I recently saw an interesting survey of the main big-ticket items people have been buying in the UK during lockdown.

The YouGov survey of over 2000 adults was performed by YouGov on behalf of National Conversation Week (see below). The survey was commissioned by insurance services company Paymentshield, who sponsor National Conversation Week.

The top ten items were as follows:

Gadgets or electronics – 22%

TV – 13%

Games console – 11%

Gym equipment – 10%

Jewellery or watch – 10%

Bike – 6%

Expensive equipment to support a hobby (e.g. photography equipment, a musical instrument) – 6%

Pet – 6%

Garden shed – 5%

Art or antiques – 3%

I thought this list made very interesting reading, especially the fact that 1 in 10 people have bought home gym equipment. With gyms closed for many months due to the pandemic, it is no surprise that many of us have been investing in stationary bikes, rowing machines and even treadmills to try to maintain our fitness. I wonder whether people will rejoin clubs in the same numbers now they have this equipment at home.

I am not surprised either to see pets on the list. Certainly in my area I have the impression that many more people now own dogs. I can understand that they provide companionship, especially for those who live alone. Though I do think some of these new owners might benefit from education about how to look after their animals, and in particular the need to pick up after them 😮

I was slightly surprised to see that so many people have been buying jewellery, watches, art and antiques. I guess this may partly reflect that those of us lucky enough to have a continuing income have had fewer ways to spend it, leaving more spare cash available. I just hope the people concerned have checked that they are covered for any expensive items on their home insurance.

Finally, it’s interesting to see garden sheds on the list, with 1 in 20 buying them. I guess this reflects the fact that so many of us are working from home now, for some of the week at least. If you have the space for it, a shed can be a great option for reducing distractions and separating work life from home life. Around here I have also seen one or two mini-pubs created in garden sheds! (See cover image.)

National Conversation Week

National Conversation Week – which this year runs from 7 to 11 June – aims to get people talking in a bid to improve the nation’s well-being, at a time we are all facing unprecedented challenges. In particular, National Conversation Week hopes to encourage frank and open conversations about money. This is especially relevant at the moment, with many people having lost their jobs due to the pandemic and facing stress and hardship as a result.

Above all else, though, be kind to yourself, and don’t suffer in silence. And equally, if you know someone who may be struggling – or you just haven’t seen or heard from them for a while – reach out by phone or at least message them to check they are okay. It may be a cliche, but we really are all in this together. And pretty much everyone is struggling in their own way.

Another month has gone by, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these since the first lockdown started in March 2020 (you can read my May 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

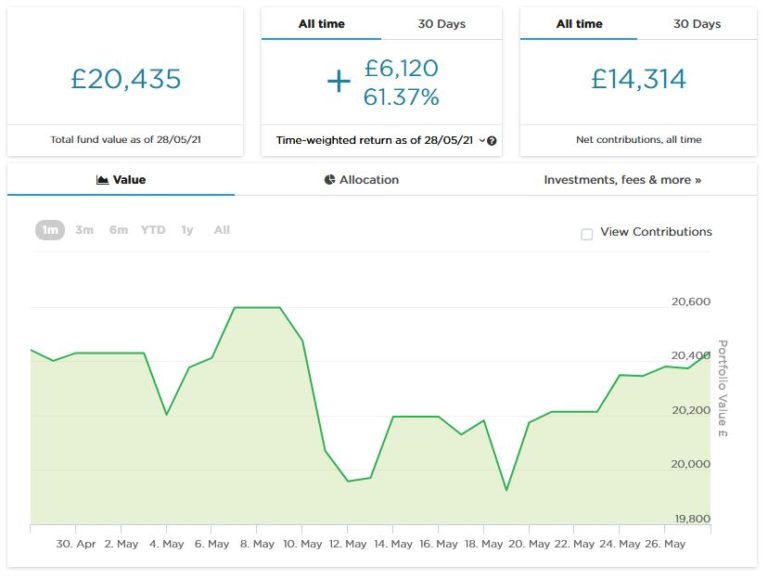

As the screenshot below shows, my main portfolio has been on a roller-coaster ride in May. It is currently valued at £20,435. Last month it stood at £20,430, so overall it has gone up by the princely sum of five pounds! Since 20th May it has been on an upward trajectory, so clearly I hope that trend continues 🙂

.

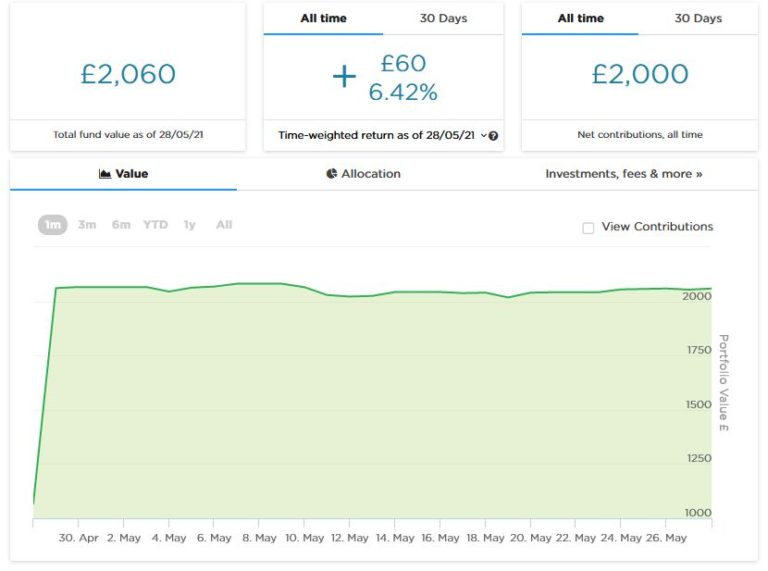

Apart from my main portfolio, six months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This did pretty well, so in April I added another £1,000 from some money returned to me from another investment. This pot is now worth £2,060 (£7 down on last month’s figure). Here is a screen capture showing performance in May 2021.

I updated my full Nutmeg review recently and you can read the latest version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth considering.

If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was truly amazed by the difference the risk level you choose makes.

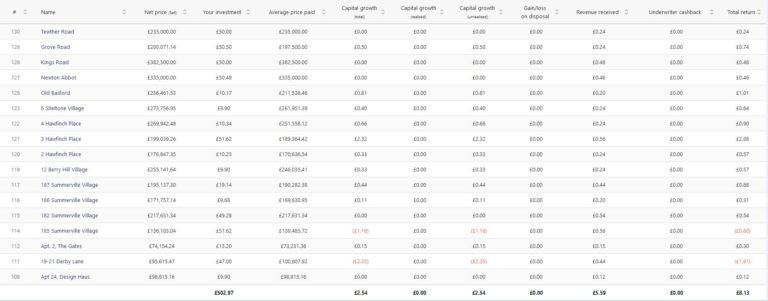

This year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Since then my portfolio has generated £5.59 in revenue received from rental and £2.54 in capital growth for a total return of £8.13. Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio with 17 different projects. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

In May several of the loans I invested in with the P2P property investment platform Kuflink were repaid (with interest) and I duly reinvested the money in other loans.

I have a well-diversified portfolio of loans with Kuflink paying annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often £100 or less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are definitely behind me now!

You can read my full Kuflink review here. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money with them. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year, with built-in automatic diversification. And I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Moving on, if you haven’t seen it yet, you might like to check out this eye-opening post about ‘how much is enough to retire on’ published on the PensionBee blog – I am quoted representing people in their 60s in this article!

You may also like to read my article on the Mouthy Money site in which I reveal why I am not a fan of premium bonds. I was recently hired as a regular contributor for Mouthy Money, so watch out for more articles from me there in the coming months. I also highly recommend reading the articles on the site by other contributors.

And finally, you can read my Q&A on the Lifeline24 blog, in which I talk about Pounds and Sense and share a few financial tips. Lifeline24 is a personal alarm service for older people and people with disabilities. If you’re interested, there is a code to get £10 off their already reasonably priced service at the end of the article. And no, I’m not getting any commission from them!

