Guest Post: Exploring the Potential of Investing in Alternative Rental Properties

Today I have a guest article for you by my colleague Jackie Edwards.

Jackie is a professional property investor and property restorer. In her article below she sets out the case for investing in alternative rental properties – in particular, for the growing over-50s market.

Over to Jackie then…

While discussion around the mortgage and rental market often focuses on younger people – particularly first-time buyers and millennials – just as important are the over 50s.

A 2022 report in The Guardian sheds light on an alarming trend: individuals over 50 are finding themselves compelled into room-sharing arrangements, a consequence of being priced out of independent living options. The data supports this unsettling shift, citing a steep 114% surge in room search enquiries from people aged 45-55, compounded by a staggering 239% uptick in enquiries from those in the 55-64 age bracket.

Despite being often well-experienced and highly skilled, these individuals find themselves at the mercy of a punishing housing market. This situation signals a promising investment opportunity for businesses and individuals prepared to invest in accommodation tailored for those aged over 50. Already, a handful of forward-thinking schemes across the nation are demonstrating this growing potential.

What’s Required

Of course, a range of factors need to be considered when providing bespoke housing to over-50s. Disability, for example. According to the Office of National Statistics, the incidence rate of disability increases significantly after the age of 50, and it becomes more likely that the applicant will need adaptations to their accommodation.

As anyone living with a disability will know, it can be difficult to find accessible housing. According to disability advocates Eachother.org.uk, only 9% of UK rentals are suitable for people with a disability. Landlords that can prepare and provide accessible accommodation, at reasonable asking prices, will be providing a valuable service which is very much in demand.

What a Rental Requires

With that in mind, it’s important to consider the specific needs of the 50s-and-over market. According to PropertyRoad.co.uk, 15% of all rentals are now occupied by people over 50, an increase of 61% from the previous recorded figures in 2012. This may not necessarily be a bad thing, however.

In the Guardian’s survey of the renting situation, an interesting factor was highlighted. While many older people are pushed into renting as a result of rising costs, many others actually prefer the flexibility of not being tied to a mortgage and, crucially, the feeling of community that comes with communal living.

One scheme the Evening Standard highlights is a house sharing scheme that specifically matches up younger and older people, with company the key factor, but with a degree of agreement from the younger party to assist with chores and housework.

Intermediate Rent

As highlighted by ShareToBuy.com, intermediate rent is a scheme where renters agree to charge lower rentals (generally at least 20% below the standard private market rates in the area) in exchange for longer-term contracts. For the younger generation who may be looking to move around a lot, these schemes are less attractive. For over 50s, who are happy in one area and looking for something affordable for the medium to long term, it may well be an excellent option.

What is crucial is that landlords and property businesses offer these properties more widely in bespoke packages for over 50s. Currently the market in such properties is very limited, though a few smaller companies and organizations have embraced this challenge. They include Cohabitas, certain schemes on Spareroom, Flatmates.co.uk and RoomPortal.

More needs to be done with alternative rental accommodation for this niche – yet rapidly growing – demographic. A lot of focus is placed on millennials, but much more needs to be done for older renters, to help them find high-quality and long-lasting accommodation. For landlords and businesses who want to generate a stable rental income while also offering a valuable service to older individuals, this could represent a very appealing proposition.

About the author: A career in property investing led Jackie Edwards to develop a passion for restoring old homes. And even in her free time, she’s renovating her own with her husband. They’re both semi-retired (though by no means retirement age) and to keep her interest alive Jackie writes articles on home and lifestyle. In any free time she has, she’s walked by her two dogs Barker and Corbett and she volunteers for a local foodbank.

Many thanks to Jackie for an interesting and thought-provoking article.

Obviously not everyone will have the money to invest in alternative rental accommodation directly. If, however, you are attracted to the idea of investing in this sector, a more affordable option is presented by Assetz Exchange.

Assetz Exchange is a P2P property crowdfunding platform. They focus on lower-risk, socially beneficial accommodation, such as supported housing for people with physical or mental disabilities.

Properties are bought jointly by investors under the usual crowdfunding/P2P model. Most are then leased to charities and housing associations. This means they are securely funded and there is a low risk of defaults.

Of course, defaults could still happen in certain circumstances – but as investors jointly own the property in question, ultimately you could still expect to get your capital (or most of it) back when the property is sold.

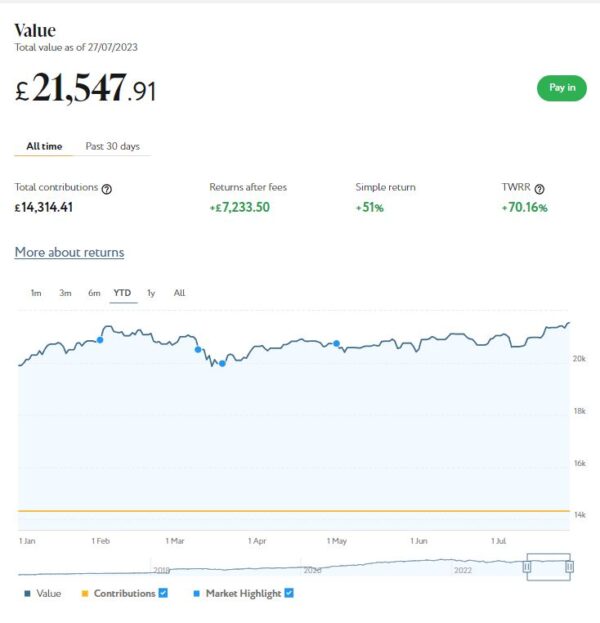

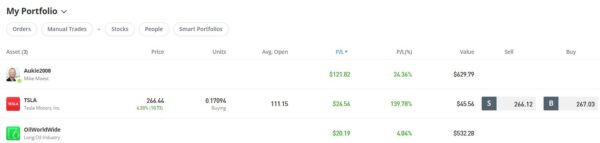

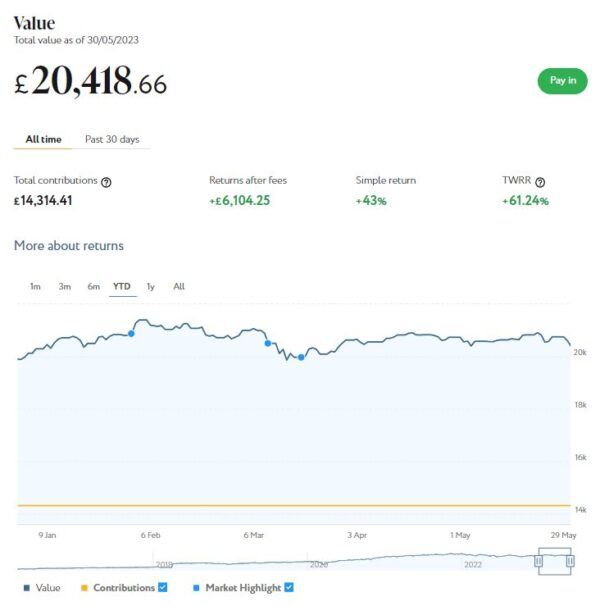

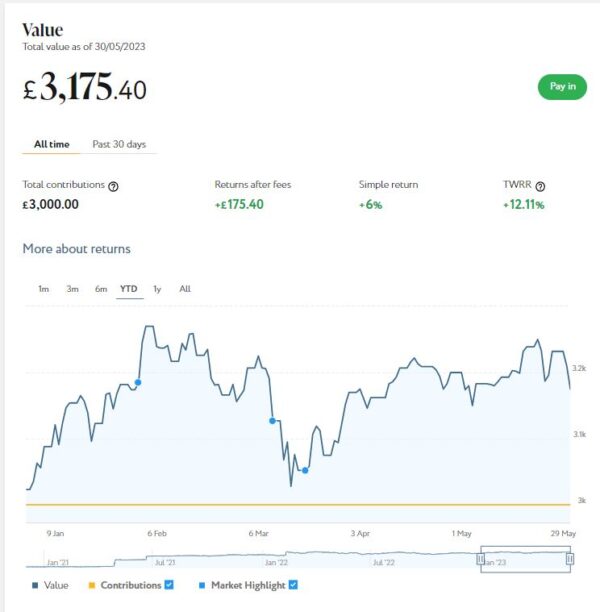

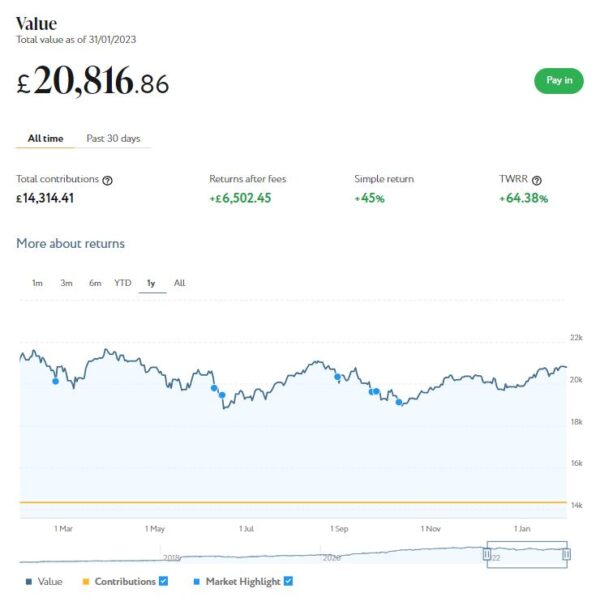

I have been investing with Assetz Exchange since February 2021 and have gradually built up the amount I have with them. I put an initial £100 into AE in February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000. Since I opened my account, my AE portfolio has generated £143.56 in revenue from rentals. That’s a decent rate of return on my £1,000 (staged) investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile (as at the moment).

I now have investments in 23 different projects and all are generating rental income as expected. Capital values have declined slightly overall – in line with the UK property market generally – but of course this isn’t really relevant until or unless you want to sell up. Overall I am very happy with how my AE investment has been doing, and the fact that projects are generally beneficial to society as well.

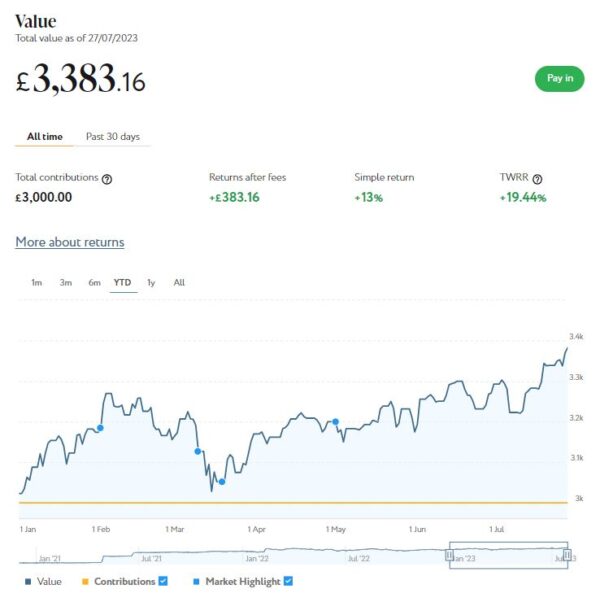

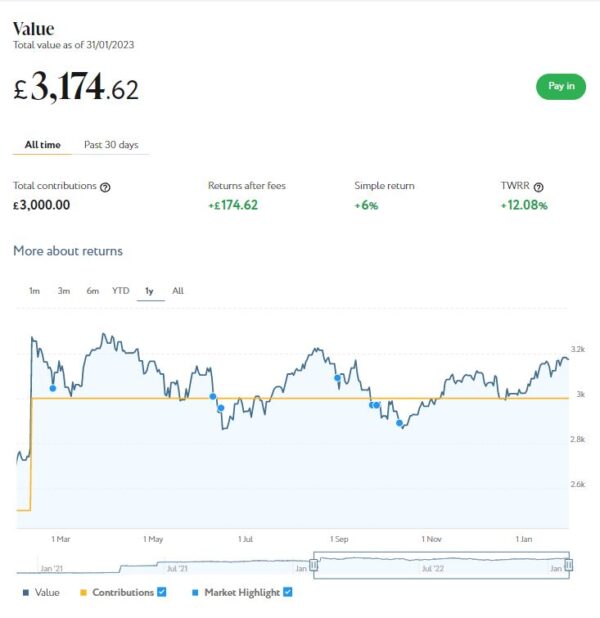

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as I am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

As always, if you have any comments or questions about this article, you are very welcome to post them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!