Today I have the first in a series of three collaborative posts on the subject of equity release. This one examines the growing popularity of equity release and why it looks set to boom in the year ahead.

The equity release industry saw a massive expansion in 2021, with a record-breaking sum of over £4.8 billion being unlocked by retirees across the UK. This unprecedented growth has been welcomed amid a global pandemic, as the Equity Release Council helps regulate a retirement product that has given many retirees the means to a desperately needed income in these tough economic times.

Mark Patterson, the equity release expert from EveryInvestor, joins the ranks of fellow industry authorities in predicting that 2022 is set to be another record-breaking year. Let’s take a look at what’s expected and determine if unlocking equity is a good idea over the next few months.

What Is Equity Release?

Equity release is a widely popular financial product for UK-based homeowners older than 55. In a nutshell, it gives you the opportunity to use your property’s equity but still live at home. With a third of UK retirees having less than £10,000 in retirement savings, equity release offers a lifeline to many. What’s more, the money can be used for any purpose.

According to figures from the Equity Release Council (ERC), equity release clients borrowed a total of £4.8 billion last year, a 24% rise on 2020’s figure.

Why is the Equity Release Industry Growing Amid a Tough Economy?

While many industries have crumbled in the wake of Covid 19, the equity release sector has grown tremendously. This is for several reasons, including:

Equity release provides financial security in a tough economic time.

The Equity Release Council has made the industry safe and is shifting a historically bad reputation.

Interest rates hit an all-time low in March 2021, and homeowners have received the best deals yet, with fixed-for-life interest rates.

Finally, growth inspires growth. As the industry expands, lenders offer more flexible products with bonus features, such as a free valuation or no completion fee.

What’s Predicted for 2022?

The future of equity release looks bright in 2022, and 80% of experts predict growth, with some believing this will be vastly beyond regular inflation. There are some key industry features that are likely to impact the industry (1).

First, the Equity Release Council announced on 31 January 2022 that all equity release lenders must offer the opportunity for voluntary loan and interest repayments. This announcement is welcome for potential borrowers, as voluntary repayments can vastly reduce the cost of your loan, yet there’s no obligation or risk of foreclosure.

On a slightly less positive note, equity release interest rates will rise in 2022 and should continue to do so until 2024. However, this could actually mean further industry growth. Rates are set to rise only slightly, and homeowners applying now will likely begin their equity release plans before we see any further increases.

Should I Unlock Equity from My Home at This Time?

With the market as it stands, it is a good idea to unlock equity if you’ve been planning to do so. However, it’s more complicated than just looking at the state of the industry.

Whether or not you should unlock equity from your home will depend on your personal circumstances and stage of life. What’s great is that equity release is safe; it’s overseen by the Equity Release Council and regulated by the Financial Conduct Authority (FCA).

However, to determine if it’s a good idea to unlock equity from your home, you should speak to a financial adviser. After all, seeking advice is compulsory when opting for an equity release product. The team at EveryInvestor will always encourage a whole-market financial adviser as they have an overview of the whole equity release market.

In Conclusion

Between flexible plans, the opportunity for voluntary repayments, and interest rates still low, now is a great time to release your property value through equity release. With another record-breaking year ahead of us, the industry is booming, and many more retirees are set to sign up to an equity release plan. Could you be next?

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

If you invest in funds rather than individual stocks and shares, you’ll almost certainly know that in many cases you can choose between two options, income or accumulation. Today I thought I’d explain what this difference is and share a few thoughts on the subject. I will be referring to my own experiences in this regard.

But to start by answering the question in the title, the difference between income and accumulation Funds is basically as follows:

Income Funds pay any income generated by your investments as, well, income. The money will appear in your account ready for you to withdraw (or reinvest). Or it may simply be paid directly into your bank account if you prefer.

Accumulation Funds, on the other hand, use any income generated by your investments to buy more units in the fund concerned. Your holding in an accumulation fund (and its value) should therefore build over time. But you won’t typically receive any income from the fund.

You might therefore think that if you want to draw an income from your investment, an income fund is the way to go. In practice it’s not as simple as that, though. For one thing, if you want to withdraw money from an accumulation fund, you always have the option to sell some of your holding, and there can be significant advantages to proceeding this way.

I will discuss this in more detail below, focusing on my personal pension as an example. Of course, everyone’s circumstances are different, so the decisions I took (and am still taking) may not be right for you. But I hope it will give you food for thought.

Why My SIPP is Mostly in Accumulation Funds

Regular readers will know that for some years I saved for my pension in the form of a SIPP (Self Invested Personal Pension). I use the Bestinvest platform for this and have always researched and chosen my investments myself. My SIPP currently has 14 funds in it. You can see a screen capture below.

As you can see, most of these are accumulation (Acc) funds with a couple of income (Inc) funds. While I was building my pot it seemed sensible to put most of my money into accumulation funds.

I am not by any stretch claiming that this is a ‘model portfolio’ that anyone else should emulate. I picked these funds based on recommendations I read in the press (and online) at the time, and there may well be better options now. I aimed to diversify as broadly as possible across different market sectors, geographical areas, investment types, and so on.

I put my SIPP into drawdown three years ago and now take £200 a month from it. I did consider switching to income funds at that time, but after careful thought (and research) decided against this.

The small number of income funds in my portfolio don’t typically generate enough to cover my monthly withdrawals. So each month I log in to my online dashboard and sell the necessary amount from whatever fund I pick that month. I must admit there is nothing very scientific about this. I typically just sell from funds I already have large holdings in.

Obviously having to do this every month is a minor hassle. However, in my view it has advantages as well. If you hold mainly income funds, the money they generate will vary from month to month. Sometimes there might not be enough to cover your monthly drawings, meaning you would still have to sell some funds anyway. Conversely, there might be months when more income is generated than you need, so you would end up with ‘spare’ money sitting in your account and not working for you.

Overall, then, I like having my SIPP money in accumulation funds because each month I can sell enough to cover my drawings that month, no more and no less. All the rest of the income that is generated by my accumulation funds is automatically reinvested.

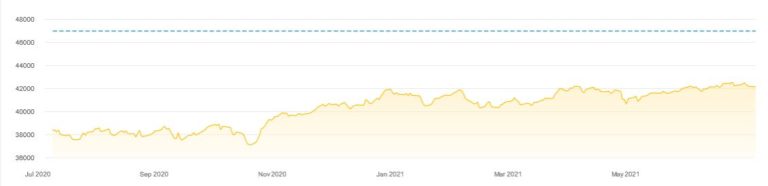

Interestingly, despite the fact that my annual withdrawals amount to almost 6% of the value of my portfolio, the overall value of my SIPP has continued to grow since I put it into drawdown three years ago (see graph below). I am not convinced that would be the case if I had switched to income funds across the board.

The standard advice is that you should withdraw no more than 4% of your portfolio each year to try to preserve its value. I have actually been taking nearly 50% more than that in the middle of a pandemic, and yet the overall value has still gone up by almost £4,000 in the last year alone. Obviously past performance is no guarantee of what may happen in future, but it is certainly food for thought.

Further Thoughts

Of course, pension funds aren’t the only sort of investment where this applies. You could, for example, be investing in a tax-free ISA, and again face the choice between income and accumulation funds. If you are aiming to build a pot, there is (of course) a strong argument for going with accumulation funds. But even if you want an income, the arguments above on behalf of accumulation funds still apply.

One further consideration is tax. If you are investing via a SIPP or ISA (or some other tax-efficient wrapper) this obviously won’t be an issue. But if you’re investing outside one of these, you do need to be aware of the tax implications.

With an income fund it’s fairly straightforward. The money you receive will count as taxable income (or taxable dividends in some cases) and be taxed accordingly.

With an accumulation fund, it’s more complicated. The income that is rolled up and reinvested is known as a ‘notional distribution’ and you will still be liable to pay tax on it at the appropriate time. This is explained in more detail in this excellent article from Shares Magazine.

As I say, investing outside a tax-efficient wrapper can be complicated, especially with accumulation funds. I would therefore recommend taking professional advice if you find yourself in this position. Ideally, though, ensure all your money is invested within a tax-free wrapper (SIPP, ISA, etc.). You won’t then have to worry about tax at all!

I hope you have found this post of interest. Whether you agree or disagree with my approach, I’d love to hear from you. Please leave any comments or questions below as usual.

Disclaimer: I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. All investment carries a risk of loss. You should always do your own ‘due diligence’ before investing, and seek professional advice if in any doubt before proceeding.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m addressing an issue that will be critical to many people approaching (or in) retirement. That is, how much to draw from your pension pot (and other investments) to supplement your state pension.

I’ll start by telling you about a conversation I had recently that made me think about this…

Talking to Mike

A few weeks ago I had my annual review with my financial adviser, Mike (if you want to know why a money blogger needs a financial adviser, you can read my post about this here). It was done by video call on this occasion, naturally.

One major topic of conversation was the fact that later this year (God willing) I will reach my 66th birthday and start receiving my state pension. I should qualify for the full state pension, which from April 2021 will be £179.60 a week or £9,339.20 a year.

As Mike pointed out, when you add this to my other income from this blog, my small private pension, other investments and my solar panels, this will put me in quite a strong financial position. So he recommended that at that time I reduce the amount I draw from the other investments or even stop taking anything at all and let them carry on growing year by year (financial downturns permitting).

I could see where Mike was coming from. If I don’t actually need the money it might be sensible to leave it all where it is. For both practical and psychological reasons, however, I told him I don’t want to do that. Here are the two main reasons I gave him:

1. If I take no income from my investments, I will still be somewhat dependent on my blog for income. While I have no plans to stop running Pounds and Sense at the moment, I don’t want to have to rely on it to cover my outgoings as I grow older. Also, the income from my solar panels will end in about ten years – possibly sooner if there are any major technical issues (or I move).

2. I don’t have any particular beneficiaries I wish to leave my money to (I live alone since my partner Jayne died a few years ago and we didn’t have children). I don’t therefore see any merit in accumulating a large ‘pot’ that simply goes to benefit my sisters (much as I love them). I would rather enjoy the money while I can, while aiming to ensure that it lasts me out.

I told him my plan was therefore to reduce my withdrawals to a sensible level where my capital should be preserved and hopefully continue to grow a little. Four percent is a common rule of thumb for this, so I am looking at that as a starting point (though willing to accept Mike’s expert advice on the exact level). I plan to review this every year, based on my needs and circumstances and how my portfolio has been performing.

If I have more money coming in than I require, I don’t see that as a problem. I will spend it (maybe on a few extra holidays), save it or reinvest it, and maybe give some to charity and/or friends/relatives who are in need. As they say, you can’t take it with you, so I have decided that will be one of my guiding principles going forward!

I shared these thoughts in a subsequent email to Mike but haven’t so far received a reply from him. If I do, I’ll update this post accordingly 🙂

That Crucial Question

I am obviously not alone in facing a decision of this nature. With most people nowadays relying on a pension pot to finance retirement rather than a guaranteed lifetime pension, many of us will have to grapple with the question of how much income we should be withdrawing to supplement the state pension.

And yes, I know the state pension will continue as long as we need it. But while it is obviously an important source of income for most people in retirement, it is nowhere near enough to finance a comfortable retirement on its own.

Of course, none of us comes with a sell-by date. Pension planning would be so much simpler if we did. If we knew the exact date we were going to expire, we could plan our retirement precisely.

So if I knew I was going to die in five years, I could live the (moderately) high life, burn my way through my savings and investments, and leave just enough for my relatives to pay for my funeral!

On the other hand, if I knew I could look forward to another thirty years, that would of course be wonderful, but I would need to plan carefully to ensure my pot didn’t run out before I did. But as none of us knows how long we have on this planet, a long-term strategy is the only sensible option really.

The question of how much to draw from your pension pot (and other investments if any) therefore needs very careful thought. In particular, the following considerations may apply:

It’s clearly sensible to try to ensure that enough money will remain in your pot to see you through to deep old age (e.g. 100).

If you’re keen to pass on a legacy to your children (or some cause dear to your heart) you will need to be more cautious about how much you withdraw.

On the other hand, if you aren’t so worried about passing your wealth on, then there is no point in depriving yourself now.

Tolerance for risk is another factor. If you worry that the 4% rule is too chancy, you could reduce your withdrawals to 3% or less.

There may be other considerations too. For example, if you have a life-limiting medical condition, that may alter the equation in favour of a more bullish approach.

There is also the matter of whether you own your home. If so, you will have the scope to raise extra money if needed by downsizing or using equity release.

Tax may be an issue as well. The state pension counts as taxable income and so do most private pensions. If the total amount you draw exceeds your personal allowance, you may have to pay tax on it. This is something you might want to discuss with a financial adviser.

And finally, if you have a particular ambition or goal you wish to achieve during retirement (going on a world cruise, for example), you will of course need to ensure enough money is set aside to cover that when the time comes.

As mentioned above, a common rule of thumb is that to provide the best chance of preserving the value of your investments, you should limit withdrawals to no more than 4% of your capital per year. So if, for example, you have a pension pot of £50,000 and draw 4% annually from that, that would be £2,000 a year or about £167 a month. Drawing that would hopefully ensure that the value of withdrawals is on average balanced out (at least) by growth in the value of your investments.

Of course, the 4% rule is only a rough guide and needs reviewing regularly according to how your portfolio performs.

When pension freedoms were introduced in 2015, there was some concern that people might ‘blow’ their pension pot on a luxury car or a yacht, but actually I think the vast majority of older people are more sensible than that. Indeed, I think the opposite mistake is more common – people drawing too little and leading a life in retirement that is unnecessarily frugal rather than enjoying the money they accrued during their working lives. But in any event, this is a question we all need to think very carefully about as we attempt to chart a balanced course into retirement and old age.

So those are my thoughts on this important subject (one I know many people don’t really like to think about). But what is YOUR view? Please post any comments or questions below as usual

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at The Good Retirement Guide, an annual guide published by Kogan Page. I bought the current 2021 edition, which was published last month.

The Good Retirement Guide 2021 is 318 pages long. The text is fairly dense but broken up by plenty of headings and bullet-point lists. There are 14 chapters and an alphabetical index at the back. The chapter titles are as follows:

Are You Looking Forward to Retirement?

Money and Budgeting

Pensions

Tax

Investment

Your Home

Leisure Activities

Starting Your Own Business

Looking for Paid Work

Voluntary Work

Health

Holidays

Caring for Elderly Parents

No-one is Immortal

The chapter titles are pretty self-explanatory. The book attempts to cover every aspect of making the most of your senior years. The style is clear and readable, and additional resources are signposted as appropriate.

In contrast with Sod 60! which I also reviewed recently, The Good Retirement Guide covers the financial aspects of later life in some detail. I thought the information about pensions and benefits in particular was very good and tells you most of what you need to know.

Some of the other chapters are a bit less comprehensive. The one on leisure activities, for example, lists various things you might like to do – or take up – in retirement, but the information is frequently sketchy and can verge on stating the obvious. Here is what it has to say about poetry, for example:

There is an increasing enthusiasm for poetry and poetry readings in clubs, pubs and other places of entertainment. Special local events may be advertised in your neighbourhood.

And apart from a mention for the Poetry Society and a link to their website, that is all you get on this subject 🙂

I don’t want to appear too harsh. Obviously in a wide-ranging book like this, it can be hard to judge the degree of detail appropriate to any particular topic. At least by mentioning a wide range of possibilities, the book may give you some ideas about activities you might like to pursue further in retirement.

The health-related content is a bit of a mixed bag. Some subjects are covered in reasonable depth, others less so. There is just half a page devoted to keeping fit, for example, with a further couple of paragraphs about yoga and Pilates. On the other hand, there is some good information (and advice) on health insurance, long-term care plans, and so forth. Again, this illustrates that the book’s primary focus is on the financial aspects of retirement.

One thing that did surprise me is that although this 2021 edition of The Good Retirement Guide was only published last month, there is no mention of the pandemic in it. You will search in vain for Coronavirus or Covid-19 in the index. I know there can be long lead times in publishing, but in an annual guide you might think they could have inserted a section about it somewhere. Maybe we will have to wait for the 2022 version?

Even so, a lot of the subjects discussed in the guide – holidays, for example – have been seriously impacted by the pandemic. The advice and procedures for travel abroad in particular may be very different even after the pandemic is officially over.

Final Thoughts

Overall, I thought The Good Retirement Guide 2021 was a helpful book for people approaching retirement. As I’ve said above, it has a strong emphasis on financial matters, and is well worth reading for that alone. Some of the other content is a bit hit-and-miss, and the surprising lack of any mention of the pandemic means that at times it reads like a guide to an alternate world where Covid never happened. Of course, none of us really knows what the ‘new normal’ will be in future. We can but hope it will be not too far removed from the old normal we remember and which this book – despite the 2021 in its title – basically depicts.

As always, if you have any thoughts or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

As you may know, this is a best-selling book by Claire Parker and Sir Muir Gray, published by Bloomsbury. I bought a hardback copy from Amazon. A slightly cheaper ebook version for Kindle is also available.

Sir Muir Gray is also the author of Sod 70!, a similar healthy living guide aimed at the over-70s.

Review

Sod 60! is 232 pages long. The text – which is very readable – is broken up by lots of sub-headings, diagrams and cartoon-style illustrations (by David Mostyn). There are nine main chapters, each covering an aspect of how to live well in your sixties. The chapter titles are as follows:

Getting Older Doesn’t Matter – Getting Active and Getting Attitude Does

Keeping Active is Fitness Friendly

Your Attitude and Its Soulmates: Mind and Mood

Keeping Your Metabolism Healthy

Take Care of Your…Bits

Rhythm and Blues

Stuff Happens

Decisions, Decisions

Health Care: Choosing and Using It Wisely

Some of those chapter titles are self-explanatory, others less so. For example, Chapter 5 ‘Take Care of Your…Bits’ isn’t about what you might think. It actually covers looking after different parts of your body, from your brain to your feet. Sexual health is then covered in Chapter 6, ‘Rhythm and Blues’. Those both seem pretty odd choices of chapter title to me, but I suppose the aim was to help give the book a ‘quirky’ personality.

That small criticism aside, the style of the book is friendly and relatable. It’s also down to earth and practical, and I like the way that the text is interspersed with exercises, resolutions, and so on. It is very much a hands-on, practical guide.

Sod 60! concerns the importance of looking after your body and mind as you grow older. The authors stress the need to stay as active as you can, both physically and mentally.

Chapter 2 includes a range of physical exercises to try, and also sets out some general principles for exercising healthily as you get older. I thought this was one of the most useful chapters in the book.

Chapter 3, which focuses on attitude, mind and mood, is also very good. It looks at the importance of keeping a positive attitude, and staying connected with friends and family, your neighbours, local community, and so on. It also discusses maintaining a good relationship with your partner (assuming you have one). Getting enough sleep and dealing with stress are covered as well, though not in great detail.

Chapter 4 ‘Keeping your Metabolism Healthy’ focuses on diet and weight. The authors advocate following a balanced and varied Mediterranean-style diet, with plenty of fresh fruit and vegetables. That seems eminently sensible to me. I wouldn’t say there was much in this chapter I hadn’t heard before, and some of the advice such as avoiding sugary drinks struck me as stating the obvious. But this is of course very important to long-term health, so I guess it had to be said.

Chapter 5, as I’ve already mentioned, focuses on different organs/parts of the body. It discusses how to keep each one healthy, and warning signs to look out for as you get older. It also covers age-related changes and what you may be able to do to help prevent problems. Having a good diet, staying active, giving up smoking and reducing alcohol intake all crop up quite frequently. Again, there were no huge surprises for me here.

Chapter 6 is about sexual health and related matters such as bladder and (for men) prostate problems. On the sexual side, the advice could be broadly summed up in five words: Use it or lose it! The advice on matters such as urinary incontinence is – to be honest – a bit depressing, but nonetheless important to be aware of.

Chapter 7 ‘Stuff Happens’ is also a bit depressing, though again it covers some important topics. These include how to deal with the problems later life can throw at you, including depression, isolation, bereavement, serious illness, and so on. There is some excellent advice here, especially on the importance of cultivating and maintaining a support network of friends, relatives, health professionals, and so on.

Finally, Chapters 8 and 9 are both about healthcare and could easily have been combined in my opinion. They look at such matters as how to navigate healthcare decisions, self-care to prevent (or at least mitigate) serious health problems, drugs and vaccinations, and so forth.

In Conclusion

Overall I thought Sod 60! was a useful guide for sixty-somethings though maybe not an earth-shattering one. The book covers a range of issues that anyone in their sixties will need to think about and prepare for. It was first published in 2016, so there is no reference to the Coronavirus pandemic. The advice in the book still applies and in some ways is even more cogent now. With the UK still in lockdown at the time of writing, for example, we all need our support networks more than ever at the moment…

Sod 60! is really a ‘mind and body’ book. It doesn’t cover financial issues such as pensions and benefits (and indeed doesn’t claim to). And it doesn’t have much to say about the challenges and opportunities retirement can bring, or the pros and cons of carrying on working. For advice on these and similar matters, something like the annual Good Retirement Guide (which I hope to review soon) would be good. And keep on reading Pounds and Sense, of course!

If you want a readable and entertaining guide to making the most of your sixties and preserving your physical and mental health, though, Sod 60! would certainly fit the bill. It would also make a great (and relatively inexpensive) birthday or Christmas gift for anyone in this age category.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

A great number of people today need to transfer currencies, or receive transfers from abroad, for many different reasons. As globalization extends, this need has become more frequent as geographical borders become less relevant.

For example, our parents couldn’t even dream about services like eBay or Alibaba, where you can buy anything and have it delivered from a dozen countries away. And the whole thing might be cheaper than buying it in your local store!

But here is where the matter of foreign currency transfers becomes important. Paying for something abroad or getting money sent to you might not be cheap. That’s because not only do you have to pay bank fees for the transaction, you also lose money on currency exchange, which is often a mandatory step in cross-border transfers.

Luckily, today there are alternative money transfer services that allow you to cut these costs. You’ll need to look into them if you require regular foreign currency exchange (FX or forex) services.

Why You Might Need to Make Foreign Currency Transfers

One reason you might need to make a large money transfer abroad is real estate. Buying property is an important part of the retirement planning process and many Britons choose to retire abroad. For example, the latest data indicates that there are about 466,000 British pensioners living in the EU. There are even more among the 5.5 million Brits living worldwide.

Even if you don’t plan on moving or buying a vacation home on some tropical beach, you might consider investing. Investing in real estate is one of the less risky methods for growing your fortune. Of course, the coronavirus crisis has heavily affected this industry. But there are still some very promising prospects for the residential housing market.

Also, today you’ll need to make international payments when booking your holiday accommodation. So, if you plan to travel at all, you’ll need to look for cheap money transfer solutions.

Anyone involved in international business also needs to make and/or accept international payments. This also includes the simple process of buying goods through one of the many e-commerce platforms.

In addition to those reasons, if you are an expat or a traveller, you’ll need to exchange money regularly. The same goes for dealing with transfers like inheritance or even accepting dividend payments from your investments.

All in all, living in the modern world makes you exposed to foreign currency exchange and transfers in many ways. Therefore, the knowledge of how to save money on these transactions is sure to be useful.

How Much Do Foreign Currency Transfers Cost in a Bank?

The cost of an international bank wire transfer is a very complicated issue. First of all, you need to understand that banks will advertise, and sometimes even show you, only the transfer fee. In the UK those range from £8 to about £40. That doesn’t seem too bad, especially for large transfers, right?

However, the truth is that banks are deceiving customers most of the time. If they were fully transparent, you would understand that what truly matters is the FX rate margin. That’s the amount that the bank charges per currency conversion on top of the mid-market exchange rate.

Simply put, high FX margins are why you lose so much money on currency conversions. Different banks use different margins and that’s why they offer different exchange rates. But if you compare the options offered by top UK banks, you’ll see that they are all very close.

Therefore, you don’t have much of a choice.

Also, there might be additional fees involved in a cross-border money transfer. The recipient bank might charge its own fees. If there are any intermediary ‘stops’ along the way, more fees will come.

All things considered, the real cost of an international money transfer can go up to 3-10% of the transfer amount. This cost will be higher for exotic currencies and transfers to remote locations. It will go down a bit for large transfers because banks might offer better terms to VIP clients.

However, the total will always be quite high.

Leading Money Transfer Service Alternatives From the UK

With bank transfer costs so high, a necessity for an alternative emerged. The solution came in the form of FX brokers and money-transfer companies. These businesses offer services similar to banks, but they have much lower overhead costs. Therefore, they are able to keep both the margins and fees very low.

In fact, many companies charge no transfer fees at all for the majority of transactions. However, they use different margins that often depend on the transfer size. Thus, you should always compare foreign currency transfers before choosing a service. This won’t be difficult as all top companies in the industry offer free quotes. They also have transparent pricing schemes.

On average, a transfer with one of these companies will cost you 1-3% of the total. Industry leaders even offer options that allow you to cut costs below 1% for large transfers.

The most notable UK-based FX companies today are TransferWise and WorldFirst. There are other notable businesses as well. However, they cannot compete with these two giants that have multi-million funding.

TransferWise

TransferWise launched not even a decade ago and it has already become a major disruptor in the banking industry. It took over the FX money transfer industry rather fast as well. The main selling point of this company was offering not merely cheap transfers but also a fixed margin scheme.

This means that TransferWise managed to offer its customers consistency and a chance to save a great deal of money. Because of the fixed margins, its services were the most affordable in the industry. The company is now valued at over $3.5 billion and it’s expanded to many countries, including the US.

WorldFirst

WorldFirst is another veteran in the FX transfer industry. This company built a solid reputation for its reliability and trustworthiness. Launched back in 2004 literally from a basement, WorldFirst became one of the industry leaders within a few years.

In 2019 this fintech business was purchased by Ant Financial of the Alibaba Group. This allowed WorldFirst to launch a major change in pricing. It had already been one of the top companies, but it could not compete with TransferWise in affordability. However, the new pricing scheme with fixed margins that go below 0.55% makes WorldFirst a cheaper alternative even to TransferWise. At the moment, there is no cheaper option for foreign currency transfers in the UK. Also, WorldFirst has a very wide reach due to its association with Alibaba, though it’s not yet available in the US.

In Conclusion: Do Your Research for Saving Money on Foreign Currency Transfers

FX money transfer companies today offer great opportunities for money saving. However, do not forget that the lowest cost doesn’t necessarily mean the best offer. These companies have a number of requirements and additional services that you should research. For example, some have a minimum transfer limit. Others offer FX hedging tools that will be essential for reducing risks for businesses and investors.

Thus, be sure to compare all options you have available and research them thoroughly. Watch out for scammers, and choose only those businesses that have a good standing in the industry.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

As you may have heard, the BBC has now confirmed that from 1st August 2020 people over 75 in the UK will lose their automatic right to a free TV licence and have to pay the same £157.50 a year as everyone else. This was originally due to happen in June 2020, but it was postponed due to the coronavirus pandemic.

For many old people, TV is their main (or only) source of company. Suddenly having to find this quite large sum out of (in many cases) a very limited income may cause them financial difficulties or downright hardship. Some may even have to choose between watching television and paying their heating bills.

This parlous situation has arisen because the BBC say they have to make economies, and continuing to subsidise free licences for the elderly would force them to cut back drastically in other areas. Meanwhile the government, despite their pre-election promises, has shown no sign of stepping in to preserve free TV licences for over 75s (which they could perfectly well do). Although charities such as Age UK have been raising petitions and applying as much pressure as they can, it now seems certain that this change is going to happen.

So what can people in this situation – or their relatives/friends/carers – do? The BBC have allowed just one concession – the poorest over-75s can continue to receive a free TV licence if they claim and receive pension credit. So let’s look at this in a bit more detail…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions, around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4% – if only!). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify. Savings Credit is only available to people who reached state pension age before 6 April 2016. Couples where only one partner reached state pension age before 6 April 2016 can also retain savings credit if the older partner had reached 65 and qualified for savings credit before that date AND they have remained continuously entitled to it ever since.

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount you’re entitled to. The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee that you will receive the amount it shows you.

To actually apply you will need to phone the DWP’s Pension Credit helpline on 0800 991234. You will need your National Insurance number, information about your income, savings and investments and your bank account details. The person you speak to will then take you through the application process. This is a subject I discussed in more detail in this blog post, as I recently helped an older friend to do this successfully.

What Does Pension Credit Entitle You To?

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional benefits. A free TV licence if you are over 75 is just one of them. You may also get:

reduced council tax (or free if you are awarded guarantee credit)

Even if you only receive a small amount of pension credit, you will be eligible for all of the above. So it really is well worth applying if there is any chance you may qualify. As mentioned above, you can check first using the free online calculator here and then apply by phoning the DWP’s Pension Credit helpline on 0800 991234.

Don’t delay, as there are now just seven weeks left before the free TV licence for all over-75s becomes a cherished memory.

Equity Release to Boost Your Income

If you’re still struggling to pay the bills even with pension credit, there are other methods to help boost your income. In particular, UK homeowners are fortunate to have opportunities to unlock their property value. An equity release loan could provide the security you desire if you require the means to pay for life’s simple pleasures or cover essential costs.

What’s more, homeowners can unlock up to 65% of their property value, with no compulsory payments required during their lifetime. There’s no limit on how you can use the tax-free cash you receive, so an income lifetime mortgage could be the ideal way to pay your bills and have a bit extra for luxuries as well.

In this recent blog post I discussed how over-75s may be able to avoid losing their free TV licence by claiming pension credit.

As I said then, I have recently done this myself on behalf of an elderly couple who are friends of mine. As promised, today I’ll be sharing my experience of the telephone application process. I hope anyone thinking of doing this themselves or on behalf of elderly friends or relatives may find this helpful.

But first, let’s recap on what pension credit is…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions (DWP), around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4%). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify.

While for most people pension credit won’t be a huge amount, it has the big advantage that it acts as a gateway to a range of other discounts and benefits. The free TV licence for over-75s is just one of them. Pension credit recipients may also get reduced council tax (or free if awarded guarantee credit), free NHS dental treatment, help towards the cost of glasses, help with the cost of travel to hospital, cold weather payments, automatic entitlement to the Warm Home Discount, help with rent, free home insulation and boiler grants, and more. All of this means it is well worth applying for, even if you’re not certain whether you qualify.

Checking Your Entitlement

The government is keen that anyone eligible for pension credit should claim it. To that end they recently launched a free online calculator you can use to work out whether you qualify and how much you might get.

You can use the calculator anonymously to check your entitlement (or someone else’s), either as an individual or a couple. You can’t actually apply via the calculator, though. It is just for guidance, to help you decide whether it’s worth putting in a claim.

The calculator asks a variety of questions about your circumstances and current income, including any pensions or other benefits you may receive. The latter may actually improve your chances of getting pension credit. For example, if you receive attendance allowance and/or carer’s credit (as my friends do) this can improve your chances of qualifying. When I did this on behalf of my friends, the calculator showed that they should be eligible for a payment of just over £10 a week.

As mentioned above, the results on the calculator are for guidance only, and there is no guarantee that you will receive the amount shown. However, in my friends’ case it definitely confirmed that applying would be worth doing.

Applying for Pension Credit

By far the easiest way to apply for pension credit is to phone the DWP’s Pension Credit Helpline on 0800 991234. You will need to have your National Insurance number, information about your income, savings and investments and your bank account details to hand.

If you’re applying on someone else’s behalf, the DWP like you to have the person concerned with you at the time. The call handler spoke briefly to my friend to confirm her personal details and that she was happy for me to take over the application process.

It turned out to be a two-stage procedure. Initially I spoke to a male call handler who asked a list of questions about my friends’ circumstances and their finances. This was basically the same set of questions I had answered on the online calculator. It was reasonably straightforward, and at the end he informed me that my friends did indeed appear to have a valid claim, so he was going to put me through to his colleague who would take me through the actual application.

This meant that I had to answer the same set of questions again from another DWP employee – a woman this time, as it happens. This did strike me and my friend as rather a waste of everyone’s time. We wondered why the answers I had given initially couldn’t just be passed on to the second person, but I suppose the DWP must have their reasons.

Anyway, we duly went through all the questions (and a few more) again. I would, incidentally, comment that the young woman I spoke to – who told me her name was Jenny – was extremely pleasant and helpful. At one point we went off at a tangent and started talking about our favourite cakes (well, it was tea-time by then). I felt she went out of her way to help us, and she certainly made the whole application process a lot less stressful.

After going through all the questions, Jenny said she would need information about how much exactly was in my friends’ bank accounts and when their (small) private pensions were paid in. This could have been problematic, as it involved logging in to my friends’ online bank accounts and finding this information there. But Jenny was patient and flexible about this, and in the end we found all the information she needed.

The whole process took a little over an hour. if you have to break off half-way through that is possible and you can ask for a reference number so you can complete the application another time. But I really wanted to get the whole thing done and dusted in one call, and thankfully – with Jenny’s help – we achieved that.

The Outcome

After about six weeks my friends received a letter from DWP saying their application had been successful and they had been awarded pension credit.

The amount was the same as had been shown on the online calculator. It was about £10.50 a week, going up to almost £12 in April (I’m sorry I can’t remember the exact figures). This money was savings credit rather than guarantee credit, but that makes no difference as far as the free TV licence is concerned. If you are over 75 and qualify for either type of pension credit (or both) you are entitled to a free TV licence.

We then submitted the short application form to the TV licence people, with a copy of the first page of the DWP letter confirming the award of pension credit. We haven’t heard any more since, but presumably my friends will receive their free TV licence in the coming weeks.

So that was my experience of applying for pension credit on my friends’ behalf. I hope it has encouraged you to proceed with your own application if you are considering making one. If you get to speak to the lovely Jenny in Scotland, do pass on my regards to her!

And if you have any comments or questions about this post, of course, pleased free free to leave them below as usual.

This is a fully updated repost of my March 2020 article.

If you enjoyed this post, please link to it on your own blog or social media:

…that’s the question I was asked recently by a Pounds and Sense reader after I mentioned in this blog post that I had a financial adviser.

Of course I replied to her directly at the time, but on reflection I thought it would be good to provide a more in-depth answer to this question on the blog.

To recap, my financial adviser is called Mike and he works for a company called Integrity Wealth Solutions. I was recommended to Mike by my accountant, and he has been advising me for over three years now.

Mike actually looks after about half of my portfolio. He advised me about this initially and set up the recommended investments on my behalf, making maximum use of my tax-free allowances. He continues to monitor my investments and makes any recommendations for adjustments as required. I see Mike once a year in person to review how things are going (both with the investments and me personally). But of course, I can also speak to him by phone (or email) any time if required.

The other half of my portfolio I look after myself, and it is fair to say it is well diversified! As regular readers of PAS will know, I have investments in property crowdfunding, P2P lending, the robo advisory platform Nutmeg, and various others.

Why then do I need Mike? Here are just some of the reasons…

1. Mike is a trained and experienced independent financial adviser/planner who works full-time in this field. I am a money blogger and obviously have a special interest in financial matters, but I have no professional training or direct work experience in this field. I can ask Mike for his professional opinion on any investment-related matters, and while I am not obliged to follow his advice I do of course take it very seriously.

2. Mike has a backup team in his office and access to specialist investment research services and software. He uses these resources to inform his advice, and also to provide in-depth reports (with snazzy-looking charts and spreadsheets!) regarding how my investments are performing.

3. As a regulated financial adviser, Mike has to follow all the correct protocols and ensure that all advice he gives follows best professional practice and is appropriate for my needs and circumstances. He cannot cut corners, invest on a whim or hunch, or let himself be distracted by the latest ‘bright shiny object’ in the investment world. I have to admit that I have been guilty of all of these things myself in the past!

4. As a professional financial adviser Mike also has access to certain investment opportunities or platforms that are not easily accessible to the general public. I won’t go into detail about this here, but it is certainly something I have had occasion to be grateful for in the current coronavirus outbreak.

