It won’t have escaped your notice that Christmas will soon be here.

It’s well known that older friends and relatives can be the hardest to choose gifts for. But don’t despair – as an older person myself (I’m 68) , I’m here with some ideas to make gift-buying for this age group a bit easier for you!

None of the suggestions below will break the bank. For the electronic ones, though, you might just want to check first how they might be received. Some older people are wary of trying new things, but I believe most will enjoy and get a lot of benefit from all these products. So a little bit of gentle encouragement if they express doubts might be in order!

Let’s start with a couple of the more techy ones then…

1.Kindle e-reader

As an older person myself I love my Kindle.

Of course, people of all ages use these devices, but for older people they have two particular advantages. One is you can adjust the brightness, font size, and so on. For those (like me) whose eyesight isn’t what it once was, the benefits of this can’t be overstated.

The other attraction is that on a Kindle you can literally carry hundreds of books around with you. If – like many of us older folk – your shelves are already groaning from the weight of books on them, a Kindle can provide a great alternative option.

In my view an Amazon Echo smart speaker with Alexa would make a great gift for any older person, even if they aren’t tech-savvy (though these devices do of course need wifi to work).

Once the speaker has been set up – which you can help with if required – they can control it using just their voice. As you may know, you can ask it to play your favourite music, set alarms and reminders, ask questions, and much more besides.

For an older person living alone especially, having an Echo can provide companionship as well as reassurance in the event of an emergency (you can ask Alexa to call any of your contacts for you, though currently you can’t get it to phone 999). And an Echo smart speaker is a present that will go on giving through Christmas and well beyond.

Again, various models are available from Amazon, including my personal favourite, the Echo Show. This has a display screen, so you can do video calls on it if you like. Prices range from £45 upwards, with generous discounts frequently on offer.

3. Afternoon Tea Voucher

Dare I say it, this might be especially popular among female friends and relatives, but plenty of men will enjoy it too. Or you could buy this as a joint gift, of course.

This is another very popular gift among older people. It’s an opportunity to enjoy an exhilarating flight in a hot air balloon with stunning views of the UK landscape.

Vouchers are available from Virgin Balloon Flights for prices between £169 and £209 for a one-hour flight, including a celebratory glass of Prosecco afterwards. Flights take place in the UK between March and October.

5. Christmas Hamper

Who doesn’t enjoy a hamper of festive food and drink at Christmas? And that applies especially to older people on a limited income, who may relish the opportunity to enjoy some little luxuries that would normally be beyond their budget, particularly in the current cost-of-living crisis.

You could put together a basket filled with quality chocolates, nuts, gourmet snacks, cakes, biscuits, and a bottle of fine wine or champagne. Alternatively you can buy a ready-made hamper from suppliers such as Prestige Hampers or Marks and Spencer. Prices range from £25 upwards (including delivery).

6. Magazine or Newspaper Subscription

Choose a magazine or newspaper subscription that aligns with their interests, e.g. gardening, travel, cooking, or current events. Another good option might be Radio Times, as many older people consume a lot of TV and radio.

This is another present that keeps on giving throughout the year. Just remember to purchase a gift subscription rather than a standard one, or your subscription will automatically renew.

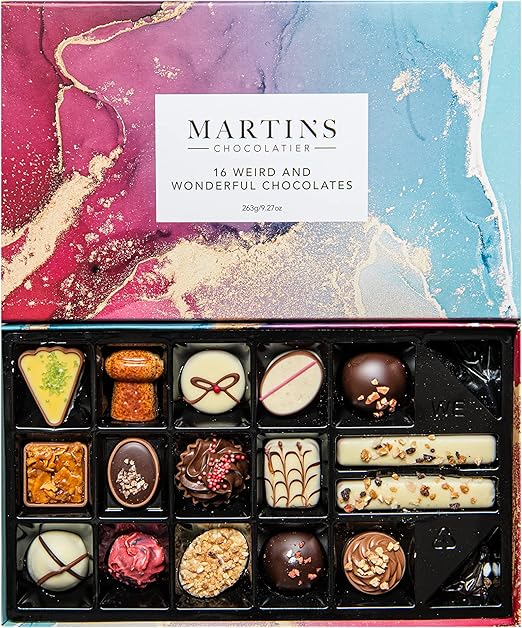

7. Artisan Chocolates

You can’t go too far wrong with chocolates. But except perhaps for your least favoured relatives, a tin of Quality Street isn’t going to cut it.

So why not push the boat out and buy them some luxury, hand-made, artisan chocolates? There are various local shops specialising in this, and as ever Amazon sell a good range. Here are some I bought my sister as a thank-you for putting me up for a few days recently. She tells me she and her husband enjoyed all the different flavours and quickly polished them off!

Prices for boxes of artisan chocolates range from £15 upwards. They are guaranteed to bring a bit of good cheer to anyone’s Christmas celebrations!

8. Digital Photo Frame

Load a digital photo frame with a collection of your friend or relative’s favourite pictures. This way, they can enjoy a rotating display of memories without the need for multiple printed photos. And compared with the latter option, it’s a great space-saver as well!

Most frames come with a remote control; they may also have extra features such as a built-in clock/calendar. Prices range from £30 upwards. You can view a selection on this Amazon web page.

9. Cosy Blanket or Throw

A soft and luxurious blanket or throw (such as the one pictured below from Amazon) is perfect for staying warm during the winter months. And of course it can help save on energy bills as well.

Prices range from £15 upwards (more for those with built-in electric heating). Look for one in their favorite colour or with a pattern that matches their decor.

10. Ergonomic Gardening Tools Set

For those with green fingers, consider a set of ergonomic gardening tools (like this one perhaps). These tools are designed to reduce the strain on joints and muscles, making gardening more comfortable and enjoyable. Prices range from about £15 upwards.

11. Subscription to a Streaming Service

Give the gift of entertainment with a subscription to a streaming service like Netflix or Amazon Prime Video. This will provide a wide range of films and TV shows for your friend or relative to enjoy at their leisure. This is another gift whose benefits will extend well beyond Christmas itself.

12. Comfortable Slippers

I’ll close with an ‘old-school’ gift, but nonetheless one that will be very much appreciated by many older people.

