My Investments Update – May 2024

Here is my latest monthly update about my investments. You can read my April 2024 Investments Update here if you like

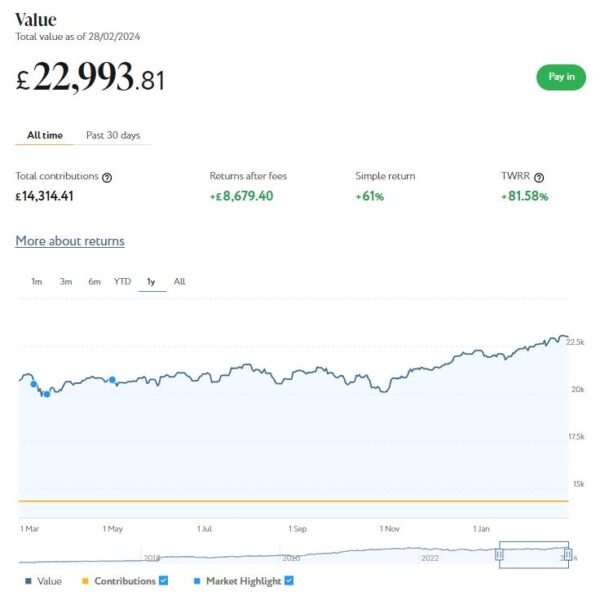

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

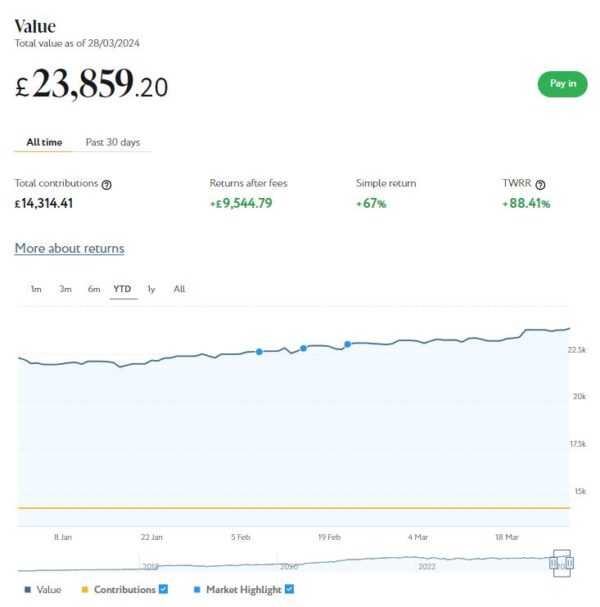

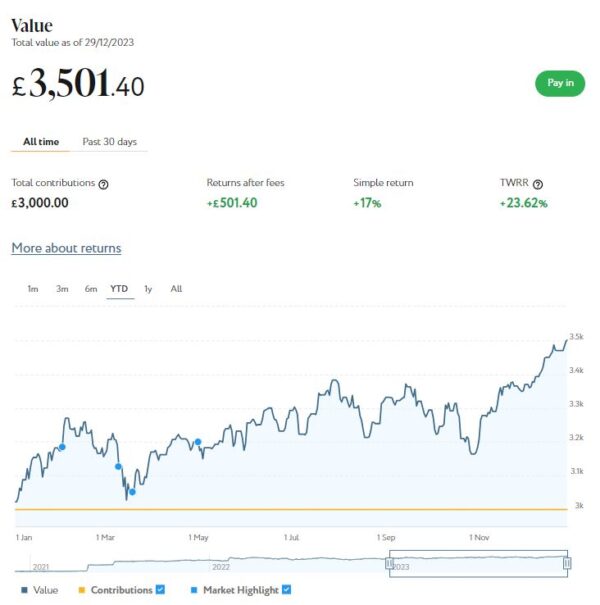

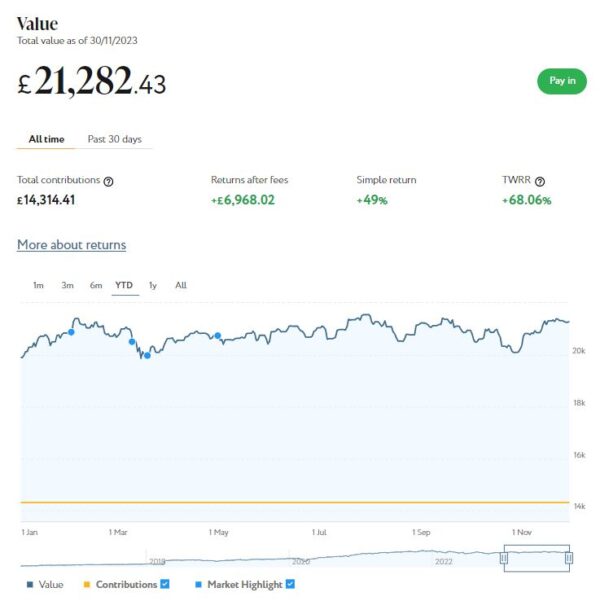

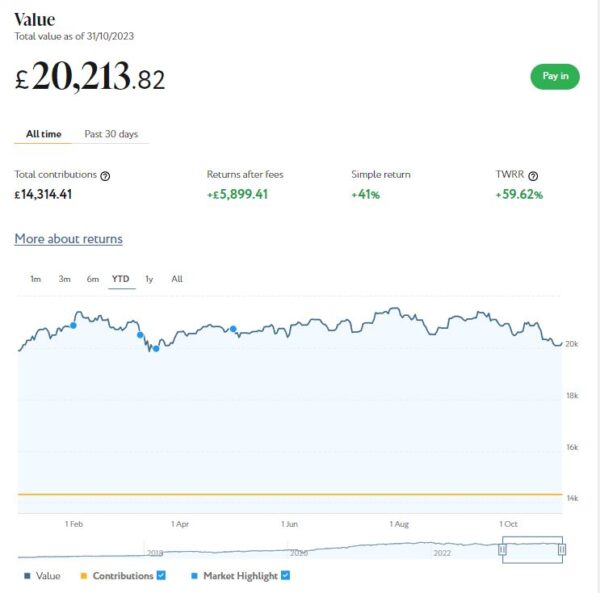

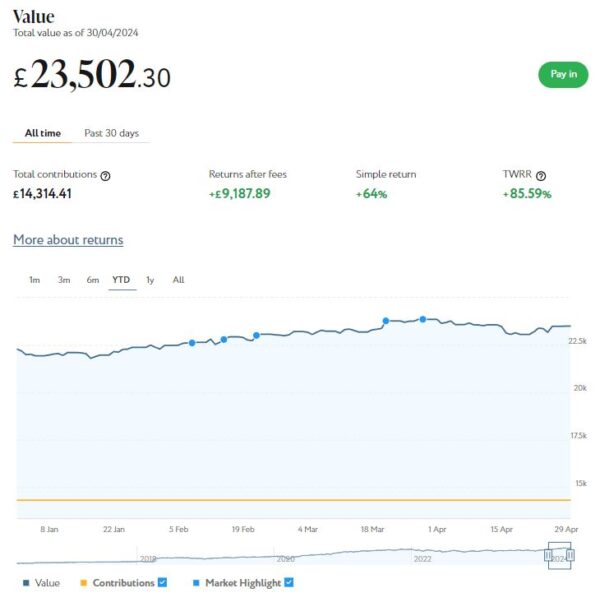

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,502. Last month it stood at £23,859, so that is a fall of £357.

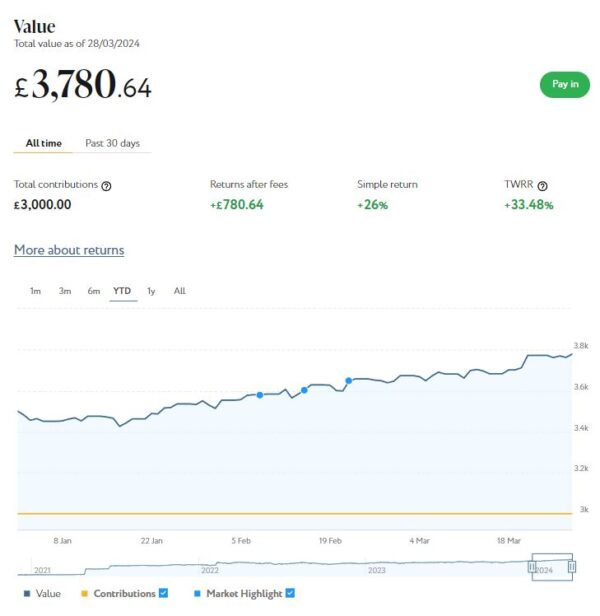

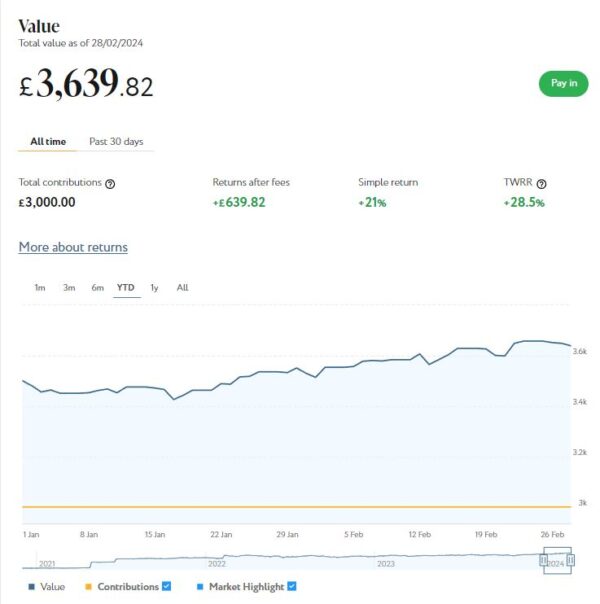

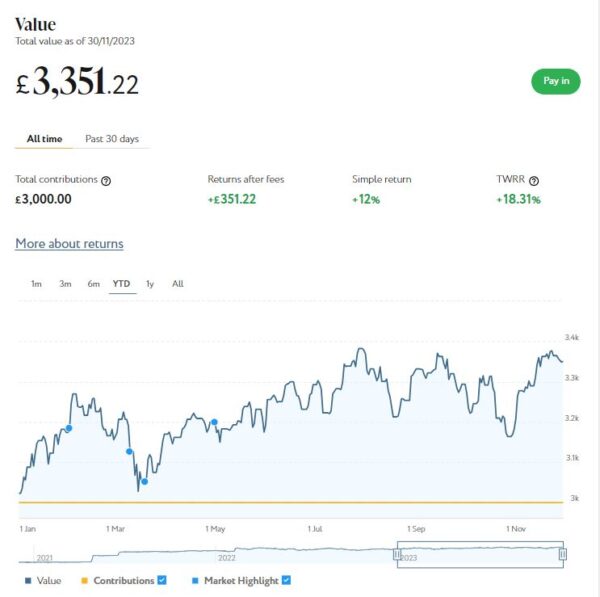

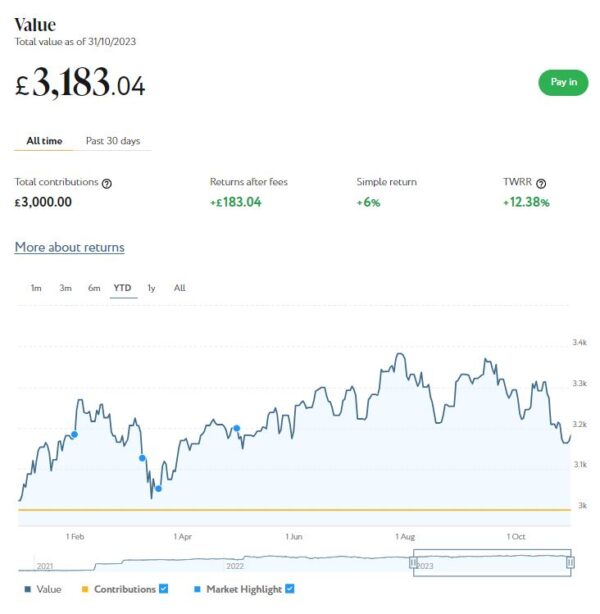

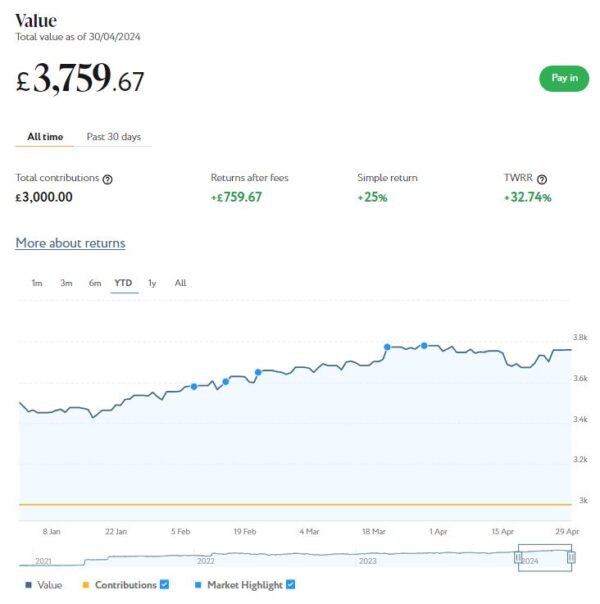

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,760 (rounded up) compared with £3,781 a month ago, a fall of £21. Here is a screen capture showing performance over the year to date.

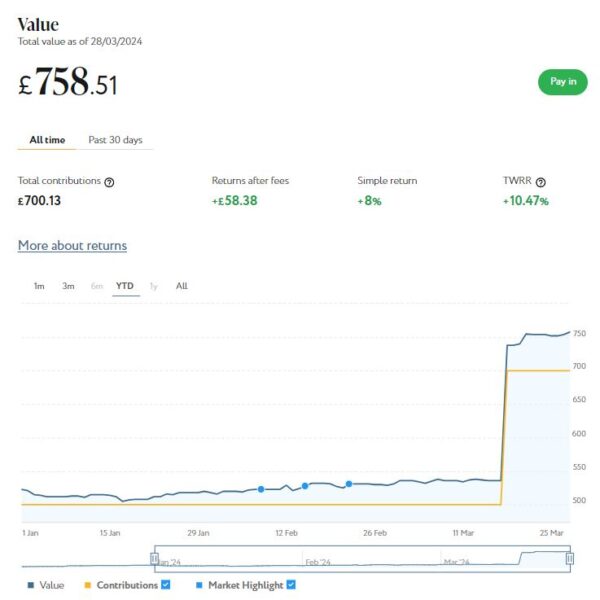

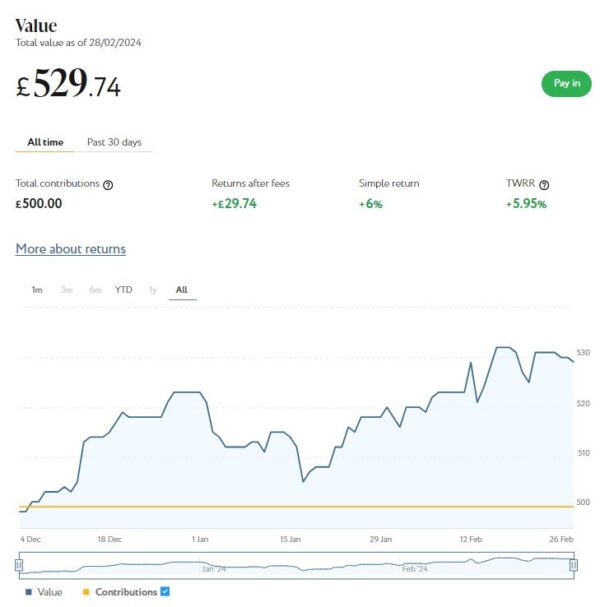

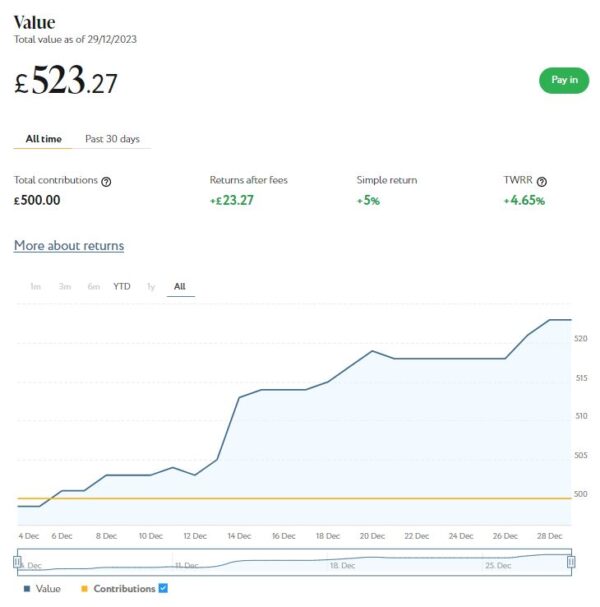

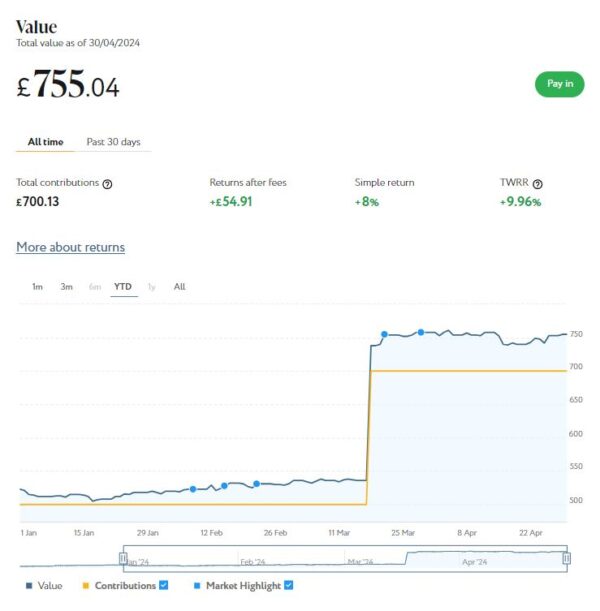

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the screen capture below, this portfolio is now worth £755 compared with £759 last month, a small decrease of £4.

It’s obviously a little disappointing that the value of my Nutmeg investments has fallen a bit this month. This is entirely to be expected with investments, however, where ups and downs are the norm. It’s also worth observing that their overall value has risen by £1,392 or 5.29% since the start of the year (not counting the £200 bonus I invested in my thematic portfolio in March).

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

- Don’t forget, the new tax year began on 6 April 2024 and and you now have a whole new £20,000 tax-free ISA allowance for 2024/25!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £179.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £38.96, meaning that overall (rental income minus capital value decrease) I am up by £140.57. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

- As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

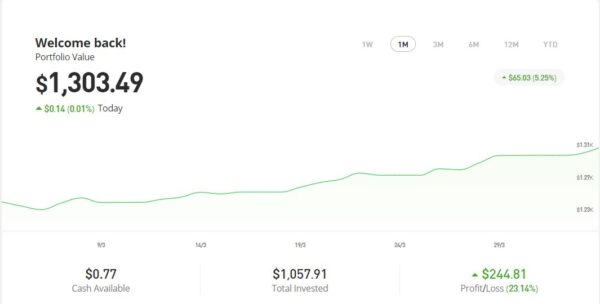

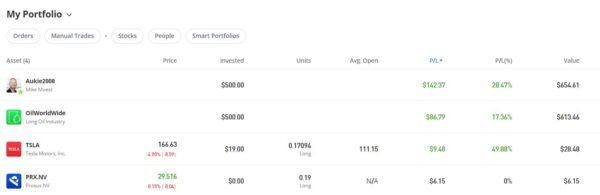

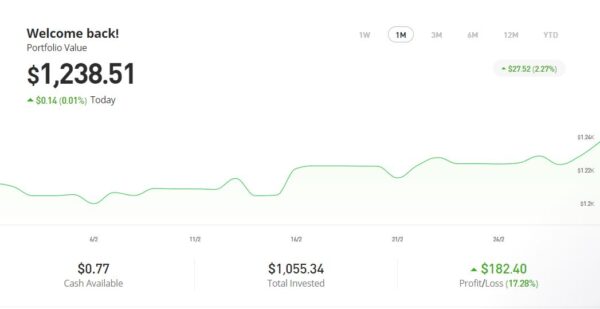

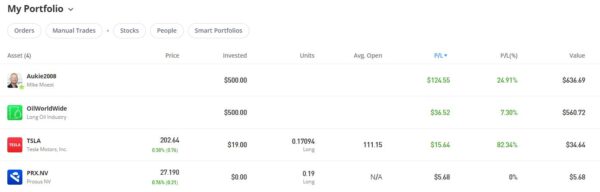

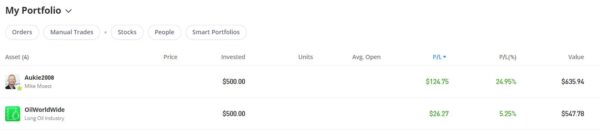

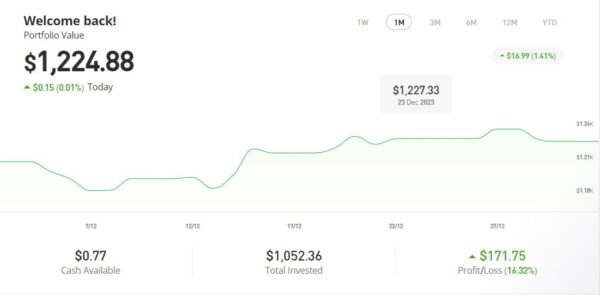

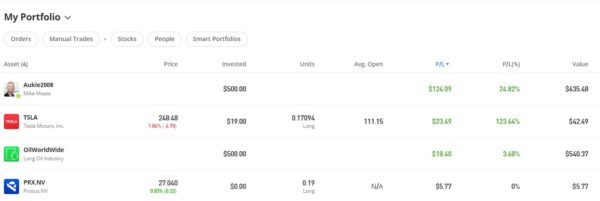

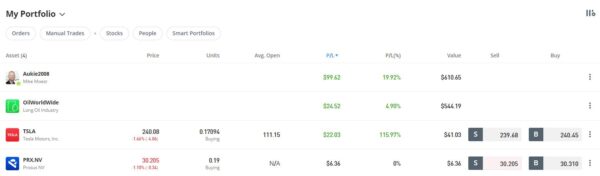

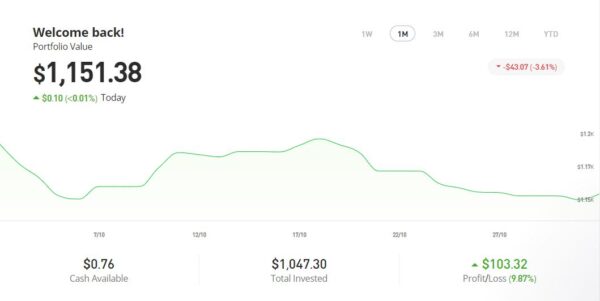

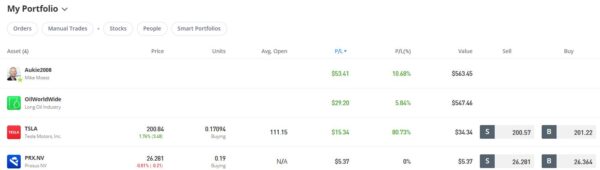

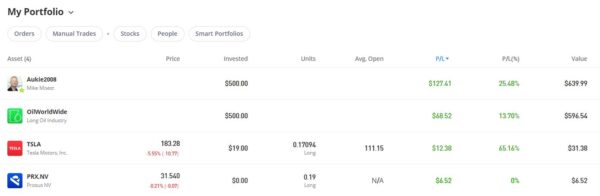

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

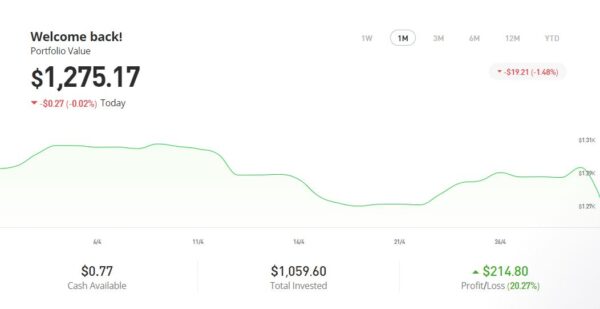

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,275.17, an overall increase of $252.91 or 24.74%.

You can read my full review of eToro here. You may also like to check out my more in-depth look at eToro copy trading. I also discussed thematic investing with eToro using Smart Portfolios in this recent post. The latter also reveals why I took the somewhat contrarian step of choosing the oil industry for my first thematic investment with them.

- eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in April on the excellent Mouthy Money website. The first is What Is Thematic Investing and Is It For You? In this article I looked at the pros and cons of thematic investing. My editor at Mouthy Money edited the article to remove the specific examples I gave, in case this was construed as personal financial advice. As a consequence the published article is a bit shorter and vaguer than I intended! However, readers of PAS will know that I have thematic investments with Nutmeg and eToro. So far – as mentioned earlier – both have been doing well, but of course there are no guarantees this will continue in future. Thematic investing isn’t for everyone, so take a look at this article, read about the pros and cons, and see if you think it might have a place in your portfolio.

Also in April Mouthy Money published How to Avoid Becoming a Telephone Scam Victim. In this article I set out some tips and advice to avoid falling victim to phone scams. As with online scams, which I discussed in another recent article on Mouthy Money, telephone scams have become an unfortunate reality of daily life in the UK. It’s important to be aware of the risk, and to ensure that any elderly friends and relatives who might be particularly vulnerable don’t fall for them.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Eight Ways to be More Mindful With Your Money sets out various ways you may be able to save money relatively painlessly by adopting a more frugal mindset. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in April. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Why Now Could Be the Ideal Time to Take Advantage of Your New Tax-Free ISA Allowance I pointed out that (other things being equal) the start of a new tax year is the perfect time to invest in a new ISA. The main reason for this is that the sooner you invest, the more time there is for the power of compounding to start working. There are other good reasons as well for investing now – read the article for more details 🙂

I also published two sponsored guest posts in April. Sponsored posts help pay my bills, but I only accept those that I feel offer genuine value and interest to PAS readers.

Six Tips for Getting Free Stuff Without Dealing With Scams has some good tips for getting valuable freebies online without opening yourself up to a torrent of spam. And Seven Top Money-Saving Websites for Freebies sets out seven websites where you can apply for (genuine) freebies. Understandably my sponsors didn’t want me to link to all the sites as well as the one they were actually promoting, but you should find them easily enough with a little help from Google.

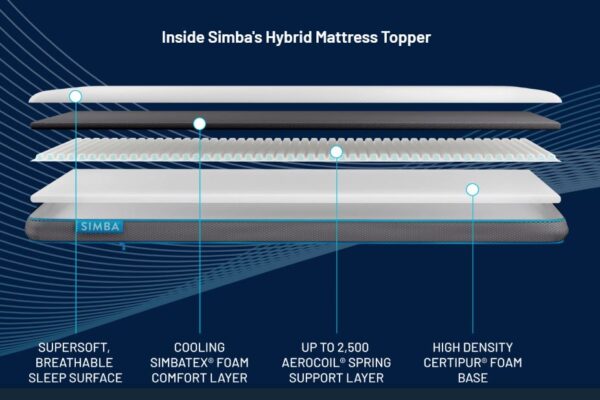

Finally, I posted My Review of the Simba Hybrid Mattress Topper. This is obviously another sponsored post, although in this case I received a free item to review rather than being paid for it. As you will see, this offer came at an opportune time for me. I was genuinely impressed with the Simba Hybrid Mattress Topper, even though it took a bit of effort to get it up the stairs and onto my bed!

Also this year I became a regular contributor to the Over 60s Discounts website. You can read my latest article here: Could You Claim Attendance Allowance? As you will gather, this is all about this invaluable benefit for older people with care needs. It’s estimated that over three million people are eligible for this benefit but not claiming it. Read this article to discover if it’s something you – or an elderly friend/relative – would be qualified to apply for.

I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

Also in April I enjoyed a short break on the beautiful Isle of Man (see cover image). It was the first time I had visited the island, and in fact the first time I had been anywhere by plane since Covid.

I had a great time, with wall-to-wall sunshine until my last day when I was going home anyway. It was a heritage-railway-themed holiday, so I got to ride on the island’s steam and electric trains, and also travelled on buses between towns not served by the railways. The trip was arranged by Newmarket Holidays, and I do recommend this if you are new to the IOM and want a well-organised introductory tour covering all the main places of interest (with a heritage-railway bias, obviously). I will aim to post a fuller review of my Isle of Man holiday on PAS soon.

- The one downside to the trip was the chaos on my outward journey from Birmingham Airport. There is loads of building work going on there and, coupled with an apparent shortage of staff, this caused massive queues and delays. Although I arrived before the check-in opened, it took me almost two hours to get through security. By then it was the final call for boarding, so I had to do a mad dash to the gate to avoid missing my flight. There are posters up at the airport saying that all this work will result in a better experience for passengers, but I’ll believe that when I see it. Currently I don’t recommend flying from Birmingham if you can possibly avoid it.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

The cover photo, taken by me, shows an Isle of Man Steam Railway train arriving at Port Erin station.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!