Personal

In May, as I’m sure you know, more of the government’s lockdown restrictions were eased. In particular, pubs and restaurants were allowed to open inside as well as out. Considering the monsoon-conditions that ensued after the outdoor reopening in April, that was a relief all round!

Last week I enjoyed my first pub lunch since the autumn at the Spread Eagle in Gailey, near Cannock. I met up with my old friend Liz, a former colleague from my days working at Wolverhampton University (the last ‘proper’ job I ever had). It was wonderful to see Liz again and in retrospect I hope I didn’t come across as too demob-happy! The food and service were both excellent. The pub was pretty quiet when we arrived at 12.30 but got busier later. There was still plenty of room inside and out, though.

Also in May I had my second Covid jab. For some reason I wasn’t able to book a slot at Whitemoor Lakes where I had my first jab, so this time I made my way to Great Wyrley Community Centre, another voyage of discovery for me. Everything went well, though bizarrely when I arrived a man at the door offered to ‘fast-track’ me if I took a lateral flow test (I declined). I had no side effects at all from this jab (the Oxford again), not even a sore arm. It is strange how people react so differently. I have friends who have had quite nasty reactions, though generally these lasted no more than a day or two. As for me, I have had (much) worse reactions from my annual flu jab.

With the better weather over the last week or two, I have resumed my habit of going for a breakfast walk. This is by far my favourite time of the day for walks, and I now have a good variety of routes to choose from around the local lanes. The photo in my cover image shows the beautiful Wisteria on Hope Cottage. This is about half a mile from where I live and features on many of my routes 🙂

Also in the last month I got back into the habit of reading again. I know many people say they read more during lockdown. However, I found that my concentration and attention-span were badly affected by the pandemic, so I more or less stopped reading for pleasure.

But in the last few weeks I’ve been feeling a bit more relaxed and that has helped me get back to reading, starting with some short books. Initially I picked up The No. 1 Ladies’ Detective Agency by Alexander McCall Smith. Having enjoyed that I moved on to the follow-up novel, Tears of the Giraffe. which is also very good. I remember that these light-hearted books were made into a TV series a few years ago, so I am thinking of buying the DVD set now.

After that, I moved on to another short novel, The Mountains of Majipoor by US science-fiction/fantasy writer Robert Silverberg.

Silverberg wrote a series of novels set on the giant world of Majipoor. I read most of them around 30 years ago, but for some reason this is the one novel in the series I never got around to.

I did enjoy it, but if you have never read any of the Majipoor novels, I wouldn’t start with this one. The place to begin is undoubtedly Lord Valentine’s Castle, a tour de force of the imagination with a compelling storyline. As a matter of interest, Lord Valentine’s Castle inspired me with the desire to learn to juggle (if you read the book you’ll understand why). But sadly despite many hours of trying I proved to have zero aptitude for it! Here’s an image link (affiliate) to the Amazon UK sales page.

The novel I’m reading at the moment is The Long Way to a Small Angry Planet by Becky Chambers. This is a longer science-fiction novel, which was recommended to me by Amazon as something I might enjoy.

Amazon recommendations can be hit or miss, of course, but I was very glad I acted on this one. The Long Way to a Small Angry Planet is a novel of great wit and charm, and I have been engrossed by it. It is mainly set on a small, commercial spaceship called The Wayfarer, whose job is to ‘tunnel’ wormholes in space. Becky does a brilliant job of bringing the ship and its (mostly) lovable multi-species crew to life.

The story is episodic – you could almost say picaresque – and told from the viewpoints of different crew members – from the reptilian pilot Sissix to the amiable alien chef/doctor called (quite reasonably) Dr Chef. There are some humans too, including the captain, Ashby, and the ship’s clerk and newest crew member, Rosemary Harper, who has a secret that is tearing her apart. There is plenty of humour and emotion alongside the science, so you definitely don’t need to be an SF aficionado to enjoy it. Anyway, I won’t rave on about it any more. If you want to find out more, here’s an image link (affiliate) to the Amazon sales page.

Finally on the subject of books, my nephew Steve (a semi-professional guitarist) has just published his first on Amazon. It’s called Crucial Guitar Basics and was written as a lockdown project. I had a very small input into it and my sister Annie rather more (she edited/proofread it). I’m no guitarist myself but thought it was a well-written and accessible introductory guide. Here’s an image link (affiliate) in case this might interest you. It’s available in both print and Kindle ebook form.

As I write this, the whole UK has just enjoyed its first day since March 2020 without a single Covid death. There is still some concern over the rise in cases of ‘The Indian Variant’, but so far these don’t appear to be causing a significant increase in hospitalizations or deaths. There is some speculation about whether the final stage of the PM’s ‘Roadmap to Recovery’ will take place on June 21st as promised. Personally I think it should, but in my view it’s more likely we will see a partial lifting of restrictions, with others retained for longer. I would particularly like to see an end to mandatory masks, as the evidence in favour of their use is weak (and many US states have done away with them for months now with no calamity ensuing). But we will see, I guess!

I hope that at some point soon I will be able to stop producing ‘Coronavirus Crisis Updates’ as normal life resumes. At that point, I may switch to creating monthly updates about my investments and maybe separate, more personal updates if anyone would be interested to read them. But I will definitely do at least one more full Coronavirus Crisis update next month.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my April 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

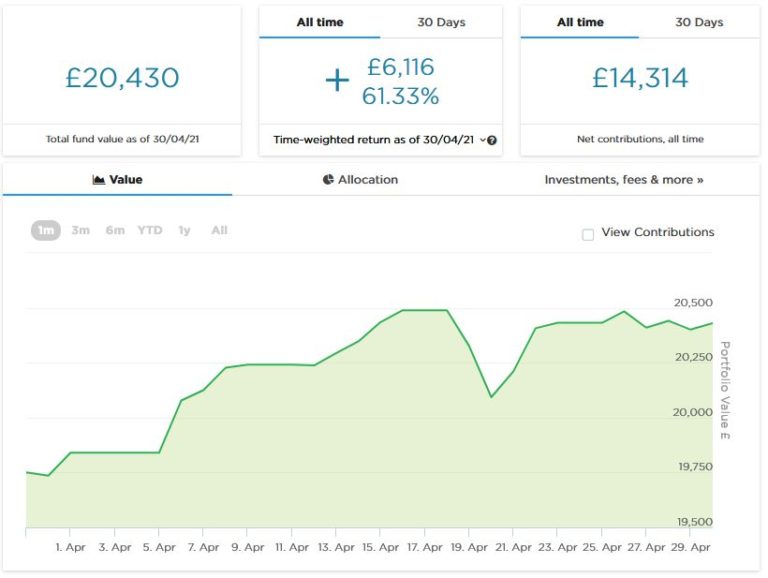

As the screenshot below shows, the value of my main portfolio rose fairly steadily in the first half of April, after which it remained around the same level (apart from a brief dip around the 20th). It is currently valued at £20,430. Last month it stood at £20,078, so overall it has gone up by £352. I am happy enough with that.

Apart from my main portfolio, five months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This has done pretty well, so in April I added another £1,000 from some money returned to me by RateSetter (as discussed in last month’s update). This pot is now worth £2,067. Here is a screen capture showing performance in April.

