As speculation mounts ahead of Rachel Reeves’ upcoming budget, many UK retirees and those approaching retirement are wondering if now is the right time to take a tax-free lump sum from their pension. Already it appears growing numbers have been doing just that in anticipation of a possible tightening of the rules.

The rumoured changes in pension taxation could have significant implications, but should these potential shifts prompt immediate action? Let’s explore the factors you should consider.

What Is the Tax-Free Lump Sum?

In the UK, retirees can typically withdraw 25% of their pension pot as a tax-free lump sum once they reach the age of 55. This is an attractive option for many, offering access to a sizable portion of their savings without incurring tax. For some, it provides the flexibility to pay off debts, invest elsewhere, or simply enjoy a more comfortable lifestyle in retirement.

Rumoured Changes in the Budget

Rachel Reeves, the Chancellor, is reportedly considering reforms to pension tax relief, which could also extend to the tax-free lump sum. While no firm details have been announced, the possibility of reducing or capping the 25% tax-free allowance is circulating. This has led to concerns that those who wait may lose out on the full benefits they could currently access.

There’s also talk of broader reforms to pension rules, aimed at increasing revenue for public services and addressing the UK’s fiscal challenges. While these changes are still speculative, they are fuelling anxiety among pension holders who fear that future alterations could make withdrawing a tax-free lump sum less advantageous.

So Should You Act Now?

1. Certainty vs. Uncertainty

One of the main arguments for taking the lump sum now is to lock in the current 25% tax-free amount before any potential changes. Given that pension reforms often take time to be enacted and may not affect existing pension holders, acting sooner rather than later could provide peace of mind. However, if the government does decide to protect current retirees from any new rules, rushing to take the lump sum might be unnecessary.

2. Immediate Need for Funds

Another key factor is your immediate financial situation. If you have debts to clear, home improvements to make, or other significant expenses on the horizon, taking the tax-free lump sum now could offer a welcome cash injection. Conversely, if your pension pot is your primary source of retirement income, withdrawing a large sum may reduce your long-term financial security.

3. Future Investment Opportunities

Withdrawing your lump sum early could also open up other investment opportunities. If you have a clear plan for how you will use or invest the funds, you may benefit from accessing the money now. However, keep in mind that once withdrawn, the lump sum will no longer benefit from the tax advantages and potential growth offered within a pension.

Though you can of course reinvest the money in another tax-efficient vehicle, e.g. an ISA (annual limit £20,000) and/or premium bonds (maximum total £50,000).

4. Impact on Future Income

Remember that taking a lump sum now will reduce the size of your remaining pension pot, potentially lowering your future retirement income. If you rely heavily on your pension for day-to-day living, this could be a risky move. Make sure you understand how much income you’ll need later in life and whether taking the lump sum will still allow you to meet those needs.

5. Pension Lifetime Allowance

Another aspect to consider is the pension lifetime allowance (LTA), which capped the total amount you could invest across all your pensions without incurring an additional tax charge. While the LTA was abolished in the 2023 budget under Jeremy Hunt, there could be changes under Labour that might bring back a revised limit, especially if tax-relief reforms are on the table.

Seeking Professional Advice

If you’re unsure whether to take the lump sum, it’s essential to consult a financial advisor who can offer guidance based on your individual circumstances. Pension decisions are complex, and making the wrong move could have long-term financial implications.

Your advisor will be able to assess whether taking a lump sum now aligns with your retirement goals, or if it’s more prudent to wait and see what changes, if any, are introduced in future budgets.

Conclusion: Is Now the Time to Act?

The potential changes in Rachel Reeves’ budget have understandably raised concerns about pension taxation. While it’s tempting to act quickly to safeguard your tax-free lump sum, it’s important to weigh your immediate financial needs against the possible impact on your future retirement income.

Without firm details of what the budget may contain, it’s impossible to predict exactly how pension rules might change. For most, the best course of action will be to stay informed, assess your own financial situation, and seek professional advice before making any significant decisions.

After all, your pension is a key part of your long-term financial security, and decisions made in haste could have lasting consequences. Keep an eye on the upcoming budget announcements, and don’t hesitate to revisit your pension strategy once more concrete information is available.

As always, if you have any comments or questions about this post, please do leave them below. But bear in mind that I am not a qualified tax adviser and cannot give personal financial advice. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at the Warm Home Discount scheme. The 2024/25 version of this has just launched.

The WHD scheme provides people on low incomes and/or certain means-tested benefits with a discount of £150 on their electricity bill. This is a one-off payment that will be credited to your electricity account by March 2025. It won’t be paid to you in cash.

If you have a pre-payment electricity meter you can still get WHD. You may be given a voucher you can use to top up your payments. Your electricity supplier will tell you exactly how and when you will receive this.

You may be able to get the discount on your gas bill instead if your supplier provides you with both gas and electricity. You will need to ask your supplier about this.

To get the £150 discount, you need to have your name on the bill and either receive a qualifying benefit or (in Scotland) qualify under your supplier’s low-income criteria (see below).

If you live in England or Wales, you will qualify if you either:

An important thing to note is that only pensioners who receive the Guarantee element of Pension Credit will qualify automatically for the Warm Home Discount. These people are known as ‘Core Group 1’ in England and Wales and the ‘Core Group’ in Scotland. If you’re in this group you should receive a letter between October 2024 and early January 2025 telling you when and how the discount will be paid. If you don’t get a letter and think you are eligible for the core group, you should contact the Warm Home Discount helpline on 0800 030 9322.

You should also still qualify for WHD if you live in England or Wales and:

your energy supplier is part of the scheme (see below)

you get certain means-tested benefits or tax credits

your property has a high energy cost score (see below)

your name (or your partner’s) is on the bill

This is known as being in ‘Core Group 2’. The qualifying means-tested benefits are:

Housing Benefit

income-related Employment and Support Allowance (ESA)

income-based Jobseeker’s Allowance (JSA)

Income Support

the ‘Savings Credit’ part of Pension Credit

Universal Credit

You could also qualify if your household income falls below a certain threshold and you get either:

Again, you should receive a letter between October 2024 and early January 2025 telling you about the discount if you’re eligible. In most cases you are no longer required to apply for it.

Most eligible households will receive an automatic discount. Your letter will say if you need to call a helpline by 28 February 2025 to confirm your details.

If you’re eligible, your electricity supplier will apply the discount to your bill by 31 March 2025.

If you live in Scotland and don’t get the Guarantee Element of Pension Credit, you may qualify to receive WHD if:

your energy supplier is part of the scheme

you (or your partner) get certain means-tested benefits or tax credits

your name (or your partner’s) is on the bill

Your supplier may have additional criteria so you will need to check with them if you’re eligible. This is known as being in the ‘broader group’. To get the discount you’ll need to stay with your supplier until it’s paid.

