A great number of people today need to transfer currencies, or receive transfers from abroad, for many different reasons. As globalization extends, this need has become more frequent as geographical borders become less relevant.

For example, our parents couldn’t even dream about services like eBay or Alibaba, where you can buy anything and have it delivered from a dozen countries away. And the whole thing might be cheaper than buying it in your local store!

But here is where the matter of foreign currency transfers becomes important. Paying for something abroad or getting money sent to you might not be cheap. That’s because not only do you have to pay bank fees for the transaction, you also lose money on currency exchange, which is often a mandatory step in cross-border transfers.

Luckily, today there are alternative money transfer services that allow you to cut these costs. You’ll need to look into them if you require regular foreign currency exchange (FX or forex) services.

Why You Might Need to Make Foreign Currency Transfers

One reason you might need to make a large money transfer abroad is real estate. Buying property is an important part of the retirement planning process and many Britons choose to retire abroad. For example, the latest data indicates that there are about 466,000 British pensioners living in the EU. There are even more among the 5.5 million Brits living worldwide.

Even if you don’t plan on moving or buying a vacation home on some tropical beach, you might consider investing. Investing in real estate is one of the less risky methods for growing your fortune. Of course, the coronavirus crisis has heavily affected this industry. But there are still some very promising prospects for the residential housing market.

Also, today you’ll need to make international payments when booking your holiday accommodation. So, if you plan to travel at all, you’ll need to look for cheap money transfer solutions.

Anyone involved in international business also needs to make and/or accept international payments. This also includes the simple process of buying goods through one of the many e-commerce platforms.

In addition to those reasons, if you are an expat or a traveller, you’ll need to exchange money regularly. The same goes for dealing with transfers like inheritance or even accepting dividend payments from your investments.

All in all, living in the modern world makes you exposed to foreign currency exchange and transfers in many ways. Therefore, the knowledge of how to save money on these transactions is sure to be useful.

How Much Do Foreign Currency Transfers Cost in a Bank?

The cost of an international bank wire transfer is a very complicated issue. First of all, you need to understand that banks will advertise, and sometimes even show you, only the transfer fee. In the UK those range from £8 to about £40. That doesn’t seem too bad, especially for large transfers, right?

However, the truth is that banks are deceiving customers most of the time. If they were fully transparent, you would understand that what truly matters is the FX rate margin. That’s the amount that the bank charges per currency conversion on top of the mid-market exchange rate.

Simply put, high FX margins are why you lose so much money on currency conversions. Different banks use different margins and that’s why they offer different exchange rates. But if you compare the options offered by top UK banks, you’ll see that they are all very close.

Therefore, you don’t have much of a choice.

Also, there might be additional fees involved in a cross-border money transfer. The recipient bank might charge its own fees. If there are any intermediary ‘stops’ along the way, more fees will come.

All things considered, the real cost of an international money transfer can go up to 3-10% of the transfer amount. This cost will be higher for exotic currencies and transfers to remote locations. It will go down a bit for large transfers because banks might offer better terms to VIP clients.

However, the total will always be quite high.

Leading Money Transfer Service Alternatives From the UK

With bank transfer costs so high, a necessity for an alternative emerged. The solution came in the form of FX brokers and money-transfer companies. These businesses offer services similar to banks, but they have much lower overhead costs. Therefore, they are able to keep both the margins and fees very low.

In fact, many companies charge no transfer fees at all for the majority of transactions. However, they use different margins that often depend on the transfer size. Thus, you should always compare foreign currency transfers before choosing a service. This won’t be difficult as all top companies in the industry offer free quotes. They also have transparent pricing schemes.

On average, a transfer with one of these companies will cost you 1-3% of the total. Industry leaders even offer options that allow you to cut costs below 1% for large transfers.

The most notable UK-based FX companies today are TransferWise and WorldFirst. There are other notable businesses as well. However, they cannot compete with these two giants that have multi-million funding.

TransferWise

TransferWise launched not even a decade ago and it has already become a major disruptor in the banking industry. It took over the FX money transfer industry rather fast as well. The main selling point of this company was offering not merely cheap transfers but also a fixed margin scheme.

This means that TransferWise managed to offer its customers consistency and a chance to save a great deal of money. Because of the fixed margins, its services were the most affordable in the industry. The company is now valued at over $3.5 billion and it’s expanded to many countries, including the US.

WorldFirst

WorldFirst is another veteran in the FX transfer industry. This company built a solid reputation for its reliability and trustworthiness. Launched back in 2004 literally from a basement, WorldFirst became one of the industry leaders within a few years.

In 2019 this fintech business was purchased by Ant Financial of the Alibaba Group. This allowed WorldFirst to launch a major change in pricing. It had already been one of the top companies, but it could not compete with TransferWise in affordability. However, the new pricing scheme with fixed margins that go below 0.55% makes WorldFirst a cheaper alternative even to TransferWise. At the moment, there is no cheaper option for foreign currency transfers in the UK. Also, WorldFirst has a very wide reach due to its association with Alibaba, though it’s not yet available in the US.

In Conclusion: Do Your Research for Saving Money on Foreign Currency Transfers

FX money transfer companies today offer great opportunities for money saving. However, do not forget that the lowest cost doesn’t necessarily mean the best offer. These companies have a number of requirements and additional services that you should research. For example, some have a minimum transfer limit. Others offer FX hedging tools that will be essential for reducing risks for businesses and investors.

Thus, be sure to compare all options you have available and research them thoroughly. Watch out for scammers, and choose only those businesses that have a good standing in the industry.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m talking about the important subject of home security.

Obviously it’s not something anyone likes to think about, but the risk of being burgled is very real. It is estimated that a burglary is committed every 40 seconds in the UK (it’s impossible to give exact figures as many such crimes aren’t reported). That means in the time it takes you to read this article, four homes are likely to have been burgled.

Of course, there are certain precautions you can take to reduce the chances of becoming a victim yourself. These include:

Keep all windows and doors locked even when you’re at home.

Keep garages and sheds locked as well, especially if they contain tools or other items that might be useful to a burglar.

Try to vary your daily routine so that burglars (who often live nearby) don’t notice and take advantage.

Avoid mentioning holiday plans too widely (especially not on Facebook or other social media).

Install timers on lights so they go on and off in a seemingly random way while you are out.

Install security lighting that will detect visitors (invited or uninvited) and illuminate them.

These and similar measures can reduce the likelihood of a burglar targeting your property. But of course, they are unlikely to be sufficient alone. You need a burglar alarm, and ideally a complete home security system. Like this one, perhaps…

Boundary Smart Security

If you’re reading this blog, chances are you have a burglar alarm already. But especially if it was fitted a few years ago, it may not be as effective as you hope.

Older alarm systems are easily defeated by determined, professional burglars. And especially if you live in a nice house and have an expensive car or other signs of wealth, you could well be targeted by such individuals. You need a modern smart security system to provide both maximum protection from burglars and the peace of mind that comes from this.

Boundary aims to provide UK residents with state-of-the-art home security at an affordable price. Their new high-tech Boundary Alarm system is based around a central hub (see cover image, above) that wirelessly connects to each Boundary device in your home and allows you to control them from anywhere using a single smartphone app. It’s a sophisticated system that can still be installed by anyone and set up easily (though optionally you can pay for professional installation if you prefer).

You can customize your alarm system as you wish with door and window sensors that detect exactly when any door or window opens in your home and set off an alarm. You can also incorporate infra-red motion detectors (wireless and pet-safe) that will detect any human movement when you’re not at home. Other features include a key tag to easily arm and disarm the system when you’re coming and going, and a 95-decibel siren (pictured below) to alert your neighbours if your home is broken into.

Plans

Boundary offer four different plans, with no long term contracts, cancellation fees or hidden costs. Full details can be viewed on the Boundary website, but briefly they are as follows…

Lite – This is the lowest cost option, with no ongoing fees. It covers two users, two sensors, the Boundary app, smart home integration and Boundary Neighbourhoods (once this service is launched). The latter is a ‘neighbourhood watch’ dashboard to allow people in local areas to connect online to share details of crime and suspicious activity. You will have the option to link your Boundary alarm so that if it goes off, your neighbours will automatically be notified.

Starter – This includes all the features above and others, including push notifications when the alarm goes off, alarm-set reminders when you leave the property, occupied home simulation (requiring smart light bulbs), and so on. This plan costs £4 a month.

Plus – This includes all the features above plus an extended three-year warranty, automated keyholder calling, partial setting (e.g. downstairs only), and more. This costs £8 a month.

Complete – This also includes police response. When the alarm goes off, a security guard at an alarm receiving centre (ARC) will be automatically notified and will immediately verify whether your home is being burgled. If confirmed, the security guard will request a police response and notify the property owner and/or nominated key holders. The complete plan also includes an annual maintenance visit by an engineer. The cost of this plan is £25 a month. Note that with this plan professional installation is mandatory.

Boundary is still in pre-launch phase and right now you can get a voucher for £50 off the price of any system costing £450 or more just by signing up to their newsletter using the form on their website (screen capture below). There is of course no obligation to use this – but if you’re at all interested, I recommend signing up now to get your hands on the £50 discount code.

Self-install alarm systems are due to be sent out by the end of August, while for those who choose professional installation, the company say that currently they expect delivery and installation to take place in October.

You can ask for a no-obligation quotation via the website to get a price for a system tailored to your exact needs, with no nasty surprises further down the line. At the very least, if you think Boundary Alarm could be the answer to your home security needs, do sign up now for their email newsletter and £50 off voucher.

Note: This is a fully updated repost of my original article from April 2020.

Disclosure: This post includes my referral link, so if you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

As you probably know, during the initial coronavirus lockdown, buying and selling property was almost impossible.

As restrictions are slowly easing, however, house buying and selling has become feasible again. Estate agents have been reporting a big upsurge in enquiries, as the long period of confinement to home has made many people more aware of the shortcomings of their current properties!

Of course, buying and selling houses while the virus remains a threat requires risks to be mitigated as much as possible. That means wearing gloves and masks when meeting agents, buyers or sellers. Following the standard hygiene rules about hand-washing and using hand sanitizers before and after any personal meetings is also vital.

The New Normal

With the need for social distancing and other precautions to reduce the risk of transmitting the virus, valuing and viewing properties has become more challenging. Most agents now offer virtual viewings – generally using a mobile phone camera – as an alternative to personal visits.

Vulnerable customers: customers that fall under the ‘vulnerable’ group as advised by the government, should let their local Yopa agent know and will then be offered a virtual valuation or viewing until there is government advice that the safety of this group is no longer a concern.

Preference: we appreciate that not everyone will want a face-to-face meeting with a Yopa agent yet – in which case, we will happily offer a virtual alternative as we have successfully throughout lockdown to date. We will keep in touch with you to understand if your preferences change as more information is issued by the government on infection rates and virus control.

Travel: we would advise our customers, where possible, to restrict travel on public transport to attend a valuation or a viewing.

Minimise contact: we ask that, at a minimum, only the buyer or seller of a property is present at a viewing or valuation – no other parties. All non-Yopa attendees should be from the same household. We would advise that we conduct viewings and valuations without the vendor present.

Distance: When meeting with a Yopa agent on a valuation or a viewing, where possible stand at a 2m distance and refrain from shaking hands.

On the property:

Gaining access: For vendors, your Yopa agent will call you when you are outside the property to gain access. For buyers, please call your Yopa agent when outside the property to gain access.

Duration: Valuation and viewing time should be kept as short as possible to minimize risk.

Air flow: we politely request that all windows and doors are opened in advance of the valuation or viewing where possible, so the Yopa agent and vendor/prospective buyer can move through the property without touching door handles or surfaces.

Refreshments: whilst very kind of our vendors to offer, we politely ask that refreshments are not offered to our agents whilst on the premises.

Documentation: as we are a digital business, no paper documentation needs to be transferred between Yopa and our customers – it can all be managed electronically.

Post valuation or viewing: if people have been shown around your current home, you should clean down surfaces, such as door handles, after each viewing with standard cleaning that products.

Yopa say that vendors conducting their own property viewings should complete these in accordance with the recommendations above.

If you are thinking of selling your home, an online agency such as Yopa is well worth considering.

They offer a full service, and say they can do anything a traditional estate agent does. They are also open at evenings and weekends.

Yopa charge a fixed fee which is agreed in advance, and never add commission. You can choose to pay when your home is sold, or up-front if you prefer.

Although Yopa are website-based, they have local agents whom they say will be with you at every step until your home is sold. You can also monitor viewings, offers and feedback any time you wish using the YopaHub online dashboard.

Finally, other services offered by Yopa include help with mortgages and conveyancing (via their commercial partners). In addition, every homeowner gets a free utilities switching service.

Final Thoughts

If you’re considering moving, it’s definitely not too soon to get started and benefit from the pent-up demand from other would-be buyers and sellers.

So why not check out the Yopa website today and see if their service could be the one to help you make your next move and find the home of your dreams 🙂

As always , if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Yopa. It includes affiliate links, so if you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect in any way the service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

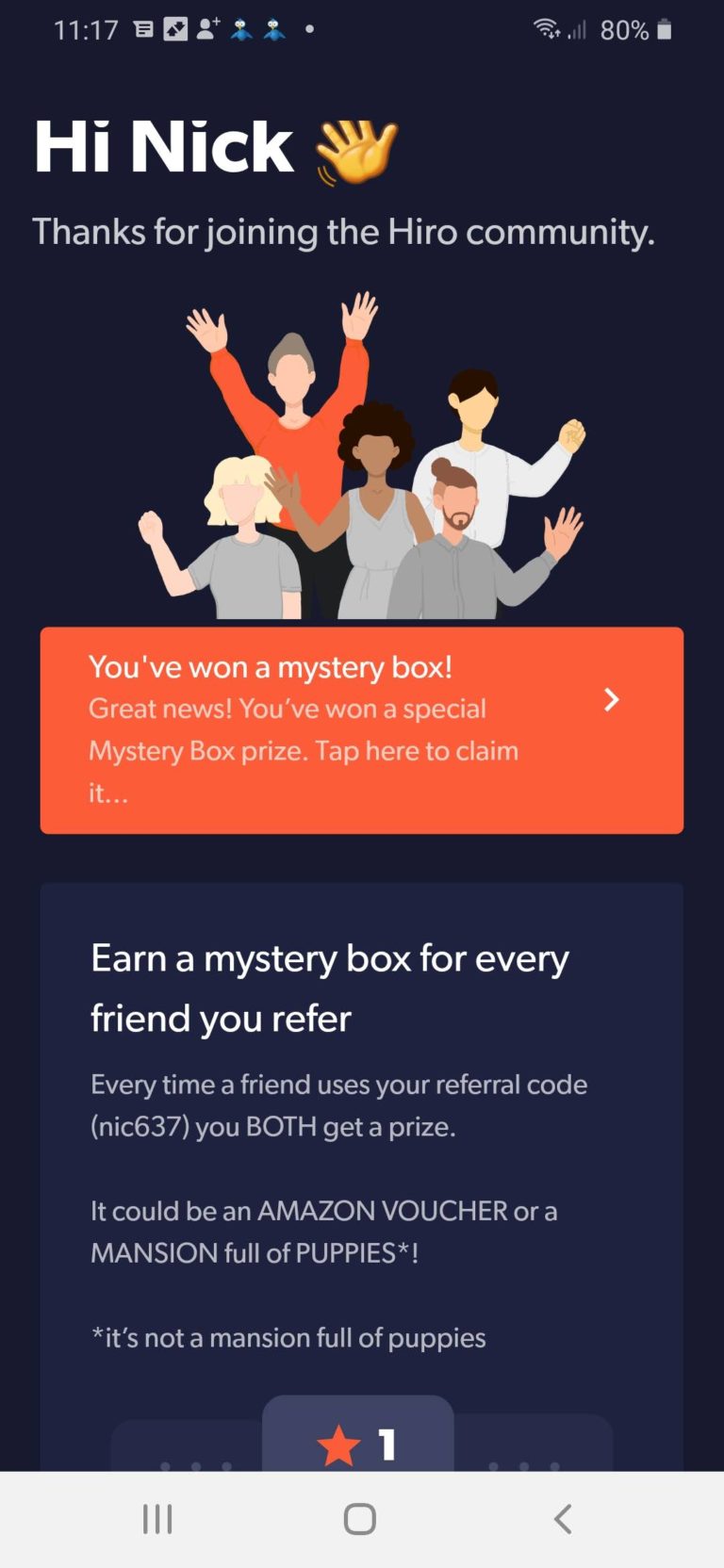

Hiro is a brand new new mobile phone app currently offering a range of incentives just for downloading it and answering a few quick questions about the smart tech you have in your home.

Hiro say that in future they plan to offer members personalized discounts on home insurance and similar products based on their home technology – from Amazon Alexa devices to smart thermostats, doorbell cameras to smart locks.

Right now, though, there is nothing to buy. They are simply looking to build a community of people who may be interested in saving money on insurance in future. And to do this they are offering gifts for downloading the app and signing up. These range from £5 Amazon gift vouchers to £5/£10 Hiro credits, and lots of other weird and wonderful things as well. Here’s how it works…

Grab Your Free Prize

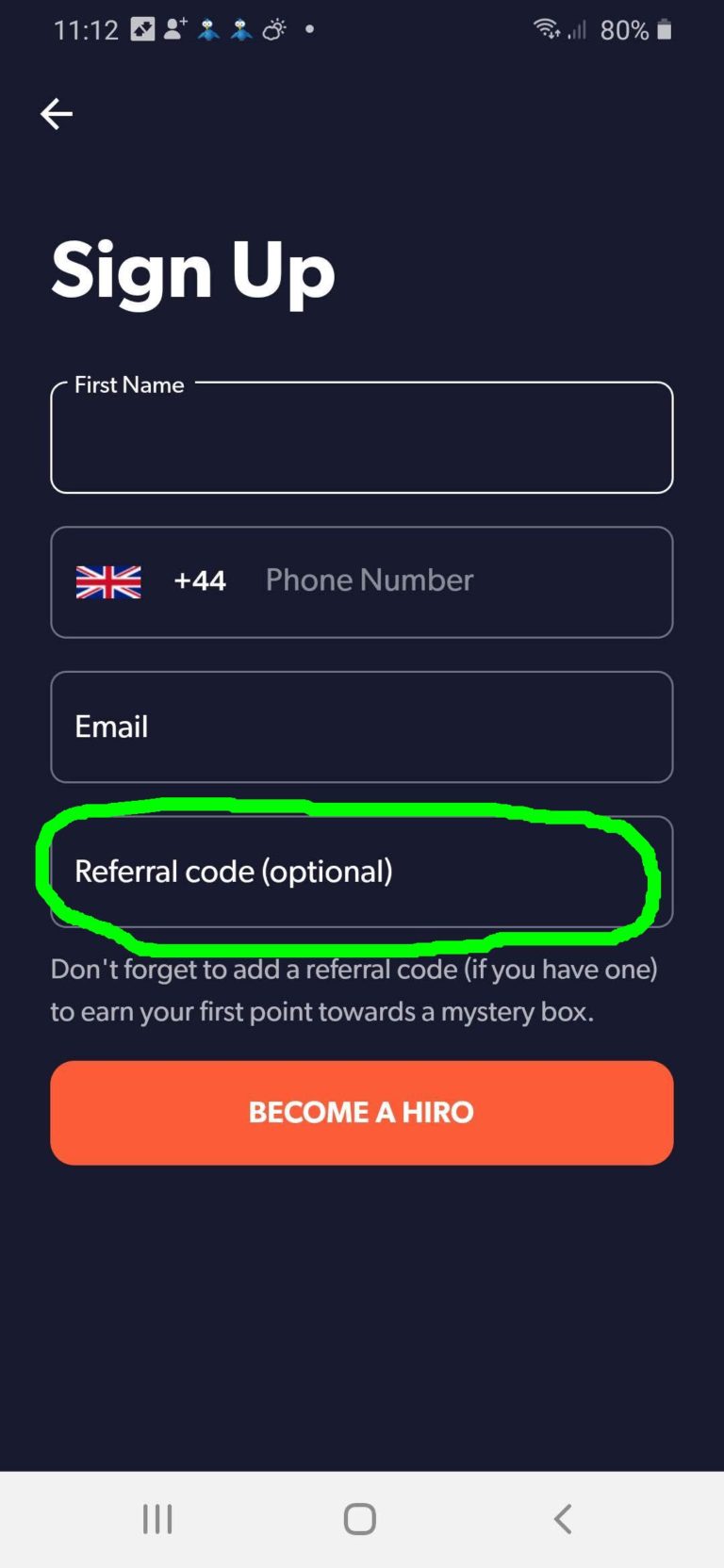

Start by downloading the Hiro app from Google Play or the Apple Store. Open the app and here is what you should see…

Enter your first name, (mobile) phone number and email address in the appropriate boxes. Where it says ‘Referral code’ (highlighted above) please enter nic637, then tap on ‘Become a Hiro’.

You will then be presented with a short questionnaire about your use of smart tech in the home. When I did this, the app told me that with my modest complement I would be eligible for a 17% discount on my home insurance. That’s nice to know, though of course it won’t mean much until Hiro start selling actual insurance.

They say as well that even if you don’t currently have any smart technology, they will be making recommendations and special offers, and explaining the extra discounts the tech in question can bring you.

In addition, once you’ve answered the questions, we will BOTH be eligible for a prize (or mystery box, as they call it). Here’s the screen you should see…

Just tap on the the orange box (see screen capture above) to see what you have won.

Of course, once you have signed up you will get a personalized link as well and be able to share this with friends and family. Any time someone signs up using your link, both of you will win a prize. As I said above, there is nothing to buy now and no obligation in future.

Good luck, and I hope you win something almost as exciting as a mansion full of puppies 🤣🤣🤣

As always, if you have any comments or questions about this post, please do leave them below..

Update 19th May 2020 – I have just heard that Hiro aren’t offering Amazon vouchers as prizes at the moment. Other prizes such as Hiro credits are still on offer.

If you enjoyed this post, please link to it on your own blog or social media:

Right now it’s difficult for savers and investors to know which way to turn. World stock markets have been in free fall, while bank and building society interest rates are at an all-time low.

Regular readers will know that I’m something of a fan of property crowdfunding and have invested through a number of such platforms (notably The House Crowd, Property Partner, Crowdlords and Kuflink). For anyone seeking half-way decent rates of return, I believe they represent an opportunity worth considering at least, especially in the current uncertain economic climate.

But before I come to that, a few words for those new to this field…

What Is Property Crowdfunding?

As the name says, in property crowdfunding a number of investors pool their money to invest in property and share in the returns pro rata to the size of their investment.

In the last ten years a number of property crowdfunding platforms have been launched to facilitate this. As well as publicizing such opportunities, these companies typically identify suitable properties, advertise and administer projects, and manage properties once they have been purchased. They also distribute payments due to investors from rent received and (eventually) from selling up. Unlike ordinary buy-to-lets, property crowdfunding projects are typically hands-off, passive investments.

There are various methods of property crowdfunding. The traditional method (if you can describe something that’s been around for under ten years as traditional) is equity crowdfunding. Here investors’ money is pooled to buy a house or larger property. Investors then (usually) receive rental income in proportion to the amount they invested plus a share of any capital gains when the property is sold.

The other main method is debt crowdfunding. Here investors lend money to a landlord or property developer so that they can complete a particular project. The money might be used for a bridging loan, or to make improvements to a property prior to selling or remortgaging it. In this type of crowdfunding, the investors never actually own the property. They play a role similar to a bank, lending money and (all being well) being repaid with interest once the project is concluded.

There are also development projects, where investors’ money is used to fund larger-scale property developments. This might involve building a new property (or properties) from scratch, or perhaps converting existing buildings to a new use. Either way, if all goes well, at the conclusion of the development the investors get their capital back along with interest. Development crowdfunding is riskier than equity crowdfunding, but the profits to be made can be bigger.

Property crowdfunding is a form of investment, and like all investments it carries risks. Clearly it’s not as safe as bank or building society savings (which are covered up to £85,000 by the Financial Services Compensation Scheme). All investments are though secured against bricks and mortar, so in the event of a borrower defaulting you should still get your money (or most of it) back once the property concerned has been sold.

The rates of return with property crowdfunding are significantly higher than those from banks and building societies, and they’re also relatively unaffected by fluctuations in the stock market. Property crowdfunding isn’t a way of hedging equity-based investments directly, but it does help spread the risk.

Property and the Coronavirus

These are undoubtedly challenging times for property investors, be they traditional buy-to-let landlords or property crowdfunders.

Even before the virus struck, property prices were at best steady or going down. And measures taken by the government in the last few years, including progressive cuts in mortgage interest tax relief and an additional 3% stamp duty on buy-to-let properties (dubbed ‘The Landlord Tax’) considerably reduced the attraction of buy-to-let for private landlords especially.

The coronavirus crisis has added a whole new layer of difficulty. In particular, measures taken by the government to mitigate the worst effects of the crisis have hit both tenants and property owners hard. Many tenants are obviously suffering financial hardship, and may therefore be having difficulty paying their rent (and other bills). Tenants are, though, currently protected from eviction, and landlords are required to provide rent holidays where appropriate. These measures are sensible and humane, but at a stroke they have reduced or cut entirely many landlords’ income streams, and there is no government scheme to assist them. Obviously I don’t expect many tears to be shed for landlords, but life has undoubtedly become a lot more challenging for them.

In addition, due to social distancing and the lockdown, only limited construction work is continuing. It’s also difficult (or impossible) for surveyors and valuers to do their jobs, or for potential buyers to visit and inspect homes and other properties. All of this means that to a great extent the UK property market has currently ground to a halt.

Despite that, it’s not all bad news. At some point – maybe quite soon – the lockdown restrictions will be eased. The government is (rightly) keen to get the economy moving again as soon as possible. And there are still plenty of people looking to move home, buy property, begin new development projects, and so on. Much as the depressed state of the stock market has presented opportunities for those willing to take a chance on buying now while prices are low, there is certainly a case that property will bounce back in the coming months and years too, rewarding those who invest in the sector now.

Property Crowdfunding Opportunities

Clearly property crowdfunding investors are not immune to the effects of the coronavirus crisis. Developments and sales have been delayed, and in some cases at least rental income has been reduced. It’s quite possible – likely even – that in the longer term the rate of defaults on loans will go up too.

Nonetheless, property crowdfunding investors are unlikely to be as badly affected as private landlords. For one thing, if they are sensibly diversified across a range of properties (and platforms) they won’t be as susceptible as someone with a single buy-to-let. And like all property investors, their money is secured by bricks and mortar, so they will get it back (or most of it) eventually – though in the current crisis, that might take some time. For most property crowdfunding investors at the moment, sitting tight is likely to be the best (or only) option.

As I said above, the crisis is also creating opportunities for those who believe that property will prove to be the resilient investment it has generally been in the past. Rather than prolong this post too much, I will focus my attentions on the four platforms I am currently invested in, and which I am therefore most familiar with.

Property Partner

Property Partner is an interesting case. They have just announced that they are suspending all dividend payments for the next three months (potentially longer). This is, of course, mainly money from rent received, which (for reasons stated above) is likely to take a hit in the coming months. Property Partner say they are taking this action to ensure that investors are protected in the longer term and all properties have sufficient cash reserves to cover any necessary expenditure.

As I said in this post a few months ago, many of the properties on Property Partner are coming up to their five-year anniversaries. This is a significant milestone, because after a property has been owned for five years, all investors have the chance to exit at a fair market price (determined by an independent surveyor). Property Partner have said they are suspending this process until June at the earliest.

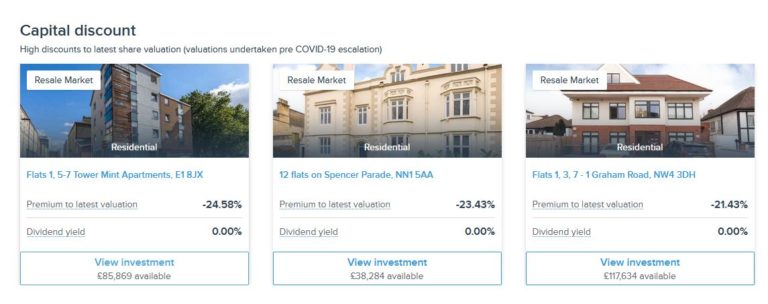

You can still buy and sell properties on Property Partner’s secondary market, and on the face of it there are some good-value buying opportunities here, with properties listed at up to 25% off their current valuations (see screen capture below).

In theory, you could buy shares in these properties on the secondary market at a big discount, and sell them at their current valuation for a good profit when the five-year sale process is reinstated.

Unfortunately it’s not quite a straightforward as that, though. For one thing, the current valuations were made before the coronavirus crisis hit, so they may no longer be an accurate reflection of a property’s value. In addition, the five-year exit mechanism depends on other investors wanting to buy the shares at the valuation stated. Failing that, the property will be sold on the open market, but that could take a long time in the current economic climate. Neither is there any guarantee what price would be achieved.

My personal view is that I do believe property prices will bounce back but it may not be for quite a while. I am looking seriously at some of the buying opportunities on Property Partner’s secondary market where I think they represent good value in the medium- to long-term, but I am not rushing to invest at the moment.

Kuflink is another property crowdfunding platform I have a soft spot for. Although I don’t have huge amounts invested with them, so far all of my investments have paid out as promised, with just a short (one-month) delay in one case.

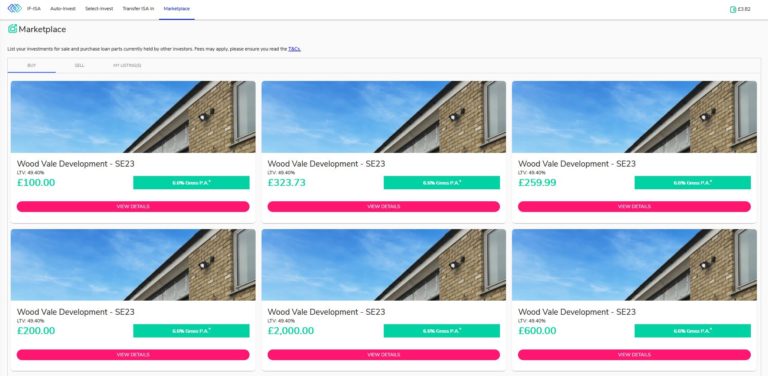

Kuflink is a property loans platform. So far anyway I have not heard of any defaults, although the longer the crisis continues, the greater the risk this may happen. Nonetheless, based on my experiences to date, I am continuing to invest (cautiously) with them. In particular, I like their new secondary market, where you can buy loan parts from other investors who want to sell up early (see screen capture below)

As you may imagine, this has been happening a lot recently, as many investors have wanted (or needed) to access their capital urgently. This has created short-term buying opportunities which I have been busily taking advantage of. These loan parts typically have only a few months to run, so you can expect to get your capital back quite quickly (and can then reinvest it). Only loans in good standing with monthly repayments up to date may be listed on the secondary market, so that offers some reassurance against default – though of course it is by no means a guarantee.

Secondary market aside, Kuflink also still has a steady stream of new investment opportunities coming to the table. Of all the property platforms, they appear to be the ones least affected by the current crisis. I am not exactly sure how they have achieved this, but obviously I hope they continue to do so!

If you haven’t invested in Kuflink before, it’s also worth mentioning that they have a generous welcome offer which is still operating. You can earn up to £4,000 in cashback with this. See my Kuflink review for full details.

The House Crowd

The House Crowd is actually the first property crowdfunding platform I invested with. My experience with them has generally been good, although as mentioned in my House Crowd review there have been some delays and defaults.

Although they started as a traditional crowdfunding platform, The House Crowd have increasingly moved towards development projects, and these have inevitably been hit by the current crisis. THC say that at present they are following a strategy of ‘prudently maintaining The HouseCrowd platform to ensure its continued and efficient operation as we see our way out of the other side of the lock down.’

That means there are fewer investment opportunities on THC at the moment. You can though if you wish still invest in their automatically diversified ‘Auto-Invest’ products, with target interest rates of 5% (Cautious) to 7% (Bold), or the new THC Fusion account, which offers even greater diversification with a target interest rate of 4% to 4.5%. More information about these can be read on the House Crowd website.

At the time of writing THC also have a couple of development projects open for investment, including their flagship project The Downs in Altrincham town centre, paying a target rate of 10% per year (see screen capture below).

Finally, Crowdlords say they have experienced a significant reduction in investment levels since February, which they put down to uncertainty caused by the pandemic. They do still have a couple of lending opportunities listed (see capture below), but not much else. I guess like The House Crowd they are hunkering down and waiting for the current restrictions to be lifted and the property market to start moving again.

Again, I am not currently planning to invest any more in Crowdlords, but am keeping an eye on any opportunities that may crop up in the months ahead. You can read my full review of Crowdlords here.

Final Thoughts

I thought I’d close by sharing a couple of nuggets of information I found while researching this post.

First, the ratings agency Fitch has downgraded the rating of UK debt to AA-. However, Fitch estimated growth next year would bounce back to 3 percent if the UK can begin to unwind the measures to tackle the health crisis in the second half of the year. The UK’s Coronavirus Job Retention scheme – a three-month programme to support employees hit by the pandemic – will cost about 1.3 per cent of GDP, according to Fitch estimates.

Second, estate agents Knight Frank have predicted that many house sales will be lost this year and the UK’s property market will see little to no growth in 2020. However, a sharp recovery has been predicted for 2021. Liam Bailey, global head of research at Knight Frank, said, “We expect a revival in activity to continue, with volumes next year expected to be 18 per cent above the level seen in 2019.”

All of this (and other sources) suggests that while property markets are in the doldrums now and probably for most of 2020, there is every chance that by next year we will see a recovery. There are undoubtedly good opportunities on offer in property investment now if you agree with this evaluation and are able to be patient in the shorter term.

In any event, if you’re looking for better returns than the banks and lower volatility than the stock markets, then property generally – and property crowdfunding in particular – remains in my view well worth considering as part of a balanced investment portfolio.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I am not a regulated financial adviser and nothing in this post should be construed as individual financial advice. You should always do your own ‘due diligence’ before investing, and seek independent financial advice if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I am something of an enthusiast for property investment (and specifically property crowdfunding). Among other things, I like the fact that you can make money from both rental income and capital growth. And investing in property can be a good way of spreading risk when you have equity-based investments.

The House Crowd was actually the first property crowdfunding company I invested with, starting in 2014. So I thought I would say a few words today about my experiences with the company and the investment opportunities they offer.

History

When I started investing with The House Crowd, they were offering mainly shares in specific properties. Investors pooled their money to buy a property and received a share of the rental income (distributed annually) with their money back – and hopefully a good profit – when the property concerned was sold. Typically a five-year timescale was specified, with investors then able to vote on whether to sell and take their profits or continue for another year (or more).

I still have shares in seven House Crowd properties. There haven’t been any disasters, though in certain cases rental income has been lower than forecast. This was typically due to voids (tenants leaving and not being replaced). There were also a few cases of tenants failing to pay their rent and absconding. And there was one ‘tenant from hell’, who apparently threatened other tenants with a knife so they all left, caused serious damage to the property, and left owing six months’ rent. Reading about this made me glad I invest via property crowdfunding platforms (and REITs) and am not a landlord myself.

One drawback of this type of investment is that it is quite illiquid. If you want your money back before a property is sold, The House Crowd will try to sell your share to another investor. There is no guarantee a buyer will be found, however, and even if one is you will only get the price you paid for your share. There is currently no formal secondary market, as on some other platforms such as Property Partner.

On the plus side, this sort of investment has its attractions from a tax perspective. Rental distributions are paid as dividends. There is currently a £2,000 annual tax-free dividend allowance which many people don’t otherwise use. And even if your dividend income exceeds £2,000, as a basic rate taxpayer you will only pay 7.5% tax on the balance above this. Gains when selling are – of course – treated as capital gains, and again there is a generous annual tax-free CGT allowance (£12,000 in 2019/20).

New Types of Investment

In recent years, recognizing that some investors were being deterred by the lack of liquidity, The House Crowd have introduced other types of investment. One of these is secured loans. Here money is lent to developers (or THC’s sister company, House Crowd Developments) for short- to medium-term projects, typically between 6 and 18 months.

Obviously you don’t get rental income with these, but you get your money back with interest once the loan is paid off. Interest rates vary, but are typically in the region of 7 to 12% per year. The rate paid generally depends on the LTV (loan to value). The higher the LTV (the loan amount compared with the property value), the riskier the loan, and the higher the interest rate on offer as a result. Some example projects open for investment at the time of writing can be seen in the cover image at the top of this post.

I have invested in loans with The House Crowd as well. The majority have gone well. For example, I invested £5,000 in a development loan for a Welsh property called Croesyceiliog Farm. I got this back with £461.99 interest ten months later.

Other loan investments haven’t gone as smoothly. For example, in 2016 I invested £1,000 in a loan for a property called Caverswall Castle. This was meant to be 12-month loan, but the borrower defaulted and legal action is now being taken to sell the property and repay investors. I still expect to get my money back eventually, but legal proceedings move at a glacial pace. How much interest I will get after all costs are covered I don’t know. At this stage, if I just get my £1,000 back, I will be more than happy.

Secured loans have various attractions for investors, and many property crowdfunding platforms as well as The House Crowd are now offering more opportunities of this nature. They have the advantage of shorter timescales than direct investment and decent rates of return (assuming the borrower doesn’t default). One drawback is that the interest paid when the loan is redeemed is treated as income, so you will have to pay tax on it at your highest marginal rate.

Auto-Invest and IFISA

In recent years The House Crowd have introduced an Auto-Invest product which you can (optionally) hold as an Innovative Finance ISA (IFISA).

As you may know, IFISAs offer the opportunity to invest in P2P lending and get tax-free returns. Everyone has a generous annual ISA allowance of £20,000 (in the current 2019/20 tax year). This can be divided any way you like among the three types of ISA. So if you open a House Crowd IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. Note that you can also only invest in one ISA of each type per financial year.

The House Crowd Auto-Invest product allows you to invest in one of three investment portfolios: Cautious, Balanced or Bold. Each of these comprises a basket of bridging and development loans, providing automatic diversification. The Cautious product has a target return of 5%, the Balanced 6%, and the Bold 7%. Note that these are target rates and they are not guaranteed. I have copied a summary table about the three products from the House Crowd website below .

As you can see, the more ‘adventurous’ the product, the higher the average LTV and the higher the maximum LTV. As mentioned earlier, the higher the LTV (other things being equal) the riskier the loan, and the higher the interest rate on offer as a result.

There is a minimum investment of £1,000 and a minimum 12-month term. After that you can withdraw by giving 30 days’ notice. Your money is protected by a legal charge secured against the borrower’s land/property, which can be possessed and sold in the event of the borrower not repaying.

It is possible to transfer another ISA to the House Crowd IFISA free of charge if it is over £5,000 (there is a £50 transfer fee for ISAs valued from £1,000 to £4,999).

Pros and Cons

As usual, here is my list of pros and cons for The House Crowd.

Pros

1. Well-established property crowdfunding platform with a good track record.

2. Customer service is fast, friendly and helpful.

3. Choice of investment types.

4. Tax-free IFISA option available.

5. Competitive rates of interest.

6. Attractive, user-friendly website.

7. Detailed information provided about loans and investments.

Cons

1. Limited liquidity with no formal secondary market.

2. Rental income (where applicable) only distributed annually.

2. Minimum £1,000 investment.

3. Some loans are currently in default.

4. Can’t open an IFISA if you have already put money in another IFISA this year.

Conclusion

For the most part I have been happy with my experiences with The House Crowd to date. Although (as mentioned above) there have been ups and downs, overall I have still made a good net return from my investments with them.

I like the new Auto-Invest/IFISA option, which is automatically diversified across a range of loans (thus reducing volatility and risk). The minimum 12 month term and withdrawal on 30 days’ notice thereafter is attractive as well. It is, however, important to be aware that the target rates of return quoted are not guaranteed.

You should also bear in mind that investments with The House Crowd do not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme. All investments are though secured against bricks and mortar, so in the event of a borrower defaulting you should still get your money (or most of it) back once the property has been sold. But obviously, this may take a while.

The lack of liquidity with property investments generally – and the absence of a formal secondary market with The House Crowd – means you should only invest money you are unlikely to need at short notice. This should be regarded as a medium- to long-term investment, therefore.

Clearly, no-one should put all their spare cash into The House Crowd (or any other investment platform). Nonetheless, it is worth considering as part of a diversified portfolio. Not only are the rates of return significantly higher than those offered by banks and building societies, they are relatively unaffected by fluctuations in the stock market. Property investments aren’t a way of hedging your equity-based investments directly, but they do help spread the risk

A further consideration is that with world stock markets in chaos at the moment due to the coronavirus outbreak, now is probably not an ideal time for the average individual to be investing in stocks and shares. P2P lending of the type offered by The House Crowd represents an alternative investment approach that may be less susceptible to the wild ups and downs (mostly downs) on stocks and shares right now..

Welcome Offer

Unfortunately at present there is no welcome offer (or referral scheme) for new investors with The House Crowd. If a welcome offer is launched in future, I will of course post full details here.

If you plan to open an account with The House Crowd after reading this review, I’d still be grateful if you could let me know by sending a message via my contact form or leaving a comment on this post. This may help me persuade THC to set up a referral scheme and/or welcome offer in future 🙂

And of course, if you have any comments or questions about this review, as always, please do leave them below.

Note: This is a fully revised and updated version of my original 2017 review.

Disclosure: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. All investments carry a risk of loss. Finally, in the interests of full disclosure, I should reveal that as well as being an investor with The House Crowd, I also own shares in the company.

If you enjoyed this post, please link to it on your own blog or social media:

I recently booked my first ever break with Airbnb.

Of course, I’ve been aware of this person-to-person accommodation booking platform for some time, but till now I’ve avoided using it myself. In the back of my mind were stories I read years ago about people renting out sofas in their living room to make a bit of extra cash. At my age that prospect – the sofa in the living room, I mean – definitely didn’t hold any appeal!

Times change, though, and it’s important to keep up with them. In my case I wanted to book a short break in a part of North Wales that isn’t well served by hotels, the Lleyn Peninsula. Okay, I could have stayed at the Haven Holidays Park (formerly Butlins) in Pwllheli, but I was pretty sure that wouldn’t be my cup of Welsh tea either.

So after researching the relatively few hotels in the Abersoch area where I wanted to stay using Booking.com (affiliate link), I decided it might be time to give Airbnb a try. In recent years, as regular readers will know, I have become more accustomed to booking self-catering accommodation for short breaks, and have realised that in some ways I prefer this to staying in hotels.

In this blog post I thought I’d share my experience of registering with Airbnb and finding and booking accommodation. I hope this might inspire you to try it yourself if you haven’t yet taken the plunge with Airbnb.

Of course, you can also become an Airbnb host and make money that way. I haven’t tried this myself, but did cover the subject in another blog post titled Boost Your Income by Renting Out a Room.

Registering with Airbnb

Before you can make a booking with Airbnb, you have to be registered on the website. You can still browse without joining but (as I found out) if you find somewhere you like available on the dates you want, you will have to go back and register and then start the whole process again. This is a frustrating waste of time. It’s free to register and doesn’t take long, so if there is any chance you might want to book through the platform, my advice would be to do this first.

Registering with Airbnb is similar to registering on other booking websites. One thing to be aware of, though, is that as well as your personal details, as proof of ID they also ask you to upload a scan of an official document such as your passport or driving licence with your photo on it. Once you have done this, you have to wait for your ID to be approved. In my case this happened within 15 minutes and I received notification by email.

Once you’ve done all that, you can start searching for your perfect holiday retreat!

Searching Airbnb

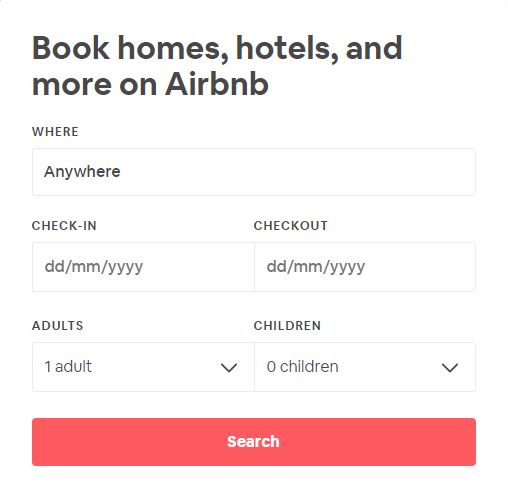

Once you are logged in, you can start your search using the box on the Airbnb front page (see below).

As you can see, you have to enter where you wish to go and the dates you want to arrive and depart. You have to choose specific dates, even if (as I was) you are flexible about this. Once you have found somewhere you like, you will be able to see what other dates that accommodation is available. If you want to check all possible places in the area, though, you may need to do a few searches using different dates.

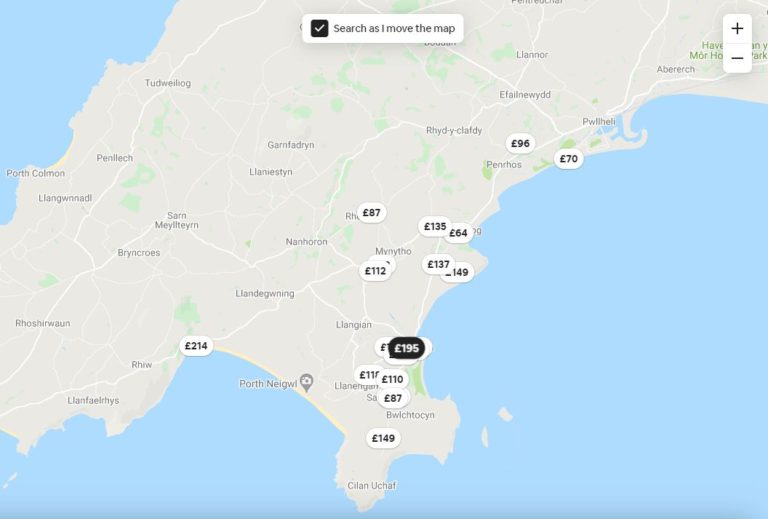

Anyway, once you have entered the relevant details and clicked on search, a new page will open showing you a map of the area in question. Here’s what I got when I searched just now for accommodation near Abersoch in early May (not actually when I am going).

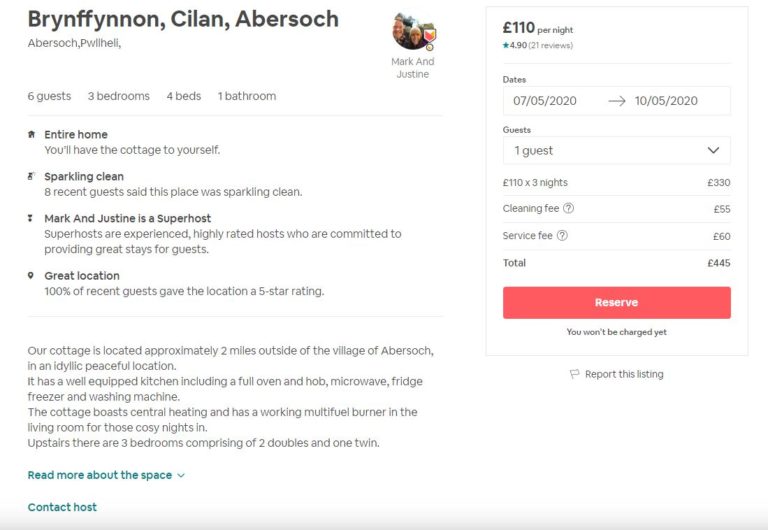

As you may gather, each of the prices in a small oval represents an Airbnb place with availability on the dates in question. The price is the cost per night. Clicking on any of these will bring up brief info about the accommodation in question. If you like the look of this, clicking again will bring up a new page with photos and more. Here’s the top of the page for a cottage I like the sound of, though it would be too large for me alone.

Also on this page are full details about the accommodation and a reservation form – see below.

As you can see, for your money you are getting considerably more than a sofa in someone’s living room 😀 £110 a night seems very reasonable to me for a cottage that can accommodate a family of six.

As you may have noticed, there are some additional charges. Many Airbnb properties – though by no means all – charge a cleaning fee. In addition, you will always be charged a service fee. This goes to Airbnb, and is one way they make their money (they also charge a fee to the property owners).

If you scroll down you will see various other items, including visitor reviews and a calendar showing when the property is (and isn’t) available. Also towards the bottom of the screen you will find the cancellation terms. These are set by the hosts and vary considerably, so be sure to study them carefully. Often you will be able to cancel free of charge until a certain date. After that, you may have to pay the service charge and perhaps part or all of the booking fee as well.

Making Your Booking

If you want to proceed, clicking on Reserve will take you to a new page where you can confirm your booking and provide payment information. This is pretty standard, although one thing you don’t normally have to do on hotel booking sites is write a message of introduction to the property owners (your hosts).

Airbnb provide a ready-written message you can use by default. This is pretty bland, however. I think it’s best to take a few minutes to write something more personal about who you are, why you want to visit the area, and so on. This is especially important if you are new to Airbnb and don’t have any history on the site or reviews written about you (yep, Airbnb hosts review guests as well as vice versa). In theory a host can decline your booking if they don’t like the sound of you, so it’s good to reassure them that you are a normal human being and will treat their property with respect.

And that’s it, basically. When I made my booking it all went through smoothly and I received a thank-you message from the hosts within an hour. I haven’t been on the holiday yet, but will post a review on this blog after my return.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Please be aware that this is a historical post. Bricklane is now closed to new investors and is winding down. Please see the comments below for the latest updates about it.

Today I am looking at another property investment platform, Bricklane.

Unlike Kuflink and Ratesetter, both of which I have discussed previously on this blog, Bricklane is not a platform for peer-to-peer loans. Neither does it arrange crowdfunded investments in specific properties like Crowdlords and Property Partner.

Bricklane is structured as a Real Estate Investment Trust, or REIT for short. For those who don’t know, REITs are property funds that use investors’ money to buy (and manage) property and provide returns in the form of rental income plus capital appreciation.

In order to qualify as a REIT in the UK, companies have to meet certain requirements. The most important are as follows:

At least 75% of their profits must come from property rental.

At least 75% of the company’s assets must be involved in the property rental business.

They must pay out 90% of their rental income to investors.

In exchange for operating within these rules – and to encourage investment in UK real estate – REITs are not required to pay corporation or capital gains tax on their property investments. That helps make REITs profitable for the companies running them, and is how they are able to generate attractive returns for investors.

Normally rental income from REITs is treated as taxable income and taxed at your highest marginal rate. However, if you invest through an ISA or SIPP (Self Invested Personal Pension) no tax is due. You therefore get the best of both worlds – your money isn’t subject to taxation while invested in the REIT, and when it comes back to you in the form of income distributions and profits on sales of shares, you don’t have to pay tax on these either.

Types of Investment

You can invest in Bricklane as a stocks and shares ISA or a SIPP, or failing that in a standard investment account, where you will be liable for tax.

To maximize the benefits from investing in a REIT, I highly recommend going down the SIPP or ISA route, if you haven’t already used up this year’s allowance. As a reminder, everyone has a £20,000 annual ISA allowance (for 2019/20) and you are also only allowed to invest in one cash ISA, one stocks and shares ISA and one Innovative Finance ISA (IFISA) in any one tax year. I invested in a stocks and shares ISA with Bricklane myself.

Bricklane has two property portfolios you can invest in. These are Regional Capitals, which includes properties in Birmingham, Manchester and Leeds. and London, with a portfolio of properties in the capital. The Regional Capitals portfolio has generated a return of 19.3% since it was launched in September 2016 and the London portfolio 8.9% since its launch in July 2017 (figures from the Bricklane website).

As a Bricklane investor, you can choose to invest in either or both portfolios, in any proportion you choose. I opted to put all my money into Regional Capitals, as I believe this is where the biggest growth potential lies. In addition, rental income in this portfolio is higher, and I am also concerned about the possible impact of Brexit on London. You might see this differently, of course!

Bricklane Pros and Cons

Based on my experiences so far – and some online research – here is my list of pros and cons for the Bricklane property investment platform.

Pros

1. Fast, easy sign-up.

2. Well-designed, intuitive website.

3. Low minimum investment of £100.

4. Bricklane take care of all the work involved in buying and managing properties. You just choose which portfolio/s to invest in.

7. Possibility to access your money at any time (though this does depend on another investor being willing to buy your shares).

8. Customer service (in my experience anyway) is fast, friendly and helpful.

9. Charges are reasonable, comprising an initial 2% fee (though see my comment below on how you may be able to offset this) and 0.85% annual management fee.

10. Potential to profit through both capital appreciation and rental income.

11. Rental income is paid into your account every three months. You can either withdraw it or reinvest it to compound your returns.

12. Up to £1,500 cashback is available for new investors of £5,000 or more via my referral link (see below).

Cons

1. No detailed information provided about the properties your money is invested in.

2. Can’t invest in an ISA if you have already put money into another stocks and shares ISA this year.

3. 20% tax deduction from rental income at source if you don’t invest via a SIPP or ISA (and additional liability if you are a higher rate taxpayer).

4. Minimum £10,000 investment for a SIPP.

5. Returns over the last few months have been disappointing (see below)

6. No absolute guarantee you will be able to sell your shares when the time comes.

My Experiences

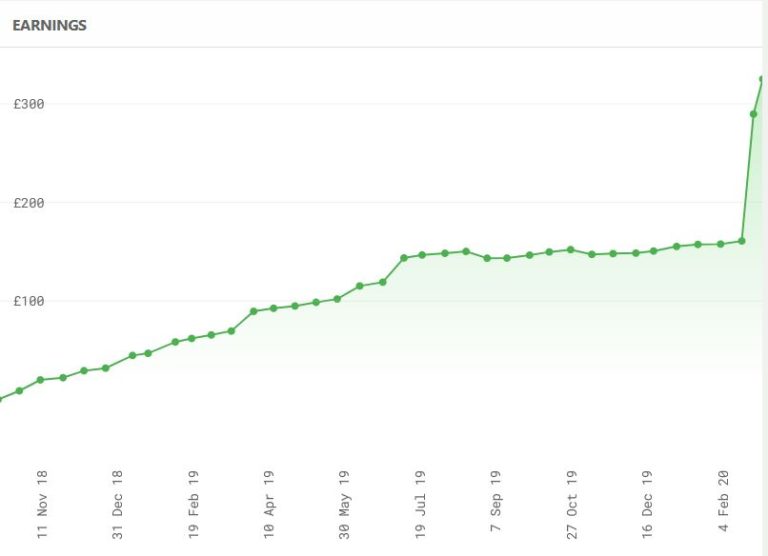

I put £5,000 into a Bricklane Stocks and Shares ISA in October 2018. As mentioned above, I chose to invest in the Regional Capitals rather than the London portfolio. The graph below – taken from my member’s page – shows the earnings generated since I opened my account.

As you will see, initially my investment performed pretty well. In the first nine months I made about £150, which equates to an annual interest rate of 4% (tax-free). That’s not spectacular, but it still beats most bank and building society accounts by a considerable margin. It is similar to the top rate currently on offer with P2P platform RateSetter in their Max account, although in their case you have to pay a fee equivalent to 90 days’ interest if you wish to withdraw. There is no withdrawal fee with Bricklane.

Since July/August 2019, however, returns have diminished considerably. My earnings between August 2019 and February 2020 were only just over £7, which is clearly a very low percentage rate. Of course, a large part of this is down to the depressed state of the property market caused by uncertainty over Brexit. I am hoping that now this is definitely happening – for better or for worse – my investment will get back on an upward trajectory again. Although recent results have been disappointing, at least the overall value of my portfolio hasn’t gone down (which has happened with some of my other property-related investments).

One other thing I should mention is that in October 2019 I withdrew £1,000 from my account to help fund a new central heating boiler after the old one packed in. This has therefore also reduced my returns a little. Although even if I still had the full £5,000 invested, earnings over the last few months would still have been nothing to write home about.

I should add that the withdrawal in question proved straightforward, although it wasn’t instant. I received the money in my bank account about a fortnight after putting in my request.

Conclusion

Clearly the performance of my Bricklane portfolio since last August has been disappointing, though overall I am still better off than I would have been if I had kept my money in a bank or building society.

I am hoping that things will start to improve in the property markets now that the Brexit issue has been resolved. There are some signs of this, although it remains to be seen whether the recovery in property prices will be sustained. For the time being, then, I am sticking with what I have in Bricklane, though I am not planning to top up my investment with them currently.

More generally, my experiences with Bricklane have been good. The sign-up process was fast and simple, and my £125 referral bonus (see below) was credited to my account instantly, completely offsetting (with a bit to spare) the initial 2% charge.

I also like the fact that any investment with Bricklane is automatically diversified across a range of properties, thus reducing volatility and risk. By contrast, with many P2P loan and property crowdfunding platforms, you invest in one loan or property at a time.

It’s also reassuring that you can ask to withdraw your money at any time – this can be an issue with property crowdfunding platforms in particular. As mentioned earlier, this does depend on someone else being willing to buy your shares, but Bricklane say that to date there hasn’t been a problem for anyone wanting to sell. As I said above, I had no issues when I wanted to release £1,000 from my own investment with them.

It is important to note that this is an investment rather than a savings account, and it does not therefore enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme (FSCS).

Clearly, no-one should put all their spare cash into Bricklane (or any other investment platform). Nonetheless, in my view it is worth considering as part of a diversified portfolio. Not only are the rates of return (other than the last few months) higher than those offered by most banks and building societies, they are less affected than shares by ups and downs in the stock market. Property investments aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

In addition, the tax treatment of REITs make them a highly tax-efficient investment, especially if you can invest in the form of a SIPP or an ISA.

Welcome Offer

As an existing Bricklane investor, I can offer a special cashback deal for anyone signing up and investing on the platform via my link. If you click through this special invitation link, sign up and invest a minimum of £5,000, you will receive £125 in cashback (and I will get £100). With a £5,000 investment this bonus will cover your initial 2% charge and still leave you £25 in profit 🙂

If you invest more, you will get even more cashback, as follows:

Over £10,000 – £250

Over £20,000 – £500

Over £50,000 – £800

Over £100,000 – £1,500

Not only that, once you are an investor with Bricklane, even if you only start with £100, you will be able to offer the same cashback bonus to your friends and relatives and earn commission yourself as well. There is no limit to the number of people you can introduce through this scheme.

Obviously, this is a generous promotional offer by Bricklane and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

If you have any comments or questions about this Bricklane review, as always, please do leave them below.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed.

Note: This is a fully revised and updated version of my original Bricklane review from October 2018

UPDATE15 March 2020: Having said that my earnings from my Bricklane ISA over the last 6-8 months were disappointing, since the start of February they have shot up by over 100% (see below).

This doesn’t exactly cancel out the recent falls in my equity-based investments due to the coronavirus, but it does demonstrate the value of having a well-diversified portfolio. And I am obviously feeling more positive about Bricklane as an investment platform now 🙂

One other thing to note is that until the end of April 2020 Bricklane are waiving all investment fees for both new and existing investors. Visit the Bricklane website for more information.

If you enjoyed this post, please link to it on your own blog or social media:

One question I get asked fairly frequently as a money blogger is what I think are the best current investment opportunities.

I have to be very careful when responding to this sort of question (and always tell people this). For one thing, I am not a qualified financial adviser, so it would be against the law for me to offer personalized investment advice. And even if I were, I still wouldn’t be allowed to give one-to-one advice without first doing an in-depth fact-find on the person in question.

Of course, this is exactly as it should be. For one thing, everyone’s circumstances are different, and what represents a good investment for me might not be the same for you. It depends on a wide range of factors, including your income and expenditure, your family responsibilities, how much you want to invest, the timescale (and purpose) you are investing for, your age and health, and so forth.

Another important consideration is your attitude to risk. Other things being equal, higher returns come with higher risks. If you’re comfortable with this and willing to accept it in exchange for the chance of better returns, that is of course your decision. On the other hand, if riskier investments would cause you sleepless nights, you are probably better off seeking a safer – if possibly less exciting – home for your money.

In addition, anything I say here is inevitably based on my own experience, and there is no guarantee yours will be the same as mine. I might, for example, have great success with one platform and suffer losses on another. But there is no way of knowing whether your experiences if you invest will be the same as mine. This applies especially if you have to choose specific investments on the platform (as with many P2P/property crowdfunding platforms) rather than putting your money into a pooled fund of some kind.

And, of course – as the financial services ads always say in the small print – past results are no guarantee of future performance…

I don’t want to come across as too negative. I am, after all, a money blogger and investor myself. So what I can – and will – do is talk about my own investing experiences and share information about what has worked well for me this year. It’s then up to you to decide if you want to investigate these opportunities any further. If so, you will need to do your own ‘due diligence’ before deciding how to proceed, perhaps taking professional advice from a qualified financial adviser as well (which I strongly recommend if you are new to investing or at all uncertain).

Although I count myself as a reasonably experienced investor, I do still have an independent financial adviser (Mike from Integrity Wealth Solutions). He oversees about half my investments, while the other half I look after myself. He also advises me on my financial situation more generally and answers any questions I can’t answer satisfactorily myself. i will talk more about this in another post. But I wanted to mention it here to show that I am not at all opposed to using a financial adviser and in general recommend it, particularly when starting out in investing.

My Best Investments of 2019

Below I have listed some of my investments that have performed best this year and/or caused me the least stress and hassle! I have included a few lines about each one, and links to any blog posts I have written about them for further info.

(1) Nutmeg

Nutmeg is a robo-advisory platform. I have used it for my Stocks and Shares ISA investments over the last three years. My investment pot has grown steadily, albeit with a few ups and downs, as is to be expected with equity-based investments. At the time of writing my Nutmeg pot has grown by about 40% since i started investing in April 2016, which is certainly a lot better than I could have achieved with a bank savings account. Of course, you shouldn’t normally invest in any equity-based product with anything less than a five-year timescale.

Nutmeg use exchange-traded funds (ETFs) as their investment vehicle. These are discussed in more detail in my in-depth Nutmeg review, which also includes details of what I invested with them and when. Note that my investment has grown by a further £1,100 since that article was published.

(2) Ratesetter

Ratesetter is a P2P lending platform. They don’t pay the highest rates, currently ranging from 3% for instant access to 4% for their Max account (where you pay a release fee of 90 days’ interest if you wish to withdraw). Though better than most bank savings accounts, those rates are clearly nothing spectacular.

One thing I particularly like about Ratesetter, though, is that they have a provision fund that effectively covers investors against defaults. That means you don’t have to worry about diversifying your investments across a range of loans, as is the case with some other P2P lending platforms. Of course, if the whole platform were to collapse the provision fund wouldn’t necessarily save you, but Ratesetter has been going for ten years now and appears professionally and competently run. It has delivered the promised returns to me with no stress or hassle, and I am happy to recommend it based on my experience.

In addition, if you check out my Ratesetter review you can discover how to get a free £20 bonus if you invest a mere £10 with them.

(3) Buy2Let Cars

I took a long time before deciding whether to invest with Buy2Let Cars, as it is quite an unusual investment. Basically what you are doing is putting up the money to buy a car for someone in a responsible job who can’t afford to buy one outright themselves. You then receive monthly repayments over a three-year period, and a final repayment of capital plus interest at the end of the loan. The minimum investment is £7,000, so this is obviously not going to work for everyone. Personally I bought one new car at a price of £14,000 in March 2018. Since then I have been receiving £250 per month in repayments, with a final payment of £8,429 due in month 37. That will give me a total net profit of £3,429 based on an annual interest rate of 10% (the rates on offer can vary but once you have signed an agreement the rate is fixed for the duration of the contract).

There are – of course – various safeguards and protections in place, fully discussed in my Buy2Let Cars review. Buy2Let Cars say that to date they have a 100% repayment record to investors, which appears to be confirmed by their Trust Pilot reviews. This investment has been working very well for me, with payments turning up in my bank account every month like clockwork. I am currently semi-retired, so it is providing a useful extra monthly income for me, with a large lump sum due in 2021, just a few months before I qualify for the state pension 🙂 If you think it might work for you, I recommend checking out my Buy2Let Cars review and speaking to my contact there, Brett Cheeseman, who helpfully answered all the questions I had at the time I invested.

(4) Kuflink

Kuflink offer the opportunity to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage.

Kuflink don’t pay the highest rates in this field – their loans are typically at an interest rate of around 7% – but in my view they offer a fair balance between risks and rewards. One thing I like about them is that interest is paid into your account monthly on all loans. I only have a relatively small amount invested, but so far everything has been going well with just the occasional short delay in repayment of capital.

Kuflink currently have a generous welcome offer, with cashback of up to £4,000 for new investors. Take a look at my Kuflink review for more information about this.

(5) Crowdlords

Crowdlords is a property crowdfunding platform. I have been investing with them almost since their launch and have made a good overall profit. Crowdlords pay competitive interest rates (over 20% in some cases) and offer a choice of equity and debt investments. Equity investments are higher risk than debt ones, but offer the potential for bigger returns if all goes well.

My only reservation about Crowdlords is that I currently have two overdue investments with them. In both cases, though, I have received full and reasonable explanations for the delays, and have been told that the money should be in my account within the next few months. Obviously, if that doesn’t happen, I will let Pounds and Sense readers know.

Crowdlords doesn’t have a welcome offer as such, but they do have a Refer a Friend scheme. If you sign up quoting my code, I will share the commission I receive 50:50 with you. Please see my Crowdlords review for more information about this.

So those are the investments that have given me the best returns and/or least stress during 2019. I do have others as well, including Primestox, ZOPA, Bricklane, The Lending Crowd, The House Crowd and Property Partner. Most of these have still made some money but none has really set the world alight.

Only Primestox actually lost me money. This is (or was) a premium food investment platform. They started promisingly and I made good returns on my early investments, but then they were hit by a series of delays and defaults. This happened with three projects I invested in. In the case of two I have received partial repayments with more promised, but in the third I have probably lost my £500. Primestox are no longer advertising investment opportunities, and I assume are re-evaluating their business model.

Property Partner is an interesting case. I have made modest returns on my portfolio this year, partly due to the fact that the property market in general has been in a slump. That said, there haven’t been any issues with delays or defaults, and dividends have been credited to my account every month as promised. It will be interesting to see what happens in 2020 as properties come up to their five-year anniversary and investors have the opportunity to exit at the current market price. As I noted in this recent blog post, this has the potential to create opportunities for both buyers and sellers.

I haven’t included certain other investments in this article. These include my Bestinvest SIPP, which is now in drawdown and holding up well in value. Neither have I included money invested via my financial adviser. This is mostly in funds from Prudential, which again are doing pretty well.

Lastly, I haven’t included the money I ‘invested’ in Football Index. My portfolio has more than doubled in value over 18 months, so in some ways it is my most successful investment of 2019! I am sure luck has played a significant part in this. Nonetheless, if you want to know more about Football Index – and read how you can get a risk-free £50 when signing up – you might like to check out this recent blog post.

I hope you have enjoyed reading this article, which has run on a bit longer than I expected. I hope also it may have given you a few ideas to investigate further if you are in the fortunate position of having money to invest.

As always, if you have any comments or questions about this article, please do post them below.

Disclaimer: As stated above, I am not a professional financial adviser, and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m sharing some thoughts about the role of property in retirement planning. The post is partly inspired by recent research and insight from retirement planning specialists Just.

In association with Opinium Research, Just surveyed 4,000 adults from all over the UK to discover what they think and feel about property, including their views on owning versus renting, how property affects their attitude to their current and long-term financial plans, whether they thought of their property as a home or an investment, what impact property ownership has across the generations, and more.

When looking at those in their 50s, the research revealed that this age group turned out to be (in some respects anyway) the most pessimistic age group.

Survey Results

The survey threw up some interesting – and in some cases concerning – findings for the 50s age group. Key points arising included the following:

Whilst those in their 50s are building up towards retirement, half (47%) feel unprepared and hit a ‘pessimistic peak’.

Among homeowners who don’t feel prepared – not having enough to retire on (52%) and not having enough to do what they want (45%) is the biggest concern. Ranking these above other concerns such as debt and handing down wealth to their children.

1 in 4 (23%) don’t know how to fund long term goals. And this goes up to almost half of renters (43%), compared to 16% of homeowners

It has become noticeably more difficult to get on the housing ladder – and this affects over a quarter (26%) of people in their 50s, who are still renting.

The impact on retirement is one of the biggest concerns for those now unable to buy, as property remains a core component of household wealth.

Even those on the property ladder are struggling to juggle their priorities and plan for the future.

You can see more information about the survey, and other findings from it, on Just’s My Home My Future website.

My Thoughts

At the age of 63 I am a little older than this age group, but I can definitely relate to these findings, both in respect of my own experiences and those of friends and relatives.