Opt for a pair of high-quality, comfortable slippers. Look for features such as memory-foam insoles and non-slip soles to ensure your friend or relative stays cosy and safe around the house.

You can expect to pay from £20 upwards for a decent pair of slippers. They are available from many high street stores including Marks and Spencer or – inevitably – from Amazon (see example below).

A personal recommendation is to avoid getting slippers with low (or no) backs, as these are easy for an older person to slip out of. Traditional high-backed slippers, such as the ones pictured above, are safer and better.

So there you have it. Twelve great gifts for older people – one for each day of Christmas – and not a sock among them!

Remember to take into account personal preferences and interests when choosing a gift, to make it truly special.

If you have any comments or questions about this article, as ever, please do post them below.

Note: This article is adapted from one originally written for my good friends at Mouthy Money.

Disclosure: This article includes affiliate links. If you click through and make a purchase, I may receive a small commission for introducing you. This will not affect the price you pay or the product you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I was recently offered the chance to review the Simba Orbit™ weighted blanket (see cover photo). This is a premium weighted blanket from the well-known Simba Sleep brand.

Weighted blankets are a growing trend right now. They purport to help reduce anxiety, promote relaxation and improve sleep. Naturally I was pleased to have the opportunity to test this out for myself.

The Simba Orbit™ blanket is available in various sizes and weights. I received the 15 lb (6.8 kg) single bed version. For reasons to be discussed, in my view this would also be perfectly suitable if (like me) you normally sleep on your own in a double bed.

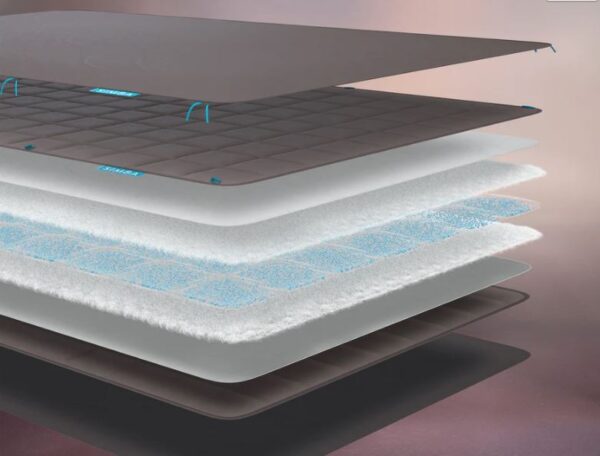

Even though I got the lightest version, I was still quite surprised how heavy it was. It comes with a machine-washable cotton cover and I got a decent workout just putting the blanket in! The cover and the blanket itself are a rather nondescript brown. It might be nice to have a choice of colours to suit your decor. That’s only a minor criticism, though.

The blanket is filled with tiny weighted-glass nano-beads. These are stitched evenly into small pockets (see picture below) to prevent clumping. I can confirm that they don’t appear to move around in the night, neither do you hear any noise from them. As they say on the Simba sales page, ‘Together they form a soothing layer that rests gently over your body, giving you a feeling of light, comforting pressure.’ The blanket and cover are also designed for maximum breathability, so the blanket feels warm in winter but cool in summer.

The theory behind the Simba Orbit™ weighted blanket (and weighted blankets generally) is Deep Pressure Therapy (DPT). This is an actual, scientific thing, with academic studies to back it up.

DPT is a calming process activated through a physical stimulus – like a hug, or the application of some sort of gentle pressure across the body. Some studies have suggested that this pressure works by helping your nervous system switch off its ‘fight or flight’ system (sympathetic) and move to its ‘rest and digest’ system (parasympathetic).

Simba say the Orbit™ weighted blanket is designed to replicate that feeling of soothing pressure. They suggest thinking of it as your ‘off switch’ – a switch that helps regulate your heartbeat, relax your muscles and set your mind at rest.

My own experience confirms this. Admittedly it took a night or two to get used to, but I did then notice I was sleeping longer and deeper and feeling more refreshed when I woke up. One thing that impressed me was how the blanket stays in place and doesn’t move around or slip off the bed once it’s in position. That is why I think the single version is also suitable for people who sleep alone in a double bed. Personally I found it worked best (and felt most comfortable) if I positioned it over the lower half of my body rather than up to my neck/chest. Your experience might be different, of course.

Clearly, weighted blankets won’t be right for everyone. In particular, as SImba themselves say, they aren’t suitable for children, the elderly or anyone suffering from breathing difficulties or circulatory issues (including diabetes). In cases of pregnancy and kidney issues, you are recommended to consult your doctor before use.

If you’re stressed and anxious and finding it hard to unwind, however, then based on my experience this weighted blanket is well worth a try. You can order direct from the SImba Orbit™ weighted blanket web page while stocks last. You can get free next day delivery if you order before 2 pm on the UK mainland, with interest-free finance options also available.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: As stated above, I received a free Simba Orbit™ weighted blanket in exchange for reviewing it here. This has not influenced my review in any way.

If you enjoyed this post, please link to it on your own blog or social media:

As speculation mounts ahead of Rachel Reeves’ upcoming budget, many UK retirees and those approaching retirement are wondering if now is the right time to take a tax-free lump sum from their pension. Already it appears growing numbers have been doing just that in anticipation of a possible tightening of the rules.

The rumoured changes in pension taxation could have significant implications, but should these potential shifts prompt immediate action? Let’s explore the factors you should consider.

What Is the Tax-Free Lump Sum?

In the UK, retirees can typically withdraw 25% of their pension pot as a tax-free lump sum once they reach the age of 55. This is an attractive option for many, offering access to a sizable portion of their savings without incurring tax. For some, it provides the flexibility to pay off debts, invest elsewhere, or simply enjoy a more comfortable lifestyle in retirement.

Rumoured Changes in the Budget

Rachel Reeves, the Chancellor, is reportedly considering reforms to pension tax relief, which could also extend to the tax-free lump sum. While no firm details have been announced, the possibility of reducing or capping the 25% tax-free allowance is circulating. This has led to concerns that those who wait may lose out on the full benefits they could currently access.

