As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2020, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a happy, Covid-free Christmas, and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a Q and A for you with my fellow money bloggers at MoneyNerd.

MoneyNerd is a UK personal finance blog that aims to help people learn to manage their finances and tackle debt. I asked a number of questions about personal finance and debt, and added my own thoughts as well. Our answers are also being shared separately on the MoneyNerd blog. I hope you find them interesting and informative.

What’s your number 1 financial tip?

MN: It’s hard to give advice that would apply for everyone, because everyone’s finances are different. But I would suggest ‘write it down’, as a fairly universal and important financial tip. Start with your financial goals, then write down the steps you’ll take to get there according to your budget. A lot of people have good financial intentions, but without having clear goals on paper, it’s easy to get led astray.

PAS: Agreed. I would also say, keep on top of your money. Know what’s going in and what’s going out every month, and budget accordingly. Always be on the lookout for ways you can maximize your income and minimize your expenditure. And try to put some money aside for the proverbial rainy day. Everyone should really have at least three months’ worth of income set aside in case of emergencies. Sorry, that’s at least three tips, I know!

What do you think are the main causes people find themselves in financial difficulty?

MN: I think financial difficulties are mainly caused by unforeseen life-events, such as bereavement, unemployment, and relationship breakdowns. These kinds of bumps-in-the-road can severely throw people off course, particularly if their financial situation was fragile in the first place. Unfortunately, all three of these examples have sky-rocketed due to the pandemic, and many people in the UK will be facing financial difficulties over the coming year.

PAS: Not much I can add to that. Although sometimes failing to monitor your income and expenditure closely enough can lead to debts mounting up before you realise it.

What personal finance tools do you currently use to track and manage your money?

MN: I’m quite old-school and still use spreadsheets for a lot of money-related things! There are some good apps out there though – Money Dashboard is a particularly good one.

PAS: I am the same and use spreadsheets a lot. I started with Microsoft Excel, but these days mainly use Google Sheets. As regards personal finance tools, I like Snoop [referral link], a relatively new app that helps you keep track of your finances and suggests easy ways you can make savings.

Any tips for people coming to financial management later in their lives?

MN: It might be a little harder to undo old habits and reinstate new ones if you’re approaching financial management from an older perspective. So start by setting simple goals, and work at them consistently. It’s probably worth taking a little time to assess what’s important to you right now, too: what range of outgoings does your money need to cover in later life that you didn’t need to consider before?

PAS: I am 64 and have friends in their seventies and eighties, so I have seen the sorts of problems older people can face. In particular, so many aspects of our personal finances are dealt with online now, from banking to applying for state benefits. The pandemic has probably accelerated this trend.

Many older people struggle with the technology and it’s often not as intuitive as it should be, especially for those whose eyesight isn’t as good as it once was. So I would say to any older people, try not to get left behind by technology, and ask younger friends and relatives for help when needed. Last year a group of us clubbed together and bought a friend (a retired builder) a Chromebook for his 80th birthday. He had never engaged with computers or the internet before and I must admit I was expecting him to struggle at first. However, he took to it like a duck to water, and was soon ordering tools and components online from a local builders merchant. So even old dogs can definitely learn new tricks!

2021 is going to be tough for many. Do you have any advice on how to keep things under control?

MN: I’d start with the obvious – plan as much as possible, in order to save as much as possible. This is so that when those ‘bumps-in-the-road’ come along, you have some kind of safety net, however small. Unfortunately, however, I imagine a lot of people will do everything right this year and still fall into difficulty. As and when that happens I would say be proactive in reaching out and seeking help. There are plenty of free services and helplines to reach out to, before matters spiral.

PAS: Yes, definitely. As I said earlier, everyone should have a financial safety net to tide them over when life throws you a curveball.

In my earlier career I worked as a debt counsellor at a citizens advice bureau, so I know that there is lots of help out there if you ask for it. And friends and family can be a good source of practical and emotional support too. Just don’t bury your head in the sand and pretend to everyone that nothing is wrong.

What would be your top tip for someone who is worried about a debt (or debts) they can’t repay?

MN: I have two tips: the first is don’t panic, the second is be proactive. If you can’t afford the repayments for a loan or credit card, contact the company and explain your situation. If you’re struggling to meet the repayment amounts, you may also need to look at whether a debt solution is appropriate for you. Having unaffordable debt can be a scary place in which to find yourself, but by taking action you can dissipate some of that anxiety by feeling you are doing something about the problem.

PAS: Yep. It’s worth bearing in mind also that if you have a debt you can’t repay, it’s not just your problem, it’s a problem for whomever you owe the money to as well. It is therefore in their best interests to work with you to find a method for paying down the debt.

What are some good ways of boosting your income?

MN: Ask yourself: do I own anything I could rent? A parking spot, a vehicle, a garden shed, even a room in your house if you own it. Then ask yourself: do I own anything I could sell? Old clothes, a bicycle, old furniture, anything in storage. Then finally, ask yourself what you could do with your spare time: dog-walking, Uber-driving, delivering takeaways/parcels, painting and decorating,completing online surveys, match betting, free-lancing, etc. I have a whole blog post which goes into this very topic in more detail: Making Money – Tips and Tricks.

PAS: Lots of great ideas there. Like MoneyNerd, I also have a section of my blog devoted to ideas for boosting your income. I like online surveys, with Prolific Academic (a website needing people to take part in academic research) a particular favourite. And I do matched betting as well, though not as much as I used to, as I’ve been restricted (or gubbed as we say in MB’ing) by many of the leading bookmakers!

What is the best way you can help a friend or family member who has debt problems?

MN: Honestly, I don’t think there’s a one-size fits all here. Everyone and everyone’s debt problems are different. But that seems like a cop-out! So I think showing genuine, non-judgemental support, and ensuring they have all the right resources (StepChange, CitizensAdvice, etc.) to hand are two good places to start.

PAS: I agree with this. But based on personal experience with a friend a few years ago, I would also advise thinking hard before lending them money, as this seldom solves the problem and may simply exacerbate it. With my friend, who lived alone, I found that acting as a lender to him changed the nature of our friendship, and not for the better. I also felt that by constantly bailing him out, I was allowing him to avoid addressing his money management issues. Eventually we had a difficult telephone conversation when he asked me to lend him money again and I refused. He took it better than I expected and our friendship actually returned to something more normal after that. He got his finances under better control, although I did on a couple of occasions afterwards send him supermarket vouchers to ensure he had enough to get food. I didn’t expect to be repaid for these, obviously!

If you had a sudden, unexpected windfall of £5,000, what would you do with it?

MN: Firstly I’d pay off any loans or outstanding credit card debts. Then I’d take my family out for a nice meal, and put what’s left-over into a tax-free ISA.

PAS: Paying off debts would be my first priority as well, though I am fortunate not to have any at the moment. I would put most of the rest in my Nutmeg stocks and shares ISA, and some in my Kuflink property loan investment account (from which I have had good results over the last three years) to provide a bit of diversification. Going out for a nice meal with family and friends sounds good too, although as I live in a Tier 3 area I might have to wait a while for that!

What was your best-ever financial decision, and what was your worst?!

MN: My best financial decision was investing in a tech based stocks and shares ISA which has done really well over the last 5 years, although don’t know if I’d recommend the same investing approach in the current economic climate.

On the other hand my worst financial decision was living in London for 10 years where rent and cost of living is exorbitant.

PAS: My best financial decision was probably paying off the mortgage when I had a windfall a few years ago. At a stroke one large item of monthly expenditure was gone, giving me greater financial flexibility as well as saving me a lot in future interest payments.

My worst decision was investing too much in property crowdfunding a few years ago when it was still new and exciting. I had money to invest at the time and liked the idea of owning stakes in a portfolio of properties across the UK. Some of my investments worked out but others didn’t, and I am currently sitting on a number I can’t access because the properties in question can’t be sold for one reason or another. The money is still there in bricks and mortar but I have no idea when or how I will be able to access it. That said, I do still believe in the property crowdfunding concept, but I do it a lot more selectively now.

About MoneyNerd

MoneyNerd.co.uk is a personal finance blog that was set up with one aim in mind: to help people learn how to manage their finances and tackle debt. The blog includes a variety of straight-talking articles that cover personal finance topics from credit card guides to mental well-being tips. These can help you understand exactly how financial products work, as well as what your rights are when dealing with debt. We want to offer authentic and truthful information that can help you deal with your situation, whatever that may be.

Many thanks again to MoneyNerd for their insights. Please do check out the MoneyNerd site for much more information about tackling debt and getting your finances under control.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers of PAS will know that I am a fan of the Nutmeg robo-adviser investment platform, and have a good portion of my own money in a Nutmeg stocks and shares ISA. You can read my in-depth review of Nutmeg here.

I was interested to hear that Nutmeg had launched a new investment style for their ISA, Lifetime ISA, Junior ISA, SIPP (personal pension) and general investment account customers. Previously such customers had a choice of three options: Fixed Allocation, Fully Managed and Socially Responsible.

All Nutmeg portfolios are managed by human experts, but the Fixed Allocation ones are altered annually, whereas the others are managed more actively. The Socially Responsible portfolio aims to optimize your investments according to various environmental, social and governance (ESG) factors. So it focuses on companies with a good track record and proactive strategy in such areas as water use, pollution, greenhouse gas emissions, proportion of female board members, and so on. Currently my own stocks and shares ISA is in the Fully Managed category (which was the only option available when I originally invested with Nutmeg).

Whilst all three of these investment styles remain available, a new one was launched in 2020…

Smart Alpha Portfolios

Nutmeg’s Smart Alpha portfolio range is powered by J.P. Morgan Asset Management. It includes five risk-rated portfolios, each holding between 10 and 14 passive and active exchange traded funds (ETFs). They are run by J.P. Morgan’s multi-asset solutions team, giving Nutmeg clients access to the investment giant’s experience and expertise. Writing on the Nutmeg blog, their Chief Investment Officer James McManus explained the benefits of this approach as follows:

The name recognises the intelligent way these portfolios are designed with the potential to achieve alpha (returns above the market) for our clients in three ways.

Firstly: The use of J.P. Morgan Asset Management’s multi-asset specialists, a team with a 50-year history of investing for institutions and professionals worldwide. These specialists inform Smart Alpha portfolios’ long-term (strategic) asset allocation.

Secondly, Smart Alpha portfolios have the ability to be flexible around this long-term asset allocation, allowing us to manage risk and capture opportunities at different stages of the market cycle.

Thirdly: Nutmeg and J.P. Morgan Asset Management have added to these capabilities a means to make smart security selections within active exchange traded funds (ETFs). These smart selections are made based on the insights of J.P. Morgan Asset Management’s research analysts with the aim being to capture returns in excess of the market benchmark (alpha).

How do these smart selections seek to gain alpha? The active ETFs we use allow us to move overweight in certain positions that J.P. Morgan Asset Management’s analysts expect to perform well and underweight in those positions they expect to perform poorly. This gives us the ability to move above and below market benchmark positions, delivering greater potential returns with similar risk to the overall market.

As well as allowing Nutmeg investors to tap into the expertise of J.P. Morgan Asset Management, these portfolios are ESG integrated, meaning that (as mentioned above) environmental, social and corporate governance considerations are factored into every research and investment decision. These portfolios are therefore suitable for the growing number of investors for whom ethical considerations are particularly important.

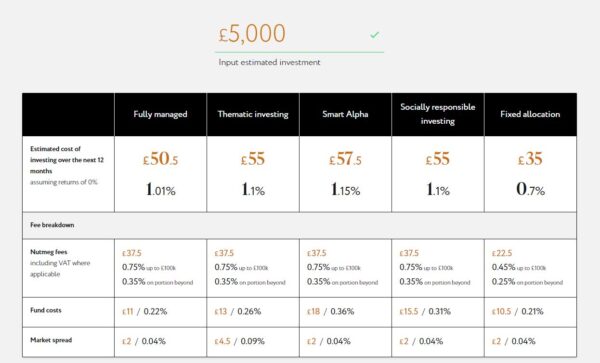

The terms and conditions for the new Smart Alpha portfolios are copied below, alongside the other portfolio types.

The above is correct as at 16 November 2023, but may have changed subsequently. Please note also that Nutmeg has also recently introduced a new ‘thematic’ investment style. More information about this can be found about this in my full Nutmeg review and on the Nutmeg website. Remember that all investing carries a risk of loss.

My Thoughts

This is undoubtedly an interesting move by Nutmeg and gives investors the opportunity to benefit from having their portfolio actively managed by a leading investment house at no extra cost. If you are a Nutmeg investor already, you can start by investing as little as £500 to test the water. You can either use ‘new money’ from your bank account or another ISA, or you can transfer money from another pot within your Nutmeg ISA account.

Personally I am very happy with the way my Nutmeg ISA has performed during this tumultuous year and don’t want to rock the boat too much. On the other hand, I am curious to see how the new Smart Alpha portfolios perform in comparison. So I have created a new £1,000 pot within my ISA and have selected Smart Alpha as the investment style. The risk level is 4/5, which roughly corresponds with the 9/10 risk level in my Fully Managed portfolio.

I will of course report back on Pounds and Sense about how my investments perform. Obviously, if my Smart Alpha pot seems to be doing significantly better than my Fully Managed one, I will switch some or all of the latter to Smart Alpha as well. It is one of the attractions of Nutmeg that you can have multiple pots within a single ISA with different investment styles and risk levels attached to them.

Capital at risk. Tax treatment depends on your individual circumstances and may change in the future.

In Conclusion

I am obviously a fan of Nutmeg and – as stated above – have a significant proportion of my investments with them.

Of course, I am not a qualified financial adviser and everyone should do their own ‘due diligence’ (and/or take professional advice) before deciding to invest. In addition, you shouldn’t consider investing with Nutmeg (or anyone else) unless you have paid off any interest-charging debts and have at least three months of easily-accessible savings in case of emergencies.

Based on my personal experiences with Nutmeg, though, I am happy to recommend them. They provide a simple, easy-to-understand investment platform, the customer service is excellent, and certainly in my case the results to date have exceeded my expectations.

If you have any comments or questions about this post or Nutmeg in general, please do leave them below.

PLEASE NOTE:As with all investing, your capital is at risk. Tax treatment depends on your individual circumstances and may be subject to change in the future. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest.

Note also that I am not a qualified independent financial adviser and nothing in this review should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any way uncertain how best to proceed. All investing carries a risk of loss.

Please note also that this review includes affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the terms you are offered or any fees you may be charged.

If you enjoyed this post, please link to it on your own blog or social media:

The number of people applying for Universal Credit has surged to record levels as a result of the Coronavirus pandemic and the numbers are set to rise further with the ongoing economic uncertainty.

In addition to a loss of income, households could also be facing a rise in energy-bills due to more time spent at home and cold weather approaching. Many will be coming to grips with the benefits system for the first time and starting to understand the rules, regulations and complexities around making a claim.

However, there is a little known silver lining for these claimants. Anyone who has claimed Universal Credit successfully will also be eligible for home improvements under the Government’s Energy Company Obligation (ECO) scheme.

This current scheme, called ECO3, targets people that have high energy costs comparative to household income. The scheme has a list of ‘qualifying benefits’ for eligibility. Universal Credit is on that list.

Plus, there are no savings or income-tests for the qualifying benefit part of the application, so if you receive any benefit on the list below (excluding Child Benefit, as that has an income cap), it’s likely you’ll be eligible.

According to Ofgem (who administer the ECO scheme), claimants will still be eligible for a period of 18 months following the date of the letter for the Universal Credit award (page 44 of the Ofgem ECO3 guidance has full details).

So if, say, you were awarded your Universal Credit in April but you got a job last week and came off Universal Credit today (for example), you still have a significant period of time (a year and a half) to apply for and install the measure, as you would still be classed as eligible even when you return to work. While you can wait to apply, it’s advisable to apply sooner rather than later, as funding rules can change at any time.

Even if you have returned to work or are planning to return to work, you will still be eligible, providing you have had at least one award for Universal Credit.

And it isn’t just Universal Credit recipients who are eligible for grants. Also on the ‘qualifying benefits’ list are the following:

You will still be eligible if you return to work as you can claim for a period of 18 months after claiming benefits.

What Grants Are Available?

There are a range of energy-efficiency measures that can be installed under the Energy Company Obligation (ECO) scheme, including boiler upgrades, home insulation and heating upgrades. The Scheme is funded by the major energy companies and if you claim benefits, you are entitled to this funding.

Table: Measures Available Under the Energy Company Obligation Scheme

Measure

Homeowners

Private Tenants

Housing Association Tenants

Landlords

Council Tenants

Air Source Heat Pump (ASHP)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Boiler Upgrade or Repair

✅

❌

❌

❌

❌

Cavity Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Electric Heating Upgrade

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

First Time Central Heating (FTCH)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Internal Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Underfloor Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

How Much Could You Get?

The amount of funding available depends on a range of factors, including property type, your existing heating, wall type and potential energy savings from proposed work.

The first step in working out what you could get is to check your eligibility online. There’s a quick form on the Energy Saving Genie website where you can enter your details to see if you are eligible.

If you meet the criteria, you can choose to apply and once your application has been submitted, it will be passed to a Registered Installer.

The Registered Installer will arrange a free survey of your property. You can choose to proceed ASAP with a survey taking place following strict health and safety guidelines or you can choose to wait until after Covid-19.

Once the survey has taken place, the surveyor will report back to the Registered Installer, who will talk you through the grants that are available towards energy-efficiency measures at your property.

The grant is paid directly to the installer and they are awarded on lifetime savings (LTS) scores. Currently electric heated properties and larger properties tend to receive the most funding. But even if your home isn’t large or heated by electricity, it is worth applying as you could still receive a significant grant towards home improvements.

So if you are one of the many million new Universal Credit claimants due to Covid-19, you can start the process of applying for a home improvement grant that will knock £££s of your energy bills for years to come, well after the pandemic has passed.

Disclosure; This is an adapted reblog of an original post by Energy Saving Genie. It is also a sponsored post. If you click through and end up taking advantage of this government scheme, I will receive a fee for introducing you. This will not affect any products or services you may receive or the value of any grants you may be awarded.

If you enjoyed this post, please link to it on your own blog or social media:

For many of us, our mortgage is our biggest monthly outgoing. So it’s important to keep a close eye on it and check regularly whether you could save money by switching to another provider.

That’s exactly what a new online service called Dashly aims to do. They evaluate your current mortgage deal against the whole market, taking into account your specific personal circumstances as well. If they find a better deal for you they let you know and – if you choose to proceed – assist you with the switching process.

How Does Dashly Work?

Dashly is available as a desktop site, with mobile apps for iOS and Android coming soon.

You start by registering and entering some details about your current mortgage and your personal circumstances. The latter is important, as things such as your income, employment type, credit score and age can all affect the deals you could be eligible for. This process takes 10-15 minutes. Dashly then compares your mortgage against an average of 10,000 products to find the best deal for you.

If they find a better deal than your present one, they send you a notification. You can then evaluate this and decide whether you want to switch. If you do, the team at Dashly will assist you with the switching process.

In addition, Dashly will continue monitoring your mortgage every month. If they find you could save money by switching again, they’ll let you know. It’s worth noting that the equity you have in your property changes on a monthly basis due to ever-changing house values and your decreasing mortgage balance. As your LTV (loan-to-value ratio) decreases, your mortgage may qualify for better, cheaper deals. Again, Dashly checks this on your behalf.

You receive a detailed personal report from Dashly about your mortgage every month. In addition, your dashboard will show you all the key facts at any time, from the changing value of your property to the amount of equity in it, any current deals that would save you money to your next payment date. It’s all there on one easy-to-read web page.

How Much Could You Save?

The savings can be substantial. Dashly say that on average their users save £2,620 (see footnote).

Of course, in practice savings will depend on a number of things, including the balance outstanding on your mortgage, the competitiveness of your current deal, the term left to run, and the effect of any early repayment penalties. Dashly takes all of these things into account in determining whether you could save money by switching to a new lender (and by how much).

Are There Any Costs?

Using Dashly is free. There are no hidden charges and Dashly say they will never hit you with advertisements or email campaigns to try to make money from you. They get paid out of mortgage provider fees, and are authorized and regulated by the Financial Conduct Authority.

Dashly are also founding members of Finance For Good, a charity run by social impact fintechs who put consumers first. They say that their security rivals that of the world’s leading banks.

In Conclusion

If you have a mortgage, in these uncertain times it’s more important than ever to ensure that you aren’t paying over the odds for it.

Dashly offers a free service that not only checks whether you are getting the best deal currently but also continues monitoring your situation month by month and recommends switching again if a new and better deal arises.

By using Dashly you could painlessly save hundreds or even thousands of pounds on the cost of your mortgage. There is never any obligation to switch or any fee to pay for the service. So you really have nothing to lose and everything to gain by registering for an account today.

Footnote: Your individual savings may vary and will depend on personal circumstances. £2,620 per year is the average amount based on research Dashly has conducted on the mortgage market. Find out more at www.dashly.com/reference-index.

Disclosure: This is a sponsored post on behalf of Dashly. If you sign up and make use of the service, I may receive a referral fee for introducing you. This will not affect in any way the service you receive or the deals you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Life insurance isn’t the most exciting of subjects, but in these uncertain times it’s something we all need to think about.

Not everyone requires life insurance. If you are single with no dependants and/or on a very low income, it may not be necessary or appropriate for you. But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death.

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

What Doesn’t It Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

Other things being equal, the younger and healthier you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Bespoke Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It is therefore important to establish what is the most appropriate option for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Bespoke Financial. They are independent insurance and mortgage brokers, and will take the time to establish your exact requirements and design a ‘bespoke’ package to suit you and your family’s needs. Their trained advisers will visit you in your home (with all necessary Covid precautions) or you can speak on the phone to them. They can arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on.

To get an initial personalized quote, click through to the Life Insurance page of their website and answer six quick questions. You can then discuss this with an adviser to ensure you will be getting exactly the right type and level of cover for your needs.

And as an added bonus for readers of my blog, you can get a free will just by asking for a quotation. You can’t say fairer than that, now can you?

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Bespoke Financial. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

A great number of people today need to transfer currencies, or receive transfers from abroad, for many different reasons. As globalization extends, this need has become more frequent as geographical borders become less relevant.

For example, our parents couldn’t even dream about services like eBay or Alibaba, where you can buy anything and have it delivered from a dozen countries away. And the whole thing might be cheaper than buying it in your local store!

But here is where the matter of foreign currency transfers becomes important. Paying for something abroad or getting money sent to you might not be cheap. That’s because not only do you have to pay bank fees for the transaction, you also lose money on currency exchange, which is often a mandatory step in cross-border transfers.

Luckily, today there are alternative money transfer services that allow you to cut these costs. You’ll need to look into them if you require regular foreign currency exchange (FX or forex) services.

Why You Might Need to Make Foreign Currency Transfers

One reason you might need to make a large money transfer abroad is real estate. Buying property is an important part of the retirement planning process and many Britons choose to retire abroad. For example, the latest data indicates that there are about 466,000 British pensioners living in the EU. There are even more among the 5.5 million Brits living worldwide.

Even if you don’t plan on moving or buying a vacation home on some tropical beach, you might consider investing. Investing in real estate is one of the less risky methods for growing your fortune. Of course, the coronavirus crisis has heavily affected this industry. But there are still some very promising prospects for the residential housing market.

Also, today you’ll need to make international payments when booking your holiday accommodation. So, if you plan to travel at all, you’ll need to look for cheap money transfer solutions.

Anyone involved in international business also needs to make and/or accept international payments. This also includes the simple process of buying goods through one of the many e-commerce platforms.

In addition to those reasons, if you are an expat or a traveller, you’ll need to exchange money regularly. The same goes for dealing with transfers like inheritance or even accepting dividend payments from your investments.

All in all, living in the modern world makes you exposed to foreign currency exchange and transfers in many ways. Therefore, the knowledge of how to save money on these transactions is sure to be useful.

How Much Do Foreign Currency Transfers Cost in a Bank?

The cost of an international bank wire transfer is a very complicated issue. First of all, you need to understand that banks will advertise, and sometimes even show you, only the transfer fee. In the UK those range from £8 to about £40. That doesn’t seem too bad, especially for large transfers, right?

However, the truth is that banks are deceiving customers most of the time. If they were fully transparent, you would understand that what truly matters is the FX rate margin. That’s the amount that the bank charges per currency conversion on top of the mid-market exchange rate.

Simply put, high FX margins are why you lose so much money on currency conversions. Different banks use different margins and that’s why they offer different exchange rates. But if you compare the options offered by top UK banks, you’ll see that they are all very close.

Therefore, you don’t have much of a choice.

Also, there might be additional fees involved in a cross-border money transfer. The recipient bank might charge its own fees. If there are any intermediary ‘stops’ along the way, more fees will come.

All things considered, the real cost of an international money transfer can go up to 3-10% of the transfer amount. This cost will be higher for exotic currencies and transfers to remote locations. It will go down a bit for large transfers because banks might offer better terms to VIP clients.

However, the total will always be quite high.

Leading Money Transfer Service Alternatives From the UK

With bank transfer costs so high, a necessity for an alternative emerged. The solution came in the form of FX brokers and money-transfer companies. These businesses offer services similar to banks, but they have much lower overhead costs. Therefore, they are able to keep both the margins and fees very low.

In fact, many companies charge no transfer fees at all for the majority of transactions. However, they use different margins that often depend on the transfer size. Thus, you should always compare foreign currency transfers before choosing a service. This won’t be difficult as all top companies in the industry offer free quotes. They also have transparent pricing schemes.

On average, a transfer with one of these companies will cost you 1-3% of the total. Industry leaders even offer options that allow you to cut costs below 1% for large transfers.

The most notable UK-based FX companies today are TransferWise and WorldFirst. There are other notable businesses as well. However, they cannot compete with these two giants that have multi-million funding.

TransferWise

TransferWise launched not even a decade ago and it has already become a major disruptor in the banking industry. It took over the FX money transfer industry rather fast as well. The main selling point of this company was offering not merely cheap transfers but also a fixed margin scheme.

This means that TransferWise managed to offer its customers consistency and a chance to save a great deal of money. Because of the fixed margins, its services were the most affordable in the industry. The company is now valued at over $3.5 billion and it’s expanded to many countries, including the US.

WorldFirst

WorldFirst is another veteran in the FX transfer industry. This company built a solid reputation for its reliability and trustworthiness. Launched back in 2004 literally from a basement, WorldFirst became one of the industry leaders within a few years.

In 2019 this fintech business was purchased by Ant Financial of the Alibaba Group. This allowed WorldFirst to launch a major change in pricing. It had already been one of the top companies, but it could not compete with TransferWise in affordability. However, the new pricing scheme with fixed margins that go below 0.55% makes WorldFirst a cheaper alternative even to TransferWise. At the moment, there is no cheaper option for foreign currency transfers in the UK. Also, WorldFirst has a very wide reach due to its association with Alibaba, though it’s not yet available in the US.

In Conclusion: Do Your Research for Saving Money on Foreign Currency Transfers

FX money transfer companies today offer great opportunities for money saving. However, do not forget that the lowest cost doesn’t necessarily mean the best offer. These companies have a number of requirements and additional services that you should research. For example, some have a minimum transfer limit. Others offer FX hedging tools that will be essential for reducing risks for businesses and investors.

Thus, be sure to compare all options you have available and research them thoroughly. Watch out for scammers, and choose only those businesses that have a good standing in the industry.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

As you probably know by now, from 1st August 2020 people over 75 in the UK lost their automatic right to a free TV licence and now have to pay the same £157.50 a year as everyone else. This was originally due to happen in June 2020, but it was postponed due to the coronavirus pandemic.

For many old people, TV is their main (or only) source of company. Suddenly having to find this quite large sum out of (in many cases) a very limited income may cause them financial difficulties or downright hardship. Some may even have to choose between watching television and paying their heating bills.

Whether you blame the government or the BBC for this parlous situation – and in my view both are culpable – many over-75s will struggle with this, at a time when many are already suffering terrible stress and isolation due to the pandemic. So in this post I will be setting out three ways they may be able to get out of paying this ‘TV tax’.

I hope that this will be helpful if you are over 75 yourself, or if you have relatives, friends or neighbours in this age group.

I’ll start with the best method if you are eligible….

1. Claim Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly if you prefer. Anyone over 75 receiving pension credit is automatically eligible for a free TV licence.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions, around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4% – if only!). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify. Savings Credit is only available to people who reached state pension age before 6 April 2016. Couples where only one partner reached state pension age before 6 April 2016 can also retain savings credit if the older partner had reached 65 and qualified for savings credit before that date AND they have remained continuously entitled to it ever since. Whether you receive guarantee credit or savings credit or both, that will qualify you for a free TV licence.

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount you’re entitled to. The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee that you will receive the amount it shows you.

To actually apply you will need to phone the DWP’s Pension Credit helpline on 0800 991234. You will need your National Insurance number, information about your income, savings and investments and your bank account details. The person you speak to will then take you through the application process. This is a subject I discussed in more detail in this blog post, as I recently helped an older friend to do this successfully.

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional benefits. A free TV licence if you are over 75 is just one of them. You may also get:

reduced council tax (or free if you are awarded guarantee credit)

Even if you only receive a small amount of pension credit, you will be eligible for all of the above. So it really is well worth applying if there is any chance you may qualify. As mentioned above, you can check first using the free online calculator here and then apply by phoning the DWP’s Pension Credit helpline on 0800 991234.

2. Cancel Your TV Licence

If you don’t qualify for pension credit and the free licence that comes with it, you may wish to opt out of paying for a TV licence altogether.

There is no legal requirement to possess a TV licence just because you own a TV. But if you don’t have a licence it’s against the law to watch (or record) most live broadcasts. This also applies to watching on other types of device such as tablets and smartphones. It also applies if you watch via a cable service or satellite TV.

Obviously you aren’t allowed to watch live TV on any of the BBC’s channels, neither can you watch catch-up TV on the BBC iPlayer. In addition, you are not allowed to watch ANY live TV on other channels, even those broadcast from overseas. And you aren’t allowed to record live broadcasts by any TV service even if you don’t watch them till later.

So what ARE you allowed to watch without a licence? You can still watch catch-up TV on other (non-BBC) channels such as ITV Player and Demand 5. You can also watch subscription services such as Amazon Prime TV and Netflix.

You are also allowed to listen to BBC radio and all other radio stations, as radio is not covered by the TV licence.

If you decide to cancel your TV licence, you can do so by going to this page of the TV Licensing website and clicking where it says ‘Tell us you don’t need a licence’. You should also cancel any direct debit you may have set up with your bank.

Note that if you are found ‘cheating’ and watching TV that requires a licence, you could be fined up to £1,000 and even face imprisonment if you fail to pay. So it is best not to cancel your TV licence unless you are sure you aren’t going to need it in future.

3. Get a Black and White TV Licence

Okay, I am cheating slightly here. You do still have to pay for a black-and-white licence, but the annual cost is just £53, so it’s over £100 cheaper.

Black-and-white TVs are available from specialist suppliers and also sold on the online auction site eBay. If you don’t mind returning to monochrome you can save over £100 a year this way. Again, you can cancel your colour licence and apply for a black-and-white licence via the TV Licensing website.

Finally, I would comment that the whole situation regarding TV licensing is currently under review. In particular, the over-75s licence debacle has highlighted the inherent unfairness of a system where people are required to pay for a TV licence even if they only ever watch non-BBC channels. It is therefore possible that in future the BBC may be required to switch to a subscription model like Netflix, meaning that people won’t have to pay a licence fee at all. In my personal opinion this would be a better, fairer system. It would also force the BBC to up its game by producing more shows the paying public really want to see.

I hope you have found this post interesting. As ever, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

One thing the virus pandemic has brought home is how ill-prepared many of us are for sudden emergencies that impact on our finances.

In a short space of time many people have been thrown out of work and/or seen their income plummet, due in part to the virus but also to the measures taken to control it.

Obviously in future there will be enquiries to determine what things government did well and what they did badly, and what lessons need to be learned. But for all of us it has been a wake-up call on how quickly things can change, and the importance of being prepared for a sudden, unexpected hit on your finances.

Of course, that need not mean another pandemic. It could just as well be an accident or illness, losing your job, or a sudden change in your domestic circumstances.

In general financial experts say you should aim to have at least three months’ worth of income in an easily accessible form to cover sudden emergencies. This will give you breathing space to respond and (hopefully) get your finances back on an even keel. The reality is, however, that many of us are not fortunate (or prudent) enough to be in this position.

A survey of 2,000 UK adults by OnePoll commissioned by online banking website Raisin produced some eye-opening results…

Survey Findings

The key findings of the Raisin survey are summarized below:

The average savings amount of a person in the UK is £9,633.30.

Men have almost double (£13,140.61) the average savings of women (£6,869.84).

The lowest average savings in the UK are found in the East Midlands (£6,438.48) followed closely by Northern Ireland (£6,710.00).

Londoners have by far the highest average savings with £28,978.40. This is more than double the second-placed West Midlands (£13,318.35).

Almost 1 in 5 of those aged 55 or over (approaching or at retirement age) has just £1000 or less in savings.

When asked ‘How much, to the nearest pound, do you have in your savings account(s) today?’ 848 of the 2,000 respondents declined to answer the question. Of the 1,152 people who did, replies were as follows:

6.5% said they have no savings whatsoever.

26% said they had less than £1,000 saved.

Using the Trimmean mean, taking the middle 66% of responses to give a realistic figure excluding outliers, the average savings of a person in the UK is £9,633.30.

Regional Variations

Those living in London have more than four times the savings of those living in the East Midlands.

The lowest average savings in the UK are found in the East Midlands (£6,438.48) followed closely by Northern Ireland (£6,710.00)

London has the highest average savings by far with £28,978.40. This is more than double second placed West Midlands (£13,318.35)

Age Variations

The survey found that in general, as you might expect, those in older age groups tend to have more savings:

Average Savings

% With £0 in Savings

% With £100 or Less in Savings

% With £1000 or Less in Savings

18 to 24

£2,481.16

10.83%

27.50%

50.83%

25 to 34

£3,544.16

12.38%

21.78%

42.08%

35 to 44

£5,995.92

7.91%

12.99%

33.33%

45 – 54

£11,013.99

6.34%

11.22%

25.85%

55 and Over

£20,028.60

2.23%

7.59%

18.08%

It’s not all good news for older people, though. Almost 1 in 5 of people aged 55 or above in the survey had less than £1,000 of savings.

The average savings among over-50s are admittedly almost double those of the 45s to 54s (and more than double the national average). But £20,028.60 – the average savings of someone over 55 in the UK – is still less than the national average salary of a full-time employee (£28,677 according to the most recent Government data).

It’s important to note that these findings don’t take into account other assets (such as properties or businesses) people may own. They do, however, represent a large cohort of people who are approaching retirement age and don’t have any significant savings to cushion them from financial turbulence.

My Thoughts

Overall, the Raisin survey indicates that many of us are ill-prepared for any crisis that may affect our finances.

Older people in general are slightly better off, but there are still large numbers heading towards retirement with almost nothing in reserve. That is especially alarming for those who – for reasons such as ill-health or caring responsibilities – are unable to work and dependent on state benefits.

There are, of course, no easy answers. I do appreciate that many people have barely enough income to cover their day-to-day spending. And the appeal of putting money into a savings account has undoubtedly reduced in recent years due to the ultra-low interest rates on offer.

Nonetheless, I do still think it’s essential for everyone to have some accessible savings for emergencies. And the earlier you start saving – even if it’s only small amounts – the more time your money has to grow.

Personally I am currently keeping most of my ’emergency savings’ in a Santander 123 Lite account (as discussed in this recent blog post). This doesn’t pay interest, but you do get cashback on a range of household bills. Even with their £1 a month fee, I am earning around £50 a year tax-free (cashback minus fees) from this account, which in this low-interest-rate environment is at least something. Santander is protected by the Financial Services Compensation Scheme (FSCS) which protects savers with UK banks against losses of up to £85,000 if the bank fails. I am therefore confident that my cash will always be available quickly if I need it.

Another savings option that might suit some people is Raisin (who sponsored the survey mentioned above). They say their ‘free one-stop online savings solution has been designed to help you earn more money from your savings. With a range of partner banks offering FSCS-protected savings accounts with competitive rates in one place, we take the hassle out of finding the right savings account for you.’ On their website Raisin also say they plan to launch an easy access savings account of their own soon.

I hope you enjoyed reading this post and found it informative. I’d love to hear what you do about emergency savings and where (if you have any) you keep them. As always, any comments or questions can be posted below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. You should always do your own ‘due diligence’ in financial matters, and seek advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

As so many of us are struggling financially right now, I’ve teamed up with some fellow UK bloggers for a great giveaway. We have over £100 worth of supermarket vouchers to help two lucky winners with their grocery shopping 🙂

The first prize is a whopping £75 voucher. The runner-up will receive a £30 voucher. Both vouchers will be for supermarkets of the winners’ choice. The prizes will be e-vouchers for supermarkets that offer home delivery, including Tesco, Asda, Sainsbury’s, Waitrose and Iceland (subject to availability).

This giveaway has been organised by my fellow blogger Kellie Steed at the comping website Prize Warriors. Do check out her excellent site if you are interested in winning more cash and prizes from consumer competitions!

To enter the Bloggers Together Giveaway, all you have to do is work down (or up) the Rafflecopter widget below. As you will see, for each action you take (e.g. following a blogger on Twitter or visiting their Facebook page) you will receive one entry. The winners will be drawn at random, so the more times you enter, the better your chances of success.

The closing date is 31st May 2020, so get clicking now!

All of the bloggers listed below have contributed towards this giveaway prize. Please check out their blogs via the links below. They are all well worth reading, and many run giveaways of their own too.

I do hope you enjoy taking part in this giveaway, and even if you don’t win a prize you discover some wonderful bloggers to follow in future.

One small point is that if a winning entry comes from following someone on social media, Kellie will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow (or claim to be following when you’re not), as your entry won’t then count.

Good luck if you enter the Bloggers Together Giveaway – it would be great if a Pounds and Sense reader won one (or both) of the prizes!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media: