Today I have a guest post for you from my friends at Broadway Autocentres. As specialists in this field, they know exactly what it takes to get the most out of your car tyres.

Over to the experts, then…

When it comes to driving your own car, all the costs seem to mount up. If you’re not saving for the next service, you’re putting money aside for the MOT. And just when that is out of the way, you realise that you don’t know how old your tyres are or when they will need to be replaced.

There is no way to have your car use less fuel or oil, and skipping services is a bad idea – but if you can reduce the wear and tear on the vehicle whenever possible, so much the better for your purse or wallet.

Tyres are one of the biggest expenses you will face, so let us look at five ways to get the most out of your tyres before you bow to fate and replace them!

Buy Them in Twos

Buying a set of four tyres can seem impossible with a tight budget, so why not replace your tyres in twos instead? Depending on whether your car is front or back wheel drive, either the front set or back set will take the most punishment. It is the most worn tyres that should be replaced, with the more lightly worn set moving to take their place and the new tyres going where they will receive less wear. This system may seem inconsistent, but it will ensure that you stay safe while on the road without needing to spend a lot of money all at once.

Drive Sensibly

Drive according to the Highway Code at all times and resist the temptation to put your car through its paces. Maintain a safe speed, avoid rough or unsurfaced roads, and increase and decrease speed slowly whenever possible. All of these will help to keep your tyres in good condition for longer, so you can keep saving for their eventual replacements.

Buy the Best

While it may seem counter-intuitive, buying the best quality tyre you can afford is often more economical when taken over time. Budget tyres are sometimes made with flaws that can weaken the tyres more quickly, or with inferior rubber that begins to crumble and break apart. Better quality tyres will last better – sometimes twice as long as budget tyres, thereby comparatively halving their cost to you. You can book your tyres in Buckinghamshire at Broadway Autocentres (01494 680914).

Regular Checks

Get into the habit of checking your tyres often, looking for early signs of damage or weakness. In many cases, prompt corrective action or a swift repair can keep the tyre in place for some time, giving you the chance to continue getting out and about without suddenly needing to spend money on a new set or pair of tyres.

Proper Inflation

Modern tyres – no matter whether budget or premium – are designed to be used within a narrow recommended range of pressure, and will often perform poorly outside of this range. Keep your tyres inflated to within the range recommended by the manufacturer (this can be found online, sometimes on the tyre itself, or inside the car owner’s handbook) to ensure that not only do your tyres last as long as possible, but you are safer on the roads during this time. Correctly inflated tyres also aid fuel economy, saving you money that way as well.

Thanks again to my friends at Broadway Autocentres for their expert advice. As always, if you have any comments of questions about this post, please do leave them below.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at P2P property investment platform Kuflink.

I have been investing with Kuflink for five years now, so this is a fully updated repost of my original review.

What is Kuflink?

Kuflink is an online platform offering opportunities to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage.

Kuflink offer three types of investment, as follows:

Auto Invest and IFISAs both automatically invest your money across a number of loans and pay a fixed interest rate, typically between 7 and 9%. You can choose a 1-year, 2-year or 3-year term, and interest is paid annually (it is automatically reinvested at the end of each year with the two-year and three-year products). The Auto-Invest product is basically the same as the IFISA, but without the tax-free wrapper.

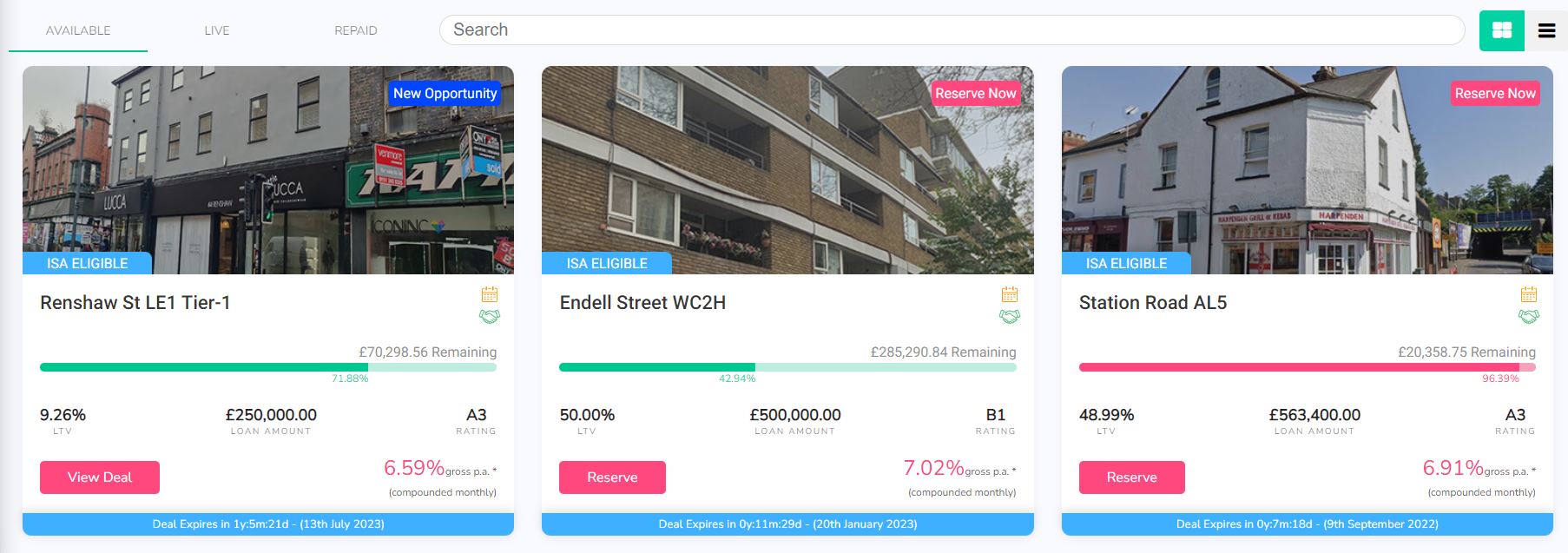

At one time only the Auto-Invest option was available for IFISAs, but nowadays you can choose your own investments if you prefer. The great majority of Self-Select loans on the Kuflink platform are IFISA-eligible. If you check out the Self-Select listings on the Kuflink website (see image below), this will tell you whether any particular loan is IFISA-eligible or not.

Individual Select-Invest loans pay interest rates varying between about 6 and 7.2%, depending largely on the LTV of the loan (loan to value, a measure of how secure the loan would be in the event of a default). The higher the LTV, the riskier the loan, and – other things being equal – the higher the interest rate paid in consequence. You can see a screen capture below of three Select-Invest loans available on the platform at the time of writing.

As a reasonably experienced P2P investor, I put my money into Select-Invest loans. These typically have a duration of six months to a year and (as mentioned above) pay interest from around 6 to 7.20 percent. That obviously isn’t as much as some P2P property platforms (e.g. BLEND), but I think it represents a fair balance between risk and reward. Kuflink also invest in every loan themselves up to 5% of the value of each loan – so, as the expression goes, they have skin in the game.

My Kuflink Review

I found signing up with Kuflink a quick and easy process. They do the obligatory money-laundering checks, but in my case anyway this was all done electronically behind the scenes. I uploaded a copy of my passport and was approved almost immediately. I started by depositing £500, but you can start with as little as £100 if you like.

Initially I put my money into a 12-month loan paying 7% annual interest. One good feature I didn’t grasp initially is that with Select-Invest loans interest is paid monthly. So once a month I receive interest payments on all the loans I am currently invested in. This is paid into a wallet, from which you can either withdraw to your bank account or reinvest.

Kuflink recently introduced an option to have monthly loan repayments automatically reinvested rather than paid into your account as cash. This effectively boosts your interest rate by the power of compounding, as you then receive interest on the reinvested payments as well. Currently this option is available for most, but not all, loans on the platform. You can see which of your loans compounding is available for via your Kuflink dashboard.

I have continued to invest in Kuflink, and have also reinvested in new loans when the original ones were paid off. Another good feature is that money invested in a loan but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

There have been no defaults so far on any of my loans, and Kuflink say on their website that to date nobody has lost a penny on their platform. I have experienced short delays with loans being repaid, but in such cases you continue to earn interest, of course.

Secondary Market

A new feature on Kuflink I like is the Marketplace (secondary market). Here you can buy loan parts from other investors who want to sell up early. You can also put up for sale any (or all) of your own loan parts.

The number of loan parts listed in the Marketplace went up in the early months of the pandemic, as many investors understandably wanted (or needed) to access their cash. This created short-term buying opportunities which I was happy to take advantage of. Loan parts offered via the Marketplace typically have only a few months to run, so you can expect to get your capital back quickly (and can then reinvest it if you wish). Only loans in good standing with monthly repayments up to date may be listed on the Marketplace, so that offers some reassurance against default – though of course it is by no means a guarantee.

In recent months the number of loan parts listed on the Marketplace has reduced considerably. And those that are tend to be snapped up quickly. As a would-be investor this is slightly disappointing, but it does indicate that people are keen to take advantage of the opportunities on offer. It also means that if you want (or need) to exit a loan early, accessing your money should be a quick and easy process.

Pros and Cons

Based on my experiences, here is my list of pros and cons for the Kuflink investment platform.

Pros

1. Easy sign-up process.

2. Low minimum investment.

3. All loans secured against property.

4. Choice of investments and approaches.

5. Manual and auto-invest options.

6. Kuflink invest in all loans themselves, so they have a strong incentive to ensure they are safe and secure.

7. They also cover the first 5% of losses on any loan before investors are affected (although this has never happened yet).

8. Money invested but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

9. In-depth information is provided on the website about all loans, so you can see exactly how your money will be used (and by whom).

10. There have been (according to Kuflink) no investor losses to date.

11. Customer service (in my experience anyway) is fast, friendly and helpful.

12. There is a 14-day cooling off period for new investors.

13. Marketplace (secondary market) for buying and selling loan parts.

14. No charges to investors lending on the primary market and only a 0.25% fee if you resell a loan part on the secondary market.

15. On most loans you can opt to reinvest monthly repayments to boost your net interest rate.

16. Tax-free IFISA option available.

Cons

1. Rates paid aren’t the highest in P2P lending.

2. Delays with some loans being repaid (although investors do earn extra interest if this happens).

3. No mobile app [UPDATE FEB 2023 – An app is now available.]

Conclusion

Overall, my experiences with Kuflink so far have been entirely positive and my investments have been generating the promised returns. I started cautiously with them, but have gradually built up the amount I have invested on the platform. Although – like all property P2P platforms – they were adversely affected by the pandemic, they appear to have come through it strongly, with new loans now being added almost daily.

