories menu at the top left of the screen. This takes you to cashback offers in the following categories:

Fashion

Food and Drink

Health and Beauty

Electricals

Travel

Broadband

Entertainment and Leisure

Utilities

Gifts

Mobile

Home and Garden

Free Cashback

Gaming

Shopping

Office and Business

Sport

Gambling

Within most of these categories there are sub-categories as well. Incidentally, ‘Free Cashback’ lists offers where you don’t have to spend money to get cashback – for example, you might just have to request a quotation for your car insurance.

As with Top Cashback and Quidco, once you have made a purchase with one of the merchants on My Money Pocket, you will then have to wait for your cashback to be tracked, approved, paid and credited to your My Money Pocket account. You will then be able to withdraw this money, either to your bank account (through BACS) or via PayPal.

One other feature is that you can refer other people to My Money Pocket and receive £5 cashback yourself when they have earned a minimum of £10 in cashback. Note that all links in this blog post include my referral code 🙂

Final Thoughts

It’s early days for My Money Pocket and the site is still to some extent a work in progress. Nonetheless, there is nothing to lose by signing up for free now and checking out the deals on offer. As I said earlier, I would recommend checking and comparing My Money Pocket, Top Cashback and Quidco to see which site is currently offering the best terms for any retailer you intend to buy from.

As always, if you have any questions or comments about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

The full cost of an NHS prescription in England is now £9. If you need regular medications, that can quickly add up to a substantial sum.

The good news, however, is that many people are entitled to free prescriptions, and others have methods open to them to save money.

Before I go into that, though, I should point out that all NHS prescriptions are now free in Scotland, Wales and Northern Ireland. So if you are lucky enough to live in one of these countries, you won’t normally be required to pay for your prescriptions.

Who Is Eligible for Free Prescriptions in England?

Here is a list of everyone eligible for free prescriptions in England, taken from the NHS website:

You can get free NHS prescriptions if, at the time the prescription is dispensed, you:

are 60 or over

are under 16

are 16 to 18 and in full-time education

are pregnant or have had a baby in the previous 12 months and have a valid maternity exemption certificate (MatEx)

have a specified medical condition (see below) and have a valid medical exemption certificate (MedEx)

have a continuing physical disability that prevents you going out without help from another person and have a valid MedEx

hold a valid war pension exemption certificate and the prescription is for your accepted disability

are an NHS inpatient

The medical conditions which qualify you for free prescriptions include cancer, diabetes (unless treated by diet only) and hyperthyroidism. For the full list, see this web page from the NHS Business Services Authority. If this applies to you, you will need to complete an application form FP92A from your GP, who will also sign it to confirm that you have the qualifying condition stated. Certificates are valid for five years, and once you have one you will be eligible for free prescriptions for any condition, not just the one through which you qualified.

You’re also entitled to free prescriptions if you or your partner (including civil partner) receive, or you’re under the age of 20 and the dependant of someone receiving:

Finally, you will qualify for free prescriptions if you’re entitled to or named on:

a valid NHS tax credit exemption certificate – if you do not have a certificate, you can show your award notice; you qualify if you get Child Tax Credits, Working Tax Credits with a disability element (or both), and have income for tax credit purposes of £15,276 or less

a valid NHS certificate for full help with health costs (HC2)

People named on an NHS certificate for partial help with health costs (HC3) may also get help with prescription costs.

What If You Don’t Qualify for Free Prescriptions?

If you don’t qualify for free prescriptions on any of the grounds set out above, there are still some things you can do to reduce the cost of your prescriptions.

One is to buy a Prescription Prepayment Certificate (PPC). These are available for three months or a year and entitle you to free NHS prescriptions for all conditions during this time.

At the time of writing a three-month PPC costs £29.10 and a year’s costs £104. In general, if you need more than one prescription a month and have to pay for it, a PPC will work out cheaper.

If you have a long-term condition, a one-year certificate will usually represent the best value. A person getting two prescriptions a month would save more than £100 a year by this means compared with paying for individual prescriptions. The simplest way to get a Prescription Prepayment Certificate is to apply via the NHS Prescriptions website.

Finally, it’s worth bearing in mind that some medications, especially for minor conditions, are available over the counter without a prescription. This can often work out cheaper than paying a prescription charge.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a post for you on how to save money on clothing.

Like it or not, we all have to spend money on clothes. And over a year those costs mount up.

Any of my friends will tell you that clothing isn’t my specialist subject, so I asked my fellow UK money bloggers for their advice on this subject. I’m pleased (and grateful) to say that they came up trumps 🙂

So here, without further ado, are the UK money bloggers’ top tips on how to save money on clothes shopping…

1. Kirsty Holden from The Money Saving Mum says, ‘Go to outlets! My new fave shop is a local Next outlet. I’ve always been a Primark girl but honestly the quality is getting worse and I only ever buy from there now if it has a red tag on it 🤣 I would never normally go into Next and pay their prices but the outlets are fab!’

2. Fiona Elizabeth Hawkes from Savvy in Somerset writes, ‘Buying second-hand from charity shops can save you a fortune and means you could afford brands you might not otherwise be able to, meaning better quality clothing for less money. Also they often have lots of brand new clothes that have never been worn with the tags still attached.’

3. Emma Jackson from Bee Money Savvy says, ‘If you’re a student, make sure to check to see if the retailer offers student discount either through the UNiDAYS app or the TOTUM/NUS card. Student discounts can save you anything between 5% and 20% at most major retailers.’

4. Laura Dempster from Thrifty Londoner writes, ‘If I’m looking for something specific I always check eBay first! I’ve got brand new jeans for £15 instead of £30 just by looking on eBay. I’ve also found that brand new books are often cheaper on eBay than Amazon.’

5. Stephanie Addison from Debt Free Family advises, ‘Buy winter clothes at the end of winter. Likewise, buy summer clothes at the end of summer. They are so much cheaper then, when the shops need to clear out.’

6. Emma Bradley from Emma’s Savvy Savings says, ‘Voucher codes – shopping online gives you extra discounts via voucher codes (quick Google search) and/or Top Cashback and Quidco. You can also try on the clothes in the comfort of your own home and not feel pressured or rushed into buying.’

7. Lisa Garwood-Cross of Living Thrifty says, ‘Take a look at websites like Everything 5 Pounds. They are often selling end-of-line high street items brand new for a fraction of the price. There may be limited sizes but the website often has loads to choose from. You won’t know which brands they are until they arrive, but you’d be amazed at what you can get for a fiver!’

8. Emma Bradley from Emma’s Savvy Savings adds, ‘Another one is not so obvious but use a personal shopper. They really are brilliant at finding and putting together outfits that suit your body shape. This saves money as you don’t buy things that you later regret and store in your wardrobe with the tags still on!’

9. Francesca Henry of From Pennies to Pounds says, ‘If it’s for a special occasion, ask your friends and family if they have anything that you can borrow first. You can return the favour – it works particularly well if you have a lot of weddings to go to!’

10. Faith Archer from Much More With Less says, ‘Pick up clothes with your food shopping. I’ve nabbed great basic T-shirts and workout gear from supermarket ranges like Tu at Sainsbury’s and George at ASDA, and they tend to offer a wide range of sizes. Great for bargain school uniform too, especially in the Tu 25% off sales.‘

11. Nikki Ramskill, who blogs as The Female Money Doctor, says, ‘I save small amounts of money every month and then when the sales are on, buy what I need then. Knowing WHAT I need really helps before I go. Do I really need another pair of jeans, when actually it’s work dresses I am lacking, for example. Saving money to have a few big shops a year to search for key pieces and creating a capsule wardrobe saves me so much money.’

12. Hayley Muncey of Miss Manypennies writes, ‘Try looking on Facebook buy/sell groups in your area. People will often have a clear-out and offer a huge bundle for free or very cheap. Then you can look through, pick out anything you like, and pass the rest on again.’

13. Claire Roach from Daily Deals UK says, ‘I clothes swap with friends – we both get to refresh our wardrobes that way for nothing. I have asked on Facebook as well once and got a great response. I got three new dresses and got rid of three that I hadn’t worn for years.’

14. Lynn James, who blogs as Mrs Mummypenny, recommends, ‘Create a capsule wardrobe! My friend Claire came shopping with me and created a wonderful capsule wardrobe for me. Everything goes with everything. And from maybe 10 items of clothing I have 20+ outfits, all timeless styles and colours. I still wear all the clothes now, bought three years ago.’

15. Emma Maslin from The Money Whisperer says, ‘I hate clothes shopping and do most of it online. I am on the email lists for my favourite brands so whenever they have a sale or promotion, I get notified and I buy then.’

16. Jennifer Graudenz of Monethalia comments, ‘I like going to fashion outlet stores and buy from their clearance sections. There isn’t as much choice, but getting as much as 90% off the normal retail price is possible.’

17. Clair Louise of Thrifty Clair says, ‘Sites like Everything 5 Pounds [also mentioned by Lisa of Living Thrifty, above] and Single Price sell ex-high street stock for a fiver an item. If you’ve got a good eye you can get some amazing items for a fraction of the original cost.’

18. Katie Schulten of Student Skint says, ‘If you’re planning on buying something brand new that’s not an immediate buy, try it on in store so you know your size then search online – eBay, Depop, Facebook marketplace, etc. – for someone selling the same one brand new with tags for much cheaper…you know it’ll fit! Just check the description for the reason they could be selling.’

19. Andrew Young from Capital Matters writes, ‘Don’t buy too cheap and don’t buy too expensive. To use an example from my own life, I used to buy £20 shoes. They rarely lasted more than six months. I switched to £45 (on-sale) Ralph Laurens. They’ve lasted years and they’re still going strong, effectively saving me money. But anything priced above that? Likely just a waste.’

20. Katie Watkins from Katie Saves says, ‘Ask for vouchers for birthdays and Christmas. I know some people don’t like giving/receiving vouchers but as I never buy for myself I look forward to having vouchers specifically to buy anything new I need.’

22. Scott Dixon of Thegrumpygit.com writes, ‘I have just been to the Sainsburys Tu sale and bought a pair of jeans on the half price rack that still qualified for the 25% off (£16 down to £5.50 less £3 on a £20 spend with a Nectar card coupon = £2.50). I also got another pair of jeans £16 & trainers £14 with 25% off. Wait for the annual Tu sales at this time of year, go with a coupon and search through the 50% off rail is my tip!’

23. Jim Gall of Money Blog Scotland writes, ‘I shop in GAP a lot and they ALWAYS have discounts on. Their high street stores almost always have 40% off, and the online store always has discounts on. Plus if you install the app, you get a voucher code which means you get a further 5% off on top of your original discount. I have NEVER paid the listed price for anything in GAP. And it’s all good quality stuff which lasts for ages.’

24. Finally, Sian Melonie, who blogs as Little Miss Frugal, is another fan of cashback websites. She says, ‘If there is something that l have my eye on from a particular store, I always check Top Cashback and Quidco to see what cashback offers are available from the store I’m wishing to purchase from. It’s then essentially free money back!’

Thank you so much to all my fellow UK money bloggers for sharing their top tips. I hope you will agree there are some great money-saving ideas and resources listed here.

I guess I should offer a tip as well, so mine is to sign up with the loyalty scheme of any clothes store you shop at regularly. Being a gentleman of a certain age, two stores where I often shop for clothes are Marks and Spencer and Debenhams.

I have a Sparks card from M&S, which gets me special offers and discounts from the store and the occasional freebie. And I have a Debenhams credit card, which (among other benefits) earns me points every time I shop there. These are then converted to Debenhams vouchers every three months. Note that I don’t advocate borrowing on a credit card as the interest quickly mounts up, but as long as you pay off your balance in full every month there won’t be anything more to pay.

Finally, please do check out the money blogs listed above – they are all linked from the blog names – and sign up to follow any you enjoy.

As always, if you have any comments or questions on this post, please add them below. I would also love to hear any other tips you may have for saving money on clothes shopping.

If you enjoyed this post, please link to it on your own blog or social media:

A couple of weeks ago I got home from a short break to find a letter and glossy leaflet on my doormat extolling the benefits of batteries for solar panel owners.

The letter said the company had purchased a list of names of local solar panel owners including my details. That put my back up a bit, as I’m not keen on having my personal information bought and sold. But I guess it’s publicly available info, so there isn’t really anything I can do about it.

Anyway, while I didn’t reply to the sales letter, it did inspire me to do a bit of research into solar energy storage batteries and whether they are worthwhile. That turns out to be quite a difficult question to answer. It doesn’t help that much of the information online comes from solar battery suppliers and installers, who are not exactly unbiased.

So here are my thoughts, based on what I have been able to find out in conjunction with my own experiences as a solar panel owner.

The Idea

The idea behind solar batteries is simple and appealing.

Solar (photovoltaic) panels generate most power when the sun shines, but this is probably not when you need it the most. If they are generating electricity in the day when you are out at work, some of that power is likely to be going to waste. (Yes, you might be able to sell some back to the grid, but most home-owners are paid a – low – ‘deemed’ tariff for this based on the total amount of power their panels generate. It makes no difference to this how much of the electricity generated you use yourself.)

If you have batteries, though, these can be charged by your panels when they are making more electricity than you need, and then used to provide power at other times (e.g. in the evening) when you need it. This should reduce the amount of electricity you have to buy, thus cutting your bills. It may also give you a backup in the event of power cuts (although don’t bank on this – see below).

The Reality

That all sounds great in theory, but the reality is a lot more complicated.

First of all, solar storage batteries are still new and, to a degree, untested technology. They are also expensive. To have batteries supplied and fitted to an existing solar panel installation is likely to cost anywhere from £5,000 to £10,000.

Solar batteries also have limited lifespans. Because the technology is so new, nobody is really sure how long they will last, but I have seen figures of 5 to 15 years quoted. That means you are likely to need to replace your batteries at least once during the 20- to 25-year working life of your solar panels.

It’s also worth bearing in mind that all batteries become less efficient over time, reducing the amount of electricity they are able to store.

My Calculation

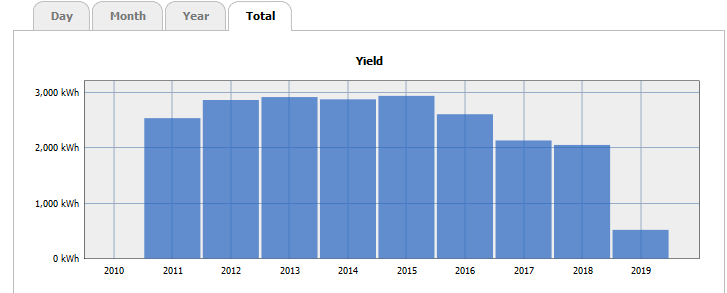

I thought I would look at my own solar panels as an example, to see if the sums added up. First of all, here is a chart showing the total amount of electricity generated by my panels since they were installed in 2011.

As you can see, the maximum my panels have generated is just under 3,000 kWh in 2015 (after that the output declined somewhat, for reasons discussed in this blog post). For the sake of my calculation, though, let’s use a figure of 3,000 kWh for the amount of power my panels generate annually.

Now, to work out how much power could be saved by installing batteries, we need to know what proportion of power generated is surplus to my requirements and currently ‘wasted’. Because I work from home and am here in the day most days, I can’t believe this is any more than 30 percent. In reality it is probably less, but I’ll use 30% for my calculation.

Let’s now assume that batteries would allow me to save the whole of that 30% (in reality that’s highly unlikely for reasons I’ll discuss shortly). That means I would be saving 3,000 kWh x 30% = 900 kWh. The electricity companies in my area currently charge in the region of 20p per kWh (including VAT), so the saving on my bill would theoretically be worth 900 x 20p = £180 a year. Assuming the cost of buying solar batteries and having them installed was an optimistic £5,000, that means it would take 5000/180 = 28 years for the cost to be recouped – well above the expected lifespan of the battery (or the panels, for that matter).

Even if I was out a lot in the day, to the point where I could save 60% of the power generated by my panels if I had batteries, the breakeven period would be 14 years. And remember, this is also assuming the highest possible output from my panels every year and 100% battery efficiency, neither of which will be the case in reality.

Complications

There is one thing you may have noticed that I didn’t account for in my calculation, and that is the fact that electricity prices go up every year. That will, of course, have the effect of increasing the potential savings from batteries and reducing the time it takes to break even. If electricity prices go up dramatically, that will certainly make solar storage batteries more attractive.

On the other hand, there are some negative factors to take into account as well. Here are just some of them.

1. Batteries are not 100% efficient. Some energy is lost charging the battery and then releasing energy from it. The technical term for this is round trip efficiency. Typically this figure is around 80%, meaning that for every 5 kWh going in to your battery, you will only get 4 kWh of useful electricity out.

2. You can only charge a battery to its maximum (100%). If on a sunny day the batteries become fully charged, any surplus energy generated after that will simply go back to the grid.

3. If you discharge a battery fully this can significantly reduce its life expectancy. Technically this is known as Depth of Discharge, or DoD for short. Most manufacturers specify a maximum DoD for optimal performance. For example, if a 10 kWh battery has a (typical) DoD of 90 percent, you shouldn’t use more than 9 kWh of the battery before recharging it. In practice, an electronic charge controller prevents over-discharging (and over-charging) from happening. The effect of this is, of course, to reduce the amount of useful energy a battery can store.

4. Batteries become less efficient over time. This varies according to the type and make of battery, but typically over 10 years efficiency will reduce by 30%. Again, this reduces the amount of electricity batteries can store and the potential savings to be made. If you are unlucky and your battery fails completely just as the warranty expires, you could be looking at a large overall loss.

5. If you use batteries to store power, this may involve sacrificing the payments you would otherwise receive for exporting power back to the grid. This may not matter if you are getting a ‘deemed’ payment based on electricity generated (as is the case for many owners currently). But with the new generation of smart meters which can measure how much electricity you are actually returning to the grid, you will certainly end up making less money this way if you divert excess electricity to batteries instead.

6. As well as the cost of buying and installing solar batteries, there is also VAT to take into account. At the time of writing this is 5%, but it is going up to 20% in October 2019. This would add £1,000 to the price of a £5,000 battery installation.

7. Finally, although solar batteries may give you a backup power source in the event of power cuts, it appears this cannot be relied on. A survey of solar battery owners by The Consumer Association found that several people reported that in the event of a power cut, their batteries stopped working as well. That is despite promises made by sales people that this wouldn’t be the case.

My Conclusions

As I said earlier, this is a complicated field and I make no claim to any special expertise on it. However, based on my own data and research, here are the conclusions I have reached.

1. If you and/or other family members are typically at home in the day, it is doubtful whether you will save enough money by installing batteries to cover the cost, let alone make any profit. The same may apply if you use electricity in the day for other purposes when nobody is there in person, e.g. washing laundry, heating water, running a dishwasher, etc.

2. If nobody is in your home for most of the day and you aren’t using any significant amount of electricity during daylight hours then the savings from batteries may be more worthwhile. But bear in mind that you are still likely to be around (and using electricity) at weekends, early mornings, evenings, holidays, sick days, and so on. And some household appliances such as fridges and freezers go on using electricity all of the time.

3. If the price of energy rises sharply, solar batteries may become a more attractive proposition. However, they are expensive to buy and install, and have various limitations (discussed above) which may reduce the benefit you get from them. They will probably also have a shorter lifespan than your panels, meaning they will need replacing at least once over the lifetime of your panels. And they will in any event decline in efficiency over time.

4. Likewise, if battery prices fall – and the technology improves – that will increase the attractiveness of solar batteries in future. But of course, if you are considering whether to get batteries now, you can only base your decision on what is currently available.

5. If you are buying a new home and/or new solar panels, buying batteries at the same time is likely to be more cost-efficient (and involve less hassle) than retro-fitting them. In this article I am mainly addressing existing solar panel owners.

6. I am also looking at this primarily from a financial standpoint. There is a case to be made for installing batteries to help contribute to the fight against global warming and climate change, although there are obviously also environmental costs involved in battery manufacture. In any event, it is for each individual to decide how important this is to them and whether the environmental benefits of having batteries with their solar panels really do stack up.