As mentioned above, if you are not in Core Group 1 in England and Wales, to qualify for WHD your property must also have a high energy cost score.

The Government models the energy cost score of your property based on official data about its characteristics. These include the property type, age, and floor area. The Government uses data from the Valuation Office Agency (VOA) to model your property’s energy cost score. They may also use your property’s Energy Performance Certificate (EPC), assuming it has one. Other sources and statistical methods may also be used for the small proportion of households where data is not otherwise available.

Each year the Government will decide what constitutes a high energy cost score. It’s not straightforward for an individual to determine whether they will be eligible under this criterion. If you fill in the online eligibility checker, however, it should indicate whether or not you are likely to qualify (when I tried this for some elderly friends, it said they would ‘probably’ qualify and should wait to receive a letter).

Which Suppliers Offer Warm Home Discount?

All the large energy suppliers offer WHD and some of the lesser-known ones as well. Below is a list of suppliers copied from the government webpage devoted to Warm Home Discount. You can check your eligibility on the supplier’s website or phone them up and ask.

100Green (formerly Green Energy UK or GEUK)

Affect Energy – see Octopus Energy

Boost

British Gas

Bulb Energy – see Octopus Energy

Co-op Energy – see Octopus Energy

E – also known as E (Gas and Electricity)

Ecotricity

E.ON Next

EDF

Fuse Energy

Good Energy

Home Energy

London Power

Octopus Energy

Outfox the Market

OVO

Rebel Energy

Sainsbury’s Energy

Scottish Gas – see British Gas

ScottishPower

Shell Energy Retail

So Energy

Tomato Energy

TruEnergy

Utilita

Utility Warehouse

The government say that if the electricity supplier you were with stops trading, you may still be eligible for the Warm Home Discount. Ofgem will appoint your new supplier for you, and you should check with the new supplier to find out if you’re eligible for the discount.

If you are in the market for a new energy supplier, you may like to know that if you switch to EDF Energy you can get £50 credited to your account by clicking on my EDF referral link. I am an EDF customer myself and will also get £50 credited to my account if you do this and switch to EDF. This will not affect in any way the service you receive or the rate you are charged.

Other Winter Fuel Benefits

Two other benefits are also available to qualifying individuals.

1. People born before 23rd September 1958 and in receipt of pension credit or certain other welfare benefits are eligible for a Winter Fuel Payment. This is worth £200 or £300 per person and will be paid in November or December 2024. More information including eligibility details can be found on the official government website. As you may know, previously all state pensioners were entitled to WFP, but the new Labour government has chosen to restrict it to the poorest pensioners only.

2. In the event of a prolonged cold spell, most people receiving Pension Credit will receive Cold Weather Payments. People on Income Support, Jobseeker’s Allowance, Employment and Support Allowance (ESA) and Universal Credit may also qualify depending on their circumstances, e.g. if they have a disability and/or a disabled child living with them. You will get this payment if the average temperature in your area is recorded as, or forecast to be, zero degrees Celsius or below for seven consecutive days. You get £25 for each seven-day period of very cold weather between 1 November and 31 March. Note that people in Scotland don’t get Cold Weather Payments but might get an annual £50 Winter Heating Payment instead. This is paid regardless of weather conditions in your area.

As always, if you have any comments or questions about this post, please do leave them below.

This is the 2024 update of an annual post.

If you enjoyed this post, please link to it on your own blog or social media:

The first budget under new Labour Chancellor Rachel Reeves is scheduled for Wednesday 30 October 2024.

Speculation is rife about potential tax rises aimed at addressing the country’s economic challenges. But while tax increases appear inevitable, there is still time to take proactive steps to minimize their impact on your finances.

Here are some tips for how to prepare for and reduce the burden of potential tax hikes.

1. Maximize Tax-Efficient Savings and Investments

One of the most effective ways to protect yourself from higher taxes is by taking full advantage of tax-efficient savings and investment vehicles. These include:

ISA Allowances: The annual ISA (Individual Savings Account) allowance is currently £20,000. Money saved in an ISA grows tax-free, meaning you won’t pay any income tax, dividend tax or capital gains tax (CGT) on any profits made. As well as Cash ISAs, you can invest in Stocks and Shares ISAs and Innovative Finance ISAs (IFISAs).

Personal Savings Allowance (PSA): Basic rate taxpayers can earn up to £1,000 in savings interest tax-free. Higher rate taxpayers get a reduced allowance of £500.

Starting Rate for Savings: For those with a low overall income, the starting rate for savings can be especially beneficial. If your total income (excluding savings interest) is less than £17,570, you may qualify for the starting rate for savings, which can provide up to an additional £5,000 in tax-free interest. This is discussed in more detail in my recent post How to Maximize Your Tax-Free Savings Interest.

Venture Capital Schemes: For those willing to take more risk, schemes like the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) offer significant tax reliefs, including income tax relief and capital gains tax exemption on profits.

2. Diversify Your Investments

Diversification remains a cornerstone of sound investment strategy, especially in times of political and economic uncertainty. By spreading your investments across different asset classes – such as equities, bonds and property – you can reduce the risk of any single investment adversely affecting your portfolio. Consider international diversification as well to hedge against possible downturns in the UK economy.

3. Consider Using a ‘Bed and ISA’ Strategy

If you hold a lot of investments outside an ISA or other tax shelter, this can be a good strategy to reduce your tax liability.

Bed-and-ISA involves selling taxable stocks and shares and then repurchasing them within an ISA wrapper. This allows you to transfer investments into a tax-protected environment, where future gains and income will be sheltered from tax. Note that you cannot transfer taxable stocks and shares directly into an ISA, but Bed-and-ISA performs the same function.

On the minus side, Bed-and-ISA may incur some costs in terms of transaction fees and any difference (spread) between selling and buying prices. You may also become liable for CGT if any profits realized exceed your annual tax-free allowance. The long-term benefits can be substantial, however. This applies especially if – as seems likely – tax-free CGT allowances are reduced and the rates payable are increased. Of course, the Conservatives started doing this when they were in power.

4. Rebalance Your Portfolio Towards Tax-Efficient Assets

Different types of investments are subject to different levels of tax. It’s important to rebalance your portfolio to favour assets that could be less impacted by tax hikes.

Dividends: The tax-free dividend allowance for 2024/25 is £500, and anything above this is taxed at rates of 8.75% (basic rate taxpayers), 33.75% (higher rate), and 39.35% (additional rate). If dividend tax rises further, you may want to limit investments in dividend-paying stocks outside of tax-free wrappers like ISAs and pensions (see above).

Capital Gains: The capital gains tax (CGT) allowance has dropped to £3,000 for the 2024/25 tax year, and there are fears it could be cut further. Consider selling assets to crystallize gains while you can still use your allowance, or shift investments into tax-free vehicles like ISAs using the ‘Bed and ISA’ (or ‘Bed and Pension’) strategy discussed above..You can also offset capital gains with capital losses. If you have investments that have performed poorly, selling them to realize a loss can help offset gains elsewhere in your portfolio. Remember that CGT only applies when a profit (or loss) is actually realised.

Bonds: Government and corporate bonds are often seen as lower-risk investments and may be less vulnerable to tax increases than equity income streams. You might want to consider including more bonds in your portfolio.

Commodities: Gold and other commodities have traditionally been seen as a safe haven in times of economic upheaval. There are risks, however, and it’s important to do your own ‘due diligence’ and seek professional advice before going down this route.

5. Use Your Pension Allowance

Pensions are one of the most tax-efficient ways to save for the future. Contributions receive tax relief at your marginal income tax rate, which means for every £100 you contribute, the government effectively adds £20 for basic-rate taxpayers, £40 for higher-rate taxpayers, and £45 for additional-rate taxpayers.

Consider increasing your pension contributions to mitigate the impact of other tax rises. Just be sure to keep within the current £60,000 annual pension contribution limit. Note that for those earning over £260,000 (adjusted income), the tax-free allowance tapers. More info about this can be found on the government website.

If you’re self-employed, consider setting up or increasing contributions to a private pension or Self-Invested Personal Pension (SIPP) to take full advantage of these benefits.

6. Plan for Inheritance Tax (IHT) Rises

Inheritance tax has long been a controversial topic, and it may well increase under the new government. Currently, the IHT threshold is £325,000, with an additional £175,000 allowance if you’re passing your main home to direct descendants. Anything above this is currently taxed at 40%.

To mitigate IHT risks:

Consider making gifts: You can give away up to £3,000 per year tax-free, with additional allowances for wedding gifts and gifts from surplus income. Gifts between spouses are normally exempt from CGT or IHT, allowing you to transfer assets and take advantage of both partners’ allowances.

Set up a trust: Placing assets in a trust may help reduce IHT liabilities.

Life insurance policies: Some people take out policies specifically designed to cover future IHT bills. Always seek professional advice, however, as trusts and insurance policies can be complex.

7. Review Your Income Structure

Reeves may target income tax thresholds and reliefs, particularly for higher earners. Reviewing how your income is structured could help mitigate the impact.

Salary Sacrifice Schemes: Consider participating in salary sacrifice schemes, where you give up part of your salary in exchange for benefits like pension contributions, childcare vouchers, or cycle-to-work schemes. This will reduce your taxable income.

Dividend Income: If you run a business or own shares, taking income as dividends can be more tax-efficient than a salary, particularly if the dividend tax rates remain lower than income tax rates. Any good accountant will be able to advise you.

Spousal Income Splitting: If your spouse is in a lower tax bracket, transferring income-generating assets to them can reduce your overall tax burden. This is particularly useful for rental income or dividends from jointly held investments.

8. Prepare for Property Tax Changes

Property taxes, including stamp duty and council tax, could see reforms or increases. Here’s how to plan.

Bring Forward Property Transactions: If you’re considering buying (or selling) property, it may be wise to do so before any potential stamp duty increases are announced. Locking in current rates could save you significant costs.

Consider Downsizing: If you anticipate increased council tax rates or other property-related taxes, downsizing to a smaller home could reduce your future tax liabilities and lower your overall living costs. And, of course, doing this should release some of the equity in your property, which you can then use to help maintain your standard of living.

9. Enhance Charitable Giving

If Reeves increases income tax or reduces the thresholds for higher tax rates, charitable giving can become a more attractive option.

Gift Aid: Donations made under Gift Aid are tax-efficient, as charities can claim an additional 25% from the government. Higher-rate taxpayers can claim back the difference between the basic rate and higher rate of tax on their donations.

Donor-Advised Funds: These funds allow you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants from the fund over time. It’s a strategic way to manage charitable giving while benefiting from tax relief.

10. Stay Informed and Seek Professional Advice

Tax planning can be complex, especially in an uncertain economic environment. Staying informed about potential changes in the budget and seeking professional financial advice can help you adapt your strategy to minimize your tax liabilities effectively.

Monitor Budget Announcements: Keep an eye on the budget and any subsequent economic statements to understand how proposed changes might affect you. Quick responses can sometimes yield significant tax savings.

Consult a Financial Adviser: A qualified financial adviser can help tailor a tax-efficient strategy to your individual circumstances, taking into account your income, assets, and long-term financial goals.

Closing Thoughts

While tax rises in Rachel Reeves’ first budget may be inevitable, UK residents have various strategies at their disposal to mitigate the impact.

By taking advantage of tax-efficient investments, restructuring income and staying informed, you can protect your wealth and ensure that any tax increases have a minimal effect on your financial well-being. As always, professional advice tailored to your specific situation is invaluable in navigating these changes effectively.

If you have any comments or questions about this post, please do leave them below. But bear in mind that I am not a qualified tax adviser and cannot provide personal financial advice. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

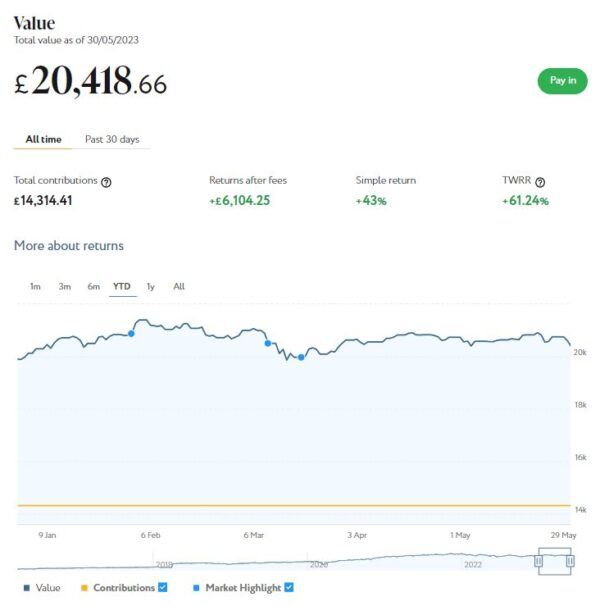

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £20,419. Last month it stood at £20,740 so that is a fall of £321.

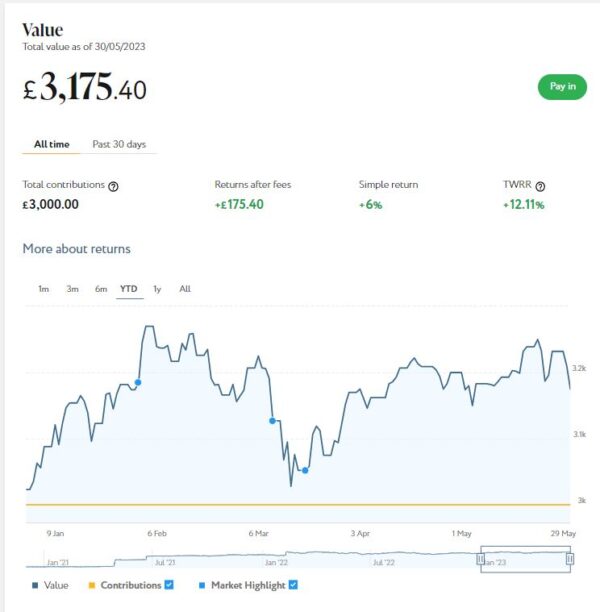

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,175 compared with £3,201 a month ago, a small decrease of £26. Here is a screen capture showing performance since the start of this year.

As you can see, this has been another up-and-down month for both my Nutmeg pots. Pro rata, though, my Smart Alpha portfolio has again done a bit better than my main portfolio. I am therefore tempted to switch more of my money into it, although there isn’t a massive difference in performance between them.

The net value of all my Nutmeg investments has fallen this month by £347 or 1.45% month on month. That is obviously disappointing, but both pots are still comfortably up on where they were at the start of the year. And their total value has risen by £1,781 (8.16%) since mid-October last year.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £117.63 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 7 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 14 are showing (small) losses. My portfolio is currently showing a net decrease in value of £23.62, meaning that overall (rental income minus capital value decrease) I am up by £94.01. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is a bit disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

I also spoke to the CEO of Assetz Exchange, Peter Read, recently. He made the point that capital values on the platform simply reflect the latest price at which shares in the property concerned have changed hands on their exchange. They do not represent objective or independent valuations of the properties. If you are investing long term with AE, the annual yield from rentals is really a much more important consideration.

Peter also made the point that the current high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. I don’t want to go into too much detail about this here, but it is a subject I may return to in a future blog post.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching every week. I currently have around £2,500 invested with them in 18 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 30 June 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 30 June 2023 if the limit is reached. For more information, click here [affiliate link].

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares. My original investment of $1,022.26 is today worth $1,093.00, an overall increase of $70.74 or 6.92%. in these turbulent times I am happy enough with that.

Since last month the price of my Tesla shares has risen and my copy trading portfolio with Aukie2008 has performed steadily. Unfortunately my most recent investment in Oil Worldwide is in the red, though. I am hoping for better things in the months ahead 🙂

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in May on the excellent Mouthy Money website. The first was How to Save Money With Cashback Sites. If you ever buy anything online, you can almost certainly save money by signing up with these sites, which include Quidco and Top Cashback. You can read about my experiences with them and my top tips in this article.

My other article was Equity Release – Is It Right for You? In these financially challenging times, more and more older people are turning to equity release to release money tied up in their homes. My article explains the main options and sets out a range of points to consider before doing this.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite and I enjoyed reading her recent article How to Start Comping and Win Big!

I also published a number of new posts on Pounds and Sense in May. One of these was about My Short Break in Aberdovey. This is a small town on the mid-Wales coast, between Aberystwyth and Tywyn. It was my first visit to Aberdovey and I recommend it for a chilled-out break – although (as I say in the article) I wouldn’t go there for the nightlife!

On a similar note, I published Get a Free ETF Share Worth up to £200 with Wealthyhood. Wealthyhood is a DIY wealth-building app aimed especially at people who are new to stock market investing. As from 1 June 2023 they changed their fee structure to make it even more attractive to small investors. It’s worth checking out, even if you only want the free share. This is an ongoing offer, but to qualify you do have to make a £20 minimum investment on the platform.

I also published an article titled Nibble Launches New Legal Strategy for investors. Nibble is a European crowdlending platform open to anyone. They are offering returns of up to 14.5% in their new Legal Strategy, which involves investing in loans that are in default and facing legal action (hence the name, of course). That is obviously higher risk, but NIbble guarantee to pay all investors in this strategy a minimum of 8% up to the maximum 14.5% depending how successful their recovery efforts prove. Average quarterly returns are currently 12.5%.

The other post I published in May was also about equity release. It’s titled Why Are People Opting for Equity Release? The article features some interesting research on why people are opting for equity release in the current economic climate, and what reasons are becoming more common. Definitely worth a look if equity release is on your radar.

One other thing I should mention is that I had an article published a couple of weeks ago in the Daily Telegraph newspaper about my investing experiences. If you read my monthly investment updates on PAS you won’t find too many surprises in it, but here’s a link anyway in case you’d like to check it out. Note that the article is behind a paywall so unless you are a Telegraph subscriber you will only be able to see the start.

Finally in May I enjoyed a short break in Yorkshire visiting my sister Liz and her family. Once again I stayed at the beautiful Hewenden MIll Cottages, between Wilsden and Cullingworth (near Haworth and ‘Bronte country’). If you’re looking for an unusual, rural-based short-break destination, Hewenden could certainly fit the bill. A photo of the old mill building (in which I stayed on a previous visit but not this time) is shown below. There is also a photo of the woodland at Hewenden in the cover image. You can read my original review of Hewenden Mill Cottages here.

That’s all for today. I hope you’re enjoying the better weather and taking the opportunity to get out and about in our beautiful country (or further afield).

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

If you enjoyed this post, please link to it on your own blog or social media:

As you probably know, equity release is a method of unlocking funds tied up in your property. It is open to homeowners aged 55 and over (60 and over in the case of home reversion plans).

In recent years equity release has become increasingly popular, and even rising interest rates have done little to dampen this trend. So today I thought I would look at the main reasons people are opting for equity release. I am indebted to my colleagues from Equity Release Supermarket for providing information (based on their internal data) on the top reasons people are releasing equity, as well as which reasons are seeing the biggest increases.

The table below shows the top reasons people have been using equity release over the last six months.

Rank

Reason for equity release

1

Repay mortgage

2

Home improvements

3

Debt consolidation

4

Supplement income

5

New/second home purchase

As the table shows, repaying a mortgage is the number one reason over 55’s have released equity. The data shows that, on average, 21.1% of completed cases planned to pay off an existing mortgage with the money released.

Home improvements are the second most common reason, with an average of 17.9% of borrowers raising money for a renovation project.

Debt consolidation is the third most common reason for equity release, at a slightly lower average of 13.7%. Interestingly, when looking at the data by month, using equity release for debt consolidation peaked at 18% in December 2022.

The data also reveals which reasons for equity release have increased in popularity over the last six months, with home improvements seeing the biggest increase, growing by 7.7%.

Gifting money is becoming an increasingly popular reason to release equity too. In the last four months alone, gifting money that has been released through an equity release scheme has risen by 2%.

“Equity release is available for homeowners over the age of 55 who wish to free up some of the money, tax-free, that has been built up in the equity of their home. The interest rate is fixed for life and the plan is repaid when the homeowner dies or moves into long term care.

“It is perhaps unsurprising that repaying a mortgage is the top reason for equity release. As interest rates and living costs continue to rise, borrowers will be looking for ways to reduce their monthly payments. By using an equity release scheme, such as a lifetime mortgage, to pay off your existing interest only mortgage you will no longer need to make monthly payments unless desired. This can help make monthly savings and alleviate financial pressures, especially for those who have seen their mortgage payments rise in recent months due to interest rates.

“It is interesting to see that gifting money through equity release has risen over the last six months. Money gifted through equity release becomes exempt from inheritance tax, provided that the gift giver lives for seven years afterwards. Inheritance tax can significantly reduce the amount of wealth that you may be able to pass on, so we often find that many people turn to equity release as a strategy for reducing the impact it will have on an estate.

“In this uncertain economic climate, it is more important than ever that borrowers are getting advice on what product options are available across the whole equity release market. For anyone considering equity release, we would suggest discussing your plans with one of our equity release advisers.”

My Thoughts

If you’re looking for a way to release money from your property – whether to pay off debts/mortgages, fund specific purchases, assist children or other family members, or just make later life more comfortable – equity release is certainly something you may want to consider.

The main downside is – of course – that ultimately there will be less money to pass on to your beneficiaries. All reputable providers, however, offer a no-negative-equity guarantee. They may also be able to arrange plans where a certain amount of cash is guaranteed to remain in your estate, if you so wish.

Equity release interest rates in most cases are fixed for life, so you will know from the start the liability you are taking on. Of course, the longer you remain living in your home, the larger the debt eventually payable from your estate will be.

If you think equity release may be right for you, you will need to discuss this fully with an independent adviser before proceeding. As well as Equity Release Supermarket other well-known firms in this field include Key Equity Release and Age Partnership. The Equity Release Council has a full list of members on its website.

The adviser will discuss your needs and circumstances, and – assuming they think equity release is right for you – make a recommendation from the range of products on the market. You can, of course, speak to two or more different advisers if you wish before making any final decision.

Thank you again to my colleagues at Equity Release Supermarket for their assistance with this post. As always, if you have any comments or questions, please do leave them below as usual.

According to the government’s own figures, around a third of retirees who would be entitled to this state benefit aren’t currently claiming it. That means they are potentially missing out on an important boost to their pension.

Even more significantly, it means they may be missing out on a raft of other benefits and discounts too, for which pension credit acts as a gateway. More about this shortly.

Applying for pension credit is especially crucial for people who reached retirement age before April 2016 and therefore receive the old basic state pension rather than the new (higher) one. While it may seem (and indeed be) unfair that older pensioners receive a lower rate, they do have the opportunity to claim the savings credit element of pension credit, which newer retirees don’t.

Savings credit payments can provide an extra boost to your income and entitle you to other payments and benefits as well. And, very importantly, the eligibility rules are different from guarantee credit and (in my view anyway) a bit less stringent. But if you don’t apply for pension credit, you won’t get either.

But before we get into that, let’s recap on what pension credit is.

What is Pension Credit?

Pension credit is a state benefit that comes in two parts: guarantee credit and savings credit.

Guarantee credit boosts your weekly income to £182.60 if you’re single or £278.70 if you’re a couple (figures correct from 6 April 2023). You should be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home).

If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments. This will be added to your total income when working out your eligibility for guarantee credit.

Savings credit is only available to people who reached the state pension age before 6 April 2016. It is meant as a reward for those who have made some additional provision for their retirement. It’s worth up to £15.94 a week for a single person or £17.84 for couples (2023/24 figures). Somewhat counter-intuitively, to qualify you must have a minimum income of £174.49 a week if you’re single and £277.12 a week for a couple (again 2023/24 figures). You must also have some savings or other extra income provision (e.g. a private pension).

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount that you’re entitled to.

The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee you will receive the amount it shows you.

Until recently to actually apply for pension credit you had to phone the DWP’s pension credit helpline on 0800 991234 with your Nl number, details of your income, savings and investments, and your bank account details. The person you spoke to would then then take you through the application process. This option is still available, but recently an option to apply online has been added. This is quite separate from the free online calculator mentioned above.

As I recently helped an elderly friend do this, I can confirm that the online method works well, though the questions asked don’t entirely correspond with the questions on the free online calculator. But using the latter first should give you an idea whether you are likely to qualify for pension credit and how much you might get. You can also try the effect of changing the amount of capital/income in the calculator to see if you might qualify in future even if you don’t at present (perhaps due to having too much in savings).

Additional Benefits

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional discounts and benefits. These may include:

Even if you only receive a small amount of pension credit, you may be eligible for any of the above. So it really is important to apply if there is any chance you may qualify.

More About Savings Credit

As I said above, only older pensioners who retired before April 2016 can get savings credit. But potentially a lot more people in this category may be eligible for it than is the case with guarantee credit.

Whereas guarantee credit is only paid to pensioners on a low income and with limited savings, that isn’t necessarily the case with savings credit. As I noted above, to qualify for savings credit there is actually a minimum earnings limit. And you do actually need to have some savings (or other income source/s apart from the state pension) to be eligible.

The rules are complicated, so – as I said above – the best thing is to use the free online calculator. If it appears you are eligible for savings credit (or guarantee credit) it will tell you, and how much.

It should be said that if you are only awarded savings credit and not guarantee credit, you may not qualify for all of the extra benefits mentioned above (free NHS dental treatment, for example). But even if, with savings credit only, you don’t qualify for the whole of the discounts mentioned, you may at least be eligible for a partial reduction.

For the latest news and information about pension credit, please click here.

Closing Thoughts

To sum up, if you’re of state pension age and have a limited income or savings, you should certainly look into pension credit. Similarly, if you have elderly friends or relatives, you should check eligibility on their behalf (with their permission, of course).

As I’ve said above, this applies especially to anyone who started receiving the state pension before April 2016 and is therefore getting the old basic state pension. This is lower than the new state pension, but you may potentially be eligible for the savings credit element of pension credit (as well as guarantee credit, which anyone of state pension age can qualify for).

While savings credit is generally only a small amount, receiving it will make you eligible for a range of other discounts and benefits, including (as from winter 2024) Winter Fuel Payments. So it really is well worth checking on the free online calculator and then applying (by phone or online) if it appears you might be eligible.

Finally, you might like to know that (thankfully) my friend’s online application was successful. He got a letter a week later saying that he would be receiving pension credit (savings credit only) at a rate of about £5 a week, rising to just over £6 a week the following April. Naturally he was pleased to hear this. And he was even more pleased when he realised he would be getting the other benefits and discounts mentioned earlier as well. As an 84-year-old man who has recently lost his wife, this will certainly help make life a little more bearable for him.

As always, if you have any comments or questions about this article, please do post them below. Just bear in mind that I am not a qualified financial adviser or benefits adviser and cannot provide personal financial advice. If you require specific advice or assistance, your local Citizens Advice office would be one good place to start.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension), from which I recently started withdrawing again.

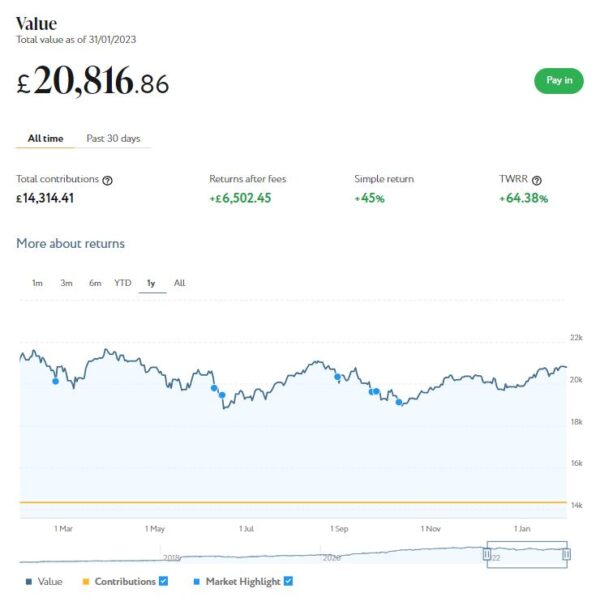

As the screenshot below of performance over the last year shows, my main Nutmeg portfolio is currently valued at £20,817. Last month it stood at £19,898 so that is a rise of £919.

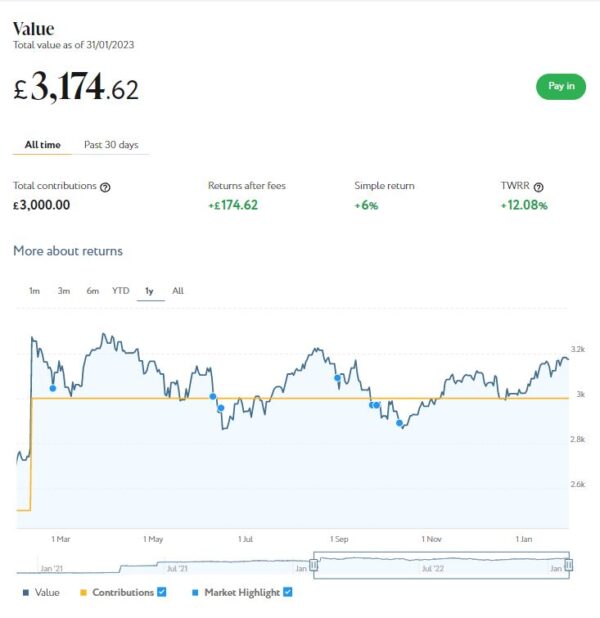

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,175 compared with £3,023 a month ago, a rise of £152.

Here is a screen capture showing performance over the last year. As you can see from the ochre line, I topped up this account in February 2022.

Clearly 2023 has started well, with the total value of my Nutmeg investments increasing by over £1,000. The strong start for equities in general in 2023 is due to various factors, including inflation rates world-wide starting to fall, the ending of most Covid restrictions in China, and a growing belief that any post-pandemic recession may not be as severe as was once thought. Of course, the war in Ukraine is still a major concern, but if that is resolved in the coming year it should give markets a further boost.

2023 is still likely to be an uncertain year for investors, with more ups and downs very much on the cards. Nonetheless, with share prices generally still below where they were a year ago, there are likely to be opportunities for investors to capitalize in the months ahead. I shall definitely be looking to invest more in Nutmeg and other equity-based platforms in the coming year.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last six years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a very respectable £96.79 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally. Even so, it’s not all bad news. At the time of writing 16 of ‘my’ properties are showing gains, 7 are showing losses, and two are breaking even. My portfolio is currently showing a small net increase in value of £13.36, meaning that overall (rental income plus capital gains) I am up by £110.15. That is still a very decent rate of return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,400 invested with them in 18 different projects (I withdrew £200 in December to help pay for Christmas). To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

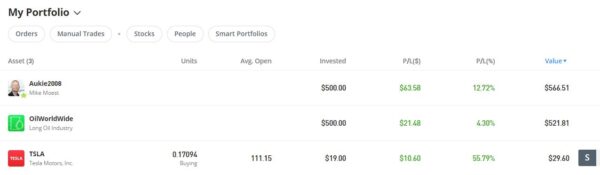

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January I added to this with another $500 investment in one of their thematic portfolios. I also invested a small amount I had left over in Tesla shares. My original investment of $1,022.26 is today worth $1,118.62, an increase of $96.36 or 9.63%. in these turbulent times I am very happy with that.

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. You can read my full review of eToro here. You may also like to check out my recent more in-depth look at eToro copy trading. I shall be publishing a post about my latest investment in an eToro thematic portfolio soon.

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in January on the always-excellent Mouthy Money website. One is A Three-Step Plan to Help Boost Your Finances in 2023. This article actually came out of an online presentation I did a few months ago to a club for older people. I hope you will find the ideas and advice it contains useful.

My other piece was Switch to Profit – How to Make Money Moving Your Bank Account. With the banks now starting to offer switching bonuses again to attract new customers, there are hundreds of pounds to be made by doing this. The article quotes my sister Annie, who is a serial switcher and shares some top tips based on her experiences. Many thanks, Annie!

That’s all for today. I hope you and your family are coping in these undoubtedly challenging times. Don’t forget to check out the government’s Help for Households website, which sets out various types of financial assistance you may be entitled to and is regularly updated.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you an expert guest post on a subject that unfortunately affects growing numbers of middle-aged and older people.

Separation and divorce can have a massive impact on your finances, so it’s important to be prepared and take advice as appropriate. Senior divorce lawyer Natalie Lester explains…

It’s always sad to see a marriage come to an end but it is particularly so when a couple have been together for 30 or 40 years. Unfortunately, divorce rates for those of retirement age are on the rise and our family law and divorce team have found a significant increase in the instructions received from those aged 55 and over.