As mentioned above, although Kuflink don’t pay the highest rates in P2P lending, I think the returns on offer are realistic and sustainable. The steady expansion of the platform seems to testify to this, as does the fact that they have received several industry awards. These include Best Alternative Business Funding Provider in the Business Moneyfacts Awards in both 2018 and 2019 and Best Service From an Alternative Funding Provider in 2020.

Kuflink are also highly rated on the independent TrustPilot website, with an average 4.6 out of 5 (‘Excellent’). At the time of writing 82% of reviewers award them the maximum five-star rating, which is among the highest figures I have seen for a financial services platform.

As with all P2P lending, your money does not enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates of return on offer are significantly better than those from most financial institutions. And the fact that all loans are secured against bricks and mortar – and Kuflink themselves have cash invested in them – clearly offers some reassurance.

From my experience, Self-Select loans tend to fill up quickly. On the positive side, this shows investors have confidence in Kuflink and want to invest through the platform. On the minus side, it means there are typically no more than two or three new loans open for investment at any time.

Clearly, no-one should put all their spare cash into Kuflink (or any other P2P investment platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return much higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P loans aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

If you have any comments or questions about this review or Kuflink in general, as always, please do leave them below.

Disclosure: As stated above, I am an investor with Kuflink myself, and if you invest £500 or more via my link above I will receive a bonus for introducing you. Money is at risk. You should always do your own ‘due diligence’ before investing, and seek advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a new UK high-speed broadband service called Cuckoo.

They are aiming to shake up the world of broadband internet with great-value prices, first-rate customer service, and a social conscience too 🙂

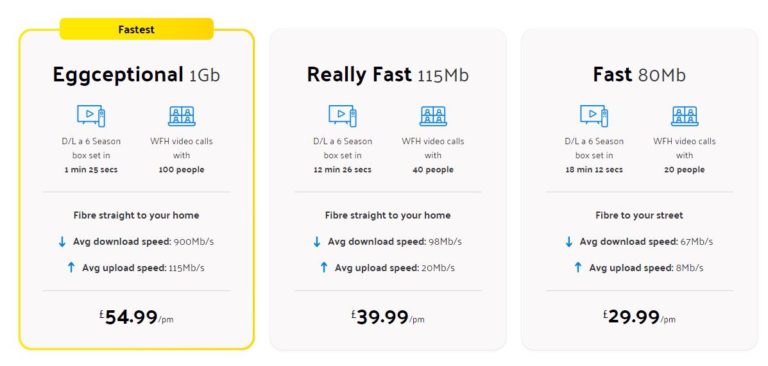

Cuckoo currently have three different customer offers based on speed. Briefly they are as follows:

Eggceptional (1 Gb) – £54.99 a month

Really Fast (115 Mb) – £39.99 a month

Fast (80 Mb) – £29.99 a month

You can see more detailed information from the Cuckoo website in the screen capture below.

Signing up is straightforward via the website and takes just a couple of minutes. Your router will then arrive in the post with full instructions for setting it up. If an engineer is needed (usually it isn’t) Cuckoo will arrange a convenient time for them to come. This is summed up in the graphic from the company website below.

As mentioned, Cuckoo is also a company with a social conscience. They take 1% of each bill and use it to help bring the Internet to places where it’s needed most. That includes conflict zones, natural disaster sites and developing communities. Customers get to choose which project they wish to to support under the Cuckoo Compass scheme.

Finally, Cuckoo aims to deliver top-notch customer service from their team of UK-based customer-support ‘Eggsperts’. Cuckoo have an impressive Trustpilot average rating of 4.6 (‘Excellent’), with 76% of people at the time of writing giving them a full five stars.

For much more information, please check out the Cuckoo website. And of course, if you have any comments or questions about this post, please feel free to leave them below as usual.

Disclosure: This sponsored post includes affiliate links. If you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2021, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a very merry Christmas (Covid and the government permitting), and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am reviewing a children’s book called Grandpa’s Fortune Fables. An ebook copy of this was kindly sent to me by the author, Will Rainey.

Grandpa’s Fortune Fables contains a series of short stories, each following from the last. The central character is a 13-year-old girl called Gail. Over the course of the book she shares a number of lessons she has learned from her Grandpa about money with a boy named Boris (no relation to our PM, I’m sure!).

Boris starts off by bullying Gail, whom he calls a ‘dork’, but she stands up to him and in time they become friends. Gail shares her Grandpa Jack’s money-saving and money-making advice with Boris. He is eager to learn, as his family have always been bad with money.

We learn that Gail’s Grandpa travelled to a (mythical) far-away island, where he learned how to look after his money and became a very wealthy man. Gail has been following his advice and even at her young age is now quite wealthy herself.

Each chapter is essentially a fable illustrating one particular lesson Gail learned from her Grandpa. So one concerns the dangers of Get Rich Quick schemes, another the importance of saving and reinvesting your money, and so on. There are also chapters on the subject of paying tax (‘The Money BIrds’) and the value of donating some of your money to charity.

At the core of Grandpa’s Fortune Fables are three key principles. I hope Will won’t mind if I reproduce them below:

1. Keep one out of every ten seeds you receive 2. Plant the seeds you keep 3. Let your trees GROW

As you may gather, the fables in the book all derive ultimately from the application of these three principles.

Grandpa’s Fortune Fables is designed to teach children about saving, investing and entrepreneurship in an entertaining but informative way (and parents/grandparents may learn some useful lessons too). The stories are all very much of the here and now – even the pandemic and lockdowns get a brief mention (to illustrate how unforeseen events can impact upon specific investments). It’s all very cleverly written, with some charming cartoon-style illustrations as well (see example below).

In my view Grandpa’s Fortune Fables would make a great Christmas/birthday gift for any child aged around 8 to 12 (it could also work for younger and older children). I like how each chapter ends with questions to provoke further thought and discussion. In addition, by correctly answering the multiple-choice questions in each chapter, a letter is revealed. If the child gets all the letters right, they spell out a message which can win them a prize. This is a great idea and a good incentive for reading every chapter (not that such an incentive would likely be needed).

Grandpa’s Fortune Fables is available in print or e-book versions from Amazon (just click on any of the links in this review), or you can order it from any good bookshop. At the time of writing the price is £9.99 for the print version or £3.99 for the e-book. I note that this title is currently number one on Amazon’s best-seller list for children’s books about money and saving, which doesn’t surprise me at all.

Thanks again to Will Rainey for sending me a review copy of his excellent book. If you have any comments or questions – for me or for Will – please do post them below.

Disclosure: As mentioned above, I received a free ebook version of Grandpa’s Fortune Fables for review purposes. In addition, this review includes Amazon affiliate links. If you click through to Amazon and make a purchase, I will receive a small commission for introducing you. This will not affect the price you pay or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Speak it softly, but there are now just seven weeks till Christmas. Touch wood, new Covid case numbers are falling steadily, and hopefully we can all look forward to a much more normal Christmas this year than last.

Of course, one thing we can definitely say is that – just like any other year – Christmas 2021 will be expensive. So today I thought I’d share a selection of tips for saving (and making) money while still enjoying the festive season and not having to face a mountain of debt in the new year.

1. Declutter for Cash

Chances are you’ll be planning to tidy up anyway before putting the decorations up, so why not take the chance to get rid of any bits and bobs you no longer need but someone else might want? You can then put the money to good use for Christmas. You could sell the items on eBay, your local Facebook sales page, or the ‘boot sale’ app Shpock. I’ve also heard good reports about Vinted, a website where you can buy and sell second-hand clothes.

2. Buy Discounted Gift Vouchers at Cardyard

Cardyard is an online marketplace for buying and selling gift vouchers. If you know where you want to do your Christmas shopping, you could buy a discount voucher for that store at Cardyard and get up to 25% off. Both physical and electronic vouchers are available. When I looked just now, you could buy a range of eGift cards for fashion store New Look at a 12% discount, e.g. a £148.50 eGift card for £130.68 (a saving of £17.82).

If you’re planning to do some of your Christmas shopping on Amazon – and let’s face it most of us do nowadays – remember that if your total order value is over £20, delivery is free of charge. If you’re just under the £20 threshold, it can make sense to buy a small item to bring it to the magic £20. Before I joined Amazon Prime (see below) I often bought a pen for this purpose.

If you can’t find a small item for the right price, visit Filler Checker. At this website you can enter whatever price you require to bring your order up to the free delivery threshold. It will then display items you can add to your order to achieve this.

5. Consider Joining Amazon Prime

Okay, this does require an annual or monthly fee, but for this you get free next-day delivery of millions of products on Amazon (and same day delivery in some cities). There is a growing range of additional benefits for Prime members as well, including instant streaming of millions of songs and thousands of movies and TV shows, free borrowing of selected Kindle e-books, and secure, unlimited photo storage with anywhere access. If you’re a regular Amazon customer – or planning to do a lot of your Christmas shopping there – it’s well worth considering Amazon Prime, especially as you can try it free for 30 days.

6. Make the Most of Black Friday Sales

Black Friday is a US tradition that in recent years has been imported into the UK (though not without some controversy at first). Officially Black Friday is Friday 26th November this year, but in practice many retailers are starting their Black Friday sales earlier than this. Just beware of being swept up by the hype. Check that the discounts on offer really are worthwhile and not just reductions of prices that were artificially inflated before.

7. Consider Part-Time or Short-Term Work

Okay, this won’t appeal to everyone, but even in these challenging times there are various seasonal opportunities on offer with companies from Amazon to the Post Office. Many supermarkets also take on additional seasonal staff, full-time and part-time. Take a look also at my blog post about Viewber, a company that needs people with a bit of time available in the day to show prospective purchasers around houses. You can earn from £20 a viewing for this, plus expenses. There are also growing numbers of part-time and full-time delivery driver opportunities (including e-bike riders and couriers) – the Service Club website lists a range in the UK and Europe. Another resource for part-time or short-term work of all kinds is the Labour Xchange app.

8. Abandon Your Shopping Cart!

When shopping online go as far as the checkout page and then close it. The stores will see this and many will send you a discount voucher or other incentive to try to persuade you to complete your purchase.

9. Use Live Chat to Haggle

This can be another effective tactic for getting money off when online shopping. Don’t go straight in with a request for a discount, but ask a few questions first. You’re unlikely to get a massive discount this way, but you may be offered 10-20% off, or a free bonus.

10. Check for Discount Codes

If you know where you want to shop, it’s always worth checking whether any discount codes are available for the store in question. Voucher Codes UK is a great place to start. When I checked just now, some of the top offers included 30% off at Adidas and a huge 52% discount on orders over £40 with The Protein Works.

11. Use This Free Service to Get Price Drop Alert Emails

A website called Love Sales lets you add items from hundreds of online retailers to your ‘wish list’ and name the price you’re willing to pay, or ask for an alert when the price drops.

You first have to register on the site. Then when you’re browsing a particular item from one retailer, add it to your list. After that, the wait is on for the price to fall and the email to arrive in your inbox.