7. Some companies are currently making a big push to promote solar batteries, and it does appear to me that some of the claims made on their behalf are exaggerated to say the least. If you are thinking of getting solar batteries, be sure to do your own ‘due diligence’ and don’t believe everything you read on company websites or are told by pushy salespeople. In particular, be very sceptical about pie-in-the-sky estimates over how much money batteries may be able to save you. I found one website claiming that 75% of the power generated by solar panels is typically wasted, which is frankly laughable.

8. Don’t, either, be swayed by arguments that you need to order now before VAT rises to 20% in October. This is (unfortunately) true, but it doesn’t make the case for installing batteries any stronger.

In summary, for most existing solar panel owners, I don’t believe that installing batteries is likely to make economic sense at present. I don’t, therefore, intend to do so myself. If prices come down and the technology improves, however, the equation may change (and reducing or scrapping the VAT would help too). This is something I will continue to monitor, and if I change my mind in future I will of course let Pounds and Sense readers know!

So those are my thoughts, but what do YOU think? I’d love to hear from you, especially if you have solar batteries yourself or are actively considering them. Please feel free to post any comments or questions below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have an eye-opening infographic for you. Do you ever wonder how you compare with the average Briton when it comes to spending your pay cheque? Are you content with your rainy-day fund or do you worry you haven’t got as much squirreled away as your friends or colleagues?

Worryingly, it appears most Brits are spending more than they bring in each month. Moreover, there is a steady shift from cash and cheques toward plastic and electronic payment methods.

According to the Office for National Statistics, British households have spent more than they received for an unprecedented nine consecutive quarters, amid a longer squeeze on real incomes. What’s more, households across the country have been net borrowers in every quarter between October 2016 – when living costs started to rise after the Brexit vote – and December 2018.

Check out the full infographic by Peachy below which neatly reviews the key household spending statistics in the UK:

Personally, I find the saving stats at the end of the infographic especially worrying. Large numbers of people say they have no savings whatsoever (and even £100 is a tiny amount really).

Living from one payday to the next is a precarious existence, though as the graphic indicates many UK citizens do exactly this. Nonetheless, it makes you very vulnerable when a sudden change of circumstances occurs that reduces your income or increases your expenditure.

An example from my own experience is when, almost five years ago, I was diagnosed with prostate cancer. My treatment involved two months of radiotherapy, requiring daily trips of 30 miles each way to the Royal Stoke University Hospital in Stoke-on-Trent. It was simply impossible for me to go on working during this time, so (as I was self-employed) my income took a big hit. Fortunately I had enough in the bank to cover my lost earnings during this time. If I hadn’t, it would have added to the already considerable stress I was under. (And yes, I’m doing fine now, thank you.)

i think it’s particularly important for older people to have some savings set aside. Not only are health problems more likely as you get older, your long-term earning potential reduces. Nobody should be entering later life with nothing in the bank to tide them over if – or more likely when – the need arises.

So I strongly believe everyone, whatever their age, should do their utmost to build a savings pot. Of course, for people on modest incomes that’s not always easy. So I recommend a two-pronged approach of reducing your outgoings and boosting your income (e.g. by starting a side hustle).

Saving money and making money are, of course, subjects I cover regularly on Pounds and Sense. By doing these things, you should hopefully build up a pot that will stand you in good stead when life hands you those inevitable lemons.

I guess another reason people aren’t saving as much – or at all – these days is the very low interest rates on offer from banks and other savings institutions. In itself that isn’t a good enough reason for not having a savings pot, but of course it does mean it’s extra important to look around for the best deal you can find.

In addition, once you have enough cash savings to tide you over for a few months, it’s good to think about investing some of your extra money for potentially higher long-term returns. Again, investing is a subject I cover regularly on Pounds and Sense. I won’t go into detail about this now, except to say that a good starting point is a tax-efficient Stocks and Shares ISA (I like Nutmeg’s automatically diversified robo-adviser platform myself). And you should put as much money as you can into your pension, of course.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Lots of us need some extra help at times, but we don’t want the hassle (or expense) of hiring an employee. If that applies to you, have you considered using a remote (or virtual) assistant?

As the name suggests, remote assistants don’t work from their client’s premises. Rather, thanks to the power of the internet and electronic communications, they work remotely from another location, which might be an office or their own home.

They could therefore be based anywhere in the world as long as it has the connectivity required. For cultural and communication reasons, however, there are obviously advantages to using assistants in the same country or area.

So how do you hire a remote assistant? There are various methods, but if you want a simple, cost-effective solution, you might like to check out Remote Bob. This fast-growing company has offices in London and Croatia and offers a remote assistant service to individuals and businesses across the UK (and further afield).

So what services can you expect your remote assistant (or team) to offer? Here are just some of the services Remote Bob offers to individuals:

Planning holidays

Ordering groceries or food

Booking sports activities and hobbies

Organizing holidays

Searching for a new flat or apartment

Helping with online clothes shopping

Helping with picking restaurants

Filling in some forms on your behalf

Managing your household

Managing your lifestyle

Buying birthday presents

Managing personal budgets

Research on properties to buy

For entrepreneurs and businesses, the services Remote Bob offer include:

Supporting office teams and directors with general operational tasks

Scheduling and coordinating meetings, appointments, presentations, and other office-related events

Opening, sorting and distributing incoming electronic correspondence

Handling requests by answering questions and providing information and data

Organizing and scheduling travel arrangements

Booking conference calls, rooms, taxis, couriers, hotels, etc.

Developing and updating administrative workflow to improve efficiency

Preparing and modifying documents including correspondence, reports, drafts, memos and emails

Assisting in the preparation of presentation materials and agendas for meetings

Maintaining electronic filing systems

Resolving administrative problems and inquiries

Performing general accounting and bookkeeping duties

Examining and reconciling expense reports of office staff

Writing letters and emails on behalf of office staff

Maintaining up-to-date employee holiday records

The staff working at Remote Bob are all EU-based, thus minimizing any potential issues with time zones and significant cultural differences.

Remote Bob handle people management, regulatory arrangements and payroll, so you don’t have to worry about this. They say they only work with proficient, well trained and approved specialists, and pledge to deliver work on time and under budget.

Special Offer

Remote Bob are kindly offering Pounds and Sense readers a huge (36%) discount on their service. By clicking through this link you can request their Personal Assistant service for one month (five hours per week) for £320 per month instead of the normal £500. Just remember to enter the code SENSE2019 in the Discount Code box.

Note that completing the inquiry form does not create any obligation to buy. Clearly everyone will have their own particular requirements for their remote assistant/s, so Remote Bob say, ‘Talk to us, tell us about your goals, your worries and your hopes. We will then construct a customized route for all your needs.’ Only when you are fully satisfied with the proposed solution will you be asked to make any commitment to buy.

I would also highly recommend you spend a little time looking around the Remote Bob website, as this will give you a good idea of the range of services on offer and how the platform works in practice.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post. If you click through a link in it and make a purchase, I will receive a commission for introducing you. This will not affect in any way the service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

As from today (1st July 2019) you can switch your mobile network provider with just a single text message. This is good news as it makes switching and saving money even easier.

If you want to keep your current number (as most people do) the process now is as follows:

1. Request a switching code by texting PAC to 65075. This is a free call.

2. You will then immediately receive a PAC (Porting Authorization Code) from your current provider.

3. You then pass this code on to your new provider when you sign up with them. They are obliged to switch you within one working day.

If you don’t want to carry over your current number, there is a slightly different procedure.

1. Text STAC to 75075 to request a Service Termination Authorization Code.

2. You then pass the STAC you receive onto your new provider. There is no need for you to contact your current provider to cancel your contract with them.

Either way, you should also receive information from your current provider about any early termination charges or pay-as-you-go credit balances that may apply.

PACs and STACs are valid for 30 days, after which if they haven’t been used they simply expire. You would then need to request another one.

This new method makes it easier and less hassle to change mobile service providers. In particular, it avoids the awkwardness of having to phone your current provider and ask them for a switching code. Many people hate doing this, as it gives your current provider the chance to twist your arm to try to persuade you to stay with them.

As regards deciding when and where to switch, that is a topic for another post. However, many price comparison services (e.g. Compare the Market and USwitch) now also allow you to compare prices for mobile phone tariffs and suppliers. I also recommend Billmonitor, a free service that analyses your usage and recommends the best deal for your needs. They send you monthly updates by email as well.

As always, if you have any comments of questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media: