The article includes advice on managing your money in later life from a number of UK money bloggers, including yours truly. As a matter of interest, here are the tips I provided, both of which are quoted in the article.

What would your main advice be for an older person wanting to manage their money well?

Don’t bury your head in the sand where money matters are concerned. Keep a close eye on your income and expenditure, and always be on the lookout for ways you can maximize the former and minimize the latter.

Just one example – use a comparison service such as Uswitch.com to see if you could save money on your energy and other utility bills. By switching to cheaper suppliers you could save hundreds of pounds a year for just an hour or two spent on the computer.

What financial mistakes do you think are most common for older people and what can be done to avoid them?

Sometimes with older people pride gets in the way of asking for help and support. That’s understandable, and in its way admirable. But for older people (especially those on low incomes) there are various welfare benefits they may be able to apply for – from Pension Credit and Council Tax Reduction to Attendance Allowance and Warm Home Discount. Nobody will come knocking on your door offering them, though! You need to be proactive about researching what you may be eligible for, perhaps using an online service such as www.entitledto.co.uk. Don’t then let misguided pride prevent you from applying. This is money set aside by the state for people in your situation and can potentially make later life a lot more comfortable for you.

I hope you enjoy reading the article – here’s the link again – and find the tips (including mine!) helpful. As always, if you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

This is a guest post by Sara Williams, who blogs about debt and credit ratings at Debt Camel. She is also an adviser at Citizens Advice.

If you get government help with some of your mortgage costs, you should have heard that this help, known as Support for Mortgage Interest (SMI), is changing from April 2018. About half the people getting SMI are pensioners who get Pension Credit. Many of the rest are disabled.

At the moment the SMI help is given as a “benefit”. But from April 2018, it will only be given as a loan that is secured on your house, so it has to be repaid when the house is sold.

This may sound very worrying. And some people are saying that it isn’t being explained very well by Serco, the firm the DWP is using to try to persuade people to sign the new loan documentation.

With only 6 weeks to go until the change, less than 5% of the people getting SMI have agreed to the new loan. And for people who don’t agree, their SMI will stop in April. This could mean people getting into mortgage arrears and ultimately having their house repossessed.

The same as now. Whatever SMI is currently paid to your mortgage lender, the same amount will be paid after April if you agree to the new loan.

But I’ll need more money each month as interest is now being added to this new loan?

You don’t have to start repaying this new loan, or the interest on it until your house is sold. So on an everyday basis, you will be in the same position as you are now.

Will the interest rate on the new loan increase?

The interest on the will be fixed to the UK Gilt rate – at the start it will be 1.7%. This is the rate at which the UK government can borrow – it will always be cheaper than most mortgage rates.

The loan is from the government, you don’t need to worry that Serco will change these rules and charge you more.

Will there be a delay before it’s paid?

If you are already getting SMI, the switch to the loan will be seamless; there won’t be any months when you aren’t helped.

If you aren’t currently getting SMI, the same waiting period of 39 weeks will apply as now.

Can I repay it if I get a new job?

Yes, you can repay the loan, or part of it, at any time. But it may be better to overpay your mortgage if you have spare money, as your mortgage rate will probably be higher than the interest rate on the SMI loan.

What other options are there?

Some options include:

ask friends or family to help you with your mortgage costs – this isn’t possible for many people;

get a lodger – but this could reduce your other benefits so get advice from Citizens Advice before deciding to do this;

use up your savings – but most people won’t have much and using what you have could leave you unable to afford an emergency;

sell the house and downsize or rent. This is a big change. It may be a good idea if your house is too large or difficult for you to manage or you have an interest-only mortgage ending soon, but you need advice on how it will affect your benefits first.

Should you agree to this?

I don’t like the change. I think it’s unfair and if people lose their homes, it could cost the government more money than it is supposed to save,

But you should make a pragmatic decision based on whether you have any better alternatives. Don’t be swayed by feelings about unfairness or politics.

Complain to your MP if you feel it’s unfair – these changes were discussed in Parliament, but they didn’t get much attention at the time – but don’t reject this loan without a better option.

The loan is cheap. Unless there are relatives who could help you, most people won’t have a good alternative. If you aren’t sure, or you have detailed questions, e.g. about what you are being asked to sign and its implications, go to your local Citizens Advice and ask for advice about the proposed loan and your finances, benefits and any other debts.

Thank you very much to Sara for a concise and informative article about the SMI change, which is clearly likely to affect some readers of this blog. If that includes you, with the new system coming in after 5 April 2018, it’s important to get to grips with the change and decide what is the best course of action for you.

If you have any comments, as always, feel free to post them below.

If you enjoyed this post, please link to it on your own blog or social media:

For older people in particular, energy bills can be one of their biggest expenses. So today I thought I’d set out some ways you can save money on them. Following these tips could save you hundreds of pounds on your annual fuel bills, perhaps even more.

Switch Energy Supplier

This would normally be my top tip for saving money on energy. Due to soaring wholesale prices, however, deals are currently thin on the ground.

Nonetheless, it’s still a good idea to spend a few minutes checking whether you could save money by switching to a different supplier. The quick and easy way of doing this is via a price comparison website. There are a number of these available, but my personal favourite is Energy Helpline [affiliate link].

Just visit this site and enter a few details, including your current supplier and tariff and how much you spend on gas and electricity in the course of a year (it doesn’t have to be exact). The site will then show you the best deals currently open to you and how much you might be able to save by switching to them. In most cases you can also start the switching process by clicking on the relevant link. Before you do, though, it’s worth checking on cashback sites like Quidco and Top Cashback, as some energy companies pay cashback via these sites to people switching their supply to them.

Switching energy suppliers is generally quick and easy, and can save you hundreds of pounds a year at a stroke. Even in these challenging times, it should still be high on your list of potential money-saving measures.

If you are one of the 1.1 million households who use oil for heating, you can save money by shopping around for suppliers too. Check out the oil price comparison service BoilerJuice. Type in your postcode and how many litres of heating oil you’re looking to buy, and BoilerJuice will show you quotes from suppliers covering your area.

Get Financial Help

If you’re in certain priority groups, you may be able to get cash payments to help offset your energy bills.

Winter Fuel Payment is a one-off annual payment of £100 to £300 made to everyone over a certain age. To qualify this winter, you must have been born on or before 26 September 1955. If that applies to you, this money should be paid automatically, but you can phone the Winter Fuel Payment Centre on 0800 731 0160 if you haven’t received the payment before and need to claim. More information can be found on this page of the government website.

In addition, those on certain welfare benefits (including Pension Credit, Income Support and Universal Credit) may be eligible for Cold Weather Payments. This is £25 for any period of seven consecutive days when temperatures fall below zero. More information can be found on this page of the government website.

