I recently returned from a three-day break in Llanbedrog. This is a village on the Llyn (or Lleyn) Peninsula in NW Wales. It was the first time I had been to Llanbedrog, although I have holidayed in North Wales quite often.

This was also the first time I had stayed at an Airbnb property. I did try last year but was scuppered by the pandemic, so had a refund voucher I needed to use up. The place I stayed was a room/apartment attached to a private house, but self-contained with its own front door. I’ll say more about it below.

Llanbedrog itself is by the coast, roughly half way between Pwllheli (famed for its Butlins camp, now run by Haven Holidays) and trendy Abersoch. Here is a map of the area from Google Maps.

Accommodation

As mentioned, I stayed at an Airbnb property in Llanbedrog. Under Airbnb’s rules I’m not supposed to reveal exactly where it was, but the location was certainly convenient. It was about 100 yards from the main road and 150 from one of the two local pubs. The beach was around ten minutes’ walk away.

You can read more about the place I stayed on this page of the Airbnb website (you can also read my post about booking a holiday with Airbnb here). It consisted of a large bedroom-cum-sitting room, along with a bathroom with excellent walk-in shower. There was also a kitchenette area with a toaster, fridge, sink, coffee-making machine and so on, but no actual cooking facilities (there wouldn’t have been room for them). For a short stay that wasn’t a problem, though. On two nights my Airbnb host, Jem, kindly cooked main meals for me for a modest extra fee. And on the other night I went to the local pub, which was very good as well 🙂

My room had a stunning view across the hosts’ beautiful garden with the sea in the background (see photo below). Another thing I enjoyed was that the garden was home to a colony of wild rabbits. They looked very cute and provided an entertaining all-day cabaret!

The apartment had free wifi which worked perfectly during my stay (not always the case in my experience). The location was quiet and peaceful, and I slept very well.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £344.98 for my three-night stay. This was made up as follows:

£91.67 x 3 nights = £275

Cleaning fee £20

Service Fee (which goes to Airbnb) £49.98

I was charged an initial deposit of £112.50, with the balance taken from my card a fortnight before my visit. As mentioned, some of the cost was covered by a refund from a booking I made with Airbnb in 2020 which had to be cancelled.

So the total price worked out to £115 a day. Obviously that’s not cheap, but prices across the board have risen due to Covid and the additional cleaning and other precautions property owners have to take. I thought it was very reasonable bearing in mind the high standard of the accommodation and the convenience of the location.

Things to Do

I won’t give you a blow-by-blow account of what I did while I was there, but here are a few highlights.

Plas yn Rhiw

This National Trust property is about 7 miles from Llanbedrog. It’s pretty remote, and I was glad to have my satnav to guide me. At one point I drove through a tiny hamlet and some children waved at me as I passed. That was a first for me!

Plas yn Rhiw is a 16th century manor house (with Georgian additions) overlooking the sea. Unfortunately due to Covid only the ground floor was open to visitors. This was basically three rooms, all roped off so you had to look at them from a distance. As you may imagine, it didn’t take me very long to go round. I did though have a nice chat with the National Trust lady who was in the kitchen. She told me about the paraffin cooking range from the 1950s (see photo below). There must have been quite a smell in the house when this was going!

The house also has some beautiful formal gardens (see photo below). And, naturally, there is a tea room. I enjoyed an excellent cappuccino with a jam and cream scone here. As I chose to sit inside (it was raining a bit at this point) I had to complete a Covid tracking form. That was no great hardship, of course.

Overall I enjoyed my visit to Play yn Rhiw even though the restrictions were frustrating. I would like to go back there again when things are more normal and see the rest of the house.

Oriel Plas Glyn y Weddw

This gothic-styled mansion built in 1857 is in Llanbedrog and was five minutes walk from where I was staying.

Nowadays the building is used as an art gallery and museum. It also has an excellent cafe attached which I visited twice during my stay. It’s free to enter and certainly worth a visit if you are staying in the Llanbedrog area. The gallery hosts a permanent collection of Welsh porcelain (said to be among the finest in Wales) along with exhibitions of works by local artists.

Oriel Plas Glyn y Weddw also has some beautiful gardens and an outdoor theatre, which had some shows advertised for later in the year (though not during my visit). In the grounds there is also this carriage from the horse-drawn tramway which used to run from Pwllheli to Llanbedrog. Apparently this was a popular tourist attraction until the track was damaged by a heavy storm in the 1930s and subsequently abandoned.

Llanbedrog Beach

As mentioned, the beach (see cover photo) was about ten minutes’ walk from my apartment. It was sandy and quiet, and offered a perfect place for children to play. The beach huts were well maintained and picturesque. There was also a beach bar serving drinks and snacks all day (though not in the evening). I didn’t go here in the end as it was quite small and I felt a bit awkward about taking up a table on my own when families were queuing up. I did hear good reports about it, though, and it was certainly a lovely location (see photo).

Final Thoughts

As you may gather, I enjoyed my short break in Llanbedrog, and am happy to recommend both the town and the accommodation where I stayed for a short break. Llanbedrog is a lovely place to relax and chill out, and with its beautiful beach could also be a good destination for families with young children. Older children and teenagers might find the lack of other entertainments a bit limiting though.

As for me, this was the first time I had been away since last autumn. After many months of lockdown, I really appreciated the sea air and (mostly) sunshine, and of course the much-needed change of scene. I definitely plan to return there before too long.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

If you’re reading this post you will almost certainly know what an ISA is.

The term stands for Individual Savings Account. ISAs effectively serve as tax-free wrappers for various types of savings account. The two best-known types are the Cash ISA and the Stocks and Shares ISA.

You get an annual allowance for your ISA investments which currently stands at a generous £20,000 a year. Money saved in an ISA is permanently exempt from taxes such as income tax, dividends tax, capital gains tax, and so on.

So What Is An IFISA?

IFISAs are a lesser-known type of ISA that can be used for peer-to-peer (P2P) lending. They were launched in April 2016. After a slow start, the range available has grown steadily.

You can put any amount into an IFISA up to your annual ISA allowance. In the current 2021/22 tax year, as mentioned, this is £20,000. This can be divided however you choose between a cash ISA, a stocks and shares ISA, a Lifetime ISA (if eligible – you have to be under 40) and an IFISA. So, for example, you could invest £6,000 in a cash ISA, £10,000 in a stocks and shares ISA and £4,000 in an IFISA.

Note that under current rules you are only allowed to invest new money in one of each type of ISA in a tax year. It is though generally possible to transfer money from one type of ISA to another without it affecting your annual entitlement (although there may be platform fees to pay).

IFISAs vary considerably in the returns they offer. Annual rates range from from around 4% to 15%. Obviously, the higher rates reflect the higher levels of risk involved.

Although all IFISAs involve P2P lending, a number of different types are available. They may include lending for all the following purposes:

property development

business loans

personal loans

green energy projects

bonds and debentures

entertainment industry loans

infrastructure projects

What Are The Risks?

All UK IFISA providers have to be authorized by the Financial Conduct Authority (FCA) and HMRC. This doesn’t in itself protect lenders (or investors if you prefer) against the failure of a platform, however. While savers with UK banks and building societies are covered by the government’s Financial Services Compensation Scheme (FSCS), which guarantees to reimburse up to £85,000 of losses, this does not generally apply to IFISA platforms.

All IFISA providers do offer various safeguards, though. These vary, but include provision funds to cover potential losses, insurance policies, and so forth. In many cases loans are made against the security of property or other assets, which in the worst case could be sold to pay off any debts.

Even so, IFISA investors don’t enjoy the same level of protection in the UK as bank savers. This is, of course, a major reason why the returns on offer are significantly higher. It’s therefore important to be aware of the risks and ensure you are comfortable with them before investing this way. It’s also important to lend across a range of platforms and loans, and not make the mistake of putting all your savings eggs into one P2P lending basket.

What Are The Attractions?

So why might you want an IFISA? There are several reasons.

One is that they offer the potential of much higher rates of return that ordinary (bank) savings accounts. Even the best of these are currently paying interest rates of under 1 percent. IFISAs typically pay several times more than that (though obviously at somewhat greater risk).

Another big attraction of an IFISA is that it provides a way of gaining extra diversification for your portfolio. As mentioned earlier, the law currently only allows you to invest in one type of stocks and shares ISA per year. This rather perverse rule actually makes it harder to diversify your investments. But you can have an IFISA as well as a stocks and shares ISA, so long as you don’t exceed your total £20,000 allowance. So having an IFISA gives you a way of diversifying your investments while keeping them all protected within a tax-free ISA wrapper.

And finally, IFISA investments are typically not tied to the performance of stock markets in the way a stocks and shares ISA would be. This is a different type of investment, with different risks and rewards. While an IFISA won’t provide a way of hedging your equity investments directly, it is likely to be less directly affected by short-term fluctuations in the markets.

Two IFISA Examples

Two IFISAs of which I have direct experience are offered by Kuflink and Assetz Exchange. Both of these platforms offer tax-free IFISA options. They are both based around property investing.

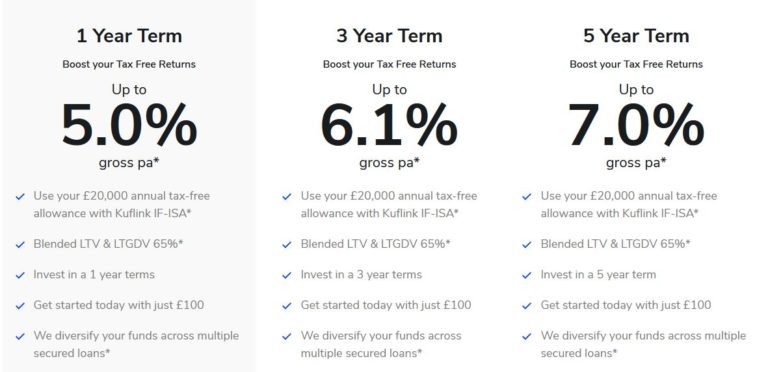

Kuflink – which I reviewed in this post – offers an automatically diversified IFISA comprising loans on property. They quote interest rates from 5% to 7%, depending how long you invest for. Your money is automatically diversified across a range of secured loans. The screen capture below from the Kuflink website sets out the main features of their IFISA.

One point to be aware of is that there is no ‘self-select’ option with the Kuflink IFISA. So you have no choice about which projects your money is invested in. But, of course, it does make investing in a Kuflink IFISA very quick and simple.

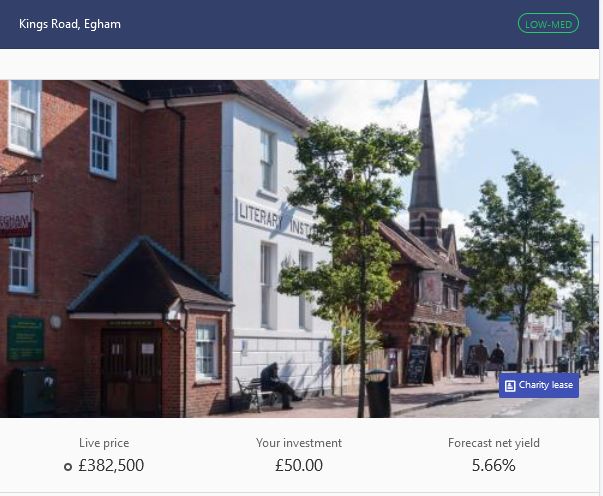

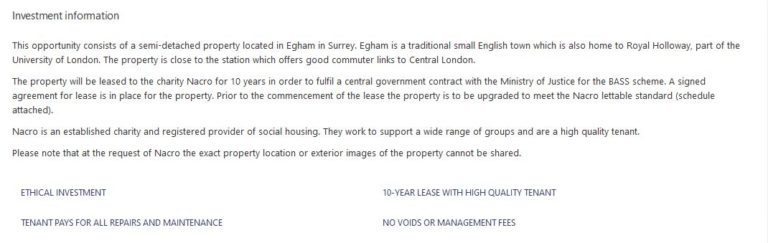

Assetz Exchange – which I reviewed in this post – has some similarities with Kuflink. But they concentrate on low-risk investments, typically with corporate clients (e.g. charities) on long leases. Here’s an example of the sort of investment I mean…

Assetz Exchange aims to offer net yields to investors of between 5.2 and 7.2% per year. One thing I especially like about them is that you can choose your own IFISA investments (indeed, they don’t currently offer an auto-select option). In addition, you can invest as little as 80 pence per project, making it easy to build a well-diversified portfolio even if you are only investing small amounts.

I am using Assetz Exchange for my 2021/22 IFISA, so here is a screen capture of my current portfolio for your interest. Note that while I have only invested £500 so far, I already have a well-diversified portfolio with 17 different investments!

Summing Up

If you are looking for a home for some of your savings that can offer better interest rates than banks and building societies and won’t incur any tax charges, an IFISA is certainly worth considering.

As well as the higher interest rates, they can add diversity to your investments, helping you ride out peaks and troughs in the financial markets.

Just be aware of the risks involved in P2P lending, diversify as widely as possible, and ensure you invest only as part of a well-balanced portfolio.

As always, if you have any comments or questions about this blog post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and speak to a professional financial adviser/planner if in any doubt before proceeding. All investments carry a risk of loss.

This post (and others on Pounds and Sense) includes my referral links. If you click through and make a qualifying transaction, I may receive a commission for introducing you. This will not affect the products or services you receive or any fees you may be charged.

If you enjoyed this post, please link to it on your own blog or social media:

Accountants are trained and experienced in all aspects of the tax system. They have both theoretical and practical knowledge of how the system works and how the (complex) rules are typically interpreted by HMRC. And they have to keep themselves up to date with the endless legal and procedural changes.

Also, unlike HMRC, an accountant is four-square on your side. They will advise you on the best way to organize your affairs to minimize your tax liability. They will answer any questions you may have, e.g. what records you need to keep. When the time comes, they will (if you want them to) compile your accounts and submit the relevant figures to HMRC in your tax return. And if any queries or problems arise, they will act on your behalf to try to resolve them.

A further benefit of having your accounts prepared by an accountant is that HMRC will know that a finance professional – someone who speaks their language – has compiled them. Other things being equal, this is likely to mean they will be more inclined to accept the figures and not dispute them.

Even if you aren’t self-employed or running a business, there may still be a strong case for getting an accountant to help with your taxes. Many older people, for example, have multiple streams of income, from stocks and shares to ISA accounts, property rentals to pensions. Some of this income may be taxable and some not, and varying tax rates and tax-free allowances may apply. Most accountants are more than happy to provide a service to people in this situation as well.

There is, of course, one drawback to engaging an accountant, and that is the cost. This will probably amount to a few hundred pounds a year (maybe more in some cases). Not to pay this, however, is in my view a false economy. A good accountant is likely to save you at least as much in unnecessary tax as they cost you. And the reassurance (and relief) of having a finance professional on your side when any queries with taxation arise is impossible to put a price on (but extremely valuable).

Of course, finding a good accountant who offers a service suitable for your needs isn’t always straightforward. And the amount they charge varies considerably. If you are looking for a keenly priced and easily accessible service, you might therefore like to check out what my friends at Simply Tax have to offer.

The Simply Tax Option

Simply Tax is a service run by professional accountants that provides a simple and inexpensive method for preparing and submitting tax returns to HMRC. They operate mainly online and are therefore able to keep charges to a bare minimum (starting from as little as £90). They say their service is for:

First time tax filers

Sole traders

CIS subcontractors

High earners (£100K+)

Landlords

Investors

Company directors

People living abroad

Anybody who needs a tax return

As the name indicates, Simply Tax aim to make the process of drawing up and submitting a tax return as simple as possible. In a nutshell, they say their procedure is as follows:

Create your free online account (just need your full name and email address)

Once verified, go into your user area and complete your personal information

Select the button to start your tax return (you’ll be taken to a screen to answer a few questions)

Once you’ve paid and been checked for your identification, simply drag and drop the information requested

We will do all the leg work and prepare the tax return for you

We’ll upload a draft tax return for you to review and approve electronically

Once you’ve approved, leave it to us to submit to HMRC

Although all of this is done online, you will be allocated a personal tax adviser whom you can contact at any time with any questions.

Simply Tax say their service will save you lots of time (they estimate between 70-80%) compared with filing your return yourself. They also estimate that their service is up to 50% cheaper than using a traditional high street accountant or tax advisor.

Finally, Simply Tax are fully regulated by the ICAEW (Institute of Chartered Accountants in England & Wales), providing added reassurance.

If you are looking for a straightforward, cost-effective way of preparing and submitting your annual tax return, in my view Simply Tax is well worth checking out. Okay, if you run a multi-million pound business empire it may not be for you. But if you are like most of us and just need a friendly, professional accountancy service who won’t charge an arm and a leg, they could certainly fit the bill.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Simply Tax. If you click through any of the links and make a purchase, I will receive a commission for introducing you. This will not affect the fee you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my April 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

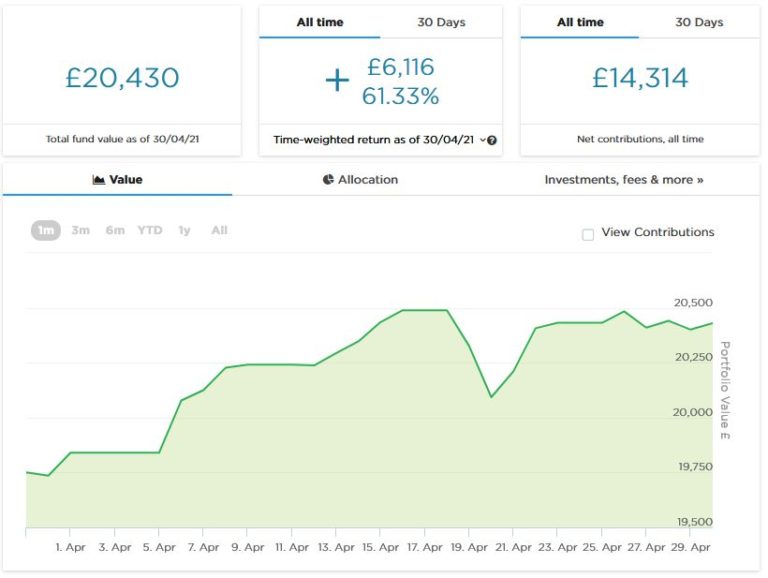

As the screenshot below shows, the value of my main portfolio rose fairly steadily in the first half of April, after which it remained around the same level (apart from a brief dip around the 20th). It is currently valued at £20,430. Last month it stood at £20,078, so overall it has gone up by £352. I am happy enough with that.

Apart from my main portfolio, five months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This has done pretty well, so in April I added another £1,000 from some money returned to me by RateSetter (as discussed in last month’s update). This pot is now worth £2,067. Here is a screen capture showing performance in April.

I updated my full Nutmeg review in April and you can read the new version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

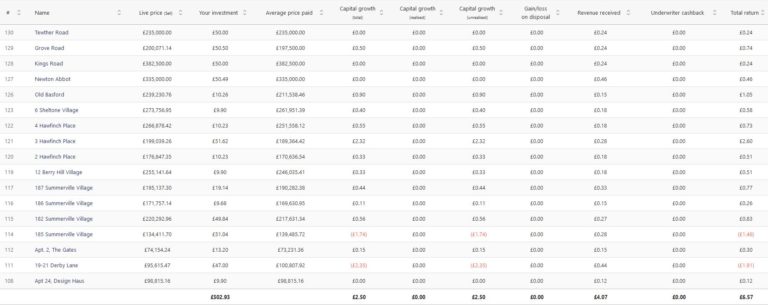

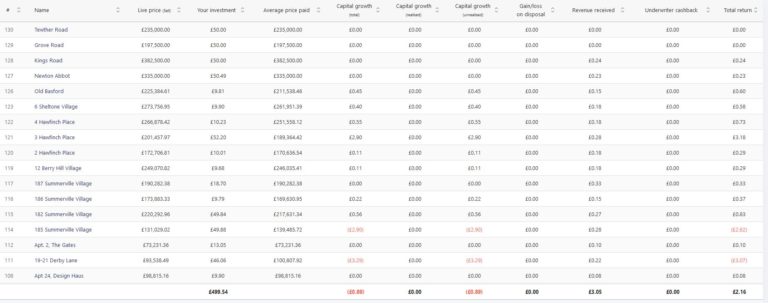

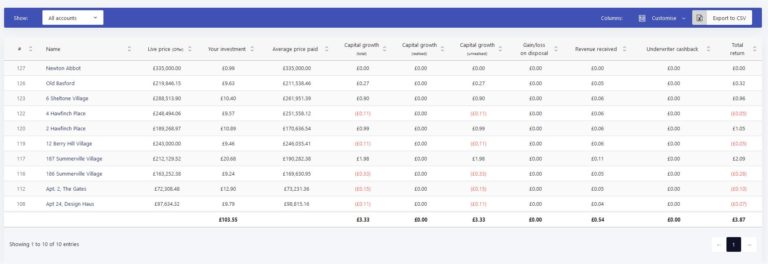

I also added £400 (from RateSetter again) to my initial test investment of £100 with Assetz Exchange. As you may recall, Assetz Exchange is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and (as mentioned) another £400 in April. Since then my portfolio has generated £3.05 in revenue received from rental (equivalent to an annual interest rate of about 10% on my original £100 investment). Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

You may also notice that some of the properties in my portfolio have gone up in value and some have gone down. This makes it a bit harder to judge overall performance compared with an equity-based investment like Nutmeg. The property values quoted by Assetz Exchange represent the best price you can sell at currently on the exchange, which is where all investments on AE are bought and sold. But they are only really relevant if you want to buy or sell that day. By contrast, Property Partner (a somewhat similar P2P property investment platform) quote a value for each property based on an independent surveyor’s valuation every 6-12 months. That means the values displayed on Property Partner are more stable, but of course they are only theoretical as there is no guarantee that this valuation would be achieved if the property was put on the market.

In case you’re not aware, everyone has a generous £20,000 tax-free ISA allowance in the current tax year (2021/22). However, for some reason the government only allows you to invest in one of each type of ISA in any particular.tax year. So you can only put new money into one stocks and shares ISA per year, but you can invest in a cash ISA and/or IFISA as well if you wish – just as long as you don’t exceed the £20,000 total limit. In the 2021/22 tax year I am therefore investing in a Nutmeg stocks and shares ISA and an Assetz Exchange IFISA. This gives me additional diversification compared with investing in just one type of ISA.

Moving on, I heard last month that I will not be eligible for any more SEISS income support payments for the self-employed. Along with many other self-employed people, my income took a hit when the pandemic struck and this money from the government came in very useful (though I do thankfully have a personal pension and other investments as well). However, I have become a victim of the rule that says to receive SEISS your average self-employed income must represent at least half of your total income.

For the first three rounds of SEISS that was indeed the case. However, the latest round of payments incorporates another set of tax returns (2019/20) when calculating average income. Because my income was lower in these accounts (partly due to the pandemic) my four-year average is now less than what I draw from my personal pension. So at a stroke I am no longer eligible for any more support. It’s not the end of the world, but I do find it bizarre that a scheme intended to support self-employed people whose livelihoods have been affected by the pandemic can cut off completely when your average income drops. Commiserations to any PAS readers who may have found themselves in a similar situation 🙁

Personal

In April, as I’m sure you know, some of the government’s lockdown restrictions finally began to be lifted.

I was glad to be able to go for a swim for the first time since Christmas, and have been doing so twice a week since it became possible again. I am a member of the David Lloyd Club in Lichfield which has two pools, one inside and one out. Although I’ve heard that you have to book slots at some swimming pools, that has never been the case at DL Lichfield, and in fact in many ways it feels reassuringly normal. Of course, you have to wear a mask as you enter the building, but thankfully not in the changing rooms or the pool 😀

I have just been told that if the pools get very busy, DL staff ask people to wait in the changing rooms until others have left. I haven’t witnessed this myself and don’t think it happens very often, but am happy to place this info on record.

What I do find bizarre is the rules about buying and consuming refreshments. The club room (aka coffee shop) at DL Lichfield is open for the purchase of drinks and light meals, but you can’t consume them within the building. You are, however, allowed to sit at a table in the club room (no need for a mask) to read and relax or just stare at the four walls. But heaven help you if you try to eat or drink anything.

I was told by a staff member that it was okay to take a drink to the outdoor pool as long as I was going for a swim, but not if I simply wanted to lie on a sunbed. Even though I am fast becoming a connoisseur of strange lockdown rules, this one seems barmy to me and I’d love to know how DL Lichfield plan to enforce it (“Unless you get in that pool in the next five minutes, I’m taking your coffee away.”). I’d like to support the DL club room/coffee shop, but the incomprehensible rules have defeated me. So I’m now taking a flask of tea and a biscuit with me and having that on the poolside or in the changing room after my swim. So far no Covid police have come for me.

I have also been pleased (and relieved) to have my hair cut again, six months after this was last done. Thankfully I didn’t have to queue up, as my hairdresser comes to me and cuts my hair in my conservatory. We have both had Covid jabs and agreed to dispense with masks and just kept the door and window open (thankfully it was quite a warm day). Again, it all felt reassuringly normal.

I haven’t so far taken advantage of the reopening of pub gardens, largely because it has been so cold (and wet) most days. It’s good to see at least some of my local pubs open again, but a shame they still aren’t allowed to open inside as well as out. Last year we had Eat Out to Help Out at a time when there were more Covid cases and deaths then there are now (just one death yesterday, I read). I am looking forward to May 17th when pubs and restaurants can reopen inside as well, but believe this has been delayed too long personally.

I am probably one of the few people who didn’t watch the Line of Duty finale. Indeed, I haven’t watched any of the series, as it didn’t really appeal to me. For one thing it sounded downbeat and depressing, and life has been grim enough recently. But also, it appeared a bit too complicated for my liking. Especially as i grow older, I find following series with large casts and labyrinthine plots increasingly challenging. I can remember laughing (affectionately) at my dad when he expressed confusion at the plot of some TV detective show, but I am obviously going down the same route myself now 😮

I have watched a couple of shows I enjoyed this month, though, so thought I’d share details in case anyone fancies giving them a try.

The first is an Amazon Prime Video series called Upload. This is a dystopian science fiction tale, set in a not-too-distant future when a method has been found for transferring people’s minds at the point of death (or before) to a virtual afterlife. This service is provided by a number of large corporations. They employ minimum-wage ‘angels’ in large warehouse-like offices to monitor these worlds and support the clients who live in them (at least, until their money runs out). It is quite a dark concept, but full of laugh-out-loud moments and some great characters. There is also a mystery in it, and a romance between a female ‘angel’ and one of her (deceased) male clients. It’s well worth a watch if you like something a bit different (and have Amazon Prime Video, of course).

I am also enjoying a US fantasy series called The Librarians (see below). I originally caught a couple of episodes on an obscure Freeview channel and decided I’d like to watch the whole (four) series from the beginning. Doing that proved a bit more challenging than I anticipated, but eventually I managed to track down a DVD box set on eBay.

The Librarians is a tongue-in-cheek fantasy series with a certain retro feel to it. It reminds me a bit of the old Avengers TV show in its heyday (with Diana Rigg as Emma Peel).

The Librarians are a group of misfits who are recruited to work at the mysterious Library, a place where magical artefacts of all kinds are stored. Early in the first series magic is released into the world again, having been suppressed for many centuries. In each episode the Librarians investigate some mysterious incident and try to stop evil individuals deploying magic for nefarious ends, generally using their intelligence rather than violence.

Again, it’s hard to explain in a few words, but you soon get the hang of things. And the characters, while perhaps excessively goofy at times, are all endearing in different ways. The Librarians is really old-fashioned family entertainment (with little if any swearing) and none the worse for that. If you can get hold of it – I’m not sure whether it’s on any streaming services – it offers an enjoyable (and at times hilarious) drop of escapism, something I guess many of us need at the moment.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

I have written about property crowdfunding on various occasions on Pounds and Sense. It’s a way for ordinary individuals to invest in bricks and mortar without requiring huge amounts of capital.

Why Property Crowdfunding?

Property investors get a double benefit – rent from tenants for as long as they own the property, and – in most cases – a profit if and when they sell.

Of course, property doesn’t come cheap. And even if you can stretch to buying a modest house or flat for investment purposes, you are taking the risk of putting all your eggs in one basket. As a result, many people of more modest means have concluded that property investment is not for them.

Property crowdfunding has changed all that, however. A number of platforms now exist that allow ordinary individuals the chance to buy a share (or fraction) in an investment property. Investors then receive a proportion of the rental income generated and also get a share of any profit when the property is sold (or refinanced).

A further attraction of property crowdfunding is that the platform (and its agents) take care of managing the property and tenants on your behalf. Unlike direct property ownership, property crowdfunding (or crowdlending if you prefer) is a genuine hands-free investment.

Brickowner Review

Brickowner is one of a number of property crowdfunding platforms that also includes Property Partner, Assetz Exchange and CrowdProperty. They allow investors to buy a share of individual property investments.

Brickowner focuses on institutional investments. They buy shares in large, high-return property investment deals that were traditionally only offered to institutions or high-net-worth individuals. They then offer smaller shares in these (a minimum of £500) to members wanting to invest in them.

How It Works

Before you can access the Brickowner platform, you will need to register on the site and confirm that you are allowed by law to invest in this type of product. This is a requirement imposed by the Financial Conduct Authority (FCA), which regulates this type of investment. In practical terms it means you will have to confirm that you meet one of the following descriptions:

High Net Worth Individual – This includes individuals who have an annual income of £100,000 or more or net assets of £250,000 or more and have made a declaration acknowledging the consequences of making investments based on financial promotions that have not been approved by an FCA-authorised firm.

Self-certified Sophisticated Investor – This includes individuals who have prior relevant investment experience and have made a declaration acknowledging the consequences of making investments based on financial promotions that have not been approved by an FCA-authorised firm.

Representative of a High Net Worth Body – This includes companies and partnerships with at least £5 million net assets and trusts with assets of £10 million.

Investment Professional – Including corporate investors and SIPP or SSAS professional service providers.

You will also be required to answer some questions to confirm that you understand the nature of the investments that can be made on the platform.

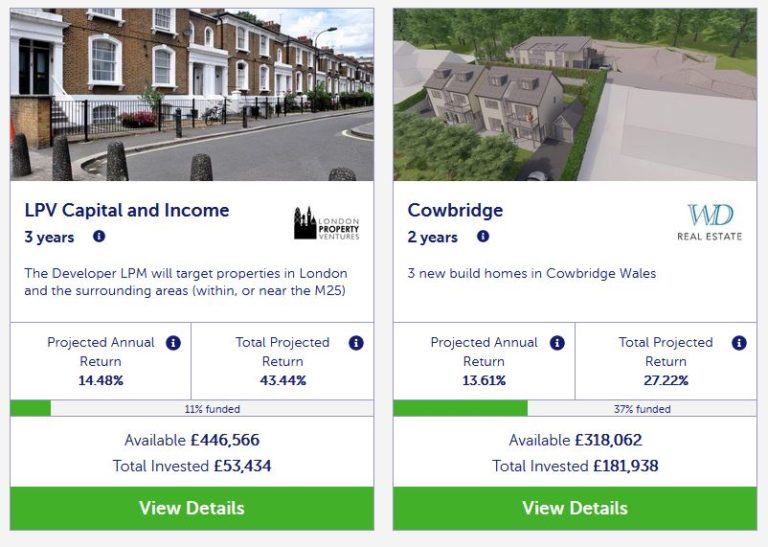

Once you are registered (and not before) you will be able to browse from the range of currently available property investments, such as the example below:

If you see a current project you like, you can invest in it, from £500 up to the maximum available. You can (and probably should) build a diversified portfolio by investing in a number of different properties. You can add funds and increase the size of your portfolio any time you want.

Investments have a fixed term: anything from one to five years. During that time you may receive dividends from any rental income received. These are added to your account and available to withdraw or reinvest. You also receive a share of any profits along with return of your capital at the end of the investment period.

In common with other property crowdfunding platforms, the pandemic has caused delays – in some cases a year or longer – to some projects on Brickowner, As far as I am aware no projects have failed completely, though.

Secondary Market

Brickowner recently introduced a secondary market where investors who need to release funds before the end of an investment term can put their share up for sale to other members. Here is a screen capture showing part of the secondary market currently.

As you may notice, some of the projects on the secondary market have less than £500 available. I asked if this meant you could therefore invest less than £500 in these cases, but was told no. Here is the exact reply I received:

£500 is the minimum investment in both the primary and secondary market. The reason there are smaller amounts on the secondary market is that there is a taxi-rank system, whereby available shares are listed and allocated in order of listing to a queue of buyers. So if I wanted to invest, say, £520 in Tamlaght, and there were no other prospective Tamlaght share buyers ahead of me BUT there were only £120 worth of shares available, I would have to wait until £520 worth of shares were available before my transaction went through. Prospective Tamlaght buyers in the queue would have to wait until my order had been filled before they moved forward in the queue.

In effect, then, you would have to place a bid for at least £500 of the project in question, and would have to wait till additional sellers materialized before getting anything. That is probably not ideal, but I can understand that Brickowner want to avoid the situation where some investors end up with tiny holdings in certain projects.

Charges

Brickowner fees are outlined within the property term sheet for each specific investment. There is no charge for depositing money with Brickowner, and no charge at the end of the investment period when your money and (hopefully) profits are returned to you.

My Thoughts

Brickowner offers an interesting option for people who want to add property to their investment portfolio. As mentioned above, there is a good case for doing this both in terms of dividends and capital growth, and to diversify your overall portfolio.

The Brickowner website is attractive and professional looking. One thing I have noticed is that most of their investment opportunities fill up very quickly. That is good insofar as it indicates that Brickowner is succeeding in attracting investors who believe in the proposition being offered. On the other hand, it does mean that at any particular time there may not be many (or any) projects to invest in. You will therefore need to build your portfolio gradually.

As mentioned above, Brickowner has a minimum investment of £500. This is not as low as some platforms (e.g. Assetz Exchange will let you invest as little as 80p) so it may be less suited to investors on a limited budget. But on the positive side, they are transparent about the fees they charge, and it is good that no fees are imposed for depositing or withdrawing money. It’s also good that a secondary market now exists for investors who wish (or need) to exit early.

As you can see from the screen capture above, the projected returns on investments with Brickowner are at the higher end for property crowdfunding platforms. Of course, this generally means the risks are higher as well. In any event it is important to read the financial information on each project carefully, to ensure that the investment aligns with your own needs and goals. Bear in mind also that some projects offer income as well as the potential for capital appreciation, while others aim for capital growth only.

During the coronavirus pandemic and lockdown, property transactions slowed considerably and many commercial property values in particular fell. However, there is clear evidence that a recovery is now under way. My own view is that there are good opportunities at present for property investors, but obviously in this uncertain time there are never any guarantees. Every investor needs to assess the situation carefully in light of their personal circumstances and tolerance for risk and proceed accordingly.

Investor Protection

The returns on offer from Brickowner are significantly better than you would get from a bank savings account at present, but clearly they don’t carry the same level of protection. For example, you are not protected by the Financial Services Compensation Scheme, which will refund up to £85,000 if a bank with which you have an account goes bust.

On the other hand, your money is invested in bricks and mortar, so it’s unlikely you would lose it all. A further level of protection is that – in common with other property crowdfunding platforms – your money is invested via an SPV (Special Purposes Vehicle). This is effectively an independent company with responsibility for the project in question. If Brickowner were to go bust, funds in the SPV would be protected and returned to investors once the property was sold.

Even if Brickowner were to go under before your money was invested, your funds are paid into a separate, ring-fenced client account. If the platform went belly-up the day after you sent the money, your funds would simply be returned to you.

Overall, then, whilst investing in Brickowner is clearly not as safe as leaving your money in the bank, the measures set out above do provide a reasonable level of protection (and reassurance). As with any investment, however, the higher potential returns on offer come with a greater risk of loss. In my view (and I’m not a qualified financial adviser, just an individual who has put thousands of pounds of his own money into property crowdfunding) Brickowner offers a reasonable balance between risk and reward. But clearly, you should invest only as part of a balanced portfolio combined with other, more liquid types of investment. .

If you would like more information about Brickowner and to set up an account, just click through any of the links in this post.

Disclosure: The links in this post are affiliate links. If you click through and set up an account at Brickowner and make an investment with them, I may receive a fee for introducing you. This will not affect the terms or returns you are offered. Please note also that I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Before making any investment it is important to do your own due diligence, and seek advice from a qualified financial adviser if you are in any doubt how best to proceed. All investment carries a risk of loss.

If you have any comments or questions about Brickowner or property crowdfunding in general, as always, please do post them below.

Note: This is a fully revised and updated repost of my original article about Brickowner.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at P2P property investment platform Assetz Exchange (launched in January 2019)..

As I have noted before on Pounds and Sense, I am something of an enthusiast for property investment (and specifically property crowdfunding). Among other things, I like the fact that you can make money from both rental income and capital growth. And investing in property can be a good way of spreading the risk when you have equity-based investments.

Of course, investing in property directly is costly and carries all the risk inherent in putting all your eggs in one basket. A major attraction of P2P property crowdfunding investment is that you can get started with much less money and build a diversified portfolio to help mitigate the risks.

In addition, if you invest this way you don’t have to deal with the day-to-day hassles of being a landlord, from finding tenants to repairing broken boilers. This is taken care of by the platform itself and/or their management company. You just have to sit back and – all being well – wait for the rental income and (hopefully) capital gains to materialize.

That said, there have been a few reversals in the P2P property sector over the last few months (see this recent post, for example). So I am now more concerned than ever to ensure that any investments I make in this category control risk as effectively as possible.

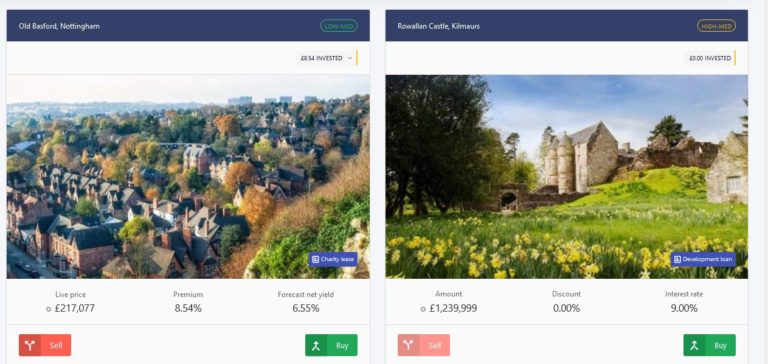

What Is Assetz Exchange?

As mentioned above, Assetz Exchange is a licensed P2P property investment platform. It is owned by well-known P2P lending platform Assetz Capital, but run quite separately from them. If you already have an account with Assetz Capital, you will have to register separately with Assetz Exchange.

Assetz Exchange aims to offer net yields to investors of between 5.2 and 7.2% per year. These are generally paid by institutional tenants through multi-year leases. All properties are unleveraged, providing additional security (and stability) for investors.

Assetz Exchange has some similarities with Property Partner, but they differ in some important ways. For one thing, many of the properties are rented out to charities (e.g. NACRO) or housing associations. These organizations generally sign longer contracts than private individuals. They don’t have voids (periods when the property is untenanted and producing no income). Neither are there any maintenance costs, as the organizations take responsibility for this themselves. And finally, these organizations are directly funded by the government, giving them a secure income stream.

Another area of specialism is show homes. Working with a national housebuilder, Avant Homes, Assetz Exchange purchases fully furnished show homes from multiple sites around the country. These are then leased back to the developer for fixed periods of up to five years to be used to help sell other plots. This eliminates potential void periods and avoids any maintenance costs. At the end of the leases, investors will be able to vote on whether to lease the houses to tenants or sell them to home-buyers on the open market.

Assetz Exchange also offers investors the chance to get involved with a new generation of modular eco-homes. This is already a popular approach to house-building in Europe and the United States. Assetz Exchange fund the acquisition and conversion of land into serviced plots, allowing buyers to then order a house to be built on that plot to their own specification. These modular-built eco-homes are sustainable and low energy. They are also typically quick to complete and have a lower impact on the environment.

Assetz Exchange do also buy and let some standard properties as well, offering investors the chance to further diversify their portfolios.

Signing Up

Before you can invest through Assetz Exchange, you will of course have to sign up on the platform. This is pretty straightforward. You just visit the Assetz Exchange website, read the information there, and click on Register in the top-right-hand corner.

You will then be required to enter your contact details and confirm which of four categories of investor you fall into. The options are as follows:

High Net Worth Investor – This includes individuals who have an annual income of £100,000 or more or net assets of £250,000 or more.

Self-certified Sophisticated Investor – This includes individuals who have made more than one peer-to-peer investment in the last two years or who meet certain other criteria relating to investment experience. This is the category I selected myself.

Investment Professional – Including corporate investors and SIPP or SSAS professional service providers.

Everyday Investor – This category is for investors who don’t fit into any of the categories above. They can still invest via Assetz Exchange but must pledge not to invest more than 10 per cent of their portfolio in P2P loans.

You will also be required to answer some multiple-choice questions to confirm that you understand the nature of investments that can be made on the platform. I found some of these questions quite challenging, and was pleased to get them all right first time. I would therefore recommend reading the information on the Assetz Exchange website (including the Help pages) carefully before proceeding to register. If you do make any mistakes, however, feedback is provided, and you can take the test again until you achieve a 100% correct score.

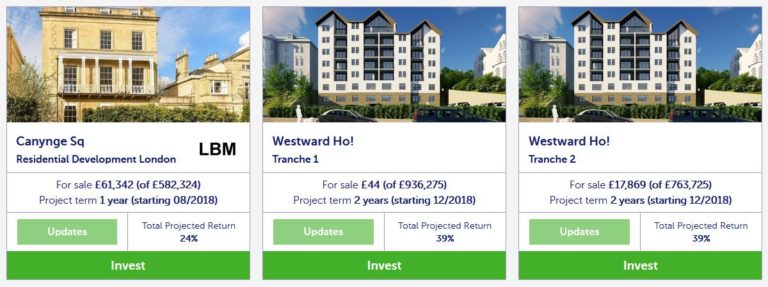

Once you have done all this, you will be able to fund your account. This must be done by bank transfer, as Assetz Exchange do not allow debit card payments. You will then be able to browse the range of currently available property investments:

Investing

Once you are registered on the platform and signed in, click on Exchange in the menu at the top of the screen and all current projects will be displayed. Here are a couple that are showing at the time of writing…

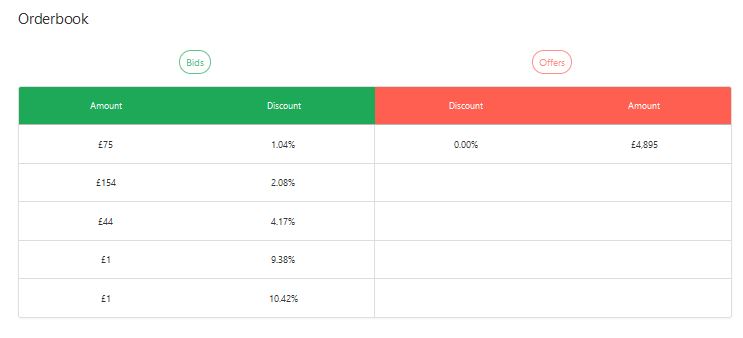

Clicking on any of these will open a page devoted to the investment concerned. Here you can read all about it, view reports and site plans, and so on. One very important area is the Order Book (see example below).

All buying and selling on the platform is conducted via an exchange (otherwise known as the Order Book) which works similarly to the secondary market on Property Partner.

So if you want to buy shares in a particular project, you can do so by accepting the best price currently available on the exchange. In the example above, there are £4,895 of shares available at zero discount (i.e. the original offer price).

If you want to get your shares at a lower price than this, you can make a bid. In the example, an investor has put in a bid for £75 at a 1.04% discount and another investor (or maybe the same one) has put in a bid for £154 at a 2.08% discount.

Conversely, if you wish to sell some or all of your shares at any time, you can accept the best bid (or bids) on the Order Book currently, or place an offer and wait to see if this is matched.

It does take a little bit of getting your head around at first, but it’s actually a simple and straightforward process. One thing to note is that if there is nothing showing on the right-hand-side of the Order Book (under Offers) you won’t be able to buy shares in that project there and then – though you can of course place a bid if you wish and see if a seller wants to match it.

In any event, if you want to buy, just click on the green Buy button (either on the Exchange page or the details page) and complete the short online form. You will need to indicate how much you want to invest, whether this should be from your General or IFISA account (see below), and whether the amount should include the FCC or not (see What Are The Charges? below).

You will also need to indicate whether you want to buy at the current best price (selected by default) or you want to try for a better price (in which case your bid will be added to the left-hand column in the Order Book).

The IFISA Option

As mentioned above, if you wish you can invest with Assetz Exchange via an IFISA (Innovative Finance ISA). As discussed in this recent post, this type of ISA for P2P investing gives you the same tax advantages as a cash or stocks and shares ISA. You don’t have to pay any tax on the money you make, whether this takes the form of dividends, income or capital gains.

Everyone has a generous annual ISA allowance of £20,000 in the current 2020/21 tax year (and next year as well). This can be divided any way you like among the three types of ISA. So if you open an Assetz Exchange IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. You can also only invest money in one of each type of ISA in any one financial year.

Choosing the IFISA option on Assetz Exchange is very easy. You can do it when first registering on the site or later. The only extra thing you have to do is enter your National Insurance number.

If you have maxed out your ISA allowance – or have already invested in another IFISA in the current tax year – you can still invest via your default ‘Regular’ account. You can invest any amount this way, but of course any profits you make will potentially be taxable.

What Are The Fees?

Assetz Exchange do not charge any monthly fees to investors (this is in contrast to Property Partner, who made the unpopular decision to impose an Assets Under Management charge and monthly fee, greatly impacting small investors on the platform especially). The company does have to make money somehow, of course, and they do this from three sources:

Arrangement fee

When a property is first purchased, Assetz Exchange charge an arrangement fee which is included in the Fixed Costs & Contingency (FCC). When parts of the property are sold on the Exchange, this fee is added to the purchase price of the buyer (see above) and so is recovered by the seller. The size of this fee is included in the loan conditions.

Monitoring fee

Assetz Exchange charge a percentage of the gross rent received for the property. The percentage is stated in the loan conditions of the property.

Property disposal fee

A fee of 2% of the gross sales proceeds is charged if investors vote to sell and the property is physically sold.

What Are The Safeguards?

Like most other property crowdfunding platforms, all investments in any project on Assetz Exchange are held in a Special Purpose Vehicle (SPV) for the project concerned. This gives investors in the project some protection if the main company were to go into administration.

A contingency balance is held within each SPV which acts in a similar manner to a provision fund, covering unexpected short-term cash-flow disruptions. It is topped up from receipts and no distributions are made to investors if it falls below a certain level.

SPVs also benefit from indemnity insurance which covers non-payments from tenants. This in theory also covers disruption to cash-flow, but it does not cover voids (periods where the property does not have a paying tenant). For reasons mentioned above, voids should not be an issue with most of the properties listed on the platform.

In common with most other P2P investment platforms, Assetz Exchange does not fall within the remit of the Financial Services Compensation Scheme (FSCS), which covers customers with UK financial services firms up to £85,000 if the institution in question were to go bust.

3. Low minimum investment (as little as £1 per project!) – this makes building a diversified portfolio straightforward.

4. Assetz Exchange take care of all the work involved in buying and managing properties. You just choose which ones to invest in.

5. Option to access money any time by selling on the secondary market (though this does depend on another investor being willing to buy your shares at a price you find acceptable).

6. Relatively low-risk investment options (though of course there are no guarantees)

7. Customer support (in my experience anyway) is fast, friendly and helpful.

8. Charges are reasonable. There is no charge for selling investments.

9. Potential to make money through both capital appreciation and rental income.

10. Rental income is paid into your account every month. You can either withdraw or reinvest it.

11. No monthly fees and only transaction-based charges to pay.

12. Opportunity to invest in socially beneficial developments such as sheltered housing

13. Tax-free IFISA option to which any investment on the platform can be added

14. Investors can vote for their favoured exit option (e.g. selling up) when the time comes

Cons

1. Can’t invest using a debit card

2. No auto-invest option currently available

3. Not as many opportunities as some P2P platforms (although the number is increasing steadily)

Closing Thoughts

I was impressed enough with Assetz Exchange to invest a small amount (£100) of my own money initially and will report back on PAS about how my portfolio fares. Here is how it’s looking at the time of writing, roughly a month after I opened my account. As you can see, my initial investment has grown by £3.87 from a combination of income received and capital growth. For a month that’s not bad at all – if it carries on growing at that rate I’ll be delighted! – but of course it is much too soon to draw any firm conclusions from this.

I particularly like the fact that with the low minimum investment on Assetz Exchange, even if you’re starting very cautiously (as I am) it’s easy to build a diversified portfolio. I like the relative simplicity of investing on the website and the fact that you can exit an investment any time via the exchange (though that does depend on willing buyers being available at a price that is acceptable to you). It is also good that there are no charges associated with selling on the exchange.

You can, of course, withdraw uninvested funds from your Assetz Exchange account at any time.

Obviously there are risks in any form of investing and it is important to do your own ‘due diligence’ before proceeding. You should also bear in mind that this type of investment is not covered by the Financial Services Compensation Scheme, which covers savers with UK banks and other financial institutions up to £85,000. On the other hand, the potential returns are significantly better than the fractions of a percent typically on offer from savings institutions right now, while the risks appear to be at the lower end of the spectrum, with many of the properties on long-term leases with corporate/institutional tenants.

To be very clear, nobody should put all their spare cash into Assetz Exchange (or any other investment platform for that matter) but in my opinion there is definitely a case for including AE within a diversified portfolio.

As mentioned above, I shall be reporting back on how my Assetz Exchange investments perform on PAS in future. In the mean time, if you have any comments or questions about this post, or Assetz Exchange more generally, please do leave them below as usual.

UPDATE JANUARY 2025 – Assetz Exchange have now rebranded as Housemartin. They continue to operate as described above, but going forward will focus entirely on supported housing projects, as these have proven the most reliable and hassle-free (not to mention the social/community benefits). For more info, see my new blog post P2P Property Investment Platform Assetz Exchange Rebrands as Housemartin.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always perform your own ‘due diligence’ before making any investment and speak to a qualified professional adviser if in any doubt how best to proceed. All investments carry a risk of loss.

Please note also that this review uses my affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect any charges you pay or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

At the time of writing there is just over a fortnight till the end of the 2020/21 ISA season. That is all the time you have left to make use of this year’s allowance of £20,000 before it is gone forever.

If you haven’t already used your allowance – and you have money available to invest – it is therefore essential to take action now. Investing via an ISA means that any profits you make will be free of Income Tax, Dividends Tax or Capital Gains Tax. And you won’t even have to declare it on your tax return, which if you’re anything like me will be a welcome simplification…

You can of course put your money into a Cash ISA, but the rates of return on such accounts are currently derisory, and basic rate taxpayers now have a £1000 tax-free savings allowance anyway (higher rate tapayers get £500 and top rate taxpayers nothing at all). The argument for investing in a cash ISA is therefore weak for most people, although if you think interest rates are likely to rise significantly in future there might still be a case for using one. Count me out, though 🙂

That leaves Stocks and Shares ISAs and the relatively new Innovative Finance ISAs (which are mainly for P2P lending). You can invest in either or both of these ISAs up to your annual £20,000 limit, though you can only put money into one of each type in any tax year. In today’s post I wanted to reveal some ways you may be able to get an extra cash boost if you plan to invest in an ISA in the next couple of weeks.

Cashback Sites

I have mentioned cashback sites on various occasions on Pounds and Sense. Basically, these sites refund some of the commission they receive from ‘introducing’ you to a company if you click through to it via a link on the cashback site. The two best-known cashback sites in the UK are Top Cashback and Quidco, though newcomers My Money Pocket are also worth joining and checking out. You might also like to try Cashback Angel, a comparison service for UK cashback websites, which I reviewed here recently.

Clearly you will need to sign up for an account with a cashback site before you can get any cashback from them. I highly recommend registering with Quidco and Top Cashback and maybe My Money Pocket too, even if you aren’t planning to invest in an ISA immediately.

So what cashback offers are currently available with ISAs? On Top Cashback (my personal favourite) one of the best comes from Fidelity. They are offering a maximum of £160 cashback if you open a new Fidelity Stocks and Shares ISA with a minimum deposit of £15,000. But even if you begin with as little as £2,500, you will get £50 cashback. You have to be a new customer and remain invested for a minimum of three months to get the cashback.

If you invest in a Shepherds Friendly Stocks and Shares ISA, an even more generous top payment of £305 is on offer for a maximum £20,000 ISA investment. Or you can earn up to £300 cashback if you set up monthly deposits, though to get this amount you will need to put in £1,500 a month or more. Again, you must remain invested for a minimum of three months to receive the cashback.

Over on Quidco there are also some great offers. With Foresters Friendly Society, for example, at the time of writing you can get £244 cashback with a maximum £20,000 investment. Or you can get £40 cashback with a minimum initial investment of £5,000 (other options are available as well). Again, you must remain invested for a minimum of three months to receive the cashback.

Please be aware that cashback offers change frequently, so I can’t promise that the exact offers mentioned above will still be available by the time you read this post.

For more ideas, just browse the Investment category on either Top Cashback or Quidco. Alternatively – or in addition – you can try searching for any ISA provider you are interested in to see if they have a cashback deal on offer.

Obviously you shouldn’t invest in an ISA purely for the cashback. But if you are thinking of doing so anyway, it is well worth checking what deals are available on cashback sites to get the benefit of the extra money available.

Special Offers

Of course, all investment platforms know that now is a peak time for ISA investment, so they compete extra vigorously to attract new customers. It is therefore well worth shopping around right now to see what offers are available.

In addition, as an ISA investor and money blogger myself, I have access to some special deals and bonuses that I can offer my readers. I’ve put a couple below, both with ISA providers I have invested with personally.

Kuflink

Kuflink is a P2P property loans platform I have been investing with for around three years now. They offer a range of investment options, including an IFISA. They have a generous welcome offer, where you can earn up to £4,000 cashback on a £100,000 investment. Of course, that’s well over the ISA annual limit. But if you invest £20,000 in an IFISA with Kuflink you can get 3 percent cashback or £600, which still isn’t too shabby. For more information about Kuflink and their welcome offer, check out my Kuflink review.

Nutmeg

Nutmeg is a robo-adviser investment platform I have been investing with since 2016. As you will see from my Nutmeg review, I have enjoyed very good returns from them (55.5% to date). They offer a Stocks and Shares ISA using ETFs (Exchange Traded Funds). If you sign up with Nutmeg via my link, while I can’t offer you a cash bonus, you will get six months’ portfolio management free of charge.

I hope this post has encouraged you to use your 2020/21 ISA allowance before it’s gone and maybe take the chance to pocket a bonus or cashback as well. If you have any comments or questions, as always, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss. In addition, please be aware that some links in this post include my affiliate (referral) code, so if you click through and make a purchase, i will receive a commission for introducing you. This will not affect in any way the terms and benefits you receive,. Indeed, as stated above, some offers are only available to people investing via my link.

If you enjoyed this post, please link to it on your own blog or social media:

FI Money (as I’ll call it for short from now on) is a self-published paperback of 222 pages (it’s also available as a Kindle ebook). It is organized into 28 main chapters plus additional material. I won’t list all the chapters here, but here are the first ten to give you a flavour of the content (and style).

Force yourself to smile

YouTube obsession

Your relationship with money

Overthinker

Understanding our ‘Chimp’ emotions

Goals written down

Crystal clear goals

Stress less

Mental training

How NOT to invest

FI Money is a personal account of one man’s journey towards financial independence (the FI referred to in the title). It is a self-development book, but as Peter says in the Introduction it isn’t the usual success story typically associated with such books. He says, ‘I am a work in progress, similar to a building under construction.’

The chapters are generally quite short. They are well written and broken up with bullet-points, headings, To Do lists, and so on. Peter focuses on different aspects of his quest for financial independence, with a particular emphasis on buy-to-let. As this is not something I have ever got into myself (apart from some investments on property crowdfunding platforms) I was particularly intrigued by this. Peter talks about his experiences with refreshing honesty and is not afraid to disclose some of the mistakes he has made along the way. If you’re thinking of investing in buy-to-let yourself, there are some valuable lessons to be learned here.

The book covers many other subjects as well, including property renovation, tax, investing, keeping records, and more. I particularly enjoyed Chapter 10 ‘How NOT to Invest’ which focuses on some of Peter’s less successful investments. These include Premium Bonds (like me he’s not a fan), Bitcoin and other cryptocurrencies, and a particularly ill-advised buy-to-let project early in his career. There are some salutary lessons to be learned from all this (and a few laughs to be had as well!).

In addition to the practical advice, FI Money has a particular emphasis on the psychological aspects of achieving financial independence – the money mindset, as Peter calls it. He is a firm believer in building your financial knowledge, but also adopting the right emotional and practical disciplines and carefully planning and managing your journey towards FI. There is a lot of food for thought in the book from someone who really has been on this particular journey himself (or at least is well on the way there).

As mentioned earlier, Peter also runs a personal finance blog called Duffmoney. This is well worth a read as well, and will give you a flavour of Peter’s style and his attitude towards investing and money matters generally.

As always, if you have any comments or questions about this review, please do post them below.

Disclosure: In common with many posts on Pounds and Sense, this review includes affiliate links. If you click through and make a purchase, I may receive a fee for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest monthly Coronavirus Crisis Update. Regular readers will know I’ve been posting these updates since the first lockdown started a year ago now (you can read my February 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

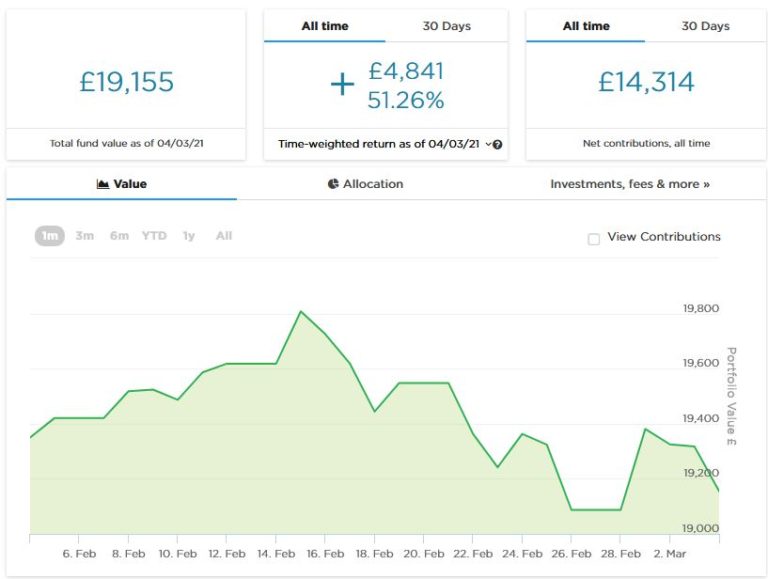

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,155. Last month it stood at £19,008, so it is at least up a little (£147) overall.

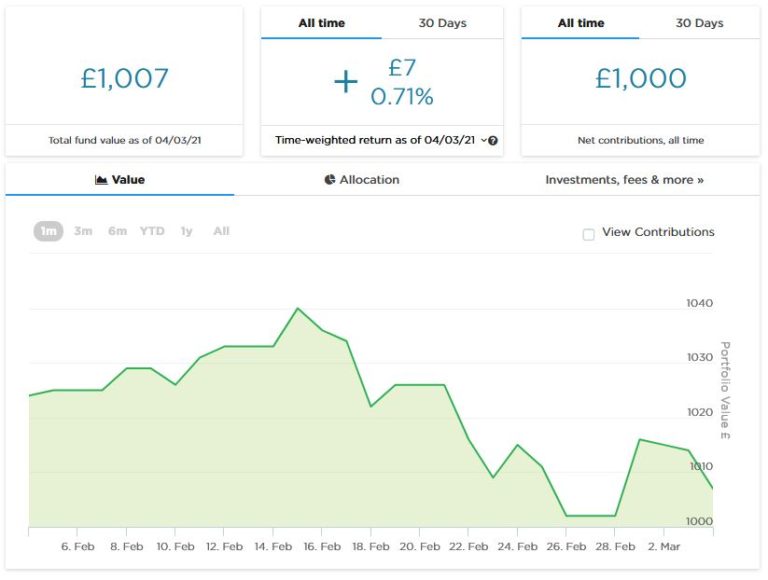

As you may recall, three months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,040 in mid-February, though it currently stands at a more modest £1,007. Here is a screen capture showing performance to date, though obviously it is much too early to draw any conclusions from this.

I mentioned last time that my first investment with P2P property investment platform Property Partner reached its five-year anniversary, at which point investors can vote to sell their shares or continue for another five years. Along with just under half of the other investors, I voted to sell my shares.

The shares of everyone who wanted to sell were duly put up for sale on the platform. Unfortunately, though, there were few buyers, so with a substantial number of shares unsold, the property has been put up for sale on the open market. That means there will be a period of several months – possibly longer – before a buyer is found, and there is no guarantee that the independent valuation price will be achieved.

That is obviously disappointing, though as I only have a very small amount invested in this property (about £50) I’m not going to lose any sleep over it. In my view Property Partner didn’t make much effort to market these shares to investors. I suspect the same may be the case with at least some of the other properties coming up to their five-year anniversaries. It may be that Property Partner are happy to get some of the smaller houses and apartments off their books, especially the city-based ones for which demand has fallen as a result of the pandemic. Currently I have another small investment going through the five-year process. I voted to sell my shares in this too, but suspect the outcome will be the same.

As I have noted before on PAS, shares in many properties on Property Partner are currently available on the secondary market at a discount to the independent valuation price Based on my experiences to date, however, I would advise caution about regarding this as a buying opportunity. If properties that are relisted attract little interest from existing PP investors, they will have to be sold on the open market. In that case you are likely to have a long wait until you see any return on your investment, and there is no guarantee of an overall profit even then. I shan’t therefore be investing on the Property Partner secondary market for the foreseeable future.

That wasn’t the only disappointing financial news last month. Property crowdfunding investment platform The House Crowd unexpectedly announced that it was going into administration. I still have some investments with THC, though thankfully not as many as I did two or three years ago.

Apart from one small loan – which I accepted some time ago had gone south – my remaining investments are in traditionally crowdfunded properties, all of which are currently up for sale. The money is therefore secured by bricks and mortar, so I expect to get at least some of it back (and have of course been receiving dividend payments from rent received). As with other property crowdfunding platforms, each THC property is owned and managed by a separate Special Purpose Vehicle (SPV), which gives it legal protection from claims against THC by creditors. How this will pan out in practice remains to be seen, but I note that the administrators have said that their appointment is ‘not expected to have a material impact on investors.’

So I am being philosophical about this and awaiting further developments. These have undoubtedly been tough times for property investors, and regular readers will know that I also recently lost money with another property crowdfunding platform called Crowdlords. Overall, when you allow for my successful property investments and rental income, I am more or less breaking even, but even so (as I have said on the blog before) I am a lot more cautious about this type of investment nowadays.

Personal

February was another long, cold month, but at least there are signs of better times ahead now. The vaccine roll-out continues to go well and case numbers are dropping rapidly, giving us all hope for a return to something approximating normal life in the weeks and months ahead.

And, of course, we are heading into the spring now, with longer, brighter days and – eventually – the prospect of some warmer ones!

One thing that always lifts my spirit at this time of year – and especially in the current circumstances – is the arrival of spring flowers. In my garden I have crocuses and snowdrops out at the moment, and it won’t be long until the daffodils are in bloom. Here’s a photo of a flower bed in my front garden…

I had my first Covid jab in February, at the Whitemore Lakes mass vaccination centre near Lichfield. It was run by a team of NHS staff, military and volunteers. Everyone was friendly and efficient. The only slight blip came when I was checking in. I happened to notice that the clerk had put ‘female’ on my form, doubtless due to my lockdown hair. She was embarrassed when I pointed this out, but of course I couldn’t just say nothing. I shall be very pleased when we are allowed to visit hairdressers again!

I received the Oxford-Astra Zeneca vaccine. After I had a bad reaction to my last flu jab (fever and nausea) I was prepared for something similar with this, but thankfully that didn’t happen. Apart from very slight soreness in my arm the next day, I had no side-effects at all. I hope I am just as lucky with my second jab, which I have already booked for May.

Also on a medical theme. I had my latest trip to the eye clinic at Queens Hospital Burton last week. Regular readers will know that last autumn I was diagnosed with a perforated retina in my left eye. My first laser treatment was only partly successful, so Iast time I received a (more powerful) top-up treatment. This visit was to check if it had been successful, and I was pleased and relieved to hear that it had. So once again I need to express my thanks and gratitude to all the staff there, and especially to Mr Brent, the consultant who performed my final laser treatment and gave me the good news this time. I have been told that if something like this happens once it increases the chances of it happening again, so I have to be on the lookout for any potentially worrying changes to my eyesight in future. But that aside I am lucky that this problem was detected early before anything more drastic (e.g. a detached retina) occurred – so big thanks to my optician at Vision Express Lichfield as well!

As I write this update, the schools are just about to reopen to all students. I am delighted about that, as I know that it has been a tough time for many children. While some schools have been very good about running online classes, these can never be a complete substitute for face-to-face teaching. I also know from speaking to friends that some schools have been less supportive, simply sending pupils written lessons or assignments to complete on their own. That is obviously less than ideal for younger children especially.

I do think it is regrettable that the government has advised that secondary school children should wear masks in classrooms. The same applies to the mandatory twice-weekly testing. In my view these measures will achieve little apart from traumatizing young people and making it harder for them to learn. I understand these measures have been introduced partly to placate the teaching unions and some worried parents, but hope they will be swiftly withdrawn when (as I fully expect) there is no big ‘spike’ in virus cases following the return. Okay, I’ll get off my soapbox now!

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

The world is an expensive place, so it’s no wonder many people are obsessed with getting freebies.

However, when entering the freebie-hunting world it is important that you adhere to certain rules in order to make the most of it. This article will set out some top tips for novice freebie-hunters – and you may learn a thing or two as a seasoned freebie-hunter as well.

If It Sounds Too Good To Be True, It Probably Is

The excitement of (potentially) getting a freebie from a favourite brand can easily cloud your judgement.

According to Karen Newman at Mega Free Stuff, the majority of transactions have both an upside and a downside; however, when a transaction is free the downside is temporarily forgotten. ‘Free’ provides people with a strong emotional charge, where the individual perceives the item on offer to be more valuable than it actually is. This basically means that the person will set aside common sense if they are being offered a freebie.

Some companies are willing to give freebies, but fans of a brand are often willing to sell their soul (or at least provide all sorts of valuable personal information) in exchange for a minute sample. This is detrimental, and it is essential that you know how big the sample is and what exactly you will be getting. Be sure the freebie is genuine and always read the terms and conditions before applying for any offers.

If You Do Not Ask, You Will Not Receive

It is always worthwhile writing letters or sending emails to companies asking if they have any samples available for you to try. This may seem obnoxious and pointless to some, but those who complete this task have often received large boxes of free items or discount vouchers from the companies as a means of gaining feedback on their products. Furthermore, if you do not like a product, be honest about this. In many cases companies are happy to offer replacement freebies (plus an extra item) if their products do not meet with the user’s approval.

Do Not Expect Too Much

A full-sized freebie is a rare occurrence, with the majority of free products being delivered in small envelopes or tiny sachets. Of course, the primary goal is not to obtain a full-sized freebie but a free sample to see if you enjoy the product for a future purchase.

Furthermore, do not expect to receive all free items applied for. Even if you have claimed a free sample noted as available online, it is unlikely that you will get a 100% return. In fact, the most you can expect is approximately 70%. Do not give up hope and keep applying, and soon you will be enjoying masses of freebies. Once again, though, be sure to check that any freebie is worthwhile, and always read the terms and conditions regarding the size and number of samples.

Do Not Feel Guilty