I updated my full Nutmeg review in April and you can read the new version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

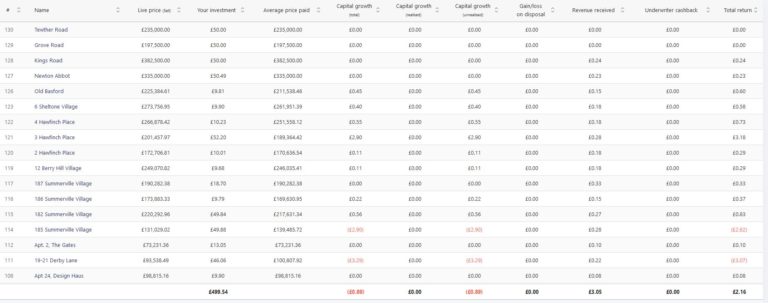

I also added £400 (from RateSetter again) to my initial test investment of £100 with Assetz Exchange. As you may recall, Assetz Exchange is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and (as mentioned) another £400 in April. Since then my portfolio has generated £3.05 in revenue received from rental (equivalent to an annual interest rate of about 10% on my original £100 investment). Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

You may also notice that some of the properties in my portfolio have gone up in value and some have gone down. This makes it a bit harder to judge overall performance compared with an equity-based investment like Nutmeg. The property values quoted by Assetz Exchange represent the best price you can sell at currently on the exchange, which is where all investments on AE are bought and sold. But they are only really relevant if you want to buy or sell that day. By contrast, Property Partner (a somewhat similar P2P property investment platform) quote a value for each property based on an independent surveyor’s valuation every 6-12 months. That means the values displayed on Property Partner are more stable, but of course they are only theoretical as there is no guarantee that this valuation would be achieved if the property was put on the market.

In case you’re not aware, everyone has a generous £20,000 tax-free ISA allowance in the current tax year (2021/22). However, for some reason the government only allows you to invest in one of each type of ISA in any particular.tax year. So you can only put new money into one stocks and shares ISA per year, but you can invest in a cash ISA and/or IFISA as well if you wish – just as long as you don’t exceed the £20,000 total limit. In the 2021/22 tax year I am therefore investing in a Nutmeg stocks and shares ISA and an Assetz Exchange IFISA. This gives me additional diversification compared with investing in just one type of ISA.

Moving on, I heard last month that I will not be eligible for any more SEISS income support payments for the self-employed. Along with many other self-employed people, my income took a hit when the pandemic struck and this money from the government came in very useful (though I do thankfully have a personal pension and other investments as well). However, I have become a victim of the rule that says to receive SEISS your average self-employed income must represent at least half of your total income.

For the first three rounds of SEISS that was indeed the case. However, the latest round of payments incorporates another set of tax returns (2019/20) when calculating average income. Because my income was lower in these accounts (partly due to the pandemic) my four-year average is now less than what I draw from my personal pension. So at a stroke I am no longer eligible for any more support. It’s not the end of the world, but I do find it bizarre that a scheme intended to support self-employed people whose livelihoods have been affected by the pandemic can cut off completely when your average income drops. Commiserations to any PAS readers who may have found themselves in a similar situation 🙁

Personal

In April, as I’m sure you know, some of the government’s lockdown restrictions finally began to be lifted.

I was glad to be able to go for a swim for the first time since Christmas, and have been doing so twice a week since it became possible again. I am a member of the David Lloyd Club in Lichfield which has two pools, one inside and one out. Although I’ve heard that you have to book slots at some swimming pools, that has never been the case at DL Lichfield, and in fact in many ways it feels reassuringly normal. Of course, you have to wear a mask as you enter the building, but thankfully not in the changing rooms or the pool 😀

I have just been told that if the pools get very busy, DL staff ask people to wait in the changing rooms until others have left. I haven’t witnessed this myself and don’t think it happens very often, but am happy to place this info on record.

What I do find bizarre is the rules about buying and consuming refreshments. The club room (aka coffee shop) at DL Lichfield is open for the purchase of drinks and light meals, but you can’t consume them within the building. You are, however, allowed to sit at a table in the club room (no need for a mask) to read and relax or just stare at the four walls. But heaven help you if you try to eat or drink anything.

I was told by a staff member that it was okay to take a drink to the outdoor pool as long as I was going for a swim, but not if I simply wanted to lie on a sunbed. Even though I am fast becoming a connoisseur of strange lockdown rules, this one seems barmy to me and I’d love to know how DL Lichfield plan to enforce it (“Unless you get in that pool in the next five minutes, I’m taking your coffee away.”). I’d like to support the DL club room/coffee shop, but the incomprehensible rules have defeated me. So I’m now taking a flask of tea and a biscuit with me and having that on the poolside or in the changing room after my swim. So far no Covid police have come for me.

I have also been pleased (and relieved) to have my hair cut again, six months after this was last done. Thankfully I didn’t have to queue up, as my hairdresser comes to me and cuts my hair in my conservatory. We have both had Covid jabs and agreed to dispense with masks and just kept the door and window open (thankfully it was quite a warm day). Again, it all felt reassuringly normal.

I haven’t so far taken advantage of the reopening of pub gardens, largely because it has been so cold (and wet) most days. It’s good to see at least some of my local pubs open again, but a shame they still aren’t allowed to open inside as well as out. Last year we had Eat Out to Help Out at a time when there were more Covid cases and deaths then there are now (just one death yesterday, I read). I am looking forward to May 17th when pubs and restaurants can reopen inside as well, but believe this has been delayed too long personally.

I am probably one of the few people who didn’t watch the Line of Duty finale. Indeed, I haven’t watched any of the series, as it didn’t really appeal to me. For one thing it sounded downbeat and depressing, and life has been grim enough recently. But also, it appeared a bit too complicated for my liking. Especially as i grow older, I find following series with large casts and labyrinthine plots increasingly challenging. I can remember laughing (affectionately) at my dad when he expressed confusion at the plot of some TV detective show, but I am obviously going down the same route myself now 😮

I have watched a couple of shows I enjoyed this month, though, so thought I’d share details in case anyone fancies giving them a try.

The first is an Amazon Prime Video series called Upload. This is a dystopian science fiction tale, set in a not-too-distant future when a method has been found for transferring people’s minds at the point of death (or before) to a virtual afterlife. This service is provided by a number of large corporations. They employ minimum-wage ‘angels’ in large warehouse-like offices to monitor these worlds and support the clients who live in them (at least, until their money runs out). It is quite a dark concept, but full of laugh-out-loud moments and some great characters. There is also a mystery in it, and a romance between a female ‘angel’ and one of her (deceased) male clients. It’s well worth a watch if you like something a bit different (and have Amazon Prime Video, of course).

I am also enjoying a US fantasy series called The Librarians (see below). I originally caught a couple of episodes on an obscure Freeview channel and decided I’d like to watch the whole (four) series from the beginning. Doing that proved a bit more challenging than I anticipated, but eventually I managed to track down a DVD box set on eBay.

The Librarians is a tongue-in-cheek fantasy series with a certain retro feel to it. It reminds me a bit of the old Avengers TV show in its heyday (with Diana Rigg as Emma Peel).

The Librarians are a group of misfits who are recruited to work at the mysterious Library, a place where magical artefacts of all kinds are stored. Early in the first series magic is released into the world again, having been suppressed for many centuries. In each episode the Librarians investigate some mysterious incident and try to stop evil individuals deploying magic for nefarious ends, generally using their intelligence rather than violence.

Again, it’s hard to explain in a few words, but you soon get the hang of things. And the characters, while perhaps excessively goofy at times, are all endearing in different ways. The Librarians is really old-fashioned family entertainment (with little if any swearing) and none the worse for that. If you can get hold of it – I’m not sure whether it’s on any streaming services – it offers an enjoyable (and at times hilarious) drop of escapism, something I guess many of us need at the moment.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Spring is here at last, and for once there is plenty of good news in the air.

The vaccine roll-out is going well, cases are way down, and across the UK Covid restrictions are being relaxed. I had my first swim for four months yesterday in the outdoor pool at David Lloyd Lichfield, and tomorrow will be having my first haircut in almost six!

To celebrate all of this, I thought it was high time for another giveaway. I have therefore got together with some of my fellow UK bloggers to offer a bundle of top-quality health and beauty products worth almost £400 for the lucky winner. You can see the full list below ↓↓↓

This giveaway has been arranged and co-ordinated by my blogging colleague Emma at www.MakeMoneyWithoutAJob.com. Do take a look at her site, where (among other things) you can sign up for a free, daily £10 prize draw. There are also articles on money-making topics from How to Make £1,000 Every Month to Online Jobs for Teens, Free Money Offers to How to Make Money Watching Netflix. Literally something for everybody!

The Bloggers Taking Part

Please show your support for all the bloggers taking part in this giveaway by visiting their blogs. They are:

One lucky winner will receive a health and beauty bundle worth almost £400.

Included in this bundle is:

La Roche-Posay Effaclar Duo+ Blemish treatment 40ml

Marc Jacobs Perfect 50ml

Glo32 Teeth Whitening System

CYO Makeup Bag Top Up Bundle

Olay Regenerist Luminous Anti-Ageing Brightening And Protecting Face Cream SPF20 50ml

Footner exfoliating socks

Liz Earle Cleanse and Polish 50ml

Champney’s Calm Reed Riffuser

Champney’s Slumber Body Butter 300ml

Maybelline Sky High Mascara x 2 (Black; Waterproof)

EcoTools – Daily Essentials Total Face Brush set

L’Oreal Paris Men Expert Get Better With Age Anti-Ageing Duo Giftset for him

Too Faced Hangover Wash Away the Day Cleanser 125ml

La Roche-Posay Anthelios Ultra-Light Invisible Fluid Sun Cream SPF50 50ml

Champney’s Weekend Treat Gift Set

Terms and Conditions

1. There is one top prize of a health and beauty bundle.

2. There are no runner-up prizes.

3. Open to UK residents aged 18 and over, excluding all bloggers involved with running the giveaway.

4. Closing date for entries is midnight on 30 April 2021.

5. The same Rafflecopter widget appears on all the blogs involved, but you only need to enter on one blog.

6. Entrants must log in to the Rafflecopter widget, and complete one or more of the tasks – each completed task earns one entry in the prize draw.

7. Tweeting about the giveaway via the Rafflecopter widget will earn five bonus entries into the prize draw.

8. One winner will be chosen at random.

9. The winner will be informed by email within 7 days of the closing date and will need to respond within 28 days with their delivery address, or a replacement winner will be chosen.

10. The winners’ names will be published in the Rafflecopter widget (unless the winner objects to this).

11. The prizes will be dispatched within 14 days of the winner confirming their address.

12. The promoter is www.MakeMoneyWithoutAJob.com

13. By participating in this prize draw, entrants confirm they have read, understood and agree to be bound by these terms and conditions.

The Giveaway

Complete any or all of the Rafflecopter entry widgets below to enter.

One final small point is that if a winning entry comes from following someone on social media, the organizer (Emma) will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and here’s hoping we can all look forward to even better times soon 🙂

If you enjoyed this post, please link to it on your own blog or social media:

At the time of writing there is just over a fortnight till the end of the 2020/21 ISA season. That is all the time you have left to make use of this year’s allowance of £20,000 before it is gone forever.

If you haven’t already used your allowance – and you have money available to invest – it is therefore essential to take action now. Investing via an ISA means that any profits you make will be free of Income Tax, Dividends Tax or Capital Gains Tax. And you won’t even have to declare it on your tax return, which if you’re anything like me will be a welcome simplification…

You can of course put your money into a Cash ISA, but the rates of return on such accounts are currently derisory, and basic rate taxpayers now have a £1000 tax-free savings allowance anyway (higher rate tapayers get £500 and top rate taxpayers nothing at all). The argument for investing in a cash ISA is therefore weak for most people, although if you think interest rates are likely to rise significantly in future there might still be a case for using one. Count me out, though 🙂

That leaves Stocks and Shares ISAs and the relatively new Innovative Finance ISAs (which are mainly for P2P lending). You can invest in either or both of these ISAs up to your annual £20,000 limit, though you can only put money into one of each type in any tax year. In today’s post I wanted to reveal some ways you may be able to get an extra cash boost if you plan to invest in an ISA in the next couple of weeks.

Cashback Sites

I have mentioned cashback sites on various occasions on Pounds and Sense. Basically, these sites refund some of the commission they receive from ‘introducing’ you to a company if you click through to it via a link on the cashback site. The two best-known cashback sites in the UK are Top Cashback and Quidco, though newcomers My Money Pocket are also worth joining and checking out. You might also like to try Cashback Angel, a comparison service for UK cashback websites, which I reviewed here recently.

Clearly you will need to sign up for an account with a cashback site before you can get any cashback from them. I highly recommend registering with Quidco and Top Cashback and maybe My Money Pocket too, even if you aren’t planning to invest in an ISA immediately.

So what cashback offers are currently available with ISAs? On Top Cashback (my personal favourite) one of the best comes from Fidelity. They are offering a maximum of £160 cashback if you open a new Fidelity Stocks and Shares ISA with a minimum deposit of £15,000. But even if you begin with as little as £2,500, you will get £50 cashback. You have to be a new customer and remain invested for a minimum of three months to get the cashback.

If you invest in a Shepherds Friendly Stocks and Shares ISA, an even more generous top payment of £305 is on offer for a maximum £20,000 ISA investment. Or you can earn up to £300 cashback if you set up monthly deposits, though to get this amount you will need to put in £1,500 a month or more. Again, you must remain invested for a minimum of three months to receive the cashback.

Over on Quidco there are also some great offers. With Foresters Friendly Society, for example, at the time of writing you can get £244 cashback with a maximum £20,000 investment. Or you can get £40 cashback with a minimum initial investment of £5,000 (other options are available as well). Again, you must remain invested for a minimum of three months to receive the cashback.

Please be aware that cashback offers change frequently, so I can’t promise that the exact offers mentioned above will still be available by the time you read this post.

For more ideas, just browse the Investment category on either Top Cashback or Quidco. Alternatively – or in addition – you can try searching for any ISA provider you are interested in to see if they have a cashback deal on offer.

Obviously you shouldn’t invest in an ISA purely for the cashback. But if you are thinking of doing so anyway, it is well worth checking what deals are available on cashback sites to get the benefit of the extra money available.

Special Offers

Of course, all investment platforms know that now is a peak time for ISA investment, so they compete extra vigorously to attract new customers. It is therefore well worth shopping around right now to see what offers are available.

In addition, as an ISA investor and money blogger myself, I have access to some special deals and bonuses that I can offer my readers. I’ve put a couple below, both with ISA providers I have invested with personally.

Kuflink

Kuflink is a P2P property loans platform I have been investing with for around three years now. They offer a range of investment options, including an IFISA. They have a generous welcome offer, where you can earn up to £4,000 cashback on a £100,000 investment. Of course, that’s well over the ISA annual limit. But if you invest £20,000 in an IFISA with Kuflink you can get 3 percent cashback or £600, which still isn’t too shabby. For more information about Kuflink and their welcome offer, check out my Kuflink review.

Nutmeg

Nutmeg is a robo-adviser investment platform I have been investing with since 2016. As you will see from my Nutmeg review, I have enjoyed very good returns from them (55.5% to date). They offer a Stocks and Shares ISA using ETFs (Exchange Traded Funds). If you sign up with Nutmeg via my link, while I can’t offer you a cash bonus, you will get six months’ portfolio management free of charge.

I hope this post has encouraged you to use your 2020/21 ISA allowance before it’s gone and maybe take the chance to pocket a bonus or cashback as well. If you have any comments or questions, as always, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss. In addition, please be aware that some links in this post include my affiliate (referral) code, so if you click through and make a purchase, i will receive a commission for introducing you. This will not affect in any way the terms and benefits you receive,. Indeed, as stated above, some offers are only available to people investing via my link.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest monthly Coronavirus Crisis Update. Regular readers will know I’ve been posting these updates since the first lockdown started a year ago now (you can read my February 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

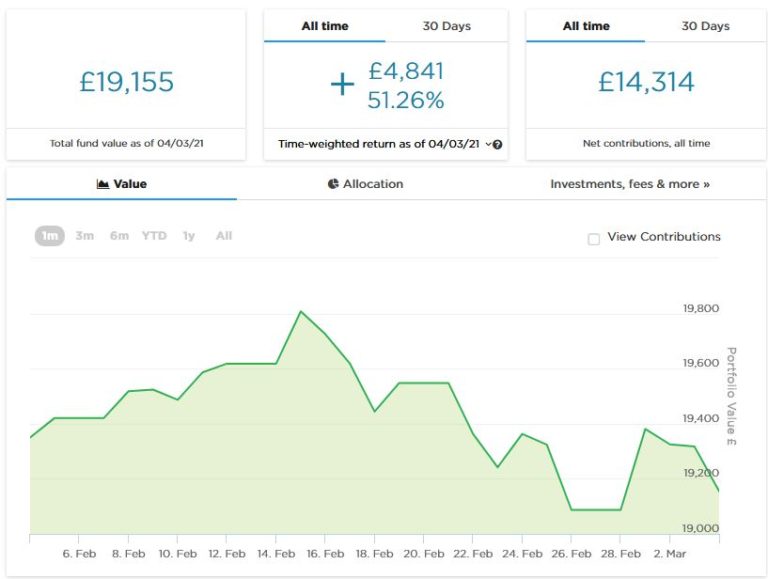

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,155. Last month it stood at £19,008, so it is at least up a little (£147) overall.

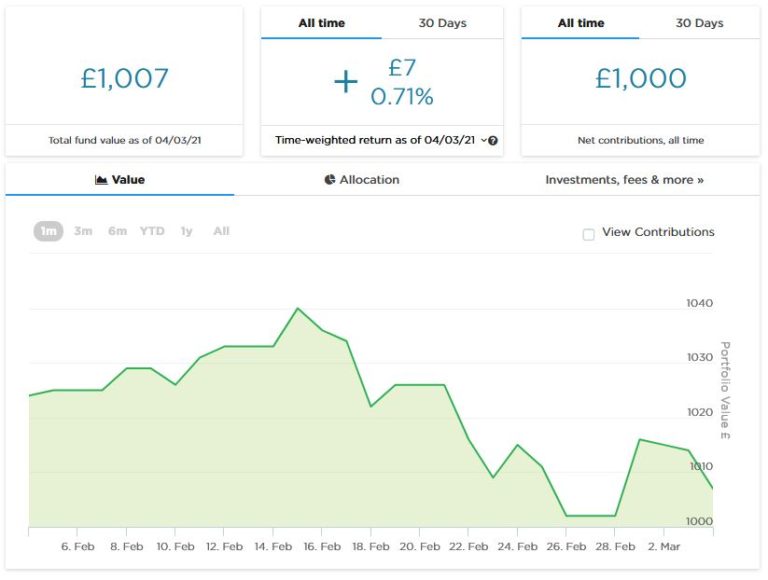

As you may recall, three months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,040 in mid-February, though it currently stands at a more modest £1,007. Here is a screen capture showing performance to date, though obviously it is much too early to draw any conclusions from this.

I mentioned last time that my first investment with P2P property investment platform Property Partner reached its five-year anniversary, at which point investors can vote to sell their shares or continue for another five years. Along with just under half of the other investors, I voted to sell my shares.

The shares of everyone who wanted to sell were duly put up for sale on the platform. Unfortunately, though, there were few buyers, so with a substantial number of shares unsold, the property has been put up for sale on the open market. That means there will be a period of several months – possibly longer – before a buyer is found, and there is no guarantee that the independent valuation price will be achieved.

That is obviously disappointing, though as I only have a very small amount invested in this property (about £50) I’m not going to lose any sleep over it. In my view Property Partner didn’t make much effort to market these shares to investors. I suspect the same may be the case with at least some of the other properties coming up to their five-year anniversaries. It may be that Property Partner are happy to get some of the smaller houses and apartments off their books, especially the city-based ones for which demand has fallen as a result of the pandemic. Currently I have another small investment going through the five-year process. I voted to sell my shares in this too, but suspect the outcome will be the same.

As I have noted before on PAS, shares in many properties on Property Partner are currently available on the secondary market at a discount to the independent valuation price Based on my experiences to date, however, I would advise caution about regarding this as a buying opportunity. If properties that are relisted attract little interest from existing PP investors, they will have to be sold on the open market. In that case you are likely to have a long wait until you see any return on your investment, and there is no guarantee of an overall profit even then. I shan’t therefore be investing on the Property Partner secondary market for the foreseeable future.

That wasn’t the only disappointing financial news last month. Property crowdfunding investment platform The House Crowd unexpectedly announced that it was going into administration. I still have some investments with THC, though thankfully not as many as I did two or three years ago.

Apart from one small loan – which I accepted some time ago had gone south – my remaining investments are in traditionally crowdfunded properties, all of which are currently up for sale. The money is therefore secured by bricks and mortar, so I expect to get at least some of it back (and have of course been receiving dividend payments from rent received). As with other property crowdfunding platforms, each THC property is owned and managed by a separate Special Purpose Vehicle (SPV), which gives it legal protection from claims against THC by creditors. How this will pan out in practice remains to be seen, but I note that the administrators have said that their appointment is ‘not expected to have a material impact on investors.’

So I am being philosophical about this and awaiting further developments. These have undoubtedly been tough times for property investors, and regular readers will know that I also recently lost money with another property crowdfunding platform called Crowdlords. Overall, when you allow for my successful property investments and rental income, I am more or less breaking even, but even so (as I have said on the blog before) I am a lot more cautious about this type of investment nowadays.

Personal

February was another long, cold month, but at least there are signs of better times ahead now. The vaccine roll-out continues to go well and case numbers are dropping rapidly, giving us all hope for a return to something approximating normal life in the weeks and months ahead.

And, of course, we are heading into the spring now, with longer, brighter days and – eventually – the prospect of some warmer ones!

One thing that always lifts my spirit at this time of year – and especially in the current circumstances – is the arrival of spring flowers. In my garden I have crocuses and snowdrops out at the moment, and it won’t be long until the daffodils are in bloom. Here’s a photo of a flower bed in my front garden…

I had my first Covid jab in February, at the Whitemore Lakes mass vaccination centre near Lichfield. It was run by a team of NHS staff, military and volunteers. Everyone was friendly and efficient. The only slight blip came when I was checking in. I happened to notice that the clerk had put ‘female’ on my form, doubtless due to my lockdown hair. She was embarrassed when I pointed this out, but of course I couldn’t just say nothing. I shall be very pleased when we are allowed to visit hairdressers again!

I received the Oxford-Astra Zeneca vaccine. After I had a bad reaction to my last flu jab (fever and nausea) I was prepared for something similar with this, but thankfully that didn’t happen. Apart from very slight soreness in my arm the next day, I had no side-effects at all. I hope I am just as lucky with my second jab, which I have already booked for May.

Also on a medical theme. I had my latest trip to the eye clinic at Queens Hospital Burton last week. Regular readers will know that last autumn I was diagnosed with a perforated retina in my left eye. My first laser treatment was only partly successful, so Iast time I received a (more powerful) top-up treatment. This visit was to check if it had been successful, and I was pleased and relieved to hear that it had. So once again I need to express my thanks and gratitude to all the staff there, and especially to Mr Brent, the consultant who performed my final laser treatment and gave me the good news this time. I have been told that if something like this happens once it increases the chances of it happening again, so I have to be on the lookout for any potentially worrying changes to my eyesight in future. But that aside I am lucky that this problem was detected early before anything more drastic (e.g. a detached retina) occurred – so big thanks to my optician at Vision Express Lichfield as well!

As I write this update, the schools are just about to reopen to all students. I am delighted about that, as I know that it has been a tough time for many children. While some schools have been very good about running online classes, these can never be a complete substitute for face-to-face teaching. I also know from speaking to friends that some schools have been less supportive, simply sending pupils written lessons or assignments to complete on their own. That is obviously less than ideal for younger children especially.

I do think it is regrettable that the government has advised that secondary school children should wear masks in classrooms. The same applies to the mandatory twice-weekly testing. In my view these measures will achieve little apart from traumatizing young people and making it harder for them to learn. I understand these measures have been introduced partly to placate the teaching unions and some worried parents, but hope they will be swiftly withdrawn when (as I fully expect) there is no big ‘spike’ in virus cases following the return. Okay, I’ll get off my soapbox now!

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

As I write this we are still stuck in what feels like everlasting lockdown. But with the successful vaccine roll-out and rapidly falling case numbers – not to mention spring on the way – there are at least a few rays of hope on the horizon.

Anyway, to cheer you up, I’ve joined forces with some of my fellow UK bloggers to put together a giveaway with a top-of-the-range Dyson Airwrap worth £450 for the lucky winner.

As a mere male I must admit I had never heard of this before. But as I have read up about it now, I can tell you that the Dyson Airwrap is a high-tech hair-styling device. It harnesses an aerodynamic phenomenon called the Coanda effect, which curves air to attract and wrap hair to the barrel. So it styles using a flow of air, not extreme heat. This reduces the risk of heat-damage to your hair.

As I am currently sporting a mop of ‘lockdown hair’, I reckon I could probably do with one of these myself!

One lucky winner will win themselves the highly coveted Dyson Airwrap worth a whopping £450! The Dyson Airwrap is currently the hottest tool on the market and with it’s hefty price tag it’s not accessible for many.

The Dyson Airwrap comes with six hair styling attachments to dry, curl, wave and smooth hair. The Airwrap with intelligent heat control measures airflow temperature over 40 times a second and regulates heat, to ensure it always stays below 150°C.

The Dyson Airwrap also comes with a tan storage case to store your Airwrap and its attachments safely.

How to Enter

To enter simply complete all or any of the Rafflecopter entry options below. The more you complete, the more chances you have of winning.

The competition ends at midnight on Sunday 14th March and a winner will be drawn on Monday 15th March. If for any reason the chosen prize is out of stock at the time of the draw, the winner will be able to select an alternative prize up to the same value.

For full entry terms and conditions please see the Rafflecopter widget below.

One final small point is that if a winning entry comes from following someone on social media, the organizer (my colleague Neesha Rees) will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and here’s hoping we can all look forward to brighter times (and better hair) soon 🙂

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest Coronavirus Crisis Update. Regular readers will know I have been posting these since the first lockdown started in the spring of 2020 (you can read my January 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

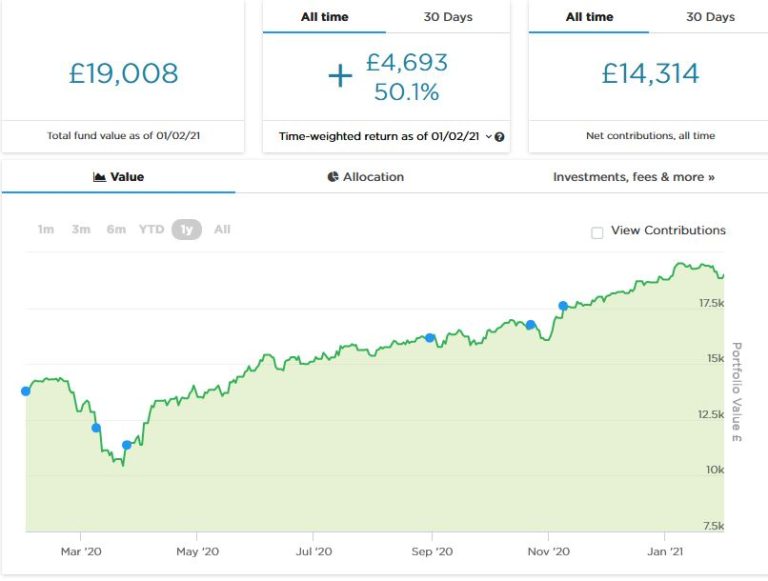

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,008. Last month it stood at £18,886, so it is at least up a little (£122) overall.

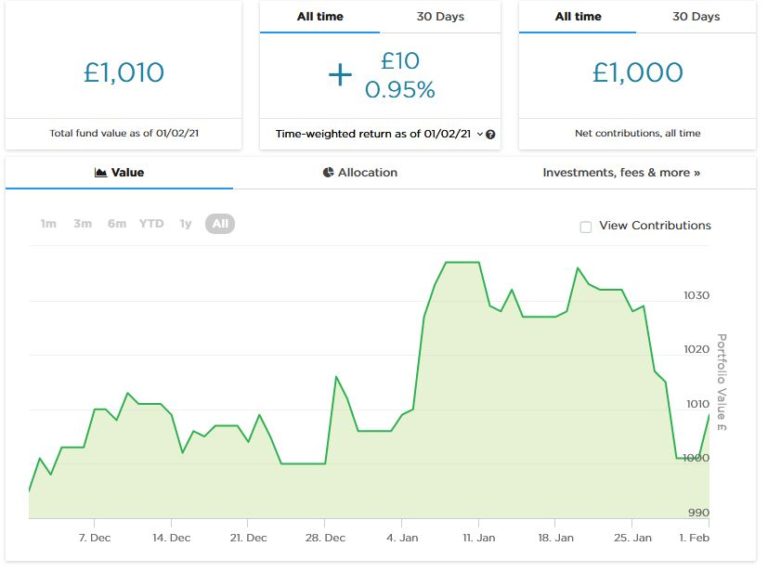

As you may recall, two months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,037 in mid-January, though it currently stands at a more modest £1,010. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

Incidentally, I was recently asked by Nutmeg to contribute an article about my ‘Investing Journey’ for their blog. This was published in early January and you can read it here if you like. In the original version I was more explicit about why I left the charity I used to work for (basically a personality clash with the new Director who saw me as a rival). Nutmeg presumably decided this might ruffle a few feathers – even 25 years on! – so they changed it to something blandly neutral. Anyway, I thought I should let you know, as the opening section reads a little oddly now 🙂

The Nutmeg article brought quite a few new subscribers to this blog – so if that includes you, welcome to Pounds and Sense! I do hope you find my posts interesting.

Moving on, I had an email this week from the peer-to-peer lending platform RateSetter saying that all their lending activity is being transferred to Metro Bank (which now owns RateSetter). All investor accounts are therefore closing at the start of April, with investors’ money being returned to them in full along with all interest due.

I know some RateSetter investors are unhappy about this, but personally in these turbulent times I’m just glad to be getting my money back with interest. I originally invested £1,000 in September 2018 with an eye to claiming the £100 new investor bonus. The latter was duly credited to my account a year later, so by April I expect there to be a total of around £1,180 in my account. That equates to an annual interest rate of around 7%, which I am perfectly happy with.

This last year has undoubtedly been tough for P2P lending companies, with rising default rates and withdrawal requests along with reduced demand for loans. This has caused some platforms to experience cashflow problems and bad publicity. The only other one I have any money left with is ZOPA, which has also had a challenging year. I have only a few hundred pounds left in ZOPA as I switched some time ago from reinvesting repayments to withdrawing them. I’m not sure I can see much of a future for P2P lending in the UK, but of course in these unique times anything is possible. I don’t foresee myself putting any more money into P2P lending for a while, though.

I also heard recently from Property Partner. As you may know, this is a property crowdfunding platform. A few years ago, when I was investing regularly in property crowdfunding, I put around £5,000 into twenty or so properties on this platform.

Anyway, the email revealed that the first property I bought shares in has now reached its fifth anniversary. All investors therefore have the opportunity to sell up at the current independent valuation or else continue for a further five years. I voted to sell my shares, since (as mentioned in this recent post) I am currently trying to reduce the total amount I have invested in property crowdfunding.

The way the five-year anniversary process works is that all shares owned by investors who want to sell are bundled together and put up for sale on the Property Partner site. Assuming they are all bought by other investors, everyone who voted to sell then gets their money back at the current valuation. If that doesn’t happen, Property Partner put the property concerned up for sale. But obviously that is likely to take months and there is no guarantee the valuation price will be achieved. So you might end up getting back less than anticipated (or perhaps more in a best-case scenario).

Obviously I’m hoping this process goes smoothly and I get my money back soon. I would comment, though, that many of the properties that are coming up to their five-year anniversary are on offer on the resale market at well under the current valuation price. So if you are of a speculative persuasion, there is an opportunity to buy shares now at a discount and maybe make a quick-ish profit through selling up via the five-year anniversary process. I must admit I am tempted to try this, but haven’t made a decision yet!

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently. I am also looking forward to receiving a substantial lump-sum payment in April when my first investment with them matures.

As I’ve said before, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website. Note that you can’t invest with Buy2LetCars through an ISA, so the interest part of the final payment will have some tax deducted. Depending on your circumstances, you may be able to reclaim this.

Finally, several more readers have now signed up with the low-key matched betting opportunity mentioned in some previous updates. New members are still being accepted, but the company has had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

I don’t know about you, but January to me has felt a very long month. It’s been cold, damp and depressing, with the whole country stuck in what seems like a never-ending lockdown.

As you may know, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so. Even so, being unable to see friends and family has been hard for me, as has the closure of my local swimming pool (which I used to visit twice a week). And I appreciate that in many ways I am one of the lucky ones. I don’t have any major financial worries, and I’m not trying to home-school any children!

I did have a ‘day out’ at the end of January when I had to go to the eye clinic at Burton Hospital for a follow-up appointment. As regular readers will know, in the autumn I was diagnosed with a perforated retina in the left eye. I had laser treatment for this, and my January appointment was to assess how successful it had been.

As it turned out, there was some good news and some bad. The consultant told me that the treatment had been three-quarters successful. In one area it hadn’t ‘taken’, meaning I needed top-up treatment. He administered this then and there. I guess he cranked up the laser a bit, as unlike my first treatment it was somewhat painful and I had a headache for a couple of days afterwards. I have to go back at the start of March for what I very much hope will be a final check-up. Keep your fingers crossed for me!

Because they put drops in my eyes at these appointments, I can’t drive. I therefore took a taxi to the hospital and caught the train back. On previous occasions the trains have been very quiet, but there were noticeably more passengers this time. The roads too seemed pretty busy. I get the impression that people are (understandably) becoming fed up with lockdown now and the government’s Stay At Home message isn’t being as well complied with. Not a criticism, just an observation.

I am still aiming to go out for a walk once a day, though with some of the bad weather in January, I have missed a few. Here is a photo of my front garden about a fortnight ago 😮

On the plus side, I do enjoy watching the snow as long as I don’t have any essential trips to make. And I like to go for a walk in it once it has fallen. It was lovely to see (and hear) the local children getting out their sledges and enjoying some much-needed fun during these difficult times.

As far as evening entertainment is concerned, I finished my box-set of the tongue-in-cheek detective series Agatha Raisin and am happy to recommend that. On a similar note, I am enjoying the new (second) series of The Mallorca Files, which is currently on BBC iPlayer. It is just a shame that because of the pandemic they were only able to record six episodes.

Also, inspired by this post by my fellow blogger Caz, I have been investigating what is on offer on Amazon Prime Video. I have Amazon Prime mainly for the fast, free deliveries. But of course members do get access to a range of free films and TV series as well.

Anyway, I found a couple of series I really enjoyed. Being a Star Trek fan, I had to check out Lower Decks, a cartoon series focusing on the junior ranks on board one of the Federation’s least illustrious starships, the USS Cerritos. This has some great laugh-out-loud moments but some good stories as well. There are plenty of allusions to familiar Star Trek tropes that will keep any fan of the franchise amused. Watch out also for an appearance by an evil incarnation of Microsoft’s infamous ‘Office Assistant’ Clippy!

Of course, if you’re a Star Trek fan and haven’t yet seen Star Trek: Picard featuring the great Patrick Stewart as the eponymous hero, you should definitely watch this on Amazon Prime Video as well 🙂

The other series I enjoyed is Undone. Indeed, this is one of the best things I’ve seen on TV for quite a while. It’s almost impossible to describe, but it’s an animation that combines elements of mystery, comedy, romance, science fiction/fantasy, and more. And all with stunning, almost psychedelic, imagery, and strong acting and characterization. Here’s a screen capture that will give you some idea of the style. If you watch nothing else on Amazon Prime Video, give this a try..

Going back to the pandemic, there has at least been some good news this month. The vaccine roll-out has been going well – I’ve just heard that 10 million people have now had their first injection – and the number of new cases has been falling rapidly. As a 65-year-old I have not yet been called for vaccination but assume this is likely to happen fairly soon.

I do hope these developments will allow lockdown and other restrictions to be eased in the coming weeks, as in my view they are causing grave harm to people’s physical and mental well-being. In particular, I would like to see schools reopen, along with swimming pools and gyms. I would also like to see pubs, restaurants and hotels allowed to reopen before many have to close their doors for good. In the (slightly) longer term I would like to see all restrictions lifted so that normal life can resume. I am not a fan of mandatory masks and would like to see them made optional for those who believe they offer some useful protection from the virus (personally I have never been convinced of this).

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Happy New Year! Here’s hoping it’s a better one for all of us than the year just past 🙁

I shall be continuing my monthly coronavirus crisis updates in 2021, at least till we are clearly over the pandemic and something resembling normal life has resumed. Obviously I very much hope that will be sooner rather than later.

Regular readers will know I have been posting these updates since the first lockdown started in the spring of 2020 (you can read my December 2020 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

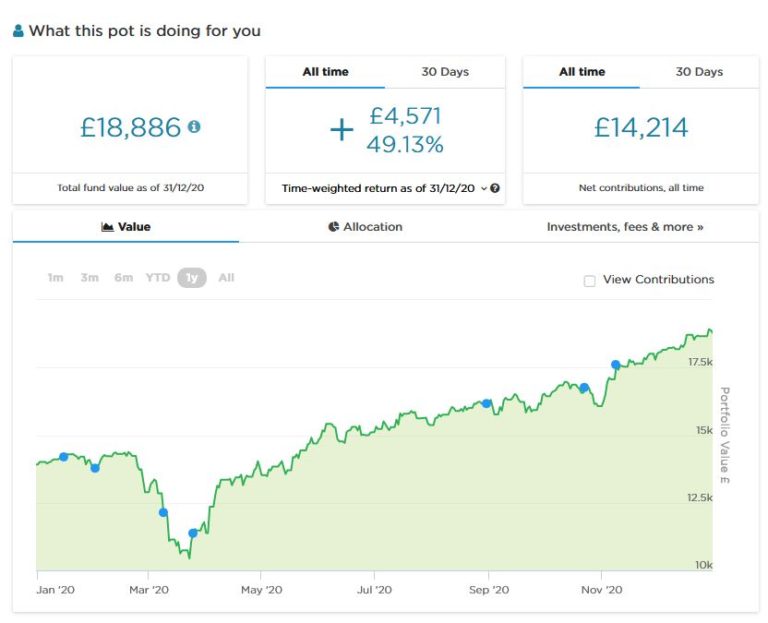

As the screenshot below shows, since last month’s update my main portfolio has continued on a generally upward trajectory and is currently valued at £18,886. Last month it stood at £18,008, so it has gone up by over £800 in value since then. Considering national and world events at the moment, I am more than happy with this.

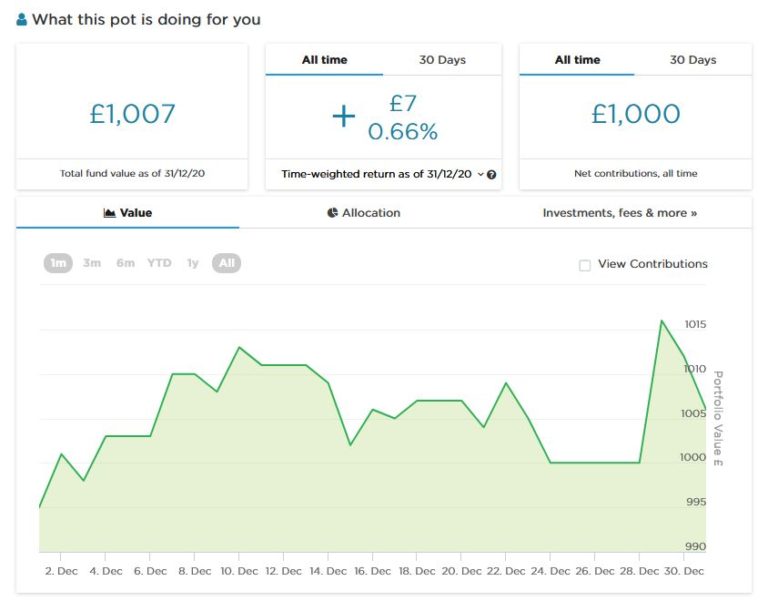

As you may recall, about a month ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. This pot has risen as high as £1,015 in value and currently stands at £1,007. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

You can see my in-depth Nutmeg review here (including a special offer for PAS readers). As a matter of interest I was recently asked by Nutmeg to contribute an article about my investing journey for their blog. I will add a link to the article here once it is published.

I had some bad financial news last month from Crowdlords, one of the property crowdfunding platforms I invested with. Three years ago I put £3,000 into a development project to build what was originally described as six eco-homes (it has lately been known more prosaically as Kennington Road). An update on the Crowdlords website revealed that due to a ‘perfect storm’ of problems caused directly or indirectly by the pandemic, the development had made a loss and investors would receive no returns. At a stroke I lost £3,000, which was (as you may imagine) a bitter pill to swallow.

I plan to write a more in-depth post about this soon, including lessons learned from the experience. But i will say two things now. One is that property development projects are inherently very risky and you shouldn’t invest in them unless it really is money you can afford to lose in a worst-case scenario. And second, while I don’t blame Crowdlords themselves for the failure of this project, I do think their communications about it could have been a lot better. I also think it would be a nice gesture if they were to offer modest ex-gratia compensation payments from their own profits to investors who have been hit hard (I know some people lost a lot more than I did). Events such as this clearly damage the reputation of property crowdfunding and mean investors are less likely to risk their money this way in future. I know I shall certainly be a lot more cautious now!

In fairness to Crowdlords I should add that I have had other investments on their platform which did deliver the promised returns, However, with the loss described above I am certainly down overall with them.

On a brighter note, a couple of the loans I invested in with Kuflink were repaid (with interest) last month, and I duly reinvested the money in other loans.

Kuflink is primarily a platform for investing in bridging loans, and generally these are safer than development projects such as the one mentioned above. There is still a risk of loss, of course, but as your investment is secured by bricks and mortar, it is unlikely you would lose all your money (though delays in repaying loans can and do happen). I have a diversified portfolio of loans with them paying annual interest rates of 6 to 7.5 percent. These days I generally invest a few hundred pounds per loan at most (and quite often under £100). My days of putting four-figure sums into any single property investment are definitely behind me now!

As you may be aware, I recently updated my full Kuflink review. You can read it here if you like. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money on the platform. I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently.

As you may remember, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website.

Finally, I am still getting a few queries about the low-key matched betting opportunity mentioned in some previous updates. I checked with my contact there and they are still accepting new members, but for reasons related to the pandemic have had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you won’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note though that this opportunity is only open to trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

December was another strange month in a depressing year.

A week before Christmas I had my 65th birthday. Normally reaching that landmark would be cause for celebration, but inevitably in the circumstances it was low key. I did at least manage to meet up with a couple of old friends for a birthday tea (don’t tell Matt Hancock!). It was great to see them and they did their best to make the occasion feel special. We had some laughs and a very nice cake, but it still wasn’t anything like I might have imagined my 65th. I didn’t even have the small consolation of being able to start claiming my state pension, as I am in the cohort of people for whom the age has just been raised to 66.

Work-wise it has remained very quiet (as you probably know, I’m a semi-retired freelance writer/editor). I’ve had very little paid work since the pandemic started and was grateful to receive further financial support from the government’s SEISS scheme. This time round you had to state that your income had been directly affected by the pandemic. I did agonize a bit over this, as it begged the question of how much money I would have been earning if things were normal. I honestly don’t know the answer to that, but it seems to me that the pandemic and government counter-measures have stopped the economy in its tracks, meaning there is less work around generally. Anyway, I applied and was paid without quibble.

The main good news over the last few weeks has concerned the vaccines. Two are now approved, with the Pfizer vaccine being distributed since before Christmas and the Oxford-AZ version coming on stream this week. One benefit of turning 65 is that I have presumably moved up the pecking order to receive it.

The government appears to be pinning all its hopes on vaccines bringing this pandemic to an end by spring/summer. I hope they are right, as the next couple of months in particular look pretty grim. At the time of writing my area has just moved to Tier 4, which effectively means lockdown. So I will have little/no opportunity to see friends or relatives, no more swimming, no more trips away, and the prospect of sporting ‘lockdown hair’ again. But I am still lucky compared to many, I know.

In my blog post Surviving the Covid Winter I mentioned some plans I had for getting through the winter months. In December I started several of these. In particular, I began a couple of DIY jobs I had been putting off. One of these was redecorating the en suite. Initially I planned just to repaint one wall where the paintwork was fading. But the new paint colour didn’t match the old one, so I am now planning to repaint the rest of the room as well. As is so often the case with DIY, what appeared a small job at first has grown into a much bigger one!

I have also taken my first tentative steps in the world of video gaming (my experience prior to this had been limited to Space Invaders/Asteroids and the games bundled with MS Windows such as Solitaire). With some trepidation I signed up with the games platform Steam and downloaded Coffee Talk to my Windows laptop. This was a game I had read about some time ago and liked the sound of. Here’s a typical scene from it…

Coffee Talk is actually more like an interactive movie or novel. You take the role of owner/barista at a late-night coffee shop in an alternative Seattle frequented by a mixture of human beings and mythological characters such as elves.

Mostly your customers chat with you and other customers about their lives and problems, while you prepare coffee and other drinks for them. This isn’t especially taxing, though I was quite pleased when one of the regulars, Freya, returned and asked for ‘the usual’ and I remembered what it was. It’s a pleasant enough way of spending a few hours, though I am thinking I might try something a little more ambitious next time 🙂

On the TV side, I finally finished the box-set of Deep Space Nine, which I very much enjoyed and recommend to any sci-fi fans among you. At the recommendation of my sister Annie (also a sci-fi aficionado) I have now purchased the box-set of Babylon Five. This is also set on a space station, though with quite a different vibe from DS9. With five (long) series, six full-length feature films, a spin-off series called Crusade, and various other extras, hopefully this will see me through to the end of the pandemic 😀

And for a change from sci-fi I also bought the box-set of Agatha Raisin, a tongue-in-cheek detective drama starring Ashley Jensen and set in the Cotswolds. I wasn’t sure about this at first, but after the first couple of episodes I thought it hit its stride, and I recommend it for a bit of amusing escapism with some gorgeous countryside settings. It’s only a shame that all three series are quite short.

Finally, as a Christmas present for myself I bought the DVD of Roger Waters’ Us + Them concert. This is an epic production, featuring a group of hugely talented musicians and some awesome visual effects (at one point a giant model of Battersea Power Station descends into the arena, accompanied – of course – by a flying pig).

Roger and his band play a selection of Pink Floyd classics alongside some of Roger’s solo compositions, all of which are excellent as well (The Last Refugee is particularly poignant). In the video below, though, they perform Time, one of my personal favourite Pink Floyd numbers. Check out Jess and Holly (aka Lucius) supplementing their backing vocal duties with some exuberant drumming!

So that’s it for now. I do hope you are staying safe and sane in these challenging times. Be kind to yourself and to others, and hopefully things will improve before too long. As ever, if you have any comments or questions, please do share them below.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2020, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a happy, Covid-free Christmas, and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

If you enjoyed this post, please link to it on your own blog or social media:

.

.