12. Check Out This Christmas Deals Predictor

Finally, you can be ahead of the game with the annual Christmas Deals Predictor on Martin Lewis’s Moneysaving Expert website. Based on previous years (and any other info they may have), this predicts the likelihood of certain offers being made in the run-up to Christmas. They say last year they predicted more than 70 deals across dozens of top retailers, and got 81% right. At the time of writing the Christmas Deals Predictor is not yet operational, but based on previous years it is likely to launch any day now.

I hope that by following these tips you will have the best Christmas possible, and a happy and debt-free new year!

If you have any comments, questions or additional suggestions for saving money at this time, please do post them below.

Note: This is a fully updated version of an annual post.

Disclosure: this post includes affiliate links. If you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect the price you are charged or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I admit I’m a bit of an Amazon addict. I love their huge range of products and the fact that you can read reviews of the products concerned from actual buyers. I’ve always found their customer service first rate as well.

Prices on Amazon are generally competitive, but over the years I’ve discovered a variety of ways to ensure you get the best value for money from them. So here are my top twelve tips for saving money on Amazon…

Always search for the product you are thinking of ordering on eBay as well. Often you will find the same product there, and sometimes cheaper as well. Of course, you will want to check that the eBay seller has good feedback and the delivery charges are reasonable.

If you’re going with Amazon, as long as your total order value is over £20, delivery is normally free of charge. If you’re just under the £20 threshold, it can make sense to buy a small item to bring it up to the magic £20. Before I joined Amazon Prime (see below) I often bought a pen for this purpose. I can always use more pens!

If you can’t find a small item for the right price, visit Filler Checker. At this website you can enter whatever price you require to bring your order up to the free delivery threshold, and it will then display items you can add to your order to achieve this.

You might also want to think about signing up with Amazon Prime. This service requires the payment of an annual (or monthly) fee, but for this you get free next-day delivery of millions of products on Amazon (and same-day delivery in some cases). There is a growing range of additional benefits for Prime members as well, including instant streaming of thousands of movies and TV shows, free borrowing of Kindle e-books, and secure, unlimited photo storage with anywhere access. If you’re a regular Amazon customer it’s well worth considering Amazon Prime, especially as you can try it free for 30 days.

Prices on Amazon go up and down to a surprising extent. Recently I was looking at a snazzy digital radio for under £50. I went back the next day and found it had gone up to over £100 😮 To keep track of the price of any item you are interested in, you can sign up at the oddly named Camel Camel Camel and they will notify you by email if and when the price of your chosen product falls below a certain level.

If you’re unsure whether a particular product is good value or not, Camel Camel Camel can tell you that as well. Enter any product details and it will show you the price that particular product has been selling at on Amazon over the preceding weeks and months. You can also install their ‘Camelizer’ browser extension (Chrome and Firefox) to view the price history of any item on Amazon.

Check out the Today’s Deals link at the top of most Amazon pages. Items listed here include ‘Deal of the Day’ and ‘Warehouse Deals’. The latter are pre-owned and refurbished items, and you can pick up some real bargains.

If there is something you buy regularly – e.g. vitamin pills or nappies – you may be able to save money by placing a regular order using Subscribe and Save. S&S typically offers a 10% price reduction initially that can increase to 15% with repeat orders over time. For some products the saving is lower, with a 5% initial reduction increasing to 10% over time. You can of course cancel your subscription at any time.

Watch out for promotional events on Amazon, including Amazon Prime Day (which has lots of special deals for Prime members) and their Black Friday/Cyber Monday sales in the run-up to Christmas. Some of the best discounts feature Amazon’s own products such as their range of Amazon Echo smart speakers with Alexa. These are typically available for as little as half the normal price during these events.

If you use cashback sites such as Quidco and Top Cashback – and as I say in this blog post you definitely should – you may be able to take your cashback in the form of Amazon vouchers. Typically you get a few percent more this way than if you ask for money.

Lots of market research and survey sites also offer Amazon vouchers as a payment option. People for Research is one that I have done well from myself. Mobile Xpression is another.

I hope you find these tips helpful. If you have any other tips for saving money on Amazon, please do share them below!

Disclosure: This post uses affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Many of us today do most of our shopping in supermarkets. Although of course it’s important to support local/specialist shops, supermarkets typically offer a much wider range of products at prices small stores find hard to match.

But there are still lots of ways savvy shoppers can save money on their supermarket shopping. Here are ten top tips to shave a few pounds (or more) off your shopping bills…

Make the Most of Loyalty Cards

All the big name supermarkets have these, though some (e.g. Morrisons) are switching from plastic to app-based cards. The benefits on offer vary, but typically you get points which can be exchanged for discounts and gifts. I shop mainly at Morrisons and Waitrose, as they have branches closest to me.

With Morrisons, their (now virtual) More card gives you special offers based on things you normally buy anyway. I have had some great discounts on my groceries with these offers, but you do of course need to remember to ‘swipe’ the app barcode at the checkout.

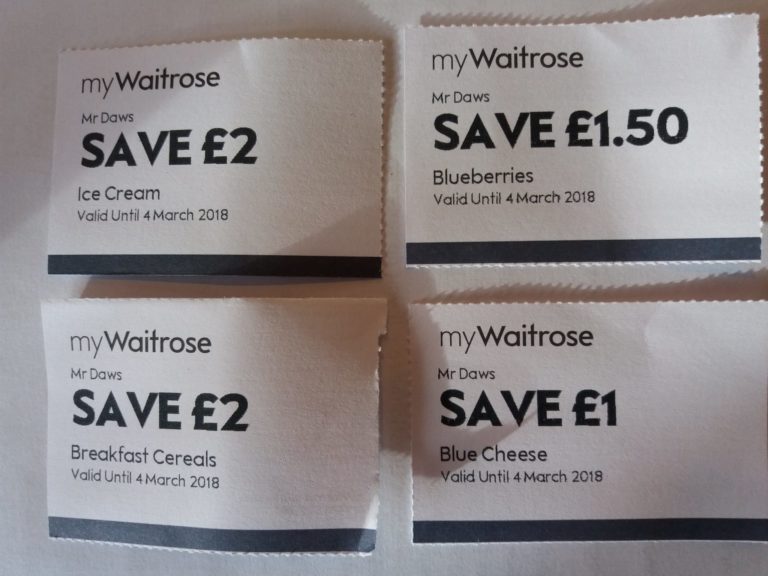

I also have a myWaitrose card. With this you can get a free newspaper with your shopping (subject to a £10 minimum spend). You can also get a free hot drink. You get vouchers sent in the post as well, such as the ones pictured below. It surprises me a bit when someone in the queue in front of me says they don’t have a myWaitrose card, but perhaps if they shop regularly at Waitrose they don’t have to worry too much about saving money 😉

Shop Late in the Day

Late in the day – ideally the hour before the store closes – is the best time to look for bargains. The shops will have stock they want to get rid of, probably because it is coming up to its ‘best before’ date. These items will often be marked down substantially, as the stores want to get at least some money for them rather than have to throw them away. Bear in mind that you can always freeze many foods if you can’t use them immediately – and in any event ‘best before’ dates aren’t set in stone.

Use Cashback Sites

I’ve talked about cashback sites like Quidco and Top Cashback on this blog before (e.g. in this post). If you shop online, you can get money back by clicking through to the retailer from the link on the cashback site. The most generous offers are generally reserved for new customers, e.g. on Top Cashback right now new Sainsbury’s online customers can get 16.5% cashback on Click and Collect orders of over £40. But even existing customers can get 5.5% cashback on Click and Collect orders of over £40 (all details correct at time of writing).

Plan Your Meals Ahead

We all lead busy lives these days. But it’s still good to devote some time to planning ahead where meals are concerned. Try to incorporate things you have in stock already, especially perishables which may not last more than a day or two. And rather than buying unusual/expensive ingredients for one dish only, see if you can find other recipes to use them up.

Batch cooking, where you make enough of a dish to last two days or more, is another great way to cut the cost of shopping. Of course, most dishes can be frozen if you can’t face having curry three days in a row!

Shop Online

Aside from the convenience of having goods delivered to your door, a big advantage of online shopping is that you will be less likely to succumb to impulse buys. Just make a list of what you need, visit the website, and add the items on your shopping list to your basket.

Admittedly you may have to pay a delivery fee, but many supermarkets now offer this free for new customers or for orders above a certain value. There are also in many cases ‘free delivery’ codes online if you search for them. And don’t forget to use cashback sites where possible as well (see above).

Search for Money Off Coupons and Vouchers

This is an old school method but it can still produce big savings. Look out for money-off vouchers in newspapers, magazines and the stores themselves. You can also search online if there are particular products you want to buy. This method can work particularly well with larger items such as dishwashers and tumble dryers [sponsored link], but it’s also worth searching for money-off vouchers for smaller/cheaper items, especially if they are things you buy regularly.

Try Own-Brand Products

All supermarkets have their own-brand products, and usually they cost less than heavily promoted consumer brands.

Many stores also have rock-bottom priced ‘Saver’ ranges. Sometimes these are not as good as more expensive branded or own-brand products. Other times, though, they are indistinguishable. For example, I now always buy Morrisons’ lowest-priced butter from their Savers range. I find it tastes just as good as the more expensive alternatives.

Use Discount Supermarkets and Stores

It’s easy to get in the habit of a weekly trip to Tesco or Sainsbury’s, but if you haven’t yet done so it’s well worth trying out discount supermarkets such as Iceland, Aldi and Lidl. They aren’t always the most attractive places to shop, but they make up for this with some amazingly low prices. Admittedly you won’t always recognize the brand names, but that doesn’t mean they aren’t high quality. Staples like bread, fruit and vegetables are often cheaper as well.

There are various apps and companies that will reward you for scanning and submitting your shopping receipts to them. One I’ve belonged to for some years now is ShopandScan. You can read more about this opportunity here.

ShopandScan pays in vouchers rather than cash, but the options include Amazon vouchers, which are of course nearly as good. I have received several thousand pounds worth of vouchers from ShopandScan since I started with them. As I say in my review, acceptance isn’t automatic, but if you apply there is every chance you will be sent an invitation within a few weeks.

Grow Your Own Food!

You can save significant sums of money by doing this. This summer I didn’t buy any tomatoes from July till mid-October, as I was eating ones I had grown myself. I highly recommend tomatoes, incidentally, not least as they are easy to grow in the garden, in a tub or hanging basket, or even on your window sill. They taste a lot better than most shop-bought varieties as well!

There are, of course, plenty of other things you can grow to save money, even if space is at a premium. Fresh herbs are one possibility, as are many types of berry (strawberries grow like weeds in my garden). I’ve also had some success with runner beans, courgettes and garlic, and salad vegetables such as chard, radishes and spring onions.

This year I also grew a pot of cut-and-come-again lettuce and was amazed by how much I got from this. It’s perfect for people who live alone like me, as you can just pick a few leaves when you want them, rather than buy a bag of salad leaves and have most of them go to waste.

I hope you’ve enjoyed this post and it has given you a few ideas for saving money on your supermarket shopping. If you have any other tips or comments, please do post them below!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a savings product that will be relevant mainly to the parents among you

A Junior ISA (sometimes abbreviated to JISA) is a savings product aimed at under-18s (and more specifically at their parents/guardians). These accounts allow money to be stashed away tax-free for a child until their 18th birthday. After this the money becomes the child’s to do with as they wish. The JISA account turns into an ordinary ISA at this time, thus retaining its tax-free status.

What Types of JISA are There?

There are two types of JISA: the Cash JISA and the Stocks and Shares JISA.

A Cash JISA is basically just a tax-free savings account. Interest is normally paid annually. According to the MoneySavingExpert website, the best-paying Cash JISA provider at the time of writing is Coventry Building Society, who are paying 4.95%. However, this is only available if you open an account in a branch or by post. If you want to open an account online, the best paying Cash JISA currently comes from Tesco Bank or NS&I, both paying 4%.

With a Stocks and Shares JISA, as the name indicates, the money is invested in the stock market. This offers the potential for greater returns, but with a higher degree of risk in the short term especially. I will say more about Stocks and Shares JISAs below.

As with adult ISAs, there is an annual limit to how much you can put into a Junior ISA. In the current (2024/25) tax year this is £9,000. You can put all of this into a Cash JISA or a Stocks and Shares JISA, or divide it between the two. You can switch providers as often as you like, but can only hold one of each type of JISA at any time.

Only a child’s parent or guardian can open a Junior ISA for them, but others including grandparents, friends, other relatives and the child him/herself can contribute. But it is important to be aware that (barring exceptional circumstances) all the money and interest in the account will be locked away until the child’s 18th birthday.

Which JISA is Best?

You won’t be surprised to hear that there is no simple answer to this.

If you want to avoid any risk of losing money, a Cash JISA is the way to go. Under the Financial Services Compensation Scheme (FSCS) the money will be completely safe so long as it’s invested with a UK-regulated provider and you have no more than £85,000 with that institution. Every year a known amount of interest will be added. The only risk you are taking is that the money won’t grow at the same rate as inflation.

On the other hand, if you are investing for at least a five-year period, there is certainly a case for putting at least some money into a Stocks and Shares JISA – and if it will be for ten years or more, the case becomes even more compelling. Over a five-year period stocks have outperformed cash in the great majority of such periods, and in almost all periods of ten years and over.

So if you are opening a JISA for a young child or infant, where the money may be invested for up to 18 years before it can be accessed, a Stocks and Shares ISA is very likely (though not guaranteed) to produce better returns than a Cash JISA. Of course, there is nothing to stop you hedging your bets and putting some money into one of each type.

What About Child Trust Funds?

Any child under the age of 18 born before January 2011 would have had a Child Trust Fund (CTF) opened for them by the government.

The government gave every child born between 1 September 2002 and 2 January 2011 a £250 voucher (£500 in the case of some low-income households). Parents could top up their child’s CTF themselves if they wished. The scheme ended in 2011 when CTFs were replaced by Junior ISAs. Unfortunately the government does not make a contribution towards these!

As with Junior ISAs, the money in a CTF could be placed in a Cash CTF or one where the money was invested in stocks and shares. Although new CTFs are no longer issued, there are many young people who still have one and will be able to access it on their 18th birthday. The first CTFs matured in September 2020, when the oldest account-holders turned 18. The last will mature in 2029. On maturity, a CTF can either be cashed in or transferred into an adult ISA.

Unfortunately the interest rates currently paid on Cash CTFs are generally very low indeed. So if your child has one, there may be a case for transferring it to a better-paying Junior ISA. Most JISA providers allow transfers from CTFs (or other JISAs), and it is certainly worth looking into this if your child has a low-interest-paying Cash CTF.

The Nutmeg Junior ISA

Regular readers of Pounds and Sense will know that I am a fan of of the Nutmeg investment platform and have a fairly large amount in an account with them. My money is invested in the form of a Stocks and Shares ISA. You can read more about this if you wish in my Nutmeg review or one of my regular investment updates such as this one.

Nutmeg do not offer a Cash JISA but they do offer a Stocks and Shares JISA. So if you are thinking of opening one of these for your child (maybe in addition to a Cash JISA) in my view they are well worth checking out.

With the Nutmeg Stocks and Shares JISA you have the same range of investment options as their adult ISA. These are discussed in detail in my Nutmeg review, but in brief they include Fully Managed, Smart Alpha, Socially Responsible and Fixed Allocation. My own investments are in the Fully Managed and Smart Alpha categories, and I am very happy with how both have been performing. But you should, of course, check the terms and conditions (and charges) carefully when deciding which is right for you.

Note that, unlike an adult ISA, in a Nutmeg JISA you cannot have different ‘pots’ within the same JISA wrapper. So you will need to pick your preferred option from one of the four mentioned, though you can change this any time later if you wish. You can also set a risk level between 1 and 10 and again you can change this at any time. You can read my recent blog post about Nutmeg risk levels here. My general advice, though, is that if you’re investing over a period of at least five years, it may pay not to be too cautious. In addition, if you choose to invest in a Nutmeg Junior ISA via my refer-a-friend link, you can get six months free of any charges.

Of course, Nutmeg are not the only providers of Junior ISAs. Some other possible options include Hargreaves Lansdown and BestInvest.

Closing Thoughts

If you are a parent or guardian, opening a Junior ISA is one of the best gifts you can give your child (or children).

The money will grow tax-free and can’t be touched until they are 18, when they can withdraw it or keep it as an ISA. It may provide a much-needed lump sum at a time when they are setting out in the world and really appreciate a financial leg-up. A JISA will also give them an early introduction to saving and investing, and form a valuable part of their financial education.

The main selling point of JISAs is, of course, their tax-free status. Admittedly this is not as big a deal with Cash JISAs as it used to be, as nowadays almost everyone has a tax-free Personal Savings Allowance of up to £1,000 and other tax-free allowances as well. As a result, interest on savings is usually paid without any deductions. So there may be no immediate tax advantage to investing in a Cash JISA if a non-JISA savings account pays better interest.

In the case of a Stocks and Shares JISA the tax-free status may be more significant, as it also gives exemption from dividend tax and capital gains tax (CGT) both of which have had their tax-free allowances slashed by the government.

Either way, though, money saved in a JISA will carry on growing tax-free forever (until it’s withdrawn) – so even if there is no immediate tax advantage, there may well be in years to come. This applies to an even greater extent if the young person stays invested on reaching maturity rather than immediately withdrawing all their money.

According to the This is Money website more parents open Cash JISAs than Stocks and Shares JISAs. As a money blogger, however, I would definitely think about opening a Stocks and Shares ISA for at least part of your child’s JISA allowance. That applies especially if it is more than ten years till their 18th birthday. As mentioned above, over almost any given ten-year period, stocks and shares have outperformed cash. And the longer timescale allows the inevitable ups and downs in the stock markets to even out. If you put all the money into a Cash JISA, by contrast, it is quite likely that the value of your child’s account will not keep up with inflation.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Everyone’s circumstances are different and what is right for one person may not be appropriate for another. It is essential to do your own ‘due diligence’ before investing and seek help from a qualified financial services professional if in any doubt how best to proceed. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make a purchase (or perform some other defined action) I may receive a fee for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing some information about personal finance podcasts. This is not a subject I previously knew very much about, so I am grateful to my friends at All Finance Tax for supplying the excellent infographic and some of the other info below.

What is a Podcast?

A podcast is like a series of radio programmes on a particular theme or topic, from politics to cycling. You can subscribe for free using a suitable app on your smartphone (or other internet-enabled device). You can then listen whenever and wherever you like, via headphones, earphones, through speakers, in the car, on the train, and so on.

Podcasts are a booming medium and one of the major trends of the last five years. There are now podcast shows on nearly every topic you can think of. And with the rise of both independent and conglomerate podcast production studios, it seems likely this new medium will be in our lives for many years to come.

In the same way people were once passionate about certain radio shows, podcasts have the same dedicated followings, thanks to hosts who become familiar audio friends. Some even run live events. As a medium, podcasts are incredibly accessible, with few barriers beyond an internet connection and a smartphone or other device that can stream audio. No matter where you are or what you’re doing, podcasts offer content that educates, inspires and entertains. If you have never listened to a podcast before, the BBC Sounds podcasts page is one good place to start.

How to Listen to a Podcast

The easiest way to find and listen to podcasts is by using an app on your smartphone.

If you have an iPhone, it will have a built-in app called Apple Podcasts. This works very well and allows you to search for and subscribe to any of a huge range of podcasts. All you have to do then is open the app any time you want to listen and choose the episode you require.

Android owners can use the free Google Podcasts app. You can download this from the Google Play Store if you don’t have it already. It is not as user-friendly as the Apple app and doesn’t have as many features, but will certainly get you started. There are also other free or inexpensive apps you can download from Google Play such as the highly-rated Pocket Casts or Castbox.FM.

Finance Podcasts

One genre with a surprisingly large, dedicated listenership is finance. While to some that might sound a dry, unpromising subject, the podcast medium has enabled content to be reinvented with an unexpected, creative approach.

With hosts ranging from seasoned finance professionals to novice FIRE (financial independence) enthusiasts, podcasts allow people who would never previously have been interested in finance – or perhaps even have been intimidated by the topic – to access valuable information presented in an engaging, inclusive way.

All Finance Tax rounds up the top finance podcasts in the infographic guide below. Find out about the must-listen shows, including podcasts about:

Entrepreneurship

Billionaire case studies

Female-led finance

Personal and couples’ finance

Start-ups

And more!

With snapshots of real reviews plus the best episodes to start with, this resource will help you find the right show for your personal interests and needs regardless of your outlook on finance. Read on for the full list of finance podcasts to start your listening journey!

Many thanks again to my friends at All Finance Tax for their help with this article. I have listed below all the podcasts recommended in the infographic, with links to their homepages (or another website) where you can find out more. You can also listen to the podcasts on the web via these pages, though using an app on your smartphone (as discussed earlier) may be more convenient generally.

One more I would add is the Ask Martin Lewis podcast from BBC Radio Five Live. Martin is, of course, a well-known personal finance guru (and founder of the hugely popular MoneySavingExpert website). Although I can take or leave his TV shows, his podcasts are less gimmicky and include valuable, accessible advice on all aspects of personal finance (not including investing).

As always, if you have any comments or questions about this post, please do leave them below. I’d also love to hear about any personal finance podcasts not mentioned above which you enjoy and recommend!

If you enjoyed this post, please link to it on your own blog or social media:

As mentioned,

As mentioned,