Finally, you may be eligible for £140 off your electricity bill under the Warm Home Discount Scheme. This is run by some (not all) of the energy companies. If you get the Guaranteed Credit element of Pension Credit you will qualify automatically. But if you’re on a low income and meet the energy supplier’s other criteria, you may also qualify. See my in-depth article about the Warm Home Discount and contact your supplier directly for more information. The large energy companies such as EDF and British Gas all operate this scheme, but some of the smaller ones don’t.

More Top Tips

Here are some more ways you may be able to save money on your energy bills.

Have your boiler serviced regularly, to ensure it is operating at peak efficiency.

If you have an old boiler that keeps breaking down, the time may have come to replace it. The Energy Saving Trust say that you could save up to up to 40 percent on your gas bill by installing a new ‘A’ rated condensing boiler with a programmer, room thermostat and thermostatic radiator controls.

Upgrading your insulation can also cut bills by reducing the amount of heat going to waste. Depending on your circumstances, you may be able to get a free boiler and/or insulation under the government’s ECO (Energy Company Obligation) scheme. You can apply for this via your energy company. Even if you’re not on a low income, you may be able to get a discount on home insulation, so it’s worth checking to see what’s available.

If your radiators aren’t heating up properly at the top, you may need to bleed them to release air in the pipes. Depending on the radiator, you may need a special key to do this or a flat-bladed screwdriver.

Turn down your thermostat by one degree - this can reduce your heating bill by as much as 10%.

Replace old light-bulbs with new energy-saving bulbs. The latest LED bulbs are just as bright as old incandescent bulbs and use a tenth of the energy. They last longer too.

Exclude draughts with heavy curtains and draught excluders by doors.

Turn off heaters in rooms you aren’t using and close the doors.

Don’t leave electrical appliances on standby.

Wash clothes at 30 degrees and try to avoid using tumble driers. Hang washing outside to dry whenever possible.

Get a smart meter installed. The energy companies are fitting these free at the moment. They are great for seeing when and where you are spending money on energy and identifying ways you could save money as a result.

If your funds are limited and you have or develop a disability you may be able to get a Disabled Facilities Grant (DFG) from your local authority to pay for adaptations such as stairlifts.

By taking these steps you should be able to cut your energy bills significantly over the course of a year.

If you have any comments or questions about this post, as always, please do leave them below.

This is a fully updated version of my original post.

If you enjoyed this post, please link to it on your own blog or social media:

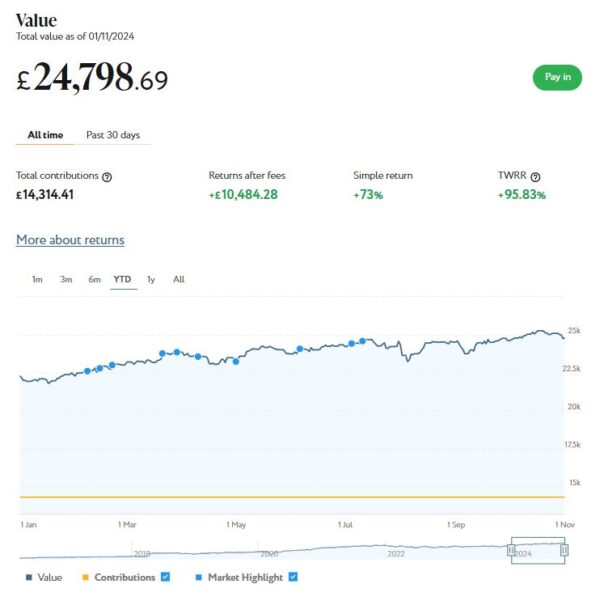

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,799 (rounded up). Last month it stood at £24,625, so that is an increase of £174.

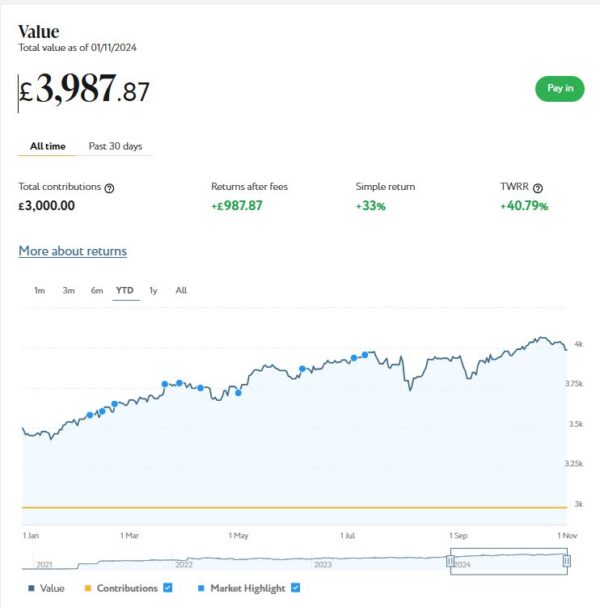

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,988 (rounded up) compared with £3,954 a month ago, a rise of £34. Here is a screen capture showing performance over the year to date.

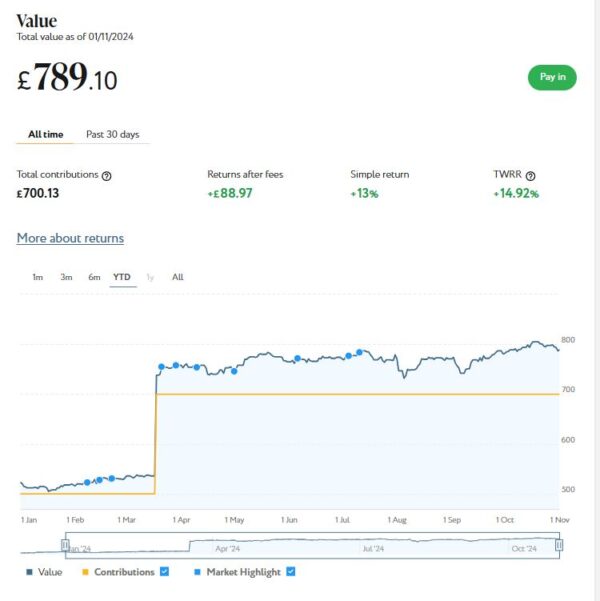

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £789 compared with £781 last month, a small rise of £8.

As you can see, October was another decent month for my Nutmeg investments, though the last few days saw a bit of a dip. The overall value has risen by £216 or 0.75% since the start of October. They are also up by £3,261 or 11.62% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024. Despite some predictions to the contrary, you still have a full £20,000 tax-free ISA allowance for 2024/25. As from this year, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Note that after this month I will not be including Kuflink in my monthly updates. I am gradually winding down my portfolio with them, as part of the de-risking process for my investments as i get older. As I’ve said above, I have no particular issue with Kuflink, though I do think increasing their minimum investment was unfortunate for the reasons stated above. But I still recommend them if their offering suits your investment strategy and risk appetite.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £215.02 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 17 are showing losses. My portfolio of 34 properties is currently showing a net decrease in value of £43.61, meaning that overall (rental income minus capital value decrease) I am up by £171.41. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

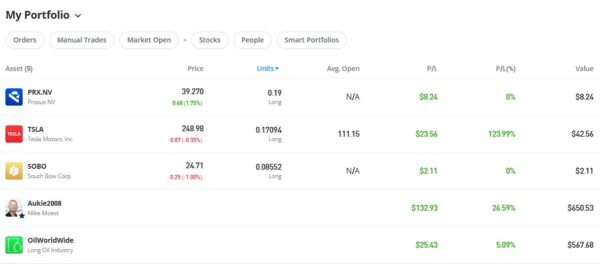

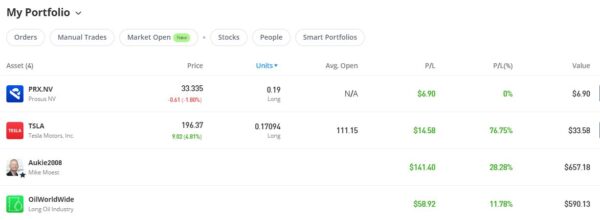

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,271.89 an overall increase of $249.63 or 24.42%.

As you can see, my Oil WorldWide investment is showing 5.09% profit. That’s a bit underwhelming, but at least it’s a profit! Obviously my copy trading investment with Aukie2008 has been doing much better.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in October on the excellent Mouthy Money website. The first is How to Cut Your Energy Bills This Winter. With the coldest winter months fast approaching, energy bills can quickly become a significant financial burden. So in this article I set out some tips to help you reduce your energy costs and keep your home warm without breaking the bank.

Also in October Mouthy Money published my article Always Wanted to be in the Movies? Let TV Studios Use Your Home for Money. As I explained in this, you definitely don’t need to live in a stately home to profit from this opportunity. A huge range of properties is required, so wherever you live there’s a chance it could be the perfect location for an upcoming project.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in October, I particularly enjoyed How to Prepare for a Frugal Winter by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published (or republished) several posts on Pounds and Sense in October. Some are no longer relevant, but I have listed the others below.

In Here’s Why I’m Not Doing EDF Energy’s ‘Sunday Saver’ Challenge I set out my reasons for being dubious about this particular money-saving opportunity. This post has actually generated more comments than any before from readers sharing their experiences. If you’re considering doing this challenge (or a similar one from another energy company) I strongly recommend reading what others are saying about it. I must admit that having seen all the comments (those from Harry especially!) I am now more enthusiastic than I was originally, and will be giving it a try in November. Watch this space!

My post on How to Prepare for Winter Blackouts revealed my reasons for believing winter blackouts are increasingly likely in the UK, from government energy policies to the conflicts in Ukraine and the Middle East. I set out a range of tips to ensure that you and your family are well-prepared should the worst happen.

In Will You Get the Warm Home Discount? I discussed this scheme which provides people on low incomes and/or certain means-tested benefits with a discount of £150 on their electricity bill. This is a one-off payment that will be credited to your electricity account by March 2025 (you won’t receive it in cash). The 2024/25 scheme has recently launched, and in this post I revealed who may be eligible.

In my post Should You Take a Lump Sum From Your Pension Now? I looked at the pros and cons of taking a tax-free lump sum from your pension. Retirees can typically withdraw 25% of their pension pot as a tax-free lump sum once they reach the age of 55. At the time I wrote this there was much speculation whether this tax-free allowance would be removed or reduced by Chancellor Rachel Reeves in her budget. That didn’t happen, but you might still find this article informative if taking a lump sum from your pension is on your agenda sometime soon.

My Review of the Simba Orbit Weighted Blanket was a sponsored post. I was sent this product free of charge by my friends at Simba Sleep. In this post I revealed what I thought of it.

And in Twelve Great Christmas Gift Ideas for Older People (That Aren’t Socks) I set out 12 suggestions for presents for older friends and relatives that – based on my experience as an older person myself – should put a smile on their faces! If you’re struggling for ideas for gifts for older friends and relatives, check this out 🙂

Lastly – as referred to earlier – in October we had Labour Chancellor Rachel Reeves’ first budget. This seemed a very long time coming and was the subject of much speculation – and no small amount of dread – beforehand.

My initial reaction was that it wasn’t as bad as it could have been. Several of the possible measures that had been touted didn’t happen. That includes cuts to the £20,000 annual tax-free ISA allowance, the ending of the old person’s bus pass, and the scrapping of the 25% council tax discount for single-person households. The last two in particular would have been very bad news indeed for older people on top of losing (in many cases) their Winter Fuel Payment. Thankfully these things haven’t happened (yet).

Also on the plus side, the additional investment in the NHS is obviously welcome, though in my view this does need to be accompanied by structural changes to boost efficiency and productivity.

On the minus side, although Reeves presented this as a budget for growth, the rise in employers’ National Insurance contributions and other changes brought in by Labour seem more likely to have the opposite effect. They will discourage investment in the UK and potentially lead to job losses as well. Farmers were particularly hard hit by inheritance tax changes. These will potentially generate huge tax bills for family farms and may result in thousands having to sell up. Any farmers among my readers have my sympathy and support.

We will obviously see how things pan out over the coming months and years, but I can’t say I am particularly optimistic over the direction in which this country is heading. In particular – as regular readers will know – I have serious concerns over the effect the government’s reckless pursuit of ‘Net Zero’ will have on our energy security and standard of living. In my view, far more effort should be put into adapting to the effects of climate change, rather than wasting billions on pie-in-the-sky virtue-signalling schemes such as carbon capture machines and giant flywheels. Okay, I’ll get off my soapbox now!

As always, if you have any comments or queries about this update, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest monthly update about my investments. Note that this month due to other commitments I am publishing this post a few days early. You can read my June 2024 Investments Update here if you like.

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

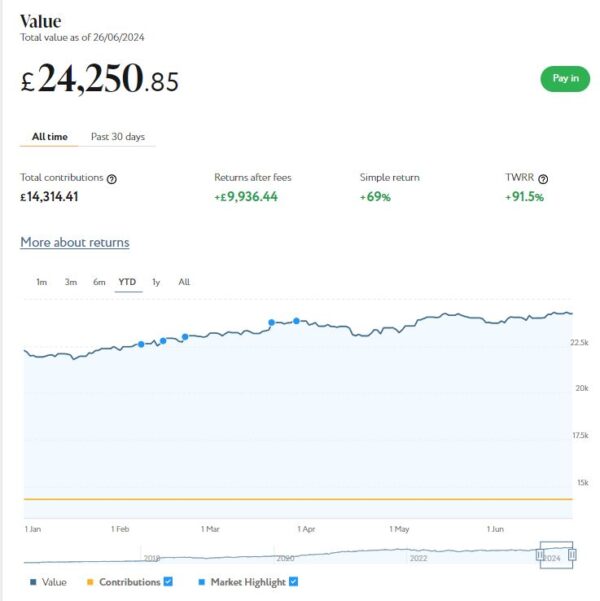

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,250. Last month it stood at £23,744, so that is an increase of £506.

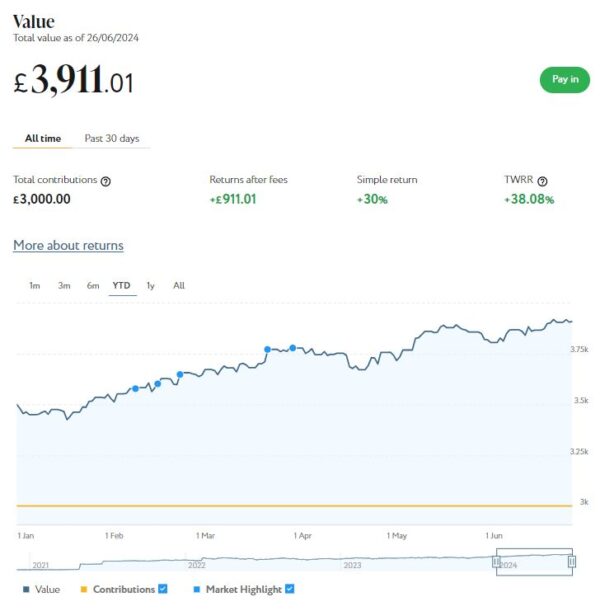

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,911 compared with £3,808 a month ago, a rise of £103. Here is a screen capture showing performance over the year to date.

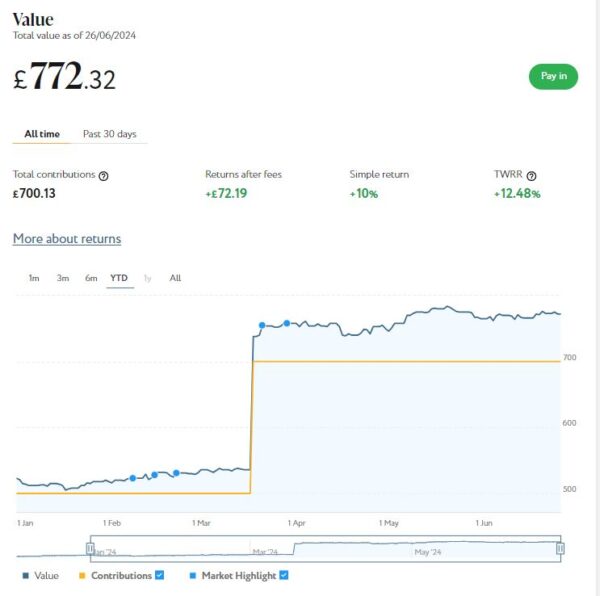

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the screen capture below, this portfolio is now worth £772 compared with £766 last month, a small rise of £6.

As you can see from the charts, June was generally a decent month for my Nutmeg investments. Their overall value has risen by £615 or 2.18% since the start of June. They are also up by £2,618 or 9.95% in the six months since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

You may like to note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to be able to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the new tax year began on 6 April 2024 and and you now have a whole new £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you so wish) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £540 in my Kuflink cash account after another loan was recently repaid. I am still considering whether to reinvest this money with Kuflink or withdraw it and invest the money elsewhere.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £188.95 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £32.84, meaning that overall (rental income minus capital value decrease) I am up by £156.11. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Note that as from this financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

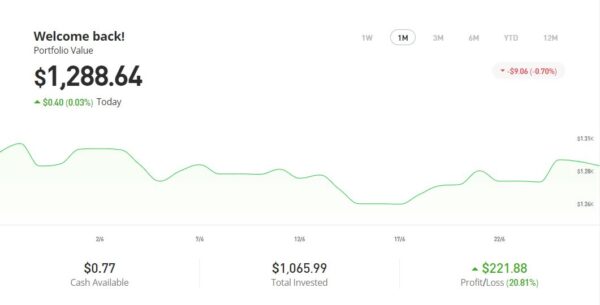

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,288.64 an overall increase of $266.38 or 26.06%.

As you can see, my Oil WorldWide investment is showing just under 12% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port is currently being rebalanced by eToro, so I am hoping this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in June on the excellent Mouthy Money website. The first is How to Save Money on Your Purchases by Haggling. In this I set out a range of tips for saving money by haggling. As I say in the article, you might think this is an ancient practice reserved for bustling bazaars or flea markets in distant lands. But it’s actually a skill that can serve you well in everyday life, even in the modern shopping landscape of the UK.

Also in Mouthy Money last month I revealed How to Cash in on Your Old Gadgets. In this article I described various ways you may be able make money from your old tech (mobile phones, tablets, cameras, satnavs, games consoles, and so on) even if – in some cases – it’s no longer working.

My third article in Mouthy Money in June was Could You Save Money With Home Wind Power? In this article I looked at home wind turbines – what they are, how they work, and the pros and cons of installing one. I also revealed an alternative way of saving money through wind power by investing in a wind farm with Ripple Energy (something I have done myself – see below).

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the wide range of articles published in June, I particularly enjoyed Things We Can Learn From Other Countries About Money by MM’s editor, Edmund Greaves. Ed has lived and worked in various countries around the world, from Argentina to South Africa. He has some eye-opening observations about attitudes to money in these different countries and what we in Britain can learn from them.

I also published several posts on Pounds and Sense in June. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In How to Ensure You Can Cast Your Vote in the General Election, I set out some tips to ensure you are able to cast your vote in the General Election on 4th July 2024. Among other things, I highlighted some issues that older people may face. I also discussed the requirement to bring some form of photo ID to the polling station with you.

Also in June I published How to Protect Your Savings and Investments Under a Labour Government. With the likelihood of this increasing, in this post I set out some hints and tips to help preserve your assets in light of the tax and other economic changes that Labour may introduce. Of course, many of these tips would apply equally to a new government of any persuasion in these challenging times.

Another post was my Review of the New Trading 212 Cash ISA. This new product from the popular Trading 212 platform has been generating a lot of interest, so in this post I took a closer look, setting out the pros and cons as I see them. I also explained why I have opened a Trading 212 Cash ISA myself

A little to my surprise, Trading 212 also reopened their free share offer last month, so I updated and republished my blog post Get a Free Share Worth Up to £100 With Trading 212. This explains how, if you haven’t done so already, you can get a free share when you open a new Invest or Stocks ISA with Trading 212. Note that opening a Cash ISA alone will not qualify you for a free share, but of course you can do both. My advice is to start by opening a Stocks ISA or (non-ISA) Invest account to qualify for your free share, and apply for the Cash ISA after that.

Finally, I published Could You Benefit From Help to Save? This is a government-backed savings account that offers a generous bonus to low-income earners. Launched in September 2018, it aims to encourage regular savings by offering a 50% bonus on the amount saved over four years. There are no age limits to apply, but you must be in receipt of one of three work-related benefits. See my blog post for more information.

Next, a few odds and ends. Last time I mentioned that I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you then decide to invest yourself, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Also as mentioned last time, I recently invested a small amount (£500) via a property loan investment platform called Crowdstacker. I have followed Crowdstacker for some time but never got around to investing with them. They are somewhat similar to Kuflink, but their minimum investment per project is lower (just £100) which makes building a diversified portfolio easier. In addition, rates of return are higher, typically 12% to 16%. Obviously higher returns are generally associated with higher risks, and it’s important to bear this in mind when investing – though as all loans are secured against property, you do have some protection. All investments are available in the form of a tax-free IFISA within your overall £20,000 annual ISA allowance.

Crowdstacker doesn’t have a referral programme as far as I know, so I am just sharing this info out of interest. If anyone has any questions or comments about Crowdstacker, feel free to leave them below as usual.

Finally, my usual reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today, except to remind you to get out and vote on 4th July. I know apathy holds sway across large parts of the country right now, but unless you cast your vote in the general election you can’t really complain about how things turn out subsequently!

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Navigating personal finances can be challenging, especially for those on a limited income. Recognising this, the UK government introduced the Help to Save scheme, which is designed to encourage and support individuals receiving certain benefits to build their savings.

Here’s an overview of how the scheme works, who is eligible, and the benefits it offers.

What is the Help to Save Scheme?

Help to Save is a government-backed savings account that offers a generous bonus to low-income earners. Launched in September 2018, the scheme aims to encourage regular savings by offering a 50% bonus on the amount saved over four years. This means that for every £1 saved, the government adds 50p, potentially providing a significant financial boost for those who participate.

Who is Eligible?

The scheme is targeted at individuals who are receiving certain benefits. Specifically, you can open a Help to Save account if you are:

receiving Working Tax Credit

entitled to Working Tax Credit and receiving Child Tax Credit

or claiming Universal Credit and have earned income of £722.45 or more in your last monthly assessment period

It’s important to note that you need to be living in the UK to be eligible, though if you are a Crown servant or a member of the armed forces posted overseas, you can still apply.

How Does It Work?

Once you open a Help to Save account, you can save between £1 and £50 each calendar month. The maximum you can save over four years is £2,400. You don’t have to pay in every month, and you can make multiple deposits each month, provided the total does not exceed £50.

The key feature of the scheme is the bonus structure. Here’s how it works:

Year 1 and 2 Bonus: After the first two years, you’ll receive a bonus of 50% of the highest balance you’ve achieved during those two years.

Year 3 and 4 Bonus: At the end of the fourth year, you’ll receive another 50% bonus on the difference between the highest balance you’ve achieved in the second two years and the highest balance in the first two years.

This means you could earn up to £1,200 in bonuses over the four years if you save the maximum amount. No other savings scheme can come close to beating this.

Are There Any Age Limits for Help to Save?

One of the appealing aspects of the Help to Save scheme is its inclusivity in terms of age. There are no specific age restrictions for opening a Help to Save account, provided you meet the eligibility criteria related to benefits and the general requirement of living in the UK (unless you are a Crown servant or a member of the armed forces posted overseas).

Theoretically there is no upper age limit for Help to Save, but all the qualifying benefits do require you to be earning some work-related income. So if you are retired and living entirely off your pensions and benefits you are unlikely to qualify. If in any doubt, however, you can always apply anyway and see what response you receive.

Why Should You Consider It?

The Help to Save scheme provides a risk-free way to build a financial cushion. The bonuses are guaranteed and tax-free, which makes it an attractive option for those looking to save a small amount regularly without any risk of losing their money.

Additionally, the flexibility of the scheme allows you to save what you can, when you can. There is no penalty for missing a month or for withdrawing your money. However, frequent withdrawals might impact the bonuses, as they are calculated based on the highest balance achieved.

How to Apply

Opening a Help to Save account is straightforward. You can apply online via the official government website or through the HMRC app. To apply, you will need a Government Gateway User ID and password. If you don’t have one, you can create one during the application process.

Closing Thoughts

For those receiving eligible benefits, the Help to Save scheme offers a valuable opportunity to build a savings pot with the added advantage of tax-free government bonuses. It’s designed to be simple and flexible, making it easier for individuals to develop a habit of saving and improve their financial security. If you qualify, it’s certainly worth considering as a step towards a more stable financial future.

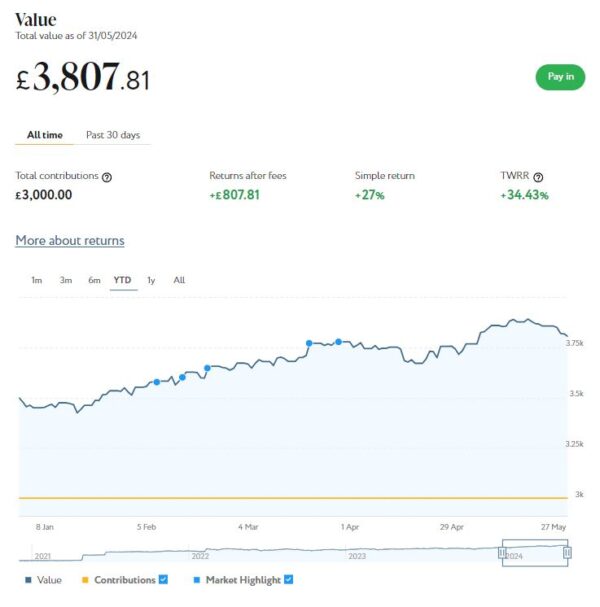

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

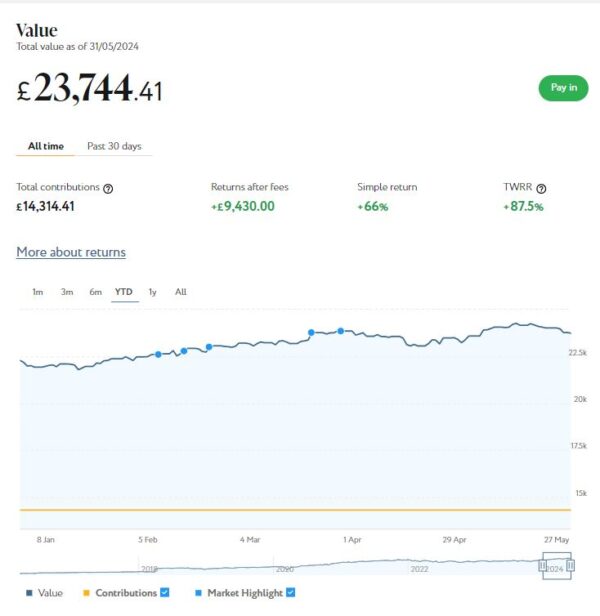

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,744. Last month it stood at £23,502, so that is an increase of £242.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,808 (rounded up) compared with £3,760 a month ago, a rise of £48. Here is a screen capture showing performance over the year to date.

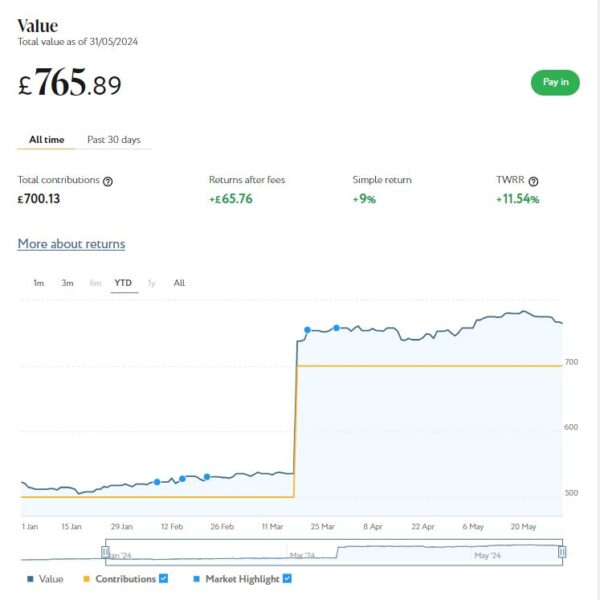

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the screen capture below, this portfolio is now worth £766 (rounded up) compared with £755 last month, a small rise of £11.

As you can see from the charts, May was an up-and-down month for my Nutmeg investments. In the the middle of the month all my portfolios were up substantiaily, but since then they have fallen back a bit. Overall, however, I am still up by £301 over the month, so it could be worse! It’s also worth observing that their overall value has risen by £1,693 or 6.85% since the start of the year (not counting the £200 bonus I invested in my thematic portfolio in March).

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

You may like to note that, for various reasons I won’t go into here, I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to be able to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated 🙂

Don’t forget, also, that the new tax year began on 6 April 2024 and and you now have a whole new £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you so wish) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I withdrew £250 from my Kuflink account last month after a couple of loans were repaid. I currently have around £1,330 invested with them in 8 different projects paying interest rates averaging around 7%. I also have £20 remaining in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £184.78 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 11 of ‘my’ properties are showing gains, 1 is breaking even, and the remaining 18 are showing losses. My portfolio is currently showing a net decrease in value of £31.44, meaning that overall (rental income minus capital value decrease) I am up by £153.34. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Note that as from this financial year (2024/25), you can open more than one IFISA per year.

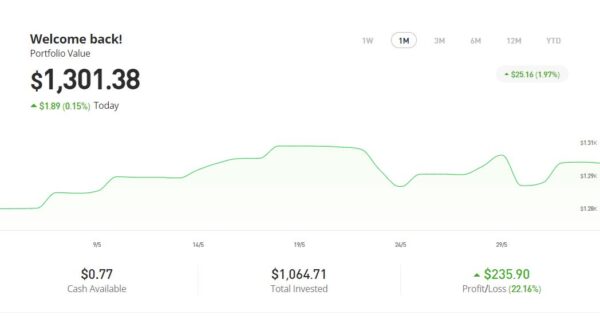

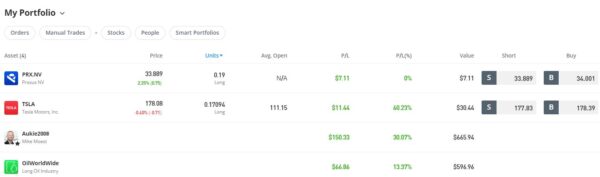

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,301.38 an overall increase of $279.12 or 27.30%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had four more articles published in April on the excellent Mouthy Money website. The first is Earn Extra Money From Online Surveys. In this article I highlight how anyone can use this method to boost their bank balance for very little effort. I set out five well-established online survey sites I use myself to get you started.

Also in April Mouthy Money published my article How to Start a Business with a Franchise. In this I discussed the various attractions of starting a business with a franchise. And I shared some tips on choosing the best franchise for you and how to get the most out of it.

Also in Mouthy Money last month I revealed How to Track Down Old Investments and Bank Accounts using a platform called Gretel. Gretel is quick and easy to use, and free of charge for individuals (Gretel make their money from the banks and other financial institutions they work with). As well as using it for yourself, you can track down lost and missing assets for people you are associated with. Examples might include deceased persons where you are acting as executor, or people for whom you have financial power of attorney.

Finally, Mouthy Money published my article Should You Get Home Storage Batteries? In this I made the point that only a few years ago home storage batteries were very costly and hard for most people to justify. Times have changed, however, with the price of batteries falling while the cost of electricity has risen dramatically. So in this article I examined the case for purchasing a battery energy storage system (or BESS as it’s sometimes called). This applies principally if you have solar PV panels (or plan to get them) but may still be relevant to you even if you don’t.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article sets out various ways you may be able to Save Money in the Sunshine. Let’s hope we actually get some soon! You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in May. In My Short Break on the Isle of Man I talked about my recent holiday on this lovely and under-appreciated island between England and Ireland. It’s less than an hour by plane from most UK airports, or you can get a ferry from Liverpool or Heysham. I went on a heritage-railway-themed break with Newmarket Travel, which I thoroughly enjoyed and recommend. Read the article for more details

Also in May I published Twenty Great Ways to Make Extra Money From Home. This is a fully revised and updated version of my original post of this title. As you will gather, it sets out twenty ways you may be able to make a few pounds extra every month to help boost your finances. None of these methods is likely to make you a fortune, but together they can certainly help keep your bank balance ticking over.

Finally, with an eye to the General Election on Thursday 4th July 2024, I published How to Apply for a Postal Vote. As Pounds and Sense is aimed primarily at over-fifties, I wanted to encourage my readers to apply for a postal vote if this might help them exercise their democratic right to vote. Having a postal vote means that if ill health, frailty or disability prevent you getting to a polling station, you still have the chance to express your political preference. Likewise, you won’t have to worry about obstacles such as bad weather or lack of transport to get to the polling station. There is still time to apply for a postal vote if you wish but you need to move smartly now. This article will tell you everything you need to know.

Also this year I became a regular contributor to Over 60s Discounts. You can read my latest article here: Set Sail for the Sun! Ten Tips for Older Cruisers. As you will gather, this is intended for older people (especially) who are considering going on a cruise – maybe for the first time – to help them get the most from it.

I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

Next, a few odds and ends. One is that I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years).

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you then decide to invest yourself, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Also, I recently invested a small amount (£500) via a property loan investment platform called Crowdstacker. I have followed Crowdstacker for some time but never got around to investing with them. They are somewhat similar to Kuflink, but their minimum investment per project is lower (just £100) which makes building a diversified portfolio easier. In addition, rates of return are higher, typically 12% to 16%. Obviously higher returns are generally associated with higher risks, and it’s important to bear this in mind when investing – though as all loans are secured against property, you do have some protection. All investments are available in the form of a tax-free IFISA within your overall £20,000 annual ISA allowance.

Crowdstacker doesn’t have a referral programme as far as I know, so I am just sharing this info out of interest. If anyone has any questions or comments about Crowdstacker, feel free to leave them below as usual.

In addition, you might remember that a few weeks ago I published a post about a service called Gubbed. This is a no-cost, no-risk opportunity to make at least £1,000 (tax-free). I just need to mention that for operational reasons Gubbed have temporarily stopped taking on new clients. This will not affect existing clients (including several PAS readers), who will still receive their guaranteed minimum £1,000 payouts in due course. But for the time being I have removed any advertising for Gubbed from Pounds and Sense. I will of course let readers know via Facebook and Twitter/X (see below) when they reopen to new clients.

Finally, my usual reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. As I only updated my full review of Nutmeg last week, however, I will keep it fairly brief today.

Nutmeg is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold to avert the risk of pound-cost ravaging.

My main Nutmeg portfolio, which I opened back in 2016, is currently valued at £19,733. Last month it stood at £19,292 so that is a rise of £441. My smaller Smart Alpha investment (opened in 2020) is currently valued at £2,987. Last month it stood at £2,921, so that is a rise of £66. My total Nutmeg investments have therefore increased by £507 month on month.

While the rise in October is of course welcome, my Nutmeg investments are still down by about 11% in value since the start of the year. As I said in my recent Nutmeg review, that’s clearly disappointing, but it’s still a lot less than the amount by which they went up in 2021 alone. And I am still over £5,400 in profit overall. I am therefore philosophical about this, recognising that all investments have their ups and downs and Nutmeg is hardly alone in seeing a drop in values this year. But I do understand why people who started investing with them in the last twelve months or so may be feeling disappointed. You might like to read this recent article on the Nutmeg blog where they discuss the performance of Nutmeg portfolios in 2022 and examine the outlook going forward.

There is actually an argument that now may be a good opportunity to invest while asset values are depressed. At some point we will see a recovery and people who invest at the present time will be well placed to benefit from this. Of course, nobody knows for sure when the recovery will happen or how much further asset values might fall first. Nonetheless, I am certainly considering adding further to my Nutmeg investments in the coming months.

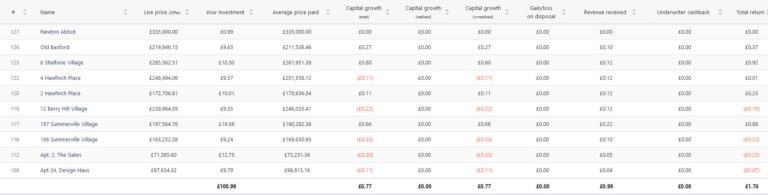

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £81.40 in revenue from rental and £30.80 in capital growth, a total of £112.20. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though five have had their repayment dates put back.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie. Unsurprisingly my investment has been up and down in the last few months, but it is currently about $8 in profit. In these turbulent times I am quite happy with that.

In addition, since I started on eToro, the pound has weakened against the US dollar, so my investment has benefited from this. My $508 US is now worth around £440 in UK pounds, so I am effectively £28 up overall. I am not claiming this as a particular benefit of eToro, but it does demonstrate how exchange rate fluctuations can sometimes work in your favour!

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full in-depth review of eToro here. I am also planning to publish a more in-depth look at eToro copy trading on the blog soon.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled How to Save Money on Petrol. I was actually commissioned to write this when petrol prices were peaking. Since then they have fallen back somewhat, but with no end in sight to the war in Ukraine prices could easily shoot back up again. In the article I discuss my favourite website for monitoring petrol prices locally and also set out my top tips for cutting your petrol (or diesel) consumption.

As a matter of interest, Mouthy Money recently asked if I could increase the number of articles I write for them (so I guess I must be doing something right!). From November they will be publishing two articles a month from me. While they don’t pay me a fortune, the extra cash will undoubtedly help a lot in the cold winter months ahead.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. By now everyone should have received the first instalment (£66) of the £400 rebate all UK residents are due on their energy bills for the next six months. If not, chase it up with your energy supplier.

I am with EDF, and they are crediting the rebate payments to my bank account once my monthly direct debit has been taken. Other energy suppliers are doing it differently, e.g. deducting the rebate from monthly direct debits before they are taken. This article from the popular Moneysavingexpert website explains how different energy suppliers are applying the rebate.

I also received a letter last week confirming that, as I receive the state pension, I shall be getting an enhanced Winter Fuel Payment of £500 in November or December this year, which will be very welcome as well 🙏

In the last few years I also qualified for the Warm Home Discount, which this year is being increased from £140 to £150. The rules are changing, however, and I suspect I shall be one of the people who misses out. The full new rules still haven’t been announced, but I will update my blog post about WHD as soon as I know more.

As I’ve said previously, the government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The Trading 212 offer closes on 8 November 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course 🙂

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

It’s the start of April, so time for another of my monthly Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my March 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

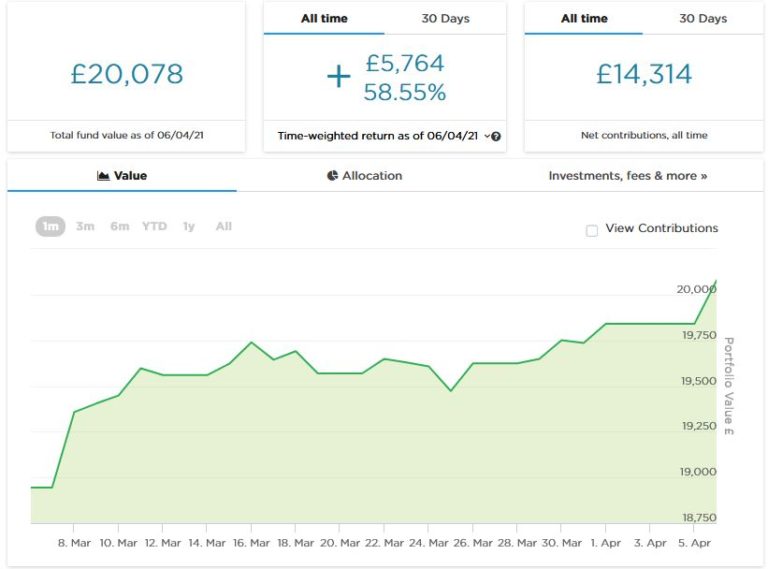

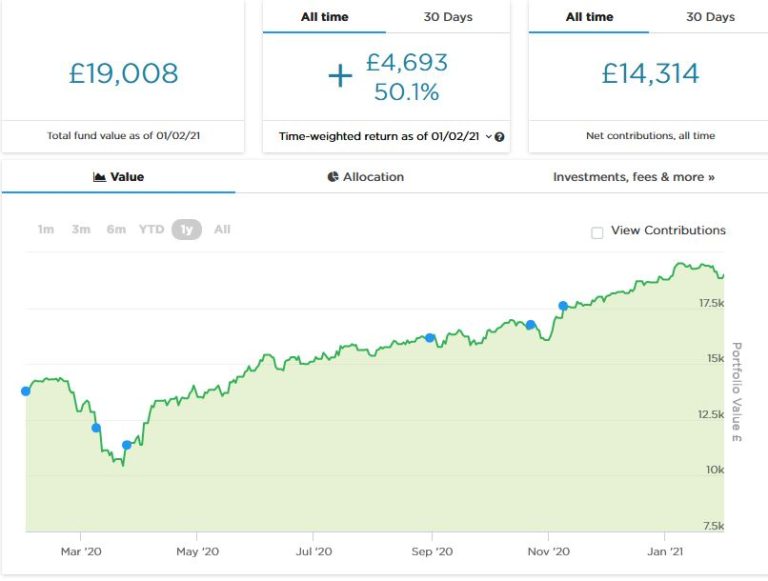

As the screenshot below shows, following a dip in early March my main portfolio has generally been on an upward trajectory. It is currently valued at £20,078. Last month it stood at £19,155, so overall it has gone up by £923. I am very happy with that, obviously.

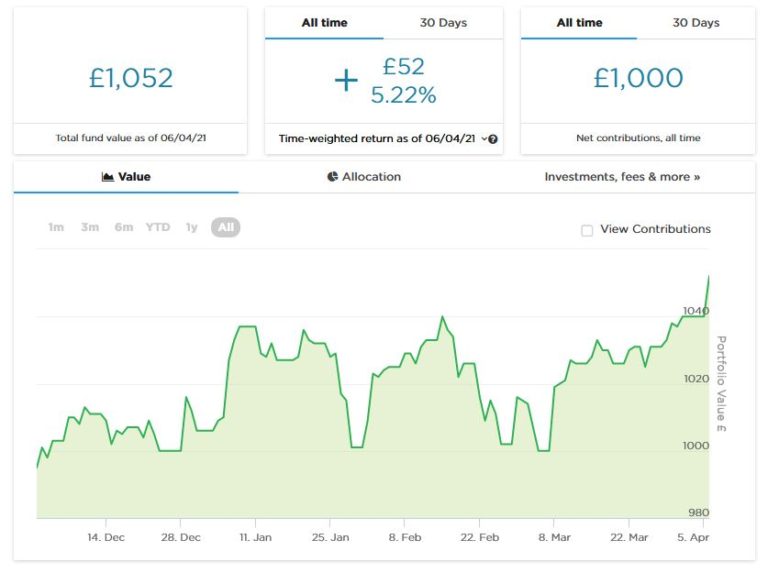

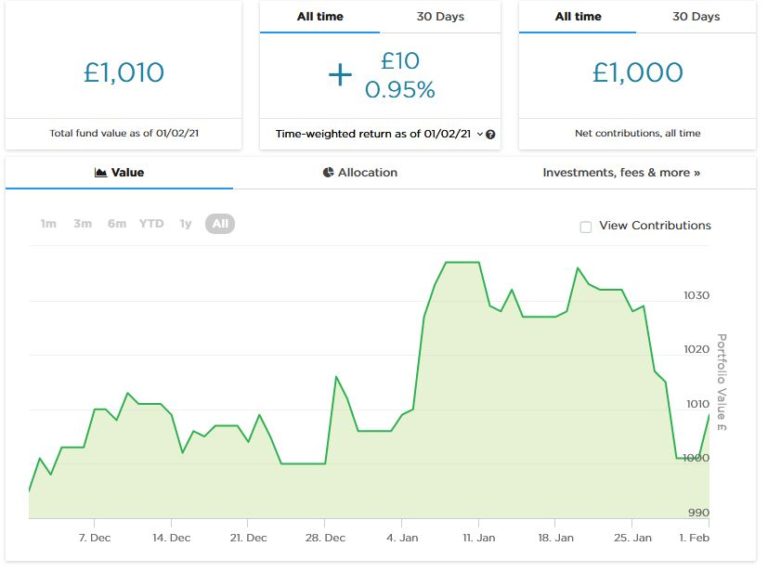

Apart from my main portfolio, four months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. This pot has seen some ups and downs, but right now it is up to £1,052. That’s an increase of 5.22% in four months, equivalent to nearly 16% annually. Here is a screen capture showing performance to date. Obviously, though, it is still too soon to draw any firm conclusions from this.

You can see my in-depth Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

That aside, last month was a mixture of good and bad news on the investment front. Probably the worst news was discovering that Buy2LetCars had gone into administration. Regular readers will know that I invested in two cars with this car loan platform. For three years everything went like clockwork, but then the FCA stepped in and froze their bank accounts due to concerns over how the company recorded the value of car leases in their accounts. This happened just before monthly payments were due to go out to investors in February. Initially Buy2LetCars said they would engage with the regulator to address their concerns, but then everything went quiet till it was announced that an administrator had been appointed to take over the company.

I don’t know any details of what has been going on with Buy2LetCars. I am still not entirely convinced that the FCA acted in investors’ best interests by freezing the company’s bank accounts just as they were about to make payments to investors. But it does certainly appear that the directors of Buy2Let Cars have questions to answer as well.

Personally I am most sorry for people who invested large sums with Buy2LetCars in recent months, including in some cases (I understand) their entire pensions. To be clear, though in the past I did recommend Buy2LetCars based on my experiences as an investor with them, I have never advocated putting all your money into this (or any other) investment platform. As things stand now, when you deduct the monthly repayments received from the capital I originally invested, I am about £10,000 down. That is clearly a major blow but not a total disaster for me.

As I said above, the company is now in the hands of the administrators and I have sent my claim form to them. It’s important to note that Buy2LetCars does still have assets including the cars themselves and the value of the leases, which their key worker clients are still paying. So in due course I am hopeful that some payments will be made to investors, though obviously it will only be a fraction of what we were promised. The letter from the administrators says they will be writing to the company’s creditors ‘within 8 weeks’ with their proposals, so hopefully I will hear something by mid-May. But any payouts are likely to take a lot longer than that to arrive, of course.