There’s also talk of broader reforms to pension rules, aimed at increasing revenue for public services and addressing the UK’s fiscal challenges. While these changes are still speculative, they are fuelling anxiety among pension holders who fear that future alterations could make withdrawing a tax-free lump sum less advantageous.

So Should You Act Now?

1. Certainty vs. Uncertainty

One of the main arguments for taking the lump sum now is to lock in the current 25% tax-free amount before any potential changes. Given that pension reforms often take time to be enacted and may not affect existing pension holders, acting sooner rather than later could provide peace of mind. However, if the government does decide to protect current retirees from any new rules, rushing to take the lump sum might be unnecessary.

2. Immediate Need for Funds

Another key factor is your immediate financial situation. If you have debts to clear, home improvements to make, or other significant expenses on the horizon, taking the tax-free lump sum now could offer a welcome cash injection. Conversely, if your pension pot is your primary source of retirement income, withdrawing a large sum may reduce your long-term financial security.

3. Future Investment Opportunities

Withdrawing your lump sum early could also open up other investment opportunities. If you have a clear plan for how you will use or invest the funds, you may benefit from accessing the money now. However, keep in mind that once withdrawn, the lump sum will no longer benefit from the tax advantages and potential growth offered within a pension.

Though you can of course reinvest the money in another tax-efficient vehicle, e.g. an ISA (annual limit £20,000) and/or premium bonds (maximum total £50,000).

4. Impact on Future Income

Remember that taking a lump sum now will reduce the size of your remaining pension pot, potentially lowering your future retirement income. If you rely heavily on your pension for day-to-day living, this could be a risky move. Make sure you understand how much income you’ll need later in life and whether taking the lump sum will still allow you to meet those needs.

5. Pension Lifetime Allowance

Another aspect to consider is the pension lifetime allowance (LTA), which capped the total amount you could invest across all your pensions without incurring an additional tax charge. While the LTA was abolished in the 2023 budget under Jeremy Hunt, there could be changes under Labour that might bring back a revised limit, especially if tax-relief reforms are on the table.

Seeking Professional Advice

If you’re unsure whether to take the lump sum, it’s essential to consult a financial advisor who can offer guidance based on your individual circumstances. Pension decisions are complex, and making the wrong move could have long-term financial implications.

Your advisor will be able to assess whether taking a lump sum now aligns with your retirement goals, or if it’s more prudent to wait and see what changes, if any, are introduced in future budgets.

Conclusion: Is Now the Time to Act?

The potential changes in Rachel Reeves’ budget have understandably raised concerns about pension taxation. While it’s tempting to act quickly to safeguard your tax-free lump sum, it’s important to weigh your immediate financial needs against the possible impact on your future retirement income.

Without firm details of what the budget may contain, it’s impossible to predict exactly how pension rules might change. For most, the best course of action will be to stay informed, assess your own financial situation, and seek professional advice before making any significant decisions.

After all, your pension is a key part of your long-term financial security, and decisions made in haste could have lasting consequences. Keep an eye on the upcoming budget announcements, and don’t hesitate to revisit your pension strategy once more concrete information is available.

As always, if you have any comments or questions about this post, please do leave them below. But bear in mind that I am not a qualified tax adviser and cannot give personal financial advice. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at the Warm Home Discount scheme. The 2024/25 version of this has just launched.

The WHD scheme provides people on low incomes and/or certain means-tested benefits with a discount of £150 on their electricity bill. This is a one-off payment that will be credited to your electricity account by March 2025. It won’t be paid to you in cash.

If you have a pre-payment electricity meter you can still get WHD. You may be given a voucher you can use to top up your payments. Your electricity supplier will tell you exactly how and when you will receive this.

You may be able to get the discount on your gas bill instead if your supplier provides you with both gas and electricity. You will need to ask your supplier about this.

To get the £150 discount, you need to have your name on the bill and either receive a qualifying benefit or (in Scotland) qualify under your supplier’s low-income criteria (see below).

If you live in England or Wales, you will qualify if you either:

An important thing to note is that only pensioners who receive the Guarantee element of Pension Credit will qualify automatically for the Warm Home Discount. These people are known as ‘Core Group 1’ in England and Wales and the ‘Core Group’ in Scotland. If you’re in this group you should receive a letter between October 2024 and early January 2025 telling you when and how the discount will be paid. If you don’t get a letter and think you are eligible for the core group, you should contact the Warm Home Discount helpline on 0800 030 9322.

You should also still qualify for WHD if you live in England or Wales and:

your energy supplier is part of the scheme (see below)

you get certain means-tested benefits or tax credits

your property has a high energy cost score (see below)

your name (or your partner’s) is on the bill

This is known as being in ‘Core Group 2’. The qualifying means-tested benefits are:

Housing Benefit

income-related Employment and Support Allowance (ESA)

income-based Jobseeker’s Allowance (JSA)

Income Support

the ‘Savings Credit’ part of Pension Credit

Universal Credit

You could also qualify if your household income falls below a certain threshold and you get either:

Again, you should receive a letter between October 2024 and early January 2025 telling you about the discount if you’re eligible. In most cases you are no longer required to apply for it.

Most eligible households will receive an automatic discount. Your letter will say if you need to call a helpline by 28 February 2025 to confirm your details.

If you’re eligible, your electricity supplier will apply the discount to your bill by 31 March 2025.

If you live in Scotland and don’t get the Guarantee Element of Pension Credit, you may qualify to receive WHD if:

your energy supplier is part of the scheme

you (or your partner) get certain means-tested benefits or tax credits

your name (or your partner’s) is on the bill

Your supplier may have additional criteria so you will need to check with them if you’re eligible. This is known as being in the ‘broader group’. To get the discount you’ll need to stay with your supplier until it’s paid.

As mentioned above, if you are not in Core Group 1 in England and Wales, to qualify for WHD your property must also have a high energy cost score.

The Government models the energy cost score of your property based on official data about its characteristics. These include the property type, age, and floor area. The Government uses data from the Valuation Office Agency (VOA) to model your property’s energy cost score. They may also use your property’s Energy Performance Certificate (EPC), assuming it has one. Other sources and statistical methods may also be used for the small proportion of households where data is not otherwise available.

Each year the Government will decide what constitutes a high energy cost score. It’s not straightforward for an individual to determine whether they will be eligible under this criterion. If you fill in the online eligibility checker, however, it should indicate whether or not you are likely to qualify (when I tried this for some elderly friends, it said they would ‘probably’ qualify and should wait to receive a letter).

Which Suppliers Offer Warm Home Discount?

All the large energy suppliers offer WHD and some of the lesser-known ones as well. Below is a list of suppliers copied from the government webpage devoted to Warm Home Discount. You can check your eligibility on the supplier’s website or phone them up and ask.

100Green (formerly Green Energy UK or GEUK)

Affect Energy – see Octopus Energy

Boost

British Gas

Bulb Energy – see Octopus Energy

Co-op Energy – see Octopus Energy

E – also known as E (Gas and Electricity)

Ecotricity

E.ON Next

EDF

Fuse Energy

Good Energy

Home Energy

London Power

Octopus Energy

Outfox the Market

OVO

Rebel Energy

Sainsbury’s Energy

Scottish Gas – see British Gas

ScottishPower

Shell Energy Retail

So Energy

Tomato Energy

TruEnergy

Utilita

Utility Warehouse

The government say that if the electricity supplier you were with stops trading, you may still be eligible for the Warm Home Discount. Ofgem will appoint your new supplier for you, and you should check with the new supplier to find out if you’re eligible for the discount.

If you are in the market for a new energy supplier, you may like to know that if you switch to EDF Energy you can get £50 credited to your account by clicking on my EDF referral link. I am an EDF customer myself and will also get £50 credited to my account if you do this and switch to EDF. This will not affect in any way the service you receive or the rate you are charged.

Other Winter Fuel Benefits

Two other benefits are also available to qualifying individuals.

1. People born before 23rd September 1958 and in receipt of pension credit or certain other welfare benefits are eligible for a Winter Fuel Payment. This is worth £200 or £300 per person and will be paid in November or December 2024. More information including eligibility details can be found on the official government website. As you may know, previously all state pensioners were entitled to WFP, but the new Labour government has chosen to restrict it to the poorest pensioners only.

2. In the event of a prolonged cold spell, most people receiving Pension Credit will receive Cold Weather Payments. People on Income Support, Jobseeker’s Allowance, Employment and Support Allowance (ESA) and Universal Credit may also qualify depending on their circumstances, e.g. if they have a disability and/or a disabled child living with them. You will get this payment if the average temperature in your area is recorded as, or forecast to be, zero degrees Celsius or below for seven consecutive days. You get £25 for each seven-day period of very cold weather between 1 November and 31 March. Note that people in Scotland don’t get Cold Weather Payments but might get an annual £50 Winter Heating Payment instead. This is paid regardless of weather conditions in your area.

As always, if you have any comments or questions about this post, please do leave them below.

This is the 2024 update of an annual post.

If you enjoyed this post, please link to it on your own blog or social media:

Recently my energy supplier, EDF Energy, has been sending me invitations to sign up for what it calls its ‘Sunday Saver’ challenge.

The way this works is that you sign up to shift some of your electricity usage on weekdays away from peak hours (4pm-7pm). When you hit your target (which is set individually for each user by EDF), you earn free electricity the following Sunday.

EDF say, ‘The more you shift, the more you earn – reduce your weekly peak usage by 40% and you could earn up to 16 hours of free electricity per week.’

The challenge is due to take place monthly, starting on the first Monday of each month.

At first glance you might think this is a good offer. But as I have looked into it more, my doubts have grown. Here are my main reservations…

To benefit from this scheme you have to cut your daily energy usage every weekday between 4pm and 7pm. That’s quite a long period (three hours), and coincides with when I would normally be cooking my evening meal. To have any realistic chance of cutting my energy use during this time, I would have to eat either ridiculously early or significantly later than normal. For various reasons, including my health, I prefer to eat between 6 and 7 pm and no later. So that in itself is a big ask and would impact drastically on my normal routine.

Free electricity on Sunday sounds great, but the devil is in the detail. EDF say that you will get ‘up to 16 hours’ of free electricity if you meet their targets, but are very vague about what this means in practice. Specifically, they don’t explain how your energy-saving targets are calculated, how any reduction in usage translates to free hours, or when on Sunday you will be able to use the free electricity awarded.

In addition, they say there are ‘fair usage’ limits to how much free electricity you can have. Again, they are vague about what this means in practice. The obvious way to use your free electricity would be to charge your EV, and I strongly suspect limits would be placed on this. As for me, I don’t have an EV and don’t want one, so my options for benefiting from the free electricity would be limited. I could shift use of appliances like my washing machine to Sunday but doubt if I could save more than a few kw/h this way (obviously the exact number would depend on how many free hours I was allocated, which is anyone’s guess). That means my free electricity would likely benefit me by no more than a pound or two.

Lastly, as a solar panel owner I already get some free electricity anyway. My panels obviously generate less in the winter, but during daylight hours they still produce something. That means any benefit from free electricity on Sundays will be reduced, especially if (as is likely) the free hours are in the day rather than at night.

Overall, then, I am not much enamoured of EDF’s Sunday Saver challenges and won’t be signing up. Ultimately, I am not prepared to make major changes to my day-to-day schedule in pursuit of what will likely be (in my case anyway) minuscule rewards.

Obviously some will see this differently and I wish them well. And it’s good that EDF (and other companies) are exploring ways to help customers reduce their bills. I do just think this particular one – for me anyway – is a non-starter.

I would be interested to hear any comments from people doing this challenge (or similar ones from other energy companies) as to whether they find it worthwhile, and whether the benefits really do justify the changes you are required to make.

I do still recommend EDF Energy based on my personal experiences with them. And as I’ve said before on PAS, I can offer anyone switching to EDF £50 off their bills if they use my refer-a-friend link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 when applying. I will also get £50 off my bill if you do this, which is duly appreciated 🙂

UPDATE 22 OCTOBER 2024 – I am indebted to the readers (especially Harry!) who have taken the time to comment on this article and address some of the points raised in my original post. Based on this I have changed my views somewhat and am considering registering for the scheme when it reopens in November. If you’re still wondering whether to take the plunge, please do take the time to read the comments as (like me) they may influence your decision. I will publish an update in due course if I proceed with it next month.

UPDATE 28 NOVEMBER 2024 – Thanks again to everyone who commented on this post. Sorry I couldn’t reply to everyone individually. You may like to know that I just added a new post about why I changed my mind and registered for the EDF ‘Sunday Saver’ Challenge and how I got on in my first month. Please see https://www.poundsandsense.com/heres-why-i-changed-my-mind-about-edf-energys-sunday-saver-challenge/

If you enjoyed this post, please link to it on your own blog or social media:

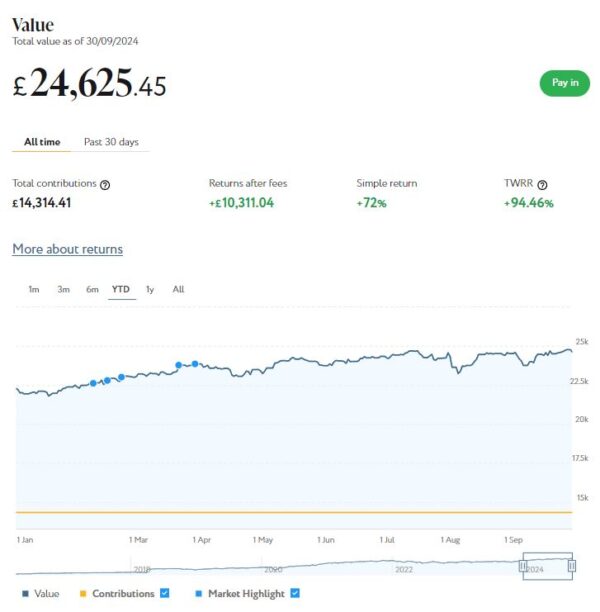

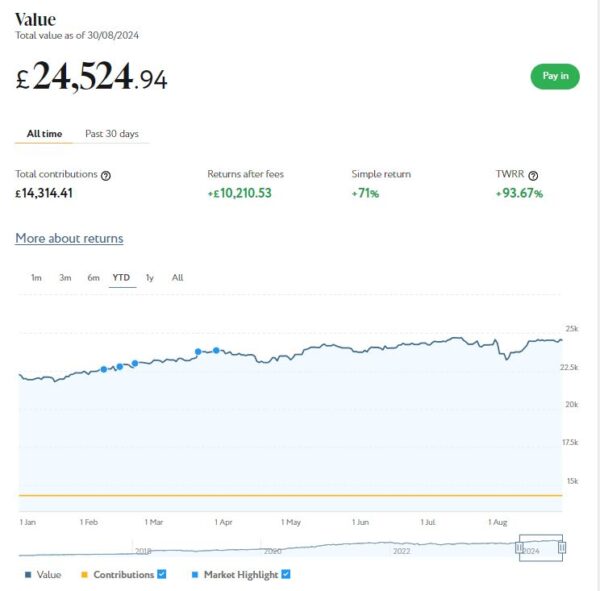

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,625. Last month it stood at £24,525, so that is an increase of £100.

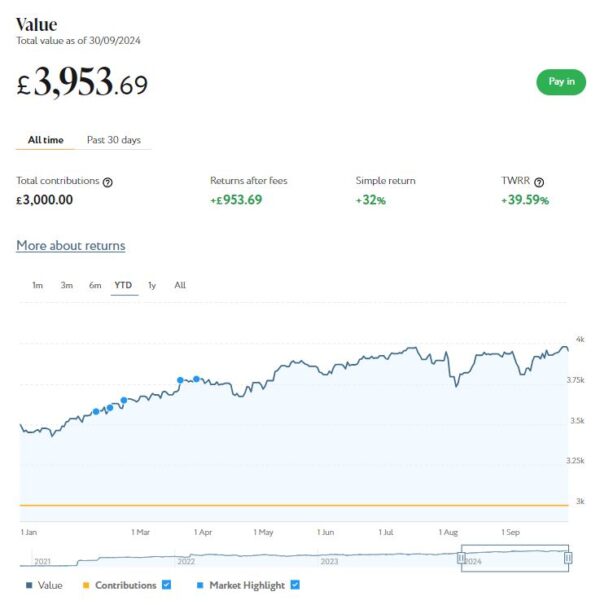

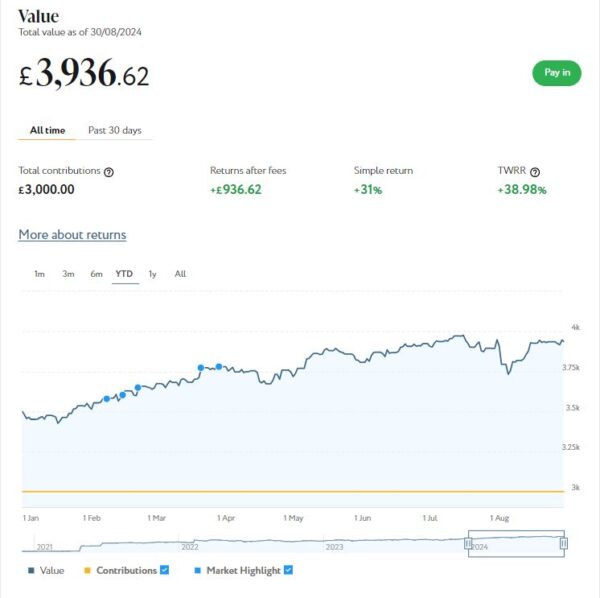

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,954 (rounded up) compared with £3,937 a month ago, a rise of £17. Here is a screen capture showing performance over the year to date.

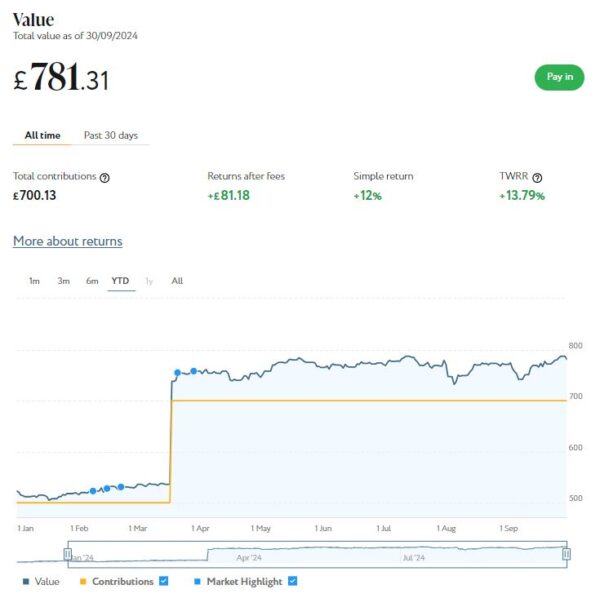

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £781 compared with £772 last month, a small rise of £9.

As you can see, September was another decent though unspectacular month for my Nutmeg investments. Their overall value has risen by £126 or 0.43% since the start of September. They are also up by £3,045 or 11.57% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024 and you have a full £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £208.97 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 11 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 17 are showing losses. My portfolio of 33 properties is currently showing a net decrease in value of £42.75, meaning that overall (rental income minus capital value decrease) I am up by £166.22. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

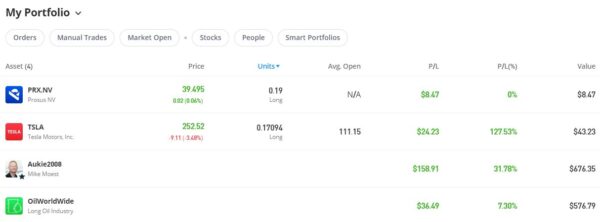

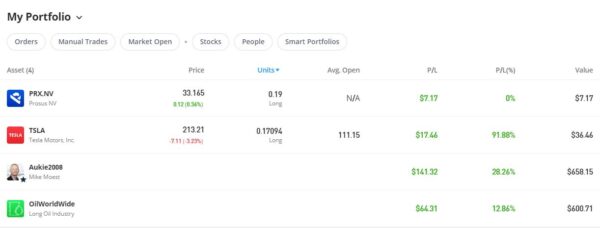

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

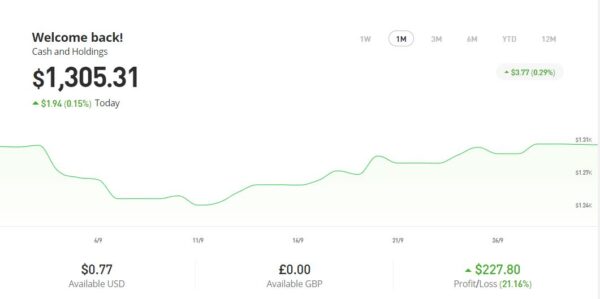

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,305.31 an overall increase of $283.05 or 27.69%.

As you can see, my Oil WorldWide investment is showing 7.30% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing much better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

As a matter of interest, since I wrote the above war has effectively broken out in the Middle East. This has led to fears that oil supplies from the region will be compromised and the price of oil will rise. As a consequence of this (I assume) the value of my Oil Worldwide investment has gone up. I say this not to gloat over the tragedy that is unfolding in the area, but to highlight the fact that a diversified portfolio can often help to hedge against economic downturns resulting from world events.

You might also notice that I have a small holding in Prosus NV, a Dutch internet group. To be honest I don’t understand how I acquired this, but it may be connected to my copy trading investment with MIke Moest (who is Dutch). In any event, I am happy to have it in my portfolio as well!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in September on the excellent Mouthy Money website. The first is Are Electric Boilers Better Than Heat Pumps?. As you doubtless know, the government are pushing heat pumps hard as a means of achieving their Net Zero goals. They are definitely not a one-size-fits-all solution, though. In this article I highlighted an alternative that may be more suitable for some, electric boilers. These are cheaper, smaller and quieter than heat pumps (though their running costs may be higher). You can read all about the pros and cons of heat pumps versus electric boilers in the article.

Also in September I revealed How to Get Free Stuff Online. In this article, I explained how you can get your hands on a wide range of freebies online, from samples and giveaways to promotional offers and rewards programmes – all without having to spend a single penny!

Finally, in September I discussed How to Save Money With Cashback Sites. If you ever buy anything online, you can almost certainly save by signing up with these sites. In this article I revealed how they work and set out some hints and tops for making the most of them.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in September, I particularly enjoyed Secondhand September: Good for Your Purse and the Planet by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published (or republished) several posts on Pounds and Sense in September. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In Can You Still Make Money From Matched Betting? I discussed this tax-free money-making opportunity. As I said in the article, this is something I did for several years and earned about £3,000 from. I am not doing it nearly as much these days, for reasons explained in the article. But if you’ve never done it before, I do still highly recommend it as a way of making some quick tax-free cash. The article explains what matched betting is and how to get started.

The price of stamps is rising again on Monday 7 October 2024. That is the second price rise this year, after they also went up in April. So in How to Beat the Postage Stamp Price Rise, I revealed just how much (some) prices are rising and suggested ways to mitigate this.

In case you didn’t know, October is Free Wills Month. So in Get Your Will Written Free of Charge in October, I discussed how you can use this no-strings scheme to get your will written free at a range of participating solicitors across the UK. There are only limited slots available, so I recommend moving quickly if you want to take advantage of this opportunity.

Also in September I published How to Save Money on Your Heating Bills This Winter. As you doubtless know, gas and electricity bills have gone up considerably in the last year or two. And many older people will no longer get Winter Fuel Payments, as the new Labour government have opted to restrict this to just the very poorest pensioners (those in receipt of Pension Credit). So in this article I set out a range of ways you may be able to save money on your heating and energy bills. Following these tips could save you hundreds of pounds in the months and years ahead.

Finally, I published Amazon Big Deals Day is Almost Here. This annual event extends over two days, Tuesday 8th and Wednesday 9th October 2024. It is is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products from leading brands including Philips, Logitech, Oral-B, Braun, Tefal, Ghd, Swarovski, Bosch, Shark, and so on.

Next, some odds and ends. First up, Trading 212 recently reopened their free share offer, so I have updated my post Get a Free Share Worth Up to £100 With Trading 212. This explains how, if you haven’t done so already, you can get a free share when you open a new Invest or Stocks ISA with Trading 212. Note that opening a Cash ISA with T212 alone will not qualify you for a free share, but of course you can do both. My advice is to start by opening a Stocks ISA or (non-ISA) Invest account to qualify for your free share and apply (if you wish) for the Cash ISA after that. This new free share offer closes on 6 November 2024.

A few months ago I invested just over £1,000 in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing. You can pay by 12 monthly instalments rather than a single lump sum if you like. If you’re interested in learning more, you can visit the Ripple website via my referral link. If you decide to invest, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you wish.

Speaking of energy, a quick reminder that if you switch to EDF Energy via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight (again) the decision by the new government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you get the full new state pension, even with no other source of income, you likely won’t qualify. I do therefore recommend writing to your MP and asking for this Draconian decision to be reversed. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK. The former has over 100,000 signatures now and the latter over half a million.

That’s all for now. If you have any comments or queries about this update, as ever, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In case you’ve not heard, Amazon Prime Big Deals Day is almost with us. It extends over two days, Tuesday 8th and Wednesday 9th October 2024.

This is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products from leading brands including Philips, Logitech, Oral-B, Braun, Tefal, Ghd, Swarovski, Bosch, Shark, and so on.

Some of the best deals will be reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts of up to 60% will be on offer for these products. If you’re thinking of buying any of them, Amazon Prime Big Deals Day is definitely the day – or two days – to do it.

There are also some great ‘early deals’ available now. For example, at the time of writing you can buy an Amazon eero mesh Wi-Fi Router 5 system (2 pack), offering up to 280 square metres coverage, for just £54.99. That’s a 57% discount on the normal £129.99 asking price (offer closes 10th October).

I have been a member of Amazon Prime for almost ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a host of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next few days, so you can benefit from the Prime Big Deals Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Big Deals Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Big Deals Day offers by clicking here.

As always, if you have any comments or questions about Amazon Prime or Prime Big Deals Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

For older people in particular, heating bills can be among their biggest expenses. And it’s especially important for older people to keep warm, as getting chilled can lower your body’s resistance to infection and – in the worst cases – lead to hypothermia.

In addition, as you doubtless know, gas and electricity bills have gone up considerably in the last year or two. And many older people will no longer get Winter Fuel Payments, as the new government have opted to restrict this to just the very poorest pensioners (those in receipt of Pension Credit).

So today I thought I’d set out some ways you may be able to save money on your heating and energy bills. Following these tips could save you hundreds of pounds in the months and years ahead.

Switch Energy Supplier

It’s important to check regularly whether you could save money by switching to a different supplier and/or tariff. The quick and easy way of doing this is via a price comparison website. There are a number of these available, including GoCompare and USwitch.

Just visit the comparison site and enter a few details, including your current supplier and tariff and how much you spend on gas and electricity in the course of a year (it doesn’t have to be exact). The site will then display the best deals currently open to you and how much you might be able to save by switching to them. In most cases you can also start the switching process by clicking on the relevant link. Before you do, though, it’s worth checking on cashback sites like Quidco and Top Cashback, as some energy companies pay cashback via these sites to people switching their supply to them.

If you are one of the 1.1 million households who use oil for heating, you can save money by shopping around for suppliers too. Check out the oil price comparison service BoilerJuice. Type in your postcode and how many litres of heating oil you’re looking to buy, and BoilerJuice will show you quotes from suppliers covering your area.

Switching energy suppliers is generally quick and easy, and can save you hundreds of pounds a year at a stroke. In these challenging times, it should be high on your list of potential money-saving strategies this winter.

Special Offer! If you switch to EDF Energy via my link, you can get a FREE £50 credited to your energy account. Terms and conditions apply. For more info, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 [referral link].

Get Financial Help

If you’re in certain priority groups, you may be able to get cash payments to help offset your energy bills.

Winter Fuel Payment is a one-off annual payment of £200 to £300 which was previously made to everyone over state pension age. Unfortunately, as mentioned above, the new government have decided to limit this benefit to the very poorest pensioners who are in receipt of pension credit (or certain other welfare benefits). To qualify this winter, you must have been born on or before 23 September 1958 and been in receipt of a qualifying benefit for at least one day during the week of 16 to 22 September 2024 (the ‘qualifying week’). If that applies to you, this money should be paid automatically, but you can phone the Winter Fuel Payment Centre on 0800 731 0160 if you haven’t received the payment before and need to claim.

If you think you might be eligible for Pension Credit but are not currently receiving it, it’s now more important than ever to apply. Not only will it qualify you to receive Winter Fuel Payments, it can act as a gateway to a range of other discounts and benefits as well. See my blog post about applying for Pension Credit for more information.

In addition, those on certain welfare benefits (including Pension Credit, Income Support and Universal Credit) may be eligible for Cold Weather Payments. This is £25 for any period of seven consecutive days when temperatures fall below zero. More information can be found on this page of the government website.

You may also be eligible for £150 off your energy bill under the Warm Home Discount Scheme. This is run by some (not all) of the energy companies. If you get the Guaranteed Credit element of Pension Credit you will qualify automatically. But if you’re on a low income and meet the energy supplier’s other criteria, you may also qualify. Contact your supplier directly for more information. The large energy companies such as EDF and British Gas all operate this scheme, but some of the smaller ones don’t. The Warm Home DIscount scheme for 2024/25 opens in October 2024. More information can be found on the official website.

Finally, if you’re on a very low income, you may qualify for help from the Household Support Fund: This is money provided to councils by the government to assist pensioners and others on very low incomes. You will need to contact your local council to find out if you’re eligible.

More Top Tips

Here are some more ways you may be able to save money on your heating and energy bills.

Have your boiler serviced regularly, to ensure it is operating at peak efficiency.

If you have an old boiler that keeps breaking down, the time may have come to replace it. The Energy Saving Trust say that you could save up to up to 40 percent on your gas bill by installing a new ‘A’ rated condensing boiler with a programmer, room thermostat and thermostatic radiator controls.

Upgrading your insulation can also cut bills by reducing the amount of heat going to waste. Depending on your circumstances, you may be able to get a free boiler and/or insulation under the government’s Energy Company Obligation (ECO) scheme. You can apply for this via your energy company. Even if you’re not on a low income, you may be able to get a discount on home insulation, so it’s worth checking to see what’s available.

If your radiators aren’t heating up properly at the top, you may need to bleed them to release air in the pipes. Depending on the radiator, you may need a special key to do this or a flat-bladed screwdriver.

Turn down your thermostat by one degree - this can reduce your heating bill by up to 10%.

Ensure you don’t put furniture right in front of radiators, as this can block heat from entering the room.

Replace old light-bulbs with new energy-saving bulbs. The latest LED bulbs are just as bright as old incandescent bulbs and use a tenth of the energy. They last longer too.

Exclude draughts with heavy curtains and draught excluders by doors.

Turn off heaters in rooms you aren’t using and close the doors to keep heat in.

Place reflective foil behind radiators on exterior walls to bounce heat back into the room.

Don’t leave electrical appliances on standby.

Wash clothes at 30 degrees and try to avoid using tumble driers. Hang washing outside whenever possible or place it over an airer.

Consider investing in a smart thermostat system such as Nest or Hive. This will give you precise, automated control over your heating system, allowing you to use just as much energy as you need and no more. See this Money Supermarket article for more information.

If your funds are limited and you have or develop a disability you may be able to get a Disabled Facilities Grant (DFG) from your local authority to pay for adaptations such as stairlifts.

By taking these steps you should be able to cut your heating and energy bills significantly this winter.

If you have any comments or questions about this post, as always, please do leave them below.

This is a fully updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, Age UK, The Stroke Association, PDSA, and many others. Free Wills Month happens twice a year, in March and October.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I have talked about the importance of creating a will and why you should get it done by a properly qualified solicitor previously on PAS. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website during October and fill in your details. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s best to apply as soon as possible to avoid disappointment.

Free Wills Month October 2024 starts officially on Tuesday 1st October 2024 but you can sign up on the FWM website to be notified when when the campaign starts in your area.

If you have any comments or questions about this subject, as ever, please do post them below.

Note: This is a revised and updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,525 (rounded up). Last month it stood at £24,237, so that is an increase of £288.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,937 compared with £3,895 a month ago, a rise of £42. Here is a screen capture showing performance over the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £772 compared with £769 last month, a small rise of £3.

As you can see from the charts, August was generally a decent month for my Nutmeg investments, despite a hiccup early in the month. Their overall value has risen by £333 or 1.16% since the start of August. They are also up by £2,919 or 11.08% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024 and you have a full £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £200.41 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 6 are breaking even, and the remaining 17 are showing losses. My portfolio of 33 properties is currently showing a net decrease in value of £43.69, meaning that overall (rental income minus capital value decrease) I am up by £156.72. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.27 an overall increase of $281.01 or 27.51%.

As you can see, my Oil WorldWide investment is showing 12.85% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

You might also notice that I have a small holding in Prosus NV, a Dutch internet group. To be honest I don’t understand how I acquired this, but it may be connected to my copy trading investment with MIke Moest (who is Dutch). In any event, I am happy to have it in my portfolio as well!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in August on the excellent Mouthy Money website. The first is Win Fame and (Maybe) Fortune as a TV Quiz Show Contestant. This can be an exciting and occasionally lucrative pastime. I revealed how to find opportunities and apply for them. I also explained how the auditioning process works, and offered some tips on how to boost your chances of success.

Also in August I revealed my Ten Top Tips for Working From Home. This is something I’ve done for over 30 years now, so in this article I set out my top ten tips based on my experience. If you have recently started working from home, or expect to do so in future, you may find this article helpful.

Finally, I wrote an article titled How Understanding Cognitive Dissonance Theory Can Help Us Manage Our Finances Better. This article drew on my experiences of studying psychology back in the 1970s. Developed by psychologist Leon Festinger in 1957, cognitive dissonance theory explores the discomfort we experience when we simultaneously hold conflicting beliefs or attitudes. By understanding this, we can gain insights into our financial behaviour, helping us make more informed decisions and achieve better financial results.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in August, I particularly enjoyed How to Save Money on Your Home Removal by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in August. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In these challenging times, we all need to ensure our savings stretch as far as possible. So in How to Maximize Your Savings Interest l set out a range of tax-free allowances you can use to help do this. They include the Personal Savings Allowance (PSA), Starting Rate for Savings, Individual Savings Accounts (ISAs), and various others.

I also published How to Win Cash and Prizes in Online Competitions. This can be another tax-free way to boost your finances! In this post I revealed how to find online competitions to enter, why you should set up dedicated ‘comping’ accounts, how to identify potential scams, and more. Good luck if you decide to try this 🤞

As we all know Labour achieved a landslide victory in the general election, and it appears that austerity measures are on the way now. So in How to Reduce the Impact of Tax Rises in Rachel Reeves’ First Budget, I set out some recommended steps to try to protect your finances in the months (and years) ahead. The Chancellor’s first budget is scheduled for 30th October 2024, with tax rises and cuts to public services widely anticipated.

Finally, in August I published What Alternatives Are There to Heat Pumps? The government are currently pushing heat pumps hard in their frantic quest to achieve Net Zero. For a range of reasons, however, they are not suitable for every property. And even if your home might theoretically be suitable, there are good reasons you might not want one (discussed a while ago in this Mouthy Money article). So in this post I set out some possible alternatives you might like to consider instead.

Next, a few odds and ends. I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you decide to invest, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Speaking of energy, a quick reminder that if you switch to EDF via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight the decision by the new Labour government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you have any source of income apart from the state pension, even a tiny one, the chances are you won’t be eligible. I do therefore recommend writing to your MP and asking for this Draconian decision to be reversed. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK. The latter is up to almost half a million signatures now.

That’s all for now. If you have any comments or queries about this update, as ever, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

.

.