My Investments Update – November 2021

As regular readers will know, I recently started posting monthly updates about my investments. These (partly) replace the ‘Coronavirus Crisis Updates’ I was posting from March 2020. You can read my October 2021 Investments Update here if you like

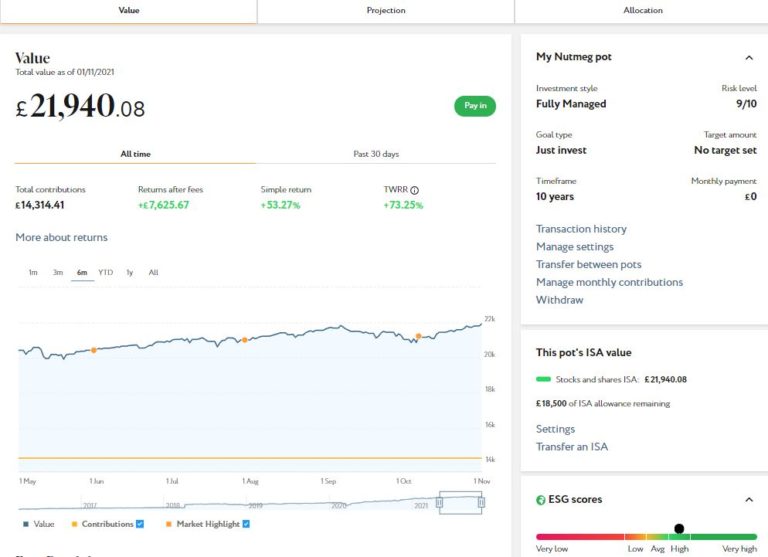

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio is currently valued at £21,940. Last month it stood at £21,046, so that is a rise of £894. That means it has recovered from the £675 drop last month and is now £250 higher in value than it was two months ago.

I know some PAS readers were worried about the falls in their Nutmeg portfolios (and equities generally) in September 2021, so I hope this will provide some reassurance. As I said last time, stock market investments in general should be regarded as medium- to long-term. In the short term some ups and downs are entirely to be expected.

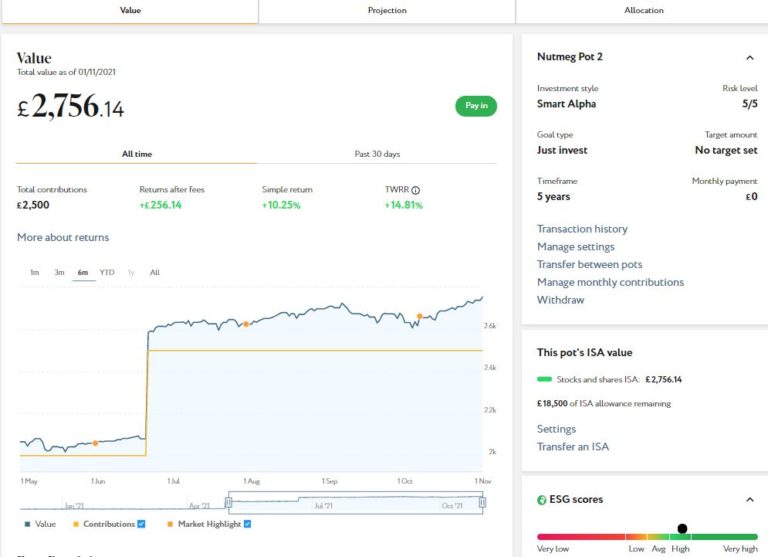

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This pot also rose in value in October. It is now worth £2,756 compared with £2,633 last month. That’s a rise of £123, which again covers the fall last month with a bit to spare. Here is a six-month screen capture showing performance to the end of October 2021.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering. If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually pretty amazed by the difference the risk level you choose makes. If you are investing for the long term (and you almost certainly should be) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I have invested a total of just under £1,000 in AE so far (I began with £100 in February 2021 and topped up twice).

Since I opened my account, my portfolio has generated £24.80 in revenue from rental and £59.97 in capital growth, for a total return of £84.77. I won’t bother publishing a statement on this occasion as it’s not massively different from last month. The bottom line is that I (still) have investments in 21 different projects with them and all are performing as expected, generating income and in most cases showing a profit on capital. So I am very happy with how this investment has been going.

- To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As mentioned, my investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here if you like. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

Another property platform I have some investments with is Kuflink [referral link]. They appear to be doing well, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, where this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £100 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

I’d also particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Kuflink has some similarities with Assetz Exchange (see above). However, it’s important to note that with Kuflink you are investing in loans secured by property, whereas with Assetz Exchange your money is going into actual bricks and mortar. Kuflink loans typically pay around 7% annual interest. With Assetz Exchange projected yields from rental are generally a bit lower at around 5%, but you do of course have the potential for capital appreciation as well. There is also an argument that investments on AE are more secure as properties are typically rented out to organizations such as housing associations which are publicly funded. But I should emphasize that over the years I have been investing with Kuflink I have never lost any money with them and I understand nobody else has either. That is of course no guarantee it couldn’t happen in the future, but personally I find it quite reassuring.

On the subject of property investments, I also have a modest amount in the property crowdfunding platform Property Partner. At one time I was a big fan of this platform, but I lost a bit of enthusiasm when they introduced a raft of extra fees and charges.

Nonetheless, I do still have investments in around a dozen properties with PP, valued from about £30 to £2000 (in one case). The five-year-anniversary process restarted a while ago after being suspended due to Covid. For those who don’t know, after five years investors in a property are given the opportunity to exit at the current market value, as long as there are enough other investors on the platform willing to buy their shares at this price. If not, the property concerned is sold on the open market.

About half of ‘my’ properties have now gone through this process. I voted to sell on each occasion, as I am looking to reduce the total I have invested in property (as I feel too much of my portfolio is still in this form). In some cases all went to plan and I received payment for my shares, which I then withdrew. In other cases, however, not enough investors wanted to buy the shares that investors such as me wanted to sell. Consequently these properties are now being sold, which may of course take many months. Unfortunately the property in which I had £2,000 invested is one of those. To add to the joy, dividends are suspended on all properties that are being sold, so all I can do now is wait for the sales to go through.

On the plus side, Property Partner was taken over a while ago by the US digital home-ownership company Better. One of the first decisions taken by the new owners was to scrap the unpopular £1 monthly account fee and reduce the AUM (Assets Under Management) fee from 1.2% p.a. to 1.0% p.a. They are also offering fee rebates for their most active traders. All of this means that Property Partner may be worth another look now, especially as there’s a steady flow of opportunities to invest in properties going through the five-year process. That means you can buy shares in these properties at a fair market price without having to pay the usual fees associated with new listings.

Anyway, if you’d like to know more, here is a link to the Property Partner website [affiliate]. Note that if you sign up with Property Partner via my link and invest with them, I will split the commission I receive with you, meaning you could get up to £750 cash back.

You can also read my original review of Property Partner here, although this is obviously somewhat out of date now.

Moving on, I have another article on the always-excellent Mouthy Money website. This is all about the difference between saving and investing and why, in my view, you should do both.

In addition, last weekend the Express newspaper published an article about me and my blog, in which I shared some top tips for saving money on food shopping. Do check it out!

That’s all for now, so please stay safe and warm, and look out for your friends and neighbours as well as we head into the cold winter months. I’ll be back again with another investments update at the start of December.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional financial advice if in any doubt before proceeding. All investing carries a risk of loss.

November 4, 2021 @ 3:25 pm

That’s good that your nutmeg ISA’s have recovered from Sep’s drop. Investing more like this is a big priority for me after we’ve paid for our wedding x

November 4, 2021 @ 3:28 pm

Thanks, Rhian. Good luck with the wedding preparations!

November 5, 2021 @ 6:54 pm

Your nutmeg certainly shows that you shouldn’t just look at that kind of investment on a monthly basis, you need a longer period to allow for a few ups and downs and then average your profit over the time.

November 5, 2021 @ 7:10 pm

Thanks, Michelle. True enough. As a matter of interest I checked my balance today and the total value of both my Nutmeg accounts is now up to £25,075. The last month has been pretty spectacular 🙂