There are several likely reasons for the increase, some of which include:

Life expectancy. People are living longer and many couples find they have grown apart by the time they get to their sixties and their children have left home. People often have many years ahead of them after they retire, and this can cause them to re-evaluate their life.

Reduced stigma. Throughout the 60s, 70s and 80s, there was a negative attitude and stigma towards divorce and divorcees. Today, we see a far more accepting attitude towards divorce in a more liberal society.

Female equality. In contrast to a few decades ago when women were far more likely to become housewives rather than pursue their own career ambitions, married women today often earn as much or even more than their husbands. Greater financial equality provides a greater sense of freedom so women of all ages are now more confident to end a marriage that has broken down.

Meeting new partners. This has become easier thanks to online dating websites and because retirees are more active in retirement., there is less fear that getting divorced will result in spending the rest of one’s life single and alone.

Menopause. This can be a particularly challenging time for couples and both partners can feel confused and concerned as they navigate the respective changes. Inevitably, it can highlight existing struggles, further damaging the connection between couples.

Divorcing and remarrying later in life typically involves added legal complexities. To address some of these, we have set out some top tips below:

Dividing assets on divorce after a long marriage

While it is always important that divorce settlements are divided fairly and in a mutually satisfactory manner, this issue is more crucial for older couples because after a long marriage, there is often a large matrimonial pot at stake. In addition, and in contrast to their younger counterparts, silver-splitters may be reliant on their pensions with no chance of acquiring new wealth through work. After a long marriage, assets are usually split 50/50.

The family home is often one of the most valuable assets in the matrimonial pot. There are various ways in which the court may decide to deal with this asset and it is important that you obtain legal advice to consider the options available. This will usually include selling the home and dividing the proceeds, transferring the property and buying the other spouse out or if there are multiple properties, one spouse retaining the home and the other spouse retaining another property. Court proceedings are a last resort and divorcing couples should take a constructive approach and consider all alternative dispute resolutions options to reach an agreement.

Like the family home, a couple’s pension is another key asset which needs to be divided up and the courts have extensive powers to deal with pensions upon divorce. One option (and the most common) is a pension sharing order. The order will state what percentage of your spouse’s pension pot you will receive. This share will be removed from the pension and placed into a pension in your sole name (some providers allow for internal pension transfers so that you can keep your pot within the same scheme). Pensions are a difficult area and you may need a pension expert to determine the real value of a pension pot and to advise on the various options. A good divorce lawyer will be able to advise on whether this is necessary.

Preparing for unforeseen circumstances

Loss of capacity. If one of you lacks capacity, then a litigation friend may be required. A litigation friend is someone who helps a “protected person” with their legal issues. This can be a parent, guardian, a family member or friend. If that is not possible, they will need to be represented by the Official Solicitor. The Official Solicitor acts for people who, because they lack mental capacity and cannot properly manage their own affairs, are unable to represent themselves and no other suitable person or agency is able or willing to act. It is important to consider who should step in as your litigation friend should you lose capacity to provide instructions to your lawyers. Your divorce cannot proceed until you have someone (other than your lawyer) acting on your behalf.

Wills. It is important to get a holding Will whilst you are going through the divorce process. If you were to die without a Will, the intestacy rules will kick-in. This would mean that your spouse would automatically inherit some or all of your estate. This is irrespective of the fact that you may be separated. A new Will should be drawn up once the divorce is finalised.

Protecting your wealth in new relationships including re-marriage

If a new relationship is on the horizon, it is important to think about getting a living together agreement drafted which will help protect your property should the new relationship fail.

Likewise, If remarriage is on the cards, a prenuptial agreement should be considered because a future marriage breakdown could significantly impact your financial position and any commitments you may have to children from a previous marriage. A lawyer specialising in succession planning will also be able to advise you on how to ringfence assets you may wish to pass to your children.

It is always wise to pay extra attention to tax planning after a long marriage. We encourage our clients to speak to an accountant, who can help with tax planning early on in the process.

While there is a lot to think about when getting divorced at a later stage in life, readers should remember that with the right advice, the process can be straightforward. Where possible, we always advise our clients to keep lines of communication open with their estranged spouse and to aim for a “good” divorce. By being open about your plans and finances, you are more likely to stay on amicable terms with your spouse which will benefit your wider family including any children, no matter how grown up they are! This will also help you to move the process along, not only saving time and money on legal fees, but also enabling you both to start what can be an exciting new chapter in your lives.

I’ve mentioned several times on PAS why I believe having an independent financial adviser makes sense, even if – like me – you consider yourself reasonably money-savvy.

So today I thought I would set out some reasons over-50s (in particular) may benefit from having an independent financial adviser (IFA) or at least speaking to one.

This post has been created in association with my colleagues at Unbiased.co.uk, a well-established financial services website that can put you in touch with suitable IFAs in your area.

Reasons for Having an IFA

1. Helping Your Children Through College or University

If you have children, you will naturally want to help them complete their education safely and with a reasonable degree of comfort. Sadly the days of student grants (which I was lucky enough to benefit from in the 1970s) are well behind us now. There are various options for helping finance your children’s college or university education and a financial adviser will be able to explore these with you. They will also explain the pros and cons of the student loans system.

2 – Pension Planning

If you are over 50 you will inevitably be thinking about pension options, including when you can retire and how much income you can expect. An IFA will go through your finances with you and look at ways you may be able to boost your pension pot. From 55 onwards you can normally start to draw your pension, but you shouldn’t do this unless a financial adviser has assured you it will last you through retirement.

3. Investing

Hopefully by your fifties you will be earning a decent salary and may also have paid off your mortgage. You may also receive an inheritance or other windfall. Either way, if you find yourself with some spare cash you will want to invest it to get the best possible returns from it. An IFA will have access to all the latest information about a vast range of investment opportunities. They will guide you towards investments that are suitable for you based on your financial goals, your investment timeframe and your appetite for risk.

4. Starting Your Own Business

Especially at this time of upheaval due to Covid, many people are looking to start their own businesses in mid-life. That may be in response to redundancy or unemployment, or simply in search of a better work/life balance. An IFA can help you with the financial aspects of doing this, including raising money for tools, premises, transport and so on, or perhaps buying a franchise.

5. Emigrating or Retiring Abroad

Another way to revitalize your life may be to start afresh somewhere else, with new challenges and opportunities (and perhaps a better climate as well!). Or you may be looking to move to a favourite vacation destination to enjoy your retirement. Either way, an IFA will be happy to discuss the pros and cons with you, point out all the things you will need to take into account, and assist you with the financial arrangements.

6. Divorce

Sadly middle age sees the largest number of divorces. Your first priority here will be appointing a good solicitor to act on your behalf and protect your interests. Beyond that, though, divorce can have major ramifications for your finances. An IFA can help you assess your situation objectively and plan for a financially secure and stable future.

7. Downsizing

As the children grow up and leave home you may want to move to a smaller property – to make life simpler, save time on housework and free up money for more exciting things. An IFA can help you explore the implications of doing this and make the necessary financial arrangements.

8. Equity Release

If you don’t want to move – and are over 55 – equity release is another option for releasing funds. In recent years it has grown a lot in popularity. There are various possibilities, including home reversion plans and flexible lifetime mortgages. Most now come with a no-negative-equity guarantee, ensuring you won’t end up passing on debts to your next of kin. An IFA can go over the options with you and point out the pros and cons before you contact any providers.

9. Estate Planning

This obviously includes writing your will, but depending on your circumstances it can cover a lot of other things as well. Nobody wants to see all their money and assets falling into the hands of the taxman rather than going to their nearest and dearest. Speaking to an IFA who specializes in estate planning can give peace of mind and ensure that your loved ones are well provided for when you are no longer here yourself.

10. Helping Elderly Relatives

If you have elderly parents (or other relatives) you may find they are increasingly reliant on you for help and support. It may be up to you to arrange care for them and/or set up power of attorney so you can manage their affairs if this becomes necessary. They may also need help with estate planning (see above). An IFA can assist with all these things as well.

Getting a Free Financial Check-Up

Independent financial advisers do of course charge for their services. They are by definition unaffiliated and do not receive commission, so any recommendations they make are based solely on their client’s best interests. As I have said before on PAS, I certainly don’t begrudge paying my own financial adviser, Mike, as he has undoubtedly saved (and made) me a lot more money than he has cost me over the years.

Nonetheless, most IFAs will be happy to see you for an initial financial healthcheck free of charge. This can focus on a particular area of concern, so you could request an investments review, a pension review or a mortgage review. Alternatively, if you’re not sure which aspect of your finances needs more attention – or indeed whether you need advice at all – you could simply request a broad financial healthcheck.

Here’s what. Adrian Kidd, a financial planner at Radcliffe & Newlands, says about his approach on the Unbiased website:

‘I’d generally offer one or possibly two free consultations, taking about an hour, and these can be as specific or as broad as required. When someone books a financial healthcheck with me, I ask them to bring along all their documents relating to their finances – savings, investments, mortgages, loans, insurance, pensions, the works – so I can build up a complete picture of their affairs. I then go through these in more detail after the consultation, and follow up with an email that gives a summary of their overall financial situation.’

In these free check-ups: advisers won’t generally talk to you about products at all. The process of choosing the right products comes later, after the adviser has built up an understanding of you as a person and your financial planning needs. Only then will they recommend products, if asked to do so.

If you follow my link to the Unbiased website, you can complete a short, step-by-step questionnaire designed to identify the best type of financial adviser for your needs. You will then be shown a selection of suitable advisers in your area with contact information. They will be happy to answer any queries you may have and arrange an initial meeting without obligation.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Unbiased.co.uk. If you click through my link and end up becoming a client of a financial adviser listed on the Unbiased site, I may receive a commission for introducing you. This will not affect the service you receive or any fees you are charged if you decide to proceed further.

This is a fully updated version of a post originally published in 2020.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have the first in a series of three collaborative posts on the subject of equity release. This one examines the growing popularity of equity release and why it looks set to boom in the year ahead.

The equity release industry saw a massive expansion in 2021, with a record-breaking sum of over £4.8 billion being unlocked by retirees across the UK. This unprecedented growth has been welcomed amid a global pandemic, as the Equity Release Council helps regulate a retirement product that has given many retirees the means to a desperately needed income in these tough economic times.

Mark Patterson, the equity release expert from EveryInvestor, joins the ranks of fellow industry authorities in predicting that 2022 is set to be another record-breaking year. Let’s take a look at what’s expected and determine if unlocking equity is a good idea over the next few months.

What Is Equity Release?

Equity release is a widely popular financial product for UK-based homeowners older than 55. In a nutshell, it gives you the opportunity to use your property’s equity but still live at home. With a third of UK retirees having less than £10,000 in retirement savings, equity release offers a lifeline to many. What’s more, the money can be used for any purpose.

According to figures from the Equity Release Council (ERC), equity release clients borrowed a total of £4.8 billion last year, a 24% rise on 2020’s figure.

Why is the Equity Release Industry Growing Amid a Tough Economy?

While many industries have crumbled in the wake of Covid 19, the equity release sector has grown tremendously. This is for several reasons, including:

Equity release provides financial security in a tough economic time.

The Equity Release Council has made the industry safe and is shifting a historically bad reputation.

Interest rates hit an all-time low in March 2021, and homeowners have received the best deals yet, with fixed-for-life interest rates.

Finally, growth inspires growth. As the industry expands, lenders offer more flexible products with bonus features, such as a free valuation or no completion fee.

What’s Predicted for 2022?

The future of equity release looks bright in 2022, and 80% of experts predict growth, with some believing this will be vastly beyond regular inflation. There are some key industry features that are likely to impact the industry (1).

First, the Equity Release Council announced on 31 January 2022 that all equity release lenders must offer the opportunity for voluntary loan and interest repayments. This announcement is welcome for potential borrowers, as voluntary repayments can vastly reduce the cost of your loan, yet there’s no obligation or risk of foreclosure.

On a slightly less positive note, equity release interest rates will rise in 2022 and should continue to do so until 2024. However, this could actually mean further industry growth. Rates are set to rise only slightly, and homeowners applying now will likely begin their equity release plans before we see any further increases.

Should I Unlock Equity from My Home at This Time?

With the market as it stands, it is a good idea to unlock equity if you’ve been planning to do so. However, it’s more complicated than just looking at the state of the industry.

Whether or not you should unlock equity from your home will depend on your personal circumstances and stage of life. What’s great is that equity release is safe; it’s overseen by the Equity Release Council and regulated by the Financial Conduct Authority (FCA).

However, to determine if it’s a good idea to unlock equity from your home, you should speak to a financial adviser. After all, seeking advice is compulsory when opting for an equity release product. The team at EveryInvestor will always encourage a whole-market financial adviser as they have an overview of the whole equity release market.

In Conclusion

Between flexible plans, the opportunity for voluntary repayments, and interest rates still low, now is a great time to release your property value through equity release. With another record-breaking year ahead of us, the industry is booming, and many more retirees are set to sign up to an equity release plan. Could you be next?

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media: