Today I have another guest post for you on the subject of saving money and getting freebies 🙂

My friends at Hot Free Stuff have put together this list of seven top money-saving websites where you can get freebies, discount codes, downloadable coupons, and more. Check them out, and don’t forget to sign up for free emails from Hot Free Stuff to get all the latest free offers daily!

Are you a stressed-out mum (or dad) trying to make the family budget work?

It takes juggling to make the household budget balance without the need for taking a calculator on every shopping trip. That is because just a click of your mouse or a swipe of your tablet can reel in huge savings on credit card bills, home goods, fashion, electricity, and fun-filled family activities!

We have done the work of trawling the Internet to find you seven of the best money-saving websites around. We’ll help you get freebies, codes, downloadable coupons and more, so that you can do more with your budget every week. Here is our point-and-click guide to savings…

HotFreeStuff.co.uk

This site gets you access to lots of free samples you can really use, from lotions to perfumes. Save money using this site on lots of household goods and get a chance to try new products for free as soon as they are available.

Gumtree

At this so-called ‘classified community’ you can snap up lots of great deals on pets to property. There are many listings for rentals and jobs throughout the UK and Ireland. You will enjoy the deals, but you can also get free items via the freebies section. Just scroll beyond the ads and sponsor links to find many free listings for household items and furniture. At the time of writing there were listings on the London site for free sofas and mattresses, a working Hotpoint fridge-freezer, and free haircuts. Just a word of caution – we suggest for any classified site that you take someone along with you to collect any items, and be careful about giving away too much personal info when responding to ads.

HotUKDeals

This site has been around for well over a decade and is the most reputable place for people to share information on the freebies and discounts they have picked up on their website travels. It is free to register and features include ‘Top 10 Hottest Offers’, requests for offers, and fun, free competitions to enter.

My Voucher Codes

Get over 2000 discount codes at Britain’s biggest voucher website. Tabs include top listings as well as categories, together with the ability to print out vouchers.

Groupon

Never underestimate the power of Groupon! Many times it can seem like a venue for free or cut-price beauty treatments. There are, however, great deals on family attractions, meals and holiday getaways as well.

Moneysaving Expert (MSE)

This massive site set up by financial journalist Martin Lewis has saved the UK millions. It is clearly written, easy to understand, and has lots of information on getting deals on everything from home and car insurance to broadband and mortgages.

Travel Supermarket

This is the best site to find travel deals and compare flights and hotel offers in one easy-to-navigate resource.

Many thanks to Hot Free Stuff for sharing their advice and information. If you have any comments or questions – or other tips and resources for saving money – please do share them below as usual.

Disclosure: this is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you on a subject I’m sure will resonate with many Pounds and Sense readers.

We all love a freebie, but how do you ensure that by providing your details you aren’t opening the floodgates to a torrent of spam? Read and follow the tips below from my friends at All Free Stuff. And don’t forget to sign up for their free email newsletter to get details of all the latest free offers daily!

It’s completely possible for you to get free stuff. There are plenty of opportunities out there.

That said, for every legitimately free thing you can get, there are two complete scams set up to get your personal information at the cost of a few free samples. If you want to get free stuff without dealing with scams, try the following steps.

1. Set up a ‘spam catcher’ e-mail. This e-mail account is one you have no plans on using for normal correspondence, but rather the address you give out for giveaways and promotions. You can also use it when you register with a company that wants your e-mail address in exchange for free gifts. If you give the company your primary e-mail address, you’ll be swamped with a mass of promotional e-mails. It won’t take long for you to abandon your e-mail account in despair if this starts to happen.

2. Avoid giving personal information. You should never give out more than your name, e-mail address, physical address, and birthday. And you should be careful about giving away all of those, as well. If you can, try using a fake name or a PO Box. The more personal information you give out, the easier it will be for other companies to get that information. In addition, some websites ask for your credit card number ‘just to ensure you’re a real person’. Once they have your credit card information, you can’t make them forget it.

3. Be realistic about what you expect. If the deal seems too good to be true, it almost certainly is. It’s certainly possible the giveaway is legitimate, and if that’s the case then they should have company contact information readily available. You should also check the internet to see if you can find information. If the offer is that great, then plenty of people will be talking about it. Of course, if it’s a scam you’re liable to find discussion about that, too.

4. Visit only legitimate websites for samples. Manufacturers’ sites are generally trustworthy, whereas some retail-specific sites are not.

5. Write to the manufacturers of products you enjoy using. Companies are always happy to give a few freebies to customers willing to go out of their way to make their voice heard. It builds goodwill and often garners more customers. And all for the cost of a few free samples.

6. Learn to use coupons properly. It can take a huge amount of patience to learn to coupon well. That said, good couponing can save you so much you may even get free groceries. Couponing is a fairly big deal, so you can find plenty of websites that can help you learn. There are also many grocery stores or manufacturer sites that will keep you informed of what great deals and amazing coupons are available.

These are some of the best ways to get free stuff without dealing with scams. Do you have any other tips yourself? Please do leave them below!

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I wanted to share with you a clever money-saving idea I came across on the excellent Wow Free Stuff website.

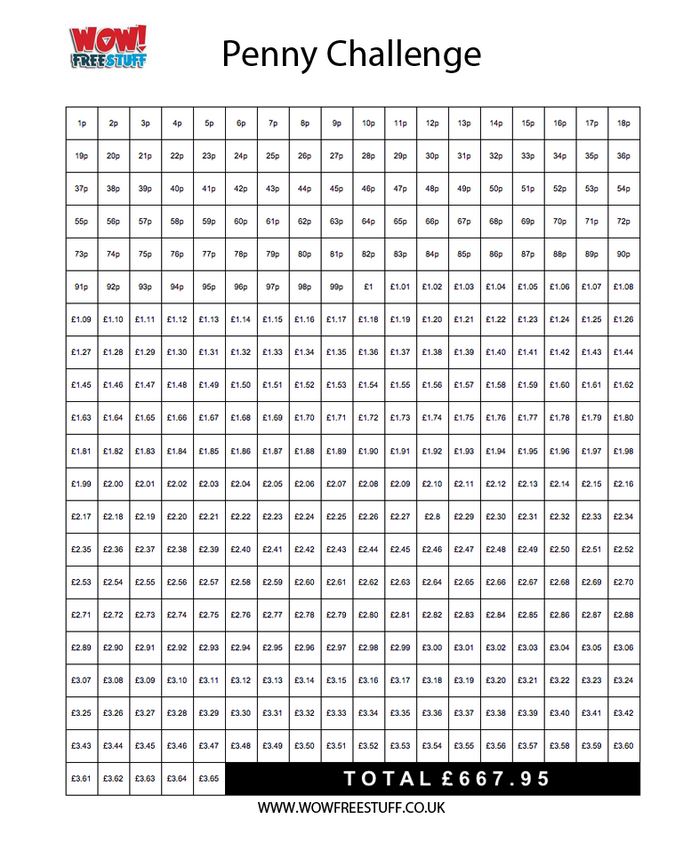

The Penny Challenge offers a painless way to save money every day – so in a year’s time you will have the substantial sum of £667.95 stashed away. That’s money you could spend on anything you like.

How It Works

The challenge itself is very simple.

On the first day you put aside one penny. Each day after that you add another penny to the amount you save. So on the second day you save 2p, on the third day 3p, and so on.

Over the course of a year (365 days) the amount you have to save each day is shown in the grid below.

As you will see, by the last day of the challenge you will have to find £3.65 – still an easily affordable sum. And once you have done that, you will have a total savings pot of £667.95.

This would be a great way to get your money-saving started painlessly in 2024. It will ensure that by January 2025 you have a handy sum set aside to pay for any large purchase you have set your heart on, and maybe treat yourself to a post-Christmas holiday as well!

Please let me know if you decide to take the Penny Challenge by posting a comment below. And, of course, if you have any other comments or queries about it, feel free to post them also.

Note: This is an updated version of a sponsored post for which I received a fee.

If you enjoyed this post, please link to it on your own blog or social media:

I’ve mentioned several times on PAS why I believe having an independent financial adviser makes sense, even if – like me – you consider yourself reasonably money-savvy.

So today I thought I would set out some reasons over-50s (in particular) may benefit from having an independent financial adviser (IFA) or at least speaking to one.

This post has been created in association with my colleagues at Unbiased.co.uk, a well-established financial services website that can put you in touch with suitable IFAs in your area.

Reasons for Having an IFA

1. Helping Your Children Through College or University

If you have children, you will naturally want to help them complete their education safely and with a reasonable degree of comfort. Sadly the days of student grants (which I was lucky enough to benefit from in the 1970s) are well behind us now. There are various options for helping finance your children’s college or university education and a financial adviser will be able to explore these with you. They will also explain the pros and cons of the student loans system.

2 – Pension Planning

If you are over 50 you will inevitably be thinking about pension options, including when you can retire and how much income you can expect. An IFA will go through your finances with you and look at ways you may be able to boost your pension pot. From 55 onwards you can normally start to draw your pension, but you shouldn’t do this unless a financial adviser has assured you it will last you through retirement.

3. Investing

Hopefully by your fifties you will be earning a decent salary and may also have paid off your mortgage. You may also receive an inheritance or other windfall. Either way, if you find yourself with some spare cash you will want to invest it to get the best possible returns from it. An IFA will have access to all the latest information about a vast range of investment opportunities. They will guide you towards investments that are suitable for you based on your financial goals, your investment timeframe and your appetite for risk.

4. Starting Your Own Business

Especially at this time of upheaval due to Covid, many people are looking to start their own businesses in mid-life. That may be in response to redundancy or unemployment, or simply in search of a better work/life balance. An IFA can help you with the financial aspects of doing this, including raising money for tools, premises, transport and so on, or perhaps buying a franchise.

5. Emigrating or Retiring Abroad

Another way to revitalize your life may be to start afresh somewhere else, with new challenges and opportunities (and perhaps a better climate as well!). Or you may be looking to move to a favourite vacation destination to enjoy your retirement. Either way, an IFA will be happy to discuss the pros and cons with you, point out all the things you will need to take into account, and assist you with the financial arrangements.

6. Divorce

Sadly middle age sees the largest number of divorces. Your first priority here will be appointing a good solicitor to act on your behalf and protect your interests. Beyond that, though, divorce can have major ramifications for your finances. An IFA can help you assess your situation objectively and plan for a financially secure and stable future.

7. Downsizing

As the children grow up and leave home you may want to move to a smaller property – to make life simpler, save time on housework and free up money for more exciting things. An IFA can help you explore the implications of doing this and make the necessary financial arrangements.

8. Equity Release

If you don’t want to move – and are over 55 – equity release is another option for releasing funds. In recent years it has grown a lot in popularity. There are various possibilities, including home reversion plans and flexible lifetime mortgages. Most now come with a no-negative-equity guarantee, ensuring you won’t end up passing on debts to your next of kin. An IFA can go over the options with you and point out the pros and cons before you contact any providers.

9. Estate Planning

This obviously includes writing your will, but depending on your circumstances it can cover a lot of other things as well. Nobody wants to see all their money and assets falling into the hands of the taxman rather than going to their nearest and dearest. Speaking to an IFA who specializes in estate planning can give peace of mind and ensure that your loved ones are well provided for when you are no longer here yourself.

10. Helping Elderly Relatives

If you have elderly parents (or other relatives) you may find they are increasingly reliant on you for help and support. It may be up to you to arrange care for them and/or set up power of attorney so you can manage their affairs if this becomes necessary. They may also need help with estate planning (see above). An IFA can assist with all these things as well.

Getting a Free Financial Check-Up

Independent financial advisers do of course charge for their services. They are by definition unaffiliated and do not receive commission, so any recommendations they make are based solely on their client’s best interests. As I have said before on PAS, I certainly don’t begrudge paying my own financial adviser, Mike, as he has undoubtedly saved (and made) me a lot more money than he has cost me over the years.

Nonetheless, most IFAs will be happy to see you for an initial financial healthcheck free of charge. This can focus on a particular area of concern, so you could request an investments review, a pension review or a mortgage review. Alternatively, if you’re not sure which aspect of your finances needs more attention – or indeed whether you need advice at all – you could simply request a broad financial healthcheck.

Here’s what. Adrian Kidd, a financial planner at Radcliffe & Newlands, says about his approach on the Unbiased website:

‘I’d generally offer one or possibly two free consultations, taking about an hour, and these can be as specific or as broad as required. When someone books a financial healthcheck with me, I ask them to bring along all their documents relating to their finances – savings, investments, mortgages, loans, insurance, pensions, the works – so I can build up a complete picture of their affairs. I then go through these in more detail after the consultation, and follow up with an email that gives a summary of their overall financial situation.’

In these free check-ups: advisers won’t generally talk to you about products at all. The process of choosing the right products comes later, after the adviser has built up an understanding of you as a person and your financial planning needs. Only then will they recommend products, if asked to do so.

If you follow my link to the Unbiased website, you can complete a short, step-by-step questionnaire designed to identify the best type of financial adviser for your needs. You will then be shown a selection of suitable advisers in your area with contact information. They will be happy to answer any queries you may have and arrange an initial meeting without obligation.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Unbiased.co.uk. If you click through my link and end up becoming a client of a financial adviser listed on the Unbiased site, I may receive a commission for introducing you. This will not affect the service you receive or any fees you are charged if you decide to proceed further.

This is a fully updated version of a post originally published in 2020.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a sponsored guest post for you from my friends at Best Free Stuff. There are some great tips and ideas for getting things free, plus at the end is a link to a free competition where you can win a Lindt Chocolate Bunny just in time for Easter!

There are lots of great ways to get free stuff. For many, this is like a treasure hunt. Once people get their deal, they tend to share the good news with others. So a free deal can go viral quickly. Here are some suggestions for how you can get loads of quality, free products.

Free samples are really popular. Manufacturers like to give them out because it is a very effective way to promote a product. When a product is launched, people may not buy it right away because they don’t know if they will like it. However, if they have a chance to try it for free, then they can buy it if they like it. You may have seen vendors giving out samples at a carnival or community festival. Companies know that no-one can resist a free product. So it’s a win-win for both companies and consumers with free samples.

You can also get freestuff when you search online. There are many websites that have a special focus on gathering information on all kinds of free offers. You can get skincare samples, snacks, cleaning products, movie rentals, and just about anything consumers would want. You just have to click on a link that is connected with the product and fill out some information. Do realize that the provider of the free item will probably add your contact information to their mailing list. So, if you request a lot of free things, you should get ready to receive a lot of email advertisements. You will get the option to unsubscribe, however. So there is little risk in signing up.

Sometimes you can get free trials on full-sized products, such as a software download or a subscription. Do beware of any free trials that require you to enter your credit card information, though. Sometimes it may not be that easy to cancel after the trial.

Don’t forget about classified ads too. Ordinary people are giving away good-quality things every day for various reasons. Perhaps their children have outgrown their toys. Maybe they are moving to a new home and don’t want to take their old furniture with them. A business that is closing offices may be liquidating office furniture and equipment. Craigslist is a popular online classified platform that lists thousands of free items every day, in all major cities around the world. You never know what will be listed each day. If you are looking for something in particular, just type in a search term under the ‘free’ category and see what comes up.

These are just some common ways you can get great free stuff. Free things get snapped up quickly, so if you want the best stuff, you need to be diligent and monitor places that list these giveaways. Sign up for email alerts and keep checking back. If you are in the right place at the right time, you can score a great deal.

If you like to enter competitions, then we found this great competition where you can win 1 of 300 Lindt Bunnies (see cover picture). Click this link to enter today!

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my friends at Broadway Autocentres. As specialists in this field, they know exactly what it takes to get the most out of your car tyres.

Over to the experts, then…

When it comes to driving your own car, all the costs seem to mount up. If you’re not saving for the next service, you’re putting money aside for the MOT. And just when that is out of the way, you realise that you don’t know how old your tyres are or when they will need to be replaced.

There is no way to have your car use less fuel or oil, and skipping services is a bad idea – but if you can reduce the wear and tear on the vehicle whenever possible, so much the better for your purse or wallet.

Tyres are one of the biggest expenses you will face, so let us look at five ways to get the most out of your tyres before you bow to fate and replace them!

Buy Them in Twos

Buying a set of four tyres can seem impossible with a tight budget, so why not replace your tyres in twos instead? Depending on whether your car is front or back wheel drive, either the front set or back set will take the most punishment. It is the most worn tyres that should be replaced, with the more lightly worn set moving to take their place and the new tyres going where they will receive less wear. This system may seem inconsistent, but it will ensure that you stay safe while on the road without needing to spend a lot of money all at once.

Drive Sensibly

Drive according to the Highway Code at all times and resist the temptation to put your car through its paces. Maintain a safe speed, avoid rough or unsurfaced roads, and increase and decrease speed slowly whenever possible. All of these will help to keep your tyres in good condition for longer, so you can keep saving for their eventual replacements.

Buy the Best

While it may seem counter-intuitive, buying the best quality tyre you can afford is often more economical when taken over time. Budget tyres are sometimes made with flaws that can weaken the tyres more quickly, or with inferior rubber that begins to crumble and break apart. Better quality tyres will last better – sometimes twice as long as budget tyres, thereby comparatively halving their cost to you. You can book your tyres in Buckinghamshire at Broadway Autocentres (01494 680914).

Regular Checks

Get into the habit of checking your tyres often, looking for early signs of damage or weakness. In many cases, prompt corrective action or a swift repair can keep the tyre in place for some time, giving you the chance to continue getting out and about without suddenly needing to spend money on a new set or pair of tyres.

Proper Inflation

Modern tyres – no matter whether budget or premium – are designed to be used within a narrow recommended range of pressure, and will often perform poorly outside of this range. Keep your tyres inflated to within the range recommended by the manufacturer (this can be found online, sometimes on the tyre itself, or inside the car owner’s handbook) to ensure that not only do your tyres last as long as possible, but you are safer on the roads during this time. Correctly inflated tyres also aid fuel economy, saving you money that way as well.

Thanks again to my friends at Broadway Autocentres for their expert advice. As always, if you have any comments of questions about this post, please do leave them below.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a new UK high-speed broadband service called Cuckoo.

They are aiming to shake up the world of broadband internet with great-value prices, first-rate customer service, and a social conscience too 🙂

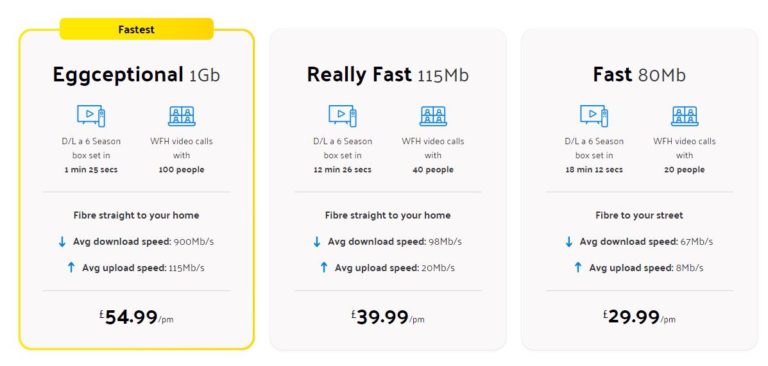

Cuckoo currently have three different customer offers based on speed. Briefly they are as follows:

Eggceptional (1 Gb) – £54.99 a month

Really Fast (115 Mb) – £39.99 a month

Fast (80 Mb) – £29.99 a month

You can see more detailed information from the Cuckoo website in the screen capture below.

Signing up is straightforward via the website and takes just a couple of minutes. Your router will then arrive in the post with full instructions for setting it up. If an engineer is needed (usually it isn’t) Cuckoo will arrange a convenient time for them to come. This is summed up in the graphic from the company website below.

As mentioned, Cuckoo is also a company with a social conscience. They take 1% of each bill and use it to help bring the Internet to places where it’s needed most. That includes conflict zones, natural disaster sites and developing communities. Customers get to choose which project they wish to to support under the Cuckoo Compass scheme.

Finally, Cuckoo aims to deliver top-notch customer service from their team of UK-based customer-support ‘Eggsperts’. Cuckoo have an impressive Trustpilot average rating of 4.6 (‘Excellent’), with 76% of people at the time of writing giving them a full five stars.

For much more information, please check out the Cuckoo website. And of course, if you have any comments or questions about this post, please feel free to leave them below as usual.

Disclosure: This sponsored post includes affiliate links. If you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a sponsored guest post for you on behalf of Top Subscription Boxes. On their website they advertise a huge range of subscription box services.

With these services, you receive a new and exciting product (or selection of products) every month. You can subscribe for as long or as short as you want (subject to minimum subscriptions). And as you will see, there is something to suit every taste and budget!

Whether you want to send someone special a gift they will really enjoy or just treat yourself (you deserve it!), the subscription box services listed below could provide the perfect solution. We tried all of these ourselves before bringing the very best together in one place.

So without further ado, let’s get started!

Glossybox

Whenever it comes to beauty and make-up subscription boxes. Glossybox always takes the top spot. Glossybox allows you to treat yourself with a perfect combination of deluxe and full-sized beauty product samples from top brands.

Each month they send you a great-value box loaded with the latest make-up products, tools and beauty creams – and it will only cost you £13.25 per month.

In their previous boxes they have featured well-known brands like La Mer, Nars, pedigree French brands such as La Roche Posay, and impressive budget make-up from the likes of Rimmel.

Beer Bods

Beer Bods is known as the UK’s #1 craft beer subscription service. They send you a box of 8 beers every two months. So basically you receive one beer a week, along with the story behind that beer. All subscribers receive the same beer at one time, and you can join in a live online tasting every Thursday at 9 pm. So you can enjoy a new beer with new friends every week and compare notes with them. The bi-monthly subscription will cost you £24.

Arena Flowers

Nothing can be better than seeing fresh flowers in the morning. They make you feel calm and give your day the perfect start.

Arena Flowers is a leading ethical floristry service. They deliver exciting bouquets through their monthly subscription service.

They’ve been sending out their beautiful bouquets for the last 14 years and have achieved the milestone of 10 million deliveries. Every bouquet you receive is hand-tied and arranged by one of their expert florists to create a unique bouquet just for you. You can subscribe by paying just £17 a week.

Gadget Discovery Club

The Gadget Discovery Club allows you to treat yourself or your loved ones by sending them subscription boxes containing 4 innovative gadgets they didn’t know they needed!

They say that every gadget they’ll deliver to your doorstep will help you to upgrade your home, entertainment or lifestyle. The subscription box contains everything from tech wearables to smart home devices, including Samsung/Philips kits and Google home speakers.

You just need to sign up and select your preferences so they can send you the latest exciting gadgets based on your profile. They offer a monthly subscription or you can also choose a yearly plan. The monthly option will cost you £33 per month.

BakedIn Baking Club

The BakedIn Baking Club is a baking subscription service that delivers a different recipe each month straight to your door. Once you’ve subscribed to this service, you will receive a beautiful baking box with a step-by-step recipe guide, along with all the dry ingredients you need and some extras too.

BakedIn allows you to make your favourite muffins, biscuits, cakes and cookies, to share with your family and friends. If you are one of those people who loves baking, then this is the subscription box service for you. The price is £7.50 a month.

Good luck, and we hope you find the perfect subscription box service for you or your loved ones!

Thank you to my friends at Top Subscription Boxes for some eye-opening suggestions. I would definitely like to try some of these services myself! They would also, of course, make excellent Christmas or birthday presents. Please do click through to their website and check out the other subscription box services as well!

As always, if you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a savings product that will be relevant mainly to the parents among you

A Junior ISA (sometimes abbreviated to JISA) is a savings product aimed at under-18s (and more specifically at their parents/guardians). These accounts allow money to be stashed away tax-free for a child until their 18th birthday. After this the money becomes the child’s to do with as they wish. The JISA account turns into an ordinary ISA at this time, thus retaining its tax-free status.

What Types of JISA are There?

There are two types of JISA: the Cash JISA and the Stocks and Shares JISA.

A Cash JISA is basically just a tax-free savings account. Interest is normally paid annually. According to the MoneySavingExpert website, the best-paying Cash JISA provider at the time of writing is Coventry Building Society, who are paying 4.95%. However, this is only available if you open an account in a branch or by post. If you want to open an account online, the best paying Cash JISA currently comes from Tesco Bank or NS&I, both paying 4%.

With a Stocks and Shares JISA, as the name indicates, the money is invested in the stock market. This offers the potential for greater returns, but with a higher degree of risk in the short term especially. I will say more about Stocks and Shares JISAs below.

As with adult ISAs, there is an annual limit to how much you can put into a Junior ISA. In the current (2024/25) tax year this is £9,000. You can put all of this into a Cash JISA or a Stocks and Shares JISA, or divide it between the two. You can switch providers as often as you like, but can only hold one of each type of JISA at any time.

Only a child’s parent or guardian can open a Junior ISA for them, but others including grandparents, friends, other relatives and the child him/herself can contribute. But it is important to be aware that (barring exceptional circumstances) all the money and interest in the account will be locked away until the child’s 18th birthday.

Which JISA is Best?

You won’t be surprised to hear that there is no simple answer to this.

If you want to avoid any risk of losing money, a Cash JISA is the way to go. Under the Financial Services Compensation Scheme (FSCS) the money will be completely safe so long as it’s invested with a UK-regulated provider and you have no more than £85,000 with that institution. Every year a known amount of interest will be added. The only risk you are taking is that the money won’t grow at the same rate as inflation.

On the other hand, if you are investing for at least a five-year period, there is certainly a case for putting at least some money into a Stocks and Shares JISA – and if it will be for ten years or more, the case becomes even more compelling. Over a five-year period stocks have outperformed cash in the great majority of such periods, and in almost all periods of ten years and over.

So if you are opening a JISA for a young child or infant, where the money may be invested for up to 18 years before it can be accessed, a Stocks and Shares ISA is very likely (though not guaranteed) to produce better returns than a Cash JISA. Of course, there is nothing to stop you hedging your bets and putting some money into one of each type.

What About Child Trust Funds?

Any child under the age of 18 born before January 2011 would have had a Child Trust Fund (CTF) opened for them by the government.

The government gave every child born between 1 September 2002 and 2 January 2011 a £250 voucher (£500 in the case of some low-income households). Parents could top up their child’s CTF themselves if they wished. The scheme ended in 2011 when CTFs were replaced by Junior ISAs. Unfortunately the government does not make a contribution towards these!

As with Junior ISAs, the money in a CTF could be placed in a Cash CTF or one where the money was invested in stocks and shares. Although new CTFs are no longer issued, there are many young people who still have one and will be able to access it on their 18th birthday. The first CTFs matured in September 2020, when the oldest account-holders turned 18. The last will mature in 2029. On maturity, a CTF can either be cashed in or transferred into an adult ISA.

Unfortunately the interest rates currently paid on Cash CTFs are generally very low indeed. So if your child has one, there may be a case for transferring it to a better-paying Junior ISA. Most JISA providers allow transfers from CTFs (or other JISAs), and it is certainly worth looking into this if your child has a low-interest-paying Cash CTF.

The Nutmeg Junior ISA

Regular readers of Pounds and Sense will know that I am a fan of of the Nutmeg investment platform and have a fairly large amount in an account with them. My money is invested in the form of a Stocks and Shares ISA. You can read more about this if you wish in my Nutmeg review or one of my regular investment updates such as this one.

Nutmeg do not offer a Cash JISA but they do offer a Stocks and Shares JISA. So if you are thinking of opening one of these for your child (maybe in addition to a Cash JISA) in my view they are well worth checking out.

With the Nutmeg Stocks and Shares JISA you have the same range of investment options as their adult ISA. These are discussed in detail in my Nutmeg review, but in brief they include Fully Managed, Smart Alpha, Socially Responsible and Fixed Allocation. My own investments are in the Fully Managed and Smart Alpha categories, and I am very happy with how both have been performing. But you should, of course, check the terms and conditions (and charges) carefully when deciding which is right for you.

Note that, unlike an adult ISA, in a Nutmeg JISA you cannot have different ‘pots’ within the same JISA wrapper. So you will need to pick your preferred option from one of the four mentioned, though you can change this any time later if you wish. You can also set a risk level between 1 and 10 and again you can change this at any time. You can read my recent blog post about Nutmeg risk levels here. My general advice, though, is that if you’re investing over a period of at least five years, it may pay not to be too cautious. In addition, if you choose to invest in a Nutmeg Junior ISA via my refer-a-friend link, you can get six months free of any charges.

Of course, Nutmeg are not the only providers of Junior ISAs. Some other possible options include Hargreaves Lansdown and BestInvest.

Closing Thoughts

If you are a parent or guardian, opening a Junior ISA is one of the best gifts you can give your child (or children).

The money will grow tax-free and can’t be touched until they are 18, when they can withdraw it or keep it as an ISA. It may provide a much-needed lump sum at a time when they are setting out in the world and really appreciate a financial leg-up. A JISA will also give them an early introduction to saving and investing, and form a valuable part of their financial education.

The main selling point of JISAs is, of course, their tax-free status. Admittedly this is not as big a deal with Cash JISAs as it used to be, as nowadays almost everyone has a tax-free Personal Savings Allowance of up to £1,000 and other tax-free allowances as well. As a result, interest on savings is usually paid without any deductions. So there may be no immediate tax advantage to investing in a Cash JISA if a non-JISA savings account pays better interest.

In the case of a Stocks and Shares JISA the tax-free status may be more significant, as it also gives exemption from dividend tax and capital gains tax (CGT) both of which have had their tax-free allowances slashed by the government.

Either way, though, money saved in a JISA will carry on growing tax-free forever (until it’s withdrawn) – so even if there is no immediate tax advantage, there may well be in years to come. This applies to an even greater extent if the young person stays invested on reaching maturity rather than immediately withdrawing all their money.

According to the This is Money website more parents open Cash JISAs than Stocks and Shares JISAs. As a money blogger, however, I would definitely think about opening a Stocks and Shares ISA for at least part of your child’s JISA allowance. That applies especially if it is more than ten years till their 18th birthday. As mentioned above, over almost any given ten-year period, stocks and shares have outperformed cash. And the longer timescale allows the inevitable ups and downs in the stock markets to even out. If you put all the money into a Cash JISA, by contrast, it is quite likely that the value of your child’s account will not keep up with inflation.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Everyone’s circumstances are different and what is right for one person may not be appropriate for another. It is essential to do your own ‘due diligence’ before investing and seek help from a qualified financial services professional if in any doubt how best to proceed. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make a purchase (or perform some other defined action) I may receive a fee for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a sponsored guest post for you on behalf of Fife Autocentre. The post sets out four advantages to using a mobile tyre-fitting service for tyre replacements and repairs.

Taking good care of your tyres is crucial to maintaining your car’s longevity and performance while keeping you safe. The best way to do this is to engage mobile tyre-fitters to get your tyres repaired, fixed or fitted.

Cost-effective

Why waste time and money trying to get to a garage for tyre replacements and repairs? Mobile tyre-fitting provides an ideal, cost-effective solution. An expert fitter will attend at your preferred location and provide a professional service when conducting repairs and replacements. You will therefore avoid the expense (and risk) involved if you do the job incorrectly yourself. For mobile tyre-fitting, check with the experts at Fife Autocentre.

Increased safety

Why risk damaging your tyres even more when you can be served by a mobile tyre-fitting service at your home or workplace? Attempting to take your car to a garage on damaged tyres is extremely dangerous, as you may end up broken down in the middle of nowhere or even having an accident. A mobile tyre fitting service will immediately respond and act accordingly.

Supremely convenient

Why stress to get tyre problems fixed if you can be reached and attended to at your convenience? Mobile tyre fitters will serve you without disrupting your day’s activities. Just call for help, then carry on with your day as normal.

Instant emergency service

Getting stranded due to tyre problems is a driver’s worst nightmare. So reaching out to a mobile tyre-fitting service is the best solution. Simply contact them and they’ll send someone directly to your location to offer the most effective solution wherever you may be. By this means you can avoid unnecessary delays and be back on the road again in the least time possible.

Final Thoughts

Mobile tyre fitting is the modern way to approach your tyre problems as it is affordable, swift and effective.

I’d just like to add my own endorsement to the advice above. Early on in the first lockdown my car had a puncture and I made the mistake of driving to a tyre and exhaust fitting centre to have it repaired.

Even though I reinflated the tyre before departing, it quickly went flat again. By the time I got to the centre the tyre was flat as a pancake and the wheel had gone out of shape as a result. Instead of paying a small fee for a puncture repair, I therefore had to shell out for a new tyre. So I am very much on board with the advice to use a mobile tyre-fitting service in this situation!

As always, if you have any comments and/or questions about this post, please do leave them below.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

As mentioned,

As mentioned,