Today I am looking at The Good Retirement Guide, an annual guide published by Kogan Page. I bought the current 2021 edition, which was published last month.

The Good Retirement Guide 2021 is 318 pages long. The text is fairly dense but broken up by plenty of headings and bullet-point lists. There are 14 chapters and an alphabetical index at the back. The chapter titles are as follows:

Are You Looking Forward to Retirement?

Money and Budgeting

Pensions

Tax

Investment

Your Home

Leisure Activities

Starting Your Own Business

Looking for Paid Work

Voluntary Work

Health

Holidays

Caring for Elderly Parents

No-one is Immortal

The chapter titles are pretty self-explanatory. The book attempts to cover every aspect of making the most of your senior years. The style is clear and readable, and additional resources are signposted as appropriate.

In contrast with Sod 60! which I also reviewed recently, The Good Retirement Guide covers the financial aspects of later life in some detail. I thought the information about pensions and benefits in particular was very good and tells you most of what you need to know.

Some of the other chapters are a bit less comprehensive. The one on leisure activities, for example, lists various things you might like to do – or take up – in retirement, but the information is frequently sketchy and can verge on stating the obvious. Here is what it has to say about poetry, for example:

There is an increasing enthusiasm for poetry and poetry readings in clubs, pubs and other places of entertainment. Special local events may be advertised in your neighbourhood.

And apart from a mention for the Poetry Society and a link to their website, that is all you get on this subject 🙂

I don’t want to appear too harsh. Obviously in a wide-ranging book like this, it can be hard to judge the degree of detail appropriate to any particular topic. At least by mentioning a wide range of possibilities, the book may give you some ideas about activities you might like to pursue further in retirement.

The health-related content is a bit of a mixed bag. Some subjects are covered in reasonable depth, others less so. There is just half a page devoted to keeping fit, for example, with a further couple of paragraphs about yoga and Pilates. On the other hand, there is some good information (and advice) on health insurance, long-term care plans, and so forth. Again, this illustrates that the book’s primary focus is on the financial aspects of retirement.

One thing that did surprise me is that although this 2021 edition of The Good Retirement Guide was only published last month, there is no mention of the pandemic in it. You will search in vain for Coronavirus or Covid-19 in the index. I know there can be long lead times in publishing, but in an annual guide you might think they could have inserted a section about it somewhere. Maybe we will have to wait for the 2022 version?

Even so, a lot of the subjects discussed in the guide – holidays, for example – have been seriously impacted by the pandemic. The advice and procedures for travel abroad in particular may be very different even after the pandemic is officially over.

Final Thoughts

Overall, I thought The Good Retirement Guide 2021 was a helpful book for people approaching retirement. As I’ve said above, it has a strong emphasis on financial matters, and is well worth reading for that alone. Some of the other content is a bit hit-and-miss, and the surprising lack of any mention of the pandemic means that at times it reads like a guide to an alternate world where Covid never happened. Of course, none of us really knows what the ‘new normal’ will be in future. We can but hope it will be not too far removed from the old normal we remember and which this book – despite the 2021 in its title – basically depicts.

As always, if you have any thoughts or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

In brief, Property Partner is a property crowdfunding platform. For the most part they specialize in ‘traditional’ property crowdfunding rather than loan or development finance.

Properties are bought and managed by Property Partner on investors’ behalf. Investors then receive a share of the rental income as dividends, and a share of any profits (plus return of their capital) when the property is sold.

Property Partner launched in January 2015. That date is significant, because after a property has been on the platform for five years, all investors get the chance to exit at a fair market price (determined by an independent surveyor). Due to the pandemic the five-year anniversary process was temporarily put on hold, but it is now proceeding again, albeit with delays as they work through the backlog.

How it operates is that in the run-up to the fifth anniversary of a property, all investors have the opportunity to say if they want to exit their investment at the valuation price or stay on for another five-year term (less than this if they subsequently exit via the resale market, of course).

All investors who have opted to leave will then have their shares pooled and put up for sale on Property Partner at the price stated. New investors are then able to buy these shares.

So long as all shares are sold, the original investors get their money (including any net profits) and the property continues under Property Partner’s management. If all shares don’t sell, however, Property Partner offer the property for sale on the open market. Investors then have to wait until the property is sold before getting their money back. As anyone who has been involved with buying or selling property will know, this is likely to take several months (quite possibly longer in the current circumstances).

The Opportunity

As Property Partner themselves have been pointing out, a number of properties that are coming up to their fifth anniversary are currently trading on the resale market at well below their latest valuation. Here is just one example:

This property in Tower Hill, London (not one I own shares in myself) is due to go through the fifth-anniversary process in April 2021 (or possibly a bit later due to the backlog). At the time of writing shares are available on the secondary market at a price of 91p, which is 28.28% below the latest valuation of £126.88. In theory, then, you could buy shares now and in the next few months sell up for a substantial short-term gain.

Of course, in practice it’s not as simple as that. Here are some reasons:

Nobody knows yet what the final five-year valuation will be. If it is lower than the current valuation (which is perfectly possible in the current economic climate) the net profit will be reduced, perhaps substantially.

There is no guarantee that the shares of all investors who wish to exit will actually sell on the platform. If they don’t, as mentioned, you could have a long wait before the property is sold on the open market. In addition, if this happens there is no guarantee that the property will sell at the valuation price. If it goes for less than this, your returns will be reduced accordingly.

There are platform fees to take into account. In particular, there is a 1% fee for buying on the secondary market and a further 0.5% stamp duty reserve tax charge. Thankfully there are no exit fees, though.

And finally, the number of shares available for any property on the secondary market is limited. Obviously the number you can buy depends on how many shares other investors want to sell at the price in question.

On the plus side, for the length of time you hold the shares you may receive monthly dividends at a rate between 1.5% and 6% per year (though dividend payments on some properties are currently suspended due to Covid). This will offset the fees mentioned above; but if you only intend to hold the shares for a few months it probably won’t cover them completely. Bear in mind that an Assets Under Management (AUM) fee is now deducted from dividends as well.

As an investor with Property Partner since almost the beginning (the cover image shows a property in Torquay I own shares in – I plan to retire there one day 😀 ), I am awaiting the five-year exit for my investments with considerable interest.

My personal circumstances have changed since I started investing with the platform, so I intend to take the opportunity to offload at least some of ‘my’ properties. Indeed, I have already voted to sell my shares in the first property I ever invested in with Property Partner (20 Phillimore Close) and am waiting to see how this pans out. I will update this post in due course once I know.

Nonetheless, I am still considering investing short term on the resale market to take advantage of the opportunity the five-year anniversary presents. In particular, I have already topped up my investments in some of the properties I already hold but am planning to dispose of.

I will, though, be cautious until I have a better idea how the first few five-year anniversaries have passed, so I can see if all shares put up by investors sell on Property Partner, or if they have to sell the properties concerned on the open market. As mentioned earlier, the latter route will clearly take longer and there is no guarantee what price would be achieved.

Would I recommend someone who is currently an investor in Property Partner to look into this? Yes, certainly. Whatever your current circumstances, you need to be aware of what is going on with any properties you hold with Property Partner. And if you wish to sell, you should definitely consider taking advantage of the five-year exit mechanic. Equally, if you have money available to invest, you could check out the opportunities buying now on the resale market – though do bear in my mind my cautionary comments above.

If you haven’t joined Property Partner, and you like the idea of investing some of your portfolio in property, the platform is certainly worth a look. As older properties come back on the market for new investors, there will be no shortage of opportunities in the months ahead. And my understanding is that, as the original costs of acquisition have been amortised, there will be less costs to cover from investors, thus boosting the potential returns from the properties in question.

In addition, as these properties have a five-year history already, you will be able to check how they have been performing in terms of dividends generated and capital appreciation. This is no guarantee of how well or badly they will do in the future, of course.

Take a look at my Property Partner review for much more information about the platform and how it works. Also, if you do decide to invest in Property Partner, there is a welcome bonus offer. For convenience I have copied details below from my review.

Welcome Offer

As an existing Property Partner investor, I can offer a special bonus for anyone joining via my link. If you click through this special invitation link, sign up and invest a minimum of £2,000 within 60 days, you will receive an extra bonus as follows (and so will I):

Not only that, once you are an investor with Property Partner, you will be able to offer the same bonus to your friends and relatives and earn commission yourself. There is no limit to the number of people you can introduce through this scheme.

If you have any comments or questions about this post, as always, please do leave them below.

Note: This is a fully updated version of a post published in 2019.

Disclosure: this post includes referral links. If you click through and make an investment, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. Be aware that all investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest Coronavirus Crisis Update. Regular readers will know I have been posting these since the first lockdown started in the spring of 2020 (you can read my January 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

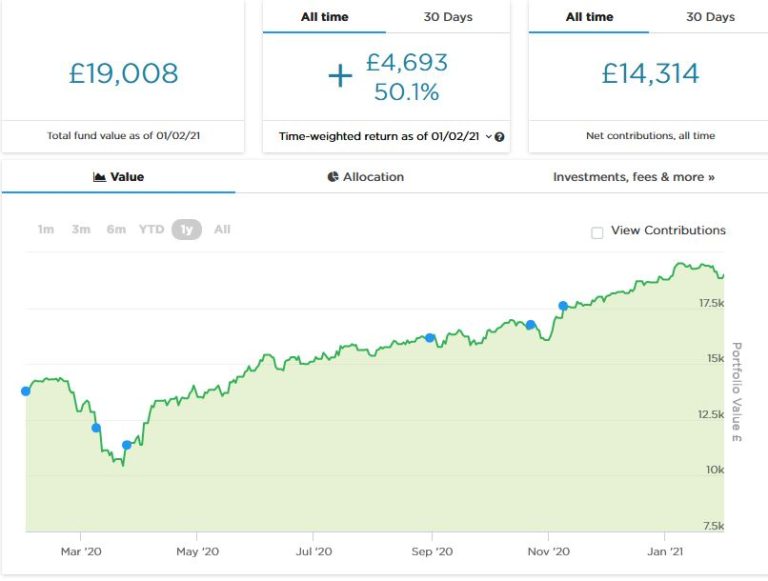

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,008. Last month it stood at £18,886, so it is at least up a little (£122) overall.

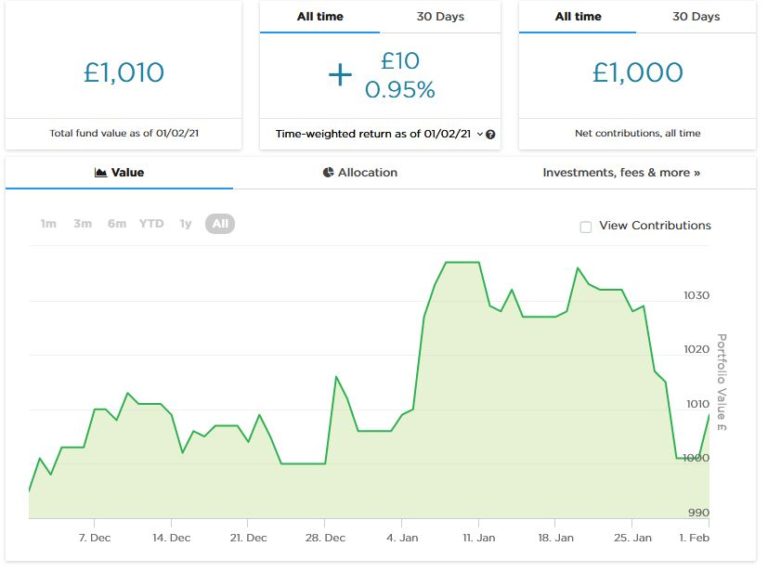

As you may recall, two months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,037 in mid-January, though it currently stands at a more modest £1,010. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

Incidentally, I was recently asked by Nutmeg to contribute an article about my ‘Investing Journey’ for their blog. This was published in early January and you can read it here if you like. In the original version I was more explicit about why I left the charity I used to work for (basically a personality clash with the new Director who saw me as a rival). Nutmeg presumably decided this might ruffle a few feathers – even 25 years on! – so they changed it to something blandly neutral. Anyway, I thought I should let you know, as the opening section reads a little oddly now 🙂

The Nutmeg article brought quite a few new subscribers to this blog – so if that includes you, welcome to Pounds and Sense! I do hope you find my posts interesting.

Moving on, I had an email this week from the peer-to-peer lending platform RateSetter saying that all their lending activity is being transferred to Metro Bank (which now owns RateSetter). All investor accounts are therefore closing at the start of April, with investors’ money being returned to them in full along with all interest due.

I know some RateSetter investors are unhappy about this, but personally in these turbulent times I’m just glad to be getting my money back with interest. I originally invested £1,000 in September 2018 with an eye to claiming the £100 new investor bonus. The latter was duly credited to my account a year later, so by April I expect there to be a total of around £1,180 in my account. That equates to an annual interest rate of around 7%, which I am perfectly happy with.

This last year has undoubtedly been tough for P2P lending companies, with rising default rates and withdrawal requests along with reduced demand for loans. This has caused some platforms to experience cashflow problems and bad publicity. The only other one I have any money left with is ZOPA, which has also had a challenging year. I have only a few hundred pounds left in ZOPA as I switched some time ago from reinvesting repayments to withdrawing them. I’m not sure I can see much of a future for P2P lending in the UK, but of course in these unique times anything is possible. I don’t foresee myself putting any more money into P2P lending for a while, though.

I also heard recently from Property Partner. As you may know, this is a property crowdfunding platform. A few years ago, when I was investing regularly in property crowdfunding, I put around £5,000 into twenty or so properties on this platform.

Anyway, the email revealed that the first property I bought shares in has now reached its fifth anniversary. All investors therefore have the opportunity to sell up at the current independent valuation or else continue for a further five years. I voted to sell my shares, since (as mentioned in this recent post) I am currently trying to reduce the total amount I have invested in property crowdfunding.

The way the five-year anniversary process works is that all shares owned by investors who want to sell are bundled together and put up for sale on the Property Partner site. Assuming they are all bought by other investors, everyone who voted to sell then gets their money back at the current valuation. If that doesn’t happen, Property Partner put the property concerned up for sale. But obviously that is likely to take months and there is no guarantee the valuation price will be achieved. So you might end up getting back less than anticipated (or perhaps more in a best-case scenario).

Obviously I’m hoping this process goes smoothly and I get my money back soon. I would comment, though, that many of the properties that are coming up to their five-year anniversary are on offer on the resale market at well under the current valuation price. So if you are of a speculative persuasion, there is an opportunity to buy shares now at a discount and maybe make a quick-ish profit through selling up via the five-year anniversary process. I must admit I am tempted to try this, but haven’t made a decision yet!

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently. I am also looking forward to receiving a substantial lump-sum payment in April when my first investment with them matures.

As I’ve said before, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website. Note that you can’t invest with Buy2LetCars through an ISA, so the interest part of the final payment will have some tax deducted. Depending on your circumstances, you may be able to reclaim this.

Finally, several more readers have now signed up with the low-key matched betting opportunity mentioned in some previous updates. New members are still being accepted, but the company has had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

I don’t know about you, but January to me has felt a very long month. It’s been cold, damp and depressing, with the whole country stuck in what seems like a never-ending lockdown.

As you may know, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so. Even so, being unable to see friends and family has been hard for me, as has the closure of my local swimming pool (which I used to visit twice a week). And I appreciate that in many ways I am one of the lucky ones. I don’t have any major financial worries, and I’m not trying to home-school any children!

I did have a ‘day out’ at the end of January when I had to go to the eye clinic at Burton Hospital for a follow-up appointment. As regular readers will know, in the autumn I was diagnosed with a perforated retina in the left eye. I had laser treatment for this, and my January appointment was to assess how successful it had been.

As it turned out, there was some good news and some bad. The consultant told me that the treatment had been three-quarters successful. In one area it hadn’t ‘taken’, meaning I needed top-up treatment. He administered this then and there. I guess he cranked up the laser a bit, as unlike my first treatment it was somewhat painful and I had a headache for a couple of days afterwards. I have to go back at the start of March for what I very much hope will be a final check-up. Keep your fingers crossed for me!

Because they put drops in my eyes at these appointments, I can’t drive. I therefore took a taxi to the hospital and caught the train back. On previous occasions the trains have been very quiet, but there were noticeably more passengers this time. The roads too seemed pretty busy. I get the impression that people are (understandably) becoming fed up with lockdown now and the government’s Stay At Home message isn’t being as well complied with. Not a criticism, just an observation.

I am still aiming to go out for a walk once a day, though with some of the bad weather in January, I have missed a few. Here is a photo of my front garden about a fortnight ago 😮

On the plus side, I do enjoy watching the snow as long as I don’t have any essential trips to make. And I like to go for a walk in it once it has fallen. It was lovely to see (and hear) the local children getting out their sledges and enjoying some much-needed fun during these difficult times.

As far as evening entertainment is concerned, I finished my box-set of the tongue-in-cheek detective series Agatha Raisin and am happy to recommend that. On a similar note, I am enjoying the new (second) series of The Mallorca Files, which is currently on BBC iPlayer. It is just a shame that because of the pandemic they were only able to record six episodes.

Also, inspired by this post by my fellow blogger Caz, I have been investigating what is on offer on Amazon Prime Video. I have Amazon Prime mainly for the fast, free deliveries. But of course members do get access to a range of free films and TV series as well.

Anyway, I found a couple of series I really enjoyed. Being a Star Trek fan, I had to check out Lower Decks, a cartoon series focusing on the junior ranks on board one of the Federation’s least illustrious starships, the USS Cerritos. This has some great laugh-out-loud moments but some good stories as well. There are plenty of allusions to familiar Star Trek tropes that will keep any fan of the franchise amused. Watch out also for an appearance by an evil incarnation of Microsoft’s infamous ‘Office Assistant’ Clippy!

Of course, if you’re a Star Trek fan and haven’t yet seen Star Trek: Picard featuring the great Patrick Stewart as the eponymous hero, you should definitely watch this on Amazon Prime Video as well 🙂

The other series I enjoyed is Undone. Indeed, this is one of the best things I’ve seen on TV for quite a while. It’s almost impossible to describe, but it’s an animation that combines elements of mystery, comedy, romance, science fiction/fantasy, and more. And all with stunning, almost psychedelic, imagery, and strong acting and characterization. Here’s a screen capture that will give you some idea of the style. If you watch nothing else on Amazon Prime Video, give this a try..

Going back to the pandemic, there has at least been some good news this month. The vaccine roll-out has been going well – I’ve just heard that 10 million people have now had their first injection – and the number of new cases has been falling rapidly. As a 65-year-old I have not yet been called for vaccination but assume this is likely to happen fairly soon.

I do hope these developments will allow lockdown and other restrictions to be eased in the coming weeks, as in my view they are causing grave harm to people’s physical and mental well-being. In particular, I would like to see schools reopen, along with swimming pools and gyms. I would also like to see pubs, restaurants and hotels allowed to reopen before many have to close their doors for good. In the (slightly) longer term I would like to see all restrictions lifted so that normal life can resume. I am not a fan of mandatory masks and would like to see them made optional for those who believe they offer some useful protection from the virus (personally I have never been convinced of this).

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

As you may know, this is a best-selling book by Claire Parker and Sir Muir Gray, published by Bloomsbury. I bought a hardback copy from Amazon. A slightly cheaper ebook version for Kindle is also available.

Sir Muir Gray is also the author of Sod 70!, a similar healthy living guide aimed at the over-70s.

Review

Sod 60! is 232 pages long. The text – which is very readable – is broken up by lots of sub-headings, diagrams and cartoon-style illustrations (by David Mostyn). There are nine main chapters, each covering an aspect of how to live well in your sixties. The chapter titles are as follows:

Getting Older Doesn’t Matter – Getting Active and Getting Attitude Does

Keeping Active is Fitness Friendly

Your Attitude and Its Soulmates: Mind and Mood

Keeping Your Metabolism Healthy

Take Care of Your…Bits

Rhythm and Blues

Stuff Happens

Decisions, Decisions

Health Care: Choosing and Using It Wisely

Some of those chapter titles are self-explanatory, others less so. For example, Chapter 5 ‘Take Care of Your…Bits’ isn’t about what you might think. It actually covers looking after different parts of your body, from your brain to your feet. Sexual health is then covered in Chapter 6, ‘Rhythm and Blues’. Those both seem pretty odd choices of chapter title to me, but I suppose the aim was to help give the book a ‘quirky’ personality.

That small criticism aside, the style of the book is friendly and relatable. It’s also down to earth and practical, and I like the way that the text is interspersed with exercises, resolutions, and so on. It is very much a hands-on, practical guide.

Sod 60! concerns the importance of looking after your body and mind as you grow older. The authors stress the need to stay as active as you can, both physically and mentally.

Chapter 2 includes a range of physical exercises to try, and also sets out some general principles for exercising healthily as you get older. I thought this was one of the most useful chapters in the book.

Chapter 3, which focuses on attitude, mind and mood, is also very good. It looks at the importance of keeping a positive attitude, and staying connected with friends and family, your neighbours, local community, and so on. It also discusses maintaining a good relationship with your partner (assuming you have one). Getting enough sleep and dealing with stress are covered as well, though not in great detail.

Chapter 4 ‘Keeping your Metabolism Healthy’ focuses on diet and weight. The authors advocate following a balanced and varied Mediterranean-style diet, with plenty of fresh fruit and vegetables. That seems eminently sensible to me. I wouldn’t say there was much in this chapter I hadn’t heard before, and some of the advice such as avoiding sugary drinks struck me as stating the obvious. But this is of course very important to long-term health, so I guess it had to be said.

Chapter 5, as I’ve already mentioned, focuses on different organs/parts of the body. It discusses how to keep each one healthy, and warning signs to look out for as you get older. It also covers age-related changes and what you may be able to do to help prevent problems. Having a good diet, staying active, giving up smoking and reducing alcohol intake all crop up quite frequently. Again, there were no huge surprises for me here.

Chapter 6 is about sexual health and related matters such as bladder and (for men) prostate problems. On the sexual side, the advice could be broadly summed up in five words: Use it or lose it! The advice on matters such as urinary incontinence is – to be honest – a bit depressing, but nonetheless important to be aware of.

Chapter 7 ‘Stuff Happens’ is also a bit depressing, though again it covers some important topics. These include how to deal with the problems later life can throw at you, including depression, isolation, bereavement, serious illness, and so on. There is some excellent advice here, especially on the importance of cultivating and maintaining a support network of friends, relatives, health professionals, and so on.

Finally, Chapters 8 and 9 are both about healthcare and could easily have been combined in my opinion. They look at such matters as how to navigate healthcare decisions, self-care to prevent (or at least mitigate) serious health problems, drugs and vaccinations, and so forth.

In Conclusion

Overall I thought Sod 60! was a useful guide for sixty-somethings though maybe not an earth-shattering one. The book covers a range of issues that anyone in their sixties will need to think about and prepare for. It was first published in 2016, so there is no reference to the Coronavirus pandemic. The advice in the book still applies and in some ways is even more cogent now. With the UK still in lockdown at the time of writing, for example, we all need our support networks more than ever at the moment…

Sod 60! is really a ‘mind and body’ book. It doesn’t cover financial issues such as pensions and benefits (and indeed doesn’t claim to). And it doesn’t have much to say about the challenges and opportunities retirement can bring, or the pros and cons of carrying on working. For advice on these and similar matters, something like the annual Good Retirement Guide (which I hope to review soon) would be good. And keep on reading Pounds and Sense, of course!

If you want a readable and entertaining guide to making the most of your sixties and preserving your physical and mental health, though, Sod 60! would certainly fit the bill. It would also make a great (and relatively inexpensive) birthday or Christmas gift for anyone in this age category.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

British people generally are not very good at saving.

A third of us have under £600, and 1 in 10 have no savings at all (source: https://www.finder.com/uk/saving-statistics). Having so little money put away makes people especially vulnerable in the event of a sudden change in their circumstances such as redundancy or divorce.

So today I thought I’d bring to your attention a money-management app called Plum that aims to help with this problem.. Plum is designed to help you set money aside painlessly for any purpose – from holidays to major purchases or simply for a ‘rainy day’ fund.

Plum is one of a growing range of apps that make use of so-called Open Banking. This allows third-party apps to access your financial information (read only) – so long as you provide the necessary authorization, of course – and perform certain transactions on your behalf, if you choose to set up a direct debit.

Open Banking is now becoming well established in the UK, and safeguards are in place to ensure that your security isn’t compromised. Even so, this is something you need to be aware of – and comfortable with – before signing up with Plum or similar apps.

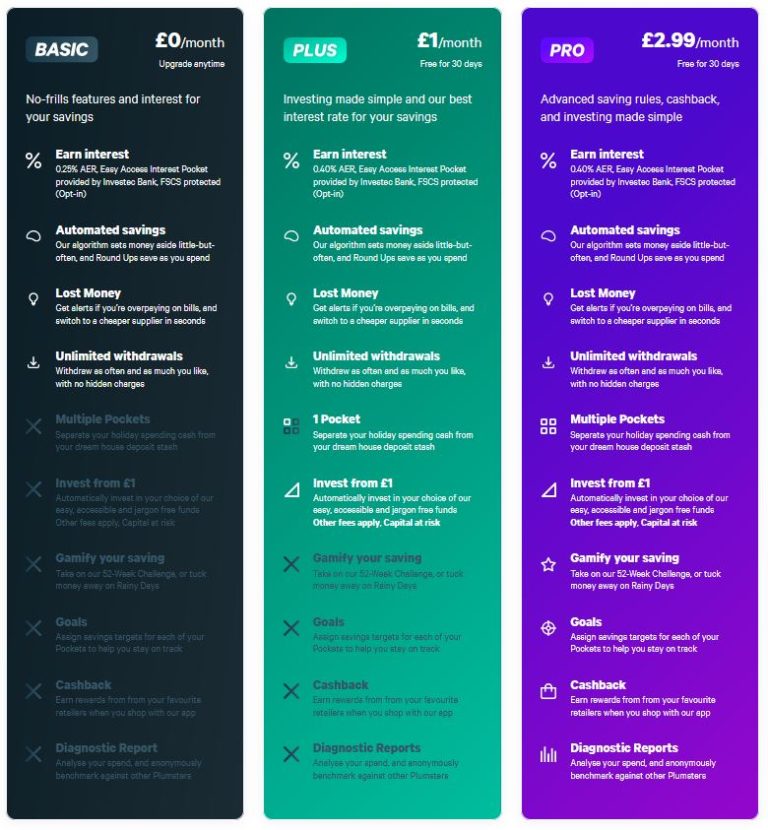

In this post I am looking at features available on the Plum Free (or Basic) account and the paid-for Plum Plus and Plum Pro Accounts. The Plum Free account is – of course – free of all charges. Plum Plus costs £1 a month (the first month is free) and Plum Pro costs £2.99 a month (again, the first month is free if upgrading from a Plum Free account). Plum Plus and Plum Pro offer a wider range of features and higher interest rates in interest-bearing ‘Pockets’ (further discussed below).

The screen capture below from the Plum website shows the features available with each type of account.

You can read more about the three account types if you wish on the Plum website.

How It Works

Plum is available as an iOS and Android app. It uses Open Banking in combination with a direct debit authorized by you to manage and grow your money for you in an intelligent way.

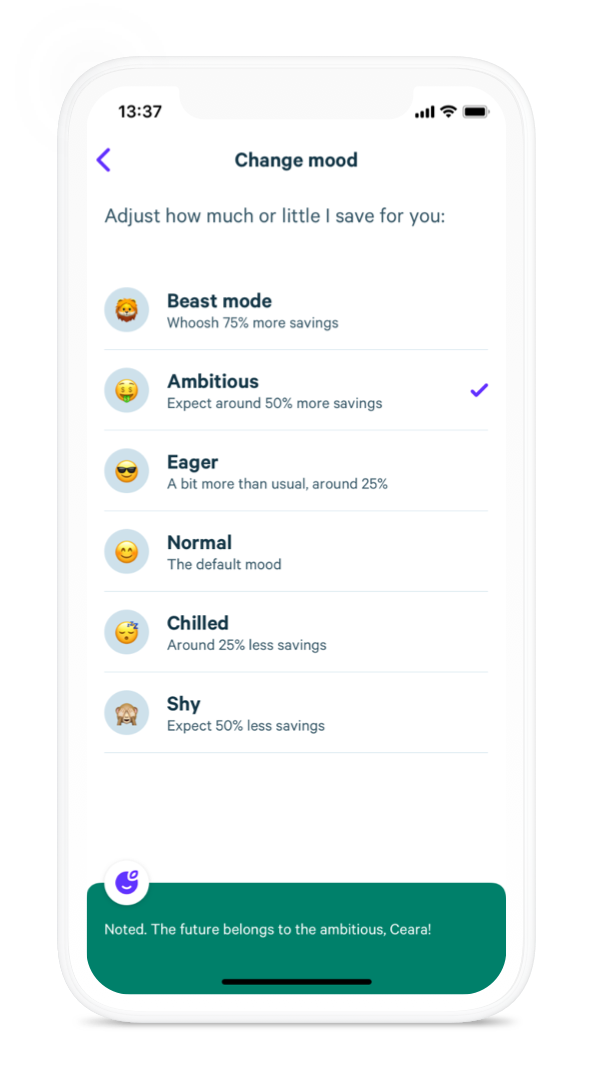

Every few days, Plum’s algorithm calculates what you can afford to stash away based on your spending habits. It then transfers that money automatically from your current account to your Plum account. In this way you put money aside regularly while barely being aware of it – so it builds up, and in due course you can spend it on things that really matter to you.

You can change the amounts the app takes at any time, and also pause the service if you wish. This means you don’t have to worry about Plum pushing you into the red. You always stay in control and can change the ‘mood’ at any time if you want to be more ambitious or cautious with your saving (see picture below).

Plum currently works with most major UK banks. The full list from the website is as follows:

Barclays

Danske Bank

First Direct

Halifax

HSBC

Lloyds

M&S

Monzo

Nationwide

Natwest

Revolut

RBS

Santander

Bank of Scotland

Starling

Tesco

TSB

Ulster Bank

Currently business accounts and joint accounts are not supported by Plum. They also do not support Channel Island bank branches.

How to Get Started

Start by downloading the app free of charge from Google Play or the Apple iStore (see links here).

Once you’ve downloaded the app and signed up, you can begin a dialogue with the Plum chatbot to help you set up your account. You will, of course, have to connect the app to your bank, so you will need to have your current account details to hand. Once it’s all set up, turn notifications on. This will allow the app to alert you when it wants to start setting money aside for you.

There is an option to speak to a real person if you need to. You can also increase or decrease the amount to stash away, set up ‘Pockets’ for specific purposes (see below), and even pause any transactions completely if you wish.

Do You Get Interest?

With the default ‘Primary Pocket’ on your Plum account the answer is no. The app is free and helps you set money aside painlessly, but Plum doesn’t pay interest on this.

Even Plum Free accounts can, however set up a secondary interest-paying Pocket. This facility is provided by Investec Bank and takes the form of an easy-access account paying 0.20% for all users

Plum Plus users can also set up one easy-access Pocket paying 0.40% interest. And Plum Pro users can have up to 10 such Pockets for different purposes, all paying 0.40% interest.

What Exactly Are Pockets?

Pockets let you set money aside with a specific goal and amount, e.g. to buy a car, save for a trip, or put down a deposit on a house. You can think of them as ‘pots’ or even jam-jars!

As money accumulates in each Pocket, the app will show your percentage progress towards achieving that goal.

All Pockets (except the default Primary Pocket) can be interest-bearing as well, as explained above. The interest paid will contribute towards achieving your goal/s.

Where Do Plum Keep Your Money (And Is It Safe?)

The app puts money away in your Plum account, which is the safeguarded account created when you sign up.

Your Plum funds in your Primary Pocket are held as e-Money by PayrNet (a subsidiary of Railsbank), Plum’s e-Money provider. Your funds are safeguarded with a UK Bank chosen by PayrNet. Your money is safeguarded because e-money cannot be lent out (this is also why it doesn’t earn interest). That same safeguarding also prevents any of Plum’s or PayrNet’s creditors from claiming your money in the event that either business should go bankrupt. Both Plum and PayrNet are regulated by the Financial Conduct Authority (the UK’s financial watchdog). Plum also boasts 256-bit TLS encryption to ensure your data is kept safe.

Money saved with Plum in interest Pockets is held on Trust with a UK Bank (Investec). A Trust is a legal mechanism that means Plum can look after your money but legally it never stops belonging to you. This means that if anything were to happen to Plum then the bank would return your money to you directly. Should something happen to the bank itself, you would be protected up to £85,000 under the Financial Services Compensation Scheme (FSCS).

How Easy Is It to Withdraw?

Transfers from non-interest Pockets back to your Primary Pocket are usually instantaneous. it is different with transfers from interest-bearing Pockets:

• When requesting an interest Pocket withdrawal before 15:00 UK time on business days, it will be completed the same day.

• When requesting after 15:00 UK time on business days or during weekends, it will be completed the next business day.

Note that withdrawals from interest and non-interest Pockets go back to your Primary Pocket initially. Withdrawals to your bank account will always be from your Primary Pocket. Such withdrawals are processed the same day (typically in around 30 mins) and will appear on your bank statement under your full name.

Other Benefits

As well as making it easier to put money aside, Plum can help you keep track of your income and expenditure. You can set it to provide daily or weekly balance updates, and it will also automatically track your transactions by category, week and month. Plum will let you know all of this without having to wade through bank statements.

In addition, Plum has AI (artificial intelligence) built in, so if it notices you are being overcharged on a bill or for a financial product, it lets you know. It will also suggest cheaper solutions for you and – if you wish – help you switch over in just a few clicks.

Plum also offers a variety of optional automated features. These include

Round Ups – Get Plum to round up your past week transactions to the nearest £1 and transfer the spare change.

52-Week Challenge – Starting with £1 in the first week, £2 in the second week and increasing up to £52 in the final week of the challenge, Plum can help you set aside £1,378 in a year. This feature is only available through Plum Pro.

Rainy Days – Once activated, Plum squirrels away extra cash automatically each day it rains where you live. This feature is also only available through Plum Pro.

Pay Days – The best time to set money aside is when you get paid, so tell Plum an amount and it’ll move this automatically for you on payday.

Plum Reviews

Plum has an average rating of 4.5 stars (‘Excellent’) from over 1200 reviewers on the independent Trust Pilot website. Just over three-quarters (76%) gave it the maximum five stars, with many mentioning the great customer service and how the app had helped them to save more. Of those who gave Plum three stars or less, the main issues mentioned were delays or problems in withdrawing. To be fair, the Plum team generally respond to such comments on the Trust Pilot website explaining how the app works and offering additional help where issues have arisen.

Final Thoughts

If you want to set more money aside but need a little help and encouragement to do so, Plum is well worth a look.

I like the way it stashes money away automatically, so in all probability you won’t even notice it. You can set it to take as much or as little as you like, and you can also make one-off additional payments if you are feeling particularly flush. You can also withdraw some or all of your money back to your bank account at any time.

Pockets are a great feature, allowing you to set aside money for specific purposes. And, as mentioned above, by using an interest-bearing Pocket, you can get interest as well (0.20% with a Plum Free account and up to 0.40% with a Plum Plus or Pro account). Obviously that’s not a fortune, but in the current low-interest rate environment it is still very competitive (and a lot better than nothing!).

In my view Plum is likely to work best for people with a regular monthly (or weekly) income. If you receive income more irregularly – e.g. you’re self-employed – it might not work quite as well. Even so, Plum say that their algorithm can detect patterns in your income and expenditure and adjust your transfer amounts accordingly.

In any event, there’s no reason not to try Plum yourself to see if it can help you set aside more. Just click through this link for more information and to sign up.

As always, if you have any comments or questions about this post, please do leave them below.

Note: This is a fully revised and extended version of my original Plum review from last year.

Disclosure: I am an affiliate for Plum so if you click through any link in this article and sign up, I will receive a modest referral fee for introducing you. This will not affect the service or benefits you receive in any way. Please note also that I am not a registered financial adviser and nothing in this post should be construed as personal financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m highlighting a fun and free way you may be able to boost your income in 2021. And all you have to do is check the website in question once a day to see if your postcode is a winner!

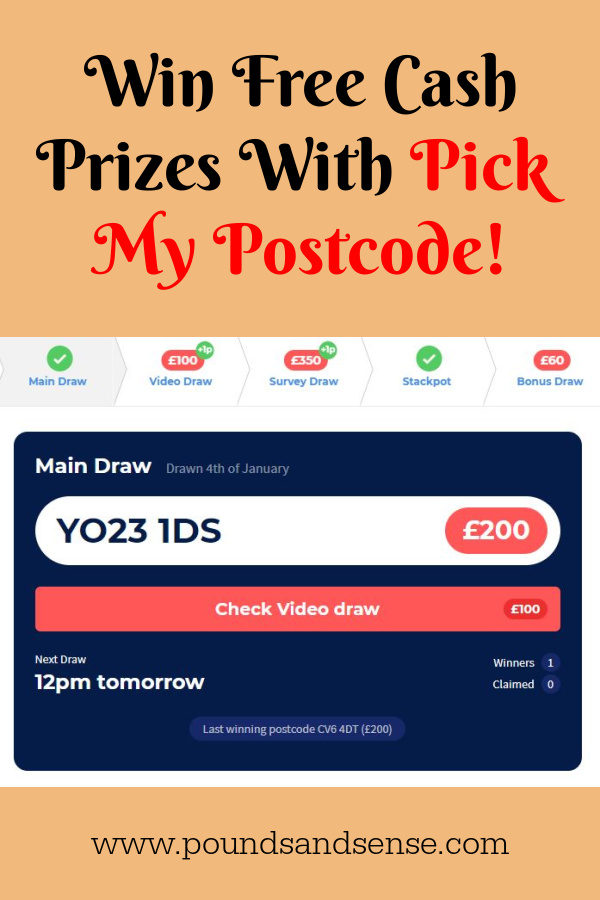

Main Draw Each day one postcode is picked at random for this draw, which has the biggest prizes. The main daily prize – which I was lucky enough to win – can be over £1,000. When I had my own win, the prize was £1,200, though as one other person in my postcode area also claimed, the prize was split between us. So I got £600 plus a small bonus (explained below) – not a life-changing amount, but certainly a day-changing one 😀

Video Draw – To see the winning postcode in this draw, you first have to watch a short video. Though to be honest I find that you just have to watch the ad that plays first and the winning postcode is then displayed – you don’t have to watch the whole of the video unless you want to. This draw pays a minimum of £50, with the prize rolling over to the next day if not claimed. I have seen up to £400 on offer in this draw.

Survey Draw – To see if you have won this draw, you first have to complete a very short survey (generally just one question). As with the Video Draw there is a minimum prize of £50 and it rolls over to the next day if unclaimed. When I checked today there was a £300 prize, so it must have rolled over for a few days previously.

Stackpot – The Stackpot lists a variable number of postcodes with £10 prizes for those claiming them. When I checked this morning there were 14 prizes up for grabs and one that had already been claimed (it is first come, first served with the Stackpot).

Bonus Draw – With the Bonus Draw there is a daily £5 prize, £10 prize and £20 prize. To be eligible you need to have built up a Bonus (see below) equal in value to the prize in question by visiting the site regularly. So to qualify for the £20 Bonus Draw, you need to have accumulated a Bonus worth at least £20 yourself.

All lottery prizes are tax-free, of course, in accordance with UK gambling laws.

One is £5 Flash Draws. These appear at random on advertising spaces around the PMP website. They look like the sample image below. They appear to individual visitors at random. I have never seen one myself, but obviously it’s worth keeping an eye out for them. If you spot one, you just have to click to claim (it doesn’t matter about your postcode). The £5 prize is paid by PayPal as usual.

As for the Bonus, this is a sum of money that is added to your prize any time you win (with the exception of the £5 Flash prizes). It accrues over time as you visit the site. It increases by 1p for every new Main Draw, Survey Draw or Video Draw that you check. That may not sound much, but if you return to the site every day it soon adds up. My Bonus is up to £41.90 now!

If you wish, you can boost your Bonus even more by referring friends and neighbours and taking up some of the offers that appear on the site.

It’s important to note that you can’t withdraw your Bonus until you win a prize. But even £10 in the Stackpot or £5 in the Bonus Draw will qualify. So if I were to win a £10 Stackpot or Bonus Draw prize today, I would actually receive £10 plus £41.90 = £51.90. Another good feature is that your Bonus is added to your winnings every time you win a prize – it doesn’t reset to zero after a win.

I am not normally a great one for lotteries, but I make an exception for Pick My Postcode. As I said above, it’s free to enter, there are loads of prizes on offer, and the longer you go on playing, the bigger those prizes can become. And obviously, having previously won over £600 on the Main Draw myself, I know that it’s genuine and would love to win again!

Finally, if you still need further reassurances about the site, check out the reviews on the independent Trust Pilot website (average 4.8/5 stars, with 94% of people rating it ‘Excellent’).

As always, if you have any comments or questions about Pick My Postcode, please do leave them below.

Disclosure: This post includes my referral link. If you click through and sign up for free, I will receive a small commission for introducing you. This will not affect your potential earnings in any way.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a Q and A for you with my fellow money bloggers at MoneyNerd.

MoneyNerd is a UK personal finance blog that aims to help people learn to manage their finances and tackle debt. I asked a number of questions about personal finance and debt, and added my own thoughts as well. Our answers are also being shared separately on the MoneyNerd blog. I hope you find them interesting and informative.

What’s your number 1 financial tip?

MN: It’s hard to give advice that would apply for everyone, because everyone’s finances are different. But I would suggest ‘write it down’, as a fairly universal and important financial tip. Start with your financial goals, then write down the steps you’ll take to get there according to your budget. A lot of people have good financial intentions, but without having clear goals on paper, it’s easy to get led astray.

PAS: Agreed. I would also say, keep on top of your money. Know what’s going in and what’s going out every month, and budget accordingly. Always be on the lookout for ways you can maximize your income and minimize your expenditure. And try to put some money aside for the proverbial rainy day. Everyone should really have at least three months’ worth of income set aside in case of emergencies. Sorry, that’s at least three tips, I know!

What do you think are the main causes people find themselves in financial difficulty?

MN: I think financial difficulties are mainly caused by unforeseen life-events, such as bereavement, unemployment, and relationship breakdowns. These kinds of bumps-in-the-road can severely throw people off course, particularly if their financial situation was fragile in the first place. Unfortunately, all three of these examples have sky-rocketed due to the pandemic, and many people in the UK will be facing financial difficulties over the coming year.

PAS: Not much I can add to that. Although sometimes failing to monitor your income and expenditure closely enough can lead to debts mounting up before you realise it.

What personal finance tools do you currently use to track and manage your money?

MN: I’m quite old-school and still use spreadsheets for a lot of money-related things! There are some good apps out there though – Money Dashboard is a particularly good one.

PAS: I am the same and use spreadsheets a lot. I started with Microsoft Excel, but these days mainly use Google Sheets. As regards personal finance tools, I like Snoop [referral link], a relatively new app that helps you keep track of your finances and suggests easy ways you can make savings.

Any tips for people coming to financial management later in their lives?

MN: It might be a little harder to undo old habits and reinstate new ones if you’re approaching financial management from an older perspective. So start by setting simple goals, and work at them consistently. It’s probably worth taking a little time to assess what’s important to you right now, too: what range of outgoings does your money need to cover in later life that you didn’t need to consider before?

PAS: I am 64 and have friends in their seventies and eighties, so I have seen the sorts of problems older people can face. In particular, so many aspects of our personal finances are dealt with online now, from banking to applying for state benefits. The pandemic has probably accelerated this trend.

Many older people struggle with the technology and it’s often not as intuitive as it should be, especially for those whose eyesight isn’t as good as it once was. So I would say to any older people, try not to get left behind by technology, and ask younger friends and relatives for help when needed. Last year a group of us clubbed together and bought a friend (a retired builder) a Chromebook for his 80th birthday. He had never engaged with computers or the internet before and I must admit I was expecting him to struggle at first. However, he took to it like a duck to water, and was soon ordering tools and components online from a local builders merchant. So even old dogs can definitely learn new tricks!

2021 is going to be tough for many. Do you have any advice on how to keep things under control?

MN: I’d start with the obvious – plan as much as possible, in order to save as much as possible. This is so that when those ‘bumps-in-the-road’ come along, you have some kind of safety net, however small. Unfortunately, however, I imagine a lot of people will do everything right this year and still fall into difficulty. As and when that happens I would say be proactive in reaching out and seeking help. There are plenty of free services and helplines to reach out to, before matters spiral.

PAS: Yes, definitely. As I said earlier, everyone should have a financial safety net to tide them over when life throws you a curveball.

In my earlier career I worked as a debt counsellor at a citizens advice bureau, so I know that there is lots of help out there if you ask for it. And friends and family can be a good source of practical and emotional support too. Just don’t bury your head in the sand and pretend to everyone that nothing is wrong.

What would be your top tip for someone who is worried about a debt (or debts) they can’t repay?

MN: I have two tips: the first is don’t panic, the second is be proactive. If you can’t afford the repayments for a loan or credit card, contact the company and explain your situation. If you’re struggling to meet the repayment amounts, you may also need to look at whether a debt solution is appropriate for you. Having unaffordable debt can be a scary place in which to find yourself, but by taking action you can dissipate some of that anxiety by feeling you are doing something about the problem.

PAS: Yep. It’s worth bearing in mind also that if you have a debt you can’t repay, it’s not just your problem, it’s a problem for whomever you owe the money to as well. It is therefore in their best interests to work with you to find a method for paying down the debt.

What are some good ways of boosting your income?

MN: Ask yourself: do I own anything I could rent? A parking spot, a vehicle, a garden shed, even a room in your house if you own it. Then ask yourself: do I own anything I could sell? Old clothes, a bicycle, old furniture, anything in storage. Then finally, ask yourself what you could do with your spare time: dog-walking, Uber-driving, delivering takeaways/parcels, painting and decorating,completing online surveys, match betting, free-lancing, etc. I have a whole blog post which goes into this very topic in more detail: Making Money – Tips and Tricks.

PAS: Lots of great ideas there. Like MoneyNerd, I also have a section of my blog devoted to ideas for boosting your income. I like online surveys, with Prolific Academic (a website needing people to take part in academic research) a particular favourite. And I do matched betting as well, though not as much as I used to, as I’ve been restricted (or gubbed as we say in MB’ing) by many of the leading bookmakers!

What is the best way you can help a friend or family member who has debt problems?

MN: Honestly, I don’t think there’s a one-size fits all here. Everyone and everyone’s debt problems are different. But that seems like a cop-out! So I think showing genuine, non-judgemental support, and ensuring they have all the right resources (StepChange, CitizensAdvice, etc.) to hand are two good places to start.

PAS: I agree with this. But based on personal experience with a friend a few years ago, I would also advise thinking hard before lending them money, as this seldom solves the problem and may simply exacerbate it. With my friend, who lived alone, I found that acting as a lender to him changed the nature of our friendship, and not for the better. I also felt that by constantly bailing him out, I was allowing him to avoid addressing his money management issues. Eventually we had a difficult telephone conversation when he asked me to lend him money again and I refused. He took it better than I expected and our friendship actually returned to something more normal after that. He got his finances under better control, although I did on a couple of occasions afterwards send him supermarket vouchers to ensure he had enough to get food. I didn’t expect to be repaid for these, obviously!

If you had a sudden, unexpected windfall of £5,000, what would you do with it?

MN: Firstly I’d pay off any loans or outstanding credit card debts. Then I’d take my family out for a nice meal, and put what’s left-over into a tax-free ISA.

PAS: Paying off debts would be my first priority as well, though I am fortunate not to have any at the moment. I would put most of the rest in my Nutmeg stocks and shares ISA, and some in my Kuflink property loan investment account (from which I have had good results over the last three years) to provide a bit of diversification. Going out for a nice meal with family and friends sounds good too, although as I live in a Tier 3 area I might have to wait a while for that!

What was your best-ever financial decision, and what was your worst?!

MN: My best financial decision was investing in a tech based stocks and shares ISA which has done really well over the last 5 years, although don’t know if I’d recommend the same investing approach in the current economic climate.

On the other hand my worst financial decision was living in London for 10 years where rent and cost of living is exorbitant.

PAS: My best financial decision was probably paying off the mortgage when I had a windfall a few years ago. At a stroke one large item of monthly expenditure was gone, giving me greater financial flexibility as well as saving me a lot in future interest payments.

My worst decision was investing too much in property crowdfunding a few years ago when it was still new and exciting. I had money to invest at the time and liked the idea of owning stakes in a portfolio of properties across the UK. Some of my investments worked out but others didn’t, and I am currently sitting on a number I can’t access because the properties in question can’t be sold for one reason or another. The money is still there in bricks and mortar but I have no idea when or how I will be able to access it. That said, I do still believe in the property crowdfunding concept, but I do it a lot more selectively now.

About MoneyNerd

MoneyNerd.co.uk is a personal finance blog that was set up with one aim in mind: to help people learn how to manage their finances and tackle debt. The blog includes a variety of straight-talking articles that cover personal finance topics from credit card guides to mental well-being tips. These can help you understand exactly how financial products work, as well as what your rights are when dealing with debt. We want to offer authentic and truthful information that can help you deal with your situation, whatever that may be.

Many thanks again to MoneyNerd for their insights. Please do check out the MoneyNerd site for much more information about tackling debt and getting your finances under control.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers of PAS will know that I am a fan of the Nutmeg robo-adviser investment platform, and have a good portion of my own money in a Nutmeg stocks and shares ISA. You can read my in-depth review of Nutmeg here.

I was interested to hear that Nutmeg had launched a new investment style for their ISA, Lifetime ISA, Junior ISA, SIPP (personal pension) and general investment account customers. Previously such customers had a choice of three options: Fixed Allocation, Fully Managed and Socially Responsible.

All Nutmeg portfolios are managed by human experts, but the Fixed Allocation ones are altered annually, whereas the others are managed more actively. The Socially Responsible portfolio aims to optimize your investments according to various environmental, social and governance (ESG) factors. So it focuses on companies with a good track record and proactive strategy in such areas as water use, pollution, greenhouse gas emissions, proportion of female board members, and so on. Currently my own stocks and shares ISA is in the Fully Managed category (which was the only option available when I originally invested with Nutmeg).

Whilst all three of these investment styles remain available, a new one was launched in 2020…

Smart Alpha Portfolios

Nutmeg’s Smart Alpha portfolio range is powered by J.P. Morgan Asset Management. It includes five risk-rated portfolios, each holding between 10 and 14 passive and active exchange traded funds (ETFs). They are run by J.P. Morgan’s multi-asset solutions team, giving Nutmeg clients access to the investment giant’s experience and expertise. Writing on the Nutmeg blog, their Chief Investment Officer James McManus explained the benefits of this approach as follows:

The name recognises the intelligent way these portfolios are designed with the potential to achieve alpha (returns above the market) for our clients in three ways.

Firstly: The use of J.P. Morgan Asset Management’s multi-asset specialists, a team with a 50-year history of investing for institutions and professionals worldwide. These specialists inform Smart Alpha portfolios’ long-term (strategic) asset allocation.

Secondly, Smart Alpha portfolios have the ability to be flexible around this long-term asset allocation, allowing us to manage risk and capture opportunities at different stages of the market cycle.

Thirdly: Nutmeg and J.P. Morgan Asset Management have added to these capabilities a means to make smart security selections within active exchange traded funds (ETFs). These smart selections are made based on the insights of J.P. Morgan Asset Management’s research analysts with the aim being to capture returns in excess of the market benchmark (alpha).

How do these smart selections seek to gain alpha? The active ETFs we use allow us to move overweight in certain positions that J.P. Morgan Asset Management’s analysts expect to perform well and underweight in those positions they expect to perform poorly. This gives us the ability to move above and below market benchmark positions, delivering greater potential returns with similar risk to the overall market.

As well as allowing Nutmeg investors to tap into the expertise of J.P. Morgan Asset Management, these portfolios are ESG integrated, meaning that (as mentioned above) environmental, social and corporate governance considerations are factored into every research and investment decision. These portfolios are therefore suitable for the growing number of investors for whom ethical considerations are particularly important.

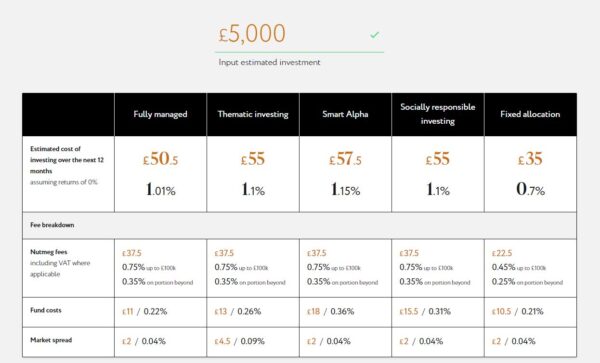

The terms and conditions for the new Smart Alpha portfolios are copied below, alongside the other portfolio types.

The above is correct as at 16 November 2023, but may have changed subsequently. Please note also that Nutmeg has also recently introduced a new ‘thematic’ investment style. More information about this can be found about this in my full Nutmeg review and on the Nutmeg website. Remember that all investing carries a risk of loss.

My Thoughts

This is undoubtedly an interesting move by Nutmeg and gives investors the opportunity to benefit from having their portfolio actively managed by a leading investment house at no extra cost. If you are a Nutmeg investor already, you can start by investing as little as £500 to test the water. You can either use ‘new money’ from your bank account or another ISA, or you can transfer money from another pot within your Nutmeg ISA account.

Personally I am very happy with the way my Nutmeg ISA has performed during this tumultuous year and don’t want to rock the boat too much. On the other hand, I am curious to see how the new Smart Alpha portfolios perform in comparison. So I have created a new £1,000 pot within my ISA and have selected Smart Alpha as the investment style. The risk level is 4/5, which roughly corresponds with the 9/10 risk level in my Fully Managed portfolio.

I will of course report back on Pounds and Sense about how my investments perform. Obviously, if my Smart Alpha pot seems to be doing significantly better than my Fully Managed one, I will switch some or all of the latter to Smart Alpha as well. It is one of the attractions of Nutmeg that you can have multiple pots within a single ISA with different investment styles and risk levels attached to them.

Capital at risk. Tax treatment depends on your individual circumstances and may change in the future.

In Conclusion

I am obviously a fan of Nutmeg and – as stated above – have a significant proportion of my investments with them.

Of course, I am not a qualified financial adviser and everyone should do their own ‘due diligence’ (and/or take professional advice) before deciding to invest. In addition, you shouldn’t consider investing with Nutmeg (or anyone else) unless you have paid off any interest-charging debts and have at least three months of easily-accessible savings in case of emergencies.

Based on my personal experiences with Nutmeg, though, I am happy to recommend them. They provide a simple, easy-to-understand investment platform, the customer service is excellent, and certainly in my case the results to date have exceeded my expectations.

If you have any comments or questions about this post or Nutmeg in general, please do leave them below.

PLEASE NOTE:As with all investing, your capital is at risk. Tax treatment depends on your individual circumstances and may be subject to change in the future. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest.

Note also that I am not a qualified independent financial adviser and nothing in this review should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any way uncertain how best to proceed. All investing carries a risk of loss.

Please note also that this review includes affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the terms you are offered or any fees you may be charged.

If you enjoyed this post, please link to it on your own blog or social media:

For many of us, our mortgage is our biggest monthly outgoing. So it’s important to keep a close eye on it and check regularly whether you could save money by switching to another provider.

That’s exactly what a new online service called Dashly aims to do. They evaluate your current mortgage deal against the whole market, taking into account your specific personal circumstances as well. If they find a better deal for you they let you know and – if you choose to proceed – assist you with the switching process.

How Does Dashly Work?

Dashly is available as a desktop site, with mobile apps for iOS and Android coming soon.

You start by registering and entering some details about your current mortgage and your personal circumstances. The latter is important, as things such as your income, employment type, credit score and age can all affect the deals you could be eligible for. This process takes 10-15 minutes. Dashly then compares your mortgage against an average of 10,000 products to find the best deal for you.

If they find a better deal than your present one, they send you a notification. You can then evaluate this and decide whether you want to switch. If you do, the team at Dashly will assist you with the switching process.

In addition, Dashly will continue monitoring your mortgage every month. If they find you could save money by switching again, they’ll let you know. It’s worth noting that the equity you have in your property changes on a monthly basis due to ever-changing house values and your decreasing mortgage balance. As your LTV (loan-to-value ratio) decreases, your mortgage may qualify for better, cheaper deals. Again, Dashly checks this on your behalf.

You receive a detailed personal report from Dashly about your mortgage every month. In addition, your dashboard will show you all the key facts at any time, from the changing value of your property to the amount of equity in it, any current deals that would save you money to your next payment date. It’s all there on one easy-to-read web page.

How Much Could You Save?

The savings can be substantial. Dashly say that on average their users save £2,620 (see footnote).

Of course, in practice savings will depend on a number of things, including the balance outstanding on your mortgage, the competitiveness of your current deal, the term left to run, and the effect of any early repayment penalties. Dashly takes all of these things into account in determining whether you could save money by switching to a new lender (and by how much).

Are There Any Costs?

Using Dashly is free. There are no hidden charges and Dashly say they will never hit you with advertisements or email campaigns to try to make money from you. They get paid out of mortgage provider fees, and are authorized and regulated by the Financial Conduct Authority.

Dashly are also founding members of Finance For Good, a charity run by social impact fintechs who put consumers first. They say that their security rivals that of the world’s leading banks.

In Conclusion

If you have a mortgage, in these uncertain times it’s more important than ever to ensure that you aren’t paying over the odds for it.

Dashly offers a free service that not only checks whether you are getting the best deal currently but also continues monitoring your situation month by month and recommends switching again if a new and better deal arises.

By using Dashly you could painlessly save hundreds or even thousands of pounds on the cost of your mortgage. There is never any obligation to switch or any fee to pay for the service. So you really have nothing to lose and everything to gain by registering for an account today.

Footnote: Your individual savings may vary and will depend on personal circumstances. £2,620 per year is the average amount based on research Dashly has conducted on the mortgage market. Find out more at www.dashly.com/reference-index.

Disclosure: This is a sponsored post on behalf of Dashly. If you sign up and make use of the service, I may receive a referral fee for introducing you. This will not affect in any way the service you receive or the deals you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since the original lockdown started (you can read my September update here if you like).

As previously I will discuss what has been happening with my finances and my life generally over the last few weeks, while trying to avoid being too repetitive!

As always, I will start with the money side of things.

Financial

As I’ve done before, I’ll begin with my Nutmeg stocks and shares ISA. This has gone up and down over the last few weeks, but currently stands at £16,578. That is over £500 up on last month, so I’m happy with that! Here is a screen capture covering the last three months…

My Property Partner and Kuflink investments are still both ticking along satisfactorily. Property Partner has resumed paying dividends on some properties, which is appreciated. The five-year sales process has also resumed. There is a backlog, though, so it will probably be longer than five years till the properties I hold shares in can be sold at the current, independently-assessed market price (or retained, of course).

There is nothing really to report about The House Crowd. I assume that the sales of the two properties in which I hold £1,000 shares are progressing, but can understand that it is a slow process at present. At least rental payments are still accruing, which should help to defray some of the selling costs.

There has been no further word either regarding my investments with Crowdlords. As I said last month, I have two remaining investments with them, Kennington Road eco-houses and Trent House. I was told they hope to have exit options for these properties by the end of the year, but I’m not holding my breath. On the plus side, they are paying 6 percent interest on my Trent House investment, which is quite generous in these days of ultra-low interest rates.

Personal

It’s been an eventful few weeks one way and the other.

As mentioned previously, I had booked a short break in Llandudno (see cover image) near the end of September. Thankfully I was able to go. If I had left it just a few days later I would have had to cancel, as the Welsh Assembly has decided to lock down the whole of the Llandudno and Conwy area due to rising infection rates. That means no-one can currently go in or out of the area without a compelling reason (and having a holiday booked there doesn’t count).

Anyway, I enjoyed my visit. I stayed in a self-catering apartment, which turned out to be a good choice in most respects. It was on two floors, with a lounge and well-equipped kitchen on the lower floor and a double bedroom and bathroom on the upper. The location was central but quiet, yet just five months’ walk from the sea. The only drawback was that parking was on the street and finding a spot was a bit of a lottery. I was lucky to get somewhere close when I arrived, but later in the holiday had to park on another road half a mile away, which was a bit of a pain. I paid £255 for my three-night stay via Booking.com, which I thought was reasonable. By comparison, the seafront hotels I checked out were charging over £600 for three nights’ bed and breakfast.

Not surprisingly Llandudno was quieter than usual for the time of year, but there were still plenty of visitors, and many of the small hotels and boarding houses had ‘No Vacancies’ signs in their windows. While some places and amenities were closed, many others were open, and I was pleased to find that the pier was fully operational (see photo below). Professor Codman’s famous Punch and Judy show on the promenade wasn’t running, though – a shame, as there were lots of young children who might have enjoyed it.

On my first day I left my car at the apartment and took a couple of bus tours. The first was the open-top bus that takes a circular route between Llandudno and Conwy and includes a running commentary. I have done this trip before and noticed that the recorded commentary hasn’t changed this year. Mind you, that may be just as well, as a post-Covid commentary would have had to include details about all the hotels and other places that have closed due to the virus, the seafront theatre that became a Covid field hospital, and so forth…

The other trip was on a vintage bus (see photo) around the Great Orme, one of the two promontories at either end of Llandudno’s seafront. This had a knowledgeable driver/guide, who provided an interesting – and up-to date – commentary. I must admit I particularly enjoyed seeing ‘Millionaire’s Row’ at the far side of the Orme. There are some amazing houses here, owned by people who like to preserve their privacy. Obviously the coach passes from a distance, but it was still a good opportunity to gawp at how the super-rich live. I particularly enjoyed hearing about the house that has its own private lift down to the beach!

On the second day of my visit I drove to the medieval walled town of Conwy, which is about three miles away. I booked a ticket online to see Plas Mawr, a restored Elizabethan town house (photo below). It was fascinating, and I was glad I took the option of borrowing one of the free electronic guides. You use these to scan a QR code in each room and it provides a commentary on the room itself and various interesting historical tidbits associated with it.

As with my visit to Dunster Castle near Minehead earlier in September, all the usual anti-virus measures were in place. I had to wear a face covering throughout, and staff ensured that there were no more than two households in a room at any one time. It worked pretty smoothly, although you had to follow a set route and there was no possibility of returning to a room once you had left it.

In case you’re wondering, the photo in my cover image shows the Haulfre Gardens Tearoom on the lower slopes of the Great Orme. It’s one of my favourite places in Llandudno, and I was pleased to find it was still open. I enjoyed afternoon tea in their lovely garden on both days of my visit. As you can see, I was pretty lucky with the weather!

As mentioned above, I was very glad to be able to make my trip before the current lockdown would have made it impossible. I feel very sorry for people who booked after me and were unable to go, especially as I have heard that some are now having problems getting their money back. But I am sorry also for the hotels and other businesses who have been left high and dry by the lockdown. I really hope for their sake it doesn’t go on too long 🙁

Moving on, I had an experience I would rather not have had in the last few weeks too. At a routine eye examination my optician saw something she didn’t like the look of in the retina of my left eye. So she packed me off to the eye clinic at Queens Hospital, Burton. The doctor there told me I had a perforation of the retina, and gave me laser treatment then and there. It wasn’t painful but it was obviously nerve-racking. The doctor did say it was a good thing my optician had spotted the problem, as it could have led to a detached retina if left untreated, which is clearly more serious. I have to go for a follow-up check this weekend, but touch wood the problem has been repaired. I guess if nothing else this does show why it’s so important to have your eyes checked regularly even if you don’t think there is anything wrong with them. That applies doubly to older people and those who (Iike me) are very short-sighted, as we are especially susceptible to this sort of thing.