5. Mike is able to provide personalized but objective advice about my finances, based on information I give him. Money and investment can be emotive subjects, and it’s great to have a sympathetic – but at the same time sensible and detached – professional advising you. I am sure Mike sometimes sighs inwardly at some of my more exotic investments, but he is always interested in what I have been doing with ‘my’ half of my portfolio and happy to offer his thoughts as appropriate.

Are there any drawbacks to having an adviser? Well, of course, you have to pay them! In the case of Mike I paid an up-front fee initially and now pay a small monthly commission. Hand on heart I can say that Mike is well worth his fee, and even in the current exceptional circumstances his charges have been more than covered by the amount by which my investments have grown.

So that is why I have a personal financial adviser. If you are fortunate enough to have money to invest, I strongly recommend you consider engaging one too.

If you would like to find out more about the service offered by Mike and his colleagues at Integrity Wealth Solutions, you can check out their website and contact them on 02476 388 911, or email them at advice@integritywealth.co.uk. They are friendly and not at all pushy, and will be delighted to talk you through the service they offer without obligation. If you do get in touch, please mention that you were recommended by Nick Daws of Pounds and Sense blog. If you end up becoming a client they have said that they will pay me a small fee to say thanks. This will help to cover my costs and ensure I am able to go on sharing tips and advice to Pounds and Sense readers.

As always, if you have any comments or questions about this post, just let me know.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a pension advisory service called AdviceBridge that may be of interest to any Pounds and Sense readers who are planning for their retirement.

There is no doubt that in recent years retirement planning has become more challenging. The pension reforms introduced by George Osborne in 2015 gave people much more freedom over how and when they can access their retirement savings. There are many benefits to those reforms – and I’m a fan of them myself – but it does mean most people now have big decisions to make over how to finance their retirement.

A further factor is the decline of ‘defined benefit’ pensions. These guaranteed a certain pension usually based on how long you had worked for an employer and how much you earned during your career. The great majority of working age people nowadays have ‘defined contribution’ pensions, where you build up a pension pot over the course of your working life. This then provides you with an income (alongside the state pension and any other investments) when you retire. Anyone with a pension of this type will have important choices to make over how, when and where to save for their pension, and what to do with it once they reach retirement age. Many people who are not financial services professionals understandably struggle with this and need some expert help (I did myself).

Getting professional financial advice can be expensive – typically pension advisers in the UK charge £2,000-£3,000 up front and then 0.5% a year. But a new service called AdviceBridge promises a personalized, affordable retirement planning service. Indeed, they say they can do this for as little as a tenth of the average adviser fee, partly by running the service online and over the phone (no face-to-face meetings required).

Although it is a low-cost service, AdviceBridge is staffed by fully trained and regulated financial advisers, and the company is authorized and regulated by the Financial Conduct Authority (FCA). AdviceBridge never holds investors’ money, even when they assist in the implementation of a retirement plan. The advice they give is though covered by the Financial Services Compensation Scheme (FSCS), which means clients can claim compensation of up to £85,000 if they receive bad advice.

Who Is AdviceBridge For?

In order to keep their charges low, AdviceBridge say that at the moment they are only able to help clients who meet the following criteria:

You are resident and domiciled in the UK.

You are generally in good health.

You do not have any unsecured loans.

You are not currently contributing to pensions with safeguarded benefits such as a final salary pension.

You do not own any buy-to-let property or any non-standard investments.

You do not receive any means-tested benefits.

You would like to plan individually, not as a couple.

How Does It Work?

Assuming you meet the criteria above, you start by filling in an online questionnaire and completing some electronically-signed compliance documents.

As well as the usual contact information, the questionnaire covers such matters as:

your age

your employment status

your annual income

any existing private or company pensions

whether you will qualify for a full state pension

other savings and investments

your target retirement age

how much income you hope to have in retirement

any major outgoings in future you need to plan for

and so on

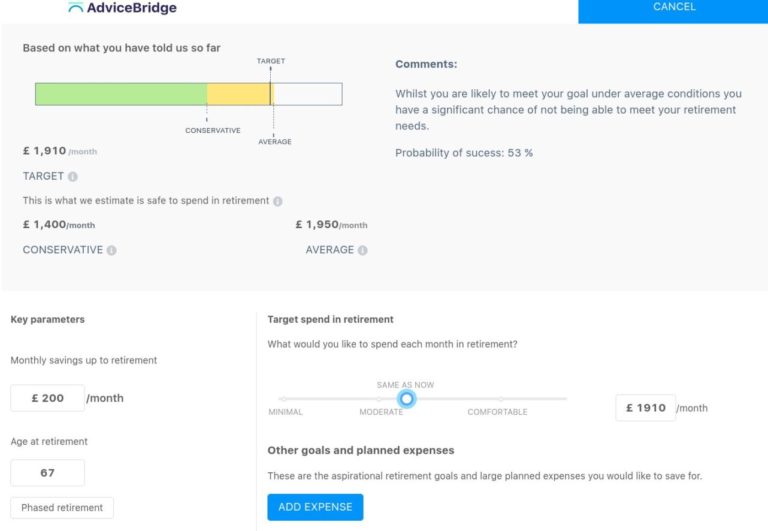

Once you have entered this information, you can create and log in to your account to see an overview of your financial situation. You can adjust the parameters in order to achieve a realistic and sustainable level of retirement income. Here is a screen capture showing part of this (an example account, not mine personally!).

Personalized Plan

Naturally, the above is just the first stage of the process. Once you have provided this information and set up your account, the AdviceBridge advisers will crunch the numbers and (with the aid of their specialist software) produce a personalized plan for you.

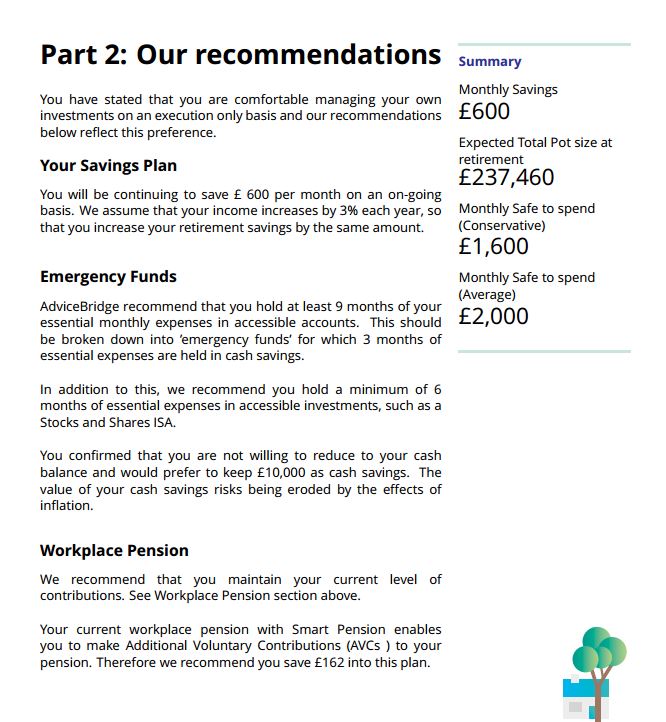

This is obviously a key document. The sample plan I saw came to 39 pages in PDF form. It was divided into three sections: About You, Our Recommendations and Advice, and Appendices.

About You sums up the information you have provided to AdviceBridge via the questionnaire. It covers your personal circumstances, your retirement savings and investments, and your progress so far towards achieving your retirement goals.

Our Recommendations and Advice is the longest section of the plan. It presents recommendations on every aspect of managing your finances for retirement, including restructuring your investment portfolio if required (with specific recommendations for low-cost personal pensions and ISAs). It also examines the likely outcome of following the recommendations, including both average and conservative projections. A sample page from this section of the plan is shown below.

Finally, the Appendices section includes a range of supplementary information, including more detail about the UK state pension, rules about annual pension allowances and taxation, your options for accessing your pension (drawdown, annuities, etc), and more.

It doesn’t end there, though. Once you have had a chance to read and digest your plan, you can arrange a call with a personal financial adviser from AdviceBridge to talk through the advice and recommendations and help you decide how to proceed. The advisers are not paid commission on product sales, so they are able to give unbiased advice about what investments may be best for you based on your specific circumstances.

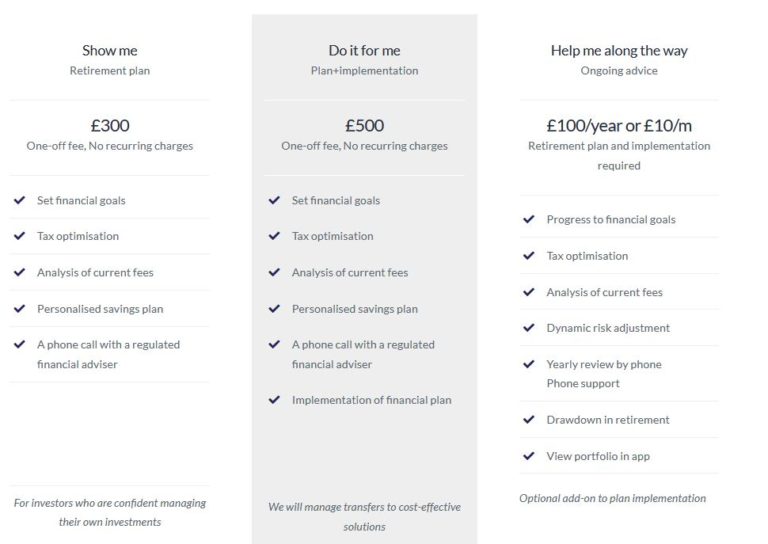

So What Does It Cost?

For the basic AdviceBridge service as described above, there is a one-off fee of £300 with no recurring charges. This service will suit people who are happy to arrange their own investments based on the advice given and the telephone call with an adviser.

If you want AdviceBridge to set up the recommended investments for you – to implement your financial plan, in other words – they will do this as well for an inclusive fee of £500, again with no recurring charges.

Finally, if you opt for the Plan+Implementation service and want ongoing support and assistance too, including dynamic risk adjustment, an annual telephone review, ongoing telephone support, assistance putting your pension into drawdown, and the opportunity to monitor your portfolio online using a dedicated app, AdviceBridge offer all this for an additional £100 a year or £10 a month.

All of the above is summed up in the table below which I have copied from the AdviceBridge website.

My Thoughts

Overall, I have been very impressed by AdviceBridge, both in terms of what they are offering and the prompt and friendly support they provided while I was writing this article. Here are some of the main things I like about their service:

much lower fees than traditional financial advisers

all fees quoted include any taxes due – what you see is what you pay

range of options according to how much (or little) work you want to take on yourself

non-commission-based advisers, so unbiased advice on what investments will suit you best

advisers are free to recommend across the entire range of investment opportunities

all digital process – no need for personal visits or face-to-face meetings

fully FCA authorized company and advisers

advice is covered up to £85,000 under the Financial Services Compensation Scheme (FSCS)

all personal information is securely encrypted

in-depth written advice and recommendations on your retirement finances backed up by telephone support

Any negatives? Well, the only real one I could find is that various groups are currently excluded from the service, e.g. buy-to-let landlords and holders of ‘non-standard investments’. I guess the latter might include me, as I have a proportion of my portfolio in P2P lending and property crowdfunding.

I do of course appreciate that to keep their service so inexpensive AdviceBridge have to streamline their service, but it is a pity if this excludes a significant proportion of people who could benefit from it. I understand that this is something that AdviceBridge keep under review and in future they may remove some of these restrictions. In the mean time, if you aren’t sure whether you are eligible, it is well worth giving them a ring or contacting them via the website to ask (without obligation).

In my opinion, if your circumstances match their criteria, AdviceBridge are well worth checking out. I particularly like their £500 Plan+Implementation service, which covers not only researching and producing a retirement plan for you but implementing it as well. I would also seriously consider paying the extra £100 a year (or £10 a month) for the ongoing service. Obviously that brings the price up a bit further, but it is still far less than you would pay a traditional financial adviser for a similar service.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: This is a sponsored post for which I am receiving a fixed fee (but no commission). Please note also that I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and take professional advice as appropriate. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media: